Europe Procedure Trays Market Size, Share, Trends & Growth Forecast Report By Product, Application and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, From (2026 to 2034)

Market Size, 2025

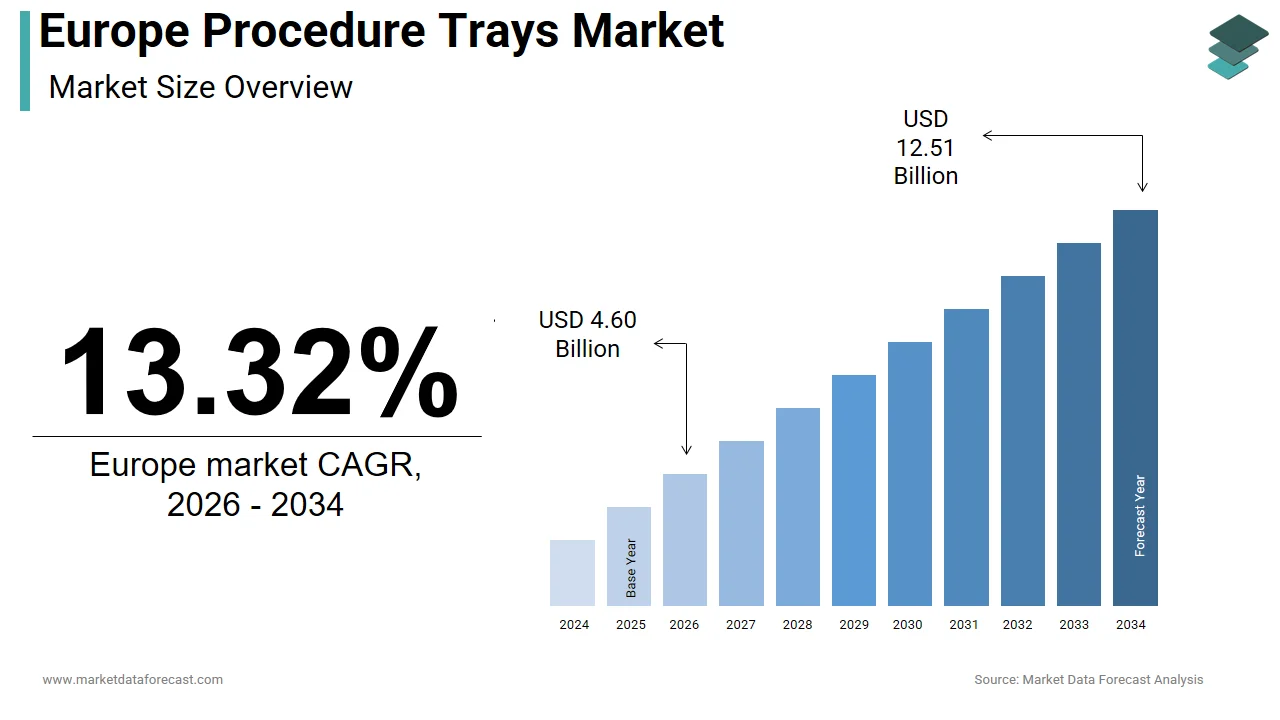

$4.06 BnMarket Estimate, 2026

$4.60 BnMarket Forecast, 2034

$12.51 BnCAGR, 2026–2034

13.32%Europe Procedure Trays Market Report Summary

The Europe procedure trays market was valued at USD 4.06 billion in 2025, is estimated to reach USD 4.60 billion in 2026, and is projected to reach USD 12.51 billion by 2034, growing at a CAGR of 13.32% from 2026 to 2034. Market expansion is driven by rising volumes of minimally invasive and outpatient surgeries, stringent EU Medical Device Regulation (MDR) requirements boosting traceability and standardized kits, and hospitals’ focus on infection prevention and operational efficiency. Increasing ambulatory care, digital integration (UDI/RFID), and demand for ready-to-use sterile systems position procedure trays as clinical quality enablers across Europe’s regulated healthcare ecosystem.

Key Market Trends

- Shift toward minimally invasive and outpatient procedures, increasing demand for standardized, single-use trays.

- Full enforcement of EU MDR and UDI traceability is driving consolidation toward compliant, certified suppliers.

