Asia Pacific Secondhand Luxury Goods Market Size, Share, Growth, Trends, and Forecast Report By Product Type (Handbags, Jewelry & Watches, Clothing, Small Leather Goods, Footwear, Accessories, and Other), Distribution Channel, and Region (India, China, Japan, South Korea, Australia & New Zealand, Thailand) - Industry Analysis from 2026 to 2034

Asia Pacific Secondhand Luxury Goods Market Size

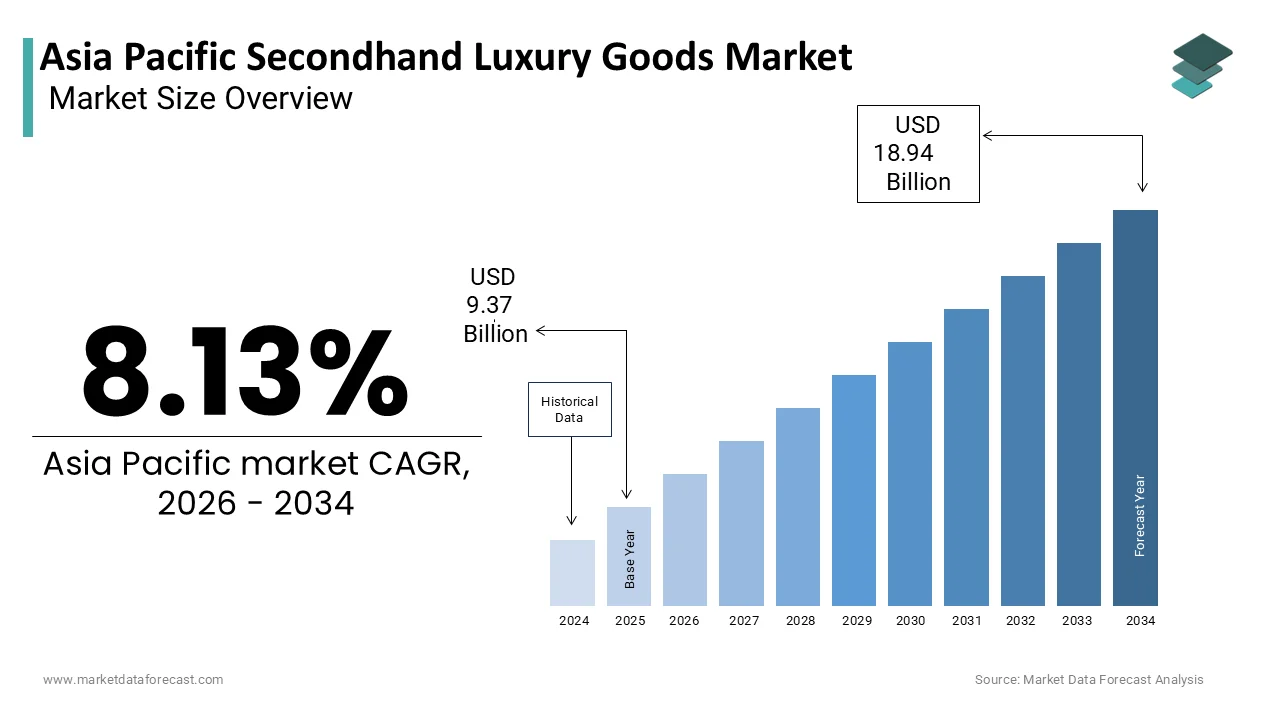

The Asia Pacific secondhand luxury goods market size was valued at USD 9.37 billion in 2025, and the market size is expected to reach USD 18.94 billion by 2034 from USD 10.14 billion in 2026. The market's promising CAGR for the predicted period is 8.13%.

Secondhand luxury goods refer to the resale of authenticated high-end fashion items, including apparel, accessories, timepieces, and jewellery, through both digital platforms and brick-and-mortar boutiques. This market has evolved beyond mere cost-saving consumption, reflecting a cultural pivot toward sustainable ownership and circular fashion economies. Japan, a longstanding hub for vintage luxury, sees nearly 40% of its luxury watch transactions occur in the secondary market, according to a 2022 report by the Japan Watch & Clock Association. This shift is further reinforced by the region’s expanding digital infrastructure, where platforms like Reebelo and Carousell integrate authentication protocols to bolster consumer trust.

