Global Clinical Laboratory Tests Market Size, Share, Trends & Growth Forecast Report By Test Type, Service Provider, End-User and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034

Market Size, 2025

$215.3 BnMarket Estimate, 2026

$228.71 BnMarket Forecast, 2034

$370.91 BnCAGR, 2026–2034

6.23%Global Clinical Laboratory Tests Market Report Summary

The global clinical laboratory tests market was valued at USD 215.3 billion in 2025, is estimated to reach USD 228.71 billion in 2026, and is projected to reach USD 370.91 billion by 2034, growing at a CAGR of 6.23% from 2026 to 2034. Market growth is driven by the increasing prevalence of chronic and infectious diseases, rising demand for early and accurate diagnosis, and expanding healthcare infrastructure worldwide. Clinical laboratory testing plays a critical role in disease detection, monitoring, and treatment planning. Additionally, advancements in diagnostic technologies, automation in laboratories, and increasing adoption of personalized medicine are further supporting market expansion.

Key Market Trends

- Rising demand for early disease detection and preventive diagnostics.

- Increasing prevalence of chronic and infectious diseases.

- Growing adoption of automated and high-throughput laboratory systems.

- Expansion of independent and reference laboratory networks.

- Advancements in molecular diagnostics and personalized medicine.

Segmental Insights

- Based on test type, the complete blood count (CBC) segment dominated the global clinical laboratory tests market by capturing 26.9% share in 2025, driven by its widespread use in routine diagnostics.

- Based on service provider, the independent and reference laboratories segment led the market with 56.1% share in 2025, supported by their specialized capabilities and large-scale operations.

- Based on end-user, the central laboratories segment held the largest share of 60.6% in 2025, due to centralized testing and high processing volumes.

Regional Insights

The global clinical laboratory tests market is witnessing steady growth across major regions due to increasing diagnostic demand and healthcare advancements.

