Europe Oil and Gas Pipeline Market Size, Share, Trends & Growth Forecast Report By Activity, By Function, By Location of Deployment, and By Country (Germany, Italy, France, United Kingdom, Netherlands & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Oil and Gas Pipeline Market Report Summary

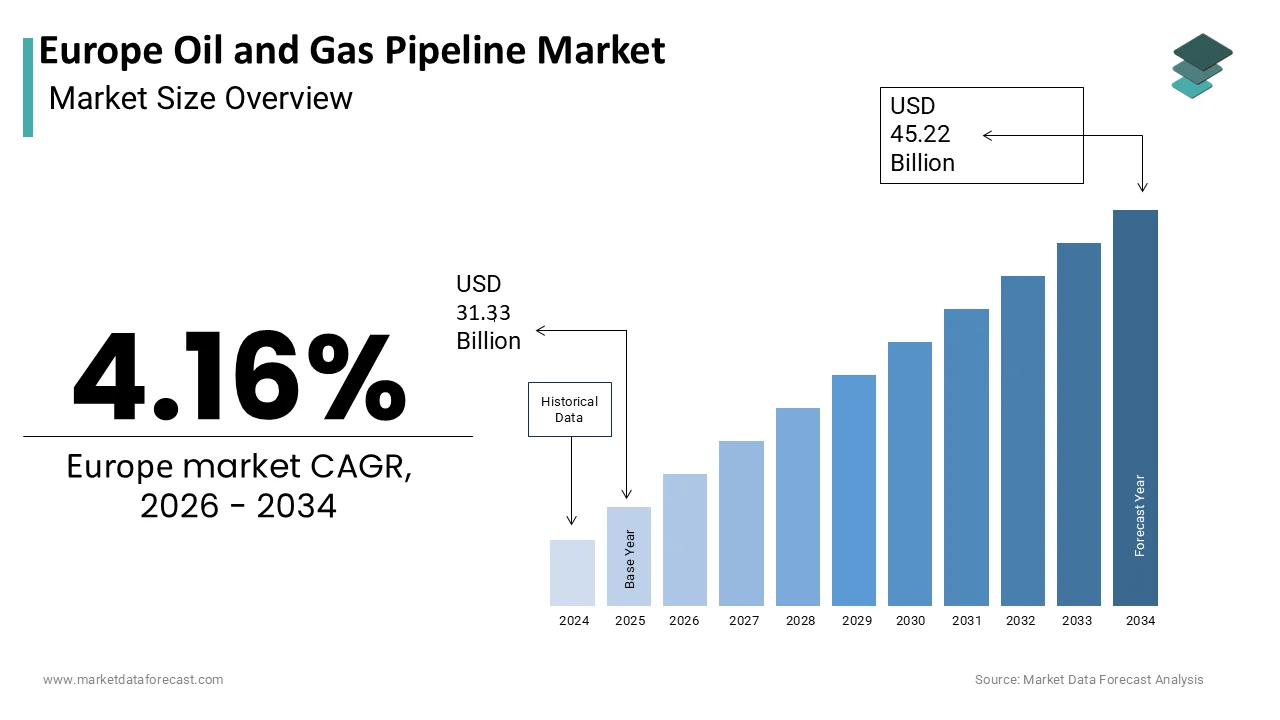

The Europe Oil and Gas Pipeline Market was valued at USD 31.33 billion in 2025 and is projected to reach USD 45.22 billion by 2034, growing from USD 32.63 billion in 2026 at a CAGR of 4.16% during the forecast period. Growth is driven by strategic diversification of supply routes for energy security, critical infrastructure modernization and integrity management requirements, and repurposing of existing assets for hydrogen and low-carbon gases. Stringent environmental permitting delays and volatile long-term demand forecasts are shaping market dynamics.

Key Market Trends

- Rising repurposing of natural gas pipelines for hydrogen transport under the European Hydrogen Backbone initiative

- Growing digitalization through smart pigging, fiber optic sensing, and AI-driven predictive maintenance

- Increasing offshore pipeline development to support new LNG terminals and floating regasification units

- Expansion of biomethane injection points into local distribution networks

- Rising EU Methane Regulation compliance driving leak detection and repair investment

Segmental Insights

- Based on activity, OPEX dominated the market in 2025, driven by mandatory integrity management and leak detection requirements for aging infrastructure.

- Based on function, transmission lines held the majority share in 2025, driven by their critical role connecting import terminals and cross-border supply routes.

- Based on location, onshore held the commanding share in 2025, accounting for over 80% of total pipeline length, driven by lower construction complexity versus offshore.

Regional Insights

- Germany led the market in 2025, supported by its Hydrogen Core Network plan and LNG terminal expansion following the Russian gas phase-out.

- Italy holds a significant share, driven by its role as a southern gateway via the Trans Adriatic Pipeline and Greenstream pipeline.

- France is a prominent market supported by biomethane grid integration and dedicated hydrogen network development for industrial hubs.

- Netherlands contributes notably due to its extensive port infrastructure and Rotterdam hydrogen backbone development.

- Offshore is the fastest-growing location segment, projected at a CAGR of 7.2%, driven by new LNG terminal connections and North Sea hydrogen pilot projects.

Competitive Landscape

The market is highly competitive, with state-owned transmission operators and private developers competing on regulatory compliance, hydrogen repurposing capability, and cross-border interconnectivity execution. Companies are investing in digitalization and asset repurposing to align with EU decarbonization mandates.

Prominent players in the market include Enagás, Snam, and Gasunie.

Europe Oil and Gas Pipeline Market Size

The Europe Oil and Gas Pipeline Market is projected to grow from USD 31.33 billion in 2025 to USD 32.63 billion in 2026 and reach USD 45.22 billion by 2034, registering a CAGR of 4.16% during the forecast period from 2026 to 2034.

