Asia Pacific In-Vitro Diagnostics (IVD) Market Size, Share, Trends & Growth Forecast Report By Test Type (clinical chemistry, molecular diagnostics), Product (Reagents, Instruments, Software & Services), Technology, Application & Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of Asia-Pacific), Industry Analysis From 2026 to 2034

Market Size, 2025

$19.50 BnMarket Estimate, 2026

$20.85 BnMarket Forecast, 2034

$35.56 BnCAGR, 2026–2034

6.9%Asia Pacific In-Vitro Diagnostics (IVD) Market Summary

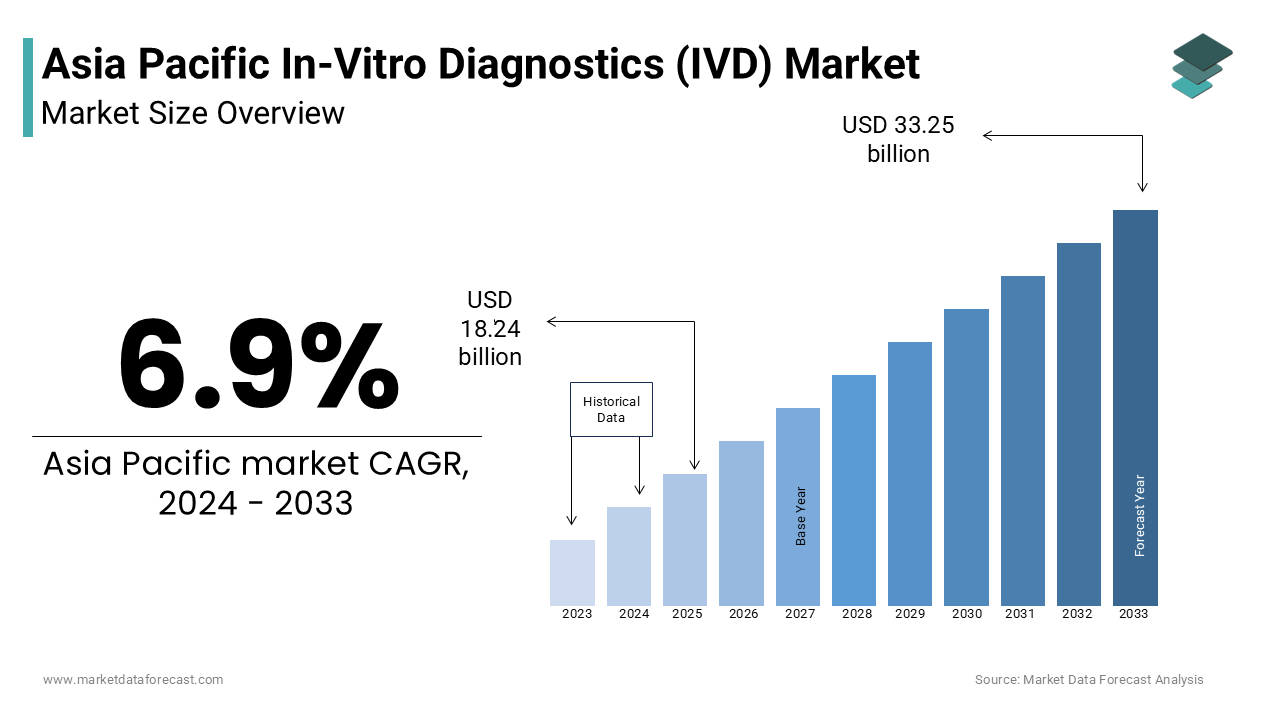

The Asia Pacific in-vitro diagnostics (IVD) market was valued at USD 19.50 billion in 2025 and is projected to reach USD 35.56 billion by 2034, growing at a CAGR of 6.9% from 2026 to 2034. IVD tools are revolutionizing healthcare by enabling early and accurate disease detection through tests on blood, urine, and tissues. Market growth is driven by rising chronic disease burden, government initiatives, healthcare infrastructure expansion, and increasing collaborations between global and local IVD players.

Key Market Trends & Insights

- China dominated the regional market, driven by a growing elderly population and advanced hospital infrastructure.

- Clinical chemistry led the test type segment with 35.4% share in 2024.

- Reagents accounted for 59.3% market share in 2024, supported by high diagnostic test volumes.