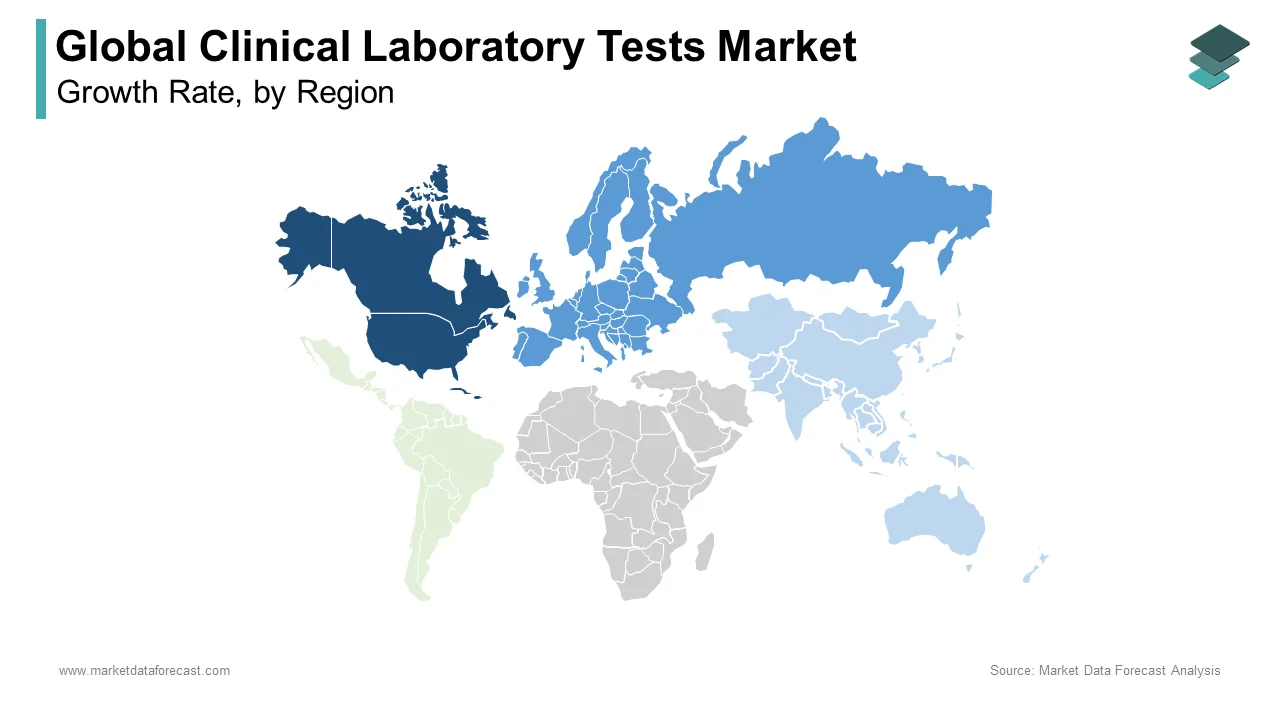

- North America led the market in 2025 with 40.2% share, supported by advanced healthcare infrastructure and high testing volumes.

- Europe followed as the second-largest market, driven by strong healthcare systems and widespread access to diagnostic services.

- Asia-Pacific is the fastest-growing region due to large population base, improving healthcare infrastructure, and increasing awareness of diagnostic testing.

Competitive Landscape

The global clinical laboratory tests market is highly competitive, with major diagnostic service providers and laboratory networks focusing on expanding their capabilities and geographic presence. Companies are investing in advanced diagnostic technologies, automation, and strategic partnerships to enhance efficiency and service quality.

Prominent companies operating in the global clinical laboratory tests market include Quest Diagnostics, Inc., Laboratory Corporation of America, LLC, Eurofins Scientific, Fresenius Medical Care, NeoGenomics Laboratories Inc., Siemens Healthineers, OPKO Health, Inc., Abbott Laboratories, Inc., Charles River Laboratories International, Inc., Sonic Healthcare Ltd., and Genoptix, Inc.

Global Clinical Laboratory Tests Market Size

The size of the global clinical laboratory tests market was worth USD 215.3 billion in 2025. The global market is anticipated to grow at a CAGR of 6.23% from 2026 to 2034 and be worth USD 370.91 billion by 2034 from USD 228.71 billion in 2026.

Clinical laboratory tests are a critical sector of healthcare dedicated to the in vitro examination of bodily fluids, tissues, and other substances to diagnose, monitor, and treat diseases. These diagnostic procedures serve as the cornerstone of modern medicine, which influences medical decisions, according to the Centers for Disease Control and Prevention. The scope ranges from routine hematology and chemistry panels to complex molecular diagnostics and genomic sequencing. In the United States, clinical laboratories process a vast number of tests annually. As per the American Clinical Laboratory Association, the immense volume is required to sustain population health management. The shift towards preventive care has amplified the necessity for early detection, with screening programs now covering a large portion of the adult population for conditions like diabetes and hypertension, according to the World Health Organization. Furthermore, the integration of laboratory data into electronic health records has streamlined clinical workflows, which allows physicians to access test results quickly, as documented by the Office of the National Coordinator for Health Information Technology. The rising prevalence of chronic diseases necessitates continuous monitoring, with millions of Americans living with at least one chronic condition that requires regular laboratory assessment, as reported by the National Institutes of Health. This ecosystem functions as the silent engine of healthcare delivery, which is providing the empirical evidence necessary for precise therapeutic interventions.

MARKET DRIVERS

Escalating Global Prevalence of Chronic and Infectious Diseases

The surging incidence of chronic conditions and persistent infectious disease outbreaks is driving the growth of the global clinical laboratory tests market. According to the World Health Organization, non-communicable diseases such as cancer, cardiovascular disorders, and diabetes contribute significantly to global mortality, which is creating an unprecedented need for diagnostic confirmation and ongoing monitoring. As per the International Agency for Research on Cancer, cancer diagnostics require extensive laboratory workups, including biopsy analysis, tumor marker testing, and genetic profiling. Diabetes management relies heavily on frequent blood glucose and HbA1c testing, with millions of adults requiring regular assessments to prevent complications, as reported by the International Diabetes Federation. Additionally, the emergence of novel pathogens and the resurgence of known infectious agents like tuberculosis and influenza mandate robust surveillance systems capable of processing large volumes of samples daily. According to the Centers for Disease Control and Prevention, laboratories perform a substantial number of respiratory viral tests during peak flu seasons to guide public health responses. The aging population further exacerbates this trend, as individuals over 65 typically undergo more laboratory tests than younger demographics due to multi-morbidity. This relentless rise in disease burden ensures a sustained and expanding volume of diagnostic requisitions across all healthcare settings.

