Europe Enteral Feeding Formulas Market Research Report - Segmented By Product (Polymeric, Monomeric, Disease-Specific Formulas), Stage, Application, End User and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis From 2024 to 2033

Europe Enteral Feeding Formulas Market Report Summary

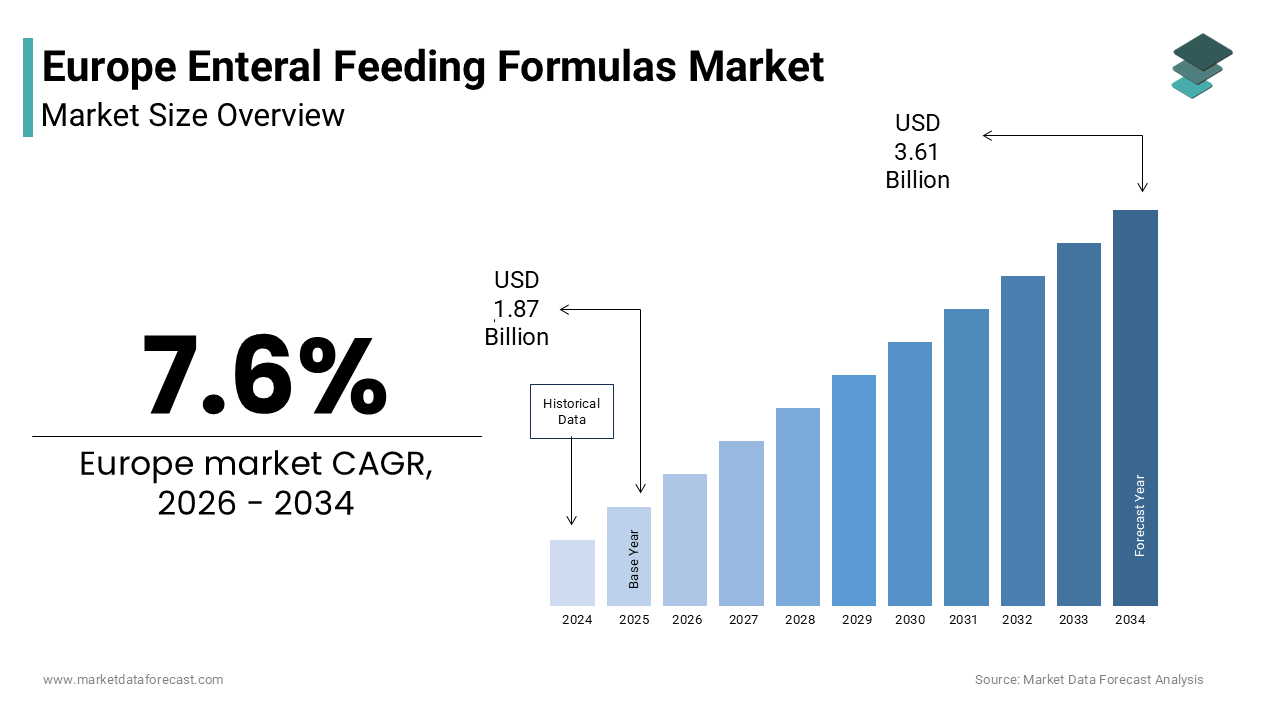

The Europe enteral feeding formulas market was valued at USD 1.87 billion in 2025, is estimated to reach USD 2.01 billion in 2026, and is projected to reach USD 3.61 billion by 2034, growing at a CAGR of 7.6% during the forecast period from 2026 to 2034. The growth of the Europe enteral feeding formulas market is driven by the rapidly expanding geriatric population, rising prevalence of chronic diseases, and increasing demand for clinical nutritional support across hospital and home care settings. Growing adoption of home enteral nutrition programs, increasing awareness regarding malnutrition management, and advancements in enteral feeding technologies are further accelerating market growth. Moreover, integration of smart feeding systems, expansion of disease-specific nutritional formulations, and increasing healthcare expenditure across European countries are supporting the expansion of the Europe enteral feeding formulas market.

Key Market Trends

- Rising adoption of home enteral nutrition programs supported by portable feeding pumps and community-based healthcare models.

- Growing demand for disease-specific enteral formulas targeting oncology, neurology, renal, and gastrointestinal disorders.

- Increasing integration of smart feeding technologies with remote monitoring and automated flow regulation capabilities.

- Strong focus on personalized nutrition and patient-centered enteral feeding solutions across European healthcare systems.

- Expansion of digital health platforms and connected care systems to improve nutritional monitoring and patient compliance.

Segmental Insights

- Based on product, the polymeric formulas segment dominated the Europe enteral feeding formulas market and held the largest share in 2025. The segment’s dominance is attributed to its comprehensive nutritional profile, broad clinical applicability, cost effectiveness, and widespread use in patients with functional gastrointestinal tracts requiring complete nutritional support.

- Based on stage, the adult segment accounted for the leading share of the Europe enteral feeding formulas market in 2025. The dominance of this segment is driven by the large aging population, increasing prevalence of chronic and neurological disorders, and rising demand for nutritional support among hospitalized and long-term care patients.

- Based on application, the oncology segment held the major share of the Europe enteral feeding formulas market in 2025 owing to the high prevalence of cancer-related malnutrition, increasing use of enteral nutrition during cancer therapy, and growing integration of nutritional support into oncology care pathways.

