Europe Point-of-Care (POC) Diagnostics Market Size, Share, Trends & Growth Forecast Report By Product (Glucose Monitoring, Infectious Diseases), End-User and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Point-of-Care (POC) Diagnostics Market Size

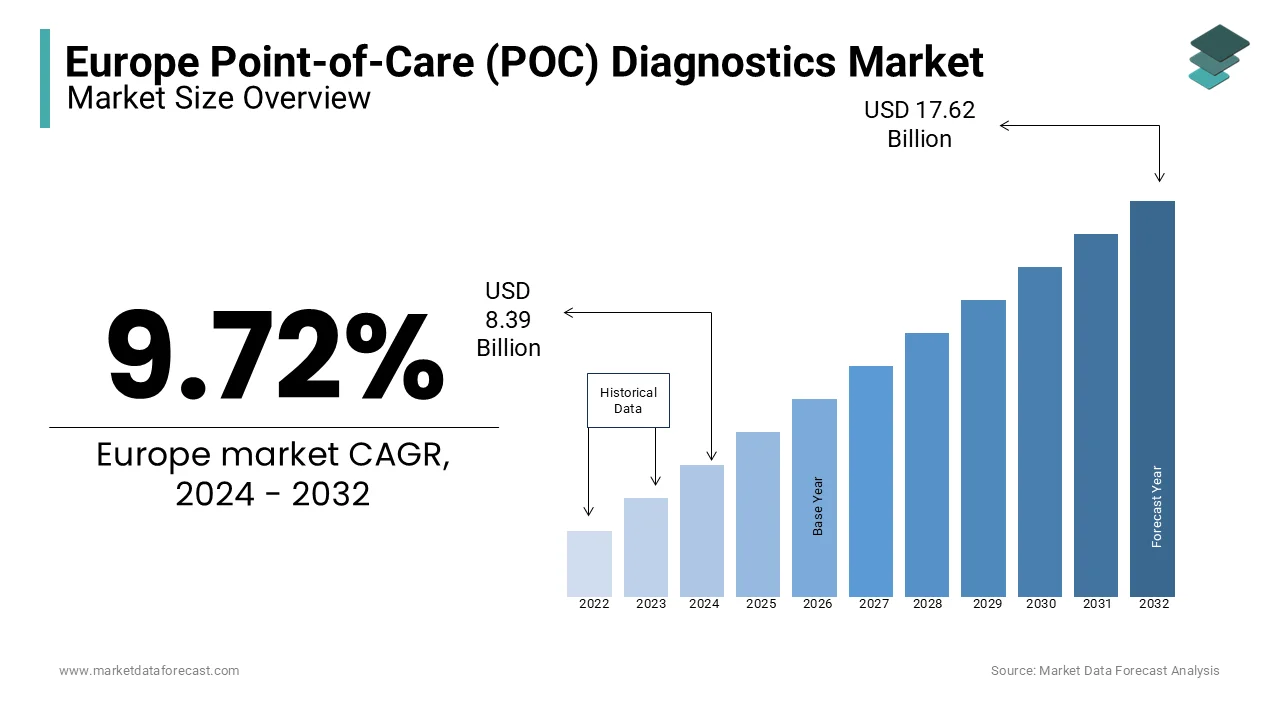

The POC diagnostics market in Europe was worth USD 8.39 billion in 2024. The European market is estimated to grow at a CAGR of 9.72% from 2025 to 2033 and be valued at US 19.34 billion by the end of 2033 from USD 9.21 billion in 2025.

Point-of-Care (POC) Diagnostics refers to the deployment of rapid, near-patient testing technologies that enable immediate clinical decision-making outside centralized laboratory environments. These diagnostic systems are utilized in diverse settings, including primary care clinics, ambulances, pharmacies, and home care, delivering real-time results for conditions such as infectious diseases, cardiovascular disorders, diabetes, and pregnancy. In recent years, many general practitioner consultations in the EU have included at least one form of diagnostic assessment, reflecting the growing role of timely testing in primary care delivery. The integration of POC testing into national health strategies has been accelerated by aging populations and rising chronic disease prevalence. For instance, Millions of adults in Europe are living with diabetes or prediabetes, creating a strong need for regular glucose monitoring.. This clinical urgency, combined with advancements in microfluidics and biosensor technology, has solidified POC diagnostics as a cornerstone of decentralized healthcare across the region.