MARKET DRIVERS

Rising Environmental Consciousness Among Younger Demographics

Environmental sustainability has emerged as a decisive influence on purchasing behaviour, particularly among Millennials and Generation Z across the Asia Pacific. The fashion industry accounts for nearly 10% of global carbon emissions, prompting regulatory scrutiny and consumer backlash, as per the United Nations Environment Programme. In response, younger buyers are increasingly turning to pre-owned luxury to reduce ecological footprints. In Australia, resale platform The RealReal reported a year-on-year increase in Gen Z users in 2024. This eco-conscious mindset is institutionalising secondhand luxury as a morally and aesthetically valid alternative.

Expansion of Digital Authentication and E-Resale Platforms

The proliferation of technologically advanced resale ecosystems has significantly lowered entry barriers for consumers seeking genuine pre-owned luxury items. Platforms such as Vestiaire Collective and LUXE.co employ AI-driven image analysis and blockchain-based provenance tracking to verify authenticity, directly addressing long-standing trust deficits. These platforms integrate real-time market valuation algorithms, enabling dynamic pricing and enhancing liquidity. Furthermore, social commerce integration on apps like WeChat and LINE has enabled peer-to-peer reselling with embedded verification, accelerating market penetration in tier-2 and tier-3 cities across the region.

MARKET RESTRAINTS

Persistent Stigma Around Pre-Owned Ownership in Emerging Economies

Despite growing acceptance, cultural reservations about secondhand consumption persist in several Asia Pacific markets, particularly where luxury ownership symbolises social ascent. The mindset is especially entrenched among older demographics, where gifting new luxury items remains a cultural norm. Additionally, the absence of formal inheritance or gifting resale frameworks discourages circulation. These socio-cultural barriers impede market fluidity and dampen resale velocity.

Regulatory Fragmentation and Lack of Standardised Authentication Frameworks

The absence of harmonised regulations governing the authentication and taxation of pre-owned luxury goods creates operational inefficiencies and legal ambiguities across the Asia Pacific. In Thailand, customs authorities classify secondhand luxury items as used goods, subjecting them to import restrictions and higher scrutiny, as outlined in the 2024 Royal Thai Customs Department guidelines. Meanwhile, cross-border resale platforms face inconsistent VAT treatments: in Australia, GST applies to all resale transactions, whereas in Singapore, private peer-to-peer sales remain untaxed. This regulatory disarray hampers scalability and deters institutional investment.

MARKET OPPORTUNITIES

Integration of Blockchain for Provenance and Ownership Tracking

Blockchain technology presents a transformative opportunity to enhance transparency and trust in the Asia Pacific’s secondhand luxury ecosystem. By creating immutable digital ledgers for ownership history, maintenance records, and authenticity verification, blockchain mitigates fraud and increases resale value retention. Hence, blockchain integration can unlock premium pricing and deepen consumer loyalty.

Strategic Partnerships Between Luxury Brands and Resale Platforms

Forward-thinking luxury brands are increasingly collaborating with certified resale operators to capture value from the secondary market, rather than ceding it to third parties. In 2024, Richemont acquired a majority stake in Watchfinder & Co., enabling direct control over pre-owned watch distribution in Asia. These alliances not only legitimise the secondhand channel but also enable brands to gather valuable post-purchase behavioural data, refine product longevity strategies, and reinforce sustainability narratives.

MARKET CHALLENGES

Proliferation of Counterfeit Goods in Informal Market Channels

The informal resale sector across the Asia Pacific remains heavily infiltrated by counterfeit luxury items, eroding consumer trust and distorting market dynamics. In Vietnam, the Saigon Commercial Bank’s 2024 retail integrity survey estimated that a portion of secondhand luxury bags sold in unauthorised markets were fake, often indistinguishable to untrained buyers. These illicit goods frequently originate from unregulated manufacturing hubs and are distributed via social media marketplaces like Facebook groups and TikTok Shop, where authentication mechanisms are absent. This undermines legitimate resale platforms and complicates brand efforts to engage with circular economies.

