Europe Orange Market Size, Share, Trends & Growth Forecast Report, Segmented By Product (Fresh Orange, Processed Orange), Application And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis From (2025 To 2033)

Europe Orange Market Report Summary

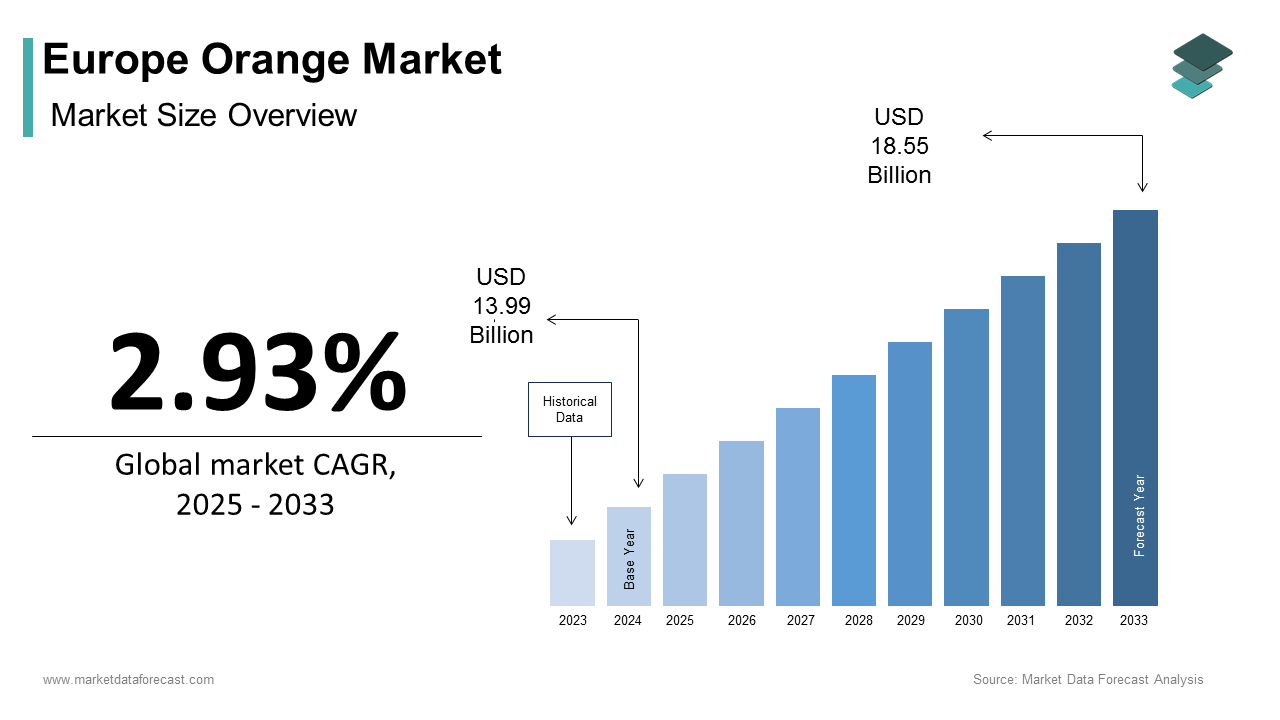

The European orange market was valued at USD 13.99 billion in 2024, is anticipated to reach USD 14.40 billion in 2025, and is projected to reach USD 18.15 billion by 2033, growing at a CAGR of 2.93% during the forecast period from 2025 to 2033. The growth of the European orange market is driven by rising demand for fresh and natural fruit products, increasing health consciousness among consumers, and the expanding use of oranges in the food, beverage, and nutraceutical sectors. The market also benefits from strong production bases in Southern Europe, growing consumer preference for vitamin-rich diets, and the increasing adoption of organic and sustainable agricultural practices.

Key Market Trends

- Growing consumer inclination toward fresh and organic oranges due to rising health awareness.

- Expansion of orange juice and beverage manufacturing driven by demand for natural, non-alcoholic drinks.

