Europe Healthcare Chatbots Market Size, Share, Trends & Growth Forecast Report By Component, Deployment Model, Application, End User and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis (2026 to 2034)

Europe Healthcare Chatbots Market Report Summary

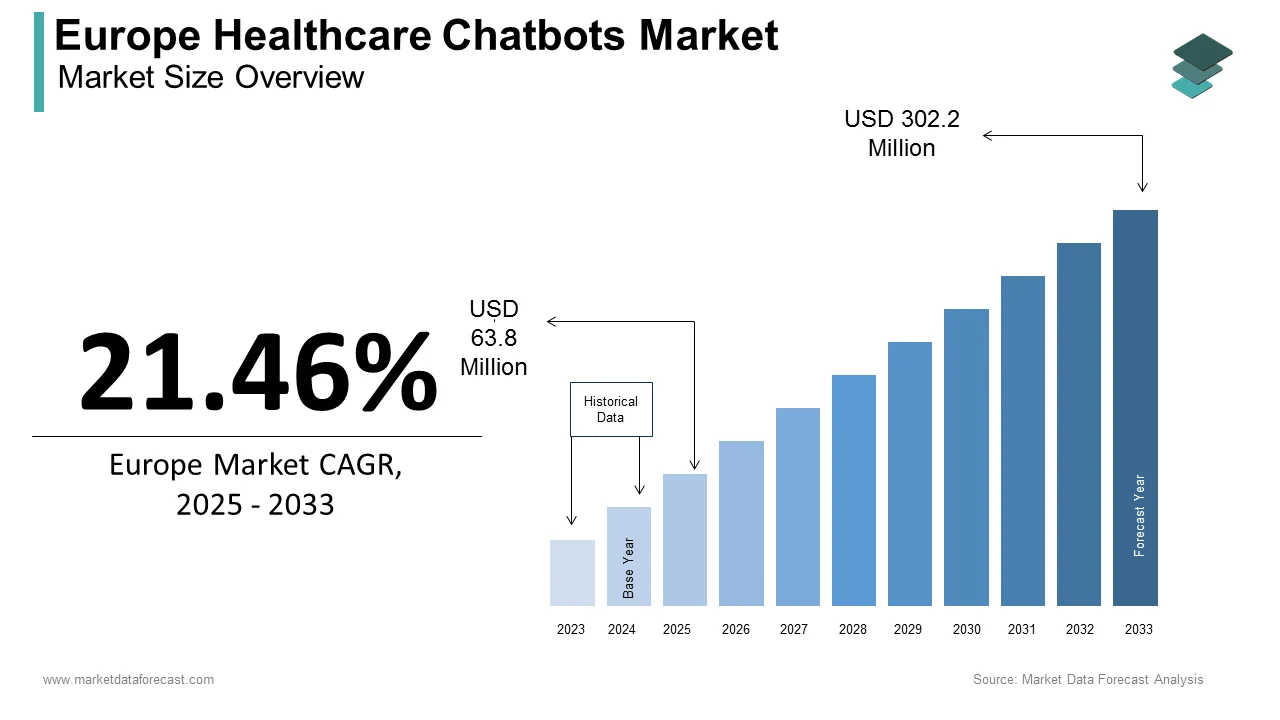

The Europe healthcare chatbots market was valued at USD 63.8 million in 2025, is estimated to reach USD 77.49 million in 2026, and is projected to reach USD 367 million by 2034, growing at a CAGR of 21.46% from 2026 to 2034. Market growth is driven by the increasing adoption of artificial intelligence in healthcare, rising demand for virtual health assistants, and the need to improve patient engagement and operational efficiency. Healthcare chatbots are widely used for appointment scheduling, symptom checking, patient monitoring, and providing medical information. The growing emphasis on digital healthcare transformation, telemedicine adoption, and cost reduction in healthcare delivery is further accelerating market expansion across Europe.

Key Market Trends

- Increasing adoption of AI-powered virtual assistants in healthcare services.

- Rising use of chatbots for patient engagement, triage, and appointment management.

- Growing integration of chatbots with telemedicine and digital health platforms.

- Expansion of cloud-based healthcare solutions for scalable chatbot deployment.

- Increasing focus on reducing healthcare operational costs through automation.