- Growing adoption of smart trays (RFID/QR/UDI) integrated with hospital ERPs and EHRs for inventory and quality control.

- Expansion of ambulatory surgical centers as high-growth end users requiring compact, single-use kits.

- Rising sustainability and circular-economy pressures are prompting eco-design and mono-material tray innovations.

Segmental Insights

- Based on product, the operating room procedure trays segment dominated the Europe market in 2024, holding 40.8% share. Its leadership is driven by high inpatient surgical volumes, alignment with surgical safety bundles, and MDR-driven traceability requirements that favor integrated OR tray systems.

- Based on application, the hospitals segment dominated with a 65.9% share in 2024, reflecting hospitals’ role in complex, high-acuity surgeries and centralized procurement programs.

Regional Insights

The Europe procedure trays market is expanding across major markets, shaped by national procurement models, hospital consolidation, and differing sustainability mandates that favor compliant, traceable tray suppliers.

- Germany was the market leader with a 22.5% share in 2024, supported by large hospital volumes, centralized purchasing groups, MDR compliance focus, and “Digital Now” automation grants that accelerated single-use tray adoption.

- United Kingdom captured a prominent share in 2024, backed by NHS modernization programs, digital inventory investments, and sustained procedural demand despite post-Brexit supply adjustments.

- France is set to register a prominent CAGR driven by centralized clinical pathway enforcement (HAS), national tenders prioritizing UDI-compliant suppliers, and rapid ambulatory surgery expansion.

Competitive Landscape

The Europe procedure trays market is competitive and consolidating under MDR pressure, with multinational medical device firms and specialized kit assemblers competing on regulatory expertise, traceability, supply resilience, and clinical partnership. Success hinges on demonstrable compliance (MDR/UDI), digital integration (RFID/ERP/EHR), sustainable packaging solutions, and robust pan-European logistics. Larger players leverage scale and regulatory resources, while agile entrants win niche ASC and specialty procedure opportunities through customization and rapid validation. Key market players include: Baxter International; Boston Scientific Corp.; B. Braun SE; Cardinal Health; CareFusion Corp.; Covidien AG; C.R. Bard Inc.; Ecolab Inc.; Hogy Medical Co., Ltd.; Hartmann Group; Medical Action Industries Inc.; Medline Industries Inc.; Precise-Pak Inc.; Smith & Nephew Plc; Teleflex Medical.

Europe Procedure Trays Market Size

The size of the Europe procedure trays market was valued at USD 4.06 billion in 2025. This market is expected to grow at a CAGR of 13.32% from 2026 to 2034 and be worth USD 12.51 billion by 2034 from USD 4.60 billion in 2026.

Procedure trays are pre-assembled, single-use or reusable sterile kits containing surgical instruments, drapes, gauzes, and disposables tailored for specific medical interventions ranging from minor biopsies to complex orthopedic procedures. These trays streamline operating room efficiency, reduce contamination risk, and standardize care protocols across healthcare settings. The market operates within Europe’s highly regulated medical device ecosystem, governed by the EU Medical Device Regulation 2017 745, which mandates rigorous conformity assessments, traceability via Unique Device Identification, and post-market surveillance. According to Eurostat, Europe performs more than 23 million inpatient surgical procedures annually, with outpatient interventions steadily increasing due to advances in minimally invasive techniques. As per the European Centre for Disease Prevention and Control, healthcare‑associated infections affect approximately 8.9 million patients each year in the EU, which is reinforcing the demand for sterile, closed‑system tray solutions. According to the European Commission, over 90% of acute care hospitals in Western Europe have adopted standardized procedure trays as part of surgical bundle protocols to enhance patient safety and operational predictability. These clinical, regulatory, and epidemiological forces position procedure trays not as commoditized supplies but as integral components of Europe’s surgical quality and infection control infrastructure.

