Europe Smart Lock Market Size, Share, Trends, & Growth Forecast Report By End-Users (Commercial, Residential), Technology (Bluetooth, Wi-Fi), Product Types (Deadbolts, Lever Handles, Padlocks, Others), Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe), Industry Analysis (2025 to 2033)

Europe Smart Lock Market Size

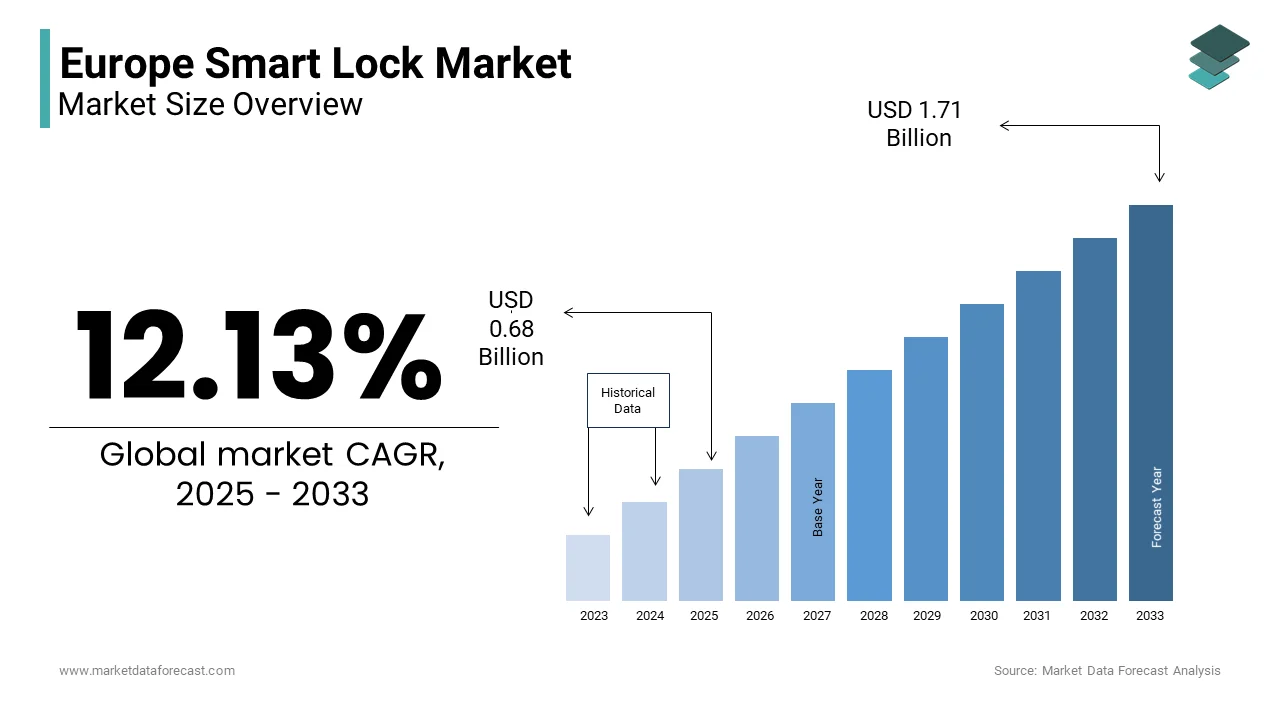

The europe smart locks market size was valued at USD 0.61 billion in 2024. The europe smart locks market Size is expected to have a 12.13 % CAGR from 2025 to 2033 and be worth USD 1.71 billion by 2033 from USD 0.68 billion in 2025.

Smart lock refers to the electronically enabled locking systems that utilize biometrics, wireless connectivity, mobile applications, or PIN-based authentication to secure residential, commercial, and institutional entry points. These devices represent a shift from mechanical access control to intelligent, data-driven security solutions integrated within broader smart home and building automation frameworks. Urbanization, rising break-in rates in major cities, and evolving consumer expectations for remote access control are transforming locks from passive barriers into active components of digital safety infrastructure.

MARKET DRIVERS

Adoption of Smart Home Ecosystems Enhancing Convenience and Security

The accelerating adoption of smart home ecosystems, where interoperability with voice assistants and centralized control platforms enhances user convenience and security integration, is a primary driver of the Europe smart lock market. Platforms like Apple HomeKit, Google Home, and Samsung SmartThings now support several certified smart lock models, enabling seamless automation, such as locking doors when the user leaves geofenced areas. This convergence of lifestyle technology and security is particularly strong among tech-savvy urban professionals, who view smart locks as essential components of a responsive, connected living environment.

