Europe Lamps Market Size, Share, Trends, and Growth Analysis Report, Segmented by Product, Type, Application, and Country – Industry Forecast From 2026 to 2034

Market Size, 2025

$1.69 BnMarket Estimate, 2026

$1.76 BnMarket Forecast, 2034

$2.49 BnCAGR, 2026–2034

4.39%Europe Lamps Market Report Summary

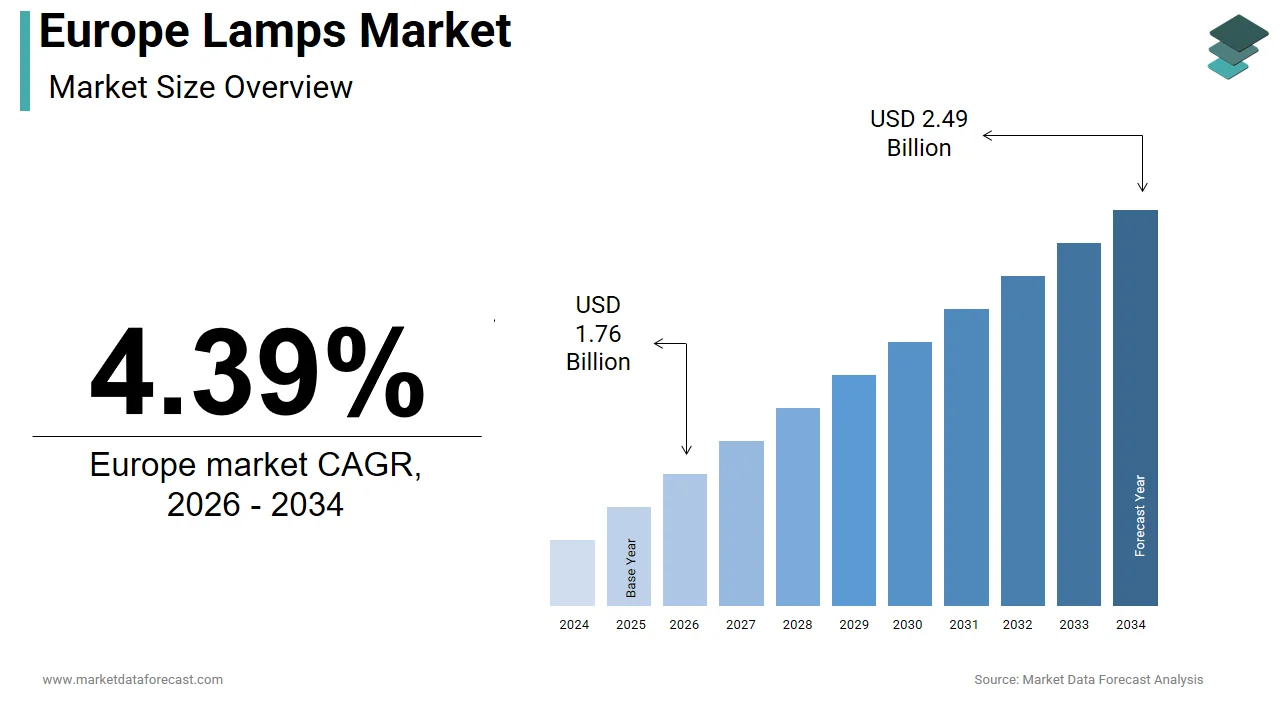

The Europe lamps market was valued at USD 1.69 billion in 2025, is anticipated to reach USD 1.76 billion in 2026, and is projected to reach USD 2.49 billion by 2034, growing at a CAGR of 4.39% from 2026 to 2034. Market growth is driven by rising demand for energy-efficient lighting solutions, increasing investments in residential and commercial infrastructure, and growing consumer preference for aesthetically appealing lighting products. The adoption of LED-based lamps, smart lighting systems, and eco-friendly materials is further supporting market expansion. Additionally, the growing focus on interior design, sustainable living, and customized lighting solutions is strengthening demand across Europe.

Key Market Trends

- Rising adoption of energy-efficient and LED-based lamps to comply with environmental regulations.

- Increasing demand for decorative and designer lighting solutions in residential and hospitality sectors.

- Growing integration of smart lighting and IoT-enabled systems.

- Expansion of sustainable and recyclable lighting materials.

- Rising popularity of customized and modular lighting designs.

