Europe Electric Ship Market Size, Share, Trends, and Growth Analysis Report, Segmented by Ship Type, Mode of Operation, Power Output, Propulsion Type, and Country – Industry Forecast From 2026 to 2034

Market Size, 2025

$1.64 BnMarket Estimate, 2026

$1.93 BnMarket Forecast, 2034

$7.21 BnCAGR, 2026–2034

17.89%Europe Electric Ship Market Report Summary

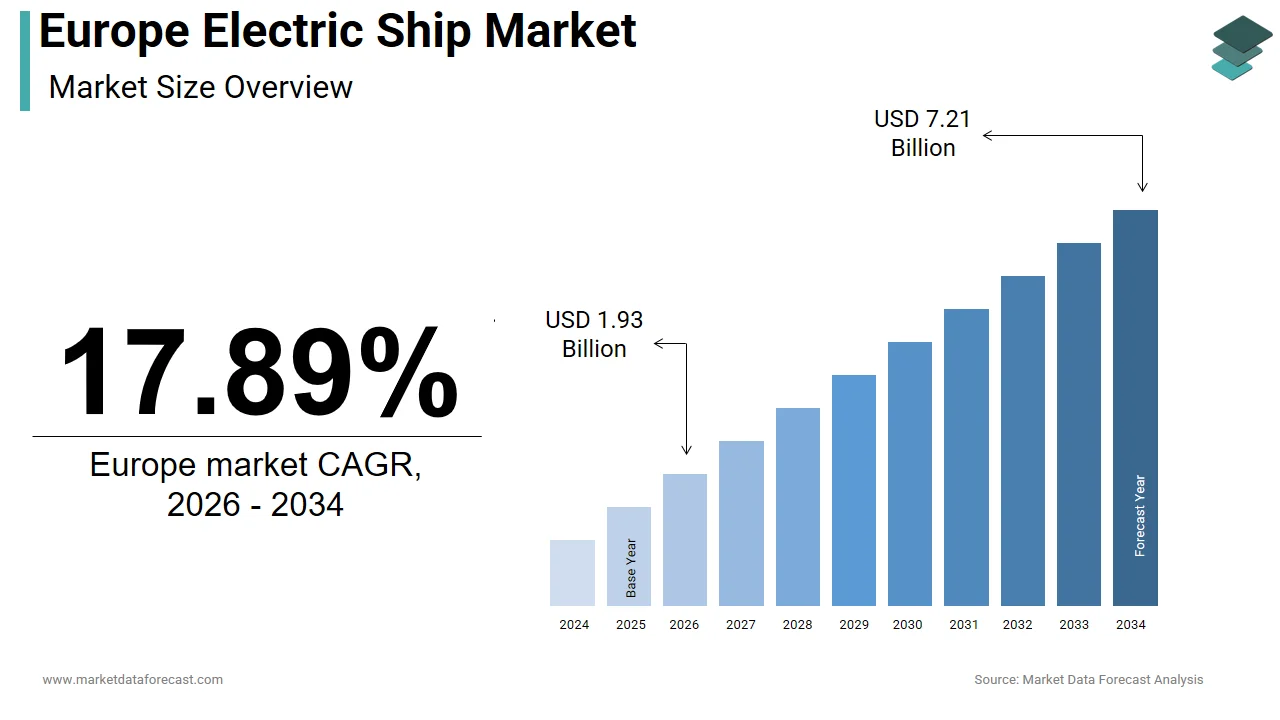

The Europe electric ship market was valued at USD 1.64 billion in 2025, is projected to reach USD 1.93 billion in 2026, and is estimated to grow to USD 7.21 billion by 2034, expanding at a CAGR of 17.89% from 2026 to 2034. Market growth is driven by stringent maritime emission regulations, increasing investments in green shipping technologies, and the transition toward sustainable marine transportation. The adoption of electric propulsion systems, especially in short-route passenger and inland waterway vessels, is accelerating across Europe. Government incentives, port electrification initiatives, and advancements in battery energy storage are further strengthening market expansion.