Rising Incidence of Residential Break-ins Driving Demand for Smart Locks

The increasing incidence of residential break-ins and perceived vulnerability in urban and peri-urban areas, which has heightened demand for advanced access control, is another significant driver. Smart locks offer real-time notifications, audit trails, and temporary access codes for guests or service providers, features that deter opportunistic intrusions. This security-conscious behavior, amplified by media coverage and neighborhood watch apps, is driving widespread consumer investment in proactive digital protection.

MARKET RESTRAINTS

Lack of Standardized Cybersecurity Regulations for Consumer-Grade Smart Locks

The lack of standardized cybersecurity regulations specific to consumer-grade smart locks, leaving devices vulnerable to digital breaches, is one major restraint in the Europe smart lock market. Without mandatory certification for encryption and over-the-air updates, consumers remain skeptical, particularly in countries like Austria and Finland, where privacy concerns outweigh convenience, slowing broader market acceptance.

High Cost of Installation and Retrofitting in Older European Buildings

The high cost of installation and retrofitting, especially in Europe’s vast stock of older buildings with non-standard door structures, is another critical restraint. According to Eurostat, 38% of residential buildings in the EU were constructed before 1970, presenting compatibility challenges for modern smart lock mechanisms. These financial and technical barriers deter cost-sensitive consumers and limit adoption in rental properties, where landlords are reluctant to invest in non-permanent upgrades, particularly in markets with strict tenancy laws.

MARKET OPPORTUNITIES

Integration with Municipal Digital Identity and E-Government Platforms

Integration with municipal digital identity and e-government platforms, particularly in Nordic and Baltic countries, pioneering digital public services, is a transformative opportunity in the Europe smart lock market. This alignment with national digitalization strategies opens avenues for public-private partnerships and institutional adoption, positioning smart locks as infrastructure components rather than consumer gadgets.

Expansion of Smart Lock Deployment in Shared and Flexible Living Spaces

The expansion of smart lock deployment in shared and flexible living spaces, including co-living facilities, student housing, and vacation rentals, is another emerging opportunity. Property managers increasingly rely on smart locks to issue time-limited digital keys, monitor guest arrivals, and eliminate physical key exchanges. Student housing providers like Uninest in the UK and Campus Living in Germany have installed smart locks in a notable portion of new developments, citing improved security and operational efficiency. This shift toward access-as-a-service models creates scalable demand beyond individual homeowners.

MARKET CHALLENGES

Fragmentation of Technical Standards and Communication Protocols

The fragmentation of technical standards and communication protocols, which hinders device interoperability and consumer confidence, is a critical challenge facing the Europe smart lock market. As of 2023, smart locks in Europe operate on at least six different wireless standards, including Zigbee, Z-Wave, Bluetooth, Wi-Fi, Thread, and Proprietary RF, many of which are incompatible across brands, according to the European Telecommunications Standards Institute (ETSI). This lack of uniformity complicates integration for users building multi-vendor smart homes and increases the risk of obsolescence. Manufacturers face higher development costs to support multiple protocols, while consumers experience confusion and reduced satisfaction, undermining trust in the technology’s reliability.

Consumer Skepticism Regarding Reliability During Power Outages or Network Failures

Consumer skepticism regarding reliability during power outages or network failures, which remains a psychological barrier to adoption, is another significant challenge. The incidents, though rare, amplify perceptions of fragility. Without fail-safe mechanisms and clear communication on backup protocols, consumer hesitation persists, particularly among older demographics and in regions with unstable internet infrastructure.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 12.13% |

| Segments Covered | By Lock Type, Type, Verticals, and Country. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, Netherlands, Rest of Europe. |

| Market Leaders Profiled | Dessmann Schliessanlagen GmbH, Salto system S.L., Samsung Electronics Co., Ltd., August Home, ZKTeco Europe, Panasonic Corp., Vivint, Inc., Assa Abloy AB, Unikey Technologies Inc., and Honeywell International, Inc., and Others. |

SEGMENTAL ANALYSIS

By Lock Type Insights

The residential segment dominated the Europe smart lock market by capturing 62.7% of total revenue in 2024. This lead position is due to the surge in private home automation adoption, particularly among new-build and renovated properties. Urban homeowners in cities like Amsterdam and Vienna are increasingly retrofitting older doors with smart deadbolts to enhance security and enable remote access for family members and service providers. The integration of smart locks into broader home ecosystems further drives demand. A further critical factor reinforcing residential dominance is the growing prevalence of home-sharing and gig economy services. Property hosts rely on smart locks to issue time-limited digital keys, eliminate physical key exchanges, and maintain audit trails of guest access. This operational efficiency, combined with rising urban break-in rates, solidifies the residential sector as the primary growth engine.

