Europe Home Care Market Size, Share, Trends & Growth Forecast Report By Product Type (Air Care, Dishwashing, Bleach, Insecticides, Laundry Care, Surface Care, Toilet Care, Others), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retail Stores, Others), and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe) – Industry Analysis From 2026 to 2034.

Market Size, 2025

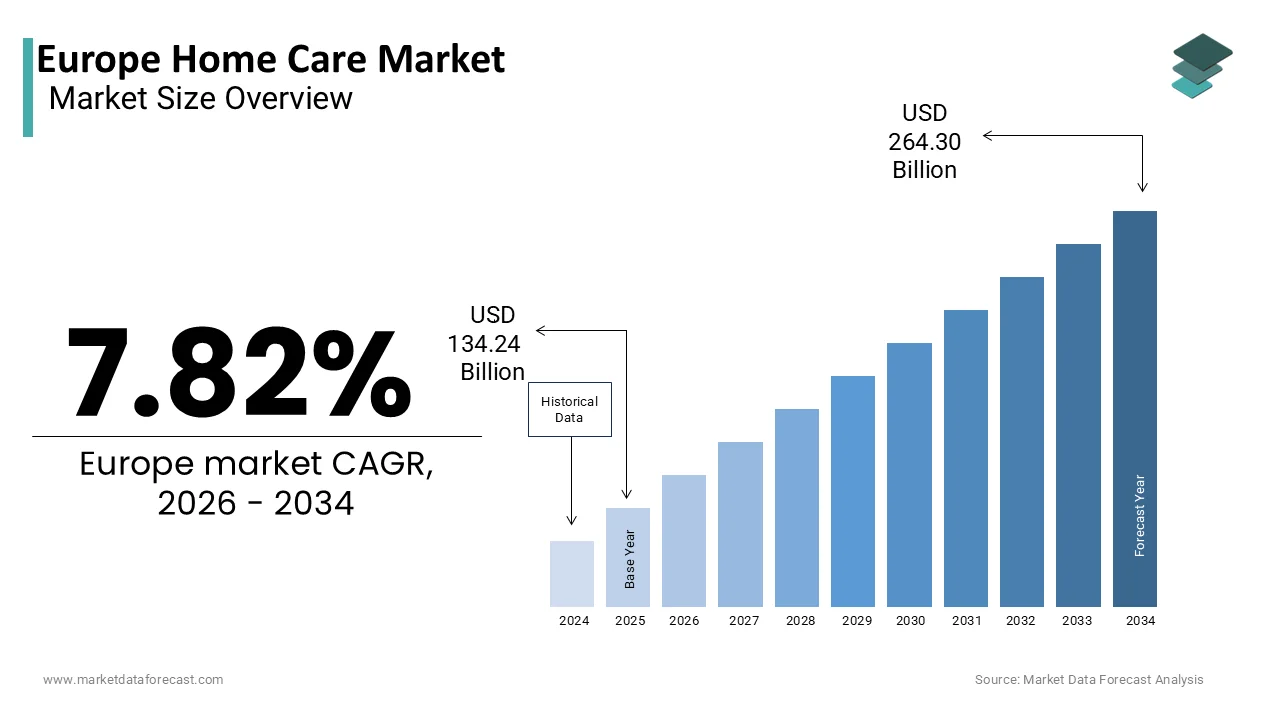

$134.24 BnMarket Estimate, 2026

$144.73 BnMarket Forecast, 2034

$264.30 BnCAGR, 2026–2034

7.82%Europe Home Care Market Summary

The Europe home care market size was estimated at USD 124 billion in 2024 and is projected to reach USD 244.18 billion by 2033, growing at a CAGR of 7.82% from 2025 to 2033. The rise in the aging population, increasing demand for chronic disease care at home, and adoption of smart health monitoring tools are driving market growth across the region.

Key Market Trends & Insights

- Germany accounted for the largest share of 22% in 2024.

- Based on product type, the laundry care segment held a significant market share of 23.4% in 2024.

- Based on distribution channel, supermarkets and hypermarkets accounted for the largest share in 2024.

- Based on distribution channel, the online retail stores are expected to expand at the fastest growth rate from 202 to 2033.