- Molecular diagnostics is the fastest-growing segment with a projected CAGR of 13.6%.

Market Size & Forecast

- 2024 Market Size: USD 18.24 Billion

- 2033 Projected Market Size: USD 33.25 Billion

- CAGR (2024–2033): 6.9%

- China: The Largest market in 2024

- India & Southeast Asia: Fast-growing and innovation-driven markets

Asia Pacific In-Vitro Diagnostics (IVD) Market Size

The Asia Pacific in-vitro diagnostics (IVD) market size was valued at USD 19.50 billion in 2025 and is anticipated to reach USD 20.85 billion in 2026 from USD 35.56 billion by 2034, growing at a CAGR of 6.9% during the forecast period from 2026 to 2034.

In vitro diagnostics (IVD) are used to perform tests on samples derived from the human body, such as blood, urine, or tissue, to detect diseases, conditions, or infections. These diagnostic tools play a pivotal role in preventive healthcare, disease management, and therapeutic monitoring by enabling early and accurate detection. For instance, countries like China, India, Japan, and South Korea are witnessing robust investments in healthcare infrastructure and biotechnology research, which directly influence the adoption of advanced diagnostic technologies. Additionally, rising prevalence of chronic diseases such as diabetes, cardiovascular disorders, and infectious diseases is fueling demand for efficient diagnostic solutions across both public and private healthcare sectors.

Government initiatives aimed at strengthening healthcare systems, coupled with increasing collaborations between global IVD manufacturers and local players, have further catalyzed market growth.

MARKET DRIVERS

Rising Incidence of Chronic and Infectious Diseases

One of the primary drivers propelling the Asia Pacific in vitro diagnostics (IVD) market is the escalating burden of chronic and infectious diseases across the region. Countries such as India, China, and Indonesia are witnessing a surge in lifestyle-related ailments like diabetes, hypertension, and cardiovascular diseases, alongside persistent challenges posed by infectious diseases such as tuberculosis, hepatitis, and dengue. According to the World Health Organization (WHO), non-communicable diseases account for over 60% of total deaths in the Western Pacific Region alone. In India, the International Diabetes Federation estimates that approximately 77 million adults were living with diabetes in 2021, a figure expected to reach nearly 134 million by 2045.

This growing disease burden necessitates extensive diagnostic testing for early detection, treatment monitoring, and disease prevention. Consequently, there has been a significant increase in laboratory testing volumes across hospitals, diagnostic centers, and point-of-care settings. Additionally, expanding health insurance coverage and government-funded screening programs in several Asia Pacific countries are enhancing access to diagnostic services among underserved populations.

Expansion of Healthcare Infrastructure and Diagnostic Facilities

Another significant driver of the Asia Pacific in vitro diagnostics (IVD) market is the rapid expansion of healthcare infrastructure and diagnostic facilities in emerging economies. Governments across the region are investing heavily in modernizing healthcare systems to meet the needs of growing and aging populations. China, too, has made substantial progress in expanding its hospital network and diagnostic laboratories. As per the National Health Commission of China, the number of healthcare institutions in the country surpassed 1.04 million in 2022, representing a compound annual growth rate of more than 4% since 2015. Moreover, the rise of private diagnostic chains and standalone labs has created a competitive environment conducive to innovation and efficiency. Companies like Metropolis Healthcare and Dr. Lal PathLabs in India have expanded their footprints significantly, offering a wide array of diagnostic tests using advanced IVD platforms. Similarly, in Southeast Asia, countries such as Thailand and Malaysia have developed robust medical tourism sectors, further driving demand for high-quality diagnostic services.

MARKET RESTRAINTS

Regulatory Complexity and Fragmentation Across the Region

A major restraint impeding the growth of the Asia Pacific in vitro diagnostics (IVD) market is the complex and fragmented regulatory landscape across different countries. Unlike the harmonized regulatory framework seen in the European Union or the United States, the Asia Pacific region consists of diverse regulatory regimes with varying requirements for product approvals, quality standards, and post-market surveillance. For instance, while Japan follows stringent regulatory guidelines akin to those of the FDA under the Pharmaceuticals and Medical Devices Agency (PMDA), other countries like Indonesia and Vietnam have less mature regulatory systems that can be inconsistent and unpredictable. As per Deloitte, navigating these disparate regulatory environments increases time-to-market for IVD manufacturers and raises compliance costs, especially for small and medium-sized enterprises. These regulatory hurdles discourage investment and delay the introduction of innovative diagnostic products, particularly in lower-tier markets where the return on investment may not justify the administrative burden.

