Europe Home Healthcare Market Size, Share, Trends & Growth Forecast Report By Product Type (Testing, Screening, & Monitoring Products, Therapeutic Products, Mobility Care Products), Type, Services Type, Software and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Home Healthcare Market Size

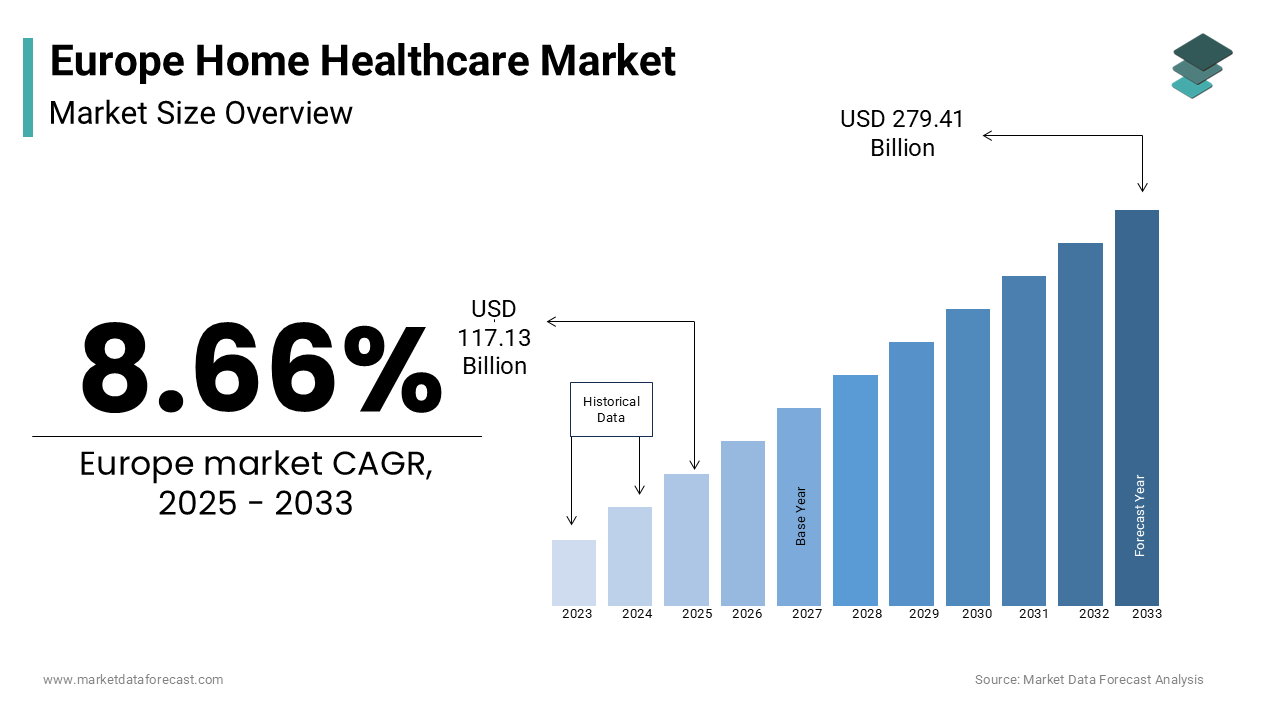

The home healthcare market in Europe was valued at USD 105.07 billion in 2024. The size of the market is estimated to value USD 279.41 billion by 2033 from USD 117.13 billion in 2025, growing at a CAGR of 8.66% during the forecast period.

Home healthcare refers to medical and non-medical services provided to patients in their homes. These services include skilled nursing, physical therapy, chronic disease management, personal care, and the provision of medical equipment. The aging population of Europe is a key factor propelling the demand for home healthcare services in this region. According to Eurostat, more than 21% of the EU population was aged 65 or older in 2022 and projections indicate continued growth in this demographic segment. The rising prevalence of chronic diseases such as diabetes and cardiovascular conditions is further fuelling the need for personalized and home-based care substantially. Additionally, national healthcare systems across Europe are investing in home healthcare solutions to alleviate pressure on hospitals and long-term care facilities. For instance, Germany and France have implemented policies to integrate home healthcare into their public health frameworks to promote its adoption as a viable alternative to institutionalized care.

