Global Digital PCR and qPCR Market Size, Share, Trends & Growth Forecast Report By Product (Consumables & Reagents and Instruments), Technology (Quantitative PCR and Digital PCR), Application (Tumors, Blood Testing, Pathogen Detection and Research & Forensics), End-User and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Market Size, 2025

$5.15 BnMarket Estimate, 2026

$5.61 BnMarket Forecast, 2034

$11.15 BnCAGR, 2026–2034

8.96%Global Digital PCR and qPCR Market Report Summary

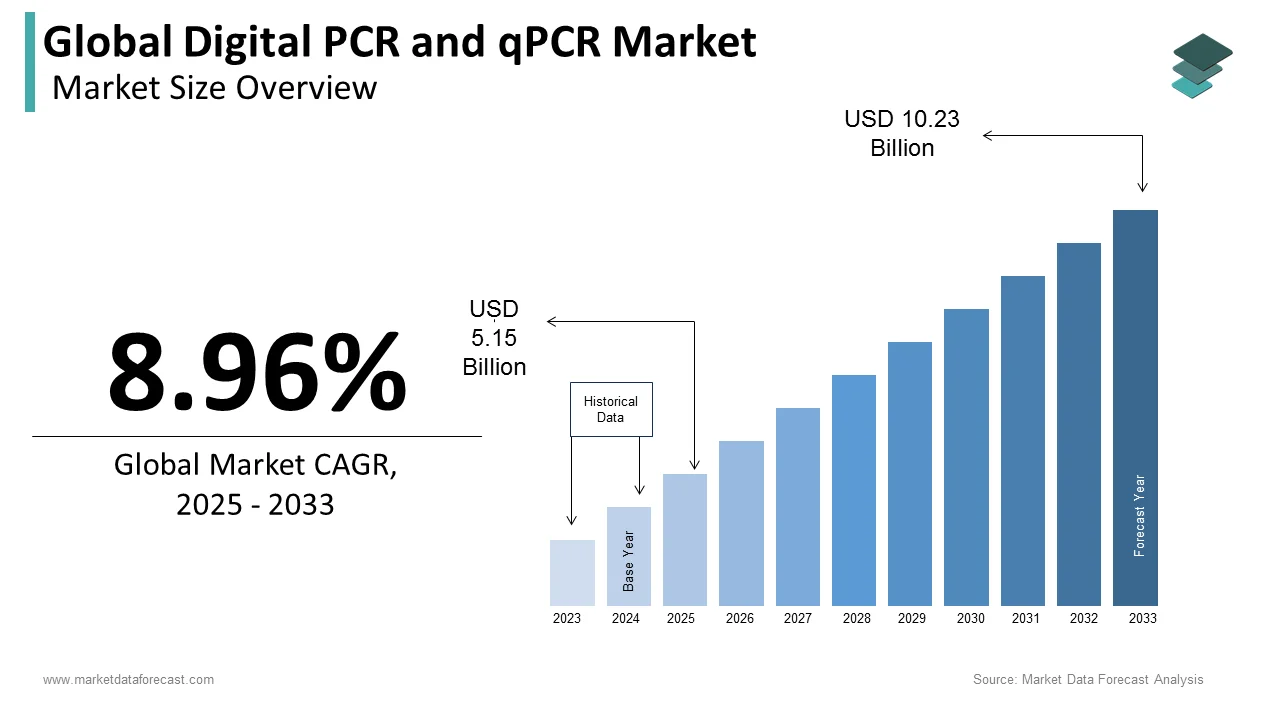

The global digital PCR and qPCR market was valued at USD 5.15 billion in 2025, is estimated to reach USD 5.61 billion in 2026, and is projected to reach USD 11.15 billion by 2034, growing at a CAGR of 8.96% from 2026 to 2034. Market growth is driven by the increasing demand for precise and sensitive molecular diagnostics, rising adoption in clinical research, and expanding applications in infectious disease detection, oncology, and genetic analysis. The growing emphasis on personalized medicine and advancements in genomic technologies are further accelerating market expansion. Additionally, increased funding for life sciences research and improvements in laboratory automation are supporting widespread adoption globally.

Key Market Trends

- Rising demand for high-precision molecular diagnostic techniques.

- Increasing adoption in oncology, infectious disease testing, and genetic analysis.

- Growth in personalized medicine and genomics research.

- Advancements in automation and high-throughput PCR technologies.

- Expansion of research and forensic applications.