Key Market Trends

- Rising adoption of electric passenger vessels for short-distance and urban water transport.

- Strong demand for semi-autonomous electric ships to improve operational efficiency and safety.

- Growing use of low-power electric propulsion systems for inland and coastal routes.

- Increasing investments in port electrification and charging infrastructure.

- Expansion of battery and energy storage solutions for maritime applications.

Segmental Insights

-

Based on ship type, the passenger ship segment dominated the Europe electric ship market with a 65.5% share in 2025, driven by the widespread use of electric ferries and urban water transport vessels.

-

Based on mode of operation, the semi-autonomous segment held a dominant 90.8% share in 2025, supported by the integration of automated navigation, monitoring, and energy management systems.

-

Based on power output, the up to 745 kW segment accounted for the leading share in 2025 due to the prevalence of small passenger and service vessels operating on short, fixed routes.

Regional Insights

The Europe electric ship market is witnessing strong growth across key maritime economies, supported by green shipping policies, inland waterway electrification, and port modernization programs.

- Norway led the market with a 30.9% share in 2025, driven by its strong electric ferry adoption, government incentives, and commitment to zero-emission maritime transport.

- Germany ranked second, with activity concentrated on inland waterways and urban river networks, supported by sustainability-focused transport policies.

- The Netherlands held a prominent share, driven by leadership in urban canal electrification and smart port innovation.

Competitive Landscape

The Europe electric ship market is characterized by a strong presence of marine technology providers, battery manufacturers, and ship system integrators focusing on sustainable propulsion solutions. Companies are investing in advanced battery systems, electric drivetrain technologies, and smart marine automation platforms. Strategic collaborations with shipbuilders, ports, and energy providers are shaping competitive advantage, with performance, reliability, and regulatory compliance being key differentiators rather than price alone.

Prominent companies in the Europe electric ship market include Kongsberg, Leclanche, Corvus Energy, Echandia Marine AB, Siemens, Vard (part of Fincantieri SpA), Norwegian Electric Systems, General Dynamics Electric Boat, MAN Energy Solutions SE, Wartsila, Schottel Group, Anglo Belgian Corporation NV, ABB Marine & Ports, Eco Marine Power, and Akasol AG.

Europe Electric Ship Market Size

The Europe electric ship market was worth USD 1.64 billion in 2025, is projected to reach USD 1.93 billion in 2026, and is estimated to grow to USD 7.21 billion by 2034, expanding at a CAGR of 17.89% from 2026 to 2034.

Electric ships range from ferries and inland waterway cargo ships to coastal patrol boats and tourist cruise vessels that rely partially or fully on electric propulsion systems powered by batteries, hybrid generators, or shore-side charging infrastructure. Unlike conventional marine vessels dependent on heavy fuel oil or marine diesel, electric ships in Europe are engineered to meet stringent environmental mandates while operating primarily in sensitive aquatic zones such as fjords, rivers, lakes, and urban harbours. According to the European Maritime Safety Agency, electrification in shipping is increasing with more vessels adopting battery energy storage systems and hybrid-electric solutions, and countries such as Norway, Germany, and the Netherlands are leading deployment. As per the European Environment Agency, maritime transport is a significant source of greenhouse gas emissions in Europe, which is contributing notably to transport-related CO2 emissions. Furthermore, the European Commission’s FuelEU Maritime Regulation, effective from 2025 and this requires reductions in the greenhouse gas intensity of marine fuels, which is accelerating the transition toward zero-emission propulsion. These regulatory and ecological imperatives position electric ships not as niche experiments but as strategic instruments in Europe’s broader decarbonization and water quality protection agenda.