MARKET DRIVERS

Growing Aging Population in Europe

The increasing proportion of elderly individuals across Europe is a significant driver of the European home healthcare market. According to Eurostat, more than 21% of the EU population was aged 65 or older in 2022, and this percentage is expected to rise to 30% by 2050. Older adults are more prone to chronic illnesses such as cardiovascular diseases, diabetes, and arthritis and require consistent and cost-effective care. Home healthcare offers a viable solution to manage these conditions while minimizing hospital visits and institutional care. Countries such as Germany and Italy have the highest aging populations in Europe and are leading adopters of home healthcare services to meet these growing demands.

Rising Prevalence of Chronic Diseases in Europe

The prevalence of chronic illnesses is another major driver of home healthcare demand in Europe. According to the World Health Organization, non-communicable diseases, including diabetes and respiratory conditions, account for nearly 87% of all deaths in Europe. Chronic diseases often involve long-term care, rehabilitation, and regular monitoring, which makes home healthcare a preferred choice for both patients and healthcare systems. In addition, as per the reports of the European Respiratory Society, chronic respiratory diseases affect over 10% of the population in the EU, which further emphasizes the need for in-home medical services to reduce the burden on traditional healthcare facilities.

MARKET RESTRAINTS

High Costs of Advanced Home Healthcare Services

While home healthcare is often viewed as cost-effective compared to institutional care, the initial setup and delivery of advanced services can be prohibitively expensive. According to a report by the European Commission, healthcare spending in the EU accounted for 9.9% of GDP in 2021 and a significant portion was allocated to chronic disease management and elderly care. However, personalized in-home services, including the use of sophisticated medical devices and telehealth solutions may incur costs that exceed the budgets of middle-income households. This financial barrier limits accessibility, particularly in regions with limited government subsidies for home healthcare initiatives.

Shortage of Skilled Healthcare Professionals

A critical shortage of qualified healthcare workers presents another significant restraint. According to the European Health Union, the EU faces a shortage of approximately one million healthcare professionals and gaps are most evident in nursing and home-based caregiving roles. This workforce deficit results from factors such as aging professionals nearing retirement and insufficient recruitment to meet growing demand. For instance, as per the data of the German Federal Employment Agency, Germany, which is a leader in home healthcare adoption, is currently struggling to fill nearly 40,000 nursing vacancies annually. This shortage impacts service quality and availability, hindering the market’s potential to expand.

MARKET OPPORTUNITIES

Integration of Digital Health Technologies

The adoption of digital health solutions such as telemedicine, remote monitoring devices, and AI-driven diagnostic tools presents a significant growth opportunity. According to the Digital Economy and Society Index of the European Commission, 84% of EU households had internet access in 2021, which enabled the proliferation of telehealth services. Remote patient monitoring devices, such as wearable sensors for chronic disease management are gaining traction due to their convenience and effectiveness. For example, as per a European Respiratory Society report, remote monitoring reduced hospital readmissions for chronic respiratory disease patients by 20% in 2020. This shows the transformative potential of digital health in home care settings.

Governmental Support and Policy Initiatives

The growing focus of European governments on promoting home healthcare solutions is another vital opportunity. The European Commission emphasizes the need for integrated care models under initiatives such as Horizon Europe and allocates significant funding to support healthcare innovation. For instance, as per the German Federal Ministry of Health, the long-term care insurance system of Germany reimburses home healthcare costs, and this benefits over 4 million citizens annually. Similarly, the healthcare reforms of France prioritize aging in place through enhanced in-home care support. These policy-driven investments enhance access and affordability and foster the market’s expansion across the region while addressing the healthcare needs of aging and chronically ill populations.

MARKET CHALLENGES

Uneven Access to Services Across Regions

Disparities in healthcare infrastructure and funding among European countries create uneven access to home healthcare services. According to the European Commission, per capita healthcare expenditure varies significantly, and countries like Germany spend €5,800 annually compared to less than €1,500 in Eastern European nations. This financial gap limits the availability and quality of home healthcare services in underfunded regions and leaves many patients underserved. Additionally, rural areas across the EU, home to about 25% of the population face logistical challenges in accessing home-based care due to limited healthcare networks and transportation difficulties, further exacerbating inequities in service delivery.

