- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

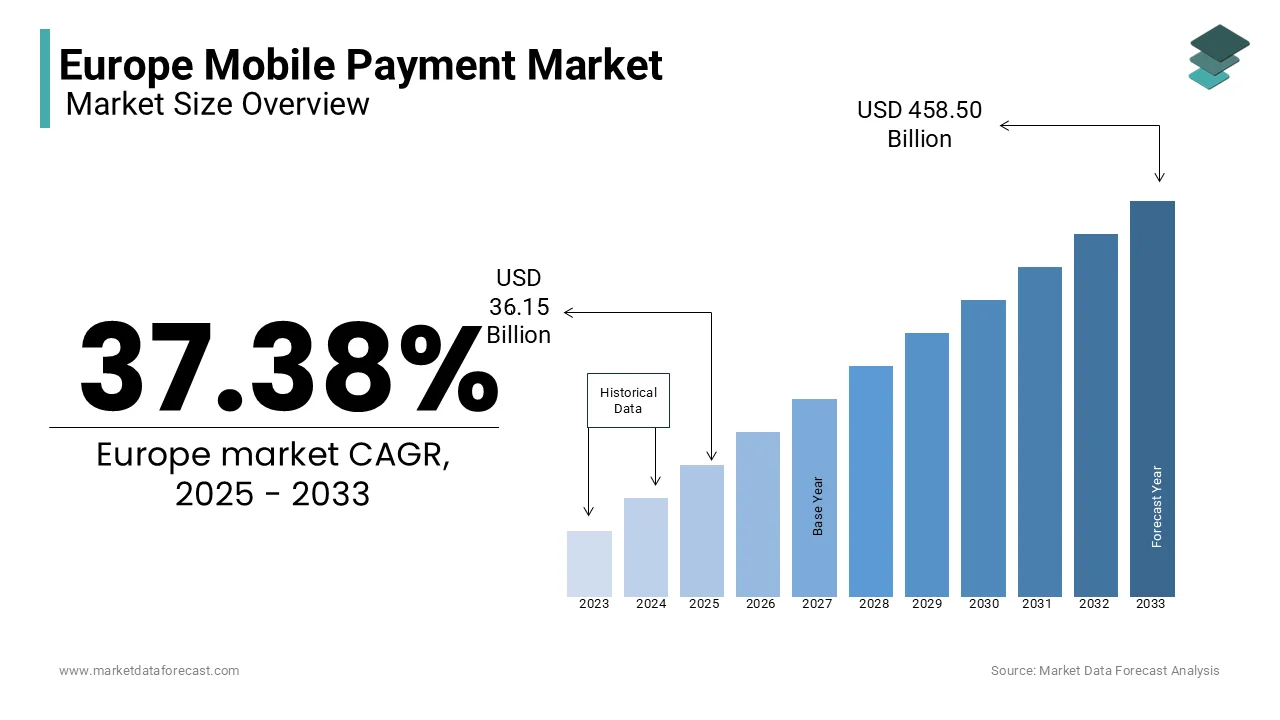

Market Size, 2025

$36.15 BnMarket Estimate, 2026

$49.66 BnMarket Forecast, 2034

$630.12 BnCAGR, 2026–2034

37.38%Europe Mobile Payment Market Report Summary

The Europe mobile payment market was valued at USD 36.15 billion in 2025, is estimated to reach USD 49.66 billion in 2026, and is projected to reach USD 630.12 billion by 2034, growing at a CAGR of 37.38% from 2026 to 2034. Market growth is driven by increasing smartphone penetration, rising adoption of digital wallets, and growing demand for fast and secure contactless payment solutions. Mobile payments enable consumers to conduct financial transactions through smartphones using technologies such as near field communication (NFC), QR codes, and mobile banking applications. The expansion of e-commerce, increasing fintech innovation, and supportive regulatory initiatives promoting digital payments are further accelerating market expansion across Europe.