- Increasing utilization of oranges in cosmetics, nutraceuticals, and confectionery applications.

- Emphasis on sustainable farming and traceability programs among European orange producers.

- Rising exports of European oranges supported by improved trade infrastructure and regional branding initiatives.

Segmental Insights

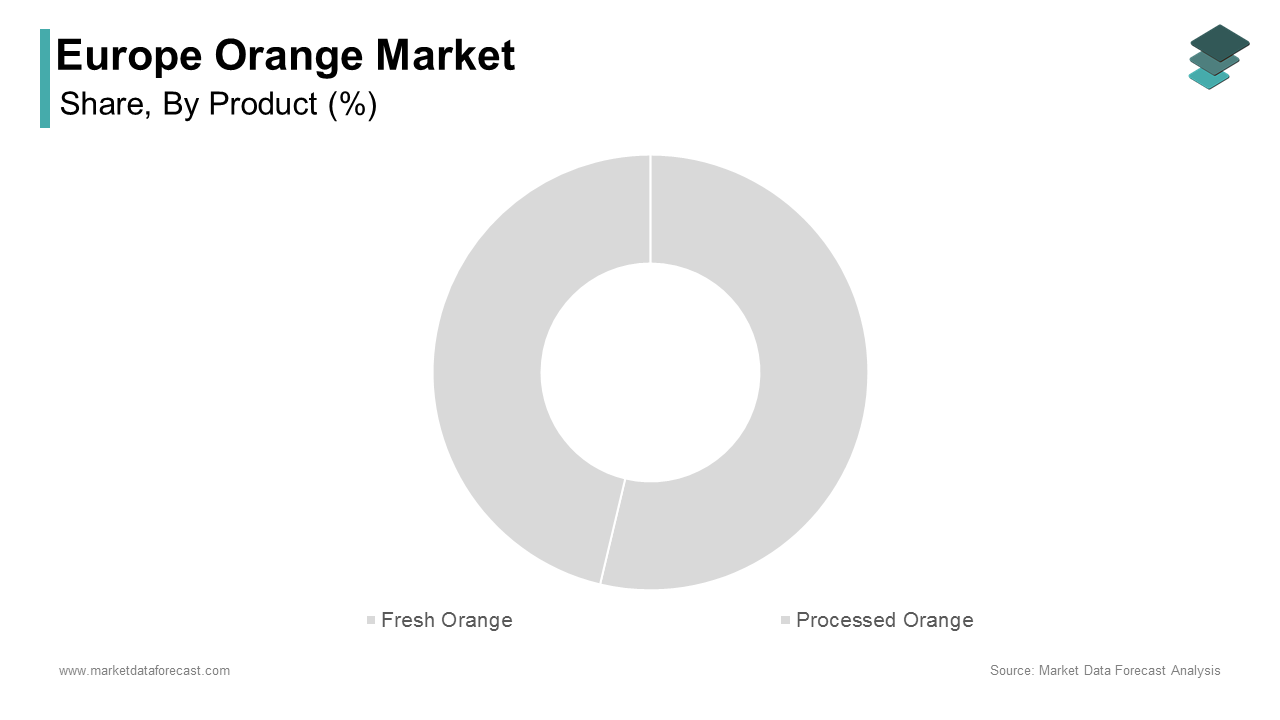

- Based on product, the fresh oranges segment dominated the European orange market in 2024, holding the largest share. This dominance is driven by the growing preference for whole fruit consumption, supported by the fruit’s nutritional value, immune-boosting properties, and longer shelf life compared to processed forms.

- Based on the application, the food and beverage segment was the most prominent in 2024, capturing a significant market share. The segment’s growth is attributed to the high consumption of orange-based juices, desserts, confectionery, and bakery products, along with the expanding use of orange flavoring in beverages across Europe.

Regional Insights

The European orange market shows significant geographical concentration, with Mediterranean countries dominating due to favorable climatic conditions and robust agricultural output.

