Europe Car Modification Market Size, Share, Trends, and Growth Analysis Report, Segmented by Vehicle Type, Modification Type, Modification Purpose, Consumer Demographics, Modification Complexity, and Country – Industry Forecast From 2026 to 2034

Market Size, 2025

$10.33 BnMarket Estimate, 2026

$10.88 BnMarket Forecast, 2034

$16.44 BnCAGR, 2026–2034

5.30%Europe Car Modification Market Report Summary

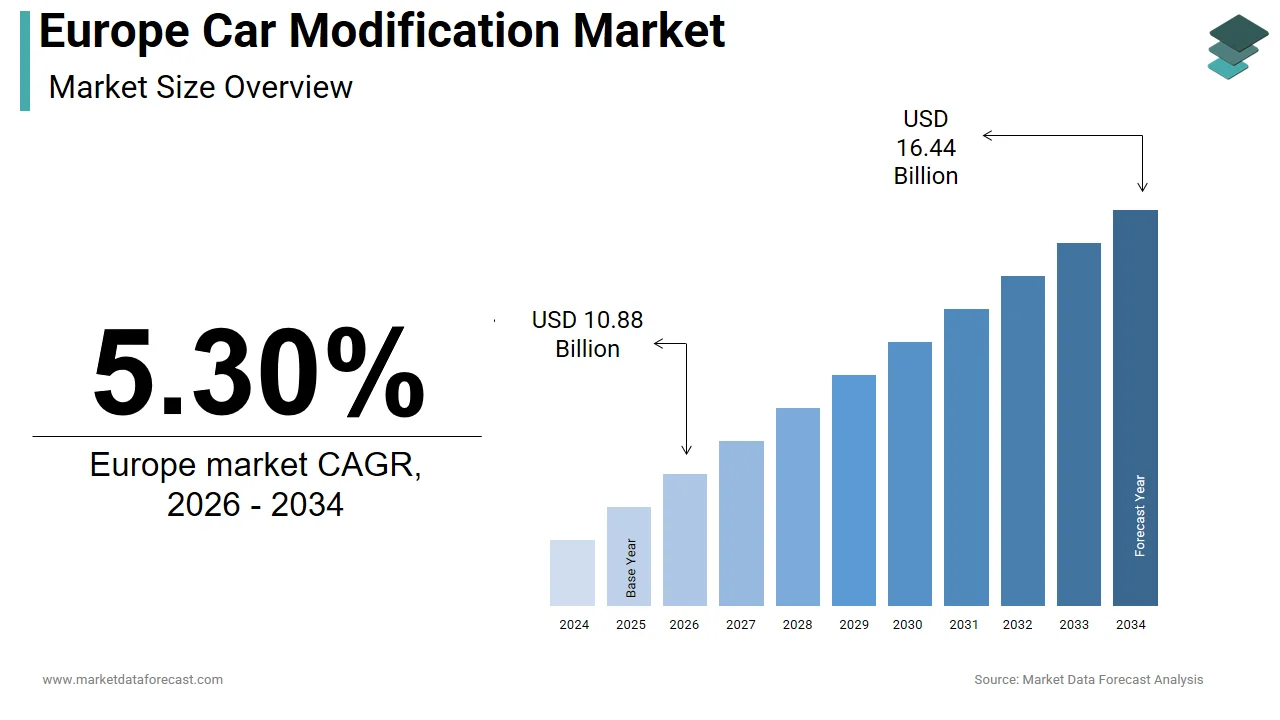

The Europe car modification market was valued at USD 10.33 billion in 2025, is estimated to reach USD 10.88 billion in 2026, and is projected to reach USD 16.44 billion by 2034, growing at a CAGR of 5.30% from 2026 to 2034. Market growth is driven by increasing consumer interest in vehicle personalization, rising demand for performance enhancement solutions, and growing popularity of luxury and sports vehicle customization across Europe. Car modification services including performance tuning, aesthetic customization, suspension upgrades, and advanced infotainment integration are gaining strong traction among automotive enthusiasts. The expansion of aftermarket automotive components, advancements in smart vehicle technologies, and increasing demand for tech-integrated upgrades are further supporting market growth.

Key Market Trends

- Rising demand for performance tuning and engine enhancement solutions.

- Increasing popularity of SUV customization and off-road utility upgrades.

- Growing adoption of tech-integrated automotive modification solutions.