Segmental Insights

- Based on product, the floor lamps segment led the Europe lamps market in 2025 by holding 58.7% market share. The segment’s dominance is attributed to rising demand for ambient and task lighting in residential and commercial interiors.

- Based on type, the decorative lamps segment dominated the market by capturing 64.1% share in 2025, supported by increasing consumer focus on home aesthetics, premium lighting designs, and lifestyle-oriented furnishings.

Regional Insights

The Europe lamps market is witnessing steady growth across major economies, supported by strong manufacturing capabilities, energy efficiency initiatives, and expanding urban development.

- Germany led the regional market in 2025 with 19% share, driven by its advanced manufacturing base, stringent energy regulations, and leadership in lighting innovation.

- The United Kingdom ranked second in 2025, supported by strong demand from residential renovation projects and commercial construction activities.

- France is expected to register steady growth over the forecast period, driven by a dual focus on regulatory compliance and design-oriented lighting solutions.

Competitive Landscape

The Europe lamps market is characterized by strong competition among global lighting manufacturers and regional design-focused brands with diversified product portfolios. Market players are focusing on developing smart lighting solutions, enhancing product aesthetics, and improving energy efficiency. Strategic partnerships, continuous product innovation, and expansion of digital sales channels are shaping competitive dynamics across the region.

Prominent companies operating in the Europe lamps market include Panasonic Holdings Corporation, Koninklijke Philips N.V., Signify Holding, Stanley Electric Co. Ltd., ams-OSRAM AG, General Electric Company, Flos SpA, Toshiba Corporation, Siemens AG, Samsung Electronics Co., Ltd., OPPLE Lighting Co Ltd., and Maxlite, Inc.

Europe Lamps Market Size

The size of the Europe lamps market was worth USD 1.69 billion in 2025. The regional market is anticipated to grow at a CAGR of 4.39% from 2026 to 2034 and be worth USD 2.49 billion by 2034 from USD 1.76 billion in 2026.

A lamp is primarily a device designed to produce artificial light or heat. As of early 2026, the European Union consists of a growing number of private households, with a significant, rising trend in single-person households, each functioning as an independent node of lighting demand influenced by diverse cultural, architectural, and regulatory factors. The European Union’s built environment constitutes a massive, diverse stock of residential and non-residential floor space, within which artificial lighting remains a significant component of indoor energy consumption and a key focus for energy efficiency improvements. Driven by stringent sustainability mandates such as the EU Ecodesign Directive, inefficient technologies like incandescent and halogen lamps have been largely phased out, accelerating the dominance of solid-state LED solutions. Simultaneously, urban regeneration projects in cities including Stockholm, Paris, and Vienna are integrating human-centric and adaptive lighting into streetscapes and civic buildings. Consumer preferences further diversify the landscape, Scandinavian minimalism prevails in the North, while ornate and warm ambient fixtures remain popular in Southern Europe. This dynamic interplay of policy, design ethos, technological capability, and end-user behavior defines the contemporary structure of the Europe lamps market.

MARKET DRIVERS

Energy Efficiency Mandates Accelerate LED Adoption

European regulatory frameworks have fundamentally reshaped lighting consumption patterns by systematically eliminating inefficient technologies, which accelerates the growth of the Europe lamps market. Regulatory actions within the European Union have phased out older lighting technologies, including incandescent and halogen bulbs. This policy transition has driven a widespread shift toward light-emitting diode (LED) lighting solutions in residential and commercial settings, contributing to reduced overall lighting electricity consumption and increased household adoption of energy-efficient alternatives. Municipal procurement policies further reinforce this trend, with cities mandating LED-only specifications for street and public building lighting. These measures not only reduce national carbon emissions but also deliver tangible savings on consumer energy bills, creating a dual incentive that sustains robust demand for compliant, high-efficacy lighting solutions.

