Europe Lateral Flow Assay Market Size, Share, Trends & Growth Forecast Report By Product, Application, Technique, End User and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, From (2026 to 2034)

Market Size, 2025

$2.27 BnMarket Estimate, 2026

$2.44 BnMarket Forecast, 2034

$4.37 BnCAGR, 2026–2034

7.54%Europe Lateral Flow Assay Market Report Summary

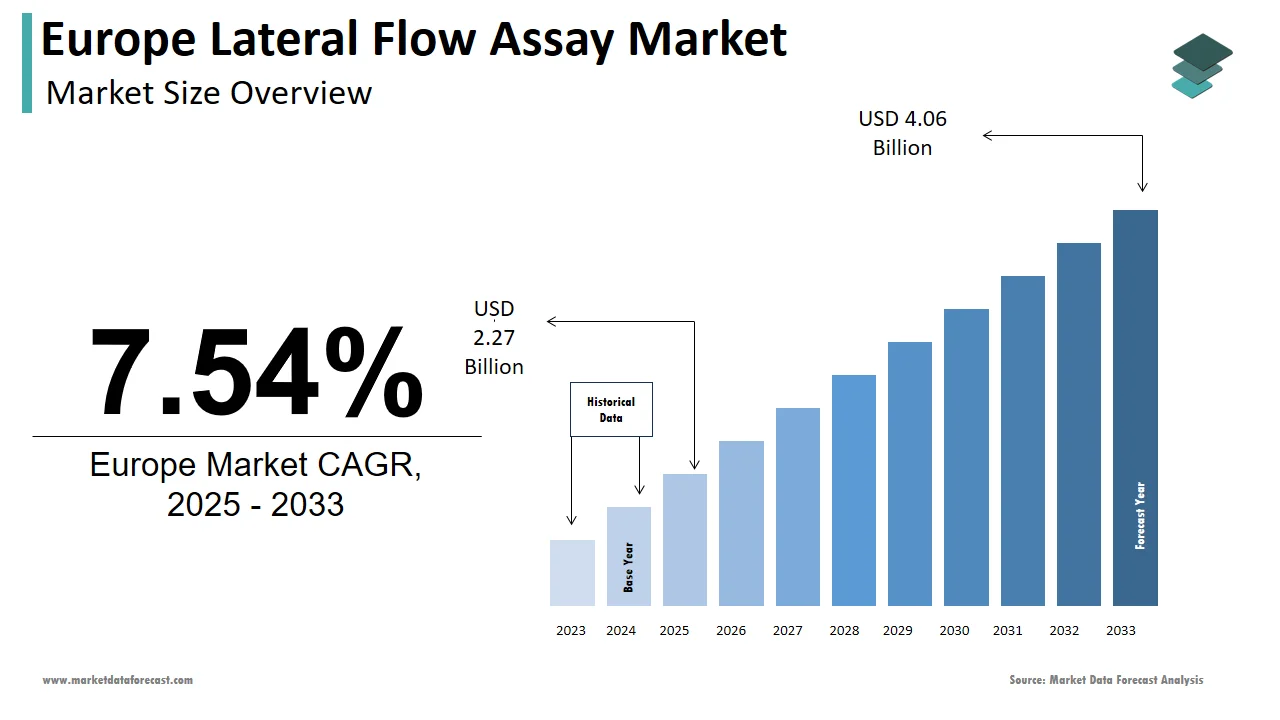

The Europe lateral flow assay market was valued at USD 2.27 billion in 2025, is estimated to reach USD 2.44 billion in 2026, and is projected to reach USD 4.37 billion by 2034, growing at a strong CAGR of 7.54% from 2026 to 2034. The market growth is driven by rising demand for rapid diagnostics, increasing prevalence of infectious diseases, and expanding use of point-of-care testing across Europe’s healthcare systems. Technological advancements in assay sensitivity, growing adoption of at-home testing kits, and enhanced integration of digital diagnostics are further accelerating market expansion across the region.