Key Market Trends

- Increasing adoption of contactless and digital wallet payment solutions.

- Rapid growth of mobile commerce and online retail transactions.

- Expansion of fintech innovation and mobile banking applications.

- Rising consumer preference for cashless and convenient payment methods.

- Increasing integration of biometric authentication and secure payment technologies.

Segmental Insights

- Based on technology, the Near Field Communication (NFC) segment dominated the Europe mobile payment market by accounting for 58.2% share in 2025, driven by the widespread availability of contactless payment terminals and NFC-enabled smartphones.

- Based on payment type, the business-to-consumer (B2C) segment held a significant share in 2025, supported by increasing consumer transactions across retail, entertainment, and service platforms.

- Based on end use, the retail and e-commerce segment led the market by capturing 48.3% share in 2025, driven by the growing adoption of mobile payments in online shopping and physical retail environments.

Regional Insights

The Europe mobile payment market is experiencing rapid growth across major countries due to strong fintech ecosystems, increasing digital adoption, and expanding contactless payment infrastructure.

- The United Kingdom led the regional market in 2025 with 22.3% share, supported by early adoption of contactless payment infrastructure and strong fintech innovation.

- Germany is witnessing strong growth due to its transition from a traditionally cash-dominated society toward a rapidly digitizing payment ecosystem.

- France is expected to grow steadily over the forecast period, supported by the strong involvement of traditional banks and financial institutions in promoting mobile payment adoption.

Competitive Landscape

The Europe mobile payment market is highly competitive and characterized by the presence of global technology companies, fintech firms, and payment network providers. Market participants are focusing on enhancing digital wallet capabilities, improving transaction security, and expanding cross-platform payment ecosystems. Strategic partnerships with financial institutions, retailers, and fintech startups are shaping competitive dynamics across the region.

Prominent companies operating in the Europe mobile payment market include Google LLC, Alipay, Amazon.com, Inc., Apple Inc., C-SAM, Inc., Tencent Holdings Ltd., MoneyGram International Inc., PayPal Holdings, Inc., Samsung Group, and Visa, Inc.

Europe Mobile Payment Market Size

The Europe mobile payment market was worth USD 36.15 billion in 2025. The European market is estimated to reach USD 630.12 billion by 2034 from USD 49.66 billion in 2026, growing at a CAGR of 37.38% from 2026 to 2034.

The mobile payment is a financial ecosystem, where monetary transactions are executed via mobile devices utilizing near field communication, quick response codes, and mobile banking applications. As per Eurostat data from 2023, approximately 91% of individuals in the European Union aged 16 to 74 used the internet regularly, with mobile devices accounting for over 60% of all web traffic. This ubiquitous connectivity creates a fertile ground for contactless payment adoption. The European Central Bank notes that the volume of non-cash payment transactions surpassed 105 billion in 2022, reflecting a decisive societal move away from physical currency. Furthermore, the Revised Payment Services Directive has standardized security protocols and mandated open banking, which shapes the operational frameworks for mobile wallet providers. Governments across the continent are actively promoting cashless initiatives to enhance tax transparency and reduce the costs associated with physical money handling.

MARKET DRIVERS

Ubiquitous Smartphone Penetration and Advanced Network Infrastructure

The widespread availability of sophisticated smartphones coupled with the rapid deployment of fifth-generation wireless networks is propelling the growth of Europe mobile payment market. Modern mobile devices serve as the essential hardware gateway for digital wallets requiring specific sensors, such as near field communication chips and biometric authentication modules, which are now standard in mid-range and premium handsets. According to the Global System for Mobile Communications Association, over 85% of the population in Western Europe owned a smartphone in 2023, creating a massive installed base capable of supporting mobile payment applications. The rollout of fifth-generation networks further accelerates this trend by providing the ultra-low latency and high bandwidth necessary for real-time transaction verification and enhanced security features. Data from the European Telecommunications Standards Institute indicates that fifth-generation coverage now reaches over 60% of populated areas in major European economies, ensuring reliable connectivity even in dense urban environments. This technological foundation allows consumers to execute payments instantly without fear of network failures or delays. The integration of advanced operating systems also enables seamless updates for security patches, which maintains user confidence in the safety of their financial data.