Rising Demand for Human-Centric and Smart Lighting Solutions

Evolving expectations around well-being and digital integration are redefining product requirements, beyond regulatory compliance, which fuels the expansion of the Europe lamps market. Human-centric lighting, designed to emulate natural daylight cycles and support circadian health, is gaining traction in workplaces, hospitals, and schools across Northern Europe. According to research, office employees exposed to dynamic lighting reported higher concentration levels and reduced fatigue. Concurrently, the expansion of smart homes is driving demand for connected lamps compatible with voice assistants and automation ecosystems. A significant portion of households across Europe now incorporate smart home technology, with connected lighting emerging as a leading category in adoption. The use of smart lighting in Dutch residences has grown, representing a measurable segment of households. The prevalence of connected devices, particularly lighting, indicates a broader shift toward automation in residential environments. Retailers and hospitality venues are also deploying tunable white systems to influence customer mood and extend dwell time. This convergence of behavioral insight and embedded intelligence is compelling manufacturers to prioritize adaptive color temperature, wireless connectivity, and sensor integration in new product development.

MARKET RESTRAINTS

Raw Material Price Volatility Constrains Profit Margins

The production of modern lamps, particularly LEDs, depends heavily on critical raw materials such as rare earth elements, copper, aluminum, and specialized semiconductors, a dependence that represents a major obstacle for the European lamp market. Price instability in these inputs directly impacts manufacturing costs and pricing strategies. Observations indicate that regional sourcing for essential raw materials is heavily concentrated, creating reliance on a single primary supplier for components used in technology manufacturing. Price fluctuations in specialized materials have demonstrated notable increases, raising costs for manufacturing inputs, while an upward trend in copper pricing has driven higher expenses for electrical and thermal management components. These trends suggest increased vulnerability in supply chain continuity and manufacturing costs for electronic components. These pressures disproportionately affect small and medium enterprises lacking hedging capabilities or vertical integration. While consumers may tolerate modest price increases, significant hikes could delay replacement cycles, especially in cost-sensitive markets in Southern and Eastern Europe. Moreover, limited recycling infrastructure for complex lamp assemblies restricts circular economy offsets, leaving manufacturers vulnerable to sustained margin compression unless they innovate in material efficiency or modular architecture.

Fragmented National Standards Impede Cross-Border Scalability

Divergent national certification, labeling, and installation requirements continue to hinder seamless market access, despite EU-level harmonization efforts, and thereby impede the expansion of the Europe lamps market. For example, France enforces additional photobiological safety testing under NF EN 62471, while Germany requires supplementary VDE electrical safety certification beyond the standard CE marking. Variations in regional requirements can increase the time required for product development and enhance testing expenses. Older, non-standard electrical infrastructure necessitates the creation of specific product variants for certain regional markets. Distributors frequently maintain separate inventories to accommodate different product specifications for diverse regional markets. Such fragmentation prevents economies of scale, complicates logistics, and elevates legal risks related to warranty interpretation and liability. Although the EU Single Market aims to eliminate technical barriers, inconsistent enforcement and historical infrastructure disparities sustain operational inefficiencies that particularly disadvantage innovative, low-volume lighting solutions seeking pan-European deployment.

MARKET OPPORTUNITIES

Retrofitting Aging Public Infrastructure Unlocks Large-Scale Contracts

The region’s vast inventory of outdated public lighting signifies a significant growth area for energy-efficient lamp suppliers, which in turn provides a major opening for the growth of the Europe lamps market. A significant portion of public lighting across the European Union continues to use older, inefficient technologies. Municipalities are adopting sustainable financing methods to facilitate the modernization of their lighting systems. Cities are implementing widespread retrofits that transition traditional streetlights to advanced LED systems. These upgrades are resulting in substantial decreases in energy usage for public lighting. National governments are providing targeted funding to support the large-scale improvement of outdoor lighting infrastructure. These projects often incorporate smart controls enabling remote diagnostics, adaptive dimming, and data collection, expanding the scope beyond simple lamp replacement. Manufacturers offering integrated hardware, software, and service packages are best positioned to secure long-term public sector contracts. Public lighting modernization is expected to see steady, high-volume demand throughout the decade, driven by the EU Mission for Climate-Neutral Cities by 2030.