MARKET DRIVERS

EU FuelEU Maritime and Zero-Emission Port Mandates Drive Electrification of Short-Sea and Inland Vessels

Europe’s regulatory architecture has become the primary catalyst for marine electrification, particularly for vessels operating on fixed short-distance routes, which is one of the key factors propelling the growth of the European electric ship market. According to the European Commission, the FuelEU Maritime Regulation requires a reduction in the greenhouse gas intensity of marine energy use starting in 2025, which is expected to escalate significantly by 2050. This effectively penalizes fossil-fueled vessels on predictable routes where battery-electric operation is technically feasible. Complementing this, the Alternative Fuels Infrastructure Regulation mandates that all major EU ports install onshore power supply systems by 2030, which enables ships to shut down engines while docked. According to the European Maritime Safety Agency, several ports, including Rotterdam, Hamburg, and Gothenburg, already offer OPS for passenger and ferry terminals. As per the International Council on Clean Transportation, electric ferries on short routes can reduce CO2 emissions substantially and eliminate sulfur oxides and particulate matter compared to diesel counterparts. This regulatory push transforms electrification from an optional sustainability gesture into a compliance necessity for operators in Europe’s dense network of inland waterways and coastal corridors.

Preservation of Sensitive Aquatic Ecosystems Spurs Adoption in Protected and Urban Waterways

European nations are increasingly restricting fossil-fueled vessel operations in ecologically and socially sensitive zones to protect water quality and public health, which is also supporting the expansion of the European electric ship market. According to the European Environment Agency, a significant share of Europe’s inland waterways flow through Natura 2000 protected areas, where noise and emissions from marine engines threaten aquatic biodiversity. In response, Norway announced bans on fossil-fueled ferries in its western fjords, UNESCO World Heritage Sites, by 2026, which is prompting the deployment of fully electric ferries. Similarly, Amsterdam and Paris have prohibited diesel-powered tourist boats on central canals by 2025, as confirmed by municipal environmental ordinances. According to the reports from the Dutch Ministry of Infrastructure, reductions in underwater noise pollution on the Amsterdam-Rhine Canal following the introduction of electric barges directly benefit fish spawning behaviors. Urban air quality regulations further amplify demand, as the City of Venice mandates zero-emission propulsion for all new public water transit by 2027 to reduce diesel particulate exposure in its densely populated lagoon. These localized bans create concentrated demand pockets where electric ships are not just preferred but legally required.

MARKET RESTRAINTS

Limited Battery Energy Density and Vessel Range Restrict Applicability to Short-Haul Routes

The fundamental technological constraint in marine electrification remains the energy density of current lithium-ion battery systems, which severely limits operational range and payload capacity. According to DNV’s Maritime Battery Handbook, state-of-the-art marine batteries deliver around 150 to 180 watt-hours per kilogram, less than half the energy density of marine diesel. This forces electric vessels to allocate a significant portion of gross tonnage to battery banks, directly reducing cargo or passenger space. Analyses by European inland waterway operators indicate that fully electric cargo barges on the Rhine lose notable payload capacity compared to diesel equivalents, making them less viable for long-distance hauls. Consequently, most of Europe’s electric ships operate on short routes with multiple daily charging opportunities, as per the European Maritime Safety Agency. Until solid-state or alternative chemistries achieve higher energy density, a milestone expected only after 2030, the market will remain confined to short-sea and inland applications, unable to penetrate deep-sea or transcontinental shipping corridors.

Fragmented and Underdeveloped Shore Charging Infrastructure Hinders Scalability

Despite policy support, the absence of a harmonized and high-capacity onshore charging network across European waterways impedes widespread electric ship adoption, which is further impeding the growth of the European electric ship market. According to the European Commission’s Alternative Fuels Infrastructure Report, only a limited share of inland ports on the Trans-European Transport Network have operational high-power marine charging stations, with significant gaps in Eastern and Southern Europe. Moreover, charging standards remain inconsistent, with Norway using one system and German Rhine ports deploying another, forcing operators to carry multiple adapters or limit routes. As per the studies by the Central Commission for the Navigation on the Rhine, many barge operators cite charging availability and interoperability as their top barrier to electrification. Grid capacity is another constraint, as the Swedish Energy Agency notes that upgrading port substations to support multi-megawatt charging can cost millions of euros per terminal. Without coordinated EU-level investment and technical standardization, the electric ship market will remain fragmented and unable to achieve the scale necessary for cost reduction and network effects.