Lack of Standardized Regulations Across the EU

The absence of harmonized regulations for home healthcare services poses a critical challenge. Each EU member state has its own policies and reimbursement systems and creating inconsistencies in service provision. For instance, according to the European Health, the fragmented nature of healthcare regulations leads to disparities in care quality, patient safety standards, and professional training requirements. This regulatory complexity increases operational hurdles for providers seeking to expand across multiple countries, restricting regional market growth. As per the reports of the World Health Organization, regulatory fragmentation can delay the adoption of innovative home healthcare solutions, impacting the timely delivery of quality care across Europe.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product Type, Type, Services Type, Software, and Region. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, and the Czech Republic, |

| Key Market Players | Almost Family Inc., Amedisys Inc., General Electric Company (GE), Kinnser Software Inc., Linde Group, Omron Corporation, Roche Holding AG, Philips Healthcare, Mckesson Corporation, LHC Group Inc., Kindred Healthcare, Fresenius Se & Co Kgaa, Abbott Laboratories, and Apria Healthcare Group |

SEGMENTAL ANALYSIS

By Product Insights

The testing screening and monitoring products segment was accounted in holding 44.2% of the Europe home healthcare market share in 2024with the rising prevalence of chronic diseases and the urgent need for continuous remote patient oversight. The widespread adoption of devices such as glucometers pulse oximeters and blood pressure monitors is further accelerated by national health policies promoting decentralized care. Eurostat data from 2022 shows that 78% of individuals aged 65 and older in the EU suffer from at least one chronic condition necessitating routine diagnostics. Additionally, the integration of Bluetooth and smartphone connectivity in home monitoring devices has improved user compliance and data sharing with clinicians.

The mobility segment is lucratively to grow lucratively with an estimated CAGR of 8.2% from 2025 to 2033, with the Europe’s rapidly aging population and increasing demand for independent living solutions. National aging strategies are amplifying this trend with countries like France and the Netherlands allocating significant public funding for home adaptations and assistive devices under long term care reforms.

By Type Insights

The home telehealth monitoring devices segment held 52.3% of the Europe home healthcare market share in 2024 with the tangible nature of hardware solutions that enable real time tracking of vital signs and chronic conditions directly in the patient’s home. According to the World Health Organization, chronic conditions such as diabetes cardiovascular disease and respiratory illnesses account for 87% of all deaths in the European Union making continuous monitoring essential. Additionally, consumer familiarity with wearable technology has accelerated acceptance with Eurostat noting that 34% of EU households owned at least one health monitoring device in 2022 up from 22 percent in 2019. Manufacturers like Withings and Omron have further driven adoption by ensuring seamless integration with national electronic health records and smartphone ecosystems.

The home telehealth software segment is likely to witness a CAGR of 14.3% during the forecast period with the increasing digitization of healthcare systems and the urgent need for interoperable platforms that connect patients clinicians and data streams. Additionally, the shortage of healthcare professionals is accelerating reliance on digital triage and remote consultation tools. Companies such as Liva Healthcare and Doctolib have seen rapid uptake with Doctolib reporting a 200 percent increase in virtual consultations across France Germany and Italy between 2021 and 2023. Furthermore, the General Data Protection Regulation has fostered trust in compliant platforms enabling secure patient engagement. These regulatory technological and workforce dynamics position software as the highest momentum layer in Europe’s evolving home telehealth ecosystem.

By Services Type Insights

The skilled nursing care services segment was the largest by occupying 29.2% of Europe home healthcare market share in 2024 with the complex and growing medical needs of Europe’s aging population which increasingly require professional clinical oversight at home rather than in institutional settings. According to the European Commission, nearly 30 percent of the EU population will be aged 65 or older creating sustained demand for wound care intravenous therapy medication management and post operative monitoring all delivered by licensed nurses.

The respiratory therapy services segment is projected to grow with an expected CAGR of 9.7% in the coming years with the rising burden of chronic respiratory diseases and the post pandemic emphasis on home based pulmonary care. The shift toward home ventilation and oxygen therapy has been reinforced by clinical evidence showing reduced hospital readmissions. National health systems are responding accordingly with the United Kingdom’s National Health Service expanding its Home Oxygen Programme to cover over 90 000 patients annually as reported by NHS England in 2023. Technological advancements such as portable oxygen concentrators and smart inhalers with usage tracking have also enhanced treatment adherence and remote monitoring capabilities.