- Expansion of premium aftermarket accessories and aesthetic customization services.

- Increasing focus on regulatory compliance and eco-friendly vehicle modifications.

Segmental Insights

- Based on vehicle type, the SUV customization segment dominated the Europe car modification market in 2025 by accounting for 36.9% market share, driven by increasing consumer preference for utility vehicles, off-road enhancements, and premium customization features.

- Based on modification type, the performance tuning segment led the market by capturing 35.3% share in 2025, supported by rising demand for enhanced engine performance, improved driving dynamics, and personalized vehicle experiences.

Regional Insights

The Europe car modification market is witnessing steady growth across major economies, supported by strong automotive culture, rising interest in vehicle personalization, and expanding aftermarket automotive industries.

- European countries are increasingly adopting stringent regulatory compliance standards while simultaneously expanding the integration of technology-enabled and smart automotive upgrades. Growing consumer demand for connected vehicle features, premium customization, and sustainable modification solutions is further shaping market growth across the region.

Competitive Landscape

The Europe car modification market is characterized by strong competition among automotive aftermarket companies, luxury vehicle customization specialists, and performance tuning providers focusing on innovation, premium personalization, and advanced vehicle enhancement solutions. Market participants are emphasizing development of high-performance components, aesthetic upgrades, and technology-integrated customization services to strengthen market positioning. Strategic collaborations, exclusive customization programs, and investments in advanced automotive engineering are shaping competitive dynamics across the market.

Prominent companies operating in the Europe car modification market include Hennessey Performance Engineering, Roush Performance, 3M Company, Continental AG, Robert Bosch GmbH, Mopar, ABT Sportsline, Brabus, TechArt, Liberty Walk, Veilside, Aston Martin Works, and Porsche Exclusive Manufaktur.

Europe Car Modification Market Size

The Europe car modification market was valued at USD 10.33 billion in 2025, is estimated to reach USD 10.88 billion in 2026, and is projected to reach USD 16.44 billion by 2034, growing at a CAGR of 5.30% from 2026 to 2034.

Car modification encompasses specialized services and products that alter vehicle performance, aesthetics, or functionality beyond original manufacturer specifications. This sector thrives on consumer desire for personalization, performance enhancement, and technological integration within automotive platforms. In Europe, the average vehicle age stands at 12.3 years, according to ACEA, which creates sustained demand for aftermarket upgrades as owners extend vehicle lifecycles through targeted modifications. Consumer expenditure patterns reveal that European households allocate approximately 13% of final spending to automotive-related purchases, as per Eurostat data, underscoring the economic significance of vehicle customization activities. With over 280 million vehicles registered across the European Union, the potential addressable market for modification services remains substantial, particularly for vehicles exceeding four years of age, which constitute approximately 70% of the regional fleet, as documented by Roland Berger research. The integration of digital technologies, sustainability mandates, and evolving consumer preferences continues to reshape modification practices across the continent.

MARKET DRIVERS

Rising Consumer Preference for Vehicle Personalization and Identity Expression

European consumers increasingly view their vehicles as extensions of personal identity, which is driving robust demand for customization solutions and is one of the major factors propelling the European car modification market growth. According to a Deloitte study, nearly 80% of consumers express frustration when personalization options remain limited during vehicle acquisition processes. This behavioral shift manifests in growing expenditure on appearance modifications, performance upgrades, and interior enhancements. In Spain and the Netherlands, car customization adoption rates exceed regional averages. The vehicle personalization market globally is projected to expand from 12.12 billion dollars in 2024 to 47.68 billion dollars by 2034, which is exhibiting substantial compound annual growth, as per Towards Automotive insights. Younger demographics, particularly those aged 18 to 35, demonstrate a heightened willingness to invest in aesthetic modifications, including custom wraps, lighting systems, and audio upgrades. Social media platforms amplify this trend by enabling enthusiasts to showcase modified vehicles, which generates aspirational demand across peer networks. Independent workshops report that appearance change services now represent one of the fastest-growing application segments within European modification markets. This sustained consumer enthusiasm for distinctive vehicle expression continues to fuel market expansion across both entry-level and premium customization tiers.