MARKET DRIVERS

Expansion of Primary and Community-Based Healthcare Infrastructure

The strategic shift toward decentralized care models, emphasizing early diagnosis and reduced hospital burden is a pivotal force behind the growth of POC diagnostics in Europe. National health systems in countries like the UK, Germany, and Sweden are increasingly channeling resources into community clinics and mobile health units equipped with rapid testing capabilities. A significant share of non-emergency patient referrals in the EU are now managed within primary care settings, where on-site POC tests are often used for conditions like infections, HbA1c, and cardiac markers. In the UK, health authorities have introduced POC CRP (C-reactive protein) testing in general practices to help reduce unnecessary antibiotic prescriptions. This institutional prioritization of front-line diagnostics enhances patient throughput and clinical efficiency, driving sustained demand for reliable, easy-to-operate POC platforms across urban and rural care networks.

Rising Burden of Chronic Diseases Requiring Frequent Monitoring

The escalating prevalence of chronic conditions across Europe has intensified the need for continuous, patient-centric monitoring, positioning POC diagnostics as essential tools in long-term disease management. Cardiovascular diseases remain a leading cause of death in the WHO European Region, accounting for millions of fatalities each year. Similarly, diabetes affects large number of adults across Europe, with many more cases thought to be undiagnosed. These conditions demand regular biomarker tracking, such as glucose, lipid profiles, and NT-proBNP, outside hospital settings. In response, countries like the Netherlands and Denmark have integrated POC lipid screening into routine pharmacy services, enabling early intervention. Some studies suggest that patients using POC HbA1c testing at regular intervals may achieve faster improvements in glycemic control compared to those relying only on lab-based results.

MARKET RESTRAINTS

Fragmented Reimbursement Frameworks Across European Countries

The lack of harmonized reimbursement policies across European healthcare systems is one of the most significant impediments to the widespread adoption of POC diagnostics. While countries like Germany and France offer structured reimbursement for specific POC tests in primary care, others such as Spain and Greece provide limited or inconsistent coverage, discouraging investment in diagnostic infrastructure. Reports indicate that only a portion of EU member states have established national reimbursement codes for common POC assays like HbA1c or influenza testing. This disparity creates financial uncertainty for clinics and pharmacies, particularly in rural areas where cost recovery is critical. Surveys suggest that many general practitioners in Southern and Eastern Europe avoid using POC devices due to unclear billing procedures, which limits broader adoption despite clinical need.

Stringent Regulatory Compliance Demands Under IVDR

The implementation of the In Vitro Diagnostic Regulation (IVDR) in May 2022 has introduced rigorous performance evaluation and clinical evidence requirements that are disproportionately affecting POC test manufacturers, particularly small and mid-sized enterprises. Unlike the previous directive, IVDR mandates extensive technical documentation, post-market surveillance, and notified body oversight for most POC devices, significantly increasing time-to-market and compliance costs. Like, a significant share of POC test submissions faced lengthy delays due to limited notified body capacity. Reports from national regulators suggest there has been a noticeable decline in new POC device certifications following the introduction of IVDR compared to the previous regulatory framework. This bottleneck restricts innovation and market access, especially for novel rapid tests targeting emerging pathogens or niche biomarkers, thereby constraining the sector’s adaptive capacity.

MARKET OPPORTUNITIES

Integration of POC Diagnostics with National Digital Health Platforms

The continent-wide push toward digital health interoperability presents a transformative opportunity for POC diagnostics to become embedded within electronic health record (EHR) ecosystems and telemedicine networks. The European Commission’s initiative aims to connect health systems across all member states, supporting data exchange between point-of-care devices and clinical databases. Countries like Estonia and Finland already support real-time upload of POC glucose and INR results into national EHRs, reducing administrative burden and improving care continuity. A recent pilot project suggested that integrating POC test data into primary care digital workflows may help reduce consultation times and improve diagnostic accuracy. As more nations adopt FHIR-based standards, POC device manufacturers are partnering with health IT firms to ensure compatibility, unlocking scalable, data-driven care models across Europe.

Growing Demand for Infectious Disease Surveillance in Community Settings

The aftermath of the COVID-19 pandemic has catalyzed a structural shift in Europe’s approach to infectious disease monitoring, with increased reliance on rapid POC testing for early outbreak detection and containment. Many EU member states have established community-based surveillance programs for respiratory viruses, often incorporating POC antigen and molecular tests. In France, large number of rapid tests were deployed during the flu season to help differentiate between influenza and SARS-CoV-2, aiming to ease the pressure on emergency departments. This institutionalized demand for decentralized pathogen screening is driving innovation in multiplex POC platforms capable of detecting multiple pathogens simultaneously, opening new commercial and public health pathways.