REGIONAL ANALYSIS

Germany Home Healthcare Market Analysis

Germany was the top performer of the Europe home healthcare market by accounting for 22.2% of share in 2024 with its robust statutory health insurance system which covers over 87 percent of the population and provides comprehensive reimbursement for home nursing chronic disease management and medical equipment. In 2022 more than 2.1 million individuals received formal home care services funded by public insurers as confirmed by the German Federal Ministry of Health. Additionally, the country hosts a dense network of certified home care agencies and advanced telehealth infrastructure with over 60% of providers using integrated clinical management software. Strong regulatory frameworks data privacy compliance under GDPR and high public trust in healthcare institutions further enhance market maturity.

United Kingdom Home Healthcare Market Analysis

The United Kingdom was positioned second by capturing 12.2% of the share in 2024. The NHS Long Term Plan launched in 2019 commits to expanding home based services including virtual wards and integrated care teams which saw a 35 percent increase in home monitoring deployments between 2021 and 2023 as reported by NHS Digital. Social care reforms including the 2023 cap on personal care costs have also improved access for middle income households. Furthermore the UK has witnessed rapid growth in private home care providers with over 12 000 registered agencies operating in England alone according to the Care Quality Commission.

France Home Healthcare Market Analysis

France market is likely to grow with prominent CAGR during the forecast period. The French market thrives on a well established public health framework that fully reimburses home nursing and medical equipment for chronic and post acute patients under the national health insurance system known as Assurance Maladie. Additionally France has a dense network of private home care agencies many of which are integrated with hospital referral systems ensuring seamless care transitions.

Italy Home Healthcare Market Analysis

Italy market growth is anticipated to have steadily in the coming years. Italy’s position is heavily influenced by its status as the oldest population in Europe with 24 percent of residents aged 65 or older and a life expectancy exceeding 83 years. Public funding covers essential nursing and rehabilitation services with over 1.3 million Italians receiving formal home assistance in 2022 according to the Ministry of Health. The National Recovery and Resilience Plan allocated 1.2 billion euros in 2021 specifically for digital transformation in community care accelerating the rollout of remote monitoring and electronic care plans. Additionally the cultural preference for family based caregiving is increasingly complemented by professional home services as female labor force participation rises reducing informal care availability.

COMPETITIVE LANDSCAPE

The Europe home healthcare market features a highly competitive landscape shaped by multinational healthcare technology firms regional service providers and agile digital health startups. Established players such as Philips Healthcare Siemens Healthineers and Medtronic dominate through advanced remote monitoring devices integrated software platforms and strong regulatory compliance across EU member states. These companies leverage deep relationships with national health systems to embed their solutions into publicly funded care models. Simultaneously local home care agencies and telehealth vendors compete on personalized service language adaptation and community based trust particularly in decentralized markets like Germany and the Netherlands. The competitive intensity is further amplified by rapid digital transformation with cloud based clinical management systems and AI enabled analytics becoming key differentiators. Regulatory frameworks such as the EU Medical Device Regulation and GDPR impose high entry barriers favoring incumbents with robust compliance infrastructure.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global home healthcare market include

-

Almost Family Inc.

-

Amedisys Inc.

-

General Electric Company (GE)

-

Kinnser Software Inc.

-

Linde Group

-

Omron Corporation

-

Roche Holding AG

-

Philips Healthcare

-

McKesson Corporation

-

LHC Group Inc.

-

Kindred Healthcare

-

Fresenius SE & Co. KGaA

-

Abbott Laboratories

-

Apria Healthcare Group

Top players in the market

Philips Healthcare

Philips Healthcare is a prominent player in the Europe home healthcare market offering a comprehensive portfolio of remote patient monitoring devices telehealth platforms and respiratory care solutions. The company has strengthened its European position through strategic partnerships with national health systems such as the UK’s NHS and Germany’s integrated care networks to deploy hospital at home programs. Recently Philips launched its updated Home Monitoring Suite with AI driven analytics to support chronic disease management. In the Asia Pacific region Philips actively expands its footprint by tailoring solutions for markets like Japan and Australia where aging populations drive demand for connected care. The company collaborates with local providers to integrate its platforms into national digital health initiatives enhancing its global relevance.