Technological Advancements in Molecular Diagnostics and Automation

Breakthroughs in molecular diagnostics and high-throughput automation have fundamentally transformed the capacity and precision of clinical laboratories, which is further fuelling the clinical laboratory tests market growth. The advent of Next Generation Sequencing has democratized access to genomic information, allowing clinicians to identify rare genetic variants and tailor treatments with unprecedented accuracy. According to the National Human Genome Research Institute, the cost of sequencing a human genome has dropped significantly, which is making personalized medicine accessible to a broader patient base. Automation technologies have revolutionized workflow efficiency, with modern analyzers capable of processing thousands of tests per hour while minimizing human error and sample handling risks. As per the College of American Pathologists, automated pre-analytical systems have improved operational throughput by reducing specimen rejection rates. The integration of artificial intelligence in image analysis for pathology has enhanced diagnostic sensitivity, enabling the detection of malignant cells with high accuracy compared to manual microscopy, as documented by the Journal of Clinical Pathology. Liquid biopsy techniques now allow for non-invasive cancer detection through simple blood draws, expanding the addressable market for early screening. These technological leaps not only increase test volumes but also create entirely new categories of diagnostic services that were previously impossible to perform at scale.

MARKET RESTRAINTS

Stringent Regulatory Frameworks and Reimbursement Pressures

Complex regulatory landscapes and aggressive reimbursement cuts pose significant barriers to market growth, which is constraining the financial viability of many laboratory providers. In the United States, the Clinical Laboratory Improvement Amendments impose rigorous quality control and personnel standards that require substantial investment in compliance infrastructure. The Centers for Medicare and Medicaid Services has implemented the Protecting Access to Medicare Act, which mandates fee schedule reductions based on private payer rates, resulting in reimbursement cuts for many common tests. According to the American Clinical Laboratory Association, these reductions have forced a notable portion of independent laboratories to reduce their test menus or cease operations entirely due to unsustainable margins. In Europe, the In-Vitro Diagnostic Regulation has increased the time and cost required to bring new tests to market, with certification timelines extending significantly as per the European Commission. The lack of coverage for emerging molecular tests by major payers further limits adoption, with insurers denying reimbursement for advanced diagnostic claims, citing insufficient clinical utility evidence as reported by the Academy of Managed Care Pharmacy. These financial and bureaucratic hurdles stifle innovation and limit access to cutting-edge diagnostics, particularly for underserved populations who rely on public insurance programs.

Acute Shortage of Skilled Laboratory Professionals

A critical deficit of trained pathologists, medical technologists, and laboratory technicians is further hampering the clinical laboratory tests market growth. The aging workforce in this sector is retiring faster than new graduates can replace them, creating a widening gap between demand for testing and available human capital. According to the American Society for Clinical Pathology, vacancy rates for medical laboratory positions in the United States remain significant, with some regions experiencing acute shortages. This scarcity leads to increased turnaround times and potential burnout among existing staff, compromising the efficiency of diagnostic services. In low and middle-income countries, the situation is even more dire, with the World Health Organization reporting that many nations face severe shortages of laboratory workers. The complexity of modern diagnostic equipment requires specialized training that many educational institutions struggle to provide due to funding constraints and faculty shortages. As per the National Accrediting Agency for Clinical Laboratory Sciences, a considerable portion of training programs had to reduce enrollment due to a lack of qualified instructors. This workforce crisis threatens the scalability of laboratory services, forcing facilities to cap test volumes or outsource work to reference labs, which increases costs and delays results for patients in urgent need of diagnosis.

MARKET OPPORTUNITIES

Expansion of Point of Care Testing and Decentralized Diagnostics

The rapid evolution of point-of-care testing provides a promising opportunity for the clinical laboratory tests market. Miniaturization of assay technologies has enabled the development of handheld devices that deliver laboratory-grade results in minutes, which is facilitating immediate clinical decision-making. The global market for point-of-care diagnostics is projected to grow as hospitals seek to reduce length of stay and emergency departments aim to triage patients more efficiently. According to the Food and Drug Administration, the number of waived tests that can be performed outside traditional laboratories has increased, expanding the scope of practice for nurses and pharmacists. Remote and rural areas stand to benefit immensely, with mobile health units utilizing portable analyzers to screen for infectious diseases and chronic conditions in underserved populations. As per the Veterans Health Administration, home-based points of care monitoring programs have demonstrated improvements in managing chronic conditions. Integration with telehealth platforms allows remote interpretation of results by specialists, bridging geographical gaps in expertise. As reimbursement policies evolve to cover decentralized testing models, the potential for market penetration in retail clinics, pharmacies, and home care settings becomes vast, which is offering a lucrative avenue for growth beyond conventional hospital laboratories.