MARKET DRIVERS

Rising Volume of Minimally Invasive and Outpatient Surgeries Drives Tray Standardization

The shift toward ambulatory and minimally invasive procedures has intensified demand for procedure trays that ensure efficiency, sterility and protocol adherence in time constrained settings, which is one of the key factors propelling the European procedure trays market growth. According to the Organisation for Economic Co‑operation and Development, outpatient surgeries now account for more than two‑thirds of all surgical interventions in high‑income European countries, up from just over half in 2015. These procedures require precise instrument sets with minimal waste, which is making pre‑configured trays indispensable. As per Germany’s Federal Joint Committee, same‑day surgical admissions have risen significantly in recent years and is directly correlating with tray utilization in endoscopy and minor operating rooms. In France, the National Authority for Health mandates standardized tray use in over 40 ambulatory procedure bundles to reduce variability and enhance infection control. According to the Karolinska Institute, pre‑packed sets reduce operating room preparation time by approximately 18 minutes per case, which enables 2–3 additional daily procedures per theatre. This operational leverage, combined with regulatory pressure for standardization, cements procedure trays as essential enablers of Europe’s surgical modernization.

Stringent EU Medical Device Regulation Increases Compliance and Traceability Requirements

The full enforcement of the EU Medical Device Regulation since May 2021 has fundamentally reshaped procedure tray design, documentation and supply chain management, which is further boosting the European procedure trays market expansion. Under this framework, every component in a tray is classified as a medical device requiring individual conformity assessment and integration into a unified technical file. According to the European Commission, the implementation of the Medical Device Regulation (MDR) between 2021 and 2023 required thousands of medical devices, including procedure trays, to undergo re‑certification under new clinical evaluation and risk management standards. Additionally, Regulation (EU) 2017/745 mandates Unique Device Identification (UDI) for Class I reusable and Class IIa single‑use medical devices, which is ensuring full traceability from manufacturer to patient. As per the Swedish Medical Products Agency, hospitals are preparing for mandatory UDI registration in the EUDAMED database with voluntary adoption already underway to strengthen digital tracking and serialized packaging systems. These requirements significantly raise barriers to entry, favouring established players with regulatory expertise while increasing compliance costs for smaller assemblers. Consequently, the market is consolidating around vendors who can navigate this complexity, which is transforming compliance from a cost center into a competitive differentiator in Europe’s safety‑first healthcare environment.

MARKET RESTRAINTS

Fragmented Reimbursement and Procurement Policies Across EU Member States

Despite regulatory harmonization under the Medical Device Regulation, hospital procurement and reimbursement for procedure trays remain highly decentralized, which is creating market access inefficiencies and impeding the regional market expansion. In Germany, centralized group purchasing organizations like GHK negotiate national contracts, whereas in Italy, individual regions set their own tender criteria, often prioritizing price over quality. According to the European Observatory on Health Systems and Policies, fragmentation across national procurement systems forces manufacturers to maintain multiple tray configurations for the same clinical procedure to satisfy local formularies. In Spain, the Catalan health service has introduced sustainability requirements such as biodegradable tray components, while Bavaria emphasizes reusable stainless-steel instruments, as these requirements are often mutually exclusive. As per the European Association of Hospital Procurement Services, adapting a single tray SKU for cross‑border use can add significant validation and documentation costs, often exceeding tens of thousands of euros. These inconsistencies delay market entry, inflate inventory complexity and discourage innovation, particularly for specialized trays used in rare procedures. Until the EU advances procurement harmonization through joint clinical assessment or common tendering frameworks, the procedure tray market will remain constrained by national silos that undermine economies of scale and clinical standardization.

Shortage of Skilled Sterile Processing Personnel Impairs Reusable Tray Viability

Europe’s acute deficit of sterile processing department staff is eroding the economic and operational case for reusable procedure trays, despite their environmental appeal, which is further hindering the procedure trays market expansion in Europe. According to the European Sterile Supply Association, there is a significant shortage of sterile processing technicians across the EU with staffing gaps particularly acute in countries such as Italy and the UK. This shortage leads to processing delays, instrument damage from improper handling and increased risk of residual contamination. As per the Irish Health Service Executive, audits have highlighted recurring sterility validation failures in reusable surgical trays, often linked to human error in decontamination cycles. Consequently, hospitals are shifting to single‑use trays to ensure reliability. According to the Netherlands’ National Institute for Public Health and the Environment (RIVM), Dutch hospitals have reported increased procurement of disposable trays in recent years to mitigate staffing‑related risks. While reusable trays have lower per‑unit costs over time, their value proposition collapses without trained personnel to manage cleaning, inspection, and reassembly. This human capital crisis accelerates the disposables shift, which is challenging sustainability goals and increasing clinical waste volumes across European healthcare systems.