MARKET CHALLENGES

Variability in Operator Competency Across Non-Laboratory Settings

A persistent challenge in the deployment of POC diagnostics is the inconsistency in test performance due to operator error, particularly in non-specialist environments such as pharmacies, care homes, and home use. Unlike centralized labs staffed by trained technicians, POC testing often relies on healthcare providers with limited diagnostic training. Evaluations in the UK have found that some POC glucose and HbA1c tests in primary care clinics showed deviations beyond acceptable clinical limits, often linked to sample handling or device calibration issues. Studies in Europe suggest that incorrect interpretation of results can contribute to misdiagnoses in cardiovascular risk assessments. This variability undermines test reliability, increases liability risks, and necessitates extensive training programs and built-in quality control mechanisms, complicating scalability.

Supply Chain Vulnerabilities for Critical POC Test Components

The European POC diagnostics sector faces growing exposure to supply chain disruptions, particularly for specialized components such as biosensors, microfluidic chips, and conjugated antibodies. A significant share of raw materials for POC test components is sourced from outside the EU, mainly from the US and Asia, leaving manufacturers exposed to geopolitical and logistical risks. Also, shortages of key materials, which affected POC test production in major markets. Additionally, geopolitical events, such as the war in Ukraine, have disrupted supplies of certain raw materials, including those used in electrochemical sensors. These dependencies compromise production stability and increase costs, forcing companies to reconfigure sourcing strategies and invest in localized manufacturing, a transition that remains in early stages.

SEGMENTAL ANALYSIS

By Product Insights

The glucose monitoring segment dominated the Europe POC diagnostics market by capturing a 32.6% of total revenue in 2024. This preeminence is rooted in the continent’s escalating diabetes burden and the clinical necessity for frequent, real-time glycemic assessment. Millions of adults in Europe are living with diabetes, with many additional cases thought to be undiagnosed, creating strong demand for continuous monitoring. The integration of POC glucose meters into primary care, pharmacies, and home settings has become standard practice, particularly in countries with aging populations such as Germany and Italy. As per the industry groups, a large proportion of type 2 diabetes patients in Western Europe engage in some form of self-monitoring of blood glucose, supporting ongoing demand for test strips and devices. Furthermore, Health programs in the UK have reported that structured glucose testing can help reduce HbA1c levels over time, reinforcing its role in diabetes management.

The infectious diseases segment is the fastest-growing and is projected to expand at a CAGR of 15.4% from 2025 to 2033. This surge is propelled by Europe’s institutionalized focus on rapid pathogen detection in community and emergency settings following the pandemic. Many EU member states have implemented permanent POC testing protocols for respiratory viruses such as influenza, RSV, and SARS-CoV-2. In France, pharmacies administered a large number of rapid antigen tests during the 2023 winter season under government-backed surveillance programs. Additionally, rising antimicrobial resistance has accelerated the adoption of POC molecular assays to guide appropriate antibiotic use. Studies suggest that decentralized testing for infections such as Group A Streptococcus in primary care can help reduce unnecessary antibiotic prescriptions, highlighting its public health value.

By End-User Insights

The Hospitals segment represented the largest end-user in the Europe POC diagnostics market by accounting for an estimated 41.5% of the Europe POC diagnostics market in 2024. Their dominance is because of the integration of rapid testing into emergency departments, intensive care units, and perioperative workflows, where immediate results are critical for clinical decision-making. In major European hospitals, many ICU admissions involve at least one POC test during the initial stages of care, such as blood gas analysis, lactate, or cardiac markers. POC INR testing for anticoagulant management has been shown to help reduce patient wait times in certain hospital settings. Additionally, hospital-affiliated maternity units widely use POC hCG and urinalysis devices for rapid triage. With centralized procurement systems and stringent quality control mandates, hospitals remain the primary adopters of high-complexity POC platforms, ensuring their continued market leadership despite the rise of decentralized care models.

The home healthcare segment is the fastest-growing and is expected to grow at a CAGR of 13.7% through 2033. This acceleration is driven by patient empowerment, aging populations, and national policies promoting self-management of chronic conditions. Many Europeans aged 65 and above live with multiple chronic diseases, creating sustained demand for at-home diagnostic tools. In the UK, there has been a notable increase in the use of home-based POC glucose and INR testing, supported by telemonitoring programs for chronic conditions. Also, chronically ill patients prefer managing their conditions at home with digital diagnostics, a shift reinforced by easier-to-use devices and integration with mobile health applications.