Key Market Trends

- Increasing shift toward rapid point-of-care diagnostics for infectious diseases, pregnancy testing, and chronic condition monitoring.

- Rising adoption of at-home testing kits and self-diagnostic tools among consumers.

- Expansion of digital diagnostics and smartphone-enabled test interpretation.

- Strong integration of lateral flow assays within public health screening programs.

- Growth in multiplex testing formats enables the detection of multiple biomarkers simultaneously.

Segmental Insights

- Based on product, the kits segment dominated the Europe lateral flow assay market in 2024, capturing a substantial share as kits remain the primary tool for rapid diagnostics across clinical, home-care, and laboratory settings. Their ease of use, affordability, and wide availability continue to drive segment growth.

- Based on application, the clinical segment held the leading share in 2024. This dominance is attributed to the broad use of lateral flow assays in infectious disease detection, cardiovascular biomarker testing, and routine diagnostic workflows in hospitals and primary care settings.

- Based on technique, the sandwich assay segment was the largest in 2024, accounting for a 61.5% share. Its high specificity, capability to detect larger analytes, and strong applicability in infectious and chronic disease diagnostics contribute to its widespread adoption.

- Based on end user, the hospitals and clinics segment held the largest share at 49.4% in 2024, driven by continuous demand for rapid diagnostic tools that support timely clinical decision-making, emergency care, and outpatient screening.

Regional Insights

The Europe lateral flow assay market is experiencing significant growth across major economies, supported by strong public health infrastructure, increasing diagnostic awareness, and rising implementation of point-of-care initiatives.

- Germany led the market, accounting for a 23.7% share in 2024, supported by advanced healthcare systems, high diagnostic testing volumes, and strong adoption of innovative assay technologies.

- The United Kingdom held the second largest position with 18.1% share in 2024, driven by widespread use of rapid tests in primary care, national screening programs, and at-home diagnostics.

- France remains a key player, supported by centralized public health initiatives and strong integration of lateral flow testing across primary and preventive care networks.

- Italy witnessed moderate expansion, driven by regional healthcare modernization efforts and pediatric diagnostic mandates that emphasize rapid testing accessibility.

- The Netherlands is expected to grow steadily from 2026 to 2034 due to its data-driven public health approach and early adoption of digital diagnostic solutions.

Competitive Landscape

The Europe lateral flow assay market is characterized by the strong presence of leading global diagnostic manufacturers and biotechnology firms offering high-sensitivity, rapid-response testing solutions. Companies are focusing on developing advanced multiplex assays, enhancing digital compatibility, and expanding production capabilities to meet regional diagnostic demands. Strategic partnerships with healthcare systems, public health authorities, and digital health platforms are strengthening market competitiveness across Europe.

Prominent companies operating in the Europe lateral flow assay market include Abbott, Alere Inc., F. Hoffmann-La Roche AG, Danaher Corporation, Siemens AG, Becton, Dickinson and Company, bioMérieux SA, Johnson & Johnson, Bio-Rad Laboratories Inc., Thermo Fisher Scientific Inc., QIAGEN N.V., and PerkinElmer Inc.

Europe Lateral Flow Assay Market Size

The lateral flow assay market size in Europe was valued at USD 2.27 billion in 2025. The European market is estimated to be worth USD 4.37 billion by 2034 from USD 2.44 billion in 2026, growing at a CAGR of 7.54% from 2026 to 2034.