Integration of Artificial Intelligence and Big Data Analytics

The convergence of artificial intelligence and big data analytics with laboratory operations offers a profound opportunity for the clinical laboratory tests market. Machine learning algorithms can analyse vast datasets from millions of test results to identify subtle patterns and anomalies that human observers might miss, leading to earlier disease detection. According to the National Institutes of Health, AI-driven predictive models can forecast critical conditions before clinical symptoms manifest. Laboratories leveraging big data can also optimize inventory management and staffing schedules, reducing operational costs as per findings from the Healthcare Information and Management Systems Society. The aggregation of genomic and phenotypic data enables the discovery of novel biomarkers, accelerating the development of targeted therapies and companion diagnostics. Cloud-based platforms facilitate seamless data sharing across healthcare networks, fostering collaborative research and real time surveillance of emerging health threats. The Department of Health and Human Services notes that interoperable laboratory data systems improve care coordination for patients with complex chronic conditions. As computational power increases and algorithms become more sophisticated, the role of AI in transforming raw laboratory data into actionable clinical insights will redefine the value proposition of diagnostic services, which is opening new revenue streams and enhancing patient outcomes.

MARKET CHALLENGES

Data Interoperability and Cybersecurity Vulnerabilities

The fragmentation of health information systems and the escalating threat of cyber-attacks are primary challenges to the clinical laboratory tests market. Despite advancements in digital health, many laboratories still operate on legacy systems that cannot seamlessly exchange data with electronic health records used by hospitals and physician practices. According to the Office of the National Coordinator for Health Information Technology, a significant portion of laboratory results are still transmitted via fax or paper, leading to delays and transcription errors that compromise patient safety. Furthermore, the centralized storage of sensitive genetic and health data makes laboratories prime targets for ransomware attacks, which have increased in the healthcare sector in recent years, as per the Federal Bureau of Investigation. A single breach can expose the medical records of millions of patients, eroding public trust and incurring massive financial penalties under regulations like HIPAA and GDPR. The lack of standardized data formats hinders the effective application of advanced analytics and artificial intelligence, limiting the potential for population health management. Implementing robust cybersecurity measures and achieving true interoperability requires significant capital investment and technical expertise that many smaller laboratories lack. Until these systemic issues are resolved, the industry remains vulnerable to operational disruptions and data compromises that could undermine the reliability of diagnostic services.

Standardization of Emerging Diagnostic Methodologies

The rapid pace of innovation in diagnostic technologies often outstrips the development of standardized protocols, and validation criteria are further challenging the global clinical laboratory tests market. New methodologies such as liquid biopsies, multiplex PCR panels, and direct-to-consumer genetic tests frequently enter the market without universally accepted reference ranges or quality control benchmarks. According to the College of American Pathologists, inter-laboratory variability for certain novel molecular tests remains a challenge, which is leading to inconsistent clinical interpretations. The absence of harmonized guidelines complicates the efforts of clinicians to compare results from different sources or track disease progression over time. Regulatory bodies struggle to keep pace with technological advancements, resulting in a patchwork of approval processes that delay the availability of critical tests in some regions while allowing premature adoption in others. As per the International Organization for Standardization, many emerging diagnostic assays still lack established international standard reference materials. This lack of uniformity undermines confidence in new testing modalities and hampers the ability to conduct large-scale multi-center clinical trials. Achieving global consensus on performance standards and validation frameworks is essential to ensure that the benefits of innovative diagnostics are realized safely and effectively across the healthcare continuum.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Test Type, Service Provider, End-User & Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Quest Diagnostics, Inc., Laboratory Corporation of America, LLC, Eurofins Scientific, Fresenius Medical Care, NeoGenomics Laboratories Inc., Siemens Healthineers, OPKO Health, Inc., Abbott Laboratories, Inc., Charles River Laboratories International, Inc., Sonic Healthcare Ltd., and Genoptix, Inc. |