Technological Advancements Enabling Sophisticated and Accessible Modifications

Innovation in automotive technology has dramatically expanded the scope and accessibility of vehicle modifications across Europe, which is further contributing to the expansion of the European car modification market. Advanced engine tuning software, lightweight composite materials, and plug-and-play electronic modules now allow enthusiasts to achieve performance gains previously reserved for professional racing applications. According to Roland Berger's analysis, independent aftermarket players invest between 3% and 10% of revenues in innovation initiatives, which is significantly exceeding the European industrial average of 2.5%. The emergence of electric vehicle modification kits represents a particularly dynamic growth vector, with the global electric vehicle aftermarket projected to reach 215.90 billion dollars by 2034. Digital diagnostics, cloud-based tuning platforms, and over-the-air update capabilities enable remote customization services, reducing dependency on physical workshop visits. European regulations supporting right-to-repair principles further empower independent modifiers by ensuring access to vehicle data and compatible components. Smart technology integration, including connected infotainment upgrades and advanced driver assistance system enhancements, now constitutes a major modification category. These technological enablers collectively lower entry barriers while expanding functional possibilities, thereby stimulating broader consumer participation in the modification ecosystem.

MARKET RESTRAINTS

Stringent Regulatory Compliance Requirements across European Jurisdictions

European vehicle modification activities face complex regulatory frameworks that significantly constrain market expansion. The European Union maintains rigorous type approval standards under Regulation (EU) 2019/2144, which governs modifications affecting vehicle safety, emissions, and structural integrity, according to European Commission documentation. Euro 7 emissions standards, scheduled for full implementation, impose additional constraints on engine tuning practices, particularly those involving exhaust system alterations or catalytic converter modifications. National variations further complicate compliance, as German law limits vehicle noise emissions to 74 decibels, while other member states enforce distinct technical specifications. The administrative burden of obtaining post-modification certification discourages both consumers and service providers from pursuing extensive customization projects. According to FIGIEFA survey data, wholesale distributors report that regulatory uncertainty represents a primary operational challenge, affecting approximately 62% of independent aftermarket participants. Non-compliant modifications risk vehicle deregistration, insurance invalidation, and substantial financial penalties, creating significant consumer hesitation. These regulatory complexities disproportionately impact smaller modification enterprises lacking dedicated compliance resources, thereby limiting market diversity and innovation capacity across the European landscape.

Vehicle Warranty Preservation Concerns Dampening Consumer Modification Intentions

Consumer apprehension regarding warranty invalidation represents a substantial psychological and financial barrier to modification adoption across European markets, which is further hampering the car modification market growth in Europe. While EU Block Exemption Regulations theoretically protect consumers who utilize independent repair services during warranty periods, many vehicle manufacturers continue to impose restrictive clauses that create ambiguity regarding modification eligibility, according to the European Union guidance. A survey by the Irish Competition and Consumer Protection Commission revealed that warranty restrictions imposed through insurer-mediated arrangements potentially limit consumer choice regarding aftermarket parts and services. According to SAP News reporting on Deloitte research, approximately 75% of European consumers still prefer purchasing from authorized dealerships, where modification policies remain conservative. The perceived risk of voiding comprehensive warranty coverage, particularly for powertrain components, discourages investment in performance-oriented modifications. Independent workshops report that warranty-related inquiries constitute nearly 40% of initial customer consultations, indicating persistent consumer uncertainty. This restraint proves particularly impactful for newer vehicles under factory warranty, where owners balance customization desires against long-term ownership cost considerations. Until regulatory clarity and manufacturer policies achieve greater alignment, warranty concerns will continue to suppress modification demand among risk-averse consumer segments.

MARKET OPPORTUNITIES

Electric Vehicle Aftermarket Customization Emerging as a High-Growth Segment

The accelerating transition toward electric mobility presents unprecedented opportunities for the Europe car modification market growth. Electric vehicle aftermarket revenue is projected to reach 154 billion euros by 2035, according to WESP analysis of over 50 million workshop invoices. Battery performance optimization, thermal management enhancements, and regenerative braking calibration represent technically sophisticated modification categories commanding premium pricing. European independent workshops increasingly develop EV-specific capabilities, including high-voltage safety training and proprietary diagnostic tooling. Lightweight component upgrades and aerodynamic refinements offer meaningful range improvements that resonate with environmentally conscious consumers. Software-based modifications enabling customizable driving modes, acceleration profiles, and energy recovery settings appeal to tech-oriented buyers seeking personalized electric driving experiences. According to ACEA projections, as the European EV fleet expands beyond 30 million units by 2030, the addressable market for electric vehicle modifications will scale proportionally. Early-mover advantage in this segment promises substantial returns for modifiers who invest in specialized expertise and compliant solution development.