- Based on end user, the hospitals segment dominated the Europe enteral feeding formulas market in 2025 due to the high concentration of acute care patients, structured nutritional support protocols, and extensive use of enteral nutrition in intensive care, oncology, and surgical units.

- The home care segment is projected to witness the fastest CAGR during the forecast period owing to healthcare policy shifts favoring community-based care, increasing patient preference for home treatment, and technological advancements enabling safe home enteral nutrition delivery.

Regional Insights

Germany dominated the Europe enteral feeding formulas market and accounted for the largest share in 2025, supported by its advanced healthcare infrastructure, strong reimbursement framework, and high prevalence of elderly patients requiring nutritional support interventions. France remains a major contributor to the market due to its comprehensive healthcare coverage, established home enteral nutrition programs, and growing emphasis on clinical nutrition management. The United Kingdom continues to maintain a prominent position owing to strong National Health Service support for enteral nutrition therapies, integrated care pathways, and increasing prevalence of chronic diseases requiring nutritional intervention. Italy and Spain are also witnessing notable growth driven by demographic aging, increasing healthcare expenditure, and expanding awareness regarding malnutrition management and clinical nutrition therapies.

Competitive Landscape

The Europe enteral feeding formulas market is highly competitive and characterized by the presence of multinational nutrition companies, medical device manufacturers, and specialized clinical nutrition providers competing through product innovation, clinical evidence generation, and digital health integration. Leading companies are focusing on expanding disease-specific nutritional portfolios, strengthening home care support services, investing in smart feeding technologies, and enhancing personalized nutrition capabilities. Strategic collaborations with healthcare providers, clinical nutrition societies, and digital health platforms are further strengthening market positioning across European healthcare systems. Prominent players in the Europe enteral feeding formulas market include Abbott Laboratories, Nestlé S.A., Danone S.A., Fresenius Kabi AG, Mead Johnson Nutrition Company, B. Braun Melsungen AG, Hormel Foods, LLC, Victus Inc., Meiji Holdings Co., Ltd., and Global Health Product Inc.

Europe Enteral Feeding Formulas Market Size

The European enteral feeding formulas market size was valued at USD 1.87 billion in 2025 and is anticipated to reach USD 2.01 billion in 2026 from USD 3.61 billion by 2034, growing at a CAGR of 7.6% during the forecast period from 2026 to 2034.

Enteral feeding formulas devices refer to the combined systems used to deliver liquid nutrition directly into a patient's digestive tract. This specialized healthcare segment addresses critical nutritional needs across hospital settings, long term care facilities, and home care environments. The clinical necessity for these interventions stems from profound demographic and epidemiological shifts across the European continent. According to Eurostat, the proportion of individuals aged 65 and above reached 21 percent of the European Union population in 2020, representing a five percentage point increase since 2001. As per the OECD Health at a Glance: Europe 2024 report, demographic shifts have seen the 65+ population rise to over 21%, with more than 40% of these individuals suffering from multiple chronic conditions that significantly increase the risk of malnutrition. The European Society for Clinical Nutrition and Metabolism (ESPEN) indicates that malnutrition prevalence among older adults varies significantly by care setting, ranging from under 10% in community dwellings to over 60% in hospital environments, necessitating structured nutritional interventions. Current healthcare expenditure in the European Union amounted to 1720 billion euros in 2023, equivalent to 10.0 percent of gross domestic product according to Eurostat statistics. These demographic pressures and clinical requirements establish a foundational context for enteral nutrition solutions that support patient recovery, manage chronic conditions, and maintain quality of life across diverse care pathways.

MARKET DRIVERS

Expanding Geriatric Population With Elevated Nutritional Vulnerability

The accelerating growth of the region's elderly demographic is a fundamental driver of the Europe enteral feeding formulas devices market. According to Eurostat data, individuals aged 80 and above nearly doubled their population share between 2001 and 2020, reaching almost 6 percent of the total European Union population. This demographic transition correlates directly with increased prevalence of dysphagia, neurological impairments, and functional decline that compromise oral intake capacity. The European Society for Clinical Nutrition and Metabolism documents that older adults in hospital settings demonstrate malnutrition prevalence ranging from 20 to 50 percent, necessitating structured nutritional support protocols. Geriatric patients frequently require prolonged enteral nutrition during recovery from acute events such as stroke, hip fracture, or surgical interventions, creating sustained demand for reliable feeding devices and specialized formulas. Healthcare systems across Germany, France, and Italy report increasing admissions of elderly patients requiring nutritional assessment and intervention upon hospital entry. The convergence of extended life expectancy, multimorbidity patterns, and age related physiological changes establishes a persistent clinical requirement for enteral feeding solutions that support nutritional status, preserve muscle mass, and facilitate rehabilitation outcomes across European care environments.