Growing Emphasis on Circularity Fuels Remanufacturing and Take-Back Models

The European Green Deal and Circular Economy Action Plan are compelling lighting companies to adopt closed-loop design principles. This compulsion offers fresh expansion possibilities for the Europe lamps market. European waste management data shows that a significant portion of electronic waste is not being collected for recycling, resulting in a low collection rate relative to the volume of new products placed on the market, which reveals a gap in systemic infrastructure and a substantial, untapped commercial opportunity for resource recovery. Leading firms are responding with certified remanufactured lamp lines where drivers, optics, and heat sinks are restored to original performance standards. Philips Lighting now operates a “Light as a Service” model in several Dutch municipalities, retaining ownership of luminaires and managing end-of-life recovery. According to life cycle assessments, remanufacturing electronic components, such as LED modules, offers a significantly lower carbon footprint than producing new units, confirming that extending product lifespans through repair and reuse is a highly effective strategy for reducing environmental impact. Extended producer responsibility schemes in Sweden and Belgium further incentivize design for disassembly by requiring manufacturers to finance collection and recycling. Startups such as Berlin-based Lumoveto are pioneering modular lamps with standardized interfaces that allow users to replace only failed components. This shift not only aligns with tightening regulatory trajectories but also resonates with B2B clients seeking verifiable environmental credentials, opening new revenue streams beyond traditional product sales.

MARKET CHALLENGES

Intensifying Competition from Low-Cost Asian Imports Undermines Local Producers

The regional lamp manufacturers face escalating pressure from competitively priced imports, predominantly from China and Vietnam, which challenges the growth of the Europe lamps market. These imports benefit from lower labor costs, state subsidies, and massive production scale. The European Union relies heavily on imported electric lighting, with a significant majority of these products sourced from a single Asian nation. Imported lighting products are often priced considerably lower than comparable items produced within Europe. While mandatory compliance markings are required for all electric lamps, the consistency of enforcement and verification across different member states varies. Market surveillance efforts have identified that a notable portion of imported lighting products fail to meet their stated performance, efficiency, or safety claims. This not only distorts fair competition but also risks eroding consumer confidence in LED technology overall. Domestic producers investing in quality, innovation, and local employment struggle to justify premium pricing in retail channels increasingly dominated by opaque online marketplaces. The contraction of Europe’s lighting manufacturing base may persist, undermining supply chain security and future innovation, unless strengthened customs monitoring and anti-dumping measures are implemented.

Consumer Confusion Over Technical Specifications Hinders Premium Segment Growth

Widespread consumer uncertainty regarding key lighting metrics, such as lumens, color rendering index, correlated color temperature, and rated lifetime, affects informed purchasing decisions and the expansion of the Europe lamps market. This is despite technological sophistication. Many European consumers struggle to shift from watt-based thinking to lumen-based purchasing when buying lighting products. This knowledge deficit particularly affects the adoption of higher value lamps featuring advanced attributes like tunable white light or high CRI above 90. Retail environments often exacerbate the problem through inconsistent labeling and minimal in-store guidance. Italian shoppers frequently prioritize visual appeal and packaging aesthetics over technical product performance data when selecting lamps. Online platforms provide more detailed specifications but suffer from information overload and a lack of standardized presentation. Until coordinated consumer education initiatives, potentially mandated under future revisions of the EU energy labeling framework, are implemented, the market will remain skewed toward commoditized, low-cost options, stifling investment in premium, health-oriented, and design-led lighting innovations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Type, Application, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Panasonic Holdings Corporation, Koninklijke Philips N.V., Signify Holding, Stanley Electric Co. Ltd., ams-OSRAM AG, General Electric Company, Flos SpA, Toshiba Corporation, Siemens AG, Samsung Electronics Co., Ltd. (Samsung Group), OPPLE Lighting Co Ltd., Maxlite, Inc., and Others. |

SEGMENTAL ANALYSIS

By Product Insights

The floor lamps segment led the Europe lamps market by holding a 58.7% share in 2025. The dominance of the floor lamp segment is driven by dual functionality as both ambient light sources and design statements in living rooms and hospitality interiors. An additional key driver is the rising trend of flexible living spaces in urban apartments across Western Europe. The prevalence of smaller new residential units in several European nations is increasing the demand for lighting solutions that offer versatility and efficiency in limited spaces. Floor lamps require no permanent installation and offer adjustable illumination without occupying desk surface area, making them ideal for compact dwellings. A different factor is the growing consumer preference for aesthetic customization. Interior designers are increasingly utilizing floor lamps, driven by both their functional, space-saving designs and their ability to complement minimalist or industrial aesthetics. Brands like Flos, Artemide, and Louis Poulsen have capitalized on this by launching limited edition designer floor lamps, which command premium pricing and reinforce the segment’s market leadership.