Segmental Insights

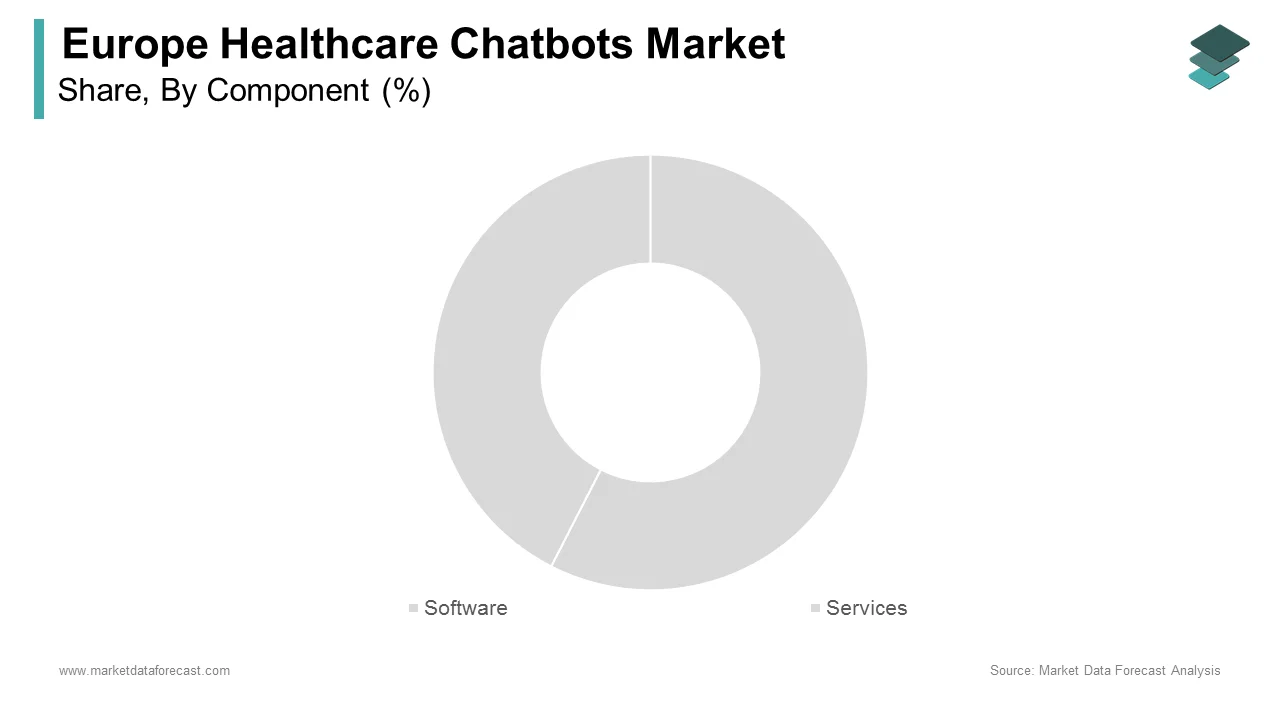

- Based on component, the software segment dominated the Europe healthcare chatbots market by accounting for 66.5% share in 2025, driven by the growing demand for AI-based chatbot platforms and applications.

- Based on deployment model, the cloud-based segment held the largest share of 70.9% in 2025, supported by the scalability, flexibility, and cost-effectiveness of cloud infrastructure.

- Based on end user, the healthcare providers segment led the market by capturing 50.9% share in 2025, driven by increasing adoption of chatbots in hospitals and clinics to enhance patient communication and streamline workflows.

Regional Insights

The Europe healthcare chatbots market is witnessing rapid growth across major countries due to increasing digitalization of healthcare systems and adoption of AI technologies.

- Germany led the regional market in 2025 with 23.5% share, supported by advanced healthcare infrastructure and strong adoption of digital health technologies.

- The United Kingdom is emerging as a promising market, driven by the growing use of AI in healthcare services and expanding telemedicine adoption.

- France is expected to hold a significant share during the forecast period due to its comprehensive national strategy focused on digitizing healthcare infrastructure and services.

Competitive Landscape

The Europe healthcare chatbots market is characterized by the presence of emerging AI startups and established digital health solution providers. Market participants are focusing on enhancing chatbot capabilities, improving natural language processing, and expanding healthcare-specific use cases. Strategic collaborations with healthcare providers and investments in AI innovation are shaping competitive dynamics across the region.

Prominent companies operating in the Europe healthcare chatbots market include Infermedica, Babylon Healthcare Service Limited, Sensely, Ada Digital Health Ltd., and PACT Care B.V.

Europe Healthcare Chatbots Market Size

The healthcare chatbot market in Europe was valued at USD 63.8 million in 2025. The European market size is expected to be valued at USD 367 million by 2034 from USD 77.49 million in 2026, growing at a CAGR of 21.46% from 2026 to 2034.

Healthcare chatbots comprise intelligent conversational agents designed to facilitate patient engagement, streamline administrative workflows, and deliver preliminary medical guidance across the European Union. These digital interfaces leverage natural language processing to interpret user queries and provide context-aware responses within the healthcare ecosystem. The adoption landscape is heavily influenced by the region's demographic shifts and digital infrastructure maturity. According to Eurostat, the proportion of individuals aged 65 and above in Europe highlights the urgent necessity for scalable remote care solutions that chatbots can effectively address. As per the European Commission, citizens in the EU now possess a strong level of basic digital skills, which establishes a robust foundation for the acceptance of automated health tools. The integration of these systems aims to alleviate pressure on traditional healthcare facilities by managing routine inquiries and triage processes. National health services across member states are increasingly recognizing the potential of artificial intelligence to bridge gaps in accessibility. This technological evolution aligns with broader public health strategies aimed at enhancing efficiency without compromising the quality of patient interaction. The market definition extends beyond simple question answering to include complex symptom checking and medication adherence monitoring, which reflects a sophisticated maturation of digital health capabilities throughout the continent.