Market Size & Forecast

- 2024 Market Size: USD 124 Billion

- 2033 Projected Market Size: USD 244.18 Billion

- CAGR (202–2033): 7.82%

- Germany: Largest market in 2024

- Online Retail Stores: Fastest-growing channel

Europe Home Care Market Size

The Europe home care market was valued at USD 134.24 billion in 2025, is estimated to reach USD 144.73 billion in 2026, and is projected to reach USD 264.30 billion by 2034, growing at a CAGR of 7.82% from 2026 to 2034

The Europe home care market refers to the services and support provided to individuals within their own homes, primarily aimed at elderly, chronically ill, or physically challenged patients. These services include medical assistance, personal care, nursing, rehabilitation, and non-medical support such as meal preparation and companionship. Unlike institutionalized healthcare settings, home care emphasizes patient comfort, independence, and continuity of care in familiar environments.

Europe has seen a growing reliance on home-based care solutions due to demographic shifts, particularly the aging population. The home care sector is supported by both public healthcare systems and private providers, with countries like Germany, France, and Sweden leading in structured home care delivery models.

Moreover, technological advancements such as remote monitoring devices, telehealth platforms, and digital care management tools are enhancing the quality and reach of home care services across the region.

MARKET DRIVERS

Aging Population and Increasing Chronic Disease Prevalence

One of the most significant drivers of the European home care market is the rapid aging of the population, which has led to a surge in demand for long-term and post-acute care services. Older adults often require ongoing medical attention, assistance with daily activities, and chronic disease management, all of which can be effectively addressed through home-based care. Additionally, the prevalence of age-related chronic conditions such as diabetes, cardiovascular diseases, and dementia has intensified the need for continuous, personalized care. Home care services offer a practical solution by reducing hospital admissions and enabling patients to receive professional treatment in familiar surroundings. Governments and healthcare institutions are increasingly endorsing home care as a cost-effective alternative to institutionalized healthcare.

Advancements in Telehealth and Remote Monitoring Technologies

Another key driver of the European home care market is the rapid adoption of telehealth and remote monitoring technologies, which enhance the efficiency and accessibility of home-based care services. Innovations such as wearable health devices, mobile health applications, and real-time patient monitoring systems allow caregivers to track vital signs, administer timely interventions, and communicate with healthcare professionals without requiring in-person visits. Countries like Germany and the Netherlands have integrated digital health records and virtual consultations into home care programs, improving coordination between patients, caregivers, and physicians. These advancements not only enhance the quality of care but also reduce the burden on formal healthcare facilities, making home care an increasingly viable option for managing both acute and chronic conditions.

MARKET RESTRAINTS

Shortage of Skilled Caregivers and Workforce Challenges

A major restraint affecting the European home care market is the persistent shortage of skilled caregivers and trained healthcare professionals, which limits the scalability and quality of home-based care services. Despite rising demand, many countries struggle to recruit and retain qualified nurses, personal care assistants, and therapists due to factors such as high workload, relatively low wages, and limited career development opportunities. Additionally, the physically demanding nature of caregiving, combined with emotional stress and irregular working hours, contributes to high turnover rates within the sector. As noted by the International Labour Organization (ILO), burnout and job dissatisfaction among home care workers have been exacerbated by the increasing complexity of patient needs, particularly in cases involving elderly individuals with multiple chronic conditions.

Regulatory Complexity and Reimbursement Barriers

Regulatory complexity and inconsistent reimbursement frameworks pose significant challenges to the expansion of the European home care market. Each country within the EU maintains its own set of regulations regarding home care eligibility, funding mechanisms, and provider accreditation, creating operational difficulties for both domestic and international service providers. As per the European Observatory on Health Systems and Policies, disparities in national healthcare coverage for home care services result in unequal access for patients. Moreover, reimbursement procedures often involve lengthy administrative processes, making it difficult for small and medium-sized home care agencies to sustain operations.

MARKET OPPORTUNITIES

Integration of AI and Smart Assistive Devices in Home Care

A significant opportunity within the Europe home care market lies in the integration of artificial intelligence (AI) and smart assistive devices to enhance patient monitoring, improve caregiver efficiency, and personalize care delivery. AI-powered tools such as predictive analytics, voice-activated assistants, and fall detection sensors are transforming how home care services are administered, allowing for early intervention and reduced hospitalization rates. According to a study conducted by the Fraunhofer Institute, AI-assisted home monitoring systems have the potential to cut emergency response times by up to 30%, particularly for elderly patients living alone. Also, smart wearables and IoT-enabled medical devices are gaining traction in home care settings, providing real-time health tracking and remote diagnostics.