Rising Burden Of Chronic Diseases Requiring Nutritional Support

The escalating prevalence of chronic conditions across the region generates substantial demand for these devices, and thereby boosts the expansion of the Europe enteral feeding formulas devices market. These products serve as integral components of disease management protocols. According to widely cited data from European health initiatives like the ICARE4EU project, an estimated 50 million people in the European Union live with multiple chronic diseases, creating complex clinical scenarios where oral nutrition becomes heavily compromised. As per the European Union health statistics, conditions such as cancer, neurological disorders, chronic obstructive pulmonary disease, and gastrointestinal pathologies frequently impair swallowing function or increase metabolic demands beyond oral intake capacity. The European Cancer Observatory reports that cancer incidence continues to rise across member states, with many patients experiencing treatment related mucositis, dysphagia, or cachexia requiring enteral nutritional support. Neurological conditions including Parkinson disease, amyotrophic lateral sclerosis, and advanced dementia affect millions of Europeans and commonly necessitate long term enteral feeding arrangements. Clinical literature from tertiary care networks indicates that while specialized enteral nutrition is standard for patients with severe swallowing disorders or critical organ failures, the precise integration rate across the broader spectrum of advanced chronic illnesses varies significantly based on individual disease trajectories. The integration of nutritional therapy into standard treatment pathways for chronic disease management reflects growing clinical recognition that adequate nutrition improves treatment tolerance, reduces complications, and enhances quality of life. This epidemiological reality drives consistent utilization of enteral feeding devices across acute care, rehabilitation, and community settings throughout Europe.

MARKET RESTRAINTS

Device Related Complications And Infection Control Concerns

Clinical complications associated with enteral feeding devices are a significant restraint to the growth of the Europe enteral feeding formulas devices market. This affects market expansion across the regional healthcare settings. Clinical studies indicate that tube clogging remains a notable mechanical complication, occurring in up to 25% of enteral feeding cases, which requires proper flushing protocols to avoid device replacement and interruptions in nutritional delivery. As per infection surveillance data from European hospital networks, peristomal wound infections at the insertion site are a known risk for patients receiving long-term enteral nutrition via gastrostomy tubes, while catheter-related bloodstream infections remain a critical risk factor tied primarily to long-term parenteral (intravenous) nutrition. Aspiration pneumonia remains a critical concern among critically ill patients receiving enteral feeding, where incidence rates vary significantly in clinical literature based on whether patients are intubated, highlighting the importance of strict patient positioning and feeding rate protocols. Caregiver training variability across home care environments introduces additional risk, as improper tube maintenance or formula handling can precipitate contamination events. The European Centre for Disease Prevention and Control emphasizes that healthcare associated infections related to medical devices impose substantial burden on patient safety systems and resource allocation. Regulatory authorities across member states maintain stringent post market surveillance requirements for enteral devices, meaning that any safety signal triggers comprehensive review processes that may temporarily limit product availability. These clinical realities necessitate continuous staff education, protocol standardization, and device innovation to mitigate complications while maintaining therapeutic efficacy across diverse European care contexts.

Stringent Regulatory Compliance Requirements Under European Frameworks

The complex regulatory landscape governing medical devices and nutritional products in the region creates substantial compliance burdens that can hinder the expansion of the Europe enteral feeding formulas devices market. According to the European Commission's implementation of the Medical Device Regulation 2017 slash 745, enteral feeding devices now face more rigorous conformity assessment procedures, clinical evidence requirements, and post market surveillance obligations compared to previous regulatory frameworks. As per frameworks outlined by the European Food Safety Authority (EFSA) under Regulation (EU) No 609/2013, enteral nutrition formulas classified as foods for special medical purposes (FSMP) must adhere to strict, codified nutritional compositions, safety profiles, and labeling standards. The transition to these enhanced MDR requirements has significantly extended product development and certification timelines for many manufacturers, driven by a industry-wide bottleneck in European Notified Body capacities. Small and medium enterprises particularly face resource challenges in navigating the expanded documentation, clinical investigation, and quality management system expectations. Furthermore, national competent authorities across member states may interpret regulatory provisions differently, creating fragmentation in approval pathways and market access strategies. The requirement for unique device identification, electronic product registration, and continuous benefit risk evaluation adds operational complexity and cost to product lifecycle management. These regulatory enhancements ultimately strengthen patient safety and product quality. However, the transitional burden and ongoing compliance demands can moderate the pace of innovation deployment and market entry for new enteral feeding solutions across European healthcare systems.

MARKET OPPORTUNITIES

Expansion Of Home Enteral Nutrition Programs Across European Healthcare Systems

The strategic shift toward community-based care models offers substantial growth potential for the Europe enteral feeding formulas devices market. According to multi-country registry reviews published in Clinical Nutrition, the incidence and prevalence of home enteral nutrition (HEN) vary widely across European nations due to differing clinical practices, showcasing massive untapped market capacity in multiple regions. As per healthcare policy analyses from the European Observatory on Health Systems and Policies, countries including Germany, France, and the United Kingdom have implemented structured reimbursement frameworks that support early hospital discharge with continued enteral nutrition management in home settings. The European Society for Clinical Nutrition and Metabolism advocates for standardized home enteral nutrition protocols that improve patient autonomy while reducing institutional care costs. Technological advancements in portable feeding pumps, low profile gastrostomy devices, and user friendly administration sets enhance feasibility of home based therapy for patients with neurological conditions, head and neck cancers, or chronic gastrointestinal disorders. Clinical literature from European healthcare providers indicates that well-supported home enteral nutrition programs significantly reduce hospital readmission rates, while simultaneously driving measurable improvements in patient satisfaction and overall quality of life metrics. The growing preference for aging in place among European seniors aligns with clinical capabilities to deliver safe, effective enteral nutrition outside traditional facilities. Payers increasingly recognize that appropriate home based nutritional support prevents complications, maintains functional status, and optimizes resource utilization across integrated care pathways. This convergence of clinical evidence, policy support, and patient preference establishes favorable conditions for expanded adoption of enteral feeding solutions in community environments throughout Europe.

