Global Digital Camera Market Size Share, Trends, and Growth Analysis Report, Segmented By Lens Type, By End User, By Sensor Size, and By Region (North America, Europe, Asia-Pacific, Middle East & Africa, Latin America) – Industry Analysis, 2026 to 2034

Global Digital Camera Market Summary

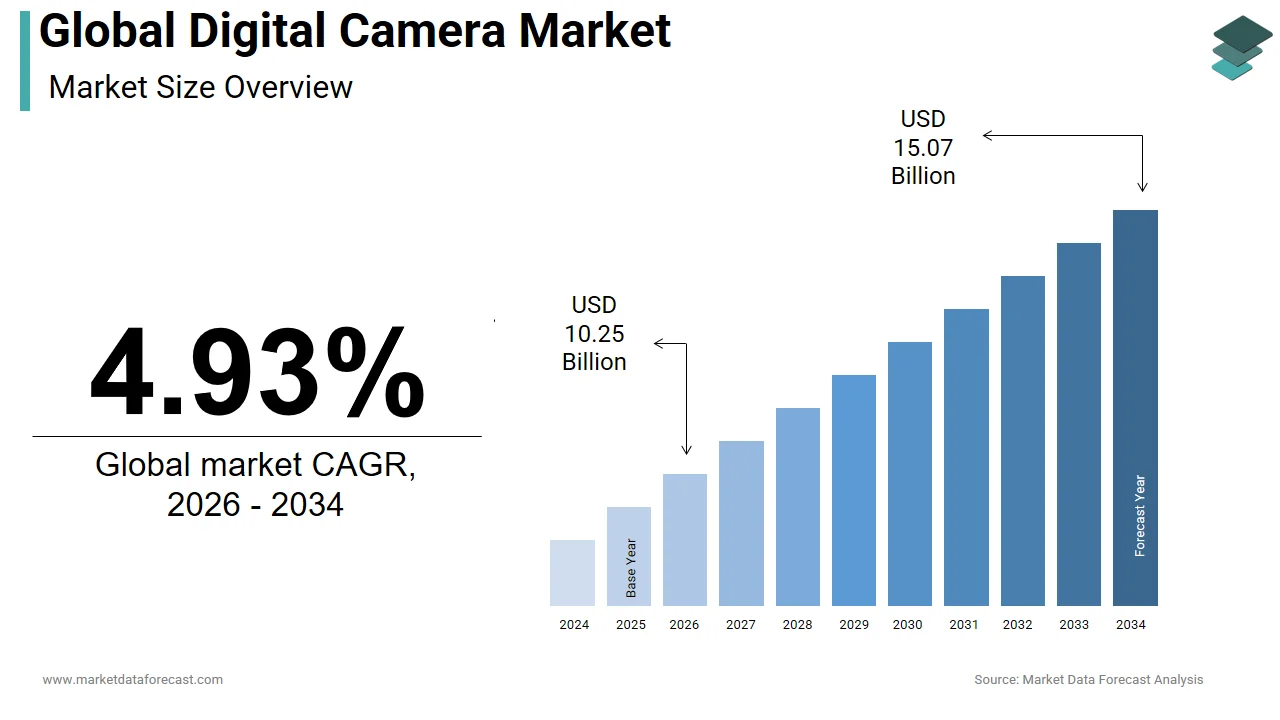

The global digital camera market was valued at USD 9.77 billion in 2025 and is estimated to reach USD 10.25 billion in 2026 and USD 15.07 billion by 2034, growing at a CAGR of 4.93% from 2026 to 2034. The growth of the digital camera market is fueled by the increasing popularity of high-quality photography and videography, the rising adoption of mirrorless cameras, and the growing demand from hobbyists, content creators, and professionals. Advancements in AI-driven imaging, 4K/8K video recording, and connectivity features are further boosting market demand.

Key Market Trends

- A rising shift from DSLRs to mirrorless cameras due to compact designs and advanced features.

- Growing demand for high-resolution imaging and video content creation across social media and streaming platforms.