Segmental Insights

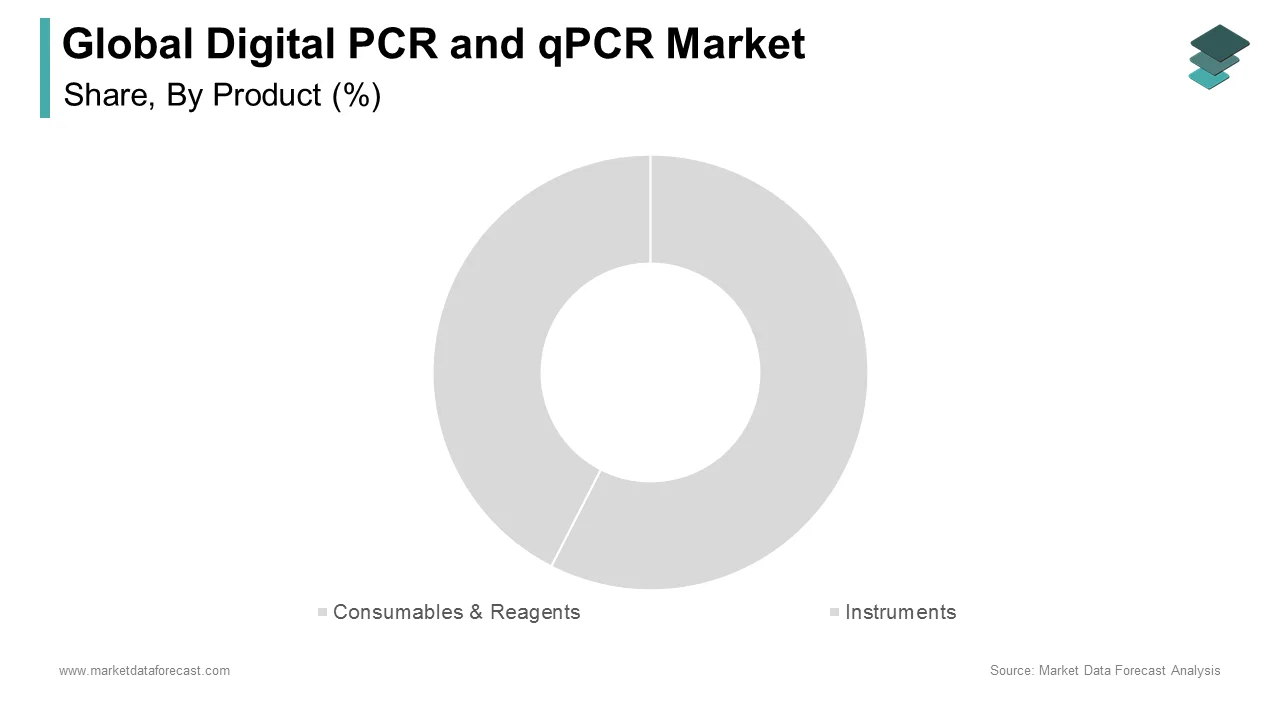

- Based on product, the consumables and reagents segment dominated the global digital PCR and qPCR market by capturing 61.2% share in 2025, driven by recurring usage in testing procedures.

- Based on technology, the quantitative PCR (qPCR) segment led the market with 71.6% share in 2025, supported by its widespread adoption and established protocols.

- Based on application, the research and forensics segment held the largest share of 46.2% in 2025, driven by extensive use in academic and investigative settings.

- Based on end user, the pharmaceutical and biotechnology firms segment dominated the market with 37.4% share in 2025, supported by growing R&D activities.

Regional Insights

The global digital PCR and qPCR market is witnessing steady growth across major regions due to advancements in molecular diagnostics and research infrastructure.

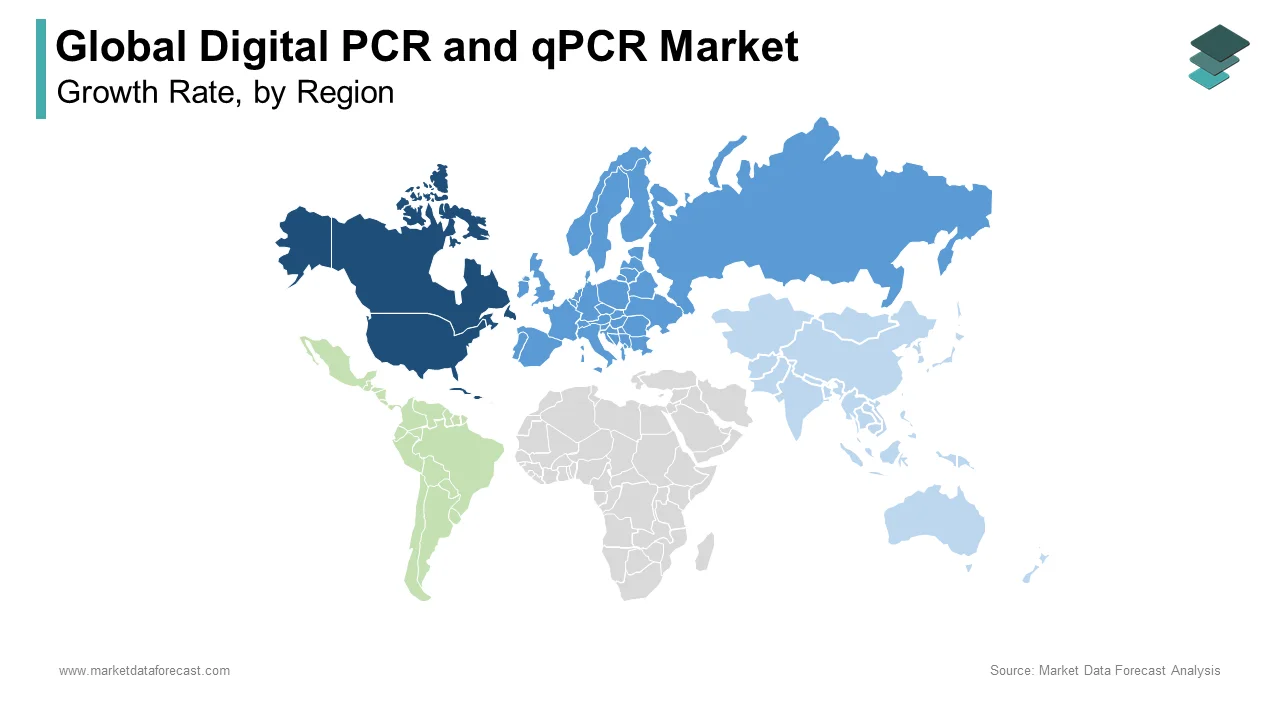

- North America led the market in 2025 with 40.9% share, supported by strong research funding and advanced healthcare systems.

- Europe followed as the second-largest market, driven by government support for life sciences research and strong clinical adoption.