- Spain was the top performer in the European orange market, accounting for 28.6% of the total regional market share in 2024, supported by its large-scale cultivation, export capabilities, and leading position in juice production.

- Italy followed as another key market, driven by its strong demand for orange-based beverages and processed products.

- France and Germany recorded steady demand growth, driven by consumer preference for organic and imported orange varieties.

- The Netherlands acted as a critical trade and distribution hub for fresh oranges and juice concentrates across Europe.

Competitive Landscape

The European orange market is moderately fragmented, with companies focusing on sustainable sourcing, value-added processing, and expansion of product portfolios through innovation in juice, concentrate, and snack segments. Strategic collaborations between growers, beverage producers, and distributors are enhancing supply chain efficiency and regional market presence. Prominent companies operating in the European orange market include Eckes-Granini Group GmbH, Refresco Group B.V., Grupo García Carrión S.A., Valensina GmbH, Zuegg S.p.A., Louis Dreyfus Company B.V., and Mercadona S.A.

Europe Orange Market Size

The Europe orange market size was calculated to be USD 13.99 billion in 2024 and is anticipated to be worth USD 18.15 billion by 2033, from USD 14.40 billion in 2025, growing at a CAGR of 2.93% during the forecast period.

An orange is a round, citrus fruit produced by the tree scientifically known as Citrus sinensis, belonging to the family Rutaceae. While Europe is not a major global producer of oranges outside of specific Mediterranean zones, the continent remains a significant consumer market with deeply ingrained citrus consumption patterns. According to a 2025 report published in Citrus Industry Magazine, the EU's total consumption of citrus fruit was 11 million tons in 2024, with figures varying significantly by member state. Spain dominates intra-European orange production, accounting for over sixty percent of the EU’s total output, as per data from the Spanish Ministry of Agriculture, Fisheries and Food. Italy and Greece contribute smaller but culturally significant volumes, particularly of specialty varieties like blood oranges. Consumption is sustained not only through fresh fruit intake but also via juice. Seasonality, climatic vulnerability, and stringent phytosanitary regulations shape supply dynamics, while evolving dietary preferences and sustainability concerns influence demand. The market is further defined by strict EU regulations on pesticide residue labeling and origin transparency, which directly impact sourcing and retail strategies.

MARKET DRIVERS

Rising Health Consciousness Fuels Fresh Orange Demand

Consumers are increasingly prioritizing whole food sources of essential nutrients, with vitamin C-rich oranges benefiting significantly from this dietary shift, and this propels the growth of the Europe orange market. The European Food Safety Authority (EFSA) publishes Dietary Reference Values for nutrients like vitamin C, which inform national health campaigns and broader public food safety initiatives like the #Safe2EatEU campaign. The behavioral trend is reflected in household purchasing data. Retailers have responded by expanding organic and traceable orange offerings. In the Netherlands, Albert Heijn introduced QR-coded oranges in 2018 by enabling consumers to verify farm origin and harvest date. These developments emphasize how health-driven demand is reshaping procurement and marketing strategies across the fresh produce sector.

Expansion of Premium Juice and Functional Beverage Segments

Value innovation added orange products, particularly premium and functional beverages, is also a factor bolstering the expansion of the Europe orange market. Orange juice continues to be the most widely enjoyed fruit juice across the European Union, as per research. However, the segment is evolving toward enhanced formulations. In Germany, fortified orange juice varieties with added nutrients have seen a notable increase in market demand, according to sources. Cold-pressed and not from concentrate juices have also gained traction. In the United Kingdom, premium orange juice is gaining popularity and now contributes significantly to the overall juice market, as per research. Spain’s juice processors have capitalized on this by investing in aseptic cold fill technology, which preserves flavor without pasteurization. Also, in Spain, the regional authorities in Andalusia have extended support to several juice exporters in achieving organic certification standards, according to sources. This shift toward functional and clean-label products is redefining orange utilization beyond basic refreshment into a health-aligned daily ritual.