MARKET OPPORTUNITIES

Integration of Smart Trays with Hospital Digital Ecosystems

Emerging smart procedure trays embedded with RFID or QR codes are unlocking new opportunities for the European procedure trays market. These digitally enabled trays automatically log usage into hospital enterprise resource planning systems, eliminating manual counting and reducing stockouts. According to Rigshospitalet in Copenhagen, Denmark’s largest hospital, an RFID surgical instrument tracking pilot saved an estimated 31,000 hours annually in operating room procedures, while also improving patient safety and sterile processing efficiency. In Sweden, Karolinska University Hospital has implemented advanced digital integration platforms such as Tietoevry Care’s Lifecare Open Platform to link surgical workflows with electronic health records, which is enabling smarter data capture and quality auditingTietoevry. As per the European Commission’s Digital Health and Care strategy, interoperability and the European Health Data Space (EHDS) are central to supporting value‑based healthcare and cross‑border data exchange. Furthermore, real‑time data from smart trays informs predictive analytics for demand forecasting, which is enabling just‑in‑time manufacturing. With UDI compliance already requiring digital identifiers, the incremental cost of adding inventory intelligence is marginal and making smart trays a low‑friction path to operational excellence and data‑driven clinical management across Europe’s digitizing healthcare infrastructure.

Expansion of Procedure Trays into Ambulatory and Point of Care Settings

The decentralization of care delivery is creating high growth opportunities for compact, self-contained procedure trays tailored for non-hospital environments such as outpatient clinics, home health and mobile diagnostic units, which is another promising opportunity for the European procedure trays market. According to the European Observatory on Health Systems and Policies, ambulatory surgical centers have expanded rapidly across the EU in recent years, each requiring standardized, space‑efficient tray systems. In Germany, the Federal Ministry of Health has introduced reimbursement for selected outpatient procedures such as wound care and dialysis access, which is driving demand for single‑patient use trays with integrated biohazard containment. Similarly, France’s “Ma Santé 2022” strategy promotes point‑of‑care diagnostics and spurring adoption of trays for skin biopsies and joint aspirations in general practitioner offices. These settings lack centralized sterile processing, making single‑use, ready‑to‑deploy trays essential. As per the European Wound Management Association, community nursing services across Europe have reported increased use of pre‑packed wound care trays citing reduced preparation time and lower infection risk. As care migrates closer to patients, procedure trays evolve from operating room tools to enablers of safe, standardized care across the entire continuum and unlocking new markets beyond traditional hospital walls.

MARKET CHALLENGES

Environmental Regulations and Medical Waste Management Pressures

The European Union’s Circular Economy Action Plan and national medical waste directives are intensifying scrutiny on the environmental footprint of single-use procedure trays, which is a notable challenge to the European procedure trays market growth. According to the European Environment Agency, healthcare facilities in the EU generate more than 2.6 million tonnes of medical waste annually with disposable trays contributing significantly to non‑recyclable plastic streams. France’s AGEC Law requires hospitals to report surgical waste volumes and set reduction targets, which is prompting procurement shifts toward reusable or recyclable alternatives. For instance, only a minority of single‑use trays are made from mono‑material plastics compatible with existing recycling streams, while most combine polymers, foils and absorbents that render them non‑recyclable. Incineration remains the default disposal method, releasing CO₂ and potentially toxic emissions. Without standardized eco‑design rules or hospital‑level recycling infrastructure, sustainability efforts remain fragmented. This regulatory and technical gap forces providers into a dilemma and posing a systemic challenge to both environmental and clinical safety objectives.