Regulatory Frameworks Promoting Open Banking and Contactless Limits

The progressive regulatory environment established by the European Union, which actively encourages competition and innovation in the payments sector through legislative measures. This factor is additionally boosting the growth of Europe mobile payment market. The Revised Payment Services Directive has been instrumental in dismantling monopolies held by traditional banks by mandating that financial institutions provide third-party providers with secure access to customer account data upon consent. As per the European Commission, over 5000 registered third-party providers were operating across the European Economic Area in 2023, leveraging these regulations to offer innovative mobile payment solutions. This legislative push has stimulated a surge in competition, where fintech startups and big tech companies can build services that compete directly with traditional card schemes. Furthermore, national regulators have significantly increased the transaction limits for contactless payments to accommodate growing consumer demand for touchless interactions. Data from the European Payments Council reveals that the average contactless limit across major European markets rose to 50 euros or higher in 2023, facilitating higher-value transactions via mobile devices without requiring additional authentication steps. These regulatory adjustments reduce friction at the point of sale and encourage both merchants and consumers to adopt mobile terminals and wallets. The clarity provided by strong customer authentication requirements has also increased trust in digital channels. This supportive legal framework ensures that the mobile payment ecosystem continues to evolve with reduced barriers to entry and enhanced consumer protection.

MARKET RESTRAINTS

Persistent Consumer Concerns Regarding Data Privacy and Security

The deep seated apprehension among consumers regarding the security of their personal financial data and the potential for fraud in digital transactions is impeding the growth of Europe mobile payment market. Despite advancements in encryption and tokenization, a substantial portion of the population remains skeptical about storing sensitive banking information on mobile devices that could be lost, stolen, or hacked. According to a survey conducted by the European Union Agency for Cybersecurity, over 45% of citizens in the European Union cited security fears as the primary reason for avoiding mobile payment methods in 2023. High-profile data breaches and sophisticated phishing attacks targeting mobile users have exacerbated these concerns, leading to hesitation in adopting new payment technologies. The complexity of understanding how data is shared between merchants, banks, and technology providers further erodes trust among less tech-savvy demographics. Data from the Ponemon Institute indicates that the perceived risk of identity theft remains a dominant factor influencing payment behavior, particularly among older generations who prefer the tangibility of cash or physical cards. Additionally, the varying levels of cybersecurity awareness across different member states create fragmented adoption rates. The constant evolution of cyber threats requires continuous education and robust demonstration of security features by providers.

Fragmented Legacy Infrastructure and Merchant Acceptance Gaps

The uneven distribution of modern point of sale terminals and the persistence of legacy payment infrastructure limit the universal acceptance of mobile payments. The fragmented legacy infrastructure and merchant acceptance gaps are another attribute degrading the growth of Europe mobile payment market. While major urban centers and Western European nations boast high densities of near field communication-enabled terminals, rural areas and smaller merchants in Eastern and Southern Europe often rely on outdated systems that do not support contactless mobile transactions. As per data from the European Central Bank, nearly 30% of small and medium-sized enterprises in certain European regions still operate without the necessary hardware to accept mobile wallet payments in 2023. This inconsistency creates a fragmented user experience where consumers cannot rely solely on their mobile devices for all purchases, forcing them to carry backup physical cards or cash. The cost associated with upgrading point of sale equipment acts as a deterrent for small business owners, who operate on thin margins and see limited immediate return on investment. Furthermore, the lack of interoperability between different mobile payment schemes and national systems complicates the landscape for cross-border travelers and multinational retailers. The slow pace of infrastructure modernization in specific sectors such as public transportation and vending machines, also restricts usage scenarios.