MARKET RESTRAINTS

Stringent EU Pesticide Regulations Limit Supply Flexibility

Supply constraints impede the growth of the Europe orange market. This is due to the European Union’s rigorous Maximum Residue Level standards for pesticides, which restrict imports from key non-EU producing countries. These rejections disrupt seasonal supply chains, especially during winter when European production is minimal. Consequently, importers must source from a narrower pool of compliant growers, increasing costs and reducing variety. This regulatory stringency, while protective of consumer health, inadvertently heightens market vulnerability to climatic shocks in domestic production zones and limits diversification of supply during shortages.

Climate-Induced Production Volatility in Southern Europe

Orange cultivation in the region is highly concentrated in climatically sensitive Mediterranean regions and makes the supply chain acutely vulnerable to extreme weather events, which hampers the expansion of the Europe orange market. According to a USDA Foreign Agricultural Service report, orange production in the European Union declined during the 2022–2023 season, with significant reductions occurring in Italy due to drought. Also, the fluctuations directly impact market availability and price stability. Many farms still rely on flood irrigation. Production instability is expected to intensify without the widespread adoption of precision irrigation and drought-resistant rootstocks. This climatic fragility not only threatens domestic output but also affects the EU’s goal of reducing import dependency for fresh produce during important off-season months.

MARKET OPPORTUNITIES

Growth of Organic and Regenerative Citrus Farming

A structural shift toward sustainable production models driven by consumer demand and policy incentives is setting up new opportunities for the growth of the Europe orange market. According to sources, "Spain led the EU in organic citrus area in 2020, and the overall EU organic area grew over this period. This expansion is supported by the Common Agricultural Policy, which allocates direct payments to farmers transitioning to organic practices. Consumer response has been robust. Price premiums of up to thirty percent are widely accepted. Furthermore, retailers like Edeka in Germany now prioritize regenerative agriculture certifications that go beyond organic to include soil health and biodiversity metrics. These developments create a premium niche that enhances grower margins while aligning with the EU’s Farm to Fork Strategy, which targets twenty-five percent of agricultural land under organic management by 2030.

Development of Circular Economy Models in Juice Processing

Innovative valorization of orange byproducts offers a key opportunity for the expansion of the Europe orange market. According to sources, millions of tons of citrus waste are generated annually in the EU, primarily from juice production. However, new technologies are transforming this waste stream into high-value outputs. In addition, the Netherlands-based company PeelPioneers operates a facility that extracts d-limonene from peels for use in eco-friendly cleaning products, supplying major retailers like Jumbo. Such circular initiatives can increase the revenue per ton of processed oranges by up to twenty percent. The EU's Horizon Europe program, particularly through the Circular Bio-based Europe Joint Undertaking (CBE JU), has provided substantial funding for various biorefinery projects since 2021. These models not only reduce landfill burden but also create new B2B revenue channels, which align the orange market with broader decarbonization and resource efficiency mandates.

MARKET CHALLENGES

Water Scarcity Threatens Long-Term Cultivation Viability

Persistent water shortages remain a major challenge for the Europe orange market. According to the European Drought Observatory, over sixty percent of Spain’s citrus growing areas in Valencia and Andalusia experienced severe to extreme drought conditions throughout 2023. In provinces severely affected by drought, irrigation water allocations for citrus farms were reduced. For example, some authorities in 2023 implemented reductions of up to forty percent or more for agricultural use. Groundwater depletion is equally concerning. These constraints are compounded by the EU Water Framework Directives that increasingly restrict agricultural withdrawals to protect ecosystems. Large-scale investment in drip irrigation and water recycling infrastructure, which requires capital outlays per hectare, many smallholder farms face existential risk. This hydrological force affects the long-term reliability of domestic orange supply and increases exposure to global market volatility.