MARKET OPPORTUNITIES

Expansion of Green Hydrogen and Ammonia Hybrid Systems Creates Dual-Fuel Transition Pathways

While battery-electric dominates short-haul segments, the integration of green hydrogen and ammonia fuel cells offers a viable decarbonization route for longer-range vessels, which is a prominent opportunity in the European electric ship market. According to the European Clean Hydrogen Partnership, multiple pilot projects for hydrogen-powered ships are underway in Europe, including the Hydroville ferry in Belgium and the hydrogen tugboat Hydrotug in Antwerp. As per the European Maritime Safety Agency, hybrid electric-hydrogen vessels can extend range while maintaining zero operational emissions. Crucially, the EU’s Renewable and Low-Carbon Fuels in Maritime Transport initiative has allocated significant funding through 2027 to develop green hydrogen bunkering infrastructure in ports such as Rotterdam and Valencia. As per DNV, hybrid systems can reduce lifecycle CO2 emissions considerably compared to diesel when using renewable hydrogen. This dual-fuel approach allows shipowners to future-proof investments without waiting for battery breakthroughs, creating a strategic bridge toward full zero-emission operations.

Public Procurement and Subsidy Programs Accelerate Fleet Renewal in Public Water Transit

Government-led initiatives are de-risking early adoption through targeted financial support and fleet mandates, which is another major opportunity in the European electric ship market. According to the European Investment Bank, billions of euros have been allocated to fund zero-emission maritime projects, with a large share directed toward public passenger vessels such as ferries and water buses. In Germany, the National Innovation Program for Hydrogen and Fuel Cell Technology has provided funding for electric ferry deployment on Lake Constance and the Elbe River. Similarly, the French Agency for Energy Transition funded the Voguéo electric water taxi service in Paris, replacing diesel boats on the Seine. According to a 2024 evaluation by the OECD, public procurement accounts for the majority of electric ship orders in Europe, creating a stable demand base that enables shipyards to achieve economies of scale. This institutional anchor not only reduces upfront costs but also validates technology performance to encourage private operators to follow suit in commercial passenger and cargo segments.

MARKET CHALLENGES

High Capital Expenditure and Total Cost of Ownership Uncertainty Deter Private Investment

Despite environmental benefits, the elevated upfront cost of electric vessels remains a formidable barrier for private shipowners operating on thin margins, which is a significant challenge to the growth of the European electric ship market. According to the European Sea Ports Organization, electric ferries cost significantly more than diesel equivalents, with battery systems accounting for a large portion of the vessel’s total price. As per the reports from the International Chamber of Shipping, small and medium-sized barge operators face longer payback periods even with subsidies compared to conventional vessels. Additionally, uncertainty around battery replacement cycles, typically warranted for several years but degrading faster under heavy cycling, introduces lifecycle cost volatility. According to the European Bank for Reconstruction and Development, private lenders remain hesitant to finance electric ships without government loan guarantees due to unproven residual values. Until battery prices fall further and standardized second-life markets emerge, private sector adoption will lag behind publicly funded projects, constraining market breadth.

Absence of Unified EU Certification and Safety Standards for High-Voltage Marine Systems

The lack of harmonized technical and safety regulations for high-voltage battery installations on ships creates compliance complexity and delays project timelines, which further challenges the expansion of the European electric ship market. While the International Maritime Organization has issued interim guidelines, the European Union has yet to adopt binding standards under the Marine Equipment Directive for battery fire suppression, thermal runaway containment, and electrical isolation. According to the European Maritime Safety Agency, national flag states such as Norway, Germany, and the Netherlands have implemented divergent safety protocols, requiring shipbuilders to redesign systems for each market. As per a 2024 audit by DNV, certification for a single electric vessel model can take many months due to redundant national testing. This regulatory fragmentation increases engineering costs and discourages cross-border fleet deployment. Without an EU-wide framework aligned with IEC 62619 and ISO 23240, the market will continue to face inefficiencies that stifle innovation, delay deliveries, and undermine investor confidence in scalable electric ship solutions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Ship Type, Mode of Operation, Power Output, Propulsion Type, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Bombardier Inc., Gulfstream Aerospace Corporation (General Dynamics Corporation), Dassault Aviation SA, Textron Inc., Embraer S.A., and Others. |