Expansion of Private Home Care Services and Insurance Coverage

An emerging opportunity in the Europe home care market is the growing expansion of private home care services and the increasing availability of insurance packages that cover home-based medical and personal care. With public healthcare systems facing capacity constraints, more individuals are turning to private providers for customized, high-quality care options tailored to their specific needs. These policies often cover services such as live-in caregivers, physiotherapy, and medication management, offering financial relief to families seeking long-term care solutions. Moreover, private home care agencies are capitalizing on rising consumer awareness and disposable incomes to expand their service offerings. Companies like Home Instead Senior Care and AlayaCare have established a strong presence across multiple European markets, leveraging digital platforms to connect patients with vetted caregivers efficiently.

MARKET CHALLENGES

Fragmentation of Service Delivery Across Countries

A major challenge confronting the Europe home care market is the fragmentation of service delivery across different countries, stemming from varying regulatory frameworks, funding models, and operational standards. Unlike centralized healthcare systems, home care services in Europe are highly localized, with each country maintaining distinct guidelines regarding eligibility, licensing, and service provision. According to the European Commission’s Joint Research Centre (JRC), disparities in home care policies make it difficult for multinational providers to standardize operations and ensure consistent service quality across borders. For example, while Germany has a well-developed statutory framework for home care under its Long-Term Care Insurance (LTCI) system, other countries such as Greece and Bulgaria rely heavily on informal family caregiving due to limited institutional support. Additionally, differences in language, cultural preferences, and patient expectations complicate the implementation of uniform care protocols.

Ensuring Data Privacy and Cybersecurity in Digital Home Care

As digital technologies become integral to home care delivery, ensuring data privacy and cybersecurity has emerged as a critical challenge for the Europe home care market. The increasing use of electronic health records, remote monitoring devices, and telehealth platforms exposes sensitive patient information to potential breaches, raising concerns about data protection and regulatory compliance. Under the General Data Protection Regulation (GDPR), healthcare providers must implement stringent safeguards to protect patient confidentiality, yet many home care organizations lack the necessary infrastructure and expertise to manage cyber risks effectively. Moreover, interoperability issues between different digital platforms used by caregivers, clinicians, and insurers create additional security vulnerabilities.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Henkel AG & Co. KGaA, Unilever PLC, Procter & Gamble Company, Reckitt Benckiser Group PLC, and Church & Dwight Co., Inc. |

SEGMENTAL ANALYSIS

By Product Type Insights

The laundry care segment held the biggest share of the Europe home care market by accounting for 23.4% of total market revenue in 2024. This dominance is primarily attributed to the high frequency of use and essential nature of laundry products in daily household routines across the region. One of the key drivers behind this segment's leadership is the consistent demand for fabric softeners, detergents, and stain removers, particularly in urban households with access to washing machines. Apart from these, the rise in dual-income households has led to an increased reliance on high-performance and time-saving laundry solutions. Another contributing factor is the introduction of premium and eco-friendly formulations by major players such as Henkel (Germany) and Reckitt Benckiser (UK), which have captured consumer interest through sustainability claims and advanced cleaning performance.

The surface care segment is projected to grow at the fastest rate in the Europe home care market, expanding at a CAGR of 6.4%. This accelerated growth is largely fueled by heightened hygiene awareness following the pandemic and a growing emphasis on clean living environments. One of the primary drivers is the increased focus on disinfection and antimicrobial protection in both residential and semi-professional settings. In response, manufacturers like Procter & Gamble and Unilever introduced multi-surface sprays and wipes infused with natural disinfectants like citric acid and essential oils. Besides, the rise in disposable incomes and urbanization rates has encouraged the adoption of premium surface care products, including ready-to-use wipes, foam cleaners, and fragrance-infused formulas.

By Distribution Channel Insights

The supermarkets and hypermarkets segment accounted for the maximum portion of the Europe home care market by capturing a 48.5% of total retail sales in 2024. This is caused by the widespread presence of large retail chains and the convenience they offer in purchasing a wide range of home care products under one roof. A major driver of this segment’s leadership is the high footfall and established supply chain networks of leading supermarket brands such as Carrefour (France), Rewe (Germany), and Tesco (UK). These retailers maintain dedicated home care sections with well-branded products, promotional offers, and private-label alternatives that attract budget-conscious yet quality-driven consumers. Another contributing factor is the integration of loyalty programs and bundled offers , which encourage repeat purchases. For instance, Lidl and Aldi have successfully leveraged competitive pricing strategies to boost home care sales, particularly in Eastern Europe.