Supply Chain Volatility and Single Source Dependencies

The Europe procedure trays market faces persistent exposure to upstream supply disruptions due to concentrated manufacturing of critical components and geopolitical dependencies. According to the European Medical Device Manufacturers Association, a significant share of non‑woven sterilization wrap used in EU trays is sourced from Asian producers, which is creating dependency on external supply chains. The 2022 Rhine River drought disrupted inland barge transport, delaying raw material deliveries and halting tray production at several European assemblers. Simultaneously, post‑Brexit customs checks added delays to UK‑bound shipments and triggered buffer stock inflation. The war in Ukraine further exposed vulnerabilities. Poland’s medical device sector reported disruptions in polypropylene supply, which is a key resin for tray thermoforming. Unlike pharmaceuticals, procedure trays lack strategic stockpiling mandates, leaving hospitals vulnerable to just‑in‑time failures. As per the European Hospital Association, many facilities across Europe reported tray shortages in the past year, leading to procedure cancellations or substitution with non‑standardized kits. Until supply chains diversify and regional sourcing incentives emerge, the market will remain exposed to external shocks that compromise surgical continuity and patient care.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Baxter International, Boston Scientific Corp., B. Braun SE, Cardinal Health, CareFusion Corp., Covidien AG, C.R. Bard Inc., Ecolab Inc., Hogy Medical Co., Ltd., Hartmann Group, Medical Action Industries Inc., Medline Industries Inc. Precise-Pak Inc., Smith & Nephew Plc, Teleflex Medical. |

SEGMENTAL ANALYSIS

By Product Insights

The operating room procedure trays segment dominated the market by holding 40.8% of the European market share in 2024. The dominance of the operating room procedure trays segment in the European market is driven by their essential role in standardizing complex surgical workflows across Europe’s high volume acute care infrastructure. Every major surgical intervention requires a meticulously curated set of instruments, drapes and disposables delivered in a sterile, ready to use format. According to the EU‑funded SAFEST project, surgical safety bundles are being promoted across Europe to standardize perioperative practices and reduce complications with the initiative aiming to improve adherence to evidence‑based protocols by 15% and lower surgical errors. In Germany, the Federal Joint Committee has documented widespread use of pre‑packed OR trays in inpatient surgeries, which is indicating efficiency gains such as reduced setup time and fewer intraoperative delays. As per the EU Medical Device Regulation, traceability requirements favour integrated tray systems where every component is documented under a single Unique Device Identifier, which is simplifying compliance. According to Eurostat, millions of major inpatient procedures are performed annually in Western Europe, which is indicating the operating room as the undisputed core of procedural care and anchoring this segment’s market leadership through clinical necessity and regulatory alignment.

The ophthalmic procedure trays segment is the fastest growing product segment and is projected to expand at a CAGR of 10.2% over the forecast period owing to the Europe’s aging population and the rising prevalence of age-related eye conditions requiring minimally invasive interventions. According to Eurostat, 21.3% of the EU population was aged 65 or older in 2023 and this share is projected to rise to nearly 30% by 2050, which is directly driving demand for cataract and retinal procedures. As per the European Society of Cataract and Refractive Surgeons, more than 4.3 million cataract surgeries are performed annually across Europe with the majority conducted in outpatient settings using standardized single‑use trays. In Sweden, the National Board of Health and Welfare has reported steady growth in ophthalmic procedures, supported by streamlined protocols for same‑day surgery that increase tray utilization. These trays are highly specialized, which is making them indispensable for precision and sterility in high‑volume, low‑risk environments. As ophthalmology leads Europe’s shift toward ambulatory care, its tray segment grows in tandem with demographic and procedural trends.

By Application Insights

The hospitals segment dominated the market and held 65.9% of the European market share in 2024. The growth of the hospitals segment in the European market is attributed to their role as the primary site for complex, high acuity surgeries requiring extensive sterile instrumentation. Europe’s network of more than 6,000 acute care hospitals performs the vast majority of inpatient and emergency procedures, each dependent on standardized tray systems to maintain operating room efficiency and infection control. The European Centre for Disease Prevention and Control (ECDC) promotes surgical safety bundles across hospitals, which include pre‑configured trays as a core component to reduce variability and healthcare‑associated infections. In France, the Haute Autorité de Santé (HAS) has issued national guidance requiring standardized procedure trays in defined surgical pathways, covering areas such as cardiac catheterization and orthopedic implants. In Germany, hospital procurement groups negotiate centralized tray contracts that standardize usage across hundreds of facilities, ensuring volume consistency and cost control. According to OECD Health Statistics, large European hospitals routinely perform tens of thousands of surgeries annually. For example, Germany alone reported over 7 million inpatient surgical procedures in 2022, which is making hospitals the structural and financial backbone of the European procedure trays ecosystem.