- Expansion of hybrid cameras supporting both professional photography and videography.

- Increasing focus on AI-enabled cameras with real-time editing and smart features.

- Rising interest from hobbyists and amateur photographers is driving mid-range camera adoption.

Segmental Insights

- By lens type, the built-in lens segment dominated the digital camera market in 2024, supported by affordability and compactness for casual users.

- By product type, the mirrorless camera segment led with 49.5% share in 2024, driven by demand for lightweight, high-performance alternatives to DSLRs.

- By end-user, the hobbyist segment accounted for 52.6% of the market in 2024, reflecting rising consumer interest in creative photography and content creation.

Regional Insights

- Asia-Pacific was the top-performing region, capturing 47.3% share in 2024, supported by strong demand in Japan, China, and South Korea—home to major manufacturers and a large base of photography enthusiasts.

- North America is witnessing steady growth, driven by professional creators, influencers, and strong online retail penetration.

- Europe shows stable demand, with a strong presence of photography hobbyists and premium camera buyers.

- Latin America and the Middle East & Africa are emerging markets, with gradual growth driven by rising disposable incomes and interest in digital content creation.

Competitive Landscape

Key players in the global digital camera market include Canon Inc., Sony Group Corporation, Nikon Corporation, Fujifilm Holdings Corporation, and Panasonic Holdings Corporation. These companies focus on next-generation mirrorless cameras, AI-enabled imaging systems, and partnerships with content creators to expand their market presence.

Global Digital Camera Market Size

The global digital camera market was valued at USD 9.77 billion in 2025, is estimated to reach USD 10.25 billion in 2026, and is projected to reach USD 15.07 billion by 2034, growing at a CAGR of 4.93% from 2026 to 2034.

A digital camera refers to the imaging devices engineered to capture, store, and process still photographs and video using digital sensors, distinct from legacy film-based systems. While smartphones have absorbed much of the consumer photography demand, digital cameras retain irreplaceable value in professional, industrial, and niche applications requiring superior optical performance. As per study, millions of interchangeable-lens digital cameras were shipped globally, according to the study. In the realm of scientific research, digital imaging systems are integral to fields such as astronomy and medical diagnostics, where high dynamic range and low-light sensitivity are paramount. NASA’s James Webb Space Telescope, equipped with advanced digital imaging sensors, has demonstrated the important role of specialized cameras in deep-space observation. Furthermore, as per the National Institute of Standards and Technology, digital cameras with calibrated sensors are now standard in forensic documentation by ensuring evidentiary accuracy in criminal investigations.

MARKET DRIVERS

Rising Demand for High-Resolution Imaging in Cinematography and Broadcast Media

The escalating demand for high-resolution imaging in professional cinematography and broadcast media is propelling the growth of the digital camera market. The global shift toward 4K and 8K content production has intensified the need for cameras capable of capturing ultra-high-definition video with precise color fidelity and dynamic range. According to the research, a portion of prime-time television content in North America was produced in 4K resolution, up from that in 2020. Cameras have become industry standards, offering native 6K recording and logarithmic gamma profiles essential for post-production grading. In Japan, NHK Broadcasting has emphasized 8K-ready equipment for its satellite broadcasts, which is accelerating procurement across production houses. As per the study, a portion of independent filmmakers use digital cinema cameras with global shutters and high bit-depth recording to achieve cinematic quality.

Growing Integration of Digital Cameras in Industrial Automation and Machine Vision

The integration of digital cameras into industrial automation and machine vision systems, particularly in precision manufacturing and quality control, is driving the growth of the digital camera market. In semiconductor fabrication, digital cameras with micron-level resolution are deployed for wafer inspection, where even sub-micron defects can compromise chip performance. According to the study, global shipments of machine vision cameras were in millions of units, reflecting a year-on-year increase. In the automotive sector, a portion of final assembly lines in Germany utilizes camera-based systems for automated defect detection, as per the research. These systems rely on high-speed CMOS sensors capable of capturing 1,000+ frames per second, enabling real-time analysis. Apart from these, in pharmaceutical manufacturing, digital imaging ensures tablet uniformity and packaging integrity. The growing reliance on AI-driven image recognition further amplifies demand for high-performance digital cameras in industrial settings by establishing a robust non-consumer growth vector.