Technological Innovations In Smart Feeding Systems And Connected Care

Emerging technological capabilities create meaningful opportunities for differentiation and value creation within the Europe enteral feeding formulas devices market. According to innovation analyses from European medical technology clusters, next generation enteral feeding systems increasingly incorporate smart sensors, wireless connectivity, and data analytics to enhance safety, personalization, and care coordination. As per research published in the Journal of Medical Engineering and Technology, prototype systems featuring automated flow regulation, aspiration detection algorithms, and remote monitoring interfaces demonstrate potential to reduce complications and support proactive clinical intervention. The integration of enteral feeding devices with electronic health records enables real time documentation of nutritional delivery, tolerance parameters, and patient outcomes across care transitions. Manufacturers are developing ENFit compatible connectors, anti reflux mechanisms, and compact pump designs that improve usability for patients and caregivers in diverse settings. Artificial intelligence applications show promise for predicting feeding intolerance, optimizing formula selection based on metabolic profiles, and alerting clinicians to potential adverse events before clinical deterioration occurs. The European Innovation Council and other funding mechanisms support development of digital health solutions that address unmet needs in chronic disease management and aging populations. Healthcare systems increasingly value technologies that generate actionable data, support evidence based practice, and facilitate value based reimbursement models. These innovation trajectories position technologically advanced enteral feeding solutions to capture growing demand for precision nutrition, remote care enablement, and outcomes focused therapeutic interventions across European healthcare environments.

MARKET CHALLENGES

Shortage Of Trained Healthcare Professionals For Device Management

Workforce constraints are a persistent hurdle affecting the optimal utilization of these devices across regional healthcare settings, which holds back the growth of the Europe enteral feeding formulas devices market. According to workforce analyses from the European Observatory on Health Systems and Policies, many member states report shortages of nurses, dietitians, and allied health professionals with specialized training in enteral nutrition assessment, device placement, and ongoing management. As per staffing data from national health services, rural regions and long term care facilities experience particularly acute gaps in personnel qualified to initiate and monitor enteral feeding protocols safely. The European Society for Clinical Nutrition and Metabolism emphasizes that appropriate enteral nutrition delivery requires multidisciplinary expertise encompassing clinical assessment, formula selection, device troubleshooting, and complication prevention. Training variability among community based caregivers further complicates home enteral nutrition programs, potentially affecting adherence, safety, and clinical outcomes. Workforce pressures within publicly funded healthcare systems, combined with increasing patient volumes and acuity, can delay timely initiation of enteral nutrition or limit capacity for comprehensive follow up. Educational institutions across Europe are expanding curricula to address these competency gaps, yet curriculum development, faculty recruitment, and clinical placement logistics require sustained investment and coordination. The challenge intensifies as demographic aging increases demand for enteral nutrition services while workforce retirement rates accelerate in many European countries. Addressing this human resource constraint requires strategic investment in education, standardized competency frameworks, and innovative care models that leverage technology to extend specialist expertise across broader care networks throughout Europe.

Reimbursement Variability Across European Healthcare Systems

Heterogeneous reimbursement policies create market access complexities for the Europe enteral feeding formulas devices market. Consequently, this challenges consistent patient access and manufacturer planning across Europe. According to health technology assessment reviews from the European Network for Health Technology Assessment, coverage criteria, reimbursement rates, and documentation requirements for enteral nutrition products vary substantially among member states and sometimes within national regions. As per policy analyses from the European Observatory on Health Systems and Policies, some healthcare systems provide comprehensive coverage for enteral formulas and devices across care settings, while others impose restrictive criteria, prior authorization processes, or patient cost sharing that may limit utilization. The classification of enteral products as medical devices, foods for special medical purposes, or pharmaceuticals triggers different regulatory and reimbursement pathways, adding administrative burden for providers and manufacturers. Budget constraints within publicly funded systems can lead to formulary restrictions or tender processes that prioritize cost over clinical nuance, potentially affecting product availability and innovation incentives. Cross border care scenarios introduce additional complexity when patients transition between healthcare systems with differing coverage policies. Manufacturers must navigate diverse health technology assessment methodologies, pricing negotiations, and contracting arrangements across multiple jurisdictions, increasing market entry costs and timeline uncertainty. While European Union initiatives aim to enhance cooperation on health technology assessment and rare disease coverage, substantial national autonomy in reimbursement decision making persists. This fragmentation challenges efforts to ensure equitable patient access to appropriate enteral nutrition solutions and complicates strategic planning for stakeholders throughout the European enteral feeding formulas devices ecosystem.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.6% |

| Segments Covered | By Product, Stage, Application, End User and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe. |

| Market Leaders Profiled | Abbott Laboratories (U.S.), Nestlé S.A. (Switzerland), Danone S.A. (France), Fresenius Kabi AG (Germany), Mead Johnson Nutrition Company (U.S.), B. Braun Melsungen AG (Germany), Hormel Foods, LLC (U.S.), Victus Inc. (U.S.), Meiji Holdings Co., Ltd. (Japan), and Global Health Product Inc. (U.S.). |