Digital Platform Integration Enabling Scalable Customization Services

The convergence of automotive modification with digital commerce platforms creates promising opportunities for market expansion and service delivery innovation. E-commerce is flourishing in European automotive spare parts and customization segments, according to Statista's analysis of regional digital trends. Online configuration tools, virtual vehicle visualization, and remote tuning services enable consumers to design and purchase modifications without physical workshop visits. Subscription-based modification models offering periodic performance updates or aesthetic refreshes generate recurring revenue streams while enhancing customer retention. Data-driven personalization algorithms analyze driving patterns and preference data to recommend tailored modification packages, increasing conversion rates and average transaction values. According to Roland Berger research, independent distributors investing in digital capabilities report 15% to 25% higher customer engagement metrics compared to traditional operations. Mobile applications facilitating modification scheduling, progress tracking, and post-installation support improve service transparency and consumer confidence. Integration with vehicle telematics enables predictive maintenance recommendations and performance optimization alerts, creating ongoing value beyond initial modification transactions. These digital enablers collectively lower customer acquisition costs, expand geographic reach, and enhance service scalability, positioning technology-forward modifiers for disproportionate growth in an increasingly connected automotive ecosystem.

MARKET CHALLENGES

Supply Chain Volatility Impacting Component Availability and Pricing Stability

European car modification enterprises face persistent supply chain disruptions that compromise service reliability and margin predictability. According to FIGIEFA survey responses from wholesale distributors, geopolitical tensions, raw material scarcity, and logistics bottlenecks have elevated component lead times by 30% to 50%. Critical modification components, including performance chips, suspension kits, and aesthetic accessories, frequently experience stockouts, forcing workshops to delay installations or substitute lower-margin alternatives. Price volatility for specialized materials, such as carbon fiber, aluminum alloys, and electronic semiconductors, introduces margin compression risks that independent modifiers struggle to absorb. According to Roland Berger's analysis, wholesale distributors carrying over 50,000 stock-keeping units report inventory management complexity as a top operational challenge, affecting 46% of respondents. Just-in-time delivery expectations from commercial fleet clients further intensify pressure on supply chain resilience. The fragmentation of European distribution networks, with over 282,000 independent parts distributors and workshop outlets, complicates coordinated inventory planning and demand forecasting. Until supply chain digitization and regional manufacturing reshoring initiatives mature, modification service providers will continue navigating availability uncertainties that constrain growth ambitions and customer satisfaction metrics.

Skilled Technician Shortage Limiting Service Capacity and Quality Consistency

The critical shortage of technicians possessing specialized expertise in advanced customization techniques and emerging vehicle architectures is also challenging the Europe car modification market expansion. According to Roland Berger documentation, the independent aftermarket employed approximately 1.1 million skilled workers across distribution and workshop operations in 2023, yet demand for EV-certified tuning specialists and software integration experts far exceeds current supply. Training pipelines struggle to keep pace with technological evolution, as modification techniques increasingly require proficiency in high-voltage systems, embedded software diagnostics, and composite material fabrication. According to FIGIEFA survey insights, independent workshops report that recruitment delays for qualified technicians extend service wait times by 2 to 4 weeks on average. The competitive labor market sees authorized dealer networks and original equipment manufacturers offering superior compensation packages that attract talent away from independent modification enterprises. This skills gap particularly impacts complex modification categories, including engine remapping, advanced driver assistance system calibration, and battery performance optimization. Without coordinated industry investment in vocational training, certification programs, and knowledge-sharing platforms, the technician shortage will constrain service scalability, quality consistency, and innovation adoption across the European modification landscape.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Vehicle Type, Modification Type, Modification Purpose, Consumer Demographics, Modification Complexity, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the rest of Europe |