Lateral flow assays refer to rapid diagnostic tests that detect the presence or absence of a target analyte, such as antigens, antibodies, or hormones, in a liquid sample through capillary action across a porous membrane strip. Widely employed in infectious disease screening, pregnancy testing, drug monitoring, and veterinary diagnostics, these point-of-care devices deliver results in minutes without requiring laboratory infrastructure. Their design aligns with Europe’s strategic push toward decentralized and accessible diagnostics, particularly in primary care and community settings. Regulatory oversight is governed by the European Union In Vitro Diagnostic Medical Devices Regulation, which mandates rigorous performance validation and post-market surveillance. According to studies, millions of lateral flow tests were distributed across EU member states for respiratory pathogen surveillance, including influenza and RSV, alongside SARS-CoV-2. As per an OECD report, between 54% and 96% of antimicrobial prescriptions in European long-term care facilities were given without laboratory or diagnostic testing, which indicates a significant underutilization of diagnostic tools in certain care settings, rather than high weekly use by GPs. Furthermore, the European Commission’s (and related European Centre for Disease Prevention and Control, ECDC) initiatives and data have consistently highlighted the potential of point-of-care (POC) testing, particularly for C-reactive protein (CRP), to help reduce unnecessary antibiotic prescriptions, especially for respiratory tract infections. These developments underscore how lateral flow assays have evolved from emergency pandemic tools to embedded components of Europe’s public health and clinical diagnostic architecture.

MARKET DRIVERS

Integration into Antimicrobial Stewardship Programs

The systematic adoption of lateral flow assays in European antimicrobial stewardship initiatives is among the key contributors to the growth of the Europe lateral flow assay market. By enabling rapid differentiation between bacterial and viral infections, these tests help clinicians avoid inappropriate antibiotic prescriptions, a vital objective given that thousands of deaths annually in the EU are attributed to antimicrobial-resistant infections. Sweden has a long history of using C-reactive protein (CRP) point-of-care tests (POCTs) in primary care for respiratory infections, though the extent of use varies, and its impact on reducing antibiotic prescriptions is debated in the literature, as per sources. Germany's Antibiotic Resistance Strategy (DART) encourages the appropriate use of point-of-care diagnostics in outpatient settings as part of its efforts to combat antimicrobial resistance. These policy-driven integrations transform lateral flow assays from optional tools into essential clinical instruments, reinforcing routine procurement and embedding them deeply within national healthcare workflows.

Expansion of Self Testing and Consumer Diagnostics Regulations

The formal recognition and regulatory enablement of self-testing through lateral flow assays have significantly broadened their user base beyond clinical settings, which further drives the expansion of the Europe lateral flow assay market. As per research, regulatory changes are making it simpler to market specific in-vitro diagnostic tests, like those for pregnancy, directly to the public, provided they are confirmed safe for use by non-professionals. This shift reflects growing public health emphasis on early detection and prevention. The sale and use of self-administered tests for conditions such as strep A are growing significantly in certain European countries, which emphasizes increased consumer acceptance and demand. Similarly, as per studies, Community-based distribution programs for self-testing kits have become a primary method for identifying new health cases in some regions, demonstrating the effectiveness of widespread access. Governing health bodies are increasingly authorizing a wider variety of consumer-facing diagnostic kits, expanding the range of self-tests available for conditions related to fertility, ovulation, and general infections. The creation of clear regulatory pathways has validated at-home diagnostics, allowing European authorities to tap into a vast new demand channel while simultaneously enabling individuals to take charge of their well-being.

MARKET RESTRAINTS

Stringent Regulatory Requirements Under IVDR

The implementation of the European Union In Vitro Diagnostic Medical Devices Regulation has introduced significant compliance complexities that restrain the growth of the Europe lateral flow assay market. Unlike the previous directive, IVDR mandates comprehensive clinical evidence post-market surveillance and unique device identification for all rapid tests, regardless of risk class. As of October 2023, only 702 IVDR certificates had been issued in total, while 1,551 IVDD (legacy) certificates were still valid. According to research, the percentage of IVDs requiring Notified Body certification is estimated to increase from less than 15% under the IVDD to between 70% and 90% under the IVDR, significantly increasing the regulatory burden. These regulatory hurdles delay innovation, reduce product diversity, and disproportionately impact specialized or low-volume assays essential for rare conditions or veterinary use, thereby constraining market dynamism despite strong clinical need.