An oil and gas pipeline is a continuous, underground or above-ground network of steel or plastic pipes used to transport crude oil, natural gas, and refined petroleum products over long distances. This market encompasses thousands of kilometers of onshore and offshore pipelines that connect production zones, import terminals, refineries, and consumption centers across diverse geopolitical landscapes. The strategic importance of this infrastructure has been magnified by recent shifts in supply dynamics following the reduction of Russian gas flows. According to Eurostat and official Council of the European Union energy metrics, the 138 billion cubic meters figure actually represents the volume of gas demand saved/reduced across the EU between August 2022 and May 2024, whereas actual net pipeline imports of natural gas into the EU sat near 155 billion cubic meters for the full year of 2023. As per Gas Infrastructure Europe (GIE) and ENTSOG, more than 42% of Europe's main transmission trunklines were laid down before 1980, establishing a multi-billion euro market focus on digital pipeline twins, leak monitoring software, and asset life extension. According to the European Network of Transmission System Operators for Gas, the total length of high-pressure gas transmission pipelines in Europe exceeds 200000 kilometers, forming one of the most complex integrated energy systems globally. Current developments focus heavily on diversifying supply routes through projects like the Southern Gas Corridor and enhancing interconnectivity between member states to prevent supply bottlenecks. Furthermore, regulatory frameworks are increasingly mandating integrity assessments and methane leak detection, driving technical upgrades across the asset base. This infrastructure serves not only current fossil fuel needs but is also being evaluated for future compatibility with low-carbon gases, positioning it at a critical juncture of transition and resilience.

MARKET DRIVERS

Strategic Diversification Of Supply Routes To Enhance Energy Security

The urgent imperative to reduce dependency on single-source suppliers is a key driver for new pipeline development and capacity expansion across the region, which fuels the growth of the Europe oil and gas pipeline market. Following the geopolitical disruptions of 2022, European nations have accelerated infrastructure projects designed to unlock alternative gas supplies from the Caspian region, North Africa, and the Eastern Mediterranean. According to the International Energy Agency (IEA), non-Russian pipeline gas deliveries to the EU actually remained flat or declined slightly (by roughly 1-2 bcm) in 2023 due to unplanned Norwegian upstream infrastructure outages, meaning the EU's massive displacement of Russian supply was structurally solved by expanding maritime LNG intake rather than spiking non-Russian pipeline volumes. Projects such as the Trans Adriatic Pipeline and the planned EastMed pipeline exemplify this strategic pivot, creating physical pathways for diversified molecules to reach Central and Western European markets. National governments are providing state guarantees and streamlined permitting to fast-track these critical infrastructure assets, recognizing them as matters of national security rather than purely commercial ventures. The European Commission’s REPowerEU plan specifically allocates funding to eliminate remaining bottlenecks in the internal gas grid, ensuring that diversified supplies can actually reach demand centers. This driver is fundamentally different from historical market forces because it prioritizes redundancy and resilience over pure cost optimization. Consequently, pipeline operators are investing in compressor station upgrades and loop lines to maximize throughput on existing corridors while new greenfield projects navigate complex regulatory approvals. This structural realignment ensures long-term demand for pipeline construction and engineering services regardless of short-term price volatility.

Critical Infrastructure Modernization And Integrity Management Requirements

The aging nature of the region’s vast pipeline network necessitates continuous capital expenditure on maintenance, rehabilitation, and technological upgrades to ensure safe and compliant operations, a trend that further propels the expansion of the Europe oil and gas pipeline market Europe Oil & Gas Pipeline Market. A significant percentage of the continent's transmission assets were installed during the mid 20th century and are now approaching or exceeding their original design life, triggering mandatory integrity management programs. According to the long-term statistical safety records analyzed by the European Gas Pipeline Incident Data Group (EGIG), external interference (such as third-party excavation, digging, and ground works) remains the number one leading cause of gas pipeline incidents at 35% of all recorded events, whereas corrosion ranks as the third leading cause at roughly 15%. Operators are deploying advanced inline inspection tools and digital twin technologies to monitor asset health in real time, replacing reactive maintenance with predictive strategies. The EU Methane Regulation adopted in 2024 imposes stringent leak detection and repair obligations, requiring operators to survey all pipeline sections regularly and fix leaks within specific timeframes. Compliance with these evolving environmental and safety standards drives sustained investment in monitoring equipment, coating replacement, and cathodic protection systems. Unlike new construction driven by market demand, this expenditure is non-discretionary and regulated, providing a stable baseline of activity for service providers and equipment manufacturers. Furthermore, upgrading legacy control systems to modern SCADA platforms enhances operational flexibility and cybersecurity, addressing both physical and digital vulnerabilities. This modernization wave ensures the existing network remains viable and safe amidst heightened scrutiny and operational demands.

MARKET RESTRAINTS

Stringent Environmental Regulations and Permitting Delays Hinder Development

The accelerating pace of climate policy and environmental opposition creates significant friction for new oil and gas pipeline projects across the region, which hampers the growth of the European market. National and supranational decarbonization targets often conflict with the multi-decade lifespan of new fossil fuel infrastructure, leading to prolonged legal battles and permit denials. According to the European Round Table for Industry (ERT), it is the complex, unharmonizedtrans-European permitting processes and localized court disputes that regularly extend grid infrastructure execution timelines past a decade. Courts in countries like Germany and the Netherlands have increasingly ruled against fossil fuel projects based on climate commitments, creating legal uncertainty for investors. The EU Taxonomy excludes unabated fossil gas infrastructure from sustainable finance classifications, restricting access to green capital and raising the cost of debt for traditional pipeline developers. Local communities and NGOs frequently utilize administrative procedures to challenge routing decisions, adding years to project timelines and inflating costs through inflation and remobilization expenses. This restraint is particularly acute for cross-border projects that must satisfy multiple jurisdictions with varying environmental priorities. Even when permits are granted, conditional requirements for biodiversity offsets or noise mitigation can alter engineering designs and increase capital intensity. Consequently, many proposed expansions remain in planning limbo, unable to secure final investment decisions despite identified market needs. This regulatory headwind fundamentally alters the risk profile of greenfield pipeline development in the region.