SEGMENTAL ANALYSIS

By Product Insights

In 2025, the polymeric formulas segment was the largest by occupying a 62.3% share of the Europe enteral feeding formulas devices market. Its comprehensive nutritional profile and broad clinical applicability support the prominence of this segment. As per the European Society for Clinical Nutrition and Metabolism, polymeric formulas containing intact proteins, complex carbohydrates, and complete lipid profiles support patients with functional gastrointestinal tracts who require complete nutrition without specialized hydrolysis. The cost effectiveness of polymeric formulas compared to specialized alternatives drives their preference in publicly funded healthcare systems across Germany, France, and the United Kingdom. Clinical guidelines from ESPEN recommend polymeric formulas as first line nutritional support for patients without severe malabsorption, reinforcing their dominant utilization patterns. Healthcare providers value the standardized composition and predictable tolerance profiles of polymeric products, which simplify protocol development and staff training across diverse care environments. The availability of multiple caloric densities and fiber enriched variants further enhances clinical flexibility, enabling personalized nutrition strategies while maintaining procurement efficiency within institutional formularies throughout Europe.

On the contrary, the disease specific formulas segment is estimated to register the fastest CAGR of 8.7% between 2026 and 2034 due to increasing clinical recognition that targeted nutritional interventions improve outcomes in patients with cancer, diabetes, renal impairment, and pulmonary conditions. As per European Commission cancer registries, approximately 2.7 million new cancer cases were diagnosed across the EU in 2022, driving a notable requirement for specialized disease-specific formulas that address cachexia, treatment-related mucositis, or altered metabolic demands. The European Renal Association (ERA) reports that approximately 700,000 individuals receive renal replacement therapy (RRT) across Europe, creating a strong, sustained demand for renal-specific enteral formulas with strictly controlled electrolyte and protein distributions for those undergoing active dialysis. Manufacturers are investing in clinical evidence generation to demonstrate that disease tailored formulas reduce complications, shorten hospital stays, and improve quality of life metrics compared to standard polymeric products. Reimbursement frameworks in countries such as Germany and France increasingly recognize the value based benefits of specialized nutrition, facilitating market access for innovative disease specific formulations. This convergence of epidemiological need, clinical evidence, and policy support positions disease specific formulas for sustained above market growth throughout the European healthcare landscape.

By Stage Insights

The adult patients segment held the majority share of the Europe enteral feeding formulas devices market in 2025. This supremacy of the segment was credited to the substantially larger population of adults requiring enteral nutrition support compared to pediatric cohorts across European healthcare systems. According to Eurostat demographic structure data, adults constitute the vast majority of the European Union population, with aggressive population aging trends intensifying the clinical demand for structured nutritional interventions. Hospital utilization data across leading European nations indicates that adult patients represent the overwhelming majority of enteral nutrition initiations, heavily driven by pathologies like stroke, oncology, and progressive neurological conditions that limit oral intake capacity. Clinical protocols in acute care and long term facilities prioritize adult nutritional assessment and intervention, reinforcing utilization patterns that sustain the segment's market leadership. The convergence of demographic aging, chronic disease burden, and established care pathways ensures that adult patients will continue to drive the majority of enteral feeding formulas demand throughout Europe.

On the other hand, the pediatric stage segment is anticipated to witness the fastest CAGR of 6.2% during the forecast period. This accelerated expansion is propelled by increasing survival rates among preterm neonates and children with complex congenital conditions who require specialized enteral nutrition support. According to neonatological literature aligned with ESPGHAN guidelines, a substantial percentage of very preterm infants born before 32 weeks gestation exhibit feeding intolerance or severe gastrointestinal complications, necessitating early tube feeding interventions. Data compiled by European rare disease networks demonstrates that thousands of children across member states navigate chronic conditions like short bowel syndrome, cystic fibrosis, or complex neuromuscular diseases, necessitating highly specialized pediatric enteral nutrition formulas. Manufacturers are developing pediatric specific formulas with adjusted macronutrient ratios, enhanced micronutrient profiles, and age appropriate delivery systems that support growth and development while minimizing complications. Healthcare systems in the United Kingdom, Netherlands, and Scandinavia have implemented structured pediatric enteral nutrition programs that facilitate early hospital discharge with continued home based support. This combination of clinical need, product innovation, and care model evolution positions the pediatric segment for sustained above market growth across European healthcare environments.

By Application Insights

The oncology segment led the Europe enteral feeding formulas devices market and captured a 26.2% share in 2025. This leading position of the segment was attributed to the substantial cancer burden across Europe and the integral role of nutritional support in comprehensive oncology care pathways. As per European Commission cancer registries, approximately 2.7 million new cancer cases were diagnosed across European Union member states in 2022, with many patients experiencing treatment-related dysphagia, mucositis, or cachexia that compromise oral intake capacity. The European Society for Medical Oncology emphasizes that malnutrition affects 40 to 80 percent of cancer patients depending on tumor type and treatment modality, creating sustained demand for enteral nutritional interventions. Clinical guidelines from ESPEN recommend early nutritional assessment and enteral support for patients undergoing head and neck, gastrointestinal, or pancreatic cancer treatments to maintain treatment tolerance and preserve functional status. Healthcare providers in tertiary cancer centers report that while enteral nutrition rates are exceptionally high among specific cohorts, such as those with head, neck, and upper gastrointestinal malignancies, the exact clinical utilization varies significantly across the broader oncology segment's market landscape. The integration of nutritional therapy into standard oncology protocols across Germany, France, and the United Kingdom ensures continued dominance of this application segment throughout the European market landscape.