The desk lamp segment is predicted to witness the highest CAGR of 6.8% between 2026 and 2034 due to the structural shift toward hybrid work models. Remote and hybrid employment remains entrenched across Northern and Western Europe. As per research, hybrid work remains a significant, structural feature of employment for knowledge workers in the EU, with a substantial portion of staff maintaining a mixed, home-and-office routine. This sustained demand for dedicated home office setups has elevated the importance of task-specific lighting. Ergonomic desk lamps with flicker-free LEDs and adjustable color temperatures are now considered essential productivity tools rather than mere accessories. Additionally, educational digitization is amplifying demand among students. UNESCO's 2025 initiatives emphasize a continuing shift towards AI and digital platforms, solidifying screen-based pedagogical practices in schools across Europe as a long-term evolution of learning environments. German national safety regulators, along with European health authorities, increasingly endorse high-fidelity, color-accurate lighting for desk-based work to improve employee visual comfort and focus. Manufacturers such as Ledvance and IKEA have responded with affordable smart desk lamps featuring circadian rhythm modes, further accelerating adoption, particularly in price-sensitive markets like Poland and Portugal.

By Type Insights

The decorative lamps segment was the largest segment in the Europe lamps market by capturing a 64.1% share in 2025. The supremacy of the decorative lamps segment is attributed to the increasing role of interior aesthetics in consumer purchasing behavior. In Europe, consumers are increasingly prioritizing aesthetic, design-focused lighting over purely functional options, leading to higher spending on decorative fixtures. In countries like Italy and France, where heritage craftsmanship and artisanal design remain culturally valued, brands such as Venini and Fontana Arte leverage Murano glass and hand-forged metal to position lamps as collectible home art. A further reinforcing factor is the rise of experiential retail and social media influence. Platforms like Instagram and Pinterest have amplified visual home styling trends, with lighting frequently featured as a focal point. Across Europe, social media platforms are seeing massive engagement with decorative lighting content, as users increasingly showcase lamps as artistic, central, and conversational pieces of interior design. Retailers, including Habitat and Maisons du Monde, now curate seasonal lamp collections aligned with color palettes and mood themes, further embedding decorative lighting into lifestyle consumption patterns.

The reading lamp segment is estimated to register the fastest CAGR of 7.2% over the forecast period, owing to the fact that aging demographics are elevating visual comfort needs, and the proliferation of e-reading and digital textbooks has paradoxically increased demand for physical task lighting. The proportion of older adults within the European population is consistently rising, indicating a long-term shift toward an aging demographic. Natural biological changes in vision associated with aging often lead to a greater need for concentrated, high-intensity light sources to maintain visual clarity. Professional guidance for eye health increasingly emphasizes the importance of specific light levels and focused beam patterns to support tasks like reading. Standard ambient lighting is frequently insufficient for detailed tasks, necessitating the use of specialized lamps designed for glare reduction and precise light distribution. In educational settings, many students maintain a hybrid approach to learning by using physical printed materials in conjunction with digital devices. The continued use of paper alongside screens suggests that learners often rely on tactile media to manage the cognitive demands of studying. This hybrid learning behavior necessitates adjustable luminaires that minimize screen reflections while illuminating paper surfaces. Companies like Beurer and Philips have introduced reading lamps with asymmetric optics and blue light filters specifically targeting this demographic, driving both volume and value growth in the segment.

COUNTRY-LEVEL ANALYSIS

Germany Lamps Market Analysis

Germany was the top performer of the Europe lamps market by holding 19% as of 2025, reflecting its advanced manufacturing base, stringent energy regulations, and leadership in lighting innovation. The country’s transition away from nuclear and fossil fuels under the Energiewende policy has accelerated the adoption of energy-efficient lighting across residential, commercial, and industrial sectors. According to the German Federal Ministry for Economic Affairs and Climate Action, over 87% of public street lighting was converted to LED technology by the end of 2024, significantly driving demand for high-performance luminaires. Additionally, Germany hosts global lighting giants like Osram and serves as a hub for smart lighting R&D, with over 120 patents filed in adaptive and human-centric lighting systems in 2024 alone, as per the European Patent Office. Strong building codes mandating minimum luminaire efficacy, such as the EnEV regulation requiring 100 lumens per watt for new installations.