Volatile Demand Forecasts Amidst Accelerated Energy Transition

Uncertainty regarding future hydrocarbon consumption volumes is a fundamental restraint on long-term infrastructure investment decisions, which impedes the expansion of the Europe oil and gas pipeline market. Pipeline assets typically require 30- to 50-year amortization periods, yet European gas demand projections vary wildly depending on renewable deployment speeds and electrification rates. According to BloombergNEF, natural gas demand in Europe could decline by up to 40 percent by 2035 under aggressive net zero scenarios, potentially stranding newly built capacity. Investors face the dilemma of either underbuilding and risking supply shortages or overbuilding and facing unrecoverable capital losses. This forecasting difficulty is compounded by the intermittent nature of renewables, which creates unpredictable peak demand patterns that are hard to size infrastructure for accurately. Financial institutions are increasingly reluctant to fund long-term gas projects without sovereign guarantees or take-or-pay contracts backed by creditworthy offtakers. The lack of consensus on the role of gas as a transition fuel further complicates planning horizons. Some member states advocate for maintaining gas capacity as backup for renewable intermittency, while others push for immediate phase-out. This policy divergence creates fragmented signals for pan-European infrastructure planners. Until clearer demand trajectories emerge or hybrid business models evolve, capital allocation for new pipelines will remain cautious and selective, limiting market growth potential despite current supply security concerns.

MARKET OPPORTUNITIES

Repurposing Existing Assets for Hydrogen and Low Carbon Gases

The adaptation of the existing natural gas grid for hydrogen transport offers a transformative opportunity to extend asset life and support decarbonization goals, which is likely to boost the growth of the Europe oil and gas pipeline market. Technical studies indicate that a significant portion of Europe’s steel transmission pipelines can be converted to carry pure hydrogen or blends with relatively modest modifications compared to building new dedicated networks. According to the European Hydrogen Backbone (EHB) initiative, repurposing existing natural gas networks is highly cost-effective because building a repurposed pipeline is estimated to cost just 10% to 20% of the capital expenditure required for an entirely new hydrogen pipeline build, drastically improving early-stage project economics. The European Commission’s Hydrogen and Decarbonised Gas Market Package establishes a regulatory framework for hydrogen networks, including third-party access and tariff regulation, providing the legal certainty needed for investment. Operators are actively conducting hydrogen readiness assessments and material compatibility tests to identify conversion candidates. This opportunity allows pipeline companies to pivot their business models toward low-carbon services while leveraging sunk capital. Countries like Germany and the Netherlands have already designated specific corridors for hydrogen transport, integrating them into national hydrogen strategies. The creation of a pan-European hydrogen backbone could connect production hubs in Southern and Northern Europe with industrial demand centers in the interior. This transition not only preserves infrastructure value but also positions pipeline operators as key enablers of the energy transition, opening new revenue streams and aligning with climate objectives.

Digitalization And Smart Grid Integration For Operational Efficiency

The integration of advanced digital technologies into pipeline operations paves the way to enhance capacity, safety, and flexibility without major civil works, which is expected to accelerate the expansion of the Europe oil and gas pipeline market. Smart pigging, fiber optic sensing, and AI-driven analytics enable operators to optimize flow rates, predict failures, and manage multi-product batching more efficiently. According to sources, implementing integrated predictive maintenance systems across complex pipeline networks can reduce unplanned equipment downtime by up to 20%, while overall AI system integration generally improves production efficiency by 5% to 8%. As European grids become more interconnected and bidirectional to accommodate diverse supply sources, sophisticated control systems are essential for managing complex flow patterns and balancing pressures. The EU’s Digitalisation of Energy Action Plan encourages investment in smart infrastructure to support system integration and resilience. Operators can monetize enhanced flexibility by offering balancing services and capacity trading products in liberalized markets. Cybersecurity upgrades also present an opportunity to harden critical infrastructure against evolving threats while meeting regulatory compliance. Digital twins allow for virtual scenario testing and operator training, reducing operational risks during transitions or emergencies. This technological layer transforms static pipes into dynamic, intelligent assets capable of responding to real-time market signals and system needs. Service providers specializing in IoT sensors, data analytics, and automation software stand to benefit from this modernization wave, creating a secondary market ecosystem around physical infrastructure.

MARKET CHALLENGES

Geopolitical Instability and Cross-Border Coordination Complexities

Managing pipeline projects across multiple jurisdictions with divergent political interests remains a persistent challenge for regional infrastructure development, which slows down the growth of the Europe oil and gas pipeline market. Energy infrastructure is inherently geopolitical, and shifting alliances or conflicts can disrupt established supply routes and cooperation frameworks overnight. As per the European Round Table for Industry (ERT), it is the unharmonized trans-European permitting regulations and lengthy local court appeals that regularly delay major cross-border grid infrastructure projects, often extending total deployment timelines past a full decade. Disputes over transit fees, environmental standards, or strategic alignment can stall projects indefinitely even after technical feasibility is confirmed. The war in Ukraine demonstrated how quickly geopolitical shocks can render existing infrastructure unusable or politically toxic, forcing rapid and costly rerouting. Coordinating permitting, funding, and construction schedules across borders requires unprecedented diplomatic effort and institutional alignment. Different national energy strategies may prioritize competing projects, leading to duplication or gaps in coverage. Sovereign guarantees and EU Project of Common Interest status help mitigate some risks but cannot eliminate political volatility entirely. Investors must price in significant geopolitical risk premiums, increasing capital costs. This complexity discourages private sector participation and places a greater burden on public entities to de-risk projects. Cross-border pipeline development will remain fraught with coordination challenges. These issues transcend pure engineering or commercial considerations until deeper regional integration mechanisms evolve.