The online retail stores segment is witnessing the swiftest development in the Europe home care market, registering a CAGR of 9.2%. This rapid expansion reflects shifting consumer behavior toward digital shopping platforms and the increasing availability of e-commerce-enabled home care solutions. One of the main factors driving this growth is the convenience and accessibility offered by online platforms, allowing consumers to compare prices, read reviews, and order products from home. Additionally, the emergence of subscription-based models and bulk ordering options has enhanced customer retention. Brands like Ecover and Frosch have partnered with online retailers to offer eco-refills and sustainable packaging, aligning with rising environmental concerns among consumers. In Germany and the UK, online home care sales surged due to targeted digital marketing and improved delivery infrastructure.

COUNTRY-LEVEL ANALYSIS

Germany led the Europe home care market by holding 22% of total market revenue in 2024. As the continent’s largest economy and a hub for consumer goods manufacturing, Germany plays a pivotal role in shaping regional home care consumption patterns. One of the primary drivers of Germany’s market position is its well-established retail infrastructure and high consumer spending on branded home care products. Leading German retailers such as Schwarz Group (which operates Lidl and Kaufland) and REWE Group ensure widespread availability of both international and private-label home care items. Apart from these, the country is witnessing a strong shift toward environmentally friendly and concentrated formulations, supported by government policies promoting sustainability.

United Kingdom’s strong consumer base, coupled with a mature retail ecosystem, supports steady demand for a diverse range of home care products. A key factor contributing to the UK’s market strength is the high penetration of premium and eco-conscious brands, particularly among urban consumers. Major retailers such as Tesco, Sainsbury’s, and Boots have expanded their green product lines to cater to this trend. Moreover, the growth of online shopping platforms has significantly influenced purchasing habits.

France is positioning itself as a key player in the regional landscape. The country’s market is characterized by a blend of traditional retail channels and emerging eco-conscious consumer trends. One of the key drivers of France’s home care market is the rising preference for natural and chemical-free cleaning products , especially among younger demographics. These products align with national sustainability goals and consumer demands for safer household alternatives. Apart from these, the expansion of private label home care ranges by major retailers has boosted affordability and accessibility. Carrefour, Leclerc, and Auchan have launched cost-effective yet high-quality cleaning products tailored to French household needs, capturing a substantial portion of the mid-tier market.

Italy contributes significantly to the Europe home care market. The Italian home care sector is shaped by a combination of traditional consumer habits, regional brand preferences, and growing environmental awareness. One of the primary drivers of Italy’s market performance is the strong presence of family-owned brands and artisanal cleaning product producers, which have maintained a loyal customer base. Companies such as Solabiol and Tea Natura have capitalized on consumer demand for locally sourced, natural ingredients, offering plant-based detergents and biodegradable disinfectants. Moreover, the expansion of modern trade formats such as discounters and hypermarkets has facilitated greater product availability. Retailers like Esselunga and Conad have strengthened their home care offerings through exclusive partnerships and in-store promotions, catering to both urban and rural consumers.

Netherlands is positioning itself as a progressive and innovative player within the region. The Dutch market is distinguished by its early adoption of sustainable practices and digital retail integration. One of the key contributors to the Netherlands’ market strength is the high consumer awareness and acceptance of green and zero-waste home care products. Brands like Ecover and Frosch have expanded their presence through eco-certified formulations and recyclable packaging. In addition, the well-developed e-commerce infrastructure supports efficient home care product distribution. Dutch consumers benefit from fast delivery services and extensive online product variety, with Bol.com and Albert Heijn Online leading the digital retail space.

KEY MARKET PLAYERS

Companies playing a prominent role in the European home care market profiled in this report are

- Henkel AG & Co. KGaA,

- Unilever PLC, Procter & Gamble Company,

- Reckitt Benckiser Group PLC,

- Church & Dwight Co., Inc.

TOP LEADING PLAYERS IN THE MARKET

One of the leading players in the Europe home care market is Henkel AG & Co. KGaA, a German multinational corporation known for its extensive portfolio of home care products under well-established brands such as Persil, Purex, and Bref. Henkel plays a pivotal role in shaping industry trends through continuous product innovation, sustainability initiatives, and strong brand positioning across multiple European markets.