SEGMENTAL ANALYSIS

By Test Type Insights

The complete blood count segment dominated the market by holding 26.9% of the global market share in 2025. The status of the complete blood count segment as the most frequently ordered diagnostic panel in medicine that serves as a fundamental screening tool for a vast array of conditions, ranging from anemia and infection to leukemia, is primarily driving the dominance of the segment in the global market. The CBC provides critical data on red blood cells, white blood cells, and platelets, making it indispensable for routine checkups, preoperative assessments, and emergency triage. According to the Centers for Disease Control and Prevention, CBC testing is widely performed, reflecting its ubiquity in standard care protocols. The test is often the first line of investigation when patients present with nonspecific symptoms such as fatigue or fever, ensuring a consistent and high-volume demand across all healthcare settings. Its integration into automated hematology analyzers allows for rapid throughput with minimal manual intervention, further cementing its position as the backbone of laboratory operations worldwide.

On the other hand, the HbA1c test segment is projected to be the fastest growing within the clinical laboratory market and expand at a CAGR of 10.2% over the forecast period. Unlike fasting glucose tests, HbA1c provides a three-month average of blood sugar levels, offering a more reliable indicator of long-term glycemic control. According to the International Diabetes Federation, the global diabetic population is expected to rise, creating an immense and expanding patient pool requiring quarterly monitoring. Regulatory bodies such as the American Diabetes Association now recommend HbA1c as the primary diagnostic criterion for prediabetes and diabetes, shifting clinical practice away from traditional glucose tolerance tests. As per the World Health Organization, diabetes cases are increasing in low and middle-income countries, driving demand for affordable and accurate diagnostic solutions. Furthermore, the correlation between elevated HbA1c levels and increased risk of cardiovascular disease, kidney failure, and neuropathy underscores the necessity of regular monitoring for diagnosed patients.

By Service Provider Insights

The independent and reference laboratories held the dominant position in the clinical laboratory services market by capturing 56.1% of the global market share in 2025. These entities specialize in high-volume testing and complex assays that require specialized equipment and expertise not typically available in hospital settings. Their ability to achieve economies of scale allows them to offer competitive pricing and rapid turnaround times, which makes them the preferred partners for physician offices, insurance companies, and government health programs. According to the American Clinical Laboratory Association, independent labs perform a significant portion of outpatient diagnostic tests, highlighting their central role in the healthcare ecosystem. Their flexibility to adopt new technologies and expand test menus quickly gives them a competitive edge over slower-moving hospital departments. The shift towards outpatient care and ambulatory surgery centers further drives referrals to these specialized facilities, reinforcing their market leadership.

On the other hand, the hospital-based laboratories segment is emerging as the fastest-growing segment in terms of strategic importance and integrated care value and is estimated to record a CAGR of 8.5% over the forecast period. While independent labs lead in volume, hospital labs are experiencing renewed growth due to the critical need for rapid STAT testing in emergency and acute care settings. Hospitals are investing heavily in modernizing their lab infrastructure to support precision medicine initiatives and real-time clinical decision support systems. According to the Joint Commission, rapid turnaround times for critical values are essential, a domain where on-site hospital labs excel. Unlike independent labs that require sample transport, hospital labs are located within the facility, enabling instant communication between clinicians and laboratorians. As per the Agency for Healthcare Research and Quality, emergency department volumes have increased, further amplifying the need for robust in-house laboratory services. As hospitals strive to improve throughput and reduce length of stay, the strategic value of having a fully equipped, responsive on-site laboratory becomes undeniable.

By End-User Insights

The central laboratories segment represented the leading end-user segment in the clinical laboratory tests market by occupying 60.6% of the global market share in 2025. These large-scale facilities serve as hubs for processing samples from multiple sources, including hospitals, physicians' offices, and clinical trial sites. Their dominance is attributed to their capacity to handle high volumes of routine and specialized tests with exceptional efficiency and consistency. The centralization of testing allows for standardized quality control measures and the utilization of advanced automation technologies that smaller settings cannot afford. According to the Global Laboratory Alliance, central labs are responsible for a significant portion of esoteric and high-complexity tests, underscoring their critical role in modern diagnostics. The ability to aggregate data from diverse populations also makes them invaluable for epidemiological surveillance and public health monitoring. As healthcare networks continue to consolidate, the reliance on central laboratories for comprehensive diagnostic services is expected to remain strong, which maintains their position as the primary endpoint for clinical testing.