Skilled Workforce Shortages and Technical Capability Gaps

The specialized labor required for pipeline construction, inspection, and maintenance is becoming increasingly scarce as experienced professionals retire and fewer entrants join the sector, which holds back the expansion of the Europe oil and gas pipeline market. According to the International Energy Agency (IEA), the rapid shift toward green infrastructure has caused severe specialized engineering talent shortages in Europe, forcing pipeline operators to aggressively reskill traditional oil and gas technicians into certified hydrogen-ready pipeline mechanics. This demographic cliff coincides with rising demand for specialized skills related to hydrogen compatibility, digital systems, and methane mitigation. Training new personnel takes years due to the hands-on nature of pipeline work and stringent certification requirements. Competition from the renewable energy sector and tech industries further drains the talent pool, driving up labor costs and causing project delays. Knowledge transfer from retiring experts is often incomplete, risking loss of institutional memory about legacy assets. Educational institutions have reduced petroleum engineering enrollments in response to energy transition narratives, exacerbating the supply gap. Contractors struggle to staff multiple simultaneous projects, leading to bidding wars and schedule slippage. This human capital constraint limits the industry’s ability to execute modernization and expansion plans at the required pace. Addressing this challenge requires coordinated efforts in vocational training, immigration policy, and industry branding to attract next-generation talent. Projects often lack adequately skilled labor. Consequently, even well-funded and permitted initiatives face execution risks that threaten their timelines and quality standards.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Activity, Function, Location of Deployment, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | Germany, Italy, France, the United Kingdom, the Netherlands |

| Market Leaders Profiled | Saipem S.p.A., Tenaris S.A., Vallourec S.A., Europipe GmbH, Mannesmann Line Pipe GmbH, TMK Group, ChelPipe Group, National Oilwell Varco, Inc. (NOV), Technip Energies N.V., Allseas Group S.A., John Wood Group plc, Subsea7 S.A. |

SEGMENTAL ANALYSIS

By Activity Insights

The Operational Expenditure (OPEX) segment dominated the Europe oil and gas pipeline market and accounted for a substantial share in 2025. This dominance of the segment was driven by stringent regulatory mandates requiring continuous monitoring, maintenance, and integrity management of aging infrastructure. The European Union’s Methane Regulation and national safety laws compel operators to conduct regular inspections, leak detection surveys, and preventive repairs to avoid severe penalties and environmental damage. As per Gas Infrastructure Europe (GIE) and ENTSOG, more than 42% of Europe's transmission trunklines were constructed before 1980, driving higher baseline operating costs for protective coatings and stress testing, whereas the European Gas Pipeline Incident Data Group (EGIG) tracks incident frequencies rather than individual asset age registries. Operators cannot defer these costs as they are directly linked to license retention and public safety obligations. The shift from reactive to predictive maintenance models requires sustained investment in skilled labor, diagnostic tools, and data analysis platforms. This recurring expenditure forms the bulk of annual budgets for transmission system operators who prioritize asset reliability over new construction. Furthermore, the complexity of cross-border networks demands coordinated operational protocols and real-time monitoring systems that incur high ongoing costs. The non-discretionary nature of these expenses ensures that OPEX remains the dominant activity segment regardless of fluctuating capital investment cycles. Regulatory bodies continuously tighten standards for emission reporting and accident prevention, forcing operators to allocate more resources toward compliance activities. This structural requirement creates a stable and growing demand for operational services, technical consulting, and maintenance contracts across the continent.

The dominance of the OPEX segment is further reinforced by the escalating costs associated with maintaining legacy infrastructure that was built during previous decades of rapid expansion. As pipelines approach the end of their design life, the frequency and intensity of maintenance activities increase significantly to prevent failures and extend serviceability. According to sources, maintenance costs for aging pipelines can be up to 30 percent higher than for newer assets due to the need for specialized repair techniques and frequent interventions. Operators face rising expenses for replacing valves, compressors, and control systems that are no longer supported by original manufacturers. The integration of digital monitoring technologies also adds to operational costs as companies invest in software licenses, cybersecurity measures, and staff training. Unlike CAPEX, which is project-based and intermittent, OPEX represents a continuous financial commitment required to keep the network functional and compliant. The volatility of energy prices does not significantly reduce these costs, as safety and reliability are paramount. Additionally, the increasing complexity of managing bidirectional flows and mixed gas qualities in a diversified supply environment requires advanced operational capabilities that drive up staffing and technology costs. This persistent need for high-level operational support ensures that OPEX remains the largest component of total pipeline expenditure. The focus on extending asset life rather than building new lines further shifts the balance toward operational spending.

The Capital Expenditure (CAPEX) segment is growing at the fastest CAGR of 6.8% due to urgent government-backed initiatives to diversify gas supply routes and reduce dependency on single sources. Following the geopolitical shifts of recent years, European nations have launched multiple large-scale pipeline projects to connect with alternative suppliers in the Caspian region, North Africa, and via LNG terminals. According to the European Commission, billions of euros have been allocated under the REPowerEU plan specifically for infrastructure upgrades and new interconnectors to enhance energy security. These greenfield and brownfield projects require substantial upfront capital for engineering, procurement, and construction activities. The urgency of these strategic priorities overrides typical commercial hesitation, leading to accelerated approval processes and state-guaranteed financing. Major projects such as the expansion of the Southern Gas Corridor and new bilateral interconnectors between member states are driving a surge in construction activity. This wave of investment is distinct from historical cycles as it is motivated by national security rather than pure market demand. The scale of these projects involves complex engineering challenges, including crossing difficult terrains and marine environments, which increasecapital intensity. Furthermore, the need to build reverse flow capabilities and upgrade compressor stations to handle diverse gas qualities adds to the capital burden. This strategic push ensures sustained high levels of CAPEX in the near-term and medium-term as countries race to secure resilient supply networks.

The rapid growth of the CAPEX segment is also fueled by significant investments in repurposing existing natural gas pipelines for hydrogen transport and building new dedicated hydrogen corridors. The European Hydrogen Backbone initiative aims to create a pan-continental network capable of transporting low-carbon gases, requiring extensive modifications to existing assets and construction of new links. According to the European Hydrogen Backbone (EHB) initiative, developing the pan-European hydrogen transmission network, spanning 31.500 kilometers of repurposed and new pipelines, is projected to require a total capital outlay of €28 billion to €43 billion by 2030. These projects involve expensive material upgrades, compressor replacements, and safety system installations to handle the different physical properties of hydrogen. Governments are providing subsidies and regulatory frameworks to de-risk these investments, encouraging transmission system operators to commit capital early. The transition from natural gas to hydrogen represents a fundamental shift in infrastructure utility, necessitating comprehensive retrofitting programs. Pilot projects in countries like Germany and the Netherlands are already underway, demonstrating the technical feasibility and triggering further investment. The need to connect industrial clusters with renewable hydrogen production sites drives the development of new regional networks. This emerging application opens a new avenue for capital expenditure that complements traditional oil and gas projects. The long-term nature of these investments aligns with climate goals, attracting both public and private funding. This strategic pivot ensures that CAPEX grows rapidly as the continent builds the foundation for a decarbonized energy system.