MARKET OPPORTUNITIES

Integration of Super Apps and Embedded Financial Services

The evolution of mobile applications into comprehensive super apps that integrate payments with a wide array of lifestyle and financial services is likely to create new opportunities for the growth of Europe mobile payment market. This trend allows users to manage banking, shopping, travel, and entertainment within a single ecosystem, thereby increasing the frequency and stickiness of mobile payment usage. According to research by Bain and Company, the number of European consumers using super apps for multiple daily activities is projected to grow by 40% by 2026, driven by the demand for seamless and consolidated digital experiences. Fintech companies and traditional banks are increasingly embedding payment functionalities into non-financial platforms, such as ride-hailing, food delivery, and social media applications. This integration transforms mobile payments from a standalone transaction tool into an invisible enabler of broader digital interactions. For instance, e-commerce platforms can now offer instant buy now, pay later options directly at checkout, powered by mobile wallet infrastructure, increasing conversion rates. The data generated from these diverse interactions provides rich insights into consumer behavior, enabling highly personalized financial products and loyalty rewards. As more industries recognize the value of seamless financial integration, the demand for robust application programming interface solutions will surge. Providers that position themselves as flexible infrastructure partners stand to capture significant market share by powering the financial ecosystems of diverse sectors beyond traditional retail.

Expansion of Peer-to-Peer Payment Solutions and Social Commerce

The rapid growth of peer-to-peer payment solutions, which facilitate instant money transfers between individuals, is increasingly being leveraged for social commerce and informal trade. The expansion of peer-to-peer payment solutions and social commerce is also to amplify the growth of Europe mobile payment market. The ability to split bills, send gifts, or pay freelancers instantly via mobile numbers or usernames addresses a need for frictionless person-to-person transactions that traditional banking systems often fail to meet efficiently. As per a study by Accenture, over 60% of millennials and Generation Z consumers in Europe prefer using mobile apps for peer-to-peer transfers rather than bank transfers or cash in 2023. This preference is driving the development of features that integrate social networking elements with financial capabilities, allowing users to request money and share payment status within social circles. The rise of the gig economy further fuels this trend as independent contractors and freelancers require quick and low-cost methods to receive payments from clients across borders. Mobile payment providers are capitalizing on this by offering multi-currency wallets and real-time foreign exchange services tailored for cross border peer to peer transactions. The viral nature of social commerce, where products are sold directly through social media platforms, creates a natural use case for integrated mobile checkout flows.

MARKET CHALLENGES

Navigating Complex Cross-Border Regulatory Compliance

The intricate difficulty of complying with diverse national regulations and anti-money laundering laws that persist despite efforts toward harmonization is posing as a major challenge for the growth of Europe mobile payment market. According to analysis by Deloitte, mobile payment operators expanding into more than five European countries must navigate over 30 distinct sets of regulatory guidelines, which increases compliance costs by an estimated 25% compared to domestic operations. This fragmentation creates significant barriers to entry for smaller fintech firms that lack the resources to manage multi-jurisdictional legal complexities. It also slows down the rollout of unified products as firms must customize their offerings to meet specific national mandates. The lack of a single passporting license that is universally accepted without additional scrutiny means that expansion strategies require meticulous planning and substantial legal overhead. Furthermore, differing interpretations of regulations by national supervisors can lead to uncertainty and inconsistent enforcement actions. This regulatory patchwork hinders the creation of a truly seamless single market for digital financial services.