MARKET DRIVERS

Rising Burden of Chronic Diseases Necessitates Scalable Remote Monitoring Solutions

The escalating prevalence of chronic conditions across Europe is a key factor propelling the growth of the European healthcare chatbots market. Noncommunicable diseases such as diabetes, cardiovascular disorders, and respiratory ailments account for a substantial portion of the regional disease burden, demanding continuous management rather than episodic care. According to the World Health Organization Regional Office for Europe, chronic diseases remain the leading cause of death in the region, placing immense strain on existing medical infrastructure. Traditional face-to-face consultations cannot sustainably accommodate the frequency of interactions required for effective chronic disease management. Healthcare chatbots offer a viable solution by providing round-the-clock monitoring, medication reminders, and lifestyle coaching without human intervention. In Germany alone, where over 7 million individuals live with diagnosed diabetes, digital tools are becoming essential for daily glucose tracking and dietary advice dissemination. The ability of these conversational agents to process vast amounts of patient data in real time allows for personalized interventions that adapt to individual health trajectories. This scalability ensures that patients receive consistent support regardless of geographical location or time of day. As national health systems struggle with workforce shortages, the automation of routine chronic care tasks through chatbots becomes not merely an option but a critical operational necessity to maintain service levels and improve long-term patient outcomes across the continent.

Accelerated Digital Transformation Initiatives Within European Public Health Systems

Aggressive government-led digitalization mandates are fundamentally reshaping the healthcare landscape and driving chatbot adoption throughout Europe, which is further boosting the European healthcare chatbots market expansion. Member states are actively implementing policies to integrate artificial intelligence into public health frameworks to enhance efficiency and reduce operational costs. As per the European Commission Digital Economy and Society Index, the integration of digital technologies in public services has been increasing, with health-specific initiatives receiving significant funding under the Digital Europe Programme. Countries like Estonia have pioneered fully digital health records, creating an interoperable environment where chatbots can seamlessly access patient history to provide accurate guidance. The French government allocated over 2 billion euros toward digital health innovation as part of its France 2030 investment plan, explicitly supporting AI-driven patient engagement tools. These financial commitments lower the barrier to entry for healthcare providers seeking to deploy advanced conversational interfaces. Furthermore, the cross-border eHealth Digital Service Infrastructure facilitates the secure exchange of health data, enabling chatbots to operate effectively across national boundaries within the Schengen Area. This regulatory and financial backing creates a fertile ground for technology vendors to introduce sophisticated solutions. The strategic alignment of national policies with technological capabilities ensures that chatbots are viewed as integral components of modern healthcare delivery rather than peripheral add-ons, thereby accelerating their penetration into both primary and secondary care settings across the region.

MARKET RESTRAINTS

Stringent Data Privacy Regulations Impede Rapid Deployment and Integration

The rigorous data protection framework established by the General Data Protection Regulation is hindering the European healthcare chatbots market growth. Medical information classified as special category data demands the highest level of security and explicit consent mechanisms, complicating the development and deployment of AI-driven conversational agents. As per the European Data Protection Board, violations involving health data can result in severe financial penalties, creating a climate of caution among healthcare providers and technology developers. The requirement for data minimization and purpose limitation often conflicts with the machine learning models that thrive on large datasets to improve accuracy and contextual understanding. Developers must engineer complex compliance architectures to ensure that every interaction adheres to strict privacy standards without compromising functionality. In countries like Italy and Spain, local data sovereignty laws further restrict where patient data can be processed and stored, limiting the use of cloud-based chatbot solutions hosted outside national borders. The extensive documentation required for Data Protection Impact Assessments delays time to market for new applications significantly. Healthcare institutions frequently hesitate to adopt innovative chatbot technologies due to fear of noncompliance and reputational damage associated with potential data breaches. This regulatory complexity increases operational costs and slows the pace of innovation, forcing vendors to prioritize legal adherence over rapid feature expansion, which is ultimately restraining the overall growth velocity of the market despite clear clinical benefits.

Persistent Interoperability Issues Across Fragmented National Health IT Ecosystems

The lack of standardized technical protocols across diverse national health information systems severely limits the functional efficacy of healthcare chatbots in Europe, which is further hampering the expansion of the European healthcare chatbots market. Each member state maintains distinct electronic health record architectures and data exchange standards, creating silos that prevent seamless integration of conversational agents into existing clinical workflows. As per the European Health Data Space regulation impact assessment, the fragmentation of health data systems results in inefficiencies and hinders the cross-border portability of digital health services. Chatbots deployed in one country often fail to communicate effectively with hospital databases in another due to incompatible application programming interfaces and varying data formats. This disconnection prevents chatbots from accessing comprehensive patient histories, thereby reducing their ability to provide accurate triage or personalized medical advice. In regions with highly decentralized healthcare governance, such as Belgium, or federal structures like Germany, achieving uniform integration across regional providers proves exceptionally challenging. The absence of a unified semantic standard means that medical terminologies and coding systems differ widely, leading to potential misinterpretations by natural language processing algorithms. Consequently, healthcare providers are reluctant to invest in chatbot solutions that cannot guarantee full interoperability with their legacy systems. This technical fragmentation necessitates costly customizations for each deployment scenario, diminishing the economic viability of scaling chatbot solutions across the continent and acting as a formidable restraint on market expansion.