MARKET RESTRAINTS

Growing Substitution of Digital Cameras by Smartphone Imaging Systems

The pervasive substitution of digital cameras by smartphone imaging systems, particularly among casual and amateur users, is hampering the growth of the digital market. Modern smartphones now feature multi-lens arrays, computational photography, and AI-enhanced image processing, eroding the functional advantage once held by standalone cameras. According to the study, a portion of adults in the United States owned a smartphone, and many of them used it as their primary device for photo capture. In emerging markets like Indonesia and Nigeria, where smartphone penetration has surged, standalone camera adoption remains negligible among first-time users.

Prolonged Product Lifecycle of High-End Digital Cameras

The prolonged product lifecycle of high-end digital cameras, which dampens replacement demand and slows revenue turnover, is restraining the growth of digital camera market. Professional-grade DSLR and mirrorless models are engineered for durability, often lasting seven to ten years under rigorous use, as noted by the Professional Photographers of America. Unlike consumer electronics with annual upgrade cycles, digital cameras are capital-intensive tools with infrequent refresh rates. According to a study, a portion of professional photographers upgrade their primary camera body only after six years or more. Apart from these, backward compatibility with legacy lenses and accessories reduces the urgency for new purchases. This longevity, while beneficial for users, creates a structural challenge for manufacturers reliant on recurring sales.

MARKET OPPORTUNITIES

Expansion of Digital Cameras in Scientific Research & Space Exploration

The expansion of digital cameras within scientific research and space exploration, where extreme environmental resilience and imaging precision are non-negotiable, is likely to promote new opportunities for the digital camera market. NASA’s Perseverance rover, equipped with many cameras, exemplifies the important role of digital imaging in planetary science. Also, each camera undergoes rigorous calibration to operate in Martian conditions, where temperatures range from -125°C to 20°C. Similarly, the European Southern Observatory employs ultra-high-sensitivity digital cameras in its Very Large Telescope to capture faint celestial objects, enabling discoveries in exoplanet research. These applications demand sensors with low noise, high quantum efficiency, and radiation-hardening capabilities beyond consumer-grade devices. Therefore, the need for robust as well as mission-specific digital cameras is expected to grow as space agencies and research institutions plan more complex missions, including lunar bases and deep-space probes, opening a high-value and innovation-driven market segment.

Adoption of Digital Cameras in Drone-Based Aerial Imaging

Another emerging opportunity is the adoption of digital cameras in drone-based aerial imaging for agriculture, surveying, and disaster response. Drones equipped with multispectral and thermal digital cameras are transforming precision farming by enabling crop health monitoring through vegetation indices such as NDVI. According to the study, millions of hectares of farmland in India and Brazil were surveyed using drone-mounted cameras to optimize irrigation and pesticide use. In Japan, it deployed drones with high-resolution digital cameras to assess typhoon damage, reducing inspection time compared to ground teams. Furthermore, regulatory easing in countries has facilitated beyond-visual-line-of-sight operations by expanding deployment potential. This convergence of aerial platforms and high-fidelity imaging is creating a new frontier for digital camera applications, particularly in geospatial analytics and environmental monitoring.

MARKET CHALLENGES

Rising Complexity and Cost of Sensor Development

The escalating complexity and cost of sensor development, which limits innovation velocity and market accessibility, are challenging the growth of the digital camera market. Fabricating cutting-edge CMOS sensors, especially backside-illuminated, stacked, or global shutter variants, requires nanometer-scale precision and access to advanced semiconductor foundries. According to the study, the cost of developing a new image sensor node has risen due to tighter lithography requirements and increased design validation cycles. Sony, which supplies sensors to most premium camera brands, operates its own fabrication plants in Nagasaki and Fukushima, representing multi-billion-dollar investments. Smaller manufacturers lack the capital to compete, thereby leading to market concentration. This technological barrier stifles competition and slows the diffusion of breakthrough features such as AI-integrated sensors or event-based vision, which constrains the market’s ability to diversify and scale rapidly.