On the other hand, the primary clinics segment is witnessing the fastest growth as an end-user segment for clinical laboratory tests and is expected to exhibit a CAGR of 9.5% over the forecast period. The shifting of care delivery from hospitals to outpatient settings and the increasing adoption of point-of-care testing technologies are driving the expansion of the primary clinics segment in the global market. Primary care providers are becoming the frontline for chronic disease management and preventive screening, which requires greater access to diagnostic tools within their practices. According to the Centers for Disease Control and Prevention, patient encounters occur predominantly in primary care settings, creating a massive volume potential for localized testing. The convenience of obtaining results during a single visit improves patient adherence and satisfaction, fueling the demand for in-clinic testing capabilities. As value-based care models emphasize early intervention and continuous monitoring, primary clinics are expanding their diagnostic offerings, driving rapid growth in this segment.

REGIONAL ANALYSIS

North America Clinical Laboratory Tests Market Analysis

North America accounted for 40.2% of the global market share in 2025 and was the most dominating regional segment in the worldwide market. The region's dominance is anchored by the United States, which boasts the world's most advanced healthcare infrastructure, the highest per capita healthcare expenditure, and a robust culture of preventive screening. The presence of major diagnostic corporations and cutting-edge research institutions fosters the rapid adoption of innovative testing technologies. Regulatory frameworks such as CLIA ensure high-quality standards, while a well-established reimbursement system supports widespread access to diagnostic services. According to the Centers for Medicare and Medicaid Services, national health spending in the US is considerably high, with a notable portion allocated to diagnostic services. The high prevalence of chronic diseases and an aging population further drives demand for frequent laboratory monitoring. The region also leads in the integration of artificial intelligence and big data into laboratory workflows, setting global benchmarks for efficiency and accuracy. Consequently, North America remains the primary engine of innovation and revenue generation for the global clinical laboratory industry.

Europe Clinical Laboratory Tests Market Analysis

Europe was another key regional segment in the global clinical laboratory tests market in 2025 and held the second-largest share of the global market. The diverse landscapes of mature and emerging healthcare systems in Europe are propelling the European market growth. Countries like Germany, France, and the United Kingdom lead the region with well-established public health networks and high standards of diagnostic care. The European market is distinguished by strong government regulation and a focus on cost-effectiveness, which influences testing patterns and reimbursement policies. The implementation of the In Vitro Diagnostic Regulation has raised quality benchmarks, ensuring patient safety and result reliability across the continent. According to the European Commission, healthcare expenditure in the EU represents a significant portion of GDP, providing a solid foundation for diagnostic services. The region is also a hub for medical tourism and cross-border healthcare collaboration, facilitating the sharing of best practices and technologies. An aging population similar to North America drives demand for chronic disease management, while increasing awareness of preventive health fuels screening programs. Europe's commitment to sustainability and digital transformation is reshaping its laboratory landscape, positioning it as a key player in the global arena.

Asia Pacific Clinical Laboratory Tests Market Analysis

Asia Pacific is the fastest-growing region in the global clinical laboratory tests market. The region encompasses a vast array of economies, from highly developed markets in Japan and Australia to rapidly emerging ones in China and India. Rising healthcare expenditures, improving infrastructure, and increasing health awareness are transforming the diagnostic landscape. Governments in countries like China and India are implementing ambitious healthcare reforms to expand coverage and improve access to quality diagnostics for their massive populations. According to the World Bank, healthcare spending in the Asia Pacific region has grown steadily in recent years. The rising prevalence of lifestyle-related diseases such as diabetes and cardiovascular conditions is creating a surge in demand for laboratory testing. The region is also becoming a manufacturing hub for diagnostic reagents and instruments, reducing costs and enhancing availability. With a young and growing workforce coupled with a rapidly aging population in East Asia, the market dynamics are unique and full of potential.