On the contrary, the neurology application segment is likely to experience the fastest CAGR of 9.1% from 2026 to 2034 owing to the rising prevalence of neurological conditions that impair swallowing function and necessitate long term enteral nutrition support. As per demographic data aligned with the European Brain Council (EBC), neurological and brain disorders affect an estimated 165 million individuals across Europe, with conditions such as stroke, Parkinson's disease, amyotrophic lateral sclerosis (ALS), and advanced dementia frequently compromising oral intake capacity. The European Stroke Organisation (ESO) reports that approximately 1.1 million stroke events occur annually across the European Union, with dysphagia affecting 30% to 50% of acute stroke patients and often requiring temporary or permanent enteral feeding arrangements. Clinical evidence from multicenter European studies demonstrates that timely enteral nutrition initiation improves neurological recovery outcomes, reduces aspiration pneumonia risk, and preserves muscle mass during rehabilitation. Healthcare systems are expanding home enteral nutrition programs for patients with progressive neurological conditions, creating sustained demand for reliable feeding devices and specialized formulas. This convergence of epidemiological trends, clinical evidence, and care model evolution positions the neurology application segment for sustained above market growth throughout European healthcare settings.

By End User Insights

The hospitals segment dominated the Europe enteral feeding formulas devices market and accounted for a 58.6% share in 2025. This dominance of the segment was driven by the concentration of acute care patients requiring intensive nutritional support and the structured procurement processes within institutional healthcare settings. As per Eurostat health expenditure data, provider-level hospital care accounts for approximately 36.8% of total healthcare spending across European Union member states, serving as a primary inpatient environment for complex enteral nutrition delivery. Healthcare providers in major medical centers report that 25% to 40% of admitted patients present a high risk of malnutrition, requiring structured clinical assessments and potential enteral interventions during their hospital stay. Public procurement frameworks in Germany, France, and Italy favor established suppliers with comprehensive product portfolios and robust supply chain capabilities, reinforcing market concentration among leading manufacturers. The integration of nutritional therapy into standard care pathways across intensive care, oncology, and surgical units ensures that hospitals will continue to drive the majority of enteral feeding formulas demand throughout Europe.

However, the home care settings segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 7.8% over the forecast period. This rapid growth is fuelled by healthcare policy shifts favoring community based care models and technological advancements enabling safe home enteral nutrition delivery. As per the European Observatory on Health Systems and Policies, countries including Germany, France, and the United Kingdom have implemented structured reimbursement frameworks that support early hospital discharge with continued enteral nutrition management in home environments. Multi-country data published across Clinical Nutrition indicates that home enteral nutrition incidence varies dramatically between European nations due to regional differences in clinical infrastructure, highlighting massive untapped growth capacity in underserved regions. The European Society for Clinical Nutrition and Metabolism advocates for standardized home enteral nutrition protocols that improve patient autonomy while reducing institutional care costs. Technological innovations in portable feeding pumps, low profile gastrostomy devices, and user friendly administration sets enhance feasibility of home based therapy for patients with neurological conditions, head and neck cancers, or chronic gastrointestinal disorders. Clinical literature shows that well-supported home enteral nutrition programs significantly reduce hospital readmission rates, while simultaneously driving measurable advancements in outpatient compliance and patient quality of life metrics. This convergence of policy support, clinical evidence, and technological enablement positions home care settings for sustained above market growth throughout European healthcare systems.

REGIONAL ANALYSIS

Germany Enteral Feeding Formulas Devices Market Analysis

Germany outperformed other countries in the Europe enteral feeding formulas devices market and accounted for a 22.4% share in 2025. This position of the German market was driven by its robust healthcare infrastructure, high healthcare expenditure per capita, and substantial aging population requiring nutritional support interventions. As per Federal Statistical Office of Germany (Destatis) data, individuals aged 65 and above represented 22.4% of the German population in 2023, with long-term forecasts indicating that one in four residents will be over the age of 67 by 2035, heavily expanding the regional requirement for enteral nutrition solutions. The German Society for Nutritional Medicine (DGEM) notes that up to 30% of all hospital patients suffer from undernutrition, with targeted clinical registries showing that malnutrition impacts over 40% of hospitalised geriatric patients, underscoring a critical demand for structured nutritional screening. Germany's statutory health insurance system provides comprehensive coverage for enteral feeding formulas and devices across hospital and home care settings, facilitating consistent patient access and manufacturer market participation. Leading manufacturers including Fresenius Kabi and B Braun maintain significant production and distribution capabilities within Germany, reinforcing supply chain efficiency and clinical support infrastructure. The integration of nutritional therapy into standard care pathways across university hospitals, community facilities, and long term care institutions ensures Germany's continued market leadership throughout the European enteral feeding formulas landscape.