By Function Insights

In 2025, the transmission lines segment held the majority share of the Europe oil and gas pipeline market because of its critical role in transporting large volumes of hydrocarbons over long distances and across national borders. These high-pressure pipelines form the backbone of the European energy grid, connecting import terminals, production fields, and storage facilities with distribution networks. According to the European Network of Transmission System Operators for Gas, the transmission network accounts for the majority of pipeline mileage and capacity, facilitating the internal market and ensuring supply stability across member states. The strategic importance of transmission lines has increased as Europe seeks to integrate diverse supply sources and balance regional disparities in demand and availability. Investments in transmission infrastructure are prioritized to eliminate bottlenecks and enhance interconnectivity, allowing gas to flow freely from entry points to consumption centers. The scale of these projects involves significant engineering complexity and capital outlay, reinforcing their dominance in the market. Transmission operators are regulated entities with mandated investment plans approved by national authorities, ensuring consistent spending on capacity expansion and reinforcement. The ability to transport gas efficiently over thousands of kilometers makes transmission lines indispensable for continental energy security. This function supports the liberalized gas market by enabling third-party access and competition. The continued focus on securing alternative supply routes ensures that transmission lines remain the primary focus of infrastructure development and maintenance efforts.

The leading position of this segment is also bolstered by regulatory mandates from the European Union aimed at creating a fully integrated and competitive internal energy market. According to European Commission infrastructure directives, the Ten-Year Network Development Plan (TYNDP) selects vital cross-border transmission corridors to receive Project of Common Interest (PCI) status, fast-tracking their permitting loops and unlocking access to systemic regional development funding. Transmission system operators must comply with strict capacity allocation and transparency rules, which necessitate continuous upgrades to metering, control, and communication systems. The push for market integration encourages the development of redundant pathways to prevent the isolation of any single region during supply disruptions. This regulatory framework creates a predictable pipeline of projects for transmission infrastructure providers. The high technical standards required for cross-border operations ensure that only experienced players can participate, maintaining the segment's value and complexity. Furthermore, the transition to a decarbonized gas system relies heavily on the transmission network to transport hydrogen and biomethane from production hubs to industrial users. This evolving role ensures that transmission lines remain central to future energy strategies. The combination of security, market, and climate objectives sustains the leading position of transmission lines in the market.

The distribution lines segment is estimated to register the fastest CAGR of 5.9% from 2026 to 2034 owing to urban expansion and the need for last-mile connectivity to residential and commercial consumers. As European cities grow and densify, the demand for reliable local gas networks increases to support heating, cooking, and industrial processes. According to Eurostat, the urban population in the EU continues to rise, with over 75 percent of Europeans living in cities, creating sustained demand for localized distribution infrastructure. Distribution system operators are investing in extending networks to new housing developments and upgrading old pipes in historic centers to improve safety and efficiency. The replacement of cast iron and steel pipes with modern polyethylene materials reduces leak rates and maintenance needs, driving replacement cycles. This segment benefits from steady, decentralized investment patterns that are less susceptible to large-scale geopolitical shocks than transmission projects. The focus on local resilience and service quality ensures consistent funding for distribution upgrades. Furthermore, the integration of smart meters and digital monitoring systems in distribution networks requires additional infrastructure investment to support data collection and remote management. This modernization effort enhances operational efficiency and customer service, justifying continued capital expenditure. The distributed nature of these projects allows for quicker execution and lower regulatory hurdles compared to major transmission lines. This agility supports faster growth rates as operators respond to local demand dynamics and municipal planning requirements.

The rapid growth of the distribution segment is also fueled by the integration of renewable gases such as biomethane and hydrogen into local grids. Many European municipalities are promoting the use of locally produced biomethane from waste treatment plants and agricultural sources, requiring connection infrastructure to inject these gases into the distribution network. According to the European Biogas Association, biomethane production in Europe has grown significantly, with hundreds of injection points connected to distribution grids in recent years. Distribution system operators are adapting their networks to handle varying gas qualities and pressures associated with renewable injections. This involves installing blending stations, quality monitoring equipment, and upgraded safety valves. The decentralization of energy production favors distribution networks as the primary interface for local renewable resources. Pilot projects for hydrogen blending in residential areas are also driving investment in distribution infrastructure modifications. These initiatives align with local climate action plans and provide opportunities for community energy projects. The flexibility of distribution networks makes them ideal testbeds for new gas technologies before wider transmission rollout. This innovation driver adds a layer of growth beyond traditional fossil fuel distribution. The support from local governments and EU funds for green gas initiatives further accelerates investment in this segment. The transition to a decentralized, renewable gas system positions distribution lines as a key growth area.

By Location Of Deployment Insights

The onshore segment was the largest in the Europe oil and gas pipeline market and occupied a commanding share in 2025. This supremacy of the segment was supported by the vast existing network of land-based pipelines and the lower technical complexity and cost of onshore construction compared to offshore projects. The majority of European transmission and distribution lines are located on land, connecting inland production sites, storage facilities, and consumption centers. According to studies, onshore pipelines account for over 80 percent of the total pipeline length in Europe, reflecting the historical development of the continental gas grid. Onshore construction benefits from easier access for heavy machinery, simpler logistics, and lower environmental risks compared to marine environments. Permitting processes, while still rigorous, are generally more straightforward than those for offshore projects, which involve maritime jurisdictions and complex ecological assessments. The maturity of onshore pipeline technology ensures reliable performance and established maintenance practices. Most new interconnectors and internal reinforcement projects are land-based, linking neighboring countries through terrestrial routes. The lower capital intensity per kilometer allows for more extensive network coverage within budget constraints. Furthermore, onshore pipelines are easier to monitor and repair, reducing operational risks and downtime. This practical advantage sustains the dominance of the onshore segment. The focus on enhancing internal European connectivity rather than new long-distance offshore imports further supports onshore deployment. The established supply chain for onshore construction materials and services ensures efficient project execution.