Limited Reimbursement for Non-Infectious Disease Applications

Reimbursement policies in the region remain narrowly focused on infectious disease testing, which hampers the growth of the Europe lateral flow assay market. This restricts the adoption of lateral flow assays in other high-potential areas such as cardiac biomarkers, fertility monitoring, and chronic disease management. Public funding for these tests is currently rare across the European Union. Reimbursement often depends on the test's intended use and location rather than the specific technology involved. Similarly, National health systems may not cover certain types of health-related tests, even those supporting significant health planning efforts. Uncertainty regarding public funding represents a major obstacle for companies looking to introduce new lateral flow test applications into the market. The absence of financial incentives drives clinicians and patients toward established laboratory options for non-acute conditions, which hinders innovation in preventive and chronic care diagnostics and confines the market to addressing only episodic infectious diseases.

MARKET OPPORTUNITIES

Development of Multiplex and Quantitative Lateral Flow Platforms

The emergence of advanced lateral flow technologies capable of detecting multiple analytes or providing semi-quantitative results provides a transformative opportunity for the growth of the Europe lateral flow assay market. Traditional lateral flow assays are qualitative, but next-generation platforms incorporating nanomaterials, digital readers, and microfluidics now enable simultaneous detection of influenza, RSV, and SARS-CoV-2 from a single sample. The innovations bridge the gap between rapid testing and laboratory accuracy, aligning with Europe’s demand for precision point of care tools and opening new clinical pathways in chronic and complex disease management.

Adoption in Veterinary and Food Safety Surveillance

The growing deployment of these assays in veterinary diagnostics and foodborne pathogen screening represents a potential opportunity for the expansion of the Europe lateral flow assay market. European regulations mandate rapid monitoring of contaminants such as aflatoxins, Salmonella, and antibiotics in the food chain, creating consistent demand for field-deployable tests. The European Food Safety Authority (EFSA) and the European Commission focus on regulating Maximum Residue Limits (MRLs) for contaminants like pesticides and heavy metals and monitoring the Rapid Alert System for Food and Feed (RASFF) incidents, rather than tracking a specific number of lateral flow kits used by member states. Germany's Federal Office of Consumer Protection (BVL) published a report in October 2024 highlighting the country's success in significantly minimizing the use of antibiotics in animals, a reduction achieved through mandatory reporting and monitoring programs where treatment frequency is benchmarked. The EU's Farm to Fork Strategy's emphasis on traceability and safety creates a stable and growing market for non-human applications, one that is not affected by healthcare reimbursement fluctuations.

MARKET CHALLENGES

Analytical Sensitivity and False Negative Risks

Analytical sensitivity, particularly in low viral load or early infection scenarios, can result in false negative outcomes, which challenges the growth of the Europe lateral flow assay market. During the 2023 RSV outbreak, rapid antigen tests used by the UK Health Security Agency were less effective at detecting the virus in young children compared to laboratory-based PCR tests. Similarly, as per research, rapid tests for strep A infections might not reliably identify all positive cases, especially in individuals who do not show symptoms. These performance gaps erode clinician confidence. Medical professional bodies, such as Germany's Association of Statutory Health Physicians, have observed a strong preference among doctors for using more definitive PCR tests to confirm negative rapid test results in vulnerable patient populations. Hesitation in critical diagnostic decisions persists because, despite increasing accuracy in new generations, medical professionals remain wary of legacy perceptions and performance disparities among different brands. Lateral flow assays will only become definitive diagnostics in complex or high-stakes clinical situations when their sensitivity is improved through innovations like signal amplification or digital quantification to the levels of molecular methods.