Latin America Clinical Laboratory Tests Market Analysis

Latin America is estimated to account for a notable share of the global clinical laboratory tests market during the forecast period. Latin America is a region with significant growth potential despite current economic challenges. Brazil and Mexico are the largest markets in the region, driven by expanding private healthcare sectors and government efforts to improve public health infrastructure. The region faces disparities in access to diagnostics between urban and rural areas, but initiatives to strengthen primary care are beginning to bridge this gap. The Pan American Health Organization plays a crucial role in coordinating health policies and promoting equitable access to essential diagnostic services. According to the Inter-American Development Bank, healthcare investment in Latin America has been increasing, with a focus on combating infectious diseases and managing rising chronic conditions. The growing middle class is driving demand for private laboratory services, while public systems struggle to meet the needs of the broader population. The region is also seeing an influx of international diagnostic companies establishing operations to capture emerging opportunities. While volatility remains a concern, the long-term outlook is positive as healthcare systems mature and diagnostic penetration increases.

Middle East and Africa Clinical Laboratory Tests Market Analysis

The market in the Middle East and Africa region is expected to showcase steady growth during the forecast period. The Gulf Cooperation Council countries, particularly the UAE and Saudi Arabia, are leading the way with high investments in world-class healthcare facilities and diagnostic centers. These nations are actively diversifying their economies and prioritizing health tourism, attracting patients from across the region. In contrast, many African nations face significant challenges related to infrastructure, funding, and workforce shortages, limiting access to basic diagnostic services. The World Health Organization emphasizes the critical need to strengthen laboratory systems in Africa to combat infectious diseases and improve maternal and child health. According to the African Society for Laboratory Medicine, there is a concerted effort to build local capacity and establish regional reference labs. The market is fragmented, with a mix of high-tech private clinics in urban centers and under-resourced public facilities in rural areas. Despite these disparities, the region is witnessing gradual improvements driven by international aid, public-private partnerships, and government commitments to health sector reform.

COMPETITIVE LANDSCAPE

The competition in the clinical laboratory tests market is intense and characterized by a mix of large multinational corporations and numerous regional or independent laboratories vying for market share. Large players leverage their extensive networks and economies of scale to offer competitive pricing and broad test menus that smaller entities struggle to match. Differentiation increasingly relies on technological innovation, such as artificial intelligence integration and rapid molecular testing capabilities, rather than price alone. Regulatory compliance and quality accreditation serve as significant barriers to entry, favoring established organizations with robust infrastructure and experienced personnel. Consolidation trends continue as major companies acquire smaller niche labs to gain access to specialized expertise and local customer bases. The shift towards value-based care forces competitors to demonstrate clinical utility and cost-effectiveness in their service offerings constantly. Price pressure from government payers and private insurers remains a persistent challenge, driving efficiency improvements across the industry. This dynamic environment fosters continuous innovation in service delivery models and diagnostic technologies to maintain a competitive advantage.

KEY MARKET PARTICIPANTS

Companies playing an influential role in the global clinical laboratory tests market profiled in this report are

- Quest Diagnostics, Inc.

- Laboratory Corporation of America, LLC

- Eurofins Scientific

- Fresenius Medical Care

- NeoGenomics Laboratories Inc.

- Siemens Healthineers

- OPKO Health, Inc.

- Abbott Laboratories, Inc.

- Charles River Laboratories International, Inc.

- Sonic Healthcare Ltd.

- Genoptix, Inc.

TOP PLAYERS IN THE MARKET

- Quest Diagnostics Incorporated stands as a preeminent provider of diagnostic information services globally with an extensive network of patient service centers and laboratories. The company delivers a comprehensive portfolio of tests ranging from routine chemistry to complex genomic sequencing for physicians and health plans. Quest recently invested heavily in digital health platforms to enhance patient access to results and streamline provider workflows through advanced data analytics. Their strategic focus includes expanding esoteric testing capabilities and forming alliances with health systems to manage population health outcomes effectively. The firm actively acquires niche laboratories to broaden its specialized test menu and geographic reach. These initiatives demonstrate their commitment to leveraging scale and technology to improve diagnostic accuracy and operational efficiency across the global healthcare continuum.