REGIONAL ANALYSIS

Germany held the largest share of the European POC diagnostics market at 21.3% in 2024. As Europe’s largest economy and a leader in medical technology innovation, Germany sets the pace for regulatory compliance, clinical integration, and technological adoption. The country’s statutory health insurance system covers a wide range of POC tests, including HbA1c, INR, and cardiac markers, when administered in certified medical facilities. Health agency data indicate that millions of POC glucose tests were reimbursed in outpatient settings, reflecting substantial outpatient testing activity. Regulators such as BfArM have taken measures to facilitate the transition to IVDR-compliant POC devices, supporting market continuity. Moreover, the country hosts key manufacturers such as Roche Diagnostics and Siemens Healthineers, reinforcing its role as both a consumer and innovator in the POC landscape.

France is distinguished by its hybrid public-private healthcare model and proactive public health initiatives. The French government has integrated POC testing into national disease management programs, particularly for diabetes and infectious diseases. Primary care clinics performed a substantial number of POC HbA1c tests, supporting earlier intervention efforts. The country’s pharmacy-based healthcare model allows pharmacists to administer certain rapid tests, including influenza and strep A. During the 2022–2023 flu season, pharmacies administered a large number of rapid antigen tests, which helped ease pressure on hospital services. Additionally, the "Ma Santé 2022" strategy promotes digital health integration, enabling POC results to be uploaded directly into the national health data platform, enhancing care coordination and driving market growth.

The United Kingdom is characterized by a centralized healthcare system that has strategically embraced POC diagnostics to improve efficiency and reduce hospital burden. The NHS Long Term Plan prioritizes decentralized testing, particularly in primary and community care. Public Health England reported substantial use of POC CRP testing in general practices to reduce antibiotic misuse, with evaluations suggesting meaningful reductions in related prescriptions. The NHS launched a diabetes prevention program that incorporated POC HbA1c screening in community settings and reached a large number of high-risk individuals. Furthermore, the UK leads in digital POC integration, with platforms like the NHS App enabling patients to log glucose and INR results from home devices, fostering continuous monitoring and personalized care pathways.

Italy is shaped by regional disparities in healthcare access and a growing emphasis on chronic disease management. With one of Europe’s oldest populations, demand for POC diagnostics in diabetes, cardiology, and geriatric care is intensifying. Medical societies report that millions in Italy live with diabetes, and a substantial share use home glucose monitoring with regional support. In 2023, policy changes expanded reimbursement for POC HbA1c testing in primary care, which was followed by a reported increase in test volumes. Southern regions, where specialist access is limited, increasingly depend on mobile clinics equipped with POC analyzers for early detection of cardiovascular risks. Additionally, the adoption of POC troponin testing in emergency departments has reduced time-to-diagnosis for acute coronary syndrome.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

A few of the notable companies operating in the European point-of-care (POC) diagnostics/testing market profiled in this report are Abbott Laboratories, Inc., Danaher Corporation, Roche Diagnostics Limited, BioMerieux, Siemens Healthcare, Beckman Coulter, Inc., Becton, Dickinson and Company, Johnson & Johnson, Alere Inc., and PTS Diagnostics.

The competition in the Europe Point-of-Care (POC) Diagnostics Market is characterized by technological differentiation, regulatory agility, and strategic alignment with national healthcare priorities. Established multinational corporations compete with agile medtech innovators to capture hospital, clinic, and home-based segments. The shift toward digital health and real-time data integration has intensified rivalry, with companies investing in cloud-connected devices and interoperability standards. IVDR compliance has emerged as a critical differentiator, separating well-resourced global players from smaller firms facing certification delays. Private-label and regional manufacturers are gaining traction in pharmacy and retail channels, pressuring premium brands to demonstrate added clinical value. Additionally, sustainability commitments and ethical sourcing are becoming competitive levers, particularly in Northern Europe. The convergence of clinical accuracy, user experience, and system integration defines the evolving competitive landscape.

Top Players in the Europe Point-of-Care (POC) Diagnostics Market

Roche Diagnostics

Roche Diagnostics is a dominant force in the European POC diagnostics landscape, renowned for its high-precision, lab-comparable testing platforms deployed across hospitals and primary care networks. The company’s cobas® Liat system, a fully automated molecular POC platform, is widely used for rapid detection of respiratory pathogens, including influenza and SARS-CoV-2, delivering results in under 20 minutes. In recent years, Roche has intensified its integration with national health systems, collaborating with public health agencies in Germany and the UK to expand decentralized infectious disease surveillance. In 2023, Roche launched an enhanced POC troponin assay on its cobas h232 platform, enabling early rule-out of myocardial infarction in emergency departments. The company has also strengthened its IVDR compliance portfolio, ensuring uninterrupted market access. By investing in connectivity solutions that link test results to electronic health records in Sweden and the Netherlands, Roche continues to set benchmarks for reliability and digital interoperability.