Trade Disruptions from Geopolitical and Phytosanitary Barriers

External supply chain disruptions owing to geopolitical tensions and evolving phytosanitary protocols obstruct the expansion of the Europe orange market. Moreover, the redirection of South African citrus exports away from Russia following the Ukraine conflict led to oversupply in European ports, depressing grower returns in 2023. Compounding these issues, the EU’s new Deforestation Regulation requires stringent traceability for agricultural commodities, which may indirectly affect orange imports if packaging or transport involves non-compliant materials. The European Court of Auditors has warned that current inspection capacity at entry points is insufficient to handle increased documentation demands, potentially causing delays. These external vulnerabilities draw attention to the market’s dependence on fragile international supply corridors and emphasize the urgency of diversifying sourcing while strengthening domestic resilience through varietal innovation and storage infrastructure.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 2.93% |

| Segments Covered | By Product, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Eckes-Granini Group GmbH, Refresco Group B.V., Grupo García Carrión S.A., Valensina GmbH, Zuegg S.p.A., Louis Dreyfus Company B.V., Mercadona S.A. |

SEGMENTAL ANALYSIS

By Product Insights

The fresh oranges segment held the leading share of the European orange market in 2024. The deep-rooted cultural consumption habits and strong retail integration across households are the key factors contributing to the growth of the fresh oranges segment. In addition, the emphasis on whole fruit in national dietary guidelines is also a primary driver of this segment. Retail innovation further sustains demand. In France, major chains have introduced seasonal freshness labeling that displays harvest dates and farm distance, enhancing consumer trust. Apart from these, the rise of convenience formats such as pre-peeled and segmented fresh oranges has expanded usage among urban professionals. This blend of tradition, convenience, and nutritional credibility ensures fresh oranges remain the cornerstone of European citrus consumption.

The processed orange segment is predicted to witness the highest CAGR of 6.8% from 2025 to 2033. The rapid growth of the processed orange segment is propelled by two interlinked forces. Moreover, the demand for clean-label beverages is reshaping juice formulation. Cold-pressed and high-pressure processed juices now occupy premium shelf space in retailers like Edeka and Tesco. In addition, the food service sector is increasingly incorporating orange derivatives into culinary and mixology applications. Furthermore, the EU’s ban on artificial colors in 2022 spurred food manufacturers to adopt orange carotenoids as natural colorants. These trends illustrate how processed orange is evolving from a commodity into a multifunctional ingredient across beverage, food, and industrial domains.

By Application Insights

The food and beverage segment was the prominent segment in the Europe orange market by capturing a significant share in 2024. The dominance of the food and beverage segment is driven by the fruit’s dual role as a standalone refreshment and a versatile ingredient. Orange juice alone represents the largest single beverage category by volume in the EU. Beyond beverages, fresh and processed oranges are integral to European culinary traditions, from marmalades in the United Kingdom to duck à l’orange in France. Modern food manufacturing further amplifies usage. The clean label movement has intensified this reliance as manufacturers replace artificial additives with citrus extracts. Retailers also drive demand through private label expansion. This pervasive integration across home cooking, industrial food, and beverage production cements Food and Beverage as the undisputed core application.

The personal care and cosmetics segment is estimated to register the fastest CAGR of 9.2% from 2025 to 2033. The clean beauty movement and regulatory shifts favoring bio-based ingredients have significantly contributed to the growth of the personal care and cosmetics segment. Orange essential oil and d-limonene are increasingly used as natural fragrances and solvents, replacing synthetic alternatives. Consumer preference is equally influential. Major brands have responded decisively. Furthermore, circular economy initiatives enhance appeal. This convergence of regulatory compliance, sustainability, and sensory appeal positions orange as a cornerstone of next-generation natural cosmetics.

REGIONAL ANALYSIS

Spain Orange Market Analysis

Spain was the top performer in the Europe orange market and accounted for a 28.6% share in 2024. The prominence of Spain in the regional market is mainly driven by its status as the EU’s largest producer and exporter of fresh citrus. The market is characterized by vertically integrated cooperatives such as Anecoop and Naranjas Dacsa that control everything from orchard to supermarket shelf, ensuring quality and traceability. Recent investments in precision agriculture have enhanced resilience. Export orientation remains strong. However, domestic consumption is also rising due to government nutrition campaigns. This dual strength in production scale and market responsiveness strengthens Spain’s dominance.