Inconsistent Valuation Standards and Price Volatility

The absence of standardised pricing models for pre-owned luxury goods leads to significant valuation disparities across platforms and geographies, discouraging both buyers and sellers. In India, the same pre-owned Chanel flap bag can vary price between online marketplaces and physical consignment stores. In Australia, the resale value of luxury watches fluctuates quarterly due to speculative trading. This volatility stems from fragmented data sources, subjective condition grading, and limited historical transaction transparency. In China, the lack of a centralised pricing database forces platforms to rely on manual appraisal, increasing turnaround time and error rates.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Distribution Channel, and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of Asia-Pacific |

| Market Leaders Profiled | Vestiaire Collective, The RealReal, FASHIONPHILE Group, Rebag, The Luxury Closet, and Luxepolis, and others |

SEGMENTAL ANALYSIS

By Product Type Insights

The handbags segment dominated the Asia Pacific secondhand luxury goods market by accounting for an estimated 34.2% of total value in 2025. This pre-eminence is anchored in the enduring collectible status of iconic designs such as the Hermès Birkin and Chanel Classic Flap, which retain or appreciate in value over time. The Birkin, in particular, has appreciated at an average annual rate of 14% over the past decade, outperforming traditional asset classes. Additionally, handbags are less susceptible to wear-and-tear compared to clothing or footwear, enhancing their resale viability. The emotional and symbolic equity attached to designer handbags—often perceived as heirlooms—further entrenches their centrality in the secondhand ecosystem.

The jewelry and watches segment is the fastest-growing product and is projected to expand at a CAGR of 12.7% from 2025 to 2033. This acceleration is fueled by rising interest in investment-grade timepieces, particularly among affluent male consumers in urban China and South Korea. Rolex and Patek Philippe watches have demonstrated consistent appreciation. Furthermore, the intrinsic material value of gold, platinum, and gemstones provides a hedge against inflation, making pre-owned fine jewelry a preferred alternative asset. Enhanced authentication technologies specific to horology, such as serial number tracing and movement analysis, have also reduced fraud risks, accelerating market trust.

By Distribution Channel Insights

The offline channels segment continued to command the Asia Pacific secondhand luxury goods market by holding a 56.4% share in 2025. This dominance is sustained by the tactile nature of luxury evaluation, where physical inspection of stitching, hardware, and patina remains critical for high-value purchases. The integration of offline stores within premium shopping malls, such as Isetan in Tokyo and Siam Paragon in Bangkok, further legitimises the secondhand sector. These physical spaces also serve as experience hubs, offering repair, refurbishment, and trade-in services that deepen customer engagement and reinforce brand credibility.

The online distribution channel is growing at the fastest pace and is registering a CAGR of 16.3% from 2025 to 203. This surge is propelled by the proliferation of mobile-first platforms and integrated authentication ecosystems that bridge trust gaps in digital transactions. These platforms employ AI-powered image recognition and blockchain-backed certificates to verify items, reducing return rates. Social commerce integration on WeChat and LINE allows peer-to-peer reselling with embedded escrow and verification, particularly in Indonesia and Thailand, where mobile penetration exceeds 85%. Additionally, logistics advancements, such as same-day delivery in Singapore and AI-driven condition grading in Australia, have streamlined the online experience, making it increasingly competitive with physical retail.

REGIONAL ANALYSIS

Japan Secondhand Luxury Goods Market Insights

Japan stood as the most mature and structurally advanced market for secondhand luxury goods in the Asia Pacific by capturing an estimated 31.6% share in 2025. The country’s dominance is rooted in a long-established culture of consignment and meticulous item care, where luxury goods are often passed down or resold after limited use. Moreover, the government’s strict regulation of secondhand dealers under the Secondhand Goods Business Act ensures transparency and reduces counterfeit circulation, fostering consumer confidence. This regulatory rigor, combined with a shrinking domestic population that encourages asset liquidation, sustains Japan’s leadership in volume, value, and market sophistication.