Rising Cybersecurity Threats in Networked Digital Cameras

The rising threat of cyber vulnerabilities in networked digital cameras, especially in surveillance and industrial applications, is degrading the growth of the digital camera market. Many modern digital cameras support IP connectivity, remote access, and cloud integration, making them susceptible to hacking and data breaches. According to the research, the number of IP camera systems in the United States was compromised due to weak default passwords and unpatched firmware. In a high-profile incident, a major European railway operator experienced a system-wide outage when its track-monitoring cameras were infiltrated via a known vulnerability in a third-party SDK. The proliferation of IoT-enabled cameras in smart cities and important infrastructure amplifies the risk surface. Manufacturers now face a mounting burden to implement end-to-end encryption, regular security patches, and compliance with standards such as IEC 62443, which diverts resources from pure imaging innovation to cybersecurity resilience.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Lens Type, Camera Type, End-user, Sensor Size, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, the Middle East, and Africa |

| Market Leaders Profiled | Canon Inc., Sony Group Corporation, Nikon Corporation, Fujifilm Holdings Corporation, Panasonic Holdings Corporation, and Others. |

SEGMENTAL ANALYSIS

By Lens Type Insights

The built-in lens segment dominated the digital camera market by capturing a significant share in 2025. The growth of the built-in lens segment is primarily driven by the widespread consumer preference for convenience and immediacy in image capture, particularly among non-professional users. According to the research, a portion of U.S. adults prioritize ease of use over advanced features when selecting imaging devices, strengthening demand for point-and-shoot functionality. Apart from these, built-in lens cameras are significantly more affordable, with entry-level models making them accessible in emerging markets. Their integration into surveillance systems, drones, and educational tools further amplifies demand beyond personal photography, ensuring sustained market position despite the broader decline in standalone camera sales.

The interchangeable lens segment is predicted to witness the highest CAGR of 6.3% from 2026 to 2034 due to the rising demand from professional photographers, content creators, and scientific institutions requiring optical flexibility and superior image quality. The proliferation of video-centric platforms such as YouTube and TikTok has intensified the need for cameras that support diverse lenses for shallow depth of field, telephoto reach, and macro precision. As per the research, a portion of independent filmmakers in the UK use mirrorless cameras with interchangeable lenses for narrative production.

By Camera Type Insights

The mirrorless camera segment led the digital camera market by revenue, capturing 49.5% of the global market share in 2024. The growth of the mirrorless camera segment is driven by its compact design, real-time electronic viewfinders, and superior video capabilities. Sony, Canon, and Nikon have redirected R&D investments toward mirrorless platforms. The shift is particularly pronounced in Asia. These cameras support high-speed burst shooting, advanced autofocus with AI subject tracking, and 4K/60fps video, features increasingly demanded by wedding photographers, wildlife documentarians, and broadcast crews. Apart from these, the integration of in-body image stabilization and silent shooting modes has made mirrorless systems indispensable in environments where discretion and stability are important, such as theater and courtroom photography.

The compact digital camera segment is predicted to witness the highest CAGR of 7.1% from 2026 to 2034 due to continuous technological innovation and strategic market repositioning. Manufacturers are increasingly embedding cinematic-grade features into mirrorless bodies, such as 10-bit color depth, dual gain sensors, and anamorphic lens support, attracting videographers and hybrid shooters. Fujifilm’s X-H2S, for example, supports 4K/120fps with minimal rolling shutter, a benchmark previously limited to cinema cameras. Apart from these, the rise of vlogging and live streaming has boosted demand for lightweight, high-performance systems with flip screens and robust audio inputs. Thus, mirrorless platforms are the sole focus of future innovation because major brands are phasing out DSLR production by ensuring sustained momentum.