Supply Chain Fragility for Critical Raw Materials

The region’s vulnerability towards disruptions in the supply of specialized raw materials hinders the expansion of the Europe lateral flow assay market. The raw materials include nitrocellulose membranes, gold nanoparticles, and monoclonal antibodies, which are sourced from a limited number of global suppliers. Apart from these, the cost of colloidal gold rose following mining restrictions in South Africa, directly impacting test affordability. These dependencies expose manufacturers to price volatility, delivery delays, and quality inconsistencies, which in turn affect regulatory compliance and public health readiness. Europe's capacity for rapid diagnostics continues to be susceptible to uncontrollable external shocks unless strategic stockpiling or regional manufacturing initiatives are implemented.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, Technique, End User, Country. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Abbott, Alere Inc., F. Hoffmann-La Roche AG, Danaher Corporation, Siemens AG, Becton, Dickinson and Company, bioMérieux SA, Johnson & Johnson, Bio-Rad Laboratories Inc., Thermo Fisher Scientific Inc., QIAGEN N.V., and PerkinElmer Inc. |

SEGMENTAL ANALYSIS

By Product Insights

The Kits segment dominated the Europe Lateral Flow Assay Market and captured a substantial share in 2024. The dominance of the kits segment is attributed to their simplicity, cost-effectiveness, and direct applicability in point-of-care and self-testing settings. These single-use disposable devices require no instrumentation and deliver visual results within minutes, making them ideal for mass screening and primary care environments. Regulatory frameworks also favor kits. Under the EU In Vitro Diagnostic Regulation, most Class A and B devices are kit format and benefit from simplified conformity routes when intended for professional or self-use. Their minimal training requirements and compatibility with decentralized care models ensure kits remain the backbone of rapid diagnostic deployment across clinical, consumer, and veterinary domains.

The reader segment is anticipated to witness the fastest CAGR of 14.6% from 2026 to 2034 due to the demand for objective quantitative results and digital integration in clinical decision-making. Unlike visual interpretation, readers use optical or electrochemical sensors to measure test line intensity, enabling semi-quantitative or fully quantitative analysis. Apart from these, multiplex assays detecting three or more analytes now require readers for accurate signal discrimination, a need amplified by the EU’s emphasis on syndromic testing for respiratory and gastrointestinal pathogens. The introduction of reimbursement codes for digital diagnostics in France and Germany is shifting readers from specialized accessories to vital diagnostic tools.

By Application Insights

The clinical segment led the Europe Lateral Flow Assay Market by capturing a significant share in 2024, as rapid tests are deeply integrated into infectious disease management, pregnancy care, and chronic condition monitoring across healthcare systems. General practitioners rely on these assays for immediate decision support, to reduce unnecessary referrals and antibiotic misuse. As per studies, many primary care physicians in the EU used rapid diagnostic tests at least once per week, with strep A, influenza, and urinary tract infection tests being the most common. National antimicrobial resistance action plans have institutionalized their use. The European Centre for Disease Prevention and Control also mandates rapid screening in long-term care facilities during outbreaks, ensuring consistent public sector demand. This systemic embedding across prevention, diagnosis, and public health surveillance solidifies clinical use as the market’s core pillar.

The food safety segment is likely to experience the fastest CAGR of 12.3% over the forecast period. The rapid expansion of the food safety segment is driven by stringent EU regulations on contaminants and the need for rapid on-site screening across the agri-food supply chain. The Farm to Fork Strategy’s emphasis on traceability and prevention further accelerates adoption as retailers like Carrefour and Aldi mandate supplier testing. Lateral flow assays (LFAs) are increasingly integrated into HACCP protocols, providing a scalable, frontline defense against foodborne pathogens whose outbreaks represent a significant cost to the EU.

By Technique Insights

The sandwich segment was the largest in the Europe Lateral Flow Assay Market and occupied a 61.5% share in 2024. Its high sensitivity, specificity, and suitability for detecting larger analytes such as proteins and antigens make it ideal for infectious disease and cardiac biomarker testing, thereby boosting the expansion of the segment. In this format, the target analyte is captured between two antibodies, creating a visible signal only when the analyte is present, which minimizes false positives. The technique is also preferred in veterinary diagnostics. Its compatibility with visual and digital readouts ensures continued dominance across both professional and consumer applications.