Siemens Healthineers

Siemens Healthineers plays a significant role in the Europe home healthcare sector through its advanced diagnostic and remote monitoring technologies designed for decentralized care settings. The company has invested in cloud based clinical data platforms that enable seamless integration between home and hospital systems across countries like France and the Netherlands. In 2023 Siemens launched a new telehealth collaboration hub in Berlin to accelerate innovation in virtual care workflows.

Medtronic

Medtronic is a key contributor to the Europe home healthcare market particularly in chronic disease management through its insulin pumps cardiac monitors and respiratory support devices used in home settings. The company has reinforced its presence by obtaining CE Mark approvals for next generation remote therapy systems and partnering with European home care agencies to deliver integrated care pathways. Recently Medtronic expanded its Guardian Connect glucose monitoring service across multiple EU countries with real time clinician alerts.

Top strategies used by the key market participants

Key players in the Europe home healthcare market focus on strategic partnerships with public health systems to integrate their solutions into national care pathways. They invest heavily in digital health platforms that enable remote monitoring data interoperability and AI driven clinical decision support. Companies prioritize regulatory compliance and CE Mark certifications to ensure swift market access across diverse EU countries. Product portfolios are continuously enhanced with user friendly designs and multilingual interfaces to address regional preferences. Additionally, firms expand their footprint through localized collaborations in emerging markets while leveraging cloud infrastructure to support scalable and secure home care delivery models.

MARKET SEGMENTATION

This research report on the European home healthcare market has been segmented and sub-segmented into the following categories.

By Product Type

- Testing, Screening, & Monitoring Products

- Therapeutic Products

- Mobility Care Products

By Type

- Home Telehealth Monitoring Devices

- Home Telehealth Services

- Home Telehealth Software

By Services Type

- Rehabilitation Therapy Services

- Infusion Therapy Services

- Unskilled Care Services

- Respiratory Therapy Services

- Pregnancy Care Services

- Skilled Nursing Care Services

- Hospice

- Palliative Care Services

By Software

- Agency Software

- Clinical Management Systems

- Hospice Solutions

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

Which countries contribute significantly to the home healthcare market in Southern Europe?

Spain and Italy are among the key contributors to the home healthcare market in Southern Europe, accounting for a substantial market share.

What are the primary drivers of home healthcare market growth in Europe?

The growing aging population, increasing prevalence of chronic diseases and a rising preference for in-home care are key factors driving the home healthcare market in Europe.

What is the Europe Home Healthcare Market?

The Europe Home Healthcare Market refers to a range of medical, diagnostic, and assistive services provided to patients at home, aimed at improving quality of life, reducing hospital visits, and supporting recovery through personalized care solutions.

What factors are driving the growth of the Europe Home Healthcare Market?

Growth is primarily driven by an aging population, rising prevalence of chronic diseases, increasing healthcare costs, and the expansion of remote monitoring technologies.

Which segment dominates the Europe Home Healthcare Market?

The home care services segment holds the largest share, while telehealth and home diagnostic equipment are emerging as the fastest-growing segments due to increasing adoption of remote care technologies.

Which technologies are transforming home healthcare in Europe?

Technologies such as wearable sensors, IoT-based medical devices, AI-driven monitoring systems, and telemedicine platforms are revolutionizing how healthcare is delivered at home.

What challenges does the home healthcare market face in Europe?

Key challenges include workforce shortages, inconsistent reimbursement policies, regulatory differences between countries, and limited digital literacy among older populations.

Which countries lead the Europe Home Healthcare Market?

Germany, the United Kingdom, France, Italy, and Spain are leading markets, supported by advanced healthcare systems, large elderly populations, and strong government support for home-based care.

What are the major opportunities for market players?

Opportunities include developing affordable home-care devices, AI-based health analytics, robotic assistance for elderly care, and subscription-based remote monitoring services.

What is the long-term outlook for the Europe Home Healthcare Market?

The market is expected to experience sustained growth, driven by technological innovation, patient-centered care models, and governmental focus on reducing hospital dependency through home-based alternatives.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com