The commercial segment is the fastest-growing end-user category and is projected to expand at a CAGR of 13.6% from 2025 to 2033. This acceleration is driven by the increasing adoption of smart access control in co-working spaces, corporate offices, and educational institutions seeking scalable, auditable entry systems. These systems allow dynamic key distribution, real-time occupancy tracking, and integration with HR software for automated onboarding and offboarding. A different key driver is the expansion of smart campuses and digitalized public infrastructure. Similarly, hospitals in the Netherlands are deploying smart lever handles with access-tier permissions to restrict entry to sensitive areas like pharmacies and ICUs. The European Commission’s 2023 Smart Buildings Initiative incentivizes digital access systems in public facilities. These institutional deployments, combined with rising cybersecurity awareness, are transforming smart locks from convenience tools into essential components of enterprise-grade physical security.

By Type Insights

The Bluetooth segment held the largest share of the Europe smart lock market at 53.1% of total technology-based installations in 2024. This dominance is rooted in Bluetooth’s low power consumption, widespread smartphone compatibility, and reliable short-range performance. In residential settings, Bluetooth allows immediate unlocking upon proximity, eliminating the need for constant internet connectivity. A further contributing factor is the cost-effectiveness and ease of integration with existing smart home ecosystems. Bluetooth-enabled locks require no additional hub in most cases, lowering installation barriers. Manufacturers like Yale and Ultraloq have optimized Bluetooth mesh networks to extend range and improve reliability, even through thick doors. Additionally, the technology supports secure key sharing via encrypted digital credentials, a feature increasingly used in rental and shared housing. Bluetooth remains the preferred protocol for entry-level and mid-tier smart locks.

The Wi-Fi segment is the fastest-growing technology in the Europe smart lock market, expanding at a CAGR of 11.8% during the forecast period. This growth is fueled by the demand for remote access and real-time monitoring, particularly in multi-occupant and commercial environments. Unlike Bluetooth, Wi-Fi-enabled locks allow users to unlock doors, receive alerts, and manage access from anywhere with internet connectivity. The integration with cloud-based platforms enables video doorbell synchronization and historical access logging, enhancing security oversight. A different key driver is the proliferation of all-in-one smart home security suites that rely on constant internet connectivity. Enterprises are adopting Wi-Fi locks for centralized management across multiple sites. Additionally, advancements in dual-band Wi-Fi 6 have improved signal penetration and reduced latency, addressing earlier reliability concerns. This shift toward always-connected, enterprise-grade access control is propelling Wi-Fi’s rapid adoption despite higher power consumption and cost.

By Verticals Insights

The deadbolts segment led the Europe smart lock market by commanding 49.6% of total product sales in 2024. This dominance is driven by their compatibility with standard residential doors and their reputation for robust physical security. Deadbolts provide superior resistance to forced entry compared to surface-mounted alternatives, making them the preferred choice for front doors. Their mechanical reliability, combined with electronic enhancements like fingerprint scanners and app control, offers a balanced upgrade path for homeowners seeking both security and modernity without structural modifications. An additional critical factor is the widespread retrofitting potential of smart deadbolts, which can replace traditional units without altering door frames. Manufacturers like Assa Abloy and Yale have developed hybrid models that retain physical key backup while adding digital access, appealing to risk-averse consumers. This blend of mechanical strength, regulatory alignment, and technological adaptability ensures deadbolts remain the cornerstone of residential smart access.

The lever handles segment is the fastest-growing product type in the Europe smart lock market, projected to expand at a CAGR of 12.4% from 2025 to 203. This growth is driven by their integration into new commercial and multi-family residential buildings, particularly in Scandinavia and the Benelux region, where lever-style doors are standard. Unlike deadbolts, smart lever handles combine locking mechanisms with door handles, offering a sleek, space-efficient design ideal for modern architecture. A further key driver is the rise of smart access in institutional settings such as hospitals, universities, and office complexes. Lever handles with embedded RFID, Bluetooth, or keypad systems allow seamless integration with access control software, enabling tiered permissions and real-time monitoring. Additionally, the technology supports hands-free operation via motion sensors or smartphone proximity, enhancing usability for disabled or elderly users. This convergence of design, functionality, and institutional demand is accelerating the segment’s ascent beyond traditional residential applications.