Intense Competition and Margin Compression in Transaction Fees

The intensifying competition among traditional banks, fintech startups, and big tech giants, which has led to severe margin compression on transaction fees and revenue streams, is also slowing down the growth of Europe mobile payment market. The reliance on interchange fees as a primary revenue source becomes risky when regulators cap these fees to protect consumers or when competitors undercut prices aggressively. Additionally, the rising cost of capital in the current economic climate makes it harder for loss-making firms to secure funding for continued expansion. Investors are increasingly demanding clear paths to profitability, which pressures companies to cut costs often at the expense of service quality or innovation. The inability to diversify revenue streams beyond basic transactional fees leaves many players vulnerable to economic downturns. Sustainable growth requires a shift towards value-added services, but the prevailing competitive dynamics make it difficult to introduce premium pricing without losing customers to cheaper alternatives. This financial strain threatens the viability of weaker players and could lead to market consolidation that disrupts the current competitive balance.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Technology, Payment Type, Location, End-use, and Country |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Google LLC, Alipay, Amazon.com, Inc. (Amazon Payments), Apple, Inc. (Apple Pay), C-SAM, Inc. (MasterCard Incorporated), Tencent Holdings Ltd. (WeChat), MoneyGram International Inc., PayPal Holdings, Inc., Samsung Group (Samsung Pay), and Visa, Inc. |

SEGMENTAL ANALYSIS

By Technology Insights

The Near Field Communication segment was the largest by holding 58.2% of the Europe Mobile Payment Market share in 2025. The growth of the segment is driven by the seamless integration of this technology into existing point of sale infrastructure and the widespread adoption of contactless cards, which familiarized consumers with tap-to-pay behaviors. According to the European Payments Council, over 85% of all point of sale terminals in the European Union were equipped with contactless capabilities by 2023, allowing users to simply tap their smartphones to complete transactions. The superior security architecture provided by tokenization and dynamic encryption inherent in Near Field Communication protocols, which alleviates consumer fears regarding data theft. The fraud rates for contactless mobile transactions remain significantly lower than those for traditional magnetic stripe or chip and pin card transactions. Furthermore, the speed of transaction processing, which typically takes less than one second, enhances the customer experience during peak hours. The ability of modern smartphones to emulate multiple cards and loyalty programs within a single digital wallet further cements the preference for this technology.

The Mobile Web Payment segment is swiftly emerging at a fastest CAGR of 24.6% throughout the forecast period, owing to the explosive rise of m-commerce and the increasing sophistication of mobile browsers that facilitate secure and frictionless checkout experiences. The shift in consumer behavior towards shopping via smartphones where optimized mobile websites and progressive web apps that reduce cart abandonment rates significantly. According to Eurostat data from 2023, over 45% of all online purchases in the European Union were made using mobile devices, reflecting a decisive move away from desktop computers. The integration of advanced authentication methods, such as biometric verification and one-time passwords directly into mobile web payment gateways, which enhances security without compromising convenience, is also expected to leverage the growth of Europe mobile payment market. Data from the European E-Commerce Association reveals that conversion rates for mobile web payments improved by 30% in 2023, due to the implementation of streamlined checkout flows and saved payment credentials. Additionally, the proliferation of buy now, pay later options embedded within mobile web interfaces allows consumers to manage larger purchases effortlessly. As fifth-generation networks improve loading speeds and reliability, the mobile web will become an even more robust platform for complex financial transactions. The inability of other technologies to support remote e-commerce transactions as effectively ensures that this segment will outpace proximity-based solutions in terms of growth velocity.

By Payment Type Insights

The business-to-consumer segment accounted for a significant share of the Europe Mobile Payment Market in 2025. The growth of the segment is majorly driven by the aggressive promotion of mobile wallets by retailers and brands that offer exclusive discounts, cashback rewards, and loyalty points to incentivize customers to pay via smartphones. Also, the convenience factor for consumers, who prefer the speed and simplicity of tapping their phones over fumbling for cash or cards in high-frequency situations, is additionally elevating the growth of the segment. Statistics from the European Commission indicate that the average frequency of mobile payment usage per consumer increased by 40% in 2023, driven largely by routine household spending. Furthermore, the integration of mobile payments with delivery apps and food ordering platforms has created a seamless ecosystem where transactions occur naturally within the user journey. The massive scale of the consumer base compared to corporate or government entities ensures that this segment remains the dominant revenue generator for mobile payment providers.