Germany Orange Market Analysis

Germany was the second-largest in the Europe orange market by capturing 22.6% share in 2024. It is the continent’s top importer and consumer of both fresh and processed oranges. The market is propelled by high consumer standards for quality and sustainability. Discount chains like Aldi and Lidl now exclusively stock oranges with EU organic or Fairtrade certification. Juice consumption is equally robust. Innovation in convenience formats is accelerating. Besides, the rise of plant-based diets has boosted demand for orange as a natural flavor enhancer in meat alternatives. This combination of volume scale, quality expectation, and product diversification makes Germany the central demand engine of the European orange economy.

France Orange Market Analysis

France is another key player in the European orange market due to its emphasis on premium quality and gastronomic application. The market is deeply influenced by culinary culture. Retail trends reflect this sophistication. Juice consumption is shifting toward functional formulations. Moreover, the government’s anti-food waste law has spurred partnerships between juice processors and supermarkets to utilize imperfect fruit. This fusion of gastronomy, wellness, and ethical sourcing defines France’s high-value approach to orange consumption.

Italy Orange Market Analysis

Italy experienced steady expansion in the European orange market owing to its unique heritage varieties and strong domestic processing industry. This differentiation enables premium pricing and export success. Domestically, oranges are central to both fresh consumption and industrial use. Conserve Italia, the country’s largest agro cooperative, processes tons annually into juice, marmalade, and essential oils. The rise of slow food and terroir-based consumption has further elevated local varieties. Besides, orange blossom water is experiencing a revival in artisanal pastry and liqueur production. This strategic focus on geographical uniqueness and value addition allows Italy to maintain relevance despite modest volume compared to Spain.

United Kingdom Orange Market Analysis

The United Kingdom is predicted to grow in the European orange market from 2025 to 2033 and is navigating a strategic recalibration of its supply chains following Brexit. Consumer behavior is shifting toward health and convenience. Retail innovation is accelerating. Juice trends reflect functional demands. Furthermore, the cost-of-living crisis has increased demand for affordable nutrition, making oranges a staple in budget meal planning. Despite logistical complexities, the UK’s adaptive import strategy and responsive retail sector ensure its continued significance in the European orange landscape.

COMPETITION OVERVIEW

The Europe orange market features a complex competitive landscape shaped by the interplay of domestic producers, importers, processors, and retail giants. Competition is not solely based on price but increasingly revolves around quality consistency, sustainability credentials, and supply chain agility. Spanish cooperatives dominate fresh supply through scale and logistical efficiency, while multinational agribusinesses leverage global sourcing to ensure year-round availability. At the same time, niche players from Italy and France compete on geographical uniqueness and premium branding, particularly with blood oranges and Corsican varieties. Processors face the insistence or burden to innovate in clean-label juices and byproduct utilization amid tightening regulations on additives and packaging. Retailers exert significant influence by setting private label standards and demanding full traceability. The entry of vertically integrated food tech startups offering direct-to-consumer citrus boxes adds further disruption. Ultimately, success hinges on the ability to balance cost efficiency with environmental responsibility while adapting to fragmented yet discerning consumer preferences across diverse European regions.

KEY MARKET PLAYERS

A few of the dominating players in the Europe orange market include

- Eckes-Granini Group GmbH

- Refresco Group B.V

- Grupo García Carrión S.A

- Valensina GmbH

- Zuegg S.p.A

- Louis Dreyfus Company B.V

- Mercadona S.A

Top Strategies Used by the Key Market Participants

Key players in the Europe orange market deploy a range of strategic approaches to secure competitive advantage and meet evolving regulatory and consumer demands. Vertical integration from farm to retail ensures quality control and supply chain resiliency, particularly during seasonal shortages. Sustainability is central, with companies investing in water-efficient irrigation, organic certification, and waste valorization to comply with the EU Farm to Fork Strategy. Digital traceability using blockchain and QR codes enhances transparency and builds consumer trust in origin and safety. Product diversification into functional beverages, premium ready-to-eat formats, and cosmetic ingredients expands revenue beyond traditional fresh fruit. Finally, strategic partnerships with retailers, governments, and research institutions drive innovation in varietal development, post-harvest technology, and circular economy models, strengthening long-term market relevance.