China Secondhand Luxury Goods Market Insights

China is also a key player in the Asia Pacific secondhand luxury market. The market’s rapid expansion is driven by a confluence of rising disposable incomes, digital adoption, and shifting generational values. Platforms like Plum and Feidieshop have scaled rapidly by integrating livestream authentication sessions and AI-powered valuation tools. Additionally, the depreciation of new luxury prices due to oversupply has made pre-owned items relatively more attractive, with some authenticated handbags trading at premiums over retail, as observed by the China Luxury Resale Index.

South Korea Secondhand Luxury Goods Market Insights

South Korea occupies strong position in the market. The country’s growth is characterised by a tech-savvy, status-conscious consumer base that increasingly embraces resale as a socially acceptable and economically rational choice. Platforms like Joonggonara and Danggeun Market have evolved from general classifieds into curated luxury resale hubs, leveraging user ratings and third-party verification to ensure credibility. The rise of “flex culture”, where consumers rotate luxury items for social media visibility, has amplified demand for short-term ownership models. Furthermore, the Korea Fair Trade Commission’s 2024 guidelines mandating transparency in secondhand pricing have reduced information asymmetry, boosting transaction volumes.

Australia Secondhand Luxury Goods Market Insights

Australia is positioning notable contributor. The market is distinguished by high per-capita spending on pre-owned luxury, particularly in urban centres like Sydney and Melbourne, where sustainability concerns are reshaping consumer priorities. Additionally, Australia’s Goods and Services Tax (GST) neutrality on secondhand goods creates a pricing advantage over new imports, making resale more financially appealing. The country’s stringent consumer protection laws further enhance trust, with the Australian Competition and Consumer Commission recording a decline in luxury resale disputes between 2021 and 2024, indicating maturing market standards.

India Secondhand Luxury Goods Market Insights

India captures small share of the regional secondhand luxury market. While still nascent compared to East Asian markets, India’s sector is gaining momentum due to the emergence of a young, digitally fluent affluent class in cities like Mumbai, Delhi, and Bengaluru. Startups such as Fashor and PreOwnedLuxury.in have introduced certification processes and buyback guarantees to counteract trust deficits. The market is also supported by the growing popularity of luxury gifting and weddings, where pre-owned items are increasingly accepted as status symbols. Despite this, rising environmental awareness and platform innovation suggest strong long-term potential.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Key players in the Asia Pacific secondhand luxury goods market include Vestiaire Collective, The RealReal, FASHIONPHILE Group, Rebag, The Luxury Closet, and Luxepolis.

The competitive landscape of the Asia Pacific secondhand luxury goods market is marked by a dynamic interplay between established regional consignment retailers and global digital platforms. Japanese players like Komehyo and Daikokuya benefit from decades of consumer trust and robust offline networks, while international entrants such as Vestiaire Collective and The RealReal leverage technology and brand partnerships to gain traction. Localized startups in India and Southeast Asia are challenging incumbents with mobile-first models tailored to younger demographics. Authentication accuracy, pricing transparency, and logistics efficiency have become key differentiators. The entry of luxury conglomerates into resale through equity stakes or collaborations further intensifies competition, pushing firms to innovate in customer experience, sustainability reporting, and cross-border accessibility.

TOP PLAYERS IN THE MARKET

Vestiaire Collective

Vestiaire Collective has established a formidable presence across the Asia Pacific by positioning itself as a curator of authenticated pre-owned fashion, with a strong foothold in Japan, South Korea, and Australia. The platform leverages a hybrid authentication model combining AI and human expertise to ensure trust, a critical factor in high-value transactions. It also partnered with Kering brands to introduce verified resale programs, allowing original manufacturers to authenticate items and earn referral fees. By integrating social commerce features and expanding logistics partnerships with DHL and Japan Post, Vestiaire has streamlined cross-border trade, making it easier for APAC consumers to access global inventory while adhering to regional customs and tax regulations.

Rebag

Rebag has extended its influence beyond North America by forging strategic alliances with logistics and authentication partners in key Asia Pacific markets, particularly in Japan and Australia. Although not operating standalone retail in the region, Rebag’s digital marketplace is accessible to APAC consumers, offering a premium catalog of handbags and accessories with transparent pricing powered by its proprietary Lorraine index. The company also introduced a carbon-neutral shipping option for international orders, appealing to environmentally conscious clients. By emphasizing data-driven valuation and luxury-grade packaging, Rebag has differentiated itself as a high-trust platform for cross-border secondhand luxury transactions, particularly among affluent Australian and expatriate consumers.