The multiplex segment is on the rise and is expected to be the fastest-growing segment in the market, projected to grow at a CAGR of 15.8% from 2026 to 2034 as healthcare systems shift toward syndromic testing to differentiate co-circulating pathogens with overlapping symptoms. These assays detect multiple analytes simultaneously on a single strip, a vital advantage during respiratory and gastrointestinal outbreak seasons. Research from 2023 linked to two European hospitals proposed that using a rapid antigen test for SARS-CoV-2/influenza, in place of the RT-PCR test, might reduce the unnecessary time patients spend in isolation. The study's findings indicated that rapid tests could be a more effective way to handle rules for isolating patients, possibly allowing for quicker access to resources. This points to a potential move toward using speedier ways to diagnose and manage highly contagious illnesses within hospitals. Multiplexing advances rapid diagnostics to the next level, which offers the precise pathogen identification required for effective antimicrobial stewardship and outbreak response.

By End User Insights

The hospitals and clinics segment held the leading share of 49.4% of the Europe lateral flow assay market in 2024 due to their role as first points of clinical contact and their integration into national diagnostic and antimicrobial stewardship protocols. Emergency departments, primary care centers, and outpatient clinics routinely deploy rapid tests to triage patients, guide therapy, and prevent hospital-acquired infections. As per sources, hospitals across the European Union have generally established standard procedures for the prompt identification of respiratory and urinary infections. Several nations have successfully implemented mandatory rapid testing programs in specific medical fields, such as Italy in pediatrics, which has led to a noticeable decrease in unneeded antibiotic prescriptions. This institutional adoption, driven by clinical utility, regulatory support, and cost containment, ensures hospitals and clinics remain the primary deployment environment for rapid diagnostics.

The home care segment is expected to exhibit a noteworthy CAGR of 13.9% from 2026 to 2034, owing to factors such as regulatory liberalization, consumer empowerment, and public health strategies promoting self-testing. The European Commission’s 2023 amendment to the In Vitro Diagnostic Regulation formally recognized certain lateral flow tests as suitable for layperson use, provided they meet usability and accuracy thresholds. Digital companion apps now enhance interpretation. Home-based rapid diagnostics are becoming a cornerstone of Europe's transition to preventive, patient-centered care, driven by an aging population, prevalent chronic diseases, and expanded telehealth services.

COUNTRY LEVEL ANALYSIS

Germany Lateral Flow Assay Market Analysis

Germany led the Europe lateral flow assay market and captured a 23.7% share in 2024. Its robust healthcare infrastructure, strong regulatory framework, and proactive public health policies are propelling the German market. The country operates one of Europe’s most extensive networks of outpatient clinics where rapid tests are routinely used for respiratory and urinary infections under national antimicrobial stewardship guidelines. According to studies, millions of lateral flow tests were reimbursed through statutory insurance, which covers HIV, hepatitis, strep A, and CRP. Germany also hosts key diagnostic manufacturers and research institutes. The Paul Ehrlich Institute maintains rigorous performance validation, ensuring high clinical trust. Germany's top position is supported by its integrated ecosystem of regulation, innovation, and reimbursement, which is bolstered by digital health legislation that mandates interoperability and government investment in point-of-care diagnostics for rural areas.

United Kingdom Lateral Flow Assay Market Analysis

The United Kingdom held the second largest position in the Europe Lateral Flow Assay Market by accounting for an 18.1% share in 2024. The growth of the UK market is driven by its large-scale public health deployment and progressive self-testing policies. The National Health Service continues to distribute free rapid tests for respiratory viruses to vulnerable groups under its seasonal protection programs. The UK also pioneered community-based HIV self-testing; a notable share of new diagnoses in 2023 originated from home kits distributed through pharmacies and online portals. Post Brexit, the UK retained alignment. The UK maintains extensive use of both clinical and consumer healthcare options, due to the deep integration of telehealth and the broad public acceptance of home-based diagnostic tools.