MARKET OPPORTUNITIES

Expansion of Telemedicine Services Creates Fertile Ground for Conversational AI Integration

The exponential growth of telemedicine across Europe offers a substantial opportunity for the European healthcare chatbots market. The pandemic-induced shift toward remote consultations has normalized digital health interactions, which is creating a receptive environment for automated triage and follow-up services. As per the European Observatory on Health Systems and Policies, telemedicine usage has significantly increased in several member states, establishing a permanent infrastructure for remote patient engagement. Chatbots can effectively serve as the first point of contact in these virtual pathways, handling initial symptom assessments and routing patients to appropriate specialists or video consultation slots. This integration optimizes the workflow for medical professionals by filtering out non-urgent cases and ensuring that valuable consultation time is reserved for complex diagnoses. In nations like Sweden and the Netherlands, where national telehealth platforms are well established, there is a strategic push to embed AI assistants directly into patient portals to enhance user experience. The ability of chatbots to operate continuously allows healthcare systems to extend their reach beyond traditional office hours, addressing the growing demand for after-hours medical advice. Furthermore, the integration of chatbots with remote monitoring devices enables proactive health management, alerting clinicians to deteriorating conditions before they become critical. This synergy between telemedicine frameworks and conversational AI presents a lucrative avenue for market players to develop specialized solutions tailored to the evolving needs of European virtual care ecosystems.

Advancements in Natural Language Processing Enable Multilingual Patient Engagement

Breakthroughs in natural language processing technologies present a promising opportunity for the European healthcare chatbots market. The continent hosts 24 official languages and numerous regional dialects, historically complicating the deployment of uniform digital health solutions. Modern large language models now possess the capability to understand and generate contextually accurate responses in multiple European languages simultaneously, allowing vendors to scale their offerings across borders with minimal customization. As per the European Language Equality initiative, advancements in low-resource language modeling are enabling AI systems to support minority languages that were previously neglected by technology developers. This linguistic inclusivity opens up vast untapped markets in regions where English proficiency is limited and localized care is paramount. Chatbots equipped with these advanced capabilities can provide culturally sensitive health education and adherence support in the native tongue of the patient, significantly improving engagement rates and health outcomes. In countries with high immigration rates, such as France and Germany, multilingual chatbots can bridge communication gaps between migrant populations and healthcare providers, ensuring equitable access to medical information. The ability to accurately interpret medical nuances across different languages reduces the risk of misdiagnosis and enhances patient trust. This technological evolution allows market participants to develop pan-European platforms that cater to the linguistic diversity of the region, turning a historical challenge into a significant competitive advantage and growth driver.

MARKET CHALLENGES

Ensuring Clinical Accuracy and Mitigating Risks of Medical Misinformation

Maintaining absolute clinical accuracy while preventing the dissemination of harmful medical misinformation remains a paramount challenge for the Europe Healthcare Chatbots Market. Unlike general customer service bots, healthcare conversational agents deal with life-critical information where even minor errors can lead to severe patient harm or legal liability. As per the European Patient Safety Report, diagnostic errors contribute significantly to adverse events in healthcare settings, raising concerns about the reliability of AI-driven symptom checkers. The probabilistic nature of generative artificial intelligence models means they can occasionally hallucinate or fabricate medical advice that sounds plausible but is factually incorrect. Validating the output of these systems against current clinical guidelines requires rigorous and continuous oversight by medical professionals, which is resource-intensive and difficult to scale. In emergency scenarios, a chatbot failing to recognize critical symptoms could delay lifesaving treatment, which is exposing developers and healthcare providers to substantial litigation risks. The dynamic nature of medical knowledge necessitates constant updates to the underlying knowledge bases of chatbots to reflect the latest research and treatment protocols. Failure to synchronize these updates in real time can result in the provision of outdated or contraindicated advice. Building trust among patients and clinicians requires demonstrable evidence of safety and efficacy, which is currently difficult to quantify uniformly across different AI architectures. This imperative for flawless performance creates a high barrier to entry and slows the adoption rate as stakeholders await more robust validation frameworks and regulatory clarity regarding liability in AI-assisted diagnosis.