By End User Insights

The hobbyist segment dominated the digital camera market by capturing 52.6% of the global market share in 2024. The growth of the hobbyist segment is driven by a growing subset of enthusiasts seek higher image quality, manual controls, and creative experimentation beyond computational photography. The rise of photography clubs, online communities like Flickr and 500px, and social media platforms emphasizing visual storytelling has reinvigorated interest in dedicated cameras. Affordable models like the Canon EOS M50 Mark II and Panasonic Lumix GX880 have lowered entry barriers, while features like Wi-Fi sharing and touchscreens bridge the usability gap with smartphones, making digital cameras appealing to tech-savvy hobbyists seeking both quality and engagement.

The semi-professional photographers and content creators segment is predicted to witness the highest CAGR of 8.4% from 2026 to 2034, owing to the democratization of media creation and monetization platforms. YouTube, Instagram, and Patreon have enabled individuals to generate income from visual content, necessitating equipment that exceeds smartphone capabilities. These devices offer full-frame sensors, weather sealing, and professional codecs, yet remain accessible in price and operation. In India, the number of freelance visual creators rose significantly, as per a study, with a portion purchasing dedicated cameras for client work. The convergence of affordability, performance, and digital distribution channels is fueling rapid adoption, positioning prosumers as the most dynamic force in market evolution.

REGIONAL ANALYSIS

Asia Pacific Digital Camera Market Insights

Asia Pacific was the top performer in the digital camera market in 2024 and accounted for 47.3% of the market share in 2024. Japan, as the birthplace of major manufacturers like Canon, Nikon, Sony, and Fujifilm, remains the technological nucleus of the industry. The country produced a large number of digital cameras, with a portion exported to North America and Europe, according to the study. Domestic demand is sustained by a strong culture of photography with millions of citizens participating in camera-related hobbies, as per research. China, while a major consumer electronics hub, imports high-end cameras for professional use. South Korea has emerged as a key market for premium compact cameras, which is driven by K-content creators requiring high-quality visuals for global audiences.

North America Digital Camera Market Insights

North America was positioned second in the digital camera market with 24.6% of the share in 2024. The United States was the largest contributor to the demand through professional sectors such as journalism, wildlife photography, and independent filmmaking. A notable number of professional photographers operate in the U.S., with a portion using interchangeable lens cameras as their primary tool, as per the study. The rise of content creation economies has further amplified demand, with platforms like YouTube supporting a significant number of U.S.-based creators who rely on high-performance cameras. Canada, though smaller in scale, mirrors this trend, with government grants supporting documentary and Indigenous storytelling projects that require robust imaging equipment, strengthening North America’s role as a high-value, innovation-driven market.

Europe Digital Camera Market Insights

Europe digital camera market growth is greatly influenced by the growth of Europe in the global market share is driven by its emphasis on heritage, craftsmanship, and technical excellence. Germany is an important hub for optical engineering, with Leica and Zeiss continuing to influence lens design standards worldwide. As per the research, a portion of high-end prime lenses used in Europe is manufactured domestically, supporting a culture of precision photography. France and the UK are major centers for photojournalism and fashion, with agencies like Magnum Photos and Condé Nast driving demand for durable as well as high-resolution systems. As per the study, a portion of field journalists in Western Europe now use mirrorless cameras for live reporting due to their compact size and streaming capabilities. Apart from these, the EU’s push for digital sovereignty has led to investments in domestic imaging sensor research. This blend of cultural prestige and technological investment ensures Europe’s sustained influence in premium segments.

Latin America Digital Camera Market Insights

Latin America grew steadily in the digital camera market. Brazil leads the regional market, accounting for a portion of camera imports, driven by a growing class of freelance photographers and wedding videographers. According to a study, the number of self-employed visual artists increased. Argentina and Mexico are also witnessing rising demand, particularly in documentary and social journalism, where reliable standalone cameras are essential in areas with unstable smartphone connectivity. However, high import tariffs limit affordability. Despite this, the used camera market is thriving, with several refurbished units traded annually, as per the study. Thus, Latin America is gradually transitioning from smartphone-only imaging to hybrid camera adoption, particularly among mid-tier professionals due to increasing internet penetration and digital content consumption.