Limited Reimbursement Coverage and Affordability Issues

Limited reimbursement coverage and affordability concerns represent another critical restraint affecting the growth of the Asia Pacific in vitro diagnostics (IVD) market. While healthcare systems in developed countries like Japan and Australia offer comprehensive reimbursement policies for diagnostic tests, many emerging economies in the region lack structured reimbursement frameworks, particularly for advanced molecular and genetic tests. In countries such as India and the Philippines, out-of-pocket expenditure constitutes a significant portion of total healthcare spending. Even when diagnostic services are available, cost remains a barrier for low-income patients. Moreover, pricing pressures from government tenders and procurement practices in public health systems further compress profit margins for IVD manufacturers. In China, for example, frequent price cuts mandated during tender rounds have affected profitability and discouraged innovation.

MARKET OPPORTUNITIES

Growth of Point-of-Care Testing in Rural and Remote Areas

One of the most promising opportunities in the Asia Pacific in vitro diagnostics (IVD) market is the growing adoption of point-of-care testing (POCT) in rural and remote areas. With vast geographical landscapes and uneven distribution of healthcare resources, many countries in the region face significant gaps in diagnostic accessibility. POCT offers a viable solution by enabling rapid, on-site diagnosis without the need for centralized laboratories. Governments and private entities across the Asia Pacific region are increasingly investing in portable diagnostic devices and mobile health units to bridge this gap. For example, in China, the Ministry of Science and Technology has launched initiatives to promote POCT technologies in primary healthcare settings, especially in underdeveloped provinces. Moreover, advancements in microfluidics, biosensors, and smartphone-based diagnostics have enabled the development of affordable and user-friendly POCT devices. Companies like Abbott and Roche have introduced compact diagnostic systems tailored for resource-limited settings.

Integration of Artificial Intelligence and Digital Health Platforms in Diagnostics

The integration of artificial intelligence (AI) and digital health platforms into diagnostic workflows presents a transformative opportunity for the Asia Pacific in vitro diagnostics (IVD) market. AI-powered analytics, machine learning algorithms, and cloud-based data management systems are increasingly being adopted to enhance diagnostic accuracy, streamline operations, and enable predictive healthcare. Countries like Singapore and South Korea are leading the way in implementing AI-driven diagnostics. For instance, Singapore’s National University Health System has partnered with tech firms to develop AI-assisted pathology tools that reduce human error and accelerate test result interpretation. Digital health platforms are also gaining traction in emerging markets. In India, telemedicine startups like Apollo Telehealth and HealthifyMe are incorporating diagnostic data into electronic health records (EHRs), allowing physicians to make real-time clinical decisions. Additionally, blockchain technology is being explored to ensure secure data exchange between diagnostic labs, hospitals, and insurers.

MARKET CHALLENGES

Talent Shortage and Skilled Workforce Deficit

A major challenge facing the Asia Pacific in vitro diagnostics (IVD) market is the shortage of skilled professionals capable of operating advanced diagnostic equipment and interpreting complex test results. Despite rapid technological advancements in diagnostic tools, the availability of trained clinical laboratory scientists, pathologists, and technicians remains inadequate, particularly in rural and semi-urban areas. According to the World Health Organization (WHO), the doctor-to-patient ratio in many parts of South and Southeast Asia is well below the recommended standard, exacerbating the strain on existing healthcare personnel. In India, for instance, the Association of Clinical Biochemists of India reports that there is a severe deficit of certified medical laboratory technologists, with only one technician available per 10,000 people. This workforce deficit hampers the efficiency and scalability of diagnostic services, particularly as demand for precision diagnostics rises. Hospitals and diagnostic centers often struggle to maintain turnaround times and ensure consistent quality due to insufficient staffing levels. Furthermore, the lack of standardized training programs across the region leads to variability in diagnostic accuracy and reliability.

Supply Chain Disruptions and Dependence on Imported Raw Materials

Supply chain disruptions and reliance on imported raw materials pose a significant challenge to the sustainability and resilience of the Asia Pacific in vitro diagnostics (IVD) market. Many countries in the region depend heavily on external suppliers for critical components such as enzymes, monoclonal antibodies, reagents, and consumables used in diagnostic assays. China and India, two of the largest IVD markets in the region, import a substantial portion of their diagnostic reagents and consumables from Europe and the United States.