United Kingdom Lamps Market Analysis

The United Kingdom was ranked second by holding 14.3% of the Europe lamps market share in 2024, with a mature retrofit ecosystem and rapid integration of connected lighting solutions. Following the EU-aligned ban on halogen and fluorescent lamps, the UK saw a 32% year on year increase in LED lamp sales in 2024, according to the Lighting Industry Association. A distinctive driver is the proliferation of smart home adoption. Data from Ofcom indicates that 58% of UK households now use voice-controlled or app-managed lighting systems, creating demand for interoperable LED products with Zigbee or Matter protocol support. Moreover, the government’s Public Sector Decarbonisation Scheme allocated 450 million pounds in 2024 to upgrade lighting in schools, hospitals, and council buildings, prioritizing IoT-enabled fixtures that allow remote monitoring and energy analytics.

France Lamps Market Analysis

France's lamp market growth is growing with a CAGR during the forecast period, with a dual focus on regulatory compliance and design-oriented lighting solutions. The French government’s “Anti Waste for a Circular Economy” law mandates that all public lighting be energy efficient and repairable by 2025, spurring large-scale municipal upgrades. As per ADEME, France’s environment agency, over 2.1 million public luminaires were replaced with LEDs in 2024 alone, thereby reducing municipal electricity consumption by an estimated 1.3 terawatt hours annually. Simultaneously, France maintains a strong heritage in decorative and architectural lighting, with brands like Vibia and Ligne Roset collaborating with designers to merge efficiency with visual artistry. The renovation of historic sites, including Parisian monuments under the “Luminous Heritage” initiative, requires custom luminaires that meet both conservation standards and modern photometric requirements.

Italy Lamps Market Analysis

Italy lamps market growth is anticipated to grow with its global reputation for lighting design and a robust residential renovation cycle. Italian manufacturers, such as Flos, Artemide, and iGuzzini, dominate the premium segment, exporting over 65% of their production while maintaining strong domestic demand fueled by tax incentive schemes. The government’s “Superbonus 110%” program, though scaled back in 2024, still supports energy-efficient home upgrades, including LED lighting retrofits, with over 420,000 households claiming lighting-related deductions in 2024, according to the Italian Revenue Agency. Italy’s lighting culture emphasizes ambiance and spatial harmony, driving demand for tunable white and directional spotlights in both urban apartments and rural villas. Furthermore, Milan’s annual Euroluce fair remains Europe’s most influential lighting exhibition, setting global trends in form and function. This fusion of artisanal craftsmanship, fiscal incentives, and consumer appreciation for light quality ensures Italy’s enduring influence in the high end of the market.

Netherlands Lamps Market Analysis

The Netherlands lamps market growth is growing with a model for circular and smart city lighting integration. Dutch municipalities have pioneered “light as a service” models where providers retain ownership of luminaires and are paid for illumination outcomes rather than product sales. Amsterdam alone has deployed over 100,000 smart streetlights equipped with motion sensors and data hubs as part of its Smart City initiative, reducing energy use by 45% since 2022, according to the City of Amsterdam’s sustainability dashboard. Companies like Signify (formerly Philips Lighting), headquartered in Eindhoven, drive innovation in biodegradable materials and modular designs that simplify disassembly. This systemic commitment to resource efficiency and urban intelligence makes the Netherlands a benchmark for next-generation lighting ecosystems in Europe.

COMPETITIVE LANDSCAPE

Competition in the Europe lamps market is characterized by a dual dynamic between mass market manufacturers and premium design-oriented brands. Large multinational corporations compete on technological sophistication, energy efficiency, and scalable smart lighting platforms while boutique and heritage Italian or Scandinavian firms emphasize aesthetics, craftsmanship, and brand legacy. The entry of low-cost Asian producers has intensified price pressure, particularly in the replacement bulb segment, prompting European players to differentiate through quality certification, sustainability credentials, and integrated services. Regulatory compliance acts as both a barrier and an enabler, favoring established firms with robust testing and certification capabilities. Innovation cycles have accelerated with companies racing to incorporate wireless protocols, voice control, and health-focused lighting features. Distribution strategies vary widely from B2B project sales to omnichannel retail, creating a fragmented yet highly specialized competitive landscape where niche expertise often outweighs scale.

KEY MARKET PLAYERS

The leading companies operating in the Europe lamps market include:

- Panasonic Holdings Corporation

- Koninklijke Philips N.V.

- Signify Holding

- Stanley Electric Co. Ltd.

- ams-OSRAM AG

- General Electric Company

- Flos SpA

- Toshiba Corporation

- Siemens AG

- Samsung Electronics Co., Ltd. (Samsung Group)

- OPPLE Lighting Co Ltd.