Deep-Seated Patient Skepticism Regarding Automated Medical Advice and Empathy

Overcoming deep-rooted patient skepticism concerning the empathetic capabilities and ethical implications of automated medical advice poses a significant challenge to market penetration in Europe. Despite technological advancements, a substantial segment of the European population remains hesitant to trust machines with sensitive health disclosures or critical decision-making processes. As per the Eurobarometer survey on attitudes towards artificial intelligence, many EU citizens express discomfort with the idea of AI making decisions that affect their health and well-being. The perceived lack of human empathy in chatbot interactions can deter patients from sharing crucial psychosocial details that are often vital for accurate diagnosis and holistic care. Cultural preferences for face-to-face doctor-patient relationships remain strong in many Southern and Eastern European countries, where personal trust is built through direct human connection rather than digital interfaces. Elderly demographics, who constitute a large portion of healthcare consumers, often lack the digital confidence to engage effectively with conversational agents, fearing misuse of their data or misunderstanding by the algorithm. This psychological barrier is compounded by high-profile media stories regarding AI failures, which reinforce public apprehension. Healthcare providers are consequently cautious about recommending chatbot services lest they damage their therapeutic alliance with patients. Addressing this skepticism requires more than just technical improvements; it demands a fundamental shift in public perception through transparent communication about AI limitations and the supplementary role of chatbots. Until patients feel genuinely understood and safe, the full potential of healthcare chatbots will remain unrealized across the diverse cultural landscape of Europe.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Component, Deployment Model, Application, End-User, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Infermedica, Babylon Healthcare Service Limited, Sensely, Ada Digital Health Ltd., PACT Care BV., and Others. |

SEGMENTAL ANALYSIS

By Component Insights

The software segment led the market by commanding the highest share of 66.5% of the regional market in 2025. The dominance of the software segment in the European market is attributed to the fundamental necessity of robust conversational engines and natural language processing algorithms as the core utility of the market. The escalating demand for proprietary AI models capable of understanding complex medical terminologies and patient intent with high precision is further contributing to the expansion of the software segment in the European market. As per the European Commission, investment in artificial intelligence research and development within the health sector has been increasing, which is directly fuelling the creation of sophisticated chatbot software architectures. Furthermore, the shift toward value-based care models necessitates software that can integrate seamlessly with electronic health records to provide real-time clinical decision support. In Germany, the Digital Healthcare Act has mandated that digital health applications, including chatbot software, meet rigorous certification standards, which has consolidated market share among high-quality software providers who can demonstrate clinical efficacy. The recurring revenue model associated with software licensing and subscription fees also contributes to its financial supremacy over one-time service contracts. Hospitals and clinics prioritize acquiring adaptable software platforms that can be updated continuously to reflect new medical guidelines, ensuring long term utility. This persistent need for advanced, compliant, and upgradable conversational intelligence solidifies the software segment as the undisputed leader in the European landscape.

On the other hand, the services segment is growing rapidly and is expected to grow at a CAGR of 25.1% over the forecast period in this regional market, owing to the critical need for specialized implementation, customization, and ongoing maintenance required to deploy chatbot solutions within complex European healthcare infrastructures. Unlike off-the-shelf software, healthcare chatbots demand extensive tailoring to align with specific national regulations, local languages, and institutional workflows. As per Eurostat, the shortage of internal IT expertise within European public hospitals has been reported at a critical level, forcing organizations to rely heavily on professional service providers for system integration, data migration, and staff training. Additionally, the stringent requirements of the General Data Protection Regulation necessitate continuous compliance auditing and security monitoring, creating a sustained demand for managed services. In France, the national health strategy emphasizes the deployment of accompanied digital tools, mandating that vendors provide comprehensive onboarding and support services to ensure successful adoption by medical practitioners. The increasing complexity of natural language models also requires regular fine-tuning and performance optimization, further expanding the scope of service contracts. Consequently, the reliance on expert guidance to navigate technical and regulatory complexities propels the services segment to become the fastest-expanding component of the market.

By Deployment Model Insights

The cloud-based model segment accounted for a major share of 70.9% of the European market in 2025. The dominating position of the cloud-based segment in the European market can be credited to the inherent scalability, cost efficiency, and rapid deployment capabilities offered by cloud infrastructure, which are essential for handling fluctuating patient volumes across diverse healthcare settings. The ability to access powerful computing resources on demand allows healthcare providers to deploy sophisticated natural language processing models without significant upfront capital expenditure on physical servers. As per the European Cloud Partnership, adoption of cloud services in the public sector has been increasing, reflecting a strategic shift toward flexible IT architectures. The cloud model facilitates seamless updates and integration with other digital health ecosystems, such as telemedicine platforms and remote monitoring devices, ensuring that chatbots remain current with the latest medical protocols. In the United Kingdom, the National Health Service has actively promoted cloud-first policies to modernize its digital infrastructure, enabling faster rollout of AI-driven patient engagement tools across its vast network. Furthermore, leading cloud providers have established data centers within Europe to address sovereignty concerns, offering compliant environments that adhere to strict local data protection laws. This combination of operational agility, economic viability, and improved regulatory compliance makes the cloud-based model the preferred choice for the majority of European healthcare organizations seeking to implement chatbot solutions.