France Lateral Flow Assay Market Analysis

France remains a key player in the Europe Lateral Flow Assay Market, with centralized public health initiatives and strong primary care integration. The government has a large-scale plan requiring doctors to use quick tests for sore throats, affecting millions of yearly visits. The national health insurance system fully covered millions of these rapid tests for patients in 2023. France also leads in veterinary diagnostics. Under a combined human and animal health initiative, a dedicated agency used many thousands of rapid tests to monitor diseases in farm animals. Regulatory support is robust, with the regulatory body for medical products having accelerated its approval process for personal use self-tests, including those for HIV and fertility. This coordinated approach across human animal, and public health ensures France remains a high-volume and high-compliance market.

Italy Lateral Flow Assay Market Analysis

Italy witnessed moderate expansion in the Europe Lateral Flow Assay Market, with growth fuelled by regional healthcare modernization and pediatric diagnostic mandates. According to sources, Italian regional health authorities broadly procured many rapid tests for identifying respiratory and urinary pathogens. Italy also faces high burdens of vector-borne diseases. Specific Italian regions, including Lazio and Veneto, used numerous dengue and chikungunya rapid tests for public health monitoring during the summer months. The Italian Medicines Agency implemented measures to simplify the regulatory transition for diagnostic tests produced within local health institutions. Italy's market for self-tests is increasingly moving beyond hospitals and clinics, supported by a wide-reaching pharmacy network and greater adoption in long-term care facilities.

Netherlands Lateral Flow Assay Market Analysis

The Netherlands is predicted to grow in the Europe lateral flow assay market from 2026 to 2034 due to its data-driven public health approach and early adoption of digital diagnostics. The National Institute for Public Health and the Environment actively promoted the widespread use of rapid tests in critical areas like nursing homes, schools, and transportation hubs to monitor the spread of respiratory viruses such as influenza, RSV, and SARS-CoV-2. The country is a leader in digital integration. Medical centers, such as those at the University of Amsterdam, introduced advanced technology to link rapid test devices directly to centralized surveillance systems, which allows for automatic and timely reporting of results. The Netherlands also pioneered multiplex testing in community pharmacies, where pharmacists conduct triplex respiratory panels under collaborative care agreements. This fusion of innovation policy and frontline practice positions the Netherlands as a high-impact market despite its smaller population size.

COMPETITIVE LANDSCAPE

Competition in the Europe Lateral Flow Assay Market is highly dynamic, involving multinational diagnostics leaders, regional innovators, and specialized rapid test developers. The enforcement of the In Vitro Diagnostic Regulation has intensified pressure on smaller firms while creating opportunities for established players with robust regulatory and manufacturing infrastructure. Differentiation is increasingly based on analytical performance, digital connectivity, and clinical validation rather than price alone. Large companies leverage global scale to accelerate IVDR certification and cross-sell into existing diagnostic ecosystems, while agile startups focus on niche applications such as veterinary or environmental testing. Public sector procurement remains a critical battleground with national health agencies favoring vendors that offer end-to-end solutions, including training, data management, and supply reliability. The ability to provide accurate, user-friendly, and interoperable rapid diagnostics will be key to competitive leadership in Europe's evolving market, which is shifting toward decentralized and preventive care.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe lateral flow assay market include

- Abbott

- Alere Inc.

- Hoffmann-La Roche AG

- Danaher Corporation

- Siemens AG

- Becton, Dickinson and Company

- bioMérieux SA

- Johnson & Johnson

- Bio-Rad Laboratories Inc.

- Thermo Fisher Scientific Inc.

- QIAGEN N.V.

- PerkinElmer Inc.

TOP PLAYERS IN THE MARKET

- Abbott Laboratories is a global leader in diagnostic solutions with a strong presence in the Europe Lateral Flow Assay Market through its BinaxNOW and Panbio rapid test portfolios. The company supplies antigen and antibody tests for infectious diseases, including influenza, dengue, and SARS-CoV-2, to hospitals, pharmacies, and public health agencies across the EU. The company also launched a digital reader compatible with its Panbio tests in Germany and France, enabling quantitative results for respiratory panels. These initiatives reinforce Abbott’s commitment to regulatory alignment, digital integration, and scalable point of care diagnostics across diverse European healthcare settings.