- Maxlite, Inc.

TOP PLAYERS IN THE MARKET

- Signify Holding, headquartered in the Netherlands, is a global leader in lighting innovation with deep roots in the European market. The company leverages its legacy as part of Philips to drive advancements in connected LED systems and human-centric lighting. In recent years, Signify has intensified its focus on sustainability, launching circular design initiatives and expanding its Light as a Service model across major European cities. It has also integrated Interact IoT platforms into commercial and municipal projects, enhancing energy efficiency and user experience. These actions reinforce its position as a technology-forward provider shaping the future of professional and consumer lighting across the continent and globally.

- Osram GmbH, based in Germany, combines precision engineering with digital lighting solutions serving automotive, industrial, and general illumination sectors. As a subsidiary of ams OSRAM, the company has accelerated its pivot toward smart lighting components including sensors and visible light communication modules. In Europe, Osram has strengthened partnerships with architectural firms and public infrastructure agencies to deploy adaptive street lighting. Its recent investments in UV-C disinfection lighting and horticultural LEDs demonstrate strategic diversification beyond traditional lamps, reinforcing its relevance in high-growth specialty segments worldwide.

- Flos SpA, an Italian design-driven lighting brand, excels in premium decorative and architectural fixtures. Renowned for collaborations with iconic designers such as Achille Castiglioni and Patricia Urquiola, Flos blends craftsmanship with contemporary aesthetics. The company has expanded its European footprint through flagship showrooms in Paris, Milan, and London while enhancing e-commerce capabilities to reach younger consumers. Recent initiatives include launching carbon-neutral collections and integrating dim to warm LED technology into classic designs. These efforts preserve its heritage while aligning with evolving sustainability and wellness trends influencing global luxury lighting demand.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe lamps market prioritize product differentiation through design innovation and smart connectivity integration. They invest heavily in research and development to embed Internet of Things capabilities, color tuning, and circadian rhythm alignment into residential and commercial luminaires. Sustainability serves as another core strategy, with companies adopting circular economy principles, including modular construction, take-back programs, and remanufacturing. Strategic partnerships with municipalities, architects, and interior designers enable early specification in construction projects. Additionally, firms are expanding direct-to-consumer channels via immersive online platforms and experiential retail spaces to capture shifting purchasing behaviors. Vertical integration of software and hardware ecosystems further strengthens competitive moats, particularly in the professional segment, where lighting-as-a-service models gain traction.

MARKET SEGMENTATION

This research report on the Europe lamps market has been segmented and sub-segmented into the following categories.

By Product

- Desk Lamp

- Floor Lamp

By Type

- Decorative Lamp

- Reading Lamp

By Application

- Commercial/Hospitality

- Residential/Retail

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe lamps market?

The Europe lamps market supplies LED, halogen, and smart lighting for homes and businesses. Energy regulations drive widespread LED adoption across member states.

What drives the Europe lamps market?

EU energy efficiency directives propel the Europe lamps market phasing out inefficient bulbs. Smart home integration accelerates connected lighting demand.

How is the Europe lamps market segmented?

The Europe lamps market segments by technology into LED, CFL, halogen plus applications spanning residential, commercial, and industrial environments.

Which countries lead the Europe lamps market?

Germany, UK, and France dominate the Europe lamps market with mature retail networks and regulatory compliance driving LED penetration.

Why LED dominates the Europe lamps market?

LED lamps offer longevity and efficiency in the Europe lamps market meeting strict EU energy standards while reducing consumer replacement costs.

What role do smart lamps play in the Europe lamps market?

Smart bulbs enable voice control in the Europe lamps market integrating with Alexa and Google Home for automated home lighting experiences.

Which applications define the Europe lamps market?

Residential replaces traditional bulbs while commercial focuses on high-bay and office task lighting in the Europe lamps market.

What challenges face the Europe lamps market?

Supply chain disruptions challenge the Europe lamps market though local manufacturing mitigates semiconductor shortages effectively.

How do regulations shape the Europe lamps market?

Ecodesign directives govern the Europe lamps market mandating minimum efficiency levels and phasing non-compliant halogen technologies

Why decorative lamps grow in the Europe lamps market?

Consumer preference for aesthetics drives decorative filament-style LEDs in the Europe lamps market blending vintage design with modern efficiency.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com