- Asia-Pacific is emerging as the fastest-growing region due to rapid economic development, increasing healthcare investments, and expanding research capabilities.

Competitive Landscape

The global digital PCR and qPCR market is highly competitive, with major biotechnology and diagnostics companies focusing on innovation, product development, and expanding their global presence. Companies are investing in advanced PCR platforms, automation, and integrated solutions to enhance efficiency and accuracy.

Prominent companies operating in the global digital PCR and qPCR market include Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd., Bio-Rad Laboratories, QIAGEN N.V., Taraka Bio Inc., Affymetrix Inc., Agilent Technologies Inc., Fluidigm Corporation, Danaher Corporation, and Becton & Dickinson Company.

Global Digital PCR and qPCR Market Size

The size of the global digital PCR and qPCR market was worth USD 5.15 billion in 2025. The global market is anticipated to grow at a CAGR of 8.96% from 2026 to 2034 and be worth USD 11.15 billion by 2034 from USD 5.61 billion in 2026.

Digital PCR and qPCR encompass two distinct yet complementary nucleic acid quantification technologies that serve as the backbone of modern molecular diagnostics, genomics research, and biopharmaceutical development. Quantitative Polymerase Chain Reaction (qPCR) measures DNA amplification in real time using fluorescent probes to determine relative or absolute quantities, while Digital PCR (dPCR) partitions samples into thousands of individual reactions to provide absolute quantification without the need for standard curves. As of 2026, these technologies are indispensable for detecting low-abundance mutations, monitoring viral loads, and ensuring the quality of gene therapies. The global urgency for precise genetic analysis is underscored by the identification of thousands of rare diseases, with the majority having a genetic origin according to the National Organization for Rare Disorders. As per the World Health Organization, accurate viral load monitoring is critical for managing conditions such as HIV and Hepatitis C, which affect millions worldwide and require regular testing to prevent disease progression. The rise of liquid biopsy techniques, which depend on the sensitivity of digital PCR to detect circulating tumor DNA, has further elevated the clinical relevance of these platforms. With the Human Genome Project highlighting that genetic variations contribute to differences in drug response, the demand for high-precision quantification tools continues to surge across academic, clinical, and industrial sectors, driving innovation in partitioning methods and fluorescence detection systems.

MARKET DRIVERS

Surging Demand for Precision Oncology and Liquid Biopsy Applications

The escalating adoption of precision oncology and liquid biopsy technologies is a key driver of the expansion of the Digital PCR and qPCR market. Clinicians increasingly rely on these platforms to detect minute quantities of circulating tumor DNA in blood samples, enabling early cancer diagnosis and real-time monitoring of treatment efficacy without invasive tissue biopsies. According to the American Cancer Society, millions of new cancer cases are diagnosed annually in the United States, creating a massive patient population requiring molecular profiling. Digital PCR offers superior sensitivity compared to traditional sequencing, which is crucial for identifying resistance mutations during therapy. As per Nature Medicine, liquid biopsy-guided treatment decisions have demonstrated improved patient survival outcomes in advanced lung cancer cases. The ability to monitor minimal residual disease after surgery allows oncologists to tailor adjuvant therapies more effectively. With insurance coverage for molecular diagnostics expanding and guidelines from organizations such as the National Comprehensive Cancer Network recommending genomic testing, the volume of samples processed through these platforms continues to grow, solidifying their role as essential tools in cancer care.

Expansion of Infectious Disease Surveillance and Pathogen Detection

The persistent threat of emerging infectious diseases and the need for robust pathogen surveillance significantly propel the growth of the Digital PCR and qPCR market. These methods remain the gold standard for diagnosing viral, bacterial, and fungal infections due to their rapid turnaround time and high specificity. According to the Centers for Disease Control and Prevention, millions of foodborne illnesses occur annually in the United States, many requiring precise molecular identification to track outbreak sources and prevent spread. The global response to pandemics has established a permanent infrastructure for high-throughput nucleic acid testing, with laboratories worldwide maintaining elevated capacity for respiratory virus detection. As per the World Health Organization, antimicrobial resistance is responsible for a significant number of deaths each year, which requires rapid molecular tests to distinguish between resistant and susceptible strains for appropriate antibiotic stewardship. Digital PCR is particularly valuable for quantifying low-level viral loads in asymptomatic carriers or monitoring the efficacy of antiviral treatments in chronic infections. Governments are investing heavily in national reference laboratories equipped with advanced qPCR systems to enhance biosecurity and preparedness. The integration of these technologies into routine workflows for sexually transmitted infections and respiratory panels ensures steady demand driven by public health imperatives and the continuous emergence of novel pathogens.

MARKET RESTRAINTS

High Capital Expenditure and Operational Costs Limit Accessibility

The substantial financial burden associated with acquiring and operating Digital PCR and advanced qPCR systems remains a significant restraint for the Digital PCR and qPCR market growth. A single high-end dPCR instrument can cost tens of thousands of dollars, while proprietary consumables such as chips, droplet generators, and specialized reagents add recurring expenses that strain laboratory budgets. According to the Association of Public Health Laboratories, many state and local public health laboratories report insufficient funding to upgrade to digital PCR technologies, which is forcing reliance on less sensitive conventional methods. The cost per sample for dPCR is often several times higher than standard qPCR, making it prohibitive for large-scale screening programs or routine clinical use. Additionally, the requirement for specialized training to operate these complex instruments and interpret data adds to operational overhead. Smaller academic labs and clinics in low-income countries frequently lack the infrastructure to support these platforms, creating disparities in access to advanced molecular diagnostics. Until manufacturers develop more affordable entry-level systems and reduce consumable costs through competition or generic alternatives, high capital and operational expenditures will continue to restrain market penetration.