| Market Leaders Profiled |

|

SEGMENTAL ANALYSIS

By Vehicle Type Insights

The SUV customization segment had 36.9% of the regional market share in 2025 and is poised to experience robust interest and expanded utility upgrades over the next few years. This dominance results from the substantial SUV fleet across Europe, which exceeded 95 million registered units in 2024, as per ACEA documentation. European consumers increasingly view SUVs as versatile platforms for both aesthetic enhancement and performance optimization, driving sustained aftermarket investment. The average SUV owner allocates approximately 1,800 euros annually toward customization activities, according to Roland Berger consumer expenditure studies. Key driving factors include the modular architecture of modern SUVs, which facilitates aftermarket component integration, and the growing preference for off-road capability enhancements among European adventure enthusiasts. Additionally, SUV modifications benefit from broader regulatory acceptance compared to sports car alterations, enabling wider consumer participation. The segment further gains momentum from commercial fleet operators who invest in protective body kits and durability upgrades for business vehicles. This trajectory reflects sustained consumer confidence in SUV platforms as long-term ownership assets warranting personalized enhancement investments.

On the other hand, the motorcycle segment is estimated to witness a CAGR of 9.2% during the forecast period in the European market, owing to the rising motorcycle registrations, which increased by 4.1% across Europe in 2024, as per European Motorcycle Industry Association data. According to Deloitte consumer insights, younger demographics, particularly those aged 20 to 35, demonstrate heightened enthusiasm for motorcycle personalization, with approximately 67% of new motorcycle buyers planning aftermarket enhancements within the first year of ownership. Performance-oriented modifications, including exhaust system upgrades and engine tuning, account for nearly 45% of motorcycle modification expenditure, reflecting strong demand for enhanced riding dynamics. The segment benefits from relatively lower regulatory barriers compared to four-wheeled vehicles, enabling faster innovation cycles and broader product availability. Social media platforms amplify motorcycle customization culture, with enthusiast communities sharing modification techniques and inspiring peer adoption. According to FIGIEFA survey responses, independent workshops report that motorcycle modification services generate 22% higher margins than passenger car equivalents. This profitability incentive encourages specialized service providers to expand motorcycle-focused offerings, further accelerating segment growth across European markets.

By Modification Type Insights

The performance tuning segment led the market by holding 35.3% of the European market share in 2025. This dominance reflects enduring consumer prioritization of enhanced driving dynamics, including acceleration, handling, and braking capabilities. European enthusiasts allocate an average of 2,100 euros annually toward performance-oriented modifications, as per Roland Berger expenditure analysis. Key growth drivers include the widespread availability of plug-and-play tuning modules, which enable significant power gains without complex mechanical alterations. The emergence of cloud-based engine calibration platforms allows remote performance optimization, expanding accessibility beyond specialized workshops. According to ACEA data, over 62% of vehicles exceeding five years of age undergo at least one performance enhancement during their lifecycle. Additionally, motorsport-inspired technologies originally developed for competitive racing increasingly filter into consumer modification offerings, creating aspirational demand. According to FIGIEFA industry surveys, independent tuning specialists report that performance upgrades generate 28% higher customer retention rates compared to cosmetic modifications. The segment further benefits from growing acceptance of certified aftermarket performance components that maintain compliance with European emissions and safety regulations. This regulatory alignment reduces consumer hesitation while preserving modification appeal, thereby sustaining robust segment expansion across diverse European markets.

However, the eco-friendly modifications segment is expected to exhibit the most rapid expansion within the European car modification market and register a CAGR of 10.4% during the forecast period due to the intensifying environmental consciousness among European consumers, with 71% expressing willingness to invest in sustainability-focused vehicle enhancements, as per Eurobarometer survey data. Key growth catalysts include advancing battery optimization technologies for hybrid and electric vehicles, which enable meaningful range extensions through aftermarket interventions. According to ACEA projections, electric vehicle registrations across Europe will surpass 35 million units by 2030, creating a substantial addressable market for eco-compatible modifications. Lightweight component upgrades, including carbon fiber body panels and aluminum suspension parts, deliver measurable fuel efficiency improvements that resonate with environmentally conscious buyers. The European Green Deal framework further incentivizes modification practices that reduce lifecycle emissions, encouraging innovation in sustainable aftermarket solutions. According to FIGIEFA industry intelligence, independent workshops report that eco-friendly modification services command premium pricing, with average transaction values 18% higher than conventional alternatives. Digital platforms enabling carbon footprint tracking for modified vehicles enhance consumer engagement and reinforce sustainability messaging. These converging factors position eco-friendly modifications for sustained outperformance relative to traditional modification categories across European markets.