By End-User Insights

The healthcare providers segment led the market by capturing 50.9% of the regional market share in 2025 due to the urgent operational imperative to alleviate administrative burdens and optimize patient flow within increasingly strained medical facilities. Chatbots serve as vital tools for automating appointment scheduling, preliminary symptom triage, and post-discharge follow-ups, allowing medical staff to focus on critical care activities. As per the Organisation for Economic Co-operation and Development, waiting times for specialist consultations in several European countries remain lengthy, creating a pressing need for automated systems that can manage initial patient interactions efficiently. In Italy, the Ministry of Health has incentivized the adoption of digital triage tools to reduce overcrowding in emergency departments, where chatbots have proven effective in filtering non-urgent cases. The integration of chatbots into hospital information systems enables providers to offer 24/7 patient support without increasing staffing costs, addressing the chronic workforce shortages plaguing the region. Furthermore, the ability of these systems to collect and analyze patient data before consultations enhances diagnostic accuracy and preparation time for physicians. The strong regulatory push for digital transformation in public healthcare, combined with the tangible operational efficiencies gained, solidifies healthcare providers as the primary adopters and revenue generators in the Europe Healthcare Chatbots Market.

However, the insurance companies segment is emerging as the fastest-growing end-user segment and is anticipated to record a CAGR of 25.3% over the forecast period. The strategic shift of insurers toward proactive health management and fraud detection mechanisms to control rising claim costs and improve member outcomes is primarily driving the rapid expansion of the insurance companies segment in the European market. Chatbots enable insurers to engage policyholders continuously, offering personalized wellness advice, medication adherence reminders, and instant claims processing support, which fosters loyalty and reduces preventable health events. As per the Swiss Re Institute, the implementation of AI-driven engagement tools in the insurance sector has been shown to reduce administrative costs while simultaneously improving customer satisfaction scores. In Germany, statutory health insurance funds are increasingly deploying chatbots to guide members through the complex landscape of covered services and preventive care programs, aiming to lower long term expenditure on chronic disease management. The capability of these conversational agents to analyze patterns in claims data also aids in the early identification of fraudulent activities, saving the industry significant amounts annually. Moreover, the competitive landscape of the European insurance market forces companies to differentiate themselves through superior digital customer experiences, making chatbot integration a priority. The convergence of cost containment pressures and the demand for hyper-personalized member services propels insurance companies to become the most rapidly adopting segment in the market.

COUNTRY-LEVEL ANALYSIS

Germany Healthcare Chatbots Market Analysis

Germany dominated the healthcare chatbots market in Europe in 2025 with 23.5% of the regional market share. The dominance of Germany in the European market can be credited to its robust industrial base, progressive digital health legislation, and the successful implementation of the Digital Healthcare Act that mandates reimbursement for digital health applications, thereby creating a lucrative environment for chatbot developers. As per the Federal Ministry of Health, prescriptions for digital health apps have been widely issued, indicating strong physician and patient acceptance. The driving factor behind this dominance is the strong collaboration between the automotive engineering sector and healthcare technology firms, resulting in high-precision AI algorithms and reliable hardware integration. Germany's aging population creates immense pressure on the healthcare system, which chatbots effectively mitigate through remote monitoring and automated care coordination. The presence of major technology hubs in Munich and Berlin fosters a vibrant ecosystem of startups and established enterprises innovating in conversational AI. Furthermore, the strict adherence to data privacy standards under German law sets a global benchmark, giving locally developed solutions a competitive edge in trust and compliance. This unique blend of regulatory support, demographic necessity, and technological prowess ensures Germany retains its position as the market leader.

United Kingdom Healthcare Chatbots Market Analysis

The United Kingdom is another promising regional segment for healthcare chatbots in Europe. The pioneering approach of the UK to integrating artificial intelligence within the National Health Service framework, aggressive government funding, and a centralized healthcare system that allows for rapid scaling of successful pilot programs across the nation are driving the UK healthcare chatbots market. As per NHS England, adoption of AI tools, including chatbots for triage and mental health support, has significantly increased since the onset of the pandemic, reflecting a systemic commitment to digital transformation. A key driving factor is the existence of world-class research institutions and a thriving fintech and healthtech sector in London that attracts significant venture capital investment. The UK government's Life Sciences Vision strategy explicitly targets the deployment of AI to improve diagnostic speed and patient access, providing a clear roadmap for market growth. Additionally, the high prevalence of chronic conditions and the need to manage limited resources efficiently drive hospitals to adopt automated solutions for routine patient interactions. The cultural readiness of the British population to embrace digital health services, coupled with a supportive regulatory environment from the Medicines and Healthcare products Regulatory Agency, fosters an atmosphere conducive to rapid innovation. These elements collectively sustain the UK's position as a critical growth engine for the European market.