SEGMENTAL ANALYSIS

By Test Type Insights

The clinical chemistry segment was the largest and held 35.4% of the Asia Pacific in vitro diagnostics market share in 2024 due to its widespread application in routine health check-ups and chronic disease monitoring, particularly for conditions such as diabetes, hypertension, and liver disorders. According to the World Health Organization (WHO), non-communicable diseases account for nearly two-thirds of all deaths in the region, reinforcing the reliance on clinical chemistry tests for early detection and long-term patient management. The rising prevalence of metabolic disorders has significantly boosted demand for biochemical assays. For instance, in India alone, over 77 million adults were living with diabetes in 2021, a number projected to reach nearly 134 million by 2045 as per the International Diabetes Federation. Additionally, government initiatives aimed at expanding diagnostic access have played a pivotal role. The Indian government’s Ayushman Bharat scheme, which covers over 500 million individuals, has increased affordability and utilization of laboratory services.

The molecular diagnostics segment is lucratively to grow with an expected CAGR of 13.6% in the coming years. One of the major catalysts for this growth is the surge in investments in genomic research and biotechnology infrastructure across the region. Japan, South Korea, and Singapore have been at the forefront of integrating molecular diagnostics into national healthcare strategies. Moreover, the ongoing impact of the COVID-19 pandemic has accelerated the deployment of RT-PCR and CRISPR-based diagnostic technologies.

By Product Insights

The reagents segment accounted in holding 59.3% of the Asia Pacific in vitro diagnostics market share in 2024. A primary driver behind the dominance of the reagents segment is the increasing volume of diagnostic tests performed across hospitals, reference labs, and point-of-care settings. Similarly, in China, the National Health Commission reported that the number of medical lab technicians surpassed 1.2 million in 2023, which indicates a robust ecosystem for continuous diagnostic activity. Another critical factor is the shift toward automated and high-throughput testing systems, which require a consistent supply of specialized reagents. Furthermore, the rise in government-backed public health programs focusing on infectious disease screening, maternal health, and chronic disease management has spurred regular procurement of diagnostic reagents.

The instruments segment is lucratively to grow lucratively with an estimated CAGR of 12.1% from 2025 to 2033 with the modernization of diagnostic infrastructure, rising investments in automation, and the expansion of centralized and decentralized testing facilities across both developed and emerging economies. Moreover, the proliferation of point-of-care testing (POCT) devices is contributing to instrument sales growth. In India, the Ministry of Health and Family Welfare supported the deployment of portable diagnostic kits under the Ayushman Bharat Digital Mission, which saw over 200,000 POCT devices distributed to primary health centers by 2023. Additionally, partnerships between global IVD manufacturers and local distributors are accelerating instrument penetration. Companies such as Roche, Abbott, and Sysmex have expanded their service and installation networks in Southeast Asia, facilitating easier access to sophisticated diagnostic equipment.

By Usability Insights

The disposable segment was the largest and held a dominant share of share in 2024. A key driver behind the widespread adoption of disposable IVD devices is the rising incidence of infectious diseases across the region. According to the World Health Organization (WHO), Southeast Asia accounts for a significant proportion of global tuberculosis and dengue cases, necessitating rapid and reliable diagnostic tools. Moreover, government initiatives promoting home-based and community-level diagnostics have further propelled the use of disposable diagnostic kits. In Indonesia, the Ministry of Health distributed over 25 million disposable malaria RDT kits in 2023 to support early detection in remote islands. As per Frost & Sullivan, the growing popularity of self-testing kits for glucose, pregnancy, and infectious diseases is another factor reinforcing the market dominance of disposable IVD devices.

The reusable segment is projected to grow with a CAGR of 10.8% in the coming years, owing to the adoption of reusable diagnostic equipment, the rising capital investment in centralized laboratories, and hospital-based diagnostics. Countries like China and Japan are increasingly favoring durable, high-throughput instruments such as automated immunoassay analyzers and hematology systems that can be reused across thousands of tests. Environmental concerns are also shaping policy frameworks that encourage the reuse of medical devices. In Australia, the National Sustainability Framework introduced guidelines in 2022 promoting the sterilization and repurposing of diagnostic instruments to reduce biomedical waste. Additionally, advancements in device sterilization techniques and digital asset tracking systems have enhanced the feasibility of reuse. In South Korea, smart hospitals equipped with IoT-enabled diagnostic machines have improved maintenance cycles and extended device lifespans.