The ambulatory surgical centers segment is predicted to showcase a promising CAGR of 11.4% over the forecast period owing to the Europe’s systemic shift toward outpatient care to reduce costs, improve patient convenience and alleviate hospital congestion. According to the OECD Health Statistics, outpatient procedures now account for over two‑thirds of all surgical interventions in high‑income EU countries, reflecting a steady rise from just over half a decade ago. Ambulatory centers rely on compact, single‑use trays that eliminate the need for on‑site sterile processing, a capability most lack. In the Netherlands, the National Institute for Public Health and the Environment (RIVM) has reported strong growth in ambulatory surgical centers, which is driven by national policies to expand same‑day surgery capacity. Spain’s Ministry of Health allocated €466 million in 2023 to strengthen outpatient and day‑surgery networks, directly boosting tray demand. These centers prioritize speed, sterility, and minimal storage footprint, which is a criteria perfectly met by pre‑packed and procedure‑specific trays. As healthcare systems incentivize care decentralization, ASCs emerge as the highest‑growth frontier for tailored, efficient tray solutions.

COUNTRY-LEVEL ANALYSIS

Germany Procedure Trays Market Analysis

Germany was the top performer in the European procedure trays market in 2024 and held 22.5% of the regional market share. The extensive hospital network, stringent quality protocols, and centralized procurement systems are primarily driving the dominance of Germany in the European procedure trays market. According to the Federal Statistical Office of Germany (Destatis), the country performs millions of inpatient and outpatient procedures annually, which is creating immense demand for standardized sterile solutions. Germany’s Federal Joint Committee (G‑BA) enforces national surgical quality and safety guidelines, which include bundled protocols that encourage the use of certified procedure trays for common interventions to ensure consistent adoption. Additionally, group purchasing organizations such as GHK negotiate unified contracts across hundreds of hospitals, which is favoring vendors who demonstrate full regulatory compliance under the EU Medical Device Regulation (MDR). The German Hospital Association (DKG) has repeatedly highlighted staffing shortages in sterile processing and nursing, which further accelerate the shift toward single‑use trays to ensure reliability and reduce reprocessing risks. This ecosystem of regulatory rigor, operational scale and workforce constraints positions Germany as one of Europe’s most systematic and volume‑driven procedure tray markets.

United Kingdom Procedure Trays Market Analysis

The UK captured a prominent share of the European procedure trays market in 2024. The growth of the UK in the European market is driven by its mature healthcare system navigating post-Brexit regulatory divergence while maintaining high clinical standards. The UK’s MHRA enforces a regulatory framework closely aligned with the EU MDR through the UKCA marking system, which is requiring full traceability and clinical evaluation for all procedure trays. Despite customs delays post‑Brexit, the NHS has worked to standardize tray usage across its 930 hospitals to reduce variation and infection risk. In 2023, the Department of Health and Social Care announced new funding streams to modernize operating room logistics, including investments in digital inventory tracking and hospital infrastructure upgrades. This commitment to operational excellence, combined with demographic pressure from an aging population, sustains the UK’s position as a stable and evolving high‑demand market for standardized surgical tray solutions.

France Procedure Trays Market Analysis

France is anticipated to register a prominent CAGR in the European procedure trays market over the forecast period owing to its highly centralized public healthcare system and national clinical pathway enforcement. France’s Ministry of Solidarity and Health has promoted standardized surgical pathways through initiatives such as “Ma Santé 2022” and the broader Parcours de Soins framework, which encourage consistent use of procedure trays to reduce variability and infection risk. The Haute Autorité de Santé (HAS) has issued national guidance on surgical safety bundles and French hospitals report measurable reductions in surgical site infections when standardized tray protocols are implemented. France’s centralized procurement agency, UGAP, runs national tenders that prioritize vendors offering full UDI compliance and environmental certifications, in line with the AGEC anti‑waste law. The country also leads in ophthalmic and endoscopic outpatient care. According to the French Ministry of Health, ambulatory surgery now accounts for more than 50% of procedures nationally, which is supported by a growing network of day‑surgery centers.