REGIONAL ANALYSIS

Germany Smart Lock Market Insights

Germany spearheaded the Europe smart lock market by accounting for 22.1% of regional revenue in 2024. The country’s position is anchored in its advanced construction sector and high homeowner investment in home automation. Rising break-in rates in cities such as Leipzig and Düsseldorf have further accelerated adoption. Strong domestic manufacturing and consumer trust in engineering quality reinforce sustained market growth.

France Smart Lock Market Insights

France is also a key player in the market, driven by urban security concerns and the expansion of short-term rentals. The government’s “Housing of the Future” initiative promotes digital safety in new developments. Additionally, Airbnb hosts in Marseille and Bordeaux are adopting smart locks to manage guest turnover. These converging residential and regulatory trends position France as a dynamic and security-conscious market.

United Kingdom Smart Lock Market Insights

The United Kingdom is characterized by strong adoption in both private and rental housing. The rise of gig economy services, such as cleaning and pet sitting, has increased demand for temporary digital access. London leads in adoption. The UK’s mature smart home ecosystem, supported by providers like BT and Sky, facilitates seamless integration. Consumer awareness campaigns have further boosted confidence in digital locks, driving steady market expansion.

KEY MARKET PLAYERS

Companies playing a prominent role in the Europe smart lock market include Dessmann Schliessanlagen GmbH, Salto System S.L., Samsung Electronics Co., Ltd., August Home, ZKTeco Europe, Panasonic Corp., Vivint, Inc., Assa Abloy AB, Unikey Technologies Inc., and Honeywell International, Inc., and Others.

TOP LEADING PLAYERS IN THE MARKET

Assa Abloy AB

Assa Abloy AB is a global leader in access solutions and a dominant force in the Europe smart lock market, renowned for its integration of mechanical security expertise with digital innovation. The company has strengthened its position through strategic acquisitions of tech-focused startups and the expansion of its smart cylinder and electronic escutcheon lines for residential and commercial use. It also partnered with leading smart home platforms like Apple HomeKey to support mobile credentialing. While its presence in the Asia Pacific market includes deploying high-security smart locks in Singapore’s public housing and Australian corporate campuses, in Europe, Assa Abloy focuses on interoperability, durability, and compliance with GDPR and EN 1303 standards to maintain trust in critical infrastructure.

Yale

Yale (a division of Allegion plc) has played a pivotal role in democratizing smart lock technology for European homeowners through user-friendly designs and affordable innovation. The company introduced the Yale Assure Lock 2 with built-in Wi-Fi and voice control compatibility, eliminating the need for additional hubs and simplifying installation for DIY consumers. It also collaborated with Airbnb to pilot digital key integration for hosts in Barcelona and Dublin, enhancing rental property management. While Yale’s Asia Pacific initiatives include smart lock rollouts in South Korean apartments and Indian smart cities, in Europe, its strategy centers on accessibility, retrofit solutions, and partnerships with property managers to drive mass-market adoption.

SCHLAGE

SCHLAGE (Allegion plc) is a key innovator in the European smart lock landscape, leveraging its heritage in mechanical security to deliver robust, digitally enhanced access systems. The company has focused on high-end residential and commercial segments, introducing the SCHLAGE Encode Plus with Apple HomeKit Secure Video integration, allowing homeowners to view and record door activity. It also enhanced cybersecurity features with end-to-end encryption and local data processing to address European privacy concerns. Though SCHLAGE’s Asia Pacific activities include supplying smart access systems for mixed-use towers in Tokyo and Sydney, in Europe, its emphasis lies on security certification, aesthetic integration, and compliance with regional building codes to establish credibility among architects and security professionals.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe smart lock market are employing a combination of technological integration, strategic partnerships, and regulatory compliance to solidify their positions. Companies are prioritizing interoperability with major smart home ecosystems such as Apple HomeKit, Google Home, and Amazon Alexa to enhance consumer appeal. Cybersecurity reinforcement through end-to-end encryption, local data storage, and adherence to GDPR is critical to gaining consumer trust. Firms are also expanding into institutional and commercial sectors by integrating smart locks with access management software for offices, universities, and healthcare facilities. Strategic collaborations with property developers, short-term rental platforms, and national digital identity programs are enabling large-scale deployment. Additionally, investment in retrofit solutions ensures compatibility with Europe’s aging building stock, broadening market reach across rental, residential, and public infrastructure segments.