The Business to Business segment is anticipated to witness the fastest CAGR of 22.8% from 2026 to 2034, with the urgent need for SMEs and large corporations to digitize their supply chain payments and improve cash flow management through real-time settlement capabilities. The adoption of mobile invoicing and instant payment solutions, which allow businesses to settle invoices on the go, reduces administrative overhead and accelerates the order-to-cash cycle. According to the European Small Business Alliance, many small and medium-sized enterprises in Europe plan to adopt mobile B2B payment tools by 2025 to enhance operational efficiency and reduce reliance on paper checks. The emergence of specialized mobile platforms that cater to specific industry needs, such as logistics field services and wholesale trade, where traditional banking channels are too slow or cumbersome. Additionally, the integration of enterprise resource planning systems with mobile payment gateways enables automated reconciliation and better financial reporting.

By End-Use Insights

The Retail and E-commerce segment accounted in holding 48.3% of the Europe Mobile Payment Market share in 2025, because retail constitutes the largest category of consumer spending and has been the earliest adopter of contactless and mobile checkout technologies. The omnichannel strategy employed by retailers, who seamlessly blend physical store experiences with online shopping, allows customers to use mobile payments for click and collect returns and in-store purchases. The relentless innovation in e-commerce platforms, which utilize mobile payments to reduce friction at checkout, thereby minimizing cart abandonment and boosting sales volumes. The ability of mobile payments to integrate with augmented reality try-on features and personalized marketing campaigns creates a highly engaging shopping environment.

The transportation segment is expected to grow at the fastest CAGR of 26.4% from 2026 to 2033 with the comprehensive modernization of public transit systems, which are replacing legacy ticketing machines with open-loop mobile payment validators. The initiative by city authorities to create seamless multimodal travel experiences, where commuters can tap their phones to access buses, trains, and bike sharing schemes without needing separate tickets or cards. According to the International Association of Public Transport, over 40 major European cities, including London, Paris, and Berlin, fully implemented mobile payment acceptance across their entire networks in 2023. The rising demand for contactless solutions in the post pandemic era has accelerated the removal of cash handling in taxi ride-hailing services and toll booths. Data from the European Railway Agency reveals that mobile ticketing usage increased by 50% in 2023 as travelers sought safer and more efficient ways to commute. Furthermore, the integration of mobility as a service platforms allows users to plan and pay for complex journeys involving multiple modes of transport through a single mobile interface. As urbanization intensifies and smart city initiatives expand, the transportation sector will become a cornerstone of mobile payment adoption.

COUNTRY-LEVEL ANALYSIS

United Kingdom Mobile Payment Market Analysis

The United Kingdom mobile payment market was the top performer by occupying 22.3% of the market share in 2025, with its early in contactless infrastructure and fintech innovation. The cultural shift, where cash usage has plummeted, and mobile wallets have become the preferred method for daily transactions among all demographics. According to UK Finance data from 2023, contactless payments, including mobile transactions, accounted for over 50% of all face-to-face card payments in the country, reflecting deep consumer trust and habit formation. The presence of global fintech giants and neobanks in London has fostered a competitive environment that continuously pushes the boundaries of payment technology and user experience. The government's supportive regulatory stance and the widespread availability ofnear-fieldd communication terminals in even the smallest retailers contribute to this dominance. Furthermore, the integration of mobile payments into the transport network of London and other major cities has normalized the behavior for millions of daily commuters. The high smartphone penetration rate and advanced telecommunications network ensure reliable connectivity for seamless transactions.