Middle East and Africa Digital Camera Market Insights

The Middle East and Africa are likely to grow in the global digital camera market during the forecast period. The growth of the Middle East and Africa in the global market can be attributed to specific regional dynamics. The United Arab Emirates stands out as a regional leader with Dubai emerging as a hub for luxury and fashion photography, hosting photo shoots annually, as per the study. High disposable income and a concentration of influencers have spurred demand for premium mirrorless systems from brands like Canon and Sony. In Saudi Arabia, Vision 2030 includes investments in creative industries. South Africa, despite economic constraints, maintains the most developed photography ecosystem in sub-Saharan Africa. Wildlife photography in countries like Kenya and Tanzania also sustains niche demand for rugged, high-performance cameras. While overall penetration remains low, the region’s focus on cultural renaissance and digital content is laying the foundation for incremental but meaningful market expansion.

COMPETITIVE LANDSCAPE

The competition in the digital camera market is characterized by a concentrated yet dynamic landscape, where legacy manufacturers face pressure to innovate while defending against technological obsolescence. Sony, Canon, and Fujifilm dominate through continuous R&D investment, proprietary ecosystems, and strong brand equity among professionals and enthusiasts. However, niche players like OM System and Panasonic are gaining traction with specialized offerings in ruggedness, stabilization, and video-centric features. The battleground has shifted from hardware alone to integrated solutions that cover lenses, software, and cloud services. Differentiation is increasingly achieved through color science, ergonomics, and AI-enhanced functionalities such as eye-tracking and subject recognition. In the Asia Pacific, local preferences for compact design and aesthetic appeal influence product development, while in Western markets, durability and modularity remain paramount. As the user base narrows to prosumers and professionals, competition intensifies over ecosystem loyalty, after-sales service, and adaptability to emerging content creation trends, making innovation velocity and customer engagement important for sustained prowess.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global digital camera market include

- Canon Inc.

- Sony Group Corporation

- Nikon Corporation

- Fujifilm Holdings Corporation

- Panasonic Holdings Corporation

Top Strategies Used By Key Market Participants

Key players in the digital camera market are deploying multifaceted strategies to sustain relevance amid smartphone dominance and shifting consumer behavior. A primary approach is technological differentiation, focusing on superior sensor performance, advanced autofocus systems, and high-resolution video capabilities that smartphones cannot replicate. Companies are investing heavily in proprietary lens ecosystems to lock in users and drive accessory sales. Vertical integration, particularly in sensor manufacturing, enables control over supply chains and innovation timelines. Strategic collaborations with content platforms, broadcasters, and educational institutions enhance brand visibility and user engagement. Expansion into hybrid use cases—such as cinema, scientific imaging, and drone integration—diversifies revenue streams beyond traditional photography. Apart from these, companies are enhancing software ecosystems with AI-powered editing tools, mobile connectivity, and cloud workflows to improve user experience. Regional localization of products, marketing, and support services further strengthens market penetration, particularly in high-growth Asia Pacific economies.

Top Players in the Market

Sony Corporation

Sony has established itself as a technological pioneer in the digital camera market, particularly in the mirrorless and professional imaging segments. In the Asia Pacific region, the company leverages its Japanese heritage and R&D infrastructure to lead in sensor innovation, supplying not only its own Alpha series cameras but also image sensors to other global brands. The company has strengthened its presence through strategic collaborations with media broadcasters and film schools across India, South Korea, and Australia. Apart from these, its partnership with Japan’s NHK for 8K broadcast solutions has strengthened its role in high-end production. By integrating AI-driven autofocus and advanced heat dissipation in its latest models, Sony continues to set industry standards, strengthening its reputation for cutting-edge imaging technology across the Asia Pacific region.

Canon Inc.