COMPETITIVE OVERVIEW

The competition in the Europe smart lock market is characterized by a blend of established hardware manufacturers, tech-driven startups, and ecosystem integrators vying for dominance in a rapidly evolving security landscape. Incumbents like Assa Abloy and Yale leverage brand trust, engineering excellence, and distribution networks to maintain leadership, particularly in retrofit and new-build residential segments. However, they face increasing pressure from agile entrants offering app-centric, low-cost models and niche solutions for co-living and smart cities. Differentiation hinges on cybersecurity robustness, seamless interoperability, and compliance with regional regulations such as GDPR and EN standards. The market is further fragmented by divergent national building codes and consumer preferences, requiring localized product adaptation. As demand shifts from standalone devices to integrated access ecosystems, competition is intensifying around software capabilities, service models, and institutional partnerships, making Europe a complex yet high-potential arena for smart lock innovation.

RECENT MARKET DEVELOPMENTS

- In January 2023, Assa Abloy launched its Aperio wireless cylinder in France and Germany, enabling the retrofit of existing mechanical doors with digital access while integrating with HID and LenelS2 security platforms.

- In May 2023, Yale partnered with Airbnb Europe to pilot mobile key sharing for hosts in Dublin, Barcelona, and Milan, streamlining guest access and reducing physical key management.

- In September 2023, SCHLAGE introduced the Encode Plus deadbolt with Apple HomeKit Secure Video support, allowing real-time door monitoring and recording for iOS users across the UK and Benelux.

- In February 2024, Nuki expanded its Smart Lock 3.0 across Scandinavia with enhanced Bluetooth 5.2 and Thread compatibility, improving reliability in multi-story apartment buildings.

- In June 2024, Eve Systems integrated its HomeKey-enabled smart lock with Germany’s Deutsche Telekom Smart Home Hub, offering seamless voice and app control for Telekom’s 2.1 million subscribers.

MARKET SEGMENTATION

This research report on the europe smart lock market is segmented and sub-segmented into the following categories.

By Lock Type

- Deadbolts

- Lever Handles

- Padlocks

- Other Locks

By Type

- Bluetooth

- Wi-Fi

- Zigbee

- Z-Wave

- Thread

- NFC

- Other Protocols

By Verticals

- Commercial

- Residential

- Institution & Government

- Industrial

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1 Which types of smart locks dominate the Europe Smart Lock Market?

Deadbolt smart locks are the dominant product type in the Europe Smart Lock Market, favored for their robust security and ease of integration.

2.What are the key technologies used in the Europe Smart Lock Market?

The Europe Smart Lock Market primarily features Wi-Fi, Bluetooth, Z-wave, Zigbee, and NFC technologies for connectivity and remote control.

3. How important is biometric authentication in the Europe Smart Lock Market?

Biometric authentication is gaining substantial market share in Europe due to its enhanced security and convenience, especially in urban tech-savvy centers.

4. What are the main drivers of the Europe Smart Lock Market growth?

Key growth drivers include rising home automation trends, security concerns, smartphone penetration, and smart home device integration within Europe.

5.Are there any security concerns in the Europe Smart Lock Market?

Yes, concerns such as hacking vulnerability and technological reliability issues exist, but are being addressed by ongoing innovations in the Europe Smart Lock Market.

6.Who are the major players in the Europe Smart Lock Market?

Prominent companies in the Europe Smart Lock Market include ASSA ABLOY, Allegion PLC, Eufy, Sentrilock LLC, and ZKTeco Co Ltd.

7.How is the Europe Smart Lock Market segmented by application?

The market covers residential, commercial, and hospitality sectors with smart locks being widely used for home security, office access, and hotel door management.

8.What role does smartphone integration play in the Europe Smart Lock Market?

Smartphone integration is crucial as it allows remote access control and monitoring, significantly boosting the adoption of smart locks in Europe.

9.Which European countries lead the smart lock adoption?

Germany leads within Europe due to high smart home adoption rates and technological innovation, followed by the UK, France, Spain, and Italy.

10.What are some recent innovations in the Europe Smart Lock Market?

Recent innovations include retrofit smart locks, integration with voice assistants, fingerprint-enabled mortise locks, and cloud-based access control systems.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com