REGIONAL ANALYSIS

European nations are anticipated to experience stringent compliance adaptations coupled with an expansion in tech-integrated upgrades over the next few years. This positioning reflects balanced market dynamics characterized by regulatory sophistication, consumer discernment, and technological leadership. According to ACEA consumer behavior studies, European vehicle owners demonstrate a strong preference for certified modification components, with approximately 68% prioritizing compliance with regional safety and emissions standards. Key growth drivers include aging vehicle fleet dynamics, with the average European vehicle age reaching 12.3 years, creating sustained demand for lifecycle enhancement services, as per Roland Berger fleet analysis. The region further benefits from advanced digital infrastructure, enabling seamless online modification, configuration, and remote performance optimization. According to FIGIEFA industry intelligence, independent European workshops report that technology-integrated modifications, including connected infotainment and advanced driver assistance system enhancements, generate 26% higher margins than conventional alternatives. Additionally, European consumers increasingly embrace sustainability-focused modifications, with eco-friendly component adoption growing by 14% annually, according to Eurobarometer environmental trends data. These converging factors sustain Europe's market relevance while enabling premium positioning amid evolving regulatory and consumer expectations across diverse regional markets.

COMPETITIVE LANDSCAPE

The car modification market exhibits moderately fragmented competitive dynamics characterized by the coexistence of global technology leaders, regional specialists, and emerging digital innovators. Established players leverage brand reputation, technical expertise, and extensive distribution networks to maintain market presence while facing pressure from agile entrants offering niche solutions and disruptive business models. Competition increasingly centers on technological differentiation, with companies investing in software-defined modification platforms, connected vehicle integration, and artificial intelligence-driven personalization capabilities. Regulatory compliance represents a critical competitive factor as companies navigate diverse regional frameworks governing emissions safety and vehicle certification. Sustainability considerations gain prominence with consumers prioritizing eco-friendly modification options and circular economy practices. Digital transformation accelerates competitive intensity as companies develop omnichannel experiences, virtual configuration tools, and data-driven customer engagement strategies. Pricing dynamics reflect a balance between premium positioning for certified components and value-oriented offerings for cost-conscious segments. Strategic partnerships and acquisitions enable capability expansion and market access while fostering innovation through collaborative development. Customer loyalty programs and professional certification initiatives strengthen retention amid intensifying competition for enthusiast and mainstream consumer segments. These converging factors shape a dynamic competitive landscape requiring continuous adaptation and strategic differentiation to sustain market position.

KEY MARKET PLAYERS

The leading companies operating in the Europe Car modification market include:

- Hennessey Performance Engineering

- Roush Performance

- 3M Company

- Continental AG

- Robert Bosch GmbH

- Mopar

- ABT Sportsline

- Brabus

- TechArt

- Liberty Walk

- Veilside

- Aston Martin Works

- Porsche Exclusive Manufaktur

TOP PLAYERS IN THE MARKET

- 3M Company maintains prominent involvement in the global car modification market through comprehensive offerings spanning protective films, adhesive solutions, and aesthetic enhancement products. The company leverages advanced material science to develop innovative vehicle wrap technologies that enable reversible customization while preserving original paint integrity. Recent strategic initiatives include expanded production capacity for premium vinyl films and strategic partnerships with digital configuration platform providers to enhance consumer visualization capabilities. 3M further strengthens its market position through sustainability-focused product development, including recyclable modification materials and low-emission adhesive formulations. The company invests in technician training programs across European and North American markets, ensuring professional installation quality and customer satisfaction. These coordinated efforts reinforce 3 M's reputation for reliability and innovation within the global modification ecosystem.

- Continental AG contributes significantly to the car modification market through advanced automotive technology solutions, including performance electronics, suspension components, and connectivity systems. The company leverages original equipment manufacturer expertise to develop aftermarket products that maintain regulatory compliance while delivering measurable performance gains. Recent strategic actions include the launch of cloud-based tuning platforms enabling remote performance optimization and expansion of electric vehicle modification portfolios addressing emerging consumer demand. Continental further strengthens its market position through strategic acquisitions of specialized tuning enterprises and investments in digital retail channels, enhancing direct consumer access. The company prioritizes sustainability through the development of energy-efficient modification components and circular economy initiatives for end-of-life component management. These integrated strategies reinforce Continental's leadership in technology-driven vehicle enhancement solutions across global markets.