Technical Complexity and Lack of Standardized Protocols

The inherent technical complexity of Digital PCR and the absence of universally standardized protocols are further hindering the global market expansion. Unlike qPCR, which has well-established guidelines for data analysis and normalization, dPCR requires a sophisticated understanding of partitioning statistics, Poisson distribution corrections, and threshold setting, which can vary significantly between platforms and operators. As noted by the Clinical and Laboratory Standards Institute, the lack of harmonized reference materials and inter-laboratory validation standards leads to inconsistent results when comparing data across different instruments or facilities. This variability complicates the regulatory approval process for diagnostic assays, as agencies require rigorous demonstration of reproducibility and accuracy that is difficult to achieve without standardized workflows. The steep learning curve for laboratory personnel often results in prolonged implementation times and potential errors in data interpretation. Furthermore, the diversity of chemistries and partitioning methods offered by different vendors creates fragmentation, making it challenging to establish universal best practices. Until industry consortia and regulatory bodies develop and enforce comprehensive standards for assay design, execution, and data reporting, technical hurdles will hinder broader acceptance of dPCR in critical diagnostic applications.

MARKET OPPORTUNITIES

Integration of Microfluidics and Lab-on-a-Chip Technologies

The convergence of Digital PCR with advanced microfluidics and lab-on-a-chip technologies presents a promising opportunity for the Digital PCR and qPCR market. By integrating sample preparation, partitioning, amplification, and detection onto a single disposable cartridge, manufacturers can create portable, point-of-care devices that eliminate the need for bulky laboratory infrastructure. Microfluidic dPCR systems can significantly reduce reagent consumption while maintaining high sensitivity, lowering the cost per test. This miniaturization enables deployment in remote clinics, field settings, and developing regions where centralized laboratories are unavailable. The ability to perform absolute quantification at the bedside or in resource-limited environments opens new markets for infectious disease monitoring and environmental testing. Companies are increasingly focusing on developing automated, user-friendly platforms that require minimal hands-on time, making them accessible to non-specialist operators. The global push towards decentralized healthcare models supports the adoption of these compact devices, with demand for mobile diagnostic solutions expected to rise. As fabrication costs for microfluidic chips decrease and production scales up, these integrated systems are poised to revolutionize nucleic acid testing by bringing laboratory-grade precision to the point of need.

Advancement of Gene Therapy and Cell Therapy Quality Control

The rapid expansion of the gene therapy and cell therapy sectors offers a lucrative opportunity for the Digital PCR and qPCR market, as these advanced treatments require rigorous quality control and potency testing. Manufacturing processes for CAR-T cells and viral vector-based gene therapies demand precise quantification of vector copy numbers, transgene expression levels, and residual host cell DNA to ensure safety and efficacy. According to the Alliance for Regenerative Medicine, there are currently hundreds of active gene and cell therapy clinical trials worldwide, which is driving the need for highly sensitive analytical tools that can detect rare events and low-abundance contaminants. Digital PCR is uniquely suited for this application due to its ability to provide absolute quantification without standard curves, which is critical for meeting strict regulatory release criteria. The complexity of these biologics necessitates multiple testing points throughout the production workflow, from raw material screening to final product characterization. As more therapies receive regulatory approval and transition to commercial-scale manufacturing, the volume of required QC tests will surge. Pharmaceutical companies are investing heavily in establishing robust analytical pipelines utilizing dPCR to support their production lines. This trend creates sustained demand for specialized assays and high-throughput instruments tailored to the unique requirements of the regenerative medicine industry.

MARKET CHALLENGES

Proliferation of Inhibitors in Complex Biological Samples

A significant challenge facing the Digital PCR and qPCR market is the presence of PCR inhibitors in complex biological samples, which can compromise assay sensitivity and accuracy. Samples such as whole blood, soil, feces, and food matrices often contain substances that interfere with polymerase activity and fluorescence detection. As per the Journal of Molecular Diagnostics, inhibitor-induced false negatives remain a concern if not properly addressed through extensive purification steps. While dPCR is generally more tolerant to inhibitors than qPCR due to the dilution effect during partitioning, high concentrations can still lead to partition failure and inaccurate quantification. The necessity for rigorous sample preparation increases turnaround time, labor costs, and the risk of sample loss or contamination. Developing robust extraction protocols that effectively remove inhibitors while preserving nucleic acid integrity remains a technical hurdle, particularly for point-of-care applications where simplified workflows are desired. Manufacturers are striving to engineer inhibitor-resistant polymerases and master mixes, but no universal solution exists for all sample types. Until more effective and streamlined sample preparation technologies are widely adopted, the impact of inhibitors will continue to limit the reliability and applicability of these quantification methods in diverse real-world scenarios.