SEGMENTAL ANALYSIS

By Ship Type Insights

The passenger ship segment dominated the market by holding 65.5% of the regional market share in 2025. The dominance of the passenger ship segment in the European market is driven by predictable short routes, high public visibility, and strong regulatory pressure in urban and protected waterways. European cities and heritage sites are enforcing zero-emission requirements for passenger vessels to improve air quality and preserve sensitive ecosystems. According to the European Environment Agency, many cities across the EU have implemented or announced bans on diesel-powered tourist boats and water taxis by 2025. In Venice, the municipal government mandated that all new public water transit vessels be fully electric by 2027 to reduce diesel particulate exposure in its historic lagoon. Similarly, Amsterdam’s Clean Boating Ordinance prohibits fossil-fuelled canal boats from 2025 onward. These localized bans directly stimulate demand for electric ferries, water buses, and sightseeing vessels. As per the Dutch Ministry of Infrastructure, a majority of new passenger vessels ordered for Amsterdam’s canal network in 2024 were battery electric, with average route lengths under 10 kilometres, enabling multiple daily charges.

The commercial ship segment is the fastest-growing segment in the European market and is estimated to grow at a CAGR of 23.1% over the forecast period. The European Commission’s Green Corridors program is catalyzing electric cargo barge adoption on high-density inland routes. As per the Central Commission for the Navigation on the Rhine, several zero-emission cargo pilot projects were launched in 2024 on the Rhine, Danube, and Rhône waterways with EU Innovation Fund support. The Port of Rotterdam’s Green Barge Initiative aims to electrify a significant share of its inland container feeders by 2030, requiring operators to deploy vessels with large battery systems. As per the reports from the European Federation of Inland Waterway Operators, electric barges on fixed routes between Duisburg and Rotterdam reduce CO2 emissions substantially and eliminate portside noise complaints. With inland shipping handling about one quarter of EU freight and under increasing pressure to decarbonize, this segment is transitioning from demonstration to commercial scale.

By Mode of Operation Insights

The semi-autonomous segment held 90.8% of the regional market share in 2025. The growth of the semi-autonomous segment in this regional market is attributed to the regulatory caution, technological maturity, and operational risk management in complex waterways. Current EU maritime regulations under the International Convention for the Safety of Life at Sea require a human master to retain ultimate control of a vessel. According to the European Maritime Safety Agency, all operational electric ships in Europe as of 2024 use semi-autonomous systems that assist with navigation, collision avoidance, and docking but require crew oversight. Fully autonomous vessels are restricted to controlled environments such as test beds or enclosed lakes. The EU’s Maritime Autonomous Surface Ships regulatory roadmap maintains a phased approach prioritizing remote monitoring over full autonomy. As per a 2024 DNV study, most shipowners cite regulatory uncertainty as the primary reason for adopting only semi-autonomous features. This legal reality ensures that human-in-the-loop systems dominate for the foreseeable future.

The fully autonomous segment is the fastest-growing segment in the regional market with a CAGR of 33.6% over the forecast period. Military and research institutions are leading the development of fully autonomous electric ships for missions requiring endurance and reduced human risk. According to the European Defence Agency, autonomous surface vessels were commissioned by EU navies in 2024 for hydrographic survey, mine countermeasures, and environmental monitoring. Sweden’s Saab launched the Pingvin electric autonomous vessel for Baltic Sea surveillance, while the UK’s Royal Navy operates the Madfox on the Thames. These platforms operate in controlled zones with pre-approved mission parameters, bypassing commercial regulatory hurdles. As per a 2024 NATO Maritime report, defense funding accounts for the majority of fully autonomous electric ship investment in Europe, enabling rapid sensor and AI integration that will eventually trickle down to commercial use.