- Laboratory Corporation of America Holdings operates as a leading life sciences company providing essential diagnostic services to patients and providers worldwide. The organization utilizes a vast logistics network to process millions of specimens daily, ensuring rapid turnaround times for critical test results. LabCorp recently strengthened its market position by integrating its clinical trials business with routine diagnostics to offer end-to-end solutions for pharmaceutical developers. They continue to innovate in molecular pathology and rare disease testing through internal research and strategic partnerships with biotechnology firms. The company emphasizes sustainability initiatives and workforce development to maintain high-quality standards amidst growing test volumes. Their dedication to precision medicine and data-driven insights solidifies their role as a critical partner in modern healthcare delivery and drug development ecosystems.

- Sonic Healthcare Limited functions as a major international medical laboratory services provider with a significant presence across multiple continents, including Europe and North America. The company distinguishes itself through a decentralized management model that empowers local laboratory directors to maintain strong community relationships while leveraging global scale. Sonic recently pursued an aggressive acquisition strategy to consolidate fragmented markets and expand its footprint in key growth regions. They invest substantially in automation technologies and artificial intelligence to enhance diagnostic precision and reduce operational costs. The firm focuses on delivering high-quality pathology and radiology services through a network of community-based laboratories and hospital contracts. These strategic moves reinforce their reputation for clinical excellence and operational flexibility in a highly competitive global diagnostic landscape.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the clinical laboratory tests market primarily utilize strategic acquisitions to consolidate fragmented regional markets and expand their specialized test menus rapidly. Companies invest heavily in advanced automation and robotics to increase throughput capacity while reducing manual errors and operational costs significantly. Developing proprietary digital platforms and mobile applications allows firms to enhance patient engagement and streamline result delivery for healthcare providers efficiently. Major participants form strategic alliances with pharmaceutical companies to support clinical trial logistics and companion diagnostic development for new therapies. Expanding into emerging markets through joint ventures or greenfield investments helps organizations capture growth opportunities in developing healthcare economies. Providers also focus on vertical integration by offering ancillary services such as phlebotomy and data analytics to create comprehensive diagnostic solutions. These collective strategies aim to drive volume growth, improve margins, and establish dominant positions in the evolving global diagnostics sector.

MARKET SEGMENTATION

This research report on the global dental market has been segmented and sub-segmented based on the test type, service provider, end-user, and region.

By Test Type

- Metabolic Panel Tests

- Basic Metabolic Panel (BMP)

- Complete Blood Count (CBC)

- Electrolytes Testing

- HGB/HCT Tests

- Hba1c Tests

- Renal Panel Tests

- Lipid Panel Tests

- Bun Creatinine Tests

- Liver Panel Tests

By Service Provider

- Independent and Reference Laboratories

- Hospital-Based Laboratories

By End-User

- Primary Clinics

- Central Laboratories

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What are key market segments in the global clinical laboratory tests market?

Segments include types like HbA1c tests, blood count, and genetic testing, with central laboratories holding the largest share in the global clinical laboratory tests market

2. Which regions dominate the global clinical laboratory tests market?

North America leads, driven by advanced diagnostics and high test volumes, followed by growing markets in Europe and Asia Pacific in the global clinical laboratory tests market

3. How do chronic diseases affect the global clinical laboratory tests market?

Rising chronic diseases like diabetes and cardiovascular conditions increase demand for diagnostic lab tests in the global clinical laboratory tests market

4. What role does technology play in the global clinical laboratory tests market?

Automation, molecular diagnostics, and point-of-care testing improve accuracy and efficiency, driving expansion in the global clinical laboratory tests market

5. What are major end users in the global clinical laboratory tests market?

Primary clinics, central laboratories, and hospitals are key end users fueling market growth in the global clinical laboratory tests market

6. How does aging population impact the global clinical laboratory tests market?

Aging populations require more frequent diagnostic testing, boosting demand in the global clinical laboratory tests market

7. What challenges does the global clinical laboratory tests market face?

Challenges include regulatory hurdles, high costs, and reimbursement issues that affect adoption rates in the global clinical laboratory tests market

8. How do laboratory-developed tests influence the global clinical laboratory tests market?

Laboratory-developed tests add innovation and growth with personalized diagnostics in the global clinical laboratory tests market

9. What trends are shaping the future of the global clinical laboratory tests market?

Growth is driven by personalized medicine, AI integration, and expanding use of molecular and genetic testing in the global clinical laboratory tests market

10. Which companies lead the global clinical laboratory tests market?

Key players include Quest Diagnostics, Abbott, LabCorp, and Siemens Healthineers in the global clinical laboratory tests market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com