The prominence of the onshore segment is driven by the strategic focus on strengthening internal European interconnectivity to enhance energy security and market integration. Projects aimed at linking isolated regions or creating reverse flow capabilities are predominantly onshore, involving cross-border land routes. According to the European Commission, the majority of Projects of Common Interest identified for gas infrastructure are onshore interconnectors designed to improve solidarity and flexibility among member states. These projects are critical for balancing supply and demand across the continent and preventing local shortages. The political will to complete the internal energy market drives consistent investment in onshore transmission lines. National governments prioritize these projects as they directly benefit domestic consumers and industries. The shorter construction timelines for onshore projects allow for quicker realization of security benefits. Additionally, the repurposing of existing onshore pipelines for hydrogen transport is a key component of the decarbonization strategy, leveraging current assets without the need for new offshore construction. This strategic alignment ensures that onshore pipelines remain the primary focus of infrastructure policy and investment. The ease of integrating onshore lines with existing distribution networks further enhances their value. The continued emphasis on land-based solutions for energy transition and security cements the leading position of the onshore segment.

The offshore segment is anticipated to witness the fastest CAGR of 7.2% between 2026 and 2034. This quick surge of the segment is fuelled by the development of new gas hubs and liquefied natural gas import terminals along European coastlines. To replace lost pipeline supplies, countries are rapidly expanding their LNG reception capacity, requiring offshore pipelines to connect floating storage units and terminal jetties to the onshore grid. According to the International Gas Union (IGU), Europe dramatically boosted its emergency LNG regasification limits in 2023 and 2024, though the dominant portion of this capacity was unlocked via Floating Storage and Regasification Units (FSRUs) chartered at existing marine piers and near-shore berths. Countries like Germany, the Netherlands, and Poland are constructing new terminals that rely on offshore pipelines for initial gas evacuation. Additionally, new exploration activities in the North Sea and Eastern Mediterranean are driving the need for subsea gathering and export lines. The technical complexity of offshore projects commands higher value per kilometer, contributing to rapid market growth in terms of revenue. The urgency to secure sea-based supply routes has accelerated permitting and funding for offshore infrastructure. These projects often involve international partnerships and advanced engineering solutions, attracting significant investment. The shift toward sea-based energy imports marks a structural change in European supply logistics, favoring offshore deployment. The strategic importance of coastal entry points ensures sustained demand for offshore pipeline construction and installation services. This trend is expected to continue as Europe diversifies its maritime energy connections.

The swift growth of the offshore segment is also propelled by the expansion of offshore wind farms and the emerging concept of hybrid energy hubs that combine wind power with hydrogen production and transport. Some projects envision using offshore pipelines to transport hydrogen produced from offshore wind electrolysis to shore, creating a new class of subsea infrastructure. As per the European Hydrogen Backbone (EHB) initiative, massive North Sea offshore wind expansions are actively exploring underwater hydrogen production, making subsea gas pipelines an alternative transport option to traditional high-voltage direct current (HVDC) subsea electrical cables. While primarily electrical, the integration of power-to-gas technologies creates potential demand for offshore hydrogen pipelines. Pilot projects in the North Sea are exploring the feasibility of subsea hydrogen transport, driving early-stage investment in offshore pipeline technology adapted for hydrogen. This innovative application opens a new growth frontier for the offshore segment beyond traditional oil and gas. The synergy between offshore renewable energy and gas infrastructure offers a pathway for decarbonizing the offshore sector. Government support for offshore hydrogen hubs provides financial incentives for developing these specialized pipelines. The technical challenges of subsea hydrogen transport drive research and development, attracting specialized engineering firms. This emerging application ensures that the offshore segment grows rapidly as it adapts to the energy transition. The convergence of renewable energy and gas infrastructure in marine environments creates unique opportunities for offshore pipeline developers.

COUNTRY LEVEL ANALYSIS

Germany Oil And Gas Pipeline Market Analysis

Germany was the top performer in the Europe oil and gas pipeline market and accounted for a substantial share in 2025. This leading position of the German market was attributed to its central location, high industrial demand, and aggressive energy transition policies. The country is actively restructuring its gas network to accommodate LNG imports from new terminals in Wilhelmshaven and Brunsbüttel, requiring significant new onshore and offshore pipeline connections. According to the official German Federal Network Agency (Bundesnetzagentur), the finalized and approved German Hydrogen Core Network comprises a total length of 9,040 kilometers to be built by 2032, out of which 60% (roughly 5,424 km) will consist of converted existing natural gas pipelines, while the rest will be newly constructed. This massive repurposing effort drives substantial CAPEX and OPEX activity. As per the Federal Ministry for Economic Affairs and Climate Action (BMWK), the sudden phase-out of Russian gas primarily forced Germany to accelerate the deployment of floating and onshore Liquefied Natural Gas (LNG) terminals along its northern coastlines. German transmission system operators are investing heavily in digitalization and methane leak detection to comply with strict national regulations. The country’s strong engineering base supports advanced pipeline construction and maintenance services. Germany serves as a key hub for Central European gas flows, making its infrastructure critical for regional security. The government’s substantial subsidies for hydrogen infrastructure de-risk investments and accelerate project timelines. The market in Germany is characterized by high technological sophistication and regulatory leadership. The focus on sustainability drives innovation in pipeline materials and monitoring systems. Germany’s strategic pivot defines broader European trends in infrastructure adaptation.