By Power Output Insights

The up to 745 kW power output segment occupied the leading share of 3.3% of the regional market in 2025 due to the prevalence of small passenger and service vessels on short fixed routes. Most electric water buses, tourist boats, and harbour service vessels operate on routes under 20 nautical miles, requiring modest power for low-speed manoeuvring. According to the European Maritime Safety Agency, a large majority of electric passenger vessels in service across Amsterdam, Venice, and Copenhagen are powered by systems under 700 kilowatts, which is enabling full battery operation with overnight charging. As per the Dutch Ministry of Infrastructure, the average electric canal boat uses motors in the 300 to 500 kW range, drawing daily energy well within the capacity of standard lithium battery banks. These lower power systems also reduce grid upgrade costs at charging terminals, which is making deployment feasible for municipal operators with limited infrastructure budgets. This alignment with urban operational profiles ensures continued dominance in the near term.

The 746–7560 kW segment is another promising segment and is anticipated to witness a CAGR of 27.7% over the forecast period. This power band enables electric operation on routes up to 100 nautical miles, covering key European ferry corridors like Norway’s western fjords and the Baltic Sea islands. According to the Norwegian Maritime Authority, ferries such as the Ampere class operating between Lavik and Oppedal use electric systems in the 1600 kW range and complete multiple daily crossings on a single charge. Similarly, the German Königstein electric ferry on the Elbe River uses propulsion systems above 2000 kW for medium-range routes. Reports from the European Ferry Association confirm that new medium power electric ferries were ordered in 2024 for routes connecting Denmark, Sweden, and Germany. These vessels balance range, payload, and charging feasibility, which makes them the sweet spot for commercial electrification beyond urban canals.

COUNTRY-LEVEL ANALYSIS

Norway Electric Ship Market Analysis

Norway held the leading share of 30.9% of the regional market in 2025. The dominance of Norway in the European market is driven by its fjord protection laws, renewable energy abundance, and pioneering maritime policy. As per the Norwegian Ministry of Climate and Environment, all ferries on UNESCO-protected western fjords must be zero-emission by 2026, a mandate that has already led to the deployment of electric and hybrid vessels. The country’s hydropower grid provides near carbon-free electricity, making battery operation truly sustainable. Additionally, Norway’s Enova agency has granted hundreds of millions of euros in subsidies for electric ship projects since 2020, accelerating technology adoption. With shipyards like Fjellstrand and Kongsberg delivering world firsts such as the fully electric Ampere ferry, Norway serves as both a testbed and export hub for European maritime electrification.

Germany Electric Ship Market Analysis

Germany commanded the second-largest share of the European electric ship market in 2025, with activity concentrated on inland waterways and urban river networks. According to the German Federal Ministry for Digital and Transport, dozens of electric passenger and cargo vessels operate on the Rhine, Elbe, and Spree rivers, with more on order. The National Innovation Program for Hydrogen and Fuel Cell Technology has allocated significant funding for electric ferry deployment on Lake Constance and the Berlin waterway system. Cities like Hamburg and Berlin mandate zero-emission public water transit by 2027, driving municipal investment. Additionally, German engineering firms such as Siemens and ABB supply critical electric propulsion and charging systems to the broader European market, reinforcing the country’s dual role as adopter and enabler of marine electrification.

Netherlands Electric Ship Market Analysis

The Netherlands occupied a prominent share of the European electric ship market in 2025, with leadership in urban canal electrification and port innovation. According to the Dutch Ministry of Infrastructure, all new passenger boats on Amsterdam’s canals must be zero emission from 2025, a rule that has spurred deployment of electric water taxis and tour boats. The Port of Rotterdam’s Green Barge Initiative aims to electrify its inland feeder fleet by 2030, leveraging the Netherlands’ dense inland shipping network that handles a large share of Rhine cargo. According to the reports from the Dutch Maritime Technology Association, Dutch shipyards delivered multiple electric vessels in 2024, among the highest in continental Europe. With strong EU funding and a culture of water management, the Netherlands exemplifies systemic integration of electric shipping into urban and logistics ecosystems.