Data Analysis Bottlenecks and Interpretation Variability

The increasing volume of data generated by high-throughput Digital PCR and multiplex qPCR systems is further challenging the expansion of the Digital PCR and qPCR market. Modern dPCR instruments can generate tens of thousands of data points per run, requiring sophisticated software algorithms to accurately distinguish positive partitions from noise and calculate absolute concentrations. According to the Association for Biomolecular Resource Facilities, many users report difficulties in selecting appropriate thresholds and handling edge cases where signal separation is poor, leading to subjective interpretation and inter-operator variability. The lack of intuitive, automated analysis tools forces laboratories to rely on manual review or custom scripts, slowing workflow and increasing the potential for human error. Furthermore, integrating this data into existing Laboratory Information Systems often requires complex customization due to incompatible file formats and data structures. As assays become more multiplexed to detect multiple targets simultaneously, computational complexity increases exponentially. Without standardized, AI-driven analysis platforms that can automatically validate data quality and provide clear, actionable results, the full potential of these high-density technologies may remain underutilized, which is hindering their transition from research tools to routine clinical diagnostics.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Technology, Application, End-User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Thermo Fisher Scientific Inc., F Hoffman-La Roche Ltd., Bio-Rad Laboratories, Qiagen N.V., Taraka Bio Inc., Affymetrix Inc., Agilent Technologies Inc., Fluidigm Corporation, Danaher Corporation, and Becton & Dickson Company. |

SEGMENTAL ANALYSIS

By Product Insights

The consumables and reagents segment dominated the global Digital PCR and qPCR market by capturing 61.2% of the global market share in 2025. The growth of the consumables and reagents segment in the global market is driven by the recurring nature of purchases required for every single experiment, creating a steady revenue stream that far exceeds the one-time capital expenditure of instruments. The operational model of PCR technologies that necessitates continuous purchases of enzymes, primers, probes, and master mixes for every test conducted is further boosting the dominance of the consumables and reagents segment in the worldwide market. Unlike instruments that last several years, reagents are single-use items that deplete rapidly in high-throughput environments such as diagnostic laboratories and pharmaceutical quality control units. According to the Association of Biomolecular Resource Facilities, mid-sized research laboratories consume large volumes of reactions monthly, translating to substantial recurring expenditures on proprietary chemistries. The shift towards multiplexing, where multiple targets are detected simultaneously in a single well, further increases the complexity and cost of reagent kits, boosting segment value. Additionally, liquid biopsy applications require highly specialized fluorescent probes that command premium pricing compared to standard dyes. As global molecular testing volumes surge due to infectious disease surveillance and cancer screening programs, aggregate demand for these disposable components grows rapidly. Manufacturers often employ a razor-and-blade business strategy, selling instruments competitively to lock customers into proprietary ecosystems of high-margin consumables, ensuring this segment remains the financial backbone of the industry.

However, the instruments segment is projected to register the highest CAGR of 14.1% over the forecast period owing to the urgent need for laboratories worldwide to upgrade legacy equipment to next-generation digital PCR systems capable of absolute quantification and higher sensitivity. The obsolescence of traditional qPCR machines and the subsequent wave of upgrades to digital PCR platforms across clinical and industrial settings is further propelling the expansion of the instruments segment in the global market. Laboratories are increasingly replacing older thermal cyclers with advanced digital systems that offer superior precision for detecting minimal residual disease and rare genetic variants, which are critical for personalized medicine. According to the College of American Pathologists, a significant portion of clinical laboratories plan to acquire new molecular instrumentation within the next two years to meet evolving accreditation standards. The transition from relative quantification to absolute quantification provided by digital PCR eliminates the need for standard curves, streamlining workflows and reducing variability. Government initiatives to strengthen biosecurity and pandemic preparedness have also led to funding allocations for upgrading public health laboratory infrastructure with high-throughput instruments. The emergence of compact benchtop digital PCR devices has lowered the barrier to entry for smaller clinics, expanding the total addressable market beyond large reference labs. As the clinical utility of precise nucleic acid measurement becomes undeniable, the replacement cycle for instrumentation accelerates, which is driving double-digit growth in this hardware segment.

By Technology Insights

The quantitative PCR technology segment led the market by holding 71.6% of the global market share in 2025. The supremacy of the qPCR segment in the European market can be credited to its status as the established gold standard for routine diagnostics, offering a proven balance of speed, cost-effectiveness, and reliability for a wide range of applications. The universal acceptance of qPCR as the gold standard for routine diagnostics and infectious disease surveillance, which is reinforced by decades of validation and regulatory approval, is further fuelling the dominance of the qPCR segment in this market. Health agencies worldwide rely on qPCR protocols for detecting pathogens such as influenza, HIV, and SARS-CoV-2 because the methodology is well-understood, robust, and supported by an extensive library of published assays. According to the World Health Organization, most molecular diagnostic tests authorized for emergency use utilize qPCR technology, cementing its role in global health security. The technology offers rapid turnaround times, often delivering results within hours, which is critical for acute care settings and outbreak management. Furthermore, the widespread availability of trained personnel familiar with qPCR workflows reduces implementation barriers. The cost per test for qPCR remains significantly lower than digital PCR, making it the economically viable choice for high-volume screening programs. The extensive installed base of qPCR instruments ensures continuous demand for compatible assays and services. Until digital PCR achieves similar levels of standardization and cost parity, qPCR will remain the workhorse of molecular biology, sustaining its overwhelming market share through sheer testing volume.

On the other hand, the digital PCR technology segment is anticipated to grow at the fastest CAGR of 16.2% over the forecast period, owing to its unique ability to provide absolute quantification without standards, addressing critical limitations of qPCR in detecting rare events and low-abundance targets. The unmatched sensitivity and precision of digital PCR in detecting rare mutations and low-abundance targets that are essential for liquid biopsy and precision oncology applications are also aiding the expansion of dPCR segment in the global market. Unlike qPCR, which relies on relative quantification, dPCR partitions samples into thousands of reactions to count target molecules directly, enabling the detection of mutations at extremely low frequencies. According to the Journal of Clinical Oncology, dPCR has identified resistance mutations in circulating tumor DNA that were missed by standard sequencing and qPCR, which is leading to timely treatment adjustments. This capability is crucial for monitoring minimal residual disease and early cancer recurrence, driving adoption in advanced cancer centers. The growing emphasis on non-invasive diagnostics encourages clinicians to replace tissue biopsies with blood-based tests, a shift that heavily favors dPCR technology. As evidence mounts regarding the clinical utility of ultra-sensitive detection for guiding therapeutic decisions, insurance reimbursement policies are evolving to cover these advanced tests. The inability of qPCR to match this level of precision ensures that dPCR becomes the preferred technology for high-stakes clinical applications, propelling its rapid market penetration.