Italy Oil And Gas Pipeline Market Analysis

Italy was the next prominent country in the Europe oil and gas pipeline market and occupied a significant share in 2025. Its role as a major southern entry point for gas from North Africa and the Caspian region has contributed to the growth of the Italian market. The country hosts key infrastructure such as the Trans Adriatic Pipeline and the Greenstream pipeline, making it a crucial gateway for diversified supplies. According to Snam, the main Italian transmission operator, significant investments are being made to reinforce the southern network and enhance interconnectivity with Central Europe [5]. Italy is also exploring hydrogen-ready pipeline upgrades to support future decarbonization goals. The country’s extensive distribution network serves a large residential and industrial base, driving steady OPEX for maintenance and safety compliance. Recent projects include the expansion of LNG terminal capacities and associated offshore tie-ins. As per the European Commission Directorate for Energy, Italy's strategic layout has successfully secured European Project of Common Interest (PCI) status for the SouthH22 Corridor (a 3,300 km pan-continental hydrogen link), distinct from the existing, gas-focused Southern Gas Corridor footprint. The regulatory framework encourages third-party access and market integration. Italian companies are active in pipeline construction and engineering services across the Mediterranean. The market benefits from strong government support for energy security projects. The focus on maintaining supply diversity ensures continued investment in transmission assets. Italy’s role as a bridge between continents sustains its market importance.

France Oil And Gas Pipeline Market Analysis

France holds a notable share in the Europe oil and gas pipeline market due to a well-developed domestic network and increasing focus on biogas integration. The country is investing in upgrading its transmission system to enhance connections with Spain, Germany, and Belgium, supporting the internal European market. According to GRTgaz, France’s asset maintenance program focuses heavily on lifespan preservation, while its future hydrogen layout prioritizes building 100% pure, dedicated hydrogen networks across industrial hubs rather than rolling out wide-scale grid blending. France has a strong regulatory stance on methane emissions, driving investment in leak detection and repair technologies. The country is also promoting the injection of biomethane into the distribution grid, requiring local infrastructure upgrades. As per RTE and GRTgaz, while previous localized stress on France’s nuclear fleet caused temporary spikes in historical gas consumption, recent grid realities show a stabilizing nuclear output that has progressively dropped gas demand for power generation to record lows. France is participating in several EU-funded interconnector projects to improve regional solidarity. The market is driven by a balance of security, sustainability, and market integration goals. French engineering firms are leaders in pipeline safety and inspection services. The emphasis on environmental compliance shapes investment priorities. France’s central role in Western Europe ensures steady market activity.

United Kingdom Oil And Gas Pipeline Market Analysis

The United Kingdom is a mature segment in the Europe oil and gas pipeline market. Its focus is on maintaining existing assets while developing offshore infrastructure for LNG and wind integration. The country has an extensive offshore pipeline network connecting North Sea production fields and LNG terminals to the national grid. According to National Gas Transmission, significant investments are being made in asset integrity management and digital monitoring to ensure safety and efficiency. The UK is exploring the repurposing of offshore pipelines for hydrogen transport from proposed wind farms. The separation from the EU internal energy market has required adjustments in trading and infrastructure management,but physical interconnectors with Belgium and the Netherlands remain vital. The UK’s advanced regulatory framework drives high standards for pipeline safety and environmental protection. The decline in domestic gas production increases reliance on imports, sustaining demand for terminal and pipeline infrastructure. The market is characterized by high technical expertise and strict compliance requirements. Offshore decommissioning and repurposing present new opportunities for pipeline service providers. The UK continues to be a leader in offshore pipeline technology. The focus onon one-zeroargets influences long-term infrastructure planning.

Netherlands Oil And Gas Pipeline Market Analysis

The Netherlands is another key player in the Europe oil and gas pipeline market due to its extensive port infrastructure and gas field legacy. The country is a major entry point for LNG and pipeline gas from Norway and Russia (historically), requiring robust transmission and distribution networks. According to industrial construction updates published by Gasunie and Hydrogen Europe, the Dutch national hydrogen backbone involves building highly specialized new regional links (such as the newly completed 32-km pipeline segment inside the Port of Rotterdam). The Netherlands is investing heavily in offshore infrastructure to support wind energy and potential hydrogen imports. The country’s flat terrain facilitates extensive distribution networks serving dense urban and industrial areas. Dutch companies are pioneers in pipeline safety technology and methane reduction techniques. The market benefits from strong government support for energy transition projects. The Netherlands acts as a gateway for gas flows into Germany and Belgium. The focus on sustainability and innovation drives market growth. The integration of renewable gases into the existing grid is a key priority. The Netherlands’ strategic position ensures continued market relevance.

COMPETITIVE LANDSCAPE

The competition in the Europe oil and gas pipeline market is characterized by a mix of state-owned transmission system operators and private infrastructure developers who compete primarily on regulatory compliance, technical expertise, and strategic alignment with national energy goals. The market exhibits high barriers to entry due to significant capital requirements, a complex permitting process, and strict safety standards. Key players distinguish themselves through their ability to execute large-scale repurposing projects for hydrogen and their proficiency in managing cross-border interconnectivity. Competition is less about price and more about reliability, security of supply,y and adherence to environmental mandates. The regulatory framework heavily influences competitive dynamics as operators must comply with EU directives on market integration and decarbonization. Collaborative ventures are common as companies join forces to share risks and costs associated with major infrastructure projects. The shift toward hydrogen creates a new competitive landscape where technological leadership and early mover advantages are critical. Established operators leverage their existing asset bases and institutional knowledge to maintain dominance while new entrants focus on niche, innovative solutions. Transparency and stakeholder engagement are increasingly important differentiators as public scrutiny of energy infrastructure intensifies. Over,, athe market rewards entities that can balance immediate security needs lonwith g-term sustainability commitments.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Oil and Gas Pipeline Market include

- Saipem S.p.A.

- Tenaris S.A.

- Vallourec S.A.

- Europipe GmbH

- Mannesmann Line Pipe GmbH

- TMK Group

- ChelPipe Group

- National Oilwell Varco, Inc. (NOV)

- Technip Energies N.V.

- Allseas Group S.A.

- John Wood Group plc

- Subsea7 S.A.