- Robert Bosch GmbH maintains substantial influence in the car modification market through comprehensive automotive systems, including engine management electronics, braking components, and diagnostic solutions. The company leverages extensive research and development capabilities to deliver aftermarket products that enhance vehicle performance while maintaining safety and emissions compliance. Recent strategic initiatives include the expansion of software-defined vehicle modification platforms enabling over-the-air performance updates, and the development of electric vehicle-specific enhancement kits addressing growing consumer interest. Bosch further strengthens its market position through strategic partnerships with independent workshop networks, ensuring broad service availability and professional installation quality. The company invests in technician certification programs and digital training resources supporting aftermarket ecosystem development. These coordinated efforts reinforce Bosch's reputation for engineering excellence and technological innovation within the global modification landscape.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key participants in the car modification market employ strategic approaches centered on technological innovation, regulatory compliance, and consumer engagement. Companies prioritize research and development investments to create advanced modification solutions that balance performance enhancement with environmental sustainability. Strategic partnerships with digital platform providers enable seamless virtual configuration and remote optimization capabilities, enhancing consumer experience. Market leaders expand distribution networks through omnichannel strategies, integrating physical retail with e-commerce platforms to maximize accessibility. Product portfolio diversification addresses emerging segments, including electric vehicle modifications and eco-friendly component offerings. Companies invest in technician training and certification programs, ensuring professional installation quality and customer satisfaction. Sustainability initiatives, including recyclable materials and circular economy practices, strengthen brand reputation among environmentally conscious consumers. Strategic acquisitions of specialized tuning enterprises accelerate technology adoption and market expansion. Digital marketing campaigns leveraging social media and enthusiast communities drive brand awareness and consumer engagement. These coordinated strategies enable market participants to navigate evolving regulatory landscapes while capturing growth opportunities across diverse global segments.

MARKET SEGMENTATION

This Europe Car modification market research report is segmented and sub-segmented into the following categories.

By Vehicle Type

- Passenger Cars

- Sports Cars

- SUVs

- Trucks

- Motorcycles

By Modification Type

- Performance Tuning

- Aesthetic Customization

- Eco-friendly Modification

- Suspension Upgrades

- Exhaust System Modification

- Engine Swaps

By Modification Purpose

- Enhanced Performance

- Improved Aesthetics

- Increased Safety

- Personal Expression

- Resale Value Enhancement

By Consumer Demographics

- Enthusiasts

- Casual Modifiers

- Professional Racers

- First-Time Modifiers

- Budget-Conscious Modifiers

By Modification Complexity

- Basic Modifications

- Intermediate Modifications

- Advanced Modifications

- Custom Fabrication

- Full Vehicle Builds

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe car modification market?

The Europe car modification market includes aftermarket services and products for customizing vehicles, such as performance upgrades, styling enhancements, and accessories across European countries.

Why is the Europe car modification market growing?

The Europe car modification market is growing due to strong car culture, high disposable incomes, passion for automotive customization, and demand for personalized vehicle performance and aesthetics.

Who uses the Europe car modification market?

Car enthusiasts, individual vehicle owners,fleet operators, and tuning companies use the Europe car modification market for performance upgrades, styling, and personalized automotive enhancements.

What modifications are popular in the Europe car modification market?

The Europe car modification market features engine tuning, exhaust upgrades, suspension modifications, body kits, wheel upgrades, interior customization, and electric vehicle conversions.

How does car culture impact the Europe car modification market?

Car culture drives the Europe car modification market through enthusiast communities, automotive events, racing heritage, and strong demand for personalized performance and styling solutions.

What challenges face the Europe car modification market?

Challenges in the Europe car modification market include strict regulatory compliance, safety standards, emission regulations, warranty concerns, and varying country-specific modification laws.

Which countries lead the Europe car modification market?

Germany, the United Kingdom, and Italy lead the Europe car modification market due to strong automotive heritage, tuning culture, and high consumer spending on vehicle customization.

How does regulation affect the Europe car modification market?

Regulations shape the Europe car modification market through emission standards, safety certifications, type approval requirements, and country-specific legal restrictions on vehicle modifications.

What role does performance tuning play in the Europe car modification market?

Performance tuning is central to the Europe car modification market, offering engine enhancements, improved handling, increased power, and optimized driving dynamics for enthusiasts.

Is the Europe car modification market competitive?

Yes, the Europe car modification market is highly competitive with numerous tuners, aftermarket brands, customization shops, and innovative products competing for enthusiast customers.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com