France Electric Ship Market Analysis

France is expected to exhibit a healthy CAGR in the European electric ship market over the forecast period, with growth fuelled by river tourism and coastal ferry modernization. According to the French Ministry of Ecological Transition, the Voguéo electric water taxi service on the Seine received funding in 2024 to replace diesel boats in Paris. Similarly, Corsica and the French Riviera are electrifying tourist ferry routes to protect Mediterranean marine habitats. The French Agency for Energy Transition also funded the SeaZen project, deploying hydrogen electric patrol boats in Marseille. Reports from the French Shipowners’ Association confirm that new electric passenger vessels were commissioned for service on the Rhône and Seine rivers in 2024. This blend of urban sustainability and coastal preservation ensures steady demand aligned with France’s broader ecological planning framework.

Sweden Electric Ship Market Analysis

Sweden is estimated to account for a notable share of the Europe electric ship market over the forecast period, with leadership in defense and archipelago ferry electrification. According to the Swedish Transport Agency, electric ferries operate in the Stockholm archipelago, serving both residents and tourists, with plans to expand significantly by 2030. The Swedish Energy Agency notes that these vessels leverage the country’s fossil-free electricity grid for true lifecycle decarbonization. Additionally, Sweden’s defense sector is advancing fully autonomous electric vessels; Saab’s Pingvin platform conducts surveillance in the Baltic Sea without crew. A 2024 innovation grant from Vinnova supported the Green Coastal Shipping initiative to electrify freight between Gothenburg and the Baltic islands. With strong public investment and a maritime culture attuned to environmental stewardship, Sweden is a high-impact niche player driving both civilian and strategic adoption.

COMPETITIVE LANDSCAPE

Competition in the Europe electric ship market is defined by a race to deliver integrated, compliant, and scalable zero-emission solutions in a highly policy-driven environment. The market is dominated by established marine technology and industrial automation firms that compete not on individual components but on end-to-end system reliability, digital intelligence, and shore-to-ship interoperability. Barriers to entry are high due to stringent safety certifications, complex integration requirements, and long project lead times. Competition is intensifying around battery energy management, high-power charging, and predictive maintenance platforms that reduce the total cost of ownership. Unlike mass markets, success here depends on deep collaboration with shipyards, ports, and regulators to navigate fragmented infrastructure and evolving standards. While passenger ferries dominate current deployments, the race is on to adapt technologies for commercial cargo and autonomous operations. In this nascent yet strategically critical sector, competitive advantage lies in technical credibility, regulatory foresight, and ecosystem integration rather than price alone.

KEY MARKET PLAYERS

The leading companies operating in the Europe electric ship market include:

- Kongsberg

- Leclanche

- Corvus Energy

- Echandia Marine AB

- Siemens

- Vard (part of Fincantieri SpA)

- Norwegian Electric Systems

- General Dynamics Electric Boat

- MAN Energy Solutions SE

- Wartsila

- Schottel Group

- Anglo Belgian Corporation NV

- ABB Marine & Ports

- Eco Marine Power

- Akasol AG

TOP PLAYERS IN THE MARKET

- Kongsberg Maritime is a global leader in marine technology with deep integration across the Europe electric ship market through its integrated electric propulsion, energy storage, and automation systems. The company pioneered the world’s first fully electric ferry, “Ampere” in Norway and continues to supply power conversion, battery management, and remote monitoring solutions for passenger and cargo vessels across the continent. In Europe, Kongsberg has strengthened its position by launching its EVOLUTION platform, which unifies electric drive control, navigation, and energy optimization into a single digital ecosystem. Recent actions include partnerships with major European shipyards to deliver turnkey zero-emission vessel packages compliant with EU FuelEU Maritime rules, enhancing its role as a systems integrator rather than just a component supplier.