Italy Procedure Trays Market Analysis

Italy is projected to hold a notable share of the European procedure trays market during the forecast period. The high surgical volumes despite fragmented regional procurement is primarily contributing to the market growth in Italy. According to ISTAT (Italian National Institute of Statistics), Italy performs millions of inpatient procedures annually with cataract, orthopedic and cardiovascular surgeries among the leading categories of demand. However, each of Italy’s 21 autonomous regions manages its own hospital tenders, which is resulting in inconsistent tray specifications and pricing and is a persistent challenge for suppliers. The National Health Service has sought to harmonize standards through reforms such as the “Piani di Rientro” (Recovery Plans) that aim to improve efficiency and reduce regional disparities, including adoption of surgical bundles in selected hospitals by 2025. At the same time, Italy faces a well‑documented healthcare workforce shortage: the Italian Society of Hospital Hygiene (SItI) and the Italian Hospital Association (AIOP) have highlighted critical gaps in sterile processing and nursing staff, which push facilities toward single‑use solutions to ensure reliability. Demographically, Italy is one of the oldest societies in Europe, which is ensuring sustained procedural demand. This combination of bureaucratic complexity, workforce constraints and demographic pressure makes Italy a high‑potential yet operationally challenging market requiring localized engagement.

Spain Procedure Trays Market Analysis

Spain is anticipated to account for a noteworthy share of the European procedure trays market over the forecast period. Spain is emerging as Europe’s leader in ambulatory surgical adoption and decentralized care innovation. The Ministry of Health’s “Plan de Cirugía Mayor Ambulatoria” aims to shift 80% of eligible procedures to outpatient settings by 2026, which is directly fueling demand for compact, single-use trays. According to Spain’s Ministry of Health, ambulatory surgical care has expanded rapidly with day‑surgery now accounting for more than 55% of all surgical procedures nationally. This growth has been supported by new ambulatory surgical centers (ASCs), which rely heavily on compact, single‑use trays to eliminate the need for on‑site sterile processing. Public hospitals also use standardized trays, but the growth engine is clearly in the community. The Catalan and Andalusian health services have pioneered digital tray tracking linked to electronic health records, improving inventory accuracy and reducing waste. Spain’s AGEC law and national efficiency programmes further encourage adoption of environmentally certified and traceable tray systems. With strong government backing, demographic pressure and a focus on efficiency, Spain represents the future trajectory of European surgical care and the procedure trays that enable it.

COMPETITIVE LANDSCAPE

The Europe procedure trays market is characterized by intense competition among multinational medical device firms, specialized sterile kit assemblers and regional manufacturers, all operating under the stringent oversight of the EU Medical Device Regulation. Competition is not driven by price alone but by demonstrable compliance, clinical relevance, supply chain resilience and environmental credentials. Large players like B. Braun and Medline leverage scale, regulatory expertise and pan European logistics, while niche vendors compete through surgical specialty focus or sustainable innovation. The market is consolidating as smaller assemblers struggle with the cost of MDR certification and UDI implementation. Hospitals increasingly favor vendors who offer digital integration, standardized configurations and robust post market surveillance. At the same time, the rise of ambulatory care is creating demand for compact, flexible tray systems, opening opportunities for agile entrants. In this high stakes environment, trust, traceability and clinical partnership are the true differentiators, making regulatory adherence a prerequisite rather than a competitive advantage.

KEY MARKET PLAYERS

The leading companies operating in the Europe application lifecycle management market include:

- Baxter International

- Boston Scientific Corp.

- Braun SE

- Cardinal Health

- CareFusion Corp.

- Covidien AG

- R. Bard Inc.

- Ecolab Inc.

- Hogy Medical Co., Ltd.

- Hartmann Group

- Medical Action Industries Inc.

- Medline Industries Inc.

- Precise-Pak Inc.

- Smith & Nephew Plc

- Teleflex Medical

TOP PLAYERS IN THE MARKET

- Braun SE is a German multinational that plays a pivotal role in the Europe procedure trays market through its comprehensive portfolio of sterile, single use surgical kits tailored for specialties ranging from vascular access to orthopedics. The company contributes globally by setting benchmarks in quality management and regulatory compliance under the EU Medical Device Regulation. In Europe, B. Braun leverages its integrated manufacturing and logistics network to supply standardized trays to over 1 500 hospitals across the continent. In 2024, the company expanded its smart tray initiative by embedding QR codes linked to digital inventory systems, enabling real time usage tracking and automated reordering for hospital clients. It also launched a new line of eco conscious trays using mono material packaging compatible with hospital recycling streams. These innovations reinforce B. Braun’s commitment to clinical efficiency, sustainability and digital integration in Europe’s evolving surgical landscape.