TOP LEADING PLAYERS IN THE MARKET

- Enagás operates as a key technical manager and transmission system operator in Spain with significant influence on the Southern European gas infrastructure landscape. The company manages an extensive high-pressure network that connects LNG terminals to the broader European grid, ensuring supply security for the Iberian Peninsula and beyond. Recent actions include accelerating the development ofhydrogen-readyy infrastructure by launching pilot projects for blending renewable hydrogen into existing natural gas pipelines. Enagás has strengthened its market position by securing EU funding for critical interconnection projects that enhance regional solidarity and eliminate energy isolation. The company actively participates in the European Hydrogen Backbone initiative, positioning itself as a leader in the energy transition. Enagás invests heavily in digitalization and methane leak detection technologies to comply with stringent environmental regulations. Their strategic focus on repurposing assets forlow-carbonn gases ensures long-term relevance. The company collaborates with international partners to develop cross-border infrastructure, facilitating diverse supply routes. This proactive approach supports national energy independence goals while contributing to continental decarbonization efforts.

- Snam is a leading Italian energy infrastructure company managing a vast network of gas transmission pipelines and storage facilities crucial for Southern European energy security. The company plays a pivotal role in transporting gas from North African and Caspian sources into Central Europe through key corridors like the Trans Adriatic Pipeline. Recent strategic initiatives include the substantial expansion of its hydrogen backbone pla,n aiming to convert thousands of kilometers of existing pipelines for hydrogen transport by 2030. Snam has strengthened its position by investing in advanced monitoring systems and predictive maintenance technologies to enhance network reliability and safety. The company actively engages in regulatory discussions to shape the framework for decarbonized gas markets in Europe. Snam also focuses on integrating biomethane injection points into its distribution netwo,,rk supporting local renewable energy production. Their commitment to sustainability is evident in aggressive methane reduction targets and transparent reporting practices. Snam leverages its geographic advantage to facilitate energy diversification and market integration across the Mediterranean region.

- Gasunie serves as the primary natural gas infrastructure operator in the Netherlands and northern Germany playing a central role in Northwest European energy logistics. The company manages a complex network of transmission pipe,lines storage faci,lities and LNG terminals that act as a gateway for gas imports into the continent. Recent actions include the rapid development of a dedicated hydrogen transport network leveraging existing assets to support industrial decarbonization in the region. Gasunie has strengthened its market position by forming strategic partnerships with offshore wind developers to explore subsea hydrogen transportation solutions. The company invests significantly in innovation labs to test new materials and technologies for hydrogen compatibility and safety. Gasunie actively supports government policies aimed at phasing out natural gas by providing low-carbon carbon alternatives. Their expertise in managing large-scale infrastructure transitions makes them a key partner for European energy planning. The company prioritizes operational excellence and environmental stewardship to maintain public trust and regulatory compliance.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe oil and gas pipeline market employ several strategic approaches to maintain competitiveness and ensure long-term viability amidst the energy transition. Asset repurposing for hydrogen transport is a primary strategy allowing companies to leverage existing infrastructure for low-carbon applications while minimizing stranded asset risks. Strategic partnerships with renewable energy developers and government bodies facilitate access to funding and regulatory support for green infrastructure projects. Investment in digitalization and advanced monitoring technologies enhances operational efficiency, safet,y and compliance with strict methane emission regulations. Companies focus on expandincross-borderer interconnectivity to strengthen regional energy security and market integration, aligning with EU policy objectives. Diversification into biomethane injection and storage services creates new revenue streams while supporting local circular economy initiatives. Regulatory engagement remains crucial as participants work to shape favorable frameworks for decarbonized gas markets. Talent development and workforce upskilling address the growing need for specialized technical capabilities in hydrogen and digital systems. These combined strategies enable operators to navigate the complex shift from fossil fuels to sustainable energy carriers.

MARKET SEGMENTATION

This research report on the europe oil and gas pipeline market is segmented and sub-segmented into the following categories.

By Activity

- Operational Expenditure (OPEX)

- Capital Expenditure (CAPEX)

By Function

- Transmission Lines

- Distribution Lines

By Location of Deployment

- Onshore

- Offshore

By Country

- Germany

- Italy

- France

- United Kingdom

- Netherlands

Frequently Asked Questions

1. What is driving the growth of the Europe oil and gas pipeline market?

The Europe oil and gas pipeline market is driven by increasing investments in energy infrastructure, the modernization of aging pipeline networks, rising natural gas demand, and efforts to strengthen regional energy security. The expansion of cross-border pipeline projects, integration of advanced pipeline monitoring technologies, and the transition toward cleaner energy sources such as natural gas are further supporting market growth. Recent EU energy security policies and diversification of gas supply routes are also influencing infrastructure investments

2. Which countries are leading the Europe oil and gas pipeline market?

Germany, the United Kingdom, France, Italy, and Norway are among the leading contributors to the Europe oil and gas pipeline market. These countries have well-developed pipeline infrastructure, significant oil and natural gas consumption, and ongoing investments in pipeline modernization and cross-border energy connectivity. Norway also plays a critical role as one of Europe's largest natural gas suppliers.

3. What are the major trends shaping the Europe oil and gas pipeline market?

Key trends include the adoption of smart pipeline monitoring systems, digital asset management, predictive maintenance using artificial intelligence, methane emission reduction initiatives, expansion of hydrogen-ready pipeline infrastructure, and increased investment in cross-border natural gas transportation. The market is also witnessing greater emphasis on sustainability, safety, and regulatory compliance.

4. What challenges are affecting the Europe oil and gas pipeline market?

The Europe oil and gas pipeline market faces challenges including stringent environmental regulations, high pipeline construction and maintenance costs, geopolitical uncertainties, permitting delays, and the ongoing transition toward renewable energy. In addition, evolving methane emission regulations and changing energy import strategies continue to influence investment decisions across the region.

5. What is the future outlook for the Europe oil and gas pipeline market?

The Europe oil and gas pipeline market is expected to witness steady growth during the forecast period, supported by investments in pipeline modernization, energy diversification strategies, increasing demand for natural gas transportation, and the development of hydrogen-compatible pipeline networks. Continued government initiatives to enhance energy resilience and improve cross-border connectivity are expected to create new opportunities for pipeline operators and infrastructure developers.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com