Abbott Laboratories

Abbott has established a robust presence in the Europe POC diagnostics market through its diverse portfolio of rapid, user-friendly testing solutions for cardiac markers, glucose, and infectious diseases. Its i-STAT1 handheld blood analyzer is extensively utilized in critical care and ambulatory settings across France, Italy, and Scandinavia, providing real-time blood gas, electrolyte, and cardiac biomarker results. In 2023, Abbott introduced the Panbio™ COVID-19/Flu A&B Ag Nasal Test, a multiplex rapid antigen assay adopted by national programs in Spain and Germany for winter respiratory surveillance. The company has also deepened its partnership with pharmacies in the UK and Belgium to expand access to its POC infectious disease kits. Abbott’s focus on microfluidics and AI-driven analytics has led to the development of next-generation platforms with improved sensitivity. Its proactive engagement with EU regulatory bodies ensures swift certification under IVDR, reinforcing its operational agility.

Siemens Healthineers

Siemens Healthineers plays a pivotal role in advancing POC diagnostics in Europe through its Atellica® and Dimension® Vista systems, which deliver rapid, semi-quantitative results in decentralized clinical environments. The company has strategically focused on integrating its POC solutions into hospital emergency departments and mobile care units, particularly in Germany and Austria, where demand for immediate cardiac and renal marker testing is high. In 2023, Siemens launched the Atellica VTLi, a compact immunoassay analyzer designed for near-patient testing of troponin, procalcitonin, and BNP, reducing turnaround time by up to 50% compared to central lab processing. The company has also enhanced its digital ecosystem by linking POC devices to its syngo.via platform, enabling seamless data flow into hospital information systems. With strong R&D investments in automation and AI-based quality control, Siemens is positioning itself at the forefront of smart, scalable POC diagnostics across the region.

Top Strategies Used by the Key Market Participants

Key players in the Europe Point-of-Care (POC) Diagnostics Market are deploying a multifaceted strategic approach to consolidate their position, including technological innovation, regulatory preparedness, digital integration, strategic partnerships, and geographic expansion. Companies are prioritizing the development of multiplex, rapid, and connected diagnostic platforms to meet evolving clinical demands. Collaborations with national health systems and telehealth providers are enhancing care pathway integration. Firms are also accelerating IVDR compliance to maintain market access amid tightening EU regulations. Expansion into underserved regions and investment in sustainable manufacturing are further differentiating market leaders. Direct-to-consumer models and AI-driven analytics are being leveraged to improve diagnostic accuracy and user engagement, ensuring competitive advantage in a rapidly transforming healthcare ecosystem.

RECENT MARKET DEVELOPMENTS

- In February 2023, Roche Diagnostics launched the cobas® Liat SARS-CoV-2 & Flu A/B assay across Germany and France, enabling healthcare providers to differentiate between viral infections within 20 minutes, supporting public health efforts to optimize treatment and reduce hospital burden during seasonal outbreaks.

- In May 2023, Abbott Laboratories received IVDR certification for its i-STAT Alinity system, ensuring continued availability in EU markets and reinforcing its position as a trusted provider of blood gas and cardiac marker testing in emergency and critical care settings across Southern and Central Europe.

- In October 2023, Siemens Healthineers partnered with the Swedish National Healthcare Registry to integrate Atellica VTLi test results into the country’s digital health infrastructure, enabling automatic data transfer to patient records and improving clinical decision-making speed in primary and emergency care.

- In January 2024, Roche expanded its POC infectious disease portfolio by introducing the Panbio™ RSV Ag test for use in pediatric clinics and general practices in the UK and Netherlands, addressing rising demand for rapid respiratory diagnostics in community settings.

- In August 2023, Abbott launched a telehealth-integrated glucose monitoring program in collaboration with Spain’s Top Doctors platform, allowing patients to share POC glucose readings directly with endocrinologists, enhancing chronic disease management and strengthening consumer engagement.

MARKET SEGMENTATION

This research report on the European point-of-care (POC) diagnostics market has been segmented and sub-segmented into the following categories.

By Product

- Glucose Monitoring

- Infectious Diseases

- Others

By End-User

- Clinics

- Hospitals

- Home Healthcare

- Ambulatory Care Settings

- Laboratories

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What was the size of the POC diagnostics market in Europe in 2023?

The Europe POC diagnostics market was valued at USD 8.39 billion in 2023.

Which year is considered as the base year for this research report?

2023 is the base year is developing this market research report.

Which country led the Europe POC diagnostics market in 2023?

The UK had the leading share of the European market in 2023.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com