By Application Insights

The infectious diseases segment was the largest and held 37.4% of the Asia Pacific in vitro diagnostics market share in 2024. According to the World Health Organization (WHO), the Western Pacific Region alone reported over 3.4 million new tuberculosis cases in 2023, making it one of the most prevalent infectious diseases in the region. Government-led public health campaigns have played a crucial role in expanding diagnostic access. In India, the Revised National Tuberculosis Control Program (RNTCP) facilitated the distribution of over 100 million GeneXpert cartridges in 2023 to enable rapid TB detection using molecular diagnostics. The post-pandemic era has also reinforced the importance of infectious disease diagnostics. In China, the National Health Commission mandated routine pathogen screening in hospitals, significantly increasing the use of multiplex PCR panels and antigen-detection kits.

The cancer/oncology segment is expected to witness a CAGR of 14.2% from 2025 to 2033, owing to the rising cancer incidence rates, increasing awareness of early detection, and the adoption of precision medicine approaches tailored to individual genetic profiles. According to the International Agency for Research on Cancer (IARC), Asia accounts for nearly 50% of global cancer cases, with China, India, and Japan witnessing sharp increases in diagnoses. In 2023, China alone recorded over 4.8 million new cancer cases, with lung, breast, and colorectal cancers being the most prevalent. Governments across the region are investing heavily in oncology diagnostics to improve survival rates. In Japan, the Ministry of Health, Labour and Welfare introduced coverage for next-generation sequencing (NGS)-based cancer profiling under the national insurance scheme in 2022.

REGIONAL ANALYSIS

China dominated the regional in-vitro diagnostics (IVD) market owing to the rising adoption of the in-vitro diagnostics (IVD) process in hospitals, growth in the older population, and increased awareness among patients. The favorable government initiatives, investments in the medical sector research and development activities, and collaborations in pharmaceutical, healthcare, and biotechnology industries are promoting the Chinese IVD market. India is an emerging nation in terms of in-vitro diagnostics supported by the rapid development.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific in vitro diagnostics market is marked by a dynamic mix of global leaders, regional players, and emerging startups striving to capture market share through differentiation and innovation. Multinational corporations leverage their technological expertise, established brand reputation, and extensive distribution networks to maintain dominance, particularly in developed markets such as Japan, South Korea, and Australia. At the same time, domestic manufacturers in countries like China and India are rapidly gaining traction by offering cost-competitive solutions tailored to local healthcare infrastructures. This dual-market dynamic fosters intense rivalry, especially in segments such as point-of-care diagnostics and molecular testing. Additionally, the rising demand for rapid and accurate diagnostic tools has led to increased collaboration between international firms and local partners, further intensifying the competitive landscape. Companies are also investing in digital integration, AI-based analytics, and automation to differentiate their offerings.

KEY MARKET PLAYERS

Noteworthy companies operating in the APAC IVD Market include

- Abbott Laboratories

- Johnson & Johnson

- Siemens Healthcare

- Becton Dickinson

- Roche Diagnostics

- Beckman Coulter Inc.

- bioMérieux

- Ortho Clinical Diagnostics, Inc.

- Bio-Rad Laboratories, Inc.

- Danaher Corporation

- Sysmex Corporation

- Thermo Fisher Scientific, Inc.

Top Players in the Asia Pacific In Vitro Diagnostics Market

One of the leading players in the Asia Pacific in vitro diagnostics market is F. Hoffmann-La Roche Ltd., commonly known as Roche. The company has a strong presence across multiple diagnostic segments, including molecular diagnostics, immunoassays, and clinical chemistry. Roche’s commitment to innovation and its focus on personalized healthcare have made it a dominant force in the region. Its diagnostic division offers a wide range of solutions, from high-end automated analyzers to companion diagnostics, supporting precision medicine initiatives. Roche also collaborates with local governments and research institutions to enhance diagnostic accessibility and efficiency.

Another key player is Abbott Laboratories, which has significantly expanded its footprint in the Asia Pacific IVD market through strategic acquisitions and localized product development. Abbott is particularly recognized for its point-of-care testing solutions, such as the Alere platform, which plays a crucial role in infectious disease diagnostics. The company emphasizes affordability and portability, making its products suitable for both urban hospitals and rural clinics. Abbott's extensive distribution network ensures widespread availability of diagnostic kits and instruments across diverse healthcare settings in the region.