Canon maintains a formidable presence in the Asia Pacific digital camera market through its extensive product range, spanning entry-level EOS M models to the professional EOS R5 and R6 series. The company operates manufacturing facilities in Taiwan and Malaysia, ensuring regional supply chain resilience and faster distribution across Southeast Asia. It also expanded its RF lens ecosystem, launching 15 new lenses in the Asia Pacific within a single year to enhance optical versatility. Canon has deepened engagement with photography communities by sponsoring events such as the Canon Photo Marathon in Singapore and Manila. Furthermore, its investment in service centers across Indonesia and Vietnam ensures robust after-sales support, strengthening customer loyalty and brand trust in a highly competitive landscape.

Fujifilm Corporation

Fujifilm has carved a distinctive niche in the Asia Pacific digital camera market by emphasizing retro design, color science, and hybrid photography-videography capabilities. The company’s X and GFX series cameras are widely adopted by creatives in Japan, South Korea, and China for their film simulation modes and compact form factors. The company has strengthened its regional footprint through the Fujifilm Imaging Square network in Tokyo, Shanghai, and Bangkok, spaces offering workshops, exhibitions, and hands-on trials. It also introduced localized firmware updates with multilingual interfaces tailored for Southeast Asian markets. By blending analog aesthetics with digital precision and fostering creative communities, Fujifilm has cultivated a loyal user base that values both performance and artistic expression.

MARKET SEGMENTATION

This global digital camera market research report is segmented and sub-segmented into the following categories.

By Lens Type

- Built-in

- Interchangeable

By Camera Type

- Compact Digital Camera

- DSLR (Digital Single-Lens Reflex)

- Mirrorless

- Action / 360°

By End User

- Professional Photographers

- Prosumers / Enthusiasts

- Hobbyists

- Content-Creators / Streamers

By Sensor Size

- Medium Format

- Full-Frame

- APS-C

- Micro Four-Thirds and Smaller

By Region

- North America

- Europe

- Asia-Pacific

- Middle East Africa

- Latin America

Frequently Asked Questions

1. What is the Digital Camera Market?

The Digital Camera Market covers manufacturing, sales, and innovation in cameras designed to capture digital images and video for consumers, professionals, and enterprise uses worldwide.

2. Who are the leading companies in the Digital Camera Market?

Canon, Nikon, Sony, Fujifilm, Panasonic, Leica, and Hasselblad dominate the global digital camera market, supported by a range of specialty brands

3. What are the main growth drivers in the Digital Camera Market?

Drivers include rising demand for high-quality image and video capture, growth of content creators and influencers, image sensor innovation, new features for vlogging and streaming, and Asia-Pacific’s expanding consumer base

4. How is the rise of smartphones impacting the Digital Camera Market?

Smartphones remain a major substitute, capturing the casual and entry-level market, but professionals and enthusiasts continue to drive demand for specialized digital cameras

5. Which camera type is growing fastest in the Digital Camera Market?

Mirrorless cameras are the fastest-growing segment, surpassing DSLRs due to compact design, advanced autofocus, and video features, with a market-leading share heading to 2030

6. How do social media and content creation shape the Digital Camera Market?

Social media and the creator economy are increasing demand for hybrid cameras with high-quality photo and video capabilities, boosting sales among influencers and aspiring professionals

7. What are the key technology trends in the Digital Camera Market?

AI-powered autofocus, high-frame-rate video, superior low-light performance, and integrated Wi-Fi/Bluetooth connectivity are major trends

8. Which regions drive the most growth in the Digital Camera Market?

Asia Pacific leads with strong consumer and tourism-driven demand, followed by North America and Europe, all supported by established photography cultures

9. How big is the action camera market within the Digital Camera Market?

Action cameras, such as those supporting 4K and 360-degree capture, continue to grow, serving sports, adventure, and influencer communities

10. How important are accessories in the Digital Camera Market?

Accessories such as lenses, tripods, flashes, bags, and memory cards—represent a significant revenue stream and support product differentiation and consumer loyalty

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com