France Enteral Feeding Formulas Devices Market Analysis

France was the next prominent country within the Europe enteral feeding formulas devices market and occupied a 16.8% share in 2025 because of its comprehensive healthcare coverage system, advanced clinical nutrition practices, and growing emphasis on home based care models. As per INSEE demographic data, the proportion of French residents aged 75 and above increased from 9 percent in 2010 to 11 percent in 2023, with continued aging trends intensifying demand for enteral nutrition interventions. The French Society for Clinical Nutrition and Metabolism indicates that malnutrition prevalence ranges from 30 to 50 percent among hospitalized older adults, reinforcing clinical guidelines that prioritize nutritional assessment and support. France's national health insurance framework provides reimbursement for enteral feeding formulas and devices across acute care, rehabilitation, and community settings, facilitating consistent patient access and manufacturer participation. Companies such as Danone and Nestlé Health Science maintain significant research, production, and distribution capabilities within France, supporting innovation and clinical education initiatives. The expansion of structured home enteral nutrition programs across French regions creates additional growth opportunities for device manufacturers and formula suppliers. This combination of demographic pressures, clinical recognition, and policy support positions France as a sustained high value market within the European enteral feeding formulas ecosystem.

United Kingdom Enteral Feeding Formulas Devices Market Analysis

The United Kingdom continues to be a major player in the Europe enteral feeding formulas devices market owing to its established healthcare infrastructure, strong clinical nutrition guidelines, and integrated care pathways that support enteral nutrition delivery. As per Office for National Statistics (ONS) data, individuals aged 65 and above accounted for approximately 18.6% of the United Kingdom population in 2023, with long-term forecasts pointing toward this segment approaching nearly 24% of the population closer to mid-century. The British Association for Parenteral and Enteral Nutrition reports that malnutrition affects approximately 3 million individuals across the United Kingdom, with prevalence exceeding 30 percent among hospitalized older adults. The National Health Service provides comprehensive coverage for enteral feeding formulas and devices across hospital and community settings, facilitating consistent patient access and manufacturer market participation. Leading manufacturers maintain significant distribution and clinical support capabilities within the United Kingdom, reinforcing supply chain efficiency and healthcare provider engagement. The integration of nutritional therapy into standard care pathways across acute care, rehabilitation, and long term care facilities ensures the United Kingdom's continued relevance within the European enteral feeding formulas market landscape.

Italy Enteral Feeding Formulas Devices Market Analysis

Italy holds a noteworthy position in the Europe enteral feeding formulas devices market due to its substantial aging population, established healthcare infrastructure, and growing recognition of clinical nutrition importance within care pathways. As per Italian National Institute of Statistics data, individuals aged 65 and above represented 24 percent of the Italian population in 2023, with this proportion projected to exceed 30 percent by 2035, intensifying demand for enteral nutrition solutions. The Italian Society for Parenteral and Enteral Nutrition indicates that malnutrition prevalence ranges from 20 to 40 percent among hospitalized older adults, reinforcing clinical guidelines that prioritize nutritional assessment and intervention. Italy's national health service provides reimbursement for enteral feeding formulas and devices across acute care and community settings, facilitating patient access and manufacturer participation. Regional healthcare authorities in Lombardy, Lazio, and Campania maintain structured procurement processes that favor established suppliers with comprehensive product portfolios. The expansion of home enteral nutrition programs across Italian regions creates additional growth opportunities for device manufacturers and formula suppliers. This combination of demographic pressures, clinical recognition, and policy support positions Italy as a sustained growth market within the European enteral feeding formulas ecosystem.

Spain Enteral Feeding Formulas Devices Market Analysis

Spain is estimated to register a healthy CAGR in the Europe enteral feeding formulas devices market over the forecast period owing to its aging demographic profile, evolving healthcare infrastructure, and increasing emphasis on nutritional support within clinical care pathways. According to the Spanish National Statistics Institute (INE), individuals aged 65 and above constituted 20.1% of the Spanish population in 2023, with progressive aging projections pointing toward this share climbing past 26% over the next two decades. The Spanish Society for Parenteral and Enteral Nutrition reports that malnutrition affects approximately 25 to 45 percent of hospitalized older adults, reinforcing clinical guidelines that prioritize nutritional assessment and structured intervention protocols. Spain's national health system provides coverage for enteral feeding formulas and devices across hospital and community settings, facilitating consistent patient access and manufacturer market participation. Leading manufacturers maintain distribution and clinical support capabilities within Spain, reinforcing supply chain efficiency and healthcare provider engagement. The integration of nutritional therapy into standard care pathways across acute care, rehabilitation, and long term care facilities ensures Spain's continued relevance within the European enteral feeding formulas market landscape.

COMPETITIVE LANDSCAPE

The Europe enteral feeding formulas devices market features a moderately consolidated competitive landscape characterized by established multinational corporations and specialized regional players. Leading manufacturers leverage comprehensive product portfolios, robust clinical evidence, and extensive distribution networks to maintain market leadership across hospital and home care settings. Competition centers on product innovation, clinical outcomes demonstration, and value based differentiation rather than price alone, reflecting the clinical criticality of enteral nutrition interventions. Regulatory compliance under the European Medical Device Regulation creates substantial barriers to entry that favor incumbent players with established quality management systems and post market surveillance capabilities. Strategic acquisitions and partnerships enable manufacturers to expand therapeutic indications, enhance technological capabilities, and strengthen geographic presence across diverse European healthcare systems. Emerging companies focus on niche applications, digital health integration, or sustainable formulation approaches to capture growth opportunities within specific market segments. The convergence of demographic aging, chronic disease burden, and healthcare system transformation sustains demand for enteral nutrition solutions while intensifying competition on clinical value, patient experience, and operational efficiency throughout the European market landscape.