Komehyo

Komehyo, a Japanese consignment giant, remains a dominant force in the Asia Pacific secondhand luxury market through its deeply rooted retail network and institutional credibility. Operating over 150 physical stores across Japan, Komehyo specializes in handbags, watches, and jewelry, with rigorous in-house authentication protocols staffed by certified appraisers. It also launched a trade-in rewards program that incentivizes repeat selling, fostering customer loyalty. Komehyo’s collaboration with MUJI to open co-branded retail zones in Osaka and Fukuoka introduced secondhand luxury to minimalist lifestyle consumers. Its emphasis on transparency—publishing detailed provenance and repair history—has solidified trust, making it a preferred destination for both domestic and international buyers sourcing authentic pre-owned items from Japan.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Key players in the Asia Pacific secondhand luxury goods market are deploying a combination of technological integration, strategic partnerships, and localization to strengthen their positions. Leading platforms are investing in AI-driven authentication systems and blockchain-based provenance tracking to enhance trust and reduce fraud. Companies are forming alliances with luxury brands to offer certified resale programs, enabling original manufacturers to participate in secondary sales. Expansion into tier-2 and tier-3 cities via mobile-first platforms and social commerce is accelerating market penetration. Physical retailers are integrating omnichannel models, combining brick-and-mortar credibility with digital scalability. Additionally, firms are launching trade-in incentives, carbon-neutral shipping, and dynamic pricing algorithms to improve customer retention and operational efficiency across diverse regulatory environments.

RECENT HAPPENINGS IN THE MARKET

- In March 2024, Vestiaire Collective launched a dedicated authentication center in Seoul, enhancing verification speed and accuracy for Korean consumers and expanding its regional trust infrastructure.

- In June 2024, Komehyo partnered with MUJI to introduce co-branded retail spaces in Osaka and Fukuoka, integrating secondhand luxury into minimalist lifestyle shopping environments.

- In September 2024, Rebag collaborated with Japanese authentication specialist Brandalley to improve verification standards for high-demand Hermès and Chanel handbags in the APAC market.

- In November 2024, Vestiaire Collective integrated blockchain-powered provenance tracking with LVMH’s AURA platform, enabling transparent ownership history for select luxury items sold in Asia.

- In February 2025, Komehyo expanded its e-commerce platform with AI-driven condition grading, reducing appraisal processing time by 40% and improving scalability across Japan and export markets.

MARKET SEGMENTATION

This research report on the Asia Pacific secondhand luxury goods market has been segmented and sub-segmented based on the following categories.

By Product Type

- Handbags

- Jewelry & Watches

- Clothing

- Small Leather Goods

- Footwear

- Accessories

- Other

By Distribution Channel

- Offline

- Online

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. What is the Asia Pacific secondhand luxury goods market?

The market includes pre-owned luxury items like handbags, watches, jewelry, and apparel.

It is driven by affordability and sustainability trends across the region.

2. What are the main growth drivers of the market?

Increasing demand for affordable luxury, sustainability awareness, and digital resale platforms.

3. Which product segment dominates the market?

Handbags and accessories are the leading segments in Asia Pacific, and their popularity stems from high resale value and global brand demand.

4. Who are the key players in this market?

Major players include Vestiaire Collective, The RealReal, FASHIONPHILE, Rebag, and The Luxury Closet.

5. Which country has the largest share of the market?

China leads the Asia Pacific secondhand luxury goods market. Japan and South Korea also hold significant shares.

6. Which age group is the largest consumer base?

Millennials and Gen Z are the biggest buyers of secondhand luxury goods.

7. What challenges does the market face?

Counterfeit products and authenticity concerns remain major hurdles. However, verification technologies are reducing these risks.

8. What is the growth outlook for the market?

The market is expected to grow steadily with rising online adoption. Luxury brands collaborating with resale platforms will boost trust.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com