By Application Insights

The research and forensics segment commanded the dominant share of 46.2% of the global market in 2025 due to the foundational role of PCR technologies in academic discovery, genetic profiling, and criminal investigation. The dominance of this segment is also attributable to the ubiquitous use of PCR technologies as fundamental tools in academic discovery and large-scale genomic studies. Virtually every molecular biology laboratory globally utilizes qPCR and increasingly dPCR for gene expression profiling, genotyping, and validating sequencing results. According to the National Science Foundation, federal funding for life sciences research in the United States alone amounts to billions annually, with a significant portion allocated to nucleic acid analysis. Genome projects and microbiome exploration require massive amounts of quantitative data that PCR provides efficiently. In forensics, PCR remains the cornerstone of DNA profiling, enabling identification from minute biological traces found at crime scenes. As per the Federal Bureau of Investigation, millions of DNA profiles are stored in national databases, all generated using PCR-based methods. The continuous publication of research papers requiring PCR validation ensures constant demand. Furthermore, CRISPR gene editing technologies rely heavily on PCR for verifying edit efficiency and off-target effects. This deep integration into scientific workflows secures the segment’s leading position.

On the other hand, the tumors segment is on the rise and is projected to experience the highest CAGR of 17.75 over the forecast period due to the paradigm shift towards precision oncology. The global move towards precision oncology, where treatment decisions are increasingly based on the genetic makeup of tumors, is further propelling the growth of the tumors segment in this global market. Oncologists routinely order molecular tests to identify actionable mutations such as EGFR, KRAS, and BRAF to prescribe targeted therapies. According to the American Society of Clinical Oncology, the number of FDA-approved targeted cancer drugs has increased significantly in recent years, each requiring companion diagnostic tests often based on PCR. Liquid biopsy applications, which use PCR to detect circulating tumor DNA, allow real-time monitoring of tumor burden and resistance mechanisms without invasive procedures. This capability is revolutionizing clinical trial designs by enabling faster assessment of drug efficacy. As per the World Health Organization, cancer incidence is projected to rise substantially by 2040, creating a massive patient population requiring molecular profiling. With healthcare systems prioritizing personalized treatment plans, demand for high-sensitivity PCR applications in oncology will accelerate rapidly.

By End User Insights

The pharmaceutical and biotechnological firms segment led the market by holding 37.4% of the worldwide market share in 2025 due to the intensive use of PCR technologies throughout drug discovery, development, and manufacturing, particularly for biologics and gene therapies. The PCR’s integral role in every stage of drug discovery and development, from target validation to clinical trial support, is further supporting the expansion of the pharmaceutical and biotechnological firms segment in the global market. Researchers rely on qPCR and dPCR to quantify gene expression changes, validate genetic targets, and assess pharmacodynamics in preclinical models. According to the Pharmaceutical Research and Manufacturers of America, the average cost to bring a new drug to market exceeds billions, with a significant portion allocated to molecular analytics and biomarker discovery. The rise of biologics and cell-based therapies has intensified demand, as these complex molecules require rigorous characterization of genetic stability and copy number variation. PCR is also essential for patient stratification in clinical trials to ensure enrolment of individuals with specific genetic markers. The need for rapid, high-throughput screening accelerates reagent and instrument consumption. As the industry shifts towards modalities like mRNA vaccines and gene editing, dependency on precise nucleic acid quantification grows and ensures pharma and biotech firms remain the largest end-user group.

However, the hospitals segment is anticipated to grow at the fastest CAGR of 15.5% over the forecast period in the global market due to the integration of molecular diagnostics into routine clinical care. The paradigm shift of integrating molecular diagnostics directly into clinical care pathways that enable faster diagnosis and treatment initiation is further contributing to the expansion of the hospitals segment in the global market. Hospitals are increasingly establishing in-house molecular labs to reduce turnaround times for critical tests such as sepsis panels, respiratory virus detection, and oncology biomarkers. According to the Centers for Medicare and Medicaid Services, reimbursement policies increasingly favor rapid molecular tests that support immediate clinical decision-making, encouraging hospitals to invest in onboard PCR capabilities. Diagnosing infections within hours rather than days allows precise antibiotic stewardship, reducing resistant organisms and healthcare costs. The COVID-19 pandemic accelerated this trend, leaving hospitals with upgraded infrastructure and expertise in molecular testing now applied to broader conditions. Compact PCR systems deployed in emergency departments and ICUs facilitate true point-of-care testing. As clinical guidelines emphasize rapid genetic profiling for personalized medicine, hospitals are compelled to expand molecular portfolios, driving significant capital and consumable spending and propelling fast growth in this segment.

REGIONAL ANALYSIS

North America Digital PCR and qPCR Market Analysis

North America dominated the digital PCR and qPCR market in 2025 by holding 40.9% of the global market share. The United States anchors this dominance with its advanced healthcare infrastructure, highest R&D expenditure, and robust regulatory framework supporting molecular diagnostics. Major players such as Thermo Fisher Scientific, Bio-Rad, and Agilent Technologies drive rapid innovation and product launches. According to the National Institutes of Health, over 45 billion USD is invested annually in biomedical research, much of which funds projects utilizing PCR technologies. Precision medicine initiatives, including the All of Us Research Program, have created massive demand for high-sensitivity genomic tools. The high prevalence of cancer and chronic diseases necessitates extensive molecular testing, while favorable reimbursement policies encourage adoption of state-of-the-art platforms. Strong collaboration between academia, industry, and regulators ensures swift translation of research into commercial applications, securing North America’s role as the primary revenue generator and innovation hub.