- ABB Marine & Ports delivers comprehensive electric and digital solutions for the European maritime sector with a strong footprint in ferry and inland vessel electrification. The company contributes globally by setting standards in marine battery technology, onboard DC grid systems, and shore-to-ship power connectivity. In Europe, ABB has reinforced its market presence by deploying its Onboard DC Grid technology on over 30 electric ferries in Norway and Germany, enabling greater energy efficiency and system reliability. It also expanded its ABB Ability Marine Remote Diagnostic System to provide real-time performance analytics and predictive maintenance for electric propulsion units. These innovations align with EU decarbonization goals and position ABB as a critical enabler of scalable zero-emission shipping infrastructure.

- Siemens Energy plays a pivotal role in the Europe electric ship market through its shore power infrastructure and integrated marine electrification systems. The company supplies high-power charging stations, battery energy storage, and digital grid management solutions that support both vessel operations and port decarbonization. In Europe, Siemens has strengthened its position by delivering megawatt-scale charging systems for electric ferries in Sweden, the Netherlands, and Germany, including the 4.5 MW terminal in Bergen, Norway. It also launched its eShip Connect platform, enabling real-time coordination between vessel energy demand and port grid capacity. These actions ensure Siemens remains central to the shore-side ecosystem that makes electric shipping operationally viable across Europe’s dense waterway network.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe electric ship market prioritize integrated system solutions combining electric propulsion, energy storage, and digital monitoring to ensure performance reliability and regulatory compliance. They form strategic partnerships with shipyards and port authorities to deliver turnkey zero-emission vessel and infrastructure packages. Companies invest in megawatt-scale shore charging technology compatible with EU grid standards to enable opportunity charging on short routes. They leverage digital platforms for remote diagnostics, energy optimization, and carbon reporting to enhance lifecycle value. Additionally, they align product development with EU FuelEU Maritime and Alternative Fuels Infrastructure Regulation mandates to secure public and private procurement opportunities in a policy-driven market.

MARKET SEGMENTATION

This research report on the Europe electric ship market has been segmented and sub-segmented into the following categories.

By Ship Type

- Commercial Ship

- Passenger Ship

By Mode of Operation

- Semi-autonomous

- Fully Autonomous

By Power Output

- Up to 745 kW

- 746-7560 kW

- Above 7560 kW

By Propulsion Type

- Hybrid

- Fully Electric

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe electric ship market?

The Europe electric ship market encompasses battery and hybrid vessels for commercial and defense use. Fully electric and hybrid types reduce emissions in ferries and support vessels.

What drives growth in the Europe electric ship market?

Stringent EU emissions regulations and green port initiatives drive the Europe electric ship market. Investments in battery tech support ferry and short-sea shipping electrification.

How is the Europe electric ship market segmented?

The Europe electric ship market segments by type into fully electric and hybrid, plus ship types like ferries, tankers, and offshore vessels for varied maritime needs.

Which countries lead the Europe electric ship market?

Germany and Norway lead the Europe electric ship market with ferry deployments and infrastructure. UK emerges fast through tech investments and policy support.

What role do ferries play in the Europe electric ship market?

Ferries dominate the Europe electric ship market due to frequent port charging. Norway's short-haul routes showcase viable zero-emission operations.

Why hybrid ships grow in the Europe electric ship market?

Hybrid ships expand the Europe electric ship market blending electric and diesel for longer ranges. They suit commercial routes with IMO sulfur compliance.

What applications define the Europe electric ship market?

Applications in the Europe electric ship market include passenger ferries, cargo, and offshore support. Defense segments adopt for quiet, emission-free missions.

What challenges hinder the Europe electric ship market?

Challenges in the Europe electric ship market involve battery limitations and charging infrastructure gaps. High upfront costs slow long-haul adoption.

How do regulations shape the Europe electric ship market?

EU Fit for 55 and IMO targets propel the Europe electric ship market mandating low-emission shipping. Incentives fund retrofits and newbuilds.

What innovations boost the Europe electric ship market?

Battery advancements and hydrogen fuel cells innovate the Europe electric ship market. They extend range and efficiency for commercial viability.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com