- Roche Diagnostics actively participates in the Europe Lateral Flow Assay Market with its rapid test solutions for infectious diseases, cardiac markers, and drugs of abuse. The company leverages its extensive distribution network to deliver professional use assays to hospitals and laboratories in over 30 European countries. It also partnered with primary care networks in the Netherlands and Sweden to integrate rapid diagnostics into antimicrobial stewardship programs. Roche bolsters its role as a trusted diagnostic partner in acute and preventive care by adapting its portfolio to align with Europe's evolving public health priorities and regulatory landscape.

- Siemens Healthineers contributes to the Europe Lateral Flow Assay Market through its Clinitek and Multistix rapid testing platforms used in urinalysis and point-of-care screening. While traditionally strong in clinical chemistry, the company has expanded its lateral flow offerings to include infectious disease and fertility tests tailored for European primary care and home use segments. It also enhanced its IVDR technical documentation for all rapid assays, ensuring timely recertification. These actions demonstrate Siemens’ strategic pivot toward integrated diagnostic ecosystems that combine simplicity with digital continuity in decentralized care models.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Lateral Flow Assay Market prioritize achieving full compliance with the In Vitro Diagnostic Regulation to ensure product continuity and market access. They invest in digital reader development to enable quantitative analysis and electronic health record integration, enhancing clinical utility. Companies expand manufacturing and logistics capabilities within the EU to mitigate supply chain risks and meet local content preferences. Strategic collaborations with public health agencies, primary care networks, and pharmacies facilitate large-scale deployment and reimbursement acceptance. Additionally, they focus on multiplex assay innovation to address syndromic testing needs and differentiate offerings in a competitive landscape increasingly driven by precision and interoperability.

MARKET SEGMENTATION

This Europe lateral flow assay market research report is segmented and sub-segmented into the following categories.

By Product

- Reader

- Kit

By Application

- Clinical

- Veterinary

- Drug Development

- Food Safety

By Technique

- Competitive

- Multiplex

- Sandwich

By End User

- Hospitals and Clinics

- Home Care

- Diagnostic Laboratories

- Pharmaceutical and Biotechnology Companies

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors drive growth in the europe lateral flow assay market?

Growth is driven by demand for rapid diagnostics, chronic disease prevalence, and supportive regulatory frameworks in the europe lateral flow assay market

2. Which countries lead the europe lateral flow assay market?

Germany, the UK, and France lead the europe lateral flow assay market due to advanced healthcare infrastructure and high adoption rates

3. How does regulation impact the europe lateral flow assay market?

The IVDR regulation strengthens product quality and transparency in the europe lateral flow assay market, influencing manufacturer compliance

4. What are the main applications of lateral flow assays in europe?

Key applications include infectious disease testing, cancer diagnostics, cardiovascular health, and self-testing in the europe lateral flow assay market

5. How is technology influencing the europe lateral flow assay market?

Advancements in reagent technology and digital lateral flow readers are enhancing sensitivity and data integration in the europe lateral flow assay market

6. What role does self-testing play in the europe lateral flow assay market?

Self-testing kits for pregnancy, fertility, and allergy screening are expanding consumer access in the europe lateral flow assay market

7. How does healthcare infrastructure affect the europe lateral flow assay market?

Robust healthcare systems in europe facilitate widespread lateral flow assay adoption across hospitals, clinics, and point-of-care settings

8. Are lateral flow assays cost-effective in europe?

Yes, the europe lateral flow assay market benefits from cost-effective testing solutions that reduce diagnostic time and resource needs

9. How important is research collaboration in the europe lateral flow assay market?

Research collaborations drive innovation and market growth in the europe lateral flow assay market by developing advanced diagnostic solutions

10. Which diseases are most commonly targeted in the europe lateral flow assay market?

Infectious diseases, cancer, diabetes, and cardiovascular diseases are primary targets in the europe lateral flow assay market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com