Another key player is Reckitt Benckiser Group plc, a UK-based global leader in consumer health and hygiene products. With popular home care brands like Dettol, Lysol, and Veet, Reckitt has a significant presence in both household and disinfectant categories. The company’s strategic focus on health-conscious formulations and digital marketing has reinforced its leadership position in the region.

The third major participant is Procter & Gamble (P&G), an American multinational with a strong foothold in Europe through iconic brands such as Ariel, Lenor, and Mr. Clean. P&G’s emphasis on research and development, eco-friendly packaging, and omnichannel retail partnerships enables it to maintain a competitive edge in the evolving European home care landscape.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe home care market are increasingly focusing on product innovation and formulation upgrades to meet changing consumer expectations around sustainability, effectiveness, and wellness. Companies are launching concentrated formulas, biodegradable packaging, and plant-based ingredients to align with environmentally conscious purchasing behaviors.

Another major strategy involves enhancing digital engagement and e-commerce capabilities. Leading brands are investing in direct-to-consumer platforms, mobile applications, and online retail partnerships to improve customer accessibility and personalize user experiences through data-driven insights and targeted marketing campaigns.

Lastly, companies are strengthening their regional presence through strategic acquisitions and partnerships , particularly with niche sustainable brands or logistics providers. These moves allow them to expand product portfolios, enter new market segments, and optimize supply chain efficiency while reinforcing brand loyalty among discerning European consumers.

COMPETITION OVERVIEW

The Europe home care market is characterized by intense competition among global giants, regional players, and emerging eco-conscious brands. Established multinational corporations dominate due to their strong brand equity, extensive distribution networks, and continuous investment in research and development. However, local and private-label brands are gaining traction by offering cost-effective alternatives tailored to specific national preferences and sustainability demands. Consumers are becoming more informed and selective, prioritizing transparency, ingredient safety, and environmental impact when choosing home care products. This shift has prompted major players to reposition their offerings and emphasize green credentials, often through certifications, recyclable packaging, and carbon-neutral production methods. Additionally, the rise of e-commerce has intensified competition by enabling new entrants to reach consumers directly, bypassing traditional retail barriers. As a result, market participants must continuously innovate, adapt to regulatory changes, and differentiate themselves through branding, formulation, and digital engagement strategies to maintain relevance and market share in this dynamic and evolving sector.

RECENT MARKET DEVELOPMENTS

- In January 2024, Henkel launched a new line of refillable cleaning products across Germany and France, aimed at reducing plastic waste and meeting growing consumer demand for sustainable home care solutions.

- In March 2024, Reckitt Benckiser partnered with a Dutch biotech startup to develop enzyme-based cleaning agents that enhance stain removal while reducing chemical dependency, reflecting its commitment to green innovation.

- In July 2023, Procter & Gamble expanded its e-commerce presence in Southern Europe by forming exclusive distribution agreements with major online retailers in Italy and Spain.

- In November 2023, Ecover introduced a carbon-neutral manufacturing facility in Belgium, marking a major step toward achieving net-zero emissions across its European supply chain.

- In May 2024, Unilever announced the acquisition of a small French eco-cleaning brand to strengthen its portfolio of natural and organic home care products and appeal to environmentally conscious consumers.

MARKET SEGMENTATION

This research report is the europe home care market research report is segmented and sub-segmented into the following categories.

By Product Type

- Air Care

- Dishwashing

- Bleach

- Insecticides

- Laundry Care

- Surface Care

- Toilet Care

- Others

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What are the main factors fueling the Europe home care market’s growth?

The Europe home care market is fueled by an aging population, increased prevalence of chronic diseases, and rapid adoption of telehealth and digital monitoring technologies that enhance care delivery and patient independence.

2. Which barriers are currently limiting the Europe home care market?

Barriers in the Europe home care market include a shortage of skilled caregivers, high turnover rates, fragmented regulations across countries, inconsistent reimbursement models, and growing concerns about data privacy and cybersecurity.

3. Where do the best opportunities for expansion exist in the Europe home care market?

Opportunities in the Europe home care market include integrating AI and smart assistive devices, expanding private home care and insurance coverage, and leveraging digital platforms for efficient patient-caregiver matching and service delivery.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com