LEADING PLAYERS IN THE EUROPE ORANGE MARKET

Louis Dreyfus Company

Louis Dreyfus Company is a global agricultural merchant with extensive operations in the European citrus supply chain, sourcing oranges from Spain, Italy, and North Africa for distribution across retail and food service channels. The company plays a pivotal role in global orange logistics by managing temperature-controlled transport and storage infrastructure that ensures year-round availability. The initiatives support its position as a responsible and technologically advanced supplier aligned with EU regulatory and consumer expectations.

Anecoop Group

Anecoop Group is a leading Spanish agricultural cooperative headquartered in Valencia and one of Europe’s largest fresh orange producers and exporters. It integrates over twelve thousand growers and operates advanced packing and cold chain facilities that serve markets from Scandinavia to the Balkans. The cooperative has intensified its focus on varietal innovation, introducing seedless and easy-peel orange cultivars tailored to Northern European consumer preferences. Its investment in digital farm management tools also enables real-time quality control, enhancing shelf life and reducing post-harvest losses across the European retail network.

Société des Agrumes du Sud Ouest

Société des Agrumes du Sud Ouest is a prominent French citrus producer specializing in premium oranges from Corsica and the Mediterranean coast. The company supplies high-end retailers and gourmet food brands across Western Europe with a strong emphasis on terroir-driven quality and Protected Geographical Indication compliance. In recent years, it has diversified into value-added products, including cold-pressed orange oil and organic marmalades, targeting the natural foods segment.

MARKET SEGMENTATION

This research report on the Europe orange market is segmented and sub-segmented into the following categories.

By Product

- Fresh Orange

- Processed Orange

By Application

- Food & Beverage

- Pharmaceuticals

- Personal Care & Cosmetics

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving the growth of the Europe orange market?

Key drivers include increasing demand for natural and vitamin C-rich beverages, rising health consciousness, growing consumption of fresh fruits, and the expansion of juice processing industries.

2. What are the major restraints affecting the market?

Challenges include climatic variability impacting orange yields, rising production costs, competition from tropical fruit imports, and fluctuating orange juice prices.

3. What are the major applications of oranges in Europe?

Oranges are primarily used for fresh consumption, juice extraction, confectionery, flavoring, and the production of essential oils and fragrances.

4. What are the main distribution channels for oranges in Europe?

The market operates through supermarkets and hypermarkets, convenience stores, specialty fruit stores, and online retail platforms.

5. Who are the key players in the Europe orange market?

Major players include Eckes-Granini Group GmbH, Refresco Group B.V., Grupo García Carrión S.A., Valensina GmbH, Zuegg S.p.A., Louis Dreyfus Company B.V., and Mercadona S.A.

6. What trends are shaping the Europe orange market?

Trends include the growing adoption of organic and sustainably sourced oranges, the rise of cold-pressed juices, and advancements in post-harvest technology and packaging.

7. How is climate change impacting orange production in Europe?

Extreme weather patterns and temperature fluctuations are affecting yield quality and harvest timing, particularly in southern Europe.

8. What is the outlook for the European orange juice segment?

The orange juice segment is expected to witness moderate growth, supported by innovations in low-sugar formulations and rising consumer preference for natural juices.

9. What opportunities exist in the Europe orange market?

Opportunities include expanding organic farming, leveraging e-commerce for fruit delivery, and developing value-added orange-based products.

10. How competitive is the Europe orange market?

The market is moderately fragmented with strong domestic players in Spain, Italy, and Germany, alongside multinational juice processors and retailers competing for market share.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com