France Healthcare Chatbots Market Analysis

France is estimated to secure a prominent position in the European healthcare chatbots market during the forecast period due to a comprehensive national strategy to digitize its healthcare infrastructure and enhance patient autonomy and significant public investment under the France 2030 plan, which allocates billions of euros specifically to health innovation and artificial intelligence development. As per the French Ministry of Solidarity and Health, deployment of telemedicine and digital assistant tools has become a cornerstone of the national health strategy, aiming to reduce medical deserts in rural areas. The primary driving factor is the government's initiative to create a unified digital health space that facilitates secure data exchange and interoperability among various healthcare actors. French healthcare providers are increasingly utilizing chatbots to manage the high volume of patient inquiries and streamline administrative processes, thereby improving overall system efficiency. The strong emphasis on preventative care and the promotion of healthy lifestyles through digital channels further accelerates adoption rates. Moreover, the presence of major pharmaceutical and technology corporations in France fosters partnerships that accelerate the development of specialized chatbot solutions for chronic disease management. The combination of state-led investment, a focus on equitable access, and a robust industrial ecosystem positions France as a pivotal player in the regional market landscape.

Italy Healthcare Chatbots Market Analysis

Italy represents a significant market contributor with a notable share of the European healthcare chatbots market in 2025 and is propelled largely by the urgent need to address the challenges posed by one of the oldest populations in the world. The market status is defined by a gradual but steady shift toward digital health solutions to sustain the national health service amidst shrinking workforce availability and rising healthcare costs. As per the Italian National Institute of Statistics, individuals over 65 account for a large portion of the population, creating unprecedented demand for remote care and monitoring technologies that chatbots effectively provide. The driving factor behind market growth is the recent legislative reforms aimed at modernizing the healthcare system, including incentives for the adoption of telehealth and AI-driven patient engagement tools. Regional health authorities in Lombardy and Emilia Romagna have pioneered the use of chatbots for managing chronic diseases and coordinating home care services, setting a precedent for national expansion. The increasing penetration of smartphones among the elderly demographic, supported by government digital literacy programs, facilitates greater acceptance of conversational agents. Additionally, the focus on reducing hospital readmission rates through continuous post discharge monitoring drives healthcare providers to integrate chatbots into their care pathways. These demographic and structural dynamics ensure Italy remains a crucial and growing segment of the European market.

Spain Healthcare Chatbots Market Analysis

Spain is anticipated to witness a healthy CAGR in the European healthcare chatbots market during the forecast period, owing to a rapidly evolving digital health landscape, strong regional government support for innovation, and a transition from traditional care models to integrated digital ecosystems, with a particular focus on enhancing accessibility in both urban centers and remote coastal regions. As per the Spanish Ministry of Health, the national digital health strategy prioritizes the implementation of AI tools to improve patient triage and reduce waiting times in primary care centers. A major driving factor is the decentralization of the healthcare system, which allows autonomous communities like Catalonia and Madrid to experiment with and deploy tailored chatbot solutions that address local needs effectively. The high tourism influx also necessitates multilingual digital health assistants to cater to international visitors, creating a unique niche for advanced conversational AI. Furthermore, the growing awareness of mental health issues has led to the deployment of empathetic chatbots designed to provide initial psychological support and counselling referrals. The collaboration between Spanish universities and technology firms fosters a steady stream of innovative applications tailored to the specific linguistic and cultural nuances of the region. This blend of regional autonomy, tourism-driven requirements, and focused health strategies positions Spain as a dynamic and expanding market within Europe.

COMPETITIVE LANDSCAPE

The competition in the Europe Healthcare Chatbots Market is characterized by a dynamic mix of specialized health technology startups and established multinational technology corporations vying for dominance through innovation and strategic alliances. The landscape features intense rivalry as companies strive to differentiate their offerings via superior clinical accuracy, seamless interoperability with legacy hospital systems, and robust data security measures that comply with European laws. New entrants often focus on niche therapeutic areas such as mental health or chronic disease management to carve out specific market segments before expanding their scope. Incumbent players leverage their extensive resources and existing customer relationships to launch comprehensive platforms that cover a wide range of medical needs. The pressure to demonstrate tangible return on investment and clinical efficacy drives continuous improvement in artificial intelligence models and user experience design. Regulatory compliance remains a critical battleground where companies must navigate complex legal frameworks to maintain operational licenses and public trust. This highly competitive environment fosters rapid technological advancement but also creates significant barriers for smaller firms lacking the capital to sustain long term development and certification processes required in this sensitive sector.

KEY MARKET PLAYERS

The leading companies operating in the Europe healthcare chatbots market include:

- Infermedica

- Babylon Healthcare Service Limited

- Sensely

- Ada Digital Health Ltd.

- PACT Care B.V.