Sysmex Corporation holds a prominent position in the Asia Pacific IVD landscape, especially in hematology and coagulation testing. Headquartered in Japan, Sysmex has leveraged its regional expertise to expand into emerging markets like India, Southeast Asia, and Oceania. The company is known for its advanced automation technologies and integrated laboratory solutions that enhance workflow efficiency and diagnostic accuracy. Sysmex also invests heavily in research and development, focusing on oncology and infectious disease diagnostics, while maintaining strong partnerships with public health agencies to support large-scale screening programs.

Top Strategies Used by Key Market Participants

Key players in the Asia Pacific in vitro diagnostics market employ several strategies to strengthen their competitive edge. One major approach is expanding through mergers and acquisitions by allowing companies to integrate complementary technologies and broaden their geographic reach. These moves help firms accelerate product development and gain access to established distribution networks, enhancing their presence in high-growth markets.

Another critical strategy is introducing innovative diagnostic platforms tailored for local healthcare needs, particularly in resource-limited settings. Companies are increasingly developing cost-effective, portable, and easy-to-use diagnostic tools that align with the infrastructure and affordability constraints of emerging economies by ensuring broader adoption and sustained market penetration.

Forming strategic collaborations with government bodies, academic institutions, and regional distributors plays a vital role in market expansion. These partnerships facilitate regulatory approvals, improve access to public health programs, and enable technology localization, thereby reinforcing long-term market positioning and brand credibility across diverse healthcare ecosystems in the Asia Pacific region.

RECENT MARKET DEVELOPMENTS

- In June 2023, Roche launched a new molecular diagnostics initiative in collaboration with Singapore General Hospital to develop AI-integrated pathology workflows. This move aimed to enhance early cancer detection capabilities and support precision medicine efforts across the region.

- In September 2023, Abbott introduced a next-generation point-of-care testing device tailored for rural healthcare settings in India. Designed to operate without constant electricity, this launch was part of Abbott’s broader effort to improve diagnostic accessibility in remote areas.

- In February 2024, Sysmex partnered with a leading Vietnamese hospital to deploy an automated hematology analyzer system. The initiative focused on improving blood disorder diagnostics and strengthening laboratory efficiency in Vietnam’s public healthcare sector.

- In May 2024, Danaher expanded its presence in the Chinese IVD market by opening a new R&D center in Shanghai. The facility was dedicated to adapting diagnostic technologies to meet the specific needs of Chinese healthcare providers and accelerating product localization.

- In August 2024, Becton Dickinson announced a joint venture with a Japanese biotech firm to co-develop novel infectious disease assays using CRISPR-based detection methods. The partnership aimed to address growing concerns around antibiotic resistance and viral outbreaks in the Asia Pacific region.

MARKET SEGMENTATION

This research report on the Asia-Pacific in-vitro diagnostics (IVD) market is segmented and sub-segmented into the following categories.

By Test Type

- clinical chemistry

- molecular diagnostics

By Product

- Reagents

- Instruments

- Software & Services

By Technique

- Immunochemistry

- Clinical Chemistry

- Molecular Diagnostics

- Hematology

- Others

By Application

- Infectious Diseases

- Oncology

- Cardiology

- Diabetes

- Autoimmune Diseases

- Nephrology

- Gastroenterology

- Others

By End User

- Clinical Laboratories

- Hospitals

- Physician’s Offices

- Others

By Region

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

What is the current size of the Asia Pacific In-Vitro Diagnostics Market?

The APAC IVD Market is expected to be valued at USD 18.24 billion in 2024.

Which countries contribute the most to the Asia Pacific In-Vitro Diagnostics Market share?

Japan, China, and India are the leading contributors to the Asia Pacific In-Vitro Diagnostics Market share

What are the key trends driving growth in the Asia Pacific In-Vitro Diagnostics Market?

Increasing adoption of advanced diagnostic technologies, rising healthcare awareness, and a growing aging population are among the key trends fueling APAC IVD market growth.

How has the COVID-19 pandemic impacted the Asia Pacific In-Vitro Diagnostics Market?

The pandemic has accelerated the demand for diagnostic solutions, leading to a surge in the adoption of in vitro diagnostics (IVD) in the APAC region.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com