- Medline Industries LP is a US based global leader with a strong and growing presence in the Europe procedure trays market, offering over 300 procedure specific tray configurations compliant with EU MDR requirements. The company differentiates itself through deep clinical collaboration, co designing trays with European surgeons to meet regional procedural nuances. In Europe, Medline has established dedicated distribution centers in the Netherlands and Poland to ensure rapid delivery and reduce supply chain risk. In 2023, it introduced a modular tray system for ambulatory surgical centers that allows customizable instrument selection within a pre validated sterile format, addressing the need for flexibility in outpatient settings. Medline also enhanced its traceability platform to align with national Unique Device Identification mandates in Germany and France. These localized, responsive strategies position Medline as a trusted partner for both large hospitals and emerging care settings across Europe.

- Hartmann Group is a German healthcare company renowned for its Paul Hartmann branded procedure trays, which emphasize infection prevention, sustainability and ergonomic design. The company contributes to the global market by pioneering biodegradable and recyclable tray components without compromising sterility or performance. In Europe, Hartmann supplies standardized surgical kits to public hospitals under national framework agreements in Germany, Austria and Scandinavia. In 2024, the company launched its “GreenTray” initiative, featuring trays made from 100% recycled polypropylene and FSC certified paper, certified under the EU Ecolabel scheme. It also integrated digital batch tracking via cloud-based portals, giving hospitals full transparency from production to point of use. By aligning clinical excellence with environmental responsibility, Hartmann strengthens its reputation as a values driven leader in Europe’s safety and sustainability focused healthcare procurement environment.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe procedure trays market are investing in digital traceability solutions such as QR codes and cloud based portals to comply with Unique Device Identification mandates and enhance hospital inventory management. They are developing eco conscious tray designs using mono material plastics and recycled content to meet EU circular economy and national waste reduction requirements. Companies are establishing regional distribution hubs within Europe to mitigate supply chain disruptions and ensure just in time delivery to hospitals and ambulatory centers. Strategic collaboration with clinicians and procurement groups enables the co-creation of procedure-specific trays that align with national surgical bundles and clinical pathways. Additionally, firms are expanding modular and customizable tray systems for outpatient settings to address the growing demand for flexible yet standardized solutions in ambulatory surgical centers.

MARKET SEGMENTATION

This Europe procedure trays market research report is segmented and sub-segmented into the following categories.

By Product

- Angiography Procedure Tray

- Ophthalmic Procedure Tray

- Operating Room Procedure Tray

- Anesthesia Room Procedure Tray

- Others

By Application

- Hospitals

- Clinics

- Ambulatory Surgical Centers

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the size of the Europe procedure trays market?

The Europe procedure trays market was valued at USD 3.58 billion in 2024 and is projected to reach USD 11.51 billion by 2034.

2. What drives growth in the Europe procedure trays market?

Rising surgeries, infection control regulations, and cost efficiencies propel the Europe procedure trays market forward.

3. Which countries lead the Europe procedure trays market?

Germany dominates the Europe procedure trays market, followed by UK and France due to advanced healthcare systems.

4. What is the CAGR of the Europe procedure trays market?

The Europe procedure trays market grows at 13.32% CAGR from 2026-2034, driven by surgical volume increases

5. What trends shape the Europe procedure trays market?

Single-use trays and minimally invasive procedures boost the Europe procedure trays market amid efficiency demands.

6. Which applications dominate the Europe procedure trays market?

Operating room trays hold the largest share in the Europe procedure trays market for standardized surgeries.

7. How do regulations impact the Europe procedure trays market?

EU sterility standards and infection prevention rules accelerate adoption in the Europe procedure trays market.

8. What role do hospitals play in the Europe procedure trays market?

Hospitals drive most demand in the Europe procedure trays market through high surgical procedure volumes.

9. Why is Germany key in the Europe procedure trays market?

Germany leads with efficient healthcare and custom tray adoption in the Europe procedure trays market.

10. What challenges face the Europe procedure trays market?

Supply chain variability and customization needs challenge the Europe procedure trays market growth.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com