Europe Digital PCR and qPCR Market Analysis

Europe held the second-largest position in the global market in 2025 due to the strong government support for life sciences research and a well-established network of university hospitals driving clinical adoption. Coordinated initiatives like Horizon Europe allocate billions in funding for health research and diagnostics. Germany, France, and the UK are key contributors, hosting world-class pharmaceutical companies and research institutions. According to Eurostat, the EU invested over 90 billion EUR in research and innovation in 2025, with a significant focus on genomics and personalized medicine. The implementation of the In Vitro Diagnostic Regulation has raised quality standards, prompting laboratories to upgrade to precise digital PCR systems. Rising infectious disease burdens and aging populations sustain demand for diagnostics. Cross-border collaborations and reference labs for rare diseases further stimulate growth. Europe’s emphasis on data privacy and ethical research practices also shapes compliant molecular solutions, solidifying its position as a key market player.

Asia Pacific Digital PCR and qPCR Market Analysis

Asia Pacific is emerging as a dynamic growth engine in the global digital PCR and qPCR market and showing the highest potential for expansion. Rapid economic development, increasing healthcare expenditure, and aggressive government investments in biotechnology drive this rise. China’s 14th Five-Year Plan prioritizes genomics, aiming for global leadership in life sciences by 2030. Government funding for biomedical research has grown steadily, directly benefiting PCR adoption. Japan remains a hub for innovation, with its aging population driving urgent demand for advanced diagnostics. India and China’s contract research organizations provide cost-effective solutions for global pharma, boosting reagent consumption. Rising awareness of preventive healthcare and expanding hospital infrastructure in emerging economies further contribute to growth. Local manufacturing of PCR components reduces dependency on imports, lowering costs and enhancing accessibility. These factors position Asia Pacific as a critical frontier for the global PCR market.

Latin America Digital PCR and qPCR Market Analysis

Latin America holds a modest but growing share of the global market. The improvements in healthcare infrastructure and increasing research activities in Brazil, Mexico, and Argentina are propelling the Latin American digital PCR and qPCR market expansion. The region is transitioning from basic research to advanced molecular applications, supported by government modernization initiatives. Brazil’s Ministry of Health has launched programs to enhance public laboratory capacity, including advanced diagnostic equipment for infectious disease surveillance. According to the Pan American Health Organization, healthcare spending in Latin America has grown steadily, facilitating the adoption of new technologies. The high prevalence of viral diseases such as Dengue, Zika, and HIV creates strong demand for accurate molecular testing. Academic institutions are collaborating internationally to access cutting-edge PCR technologies. While economic volatility and limited reimbursement policies pose challenges, growing awareness of early diagnosis benefits and an expanding biotech sector foster a conducive environment for gradual market growth.

Middle East and Africa Digital PCR and qPCR Market Analysis

The Middle East and African digital PCR and qPCR market is anticipated to record steady growth during the forecast period due to the strategic diversification and healthcare improvements. Gulf Cooperation Council countries, particularly Saudi Arabia and the UAE, are investing heavily in healthcare infrastructure and research as part of their Vision 2030 agendas. Billions are being allocated to build medical cities and research centers equipped with advanced PCR technologies. The rising prevalence of genetic disorders and diabetes necessitates advanced diagnostics, spurring demand. South Africa serves as a key hub for infectious disease genomics, supported by international grants. The World Bank notes that healthcare investment in the region has increased, though baseline levels remain low compared to other regions. Challenges such as a limited-skilled workforce and infrastructure gaps persist, but initiatives to train local talent and establish centers of excellence are addressing these issues. Gradual improvements in regulatory frameworks indicate a positive trajectory for market expansion, with long-term potential driven by high disease burden and government commitments.

COMPETITIVE LANDSCAPE

The competition in the digital PCR and qPCR market is characterized by intense rivalry among established life science giants and agile biotechnology startups striving for technological supremacy in nucleic acid quantification. Major corporations leverage their extensive distribution networks and broad product portfolios to maintain dominance, while smaller firms differentiate themselves through specialized innovations in microfluidics and enzyme chemistry. The landscape is dynamic with frequent mergers and acquisitions as larger entities seek to absorb novel technologies that enhance sensitivity and multiplexing capabilities. Competitive pressure drives continuous investment in research and development to lower costs and improve ease of use for clinical applications. Companies are increasingly competing on the ability to provide integrated solutions that combine hardware, reagents, and sophisticated software into seamless workflows. Regulatory compliance and the speed of obtaining approvals for diagnostic kits also serve as critical battlegrounds. The push towards precision medicine and liquid biopsy further intensifies competition as firms race to develop proprietary assays that offer unique clinical insights and secure lucrative contracts with healthcare providers and pharmaceutical partners globally.

KEY MARKET PARTICIPANTS

Some of the notable companies dominating the global digital PCR and qPCR market profiled in this report are

- Thermo Fisher Scientific Inc.

- F. Hoffmann-La Roche Ltd.

- Bio-Rad Laboratories

- Qiagen N.V.

- Taraka Bio Inc.

- Affymetrix Inc.

- Agilent Technologies Inc.