TOP PLAYERS IN THE MARKET

- Babylon Health stands as a pioneering force in the European digital health sector by integrating artificial intelligence with clinical expertise to deliver accessible care. The company has significantly influenced the global market by demonstrating the viability of AI-driven triage and remote consultation models at scale. Recently, Babylon has strengthened its position through strategic partnerships with national health services and insurance providers across the United Kingdom and Rwanda to expand its reach. The firm continues to refine its symptom checker algorithms using vast datasets to improve diagnostic accuracy and patient trust. Their focus on regulatory compliance and clinical validation ensures their chatbot solutions meet rigorous European standards while setting benchmarks for global competitors. This commitment to evidence-based digital medicine solidifies their role as a primary innovator shaping the future of conversational healthcare technologies worldwide.

- Ada Health operates as a leading German-based digital health company that has revolutionized personal health assessment through its sophisticated AI-powered chatbot application. The platform serves millions of users globally by providing personalized health information and guiding individuals through complex medical queries with high precision. Ada recently enhanced its market standing by collaborating with major pharmaceutical companies and healthcare systems to integrate its technology into chronic disease management programs. The company focuses heavily on multilingual support to cater to the diverse linguistic landscape of Europe and beyond. Their continuous investment in natural language processing research ensures the chatbot understands nuanced symptoms and cultural contexts effectively. By prioritizing data privacy and clinical safety, Ada has established itself as a trusted partner for healthcare providers seeking to deploy reliable conversational agents that improve patient engagement and outcomes internationally.

- Sensely distinguishes itself in the market by offering a unique virtual nurse assistant platform that combines conversational AI with animated avatars to enhance patient interaction. The company has made substantial contributions to the global healthcare landscape by enabling health systems to automate routine care tasks and monitor patients remotely with a human touch. Sensely recently expanded its European footprint through alliances with hospital networks in Spain and the United Kingdom to deploy its Molly avatar for triage and post-discharge follow-up. Their technology supports multiple languages and integrates seamlessly with existing electronic health records to provide continuity of care. The firm actively pursues certifications from European regulatory bodies to ensure its solutions comply with strict medical device standards. This dedication to creating empathetic and clinically validated digital assistants allows Sensely to maintain a competitive edge and drive the adoption of virtual nursing solutions across international markets.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe Healthcare Chatbots Market primarily employ strategic partnerships and collaborations with established healthcare institutions to accelerate adoption and ensure clinical validity. Companies frequently engage in mergers and acquisitions to integrate advanced natural language processing capabilities and expand their geographical reach across diverse European nations. Another prevalent strategy involves heavy investment in research and development to enhance algorithmic accuracy and achieve compliance with stringent regional data protection regulations like GDPR. Market participants also focus on developing multilingual interfaces to address the linguistic diversity of the continent and broaden their user base significantly. Furthermore, firms are increasingly adopting a software as a service model to lower entry barriers for smaller clinics and ensure recurring revenue streams while providing continuous updates and support to their clients.

MARKET SEGMENTATION

This research report on the European healthcare chatbots market has been segmented and sub-segmented into the following categories.

By Component

- Software

- Services

By Deployment Model

- On-premise Model

- Cloud-based Model

By Application

- Symptom checking & Medication Assistance

- Appointment Scheduling & Medical Guidance

By End-User

- Patients

- Healthcare Providers

- Insurance Companies

- Other End Users

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe healthcare chatbot market?

The Europe healthcare chatbot market provides AI symptom checkers and appointment bots integrated with EHR systems. Germany dominates hospital deployments while UK leads consumer health apps.

How does the Europe healthcare chatbot market function?

The Europe healthcare chatbot market functions through NLP processing medical queries with multilingual support. Decision trees guide triage while APIs connect to clinical workflows seamlessly.

What drives growth in the Europe healthcare chatbot market?

Telehealth expansion drives the Europe healthcare chatbot market alongside physician shortages. GDPR-compliant automation reduces administrative burdens across healthcare systems.

Which countries lead the Europe healthcare chatbot market?

Germany leads the Europe healthcare chatbot market through digital prescribing platforms. Netherlands follows rapidly with integrated primary care chatbot solutions.

What applications define the Europe healthcare chatbot market?

Patient triage dominates the Europe healthcare chatbot market alongside appointment scheduling. Mental health support chatbots gain widespread clinical acceptance.

What technologies shape the Europe healthcare chatbot market?

NLP and ML algorithms define the Europe healthcare chatbot market enabling contextual medical conversations. Voice recognition supports hands-free hospital applications.

How does regulation influence the Europe healthcare chatbot market?

GDPR and EU AI Act govern the Europe healthcare chatbot market ensuring medical data security. CE marking validates clinical decision support reliability.

What trends affect the Europe healthcare chatbot market?

Multimodal chatbots transform the Europe healthcare chatbot market combining text, voice, and video. Emotion recognition enhances mental health interventions.

What challenges face the Europe healthcare chatbot market?

Clinical validation challenges the Europe healthcare chatbot market though randomized trials help. Multilingual medical accuracy ensures pan-European deployment.

How has COVID impacted the Europe healthcare chatbot market?

Pandemic triage accelerated the Europe healthcare chatbot market reducing emergency overloads. Remote monitoring chatbots became standard telehealth components.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com