Germany Mobile Payment Market Analysis

Germany's mobile payment market growth is likely to be driven by the remarkable transformation from a historically cash-dominant society to a rapidly digitizing economy. The shifts in consumer behavior accelerated by the pandemic, which forced everyone to embrace digital payment methods is greatly influencing the growth of Europe mobile payment market. The robust manufacturing and automotive sectors are increasingly integrating mobile B2B payment solutions to streamline supply chain finance and vendor settlements. The regulatory framework under BaFin ensures high security standards, which builds trust in digital channels despite initial awareness regarding data privacy. Major institutions and retailers are investing billions in modernizing point-of-sale systems to accept mobile wallets, catering to both domestic and international tourists.

France Mobile Payment Market Analysis

France mobile payment market growth is expected to have a steady pace throughout the forecast period, with the strong involvement of traditional banks in driving mobile payment adoption. The proactive strategies of major banking groups have integrated mobile wallet functionalities directly into their proprietary banking applications. According to data from the French Banking Federation, over 30 million active users utilized bank-led mobile payment solutions in 2023, reflecting a high level of customer loyalty and trust in established financial institutions. The government's commitment to becoming a cash-lite society has led to legislative measures encouraging merchants to accept electronic payments and limiting cash transaction thresholds. The vibrant startup ecosystem in Paris contributes to the development of innovative peer-to-peer and social payment features that appeal to younger consumers. The widespread deployment of contactless terminals in bakeries, supermarkets, and public transport networks facilitates easy adoption. Furthermore, the focus on securing transactions through strong customer authentication aligns with European regulations while maintaining user convenience.

Netherlands Mobile Payment Market Analysis

The Netherlands mobile payment market growth is likely to grow with its exceptionally high adoption rates of digital wallets and near total elimination of cash in many sectors. As per statistics from De Nederlandsche Bank, over 90% of the population uses mobile banking and payment apps regularly, making it one of the highest penetration rates globally. Dutch consumers are early adopters of new technologies such as wearables for payments and biometric authenticatio,n which enhance security and convenience. The government actively supports digital innovation through policies that encourage electronic transactions and reduce reliance on physical currency. The high level of English proficiency and digital literacy among the populace facilitates the rapid rollout of international fintech solutions.

Sweden Mobile Payment Market Analysis

Sweden Mobile Payment Market growth is propelled by the fact that it is the most cashless society in the world, where mobile payments are the norm for everything from street vendors to church donations. According to Statistics Sweden, the usage of cash in retail transactions fell below 10% in 2023 as merchants and consumers alike adapted fully to digital norms. Swedish banks are aggressively launching mobile-first products to capture the attention of users, who rarely visit physical branches. The tech-savvy population and strong government support for digitalization create an ideal testing ground for new payment innovations. Government programs aimed at promoting digital literacy have further accelerated adoption rates among all age groups.

COMPETITIVE LANDSCAPE

The competition within the Europe Mobile Payment Market is characterized by an intense rivalry between global technology giants, established financial institutions, and agile fintech startups vying for dominance in a rapidly evolving sector. Incumbent banks leverage their existing customer relationships and regulatory licenses to launch proprietary mobile wallets while tech companies compete on superior user experience and seamless integration with hardware ecosystems. The market landscape is fragmented yet consolidating as major entities acquire innovative startups to enhance their solution offerings and accelerate time to market. Differentiation increasingly relies on the ability to provide value-added services such as integrated loyalty programs, expense management tools, and real-time financial insights beyond simple transaction processing. Price competition exists but is often secondary to the value proposition of security features and widespread merchant acceptance, which are critical for consumer adoption. Regulatory compliance acts as a formidable barrier to entry, ensuring that only firms with robust governance systems can operate across multiple European jurisdictions. The push for open banking has further intensified competition by allowing third-party providers to access bank data and create aggregated financial services. Strategic collaborations with merchants and transport operators have become common as firms seek to embed payments into everyday activities.

KEY MARKET PLAYERS

The leading companies operating in the Europe mobile payment market include:

- Google LLC

- Alipay

- com, Inc.