- Fluidigm Corporation

- Danaher Corporation

- Becton & Dickinson Company

TOP PLAYERS IN THE MARKET

- Thermo Fisher Scientific stands as a preeminent global leader by offering an extensive portfolio of quantitative and digital polymerase chain reaction solutions that serve research, clinical, and industrial sectors. The company provides integrated workflows ranging from sample preparation to data analysis, ensuring high precision and reproducibility for users worldwide. Their recent strategic actions focus on expanding their menu of validated assays for oncology and infectious diseases while enhancing the sensitivity of their digital PCR platforms. Thermo Fisher actively invests in developing automated systems that reduce manual handling errors and increase throughput for large-scale laboratories. They have also strengthened their position through collaborations with academic institutions to validate new biomarkers using their technologies. By continuously innovating their reagent chemistries and instrument software, they maintain a competitive edge in delivering reliable nucleic acid quantification tools that drive scientific discovery and diagnostic accuracy across the globe.

- Bio-Rad Laboratories maintains a significant presence in the market through its pioneering droplet digital PCR technology, which has set industry standards for absolute quantification without standard curves. The company specializes in providing robust instruments and consumables that enable researchers to detect rare mutations and measure low-abundance targets with exceptional precision. Bio-Rad recently intensified its efforts to expand applications in liquid biopsy and gene therapy quality control by launching new kits tailored for these high-growth areas. They have focused on improving user experience by integrating advanced data analysis software that simplifies complex statistical interpretations for laboratory personnel. Their strategy involves strengthening global distribution networks to ensure rapid access to critical reagents and technical support for customers in emerging markets. Bio-Rad also prioritizes educational initiatives to train scientists on best practices for digital PCR implementation. These continuous innovations and customer-centric approaches solidify their role as a key enabler of advanced molecular biology research and clinical diagnostics.

- Agilent Technologies contributes substantially to the global market by delivering high-performance quantitative PCR systems known for their reliability, speed, and versatility in diverse applications. The company leverages its expertise in analytical instrumentation to offer comprehensive solutions that include thermal cyclers, detection modules, and specialized consumables for gene expression and pathogen detection. Agilent has recently expanded its portfolio by introducing compact and cost-effective instruments designed for smaller laboratories and point-of-care settings. They are actively investing in developing multiplexing capabilities that allow simultaneous detection of multiple targets to increase efficiency and reduce sample consumption. Their strategic partnerships with diagnostic developers help accelerate the commercialization of novel tests based on their platforms. Agilent also focuses on sustainability by optimizing energy consumption in its instruments and reducing plastic waste in packaging. These efforts to enhance product performance and accessibility ensure they remain a trusted partner for scientists and clinicians seeking accurate and efficient nucleic acid analysis tools.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the digital PCR and qPCR market primarily employ strategic acquisitions and partnerships to expand their technological capabilities and product portfolios. Companies frequently acquire innovative startups specializing in novel microfluidics or enzyme engineering to enhance assay sensitivity and throughput. Another major strategy involves heavy investment in research and development to create next-generation platforms that integrate artificial intelligence for advanced data analytics and automation. Manufacturers are increasingly focusing on developing closed ecosystem models where proprietary instruments work exclusively with specific reagents to ensure quality and recurring revenue. Collaborations with academic institutions and pharmaceutical giants help validate new biomarkers and accelerate regulatory approvals for diagnostic applications. Expanding global distribution networks ensures faster delivery of consumables and instruments to emerging markets. Additionally, companies are standardizing protocols and offering comprehensive training programs to reduce the complexity of adoption for end users and foster long-term customer loyalty in this highly competitive landscape.

MARKET SEGMENTATION

This research report on the global digital PCR and qPCR market has been segmented and sub-segmented into the following categories.

By Product

- Consumables & Reagents

- Instruments

By Technology

- Quantitative PCR

- Digital PCR

By Application

- Tumors

- Blood Testing

- Pathogen Detection

- Research & Forensics

By End User

- Hospitals

- Research & Forensic Centers

- Pharmaceutical & Bio-Technological Firms

- Academic Institutions

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. Which technologies dominate the global digital PCR and qPCR market?

Real-time PCR (qPCR) holds the largest share, while digital PCR (dPCR) is rapidly growing due to high sensitivity in the global digital PCR and qPCR market

2. What are key applications in the global digital PCR and qPCR market?

Applications include infectious disease diagnosis, oncology, genetic testing, and personalized medicine in the global digital PCR and qPCR market

3. How does molecular diagnostics impact the global digital PCR and qPCR market?

Increased demand for precise nucleic acid quantification in molecular diagnostics boosts growth in the global digital PCR and qPCR market

4. How do pharmaceutical companies use digital PCR and qPCR?

Pharma relies on these technologies for biomarker identification and drug development in the global digital PCR and qPCR market

5. What role does multiplex PCR play in the global digital PCR and qPCR market?

Multiplex PCR enables simultaneous detection of multiple targets, increasing throughput and efficiency in the global digital PCR and qPCR market

6. What role does multiplex PCR play in the global digital PCR and qPCR market?

Multiplex PCR enables simultaneous detection of multiple targets, increasing throughput and efficiency in the global digital PCR and qPCR market

7. How are instruments and reagents segmented in the global digital PCR and qPCR market?

Instruments lead revenue, but consumables and reagents show strong growth in the global digital PCR and qPCR market

8. What are the main end users in the global digital PCR and qPCR market?

Academic research, clinical diagnostics labs, biotech, and pharma companies are major stakeholders in the global digital PCR and qPCR market

9. How is automation influencing the global digital PCR and qPCR market?

Automation improves PCR workflow efficiency, reproducibility, and throughput, driving adoption in the global digital PCR and qPCR market

10. What challenges face the global digital PCR and qPCR market?

High costs, regulatory hurdles, and complex data interpretation limit broader use in some regions of the global digital PCR and qPCR market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com