KEY MARKET PLAYERS

Companies playing a leading role in the European enteral feeding formulas market include

- Abbott Laboratories (U.S.)

- Nestlé S.A. (Switzerland)

- Danone S.A. (France)

- Fresenius Kabi AG (Germany)

- Mead Johnson Nutrition Company (U.S.)

- B. Braun Melsungen AG (Germany)

- Hormel Foods, LLC (U.S.)

- Victus Inc. (U.S.)

- Meiji Holdings Co., Ltd. (Japan)

- Global Health Product Inc. (U.S.)

Top Market Players

Fresenius Kabi AG

Fresenius Kabi AG maintains a prominent position in the Europe enteral feeding formulas devices market through its comprehensive portfolio of clinical nutrition products and enteral delivery systems. The company leverages its German headquarters and extensive European manufacturing footprint to ensure reliable supply chain operations and rapid response to clinical needs. Fresenius Kabi invests substantially in research and development to advance disease specific formulations, smart feeding technologies, and patient centered delivery systems that address evolving healthcare requirements. The company collaborates with European clinical societies to support education initiatives and evidence generation that reinforce best practices in enteral nutrition management. Recent strategic actions include expansion of production capabilities for specialized formulas and enhancement of digital health integration features within feeding devices. Fresenius Kabi's commitment to quality, innovation, and clinical partnership strengthens its competitive position across hospital and home care settings throughout Europe.

Nestlé Health Science

Nestlé Health Science contributes significantly to the Europe enteral feeding formulas devices market through its specialized medical nutrition portfolio and patient focused innovation approach. The company leverages global research capabilities and European clinical insights to develop targeted nutritional solutions for oncology, neurology, and gastrointestinal conditions. Nestlé Health Science maintains strong relationships with healthcare providers and payers across European markets to facilitate appropriate product utilization and reimbursement access. The company invests in digital health platforms that support remote monitoring, adherence tracking, and personalized nutrition guidance for patients receiving enteral support. Recent strategic initiatives include expansion of plant based formula options and enhancement of home care delivery systems that improve patient experience and clinical outcomes. Nestlé Health Science's integration of nutritional science, clinical evidence, and patient centered design reinforces its competitive position within the European enteral feeding ecosystem.

Danone S.A.

Danone S.A. plays a substantial role in the Europe enteral feeding formulas devices market through its medical nutrition division and commitment to specialized nutritional solutions. The company leverages its French headquarters and European manufacturing network to ensure consistent product availability and responsive supply chain operations. Danone invests in clinical research to demonstrate the efficacy of disease specific formulas and advanced delivery systems that address complex patient needs. The company collaborates with healthcare professionals and patient organizations to support education initiatives and improve nutritional care standards across European healthcare settings. Recent strategic actions include portfolio expansion for renal and oncology indications and enhancement of home care support services that facilitate safe enteral nutrition management outside hospital environments. Danone's focus on scientific rigor, patient experience, and sustainable nutrition practices strengthens its competitive position throughout the European enteral feeding formulas market.

Top Strategies Used By Key Market Participants

Key participants in the Europe enteral feeding formulas devices market employ several strategic approaches to strengthen competitive positioning and drive sustainable growth. Product innovation remains central, with manufacturers investing in disease specific formulations, smart feeding technologies, and patient centered delivery systems that address evolving clinical requirements. Strategic partnerships with healthcare providers, clinical societies, and payers facilitate evidence generation, guideline integration, and reimbursement access that support appropriate product utilization. Geographic expansion within high growth European regions enables manufacturers to capture emerging demand while leveraging established distribution infrastructure. Digital health integration represents a growing strategic priority, with companies developing remote monitoring capabilities, adherence tracking tools, and personalized nutrition platforms that enhance patient outcomes and care coordination. Supply chain resilience initiatives ensure consistent product availability and rapid response to clinical needs across diverse healthcare settings. These multifaceted strategies enable market participants to navigate regulatory complexity, demonstrate clinical value, and capture growth opportunities throughout the European enteral feeding formulas ecosystem.

RECENT MARKET DEVELOPMENTS

- In March 2025, Fresenius Kabi announced expansion of its European innovation center to advance enteral and patient specific nutrition solutions for European and global markets. This expansion is anticipated to allow Fresenius Kabi to accelerate development of disease specific formulas and strengthen the Europe Enteral Feeding Formulas Devices Market presence.

- In February 2024, Fresenius Kabi reinforced its leadership in clinical nutrition across Europe by extending its collaboration with ESICM to support education and professional development in intensive care nutrition. This collaboration is anticipated to allow Fresenius Kabi to enhance clinical evidence generation and strengthen the Europe Enteral Feeding Formulas Devices Market presence.

MARKET SEGMENTATION

This research report on the European enteral feeding formulas market has been segmented and sub-segmented into the following categories:

By Product

- Polymeric

- Monomeric

- Disease-Specific Formulas

By Stage

- Adults

- Pediatrics

By Application

- Oncology

- Gastroenterology

- Neurology

By End User

- Hospitals

- LTCS

- Home Care

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com