- Apple, Inc.

- C-SAM, Inc.

- Tencent Holdings Ltd.

- MoneyGram International Inc.

- PayPal Holdings, Inc.

- Samsung Group

- Visa, Inc.

TOP PLAYERS IN THE MARKET

- Apple Inc operates as a dominant force in the Europe Mobile Payment Market through its Apple Pay service, which leverages near-field communication technology across its vast ecosystem of devices. The company contributes globally by setting high standards for security and user privacy through tokenization and biometric authentication methods. Recently, Apple has strengthened its market position by expanding tap-to-pay functionality to allow merchants to accept payments directly on iPhones without additional hardware. The firm actively collaborates with European banks and transit authorities to integrate Apple Pay into public transportation systems across major cities. By continuously enhancing its wallet application to include digital identities and keys, Apple reinforces its role as a central hub for daily digital interactions. These strategic moves solidify its reputation as a leader capable of driving mass adoption of contactless payments while maintaining rigorous security protocols for users worldwide.

- Google LLC stands as a premier provider of mobile payment solutions via Google Wallet and Google Pay, serving millions of users with seamless transaction capabilities. The company contributes globally by integrating payment services deeply into its Android operating system and broader suite of productivity tools. Recent actions include partnering with major European retailers to enable smart checkout experiences that utilize saved loyalty cards and ticketing within the wallet application. Google actively invests in enhancing security features, such as virtual account numbers, to protect user data during online and in-store transactions. The firm also focuses on expanding support for peer-to-peer payments and cross-border transfers to facilitate easier money movement for European consumers. These initiatives demonstrate how the company strengthens its market position by becoming an indispensable part of the daily financial lives of individuals and businesses throughout the continent.

- PayPal Holdings Inc is a pioneering digital payment platform that maintains a significant foothold in the Europe Mobile Payment Market through its versatile app and robust merchant network. The company delivers a wide array of services, including peer-to-peer transfers, online checkout solutions, and buy now, pay later options tailored for European consumers. Globally, PayPal contributes by enabling secure cross-border commerce and supporting small businesses with an accessible digital payment infrastructure. Recent strategic initiatives involve the acquisition of specialized fintech firms to enhance cryptocurrency trading capabilities and streamline point-of-sale interactions for physical retailers. The firm has also strengthened its position by launching advanced fraud detection systems powered by artificial intelligence to ensure transaction safety. PayPal focuses heavily on expanding its QR code payment acceptance to cater to smaller merchants who lack traditional terminal infrastructure. These efforts demonstrate its commitment to providing flexible and secure payment solutions that meet the evolving needs of the European digital economy.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe Mobile Payment Market primarily employ strategic partnerships with traditional banks and retailers to expand their acceptance networks and integrate services into existing customer workflows. Companies frequently invest heavily in research and development to innovate security protocols such as biometric authentication and tokenization that build consumer trust and reduce fraud risks. Manufacturers are increasingly focusing on super app ecosystems that consolidate payments with loyalty programs, ticketing, and identity management to increase user retention. Localization of services serves as a critical approach where firms adapt their platforms to comply with specific national regulations and support local payment schemes. Furthermore, participants prioritize incentivizing adoption through cashback rewards and zero fee structures to attract price-sensitive consumers and merchants. These collective strategies aim to build scale, foster innovation, and secure a competitive advantage in a market driven by convenience and stringent regulatory compliance.

MARKET SEGMENTATION

This research report on the Europe mobile payment market has been segmented and sub-segmented into the following categories.

By Technology

- Near Field Communication

- Direct Mobile Billing

- Mobile Web Payment

- SMS

By Payment Type

- B2B

- B2C

- B2G

- Others

By Location

- Remote Payment

- Proximity Payment

By End-use

- BFSI

- Healthcare

- IT & Telecom

- Media & Entertainment

- Retail & E-commerce

- Transportation

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe