Europe Software Defined Vehicles Market Size, Share, Trends And Growth Forecasts Research Report, Segmented By Deployment Mode, Type, Application and Country - Industry Analysis (2026 to 2034)

Europe Software-Defined Vehicles Market Size

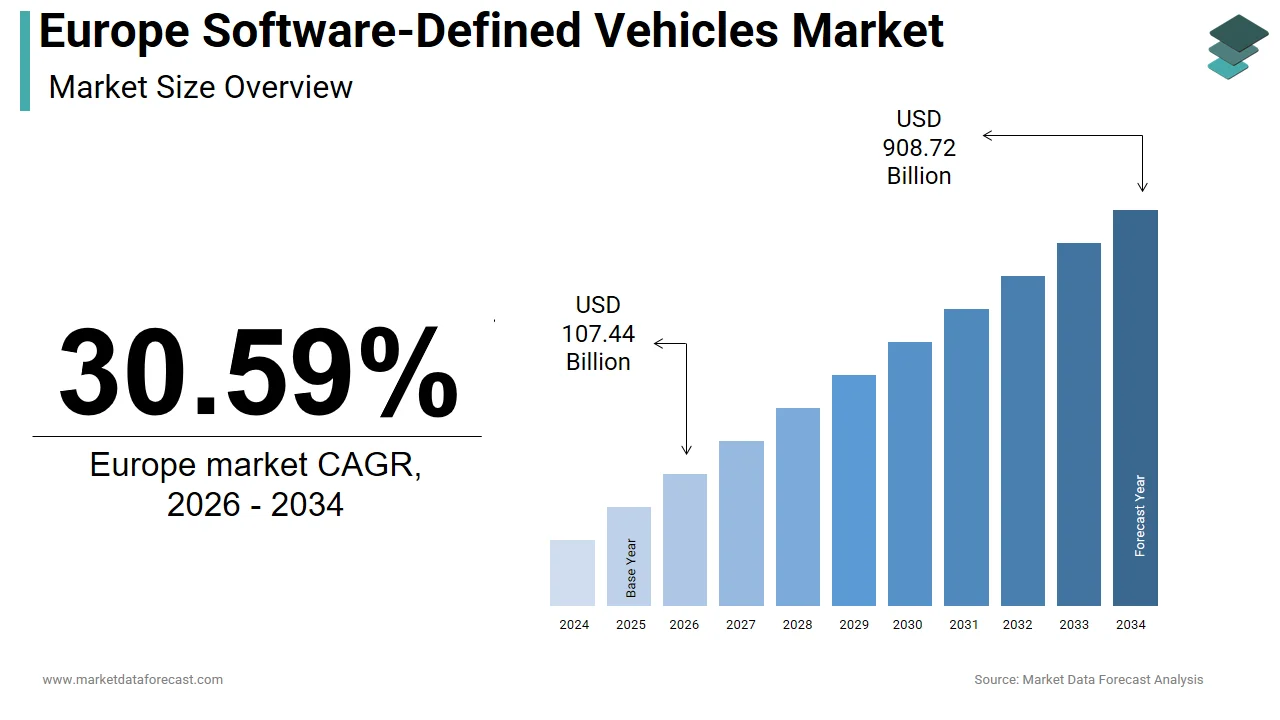

The Europe software-defined vehicles market was valued at USD 82.27 billion in 2025, is estimated to reach USD 107.44 billion in 2026, and is projected to reach USD 908.72 billion by 2034, growing at a CAGR of 30.59% from 2026 to 2034.

Software-defined vehicles are a paradigm shift in automotive engineering, wherein core functionalities ranging from powertrain control and advanced driver assistance to infotainment and over-the-air updates are managed by centralized software platforms rather than fixed hardware configurations. In Europe, this transformation is accelerating as automakers transition from mechanical to digital product architectures to meet stringent emissions targets, evolving safety mandates, and consumer expectations for continuous feature enhancement. As per the European Commission’s 2023 Cyber Resilience Act, further mandates secure software update mechanisms for all connected vehicles, institutionalizing this architecture.

MARKET DRIVERS

EU Regulatory Frameworks Mandate Over-the-Air Update Capabilities

The European Union’s progressive regulatory framework for software-defined vehicle adoption, with binding legislation requiring secure and functional over-the-air update systems in all new connected vehicles, is escalating the growth of Europe's software-defined vehicles market. The manufacturers implement robust software update mechanisms to patch vulnerabilities throughout a vehicle’s lifecycle, directly necessitating a software-defined architecture. As per the European Commission, non-compliance can result in fines up to 15 million euros or 2.5 % of global turnover. Complementing this, the General Safety Regulation Phase 2, which is effective from July 2024 that requires intelligent speed assistance, driver drowsiness detection, and event data recorders, all of which rely on updatable software modules. Furthermore, the EU’s upcoming Type Approval framework for automated vehicles, expected in 2025, will require real-time validation of software performance, making static hardware-based systems obsolete. These regulations transform software from an optional feature into a legal prerequisite, compelling even legacy manufacturers to overhaul their electronic and electrical architectures.

Consumer Demand for Personalized and Evolving In-Vehicle Experiences

European consumers are increasingly prioritizing digital features and post-purchase value enhancement over traditional mechanical attributes, which is driving automakers to embed software-defined capabilities as standard. This factor is propelling the growth of the Europe software-defined vehicles market. According to a 2024 survey by the European Consumer Organisation, new car buyers in Germany and France consider over-the-air update functionality a decisive purchase factor, while 57% expect subscription-based access to features like enhanced navigation or performance modes. Premium brands have responded aggressively, where Mercedes-Benz’s MB.OS platform enables owners to activate rear axle steering or ambient lighting packages months after purchase, generating recurring revenue.

MARKET RESTRAINTS

Fragmented Legacy Electronic Architectures Impede Scalable Integration

The entrenched legacy of distributed electronic control units across existing vehicle platforms is restricting the growth of Europe's software-defined vehicles market. Most conventional cars operate on architectures with 70 to 150 discrete ECUs from multiple suppliers, each running proprietary code with limited interoperability. According to the Technical University of Munich, retrofitting such systems for centralized software control requires complete rewiring and revalidation, increasing development costs by up to 35%. Legacy platforms like Volkswagen’s MQB or PSA’s EMP2 were not designed for high-speed data backbones such as Ethernet, which limits bandwidth for real-time software functions. This technical debt forces manufacturers into costly parallel development tracks, which involve maintaining legacy models while investing in new architectures like Volkswagen’s SSP or Renault’s AmpR.

Stringent Data Privacy and Cross-Border Compliance Complexities

The substantial friction from the region’s rigorous and multi-layered data governance regime, which complicates the collection, processing, and transfer of vehicle-generated data, is restricting the growth of Europe's software-defined vehicles market. The anonymization of telematics data must meet strict statistical irreversibility standards, which render many machine learning training datasets non-compliant. Furthermore, the EU’s Data Act, effective from September 2025, grants users the right to share their vehicle data with third parties, but mandates complex interoperability and security protocols that manufacturers must implement. Cross-border data flows add another layer; the European Court of Justice’s Schrems II ruling invalidated standard contractual clauses for transfers to certain non-EU jurisdictions, which is affecting cloud-based training for AI driving systems.

MARKET OPPORTUNITIES

Monetization Through Feature on Demand and Subscription Services

The emergence of feature-on-demand and subscription-based revenue models is elevating new opportunities for the expansion of Europe's software-defined vehicles market by decoupling hardware sales from service income. Automakers can now activate dormant capabilities, such as heated seats, advanced parking assist, or performance upgrades via software licenses after purchase. BMW’s “Driving Assistant Professional” subscription that priced at 23 Euros monthly, has attracted over 200000 active users across Germany and France. Similarly, Volvo’s Care by Volvo program bundles insurance, maintenance, and software features into a single monthly payment, which is enhancing customer retention.

Integration of Vehicle to Grid and Smart Energy Ecosystems

The software-defined vehicles are poised to become active nodes in Europe’s expanding smart energy infrastructure through bidirectional energy management and grid services, which is also expected to escalate the growth of Europe's software-defined vehicles market. The European Union’s Alternative Fuels Infrastructure Regulation mandates that all new electric vehicles sold from 2026 support smart charging and, where technically feasible, vehicle-to-grid functionality. As per the European Environment Agency, Europe will have over 45 million electric vehicles by 2030, with a distributed energy storage capacity exceeding 2000 gigawatt hours. Software-defined architectures enable real-time coordination with energy providers; Ford’s collaboration with E.ON in Germany allows Mustang Mach E owners to sell stored energy back to the grid during peak demand, earning credits via an integrated app.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Centralized Vehicle Architectures

The consolidation of vehicle functions into centralized software platforms significantly expands the attack surface for cyber threats, which is a challenge to the Europe software-defined vehicles market growth. The software-defined vehicles rely on high-speed data buses and cloud connectivity by creating multiple entry points for malicious actors. The 2023 breach of a major German automaker’s telematics server exposed real-time location data of over 800000 vehicles. Compliance with the EU Cyber Resilience Act requires continuous vulnerability scanning and secure boot mechanisms, but implementation remains inconsistent. The shortage of automotive cybersecurity talent exacerbates the issue, where Europe faces a deficit of over 300000 qualified professionals. These vulnerabilities not only risk safety and privacy but also trigger regulatory penalties and brand erosion, which demand unprecedented investment in embedded security.

Shortage of Skilled Software Talent and Development Infrastructure

The severe shortage of engineers proficient in automotive-grade software development, real-time operating systems, and functional safety standards may also slow down the growth of Europe's software-defined vehicles market. This gap is particularly acute in domains like AUTOSAR Adaptive, POSIX-compliant systems, and ISO 21434 cybersecurity engineering. Legacy automakers struggle to compete with tech firms for talent. A 2023 study by the Technical University of Berlin, automotive software graduates accepted offers from non-automotive employers due to higher compensation and agile work cultures. Moreover, Europe lacks sufficient high-performance computing infrastructure for large-scale simulation and AI training.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Deployment Mode, Type, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Aptiv PLC, General Motors Company, Hyundai Motor Company, Mercedes-Benz Group AG, NVIDIA Corporation, Qualcomm Technologies, Inc., Robert Bosch GmbH, Tesla, Inc., and Toyota Motor Corporation. |

SEGMENTAL ANALYSIS

By Deployment Mode Insights

The On-board (edge) deployment segment held a dominant share of the Europe software-defined vehicles market in 2025, with the non-negotiable requirement for ultra-low latency in safety vehicle functions such as automatic emergency braking, lane keeping, and adaptive cruise control. These systems must respond within milliseconds, far faster than cloud round-trip times permit, which necessitates powerful onboard platforms. As per the Technical University of Munich, edge processing in modern vehicles handles over 95 % of real-time decision making, with only non-urgent tasks like map updates or diagnostics routed to the cloud. The European New Car Assessment Programme’s 2023 safety protocols now award higher ratings to vehicles with redundant onboard AI processors capable of fail-operational performance. Additionally, the EU Cyber Resilience Act mandates that core safety functions remain operational even during network outages with edge reliance.

The cloud-based deployment segment is expected to witness the fastest CAGR of 24.3% throughout the forecast period, with the rising demand for data-intensive services that do not require real-time response but benefit from centralized processing and machine learning at scale. Predictive maintenance, personalized infotainment, traffic pattern analysis, and fleet management all leverage cloud infrastructure to aggregate and analyze data from millions of vehicles. The standardized APIs for third-party access to this data, by enabling new cloud-based mobility services, are made mandatory in most countries. Volkswagen’s partnership with Microsoft Azure processes over 5 million vehicle data points daily to refine battery health algorithms across its ID series.

By Type Insights

The Hybrid software segment was the largest by holding a dominant share of the Europe software-defined vehicles market in 2025, with the current technological and regulatory reality wherein full autonomy remains limited to controlled environments, while most consumer vehicles integrate software-defined features within human-supervised driving frameworks. These hybrids combine advanced driver assistance systems with upgradable infotainment, telematics, and powertrain software, which offers immediate value without requiring Level 4 or 5 certification. Major European OEMs have strategically focused here, where Stellantis’ STLA Brain architecture powers over 3 million hybrid software-defined vehicles across Peugeot, Citroën, and Opel brands.

The autonomous software segment is likely to grow at an anticipated CAGR of 31.7% throughout the forecast period, with the targeted deployment in geofenced commercial and public transport applications where regulatory pathways are clearer and economic returns are measurable. Autonomous shuttles in cities like Helsinki and Lyon now operate daily routes under EU Horizon Europe-funded pilots, with each vehicle generating over 2 terabytes of sensor data daily for continuous learning. These controlled, high-value use cases are combined with advancing AI validation methods like scenario-based testing endorsed by the German Federal Highway Research Institute that create a viable trajectory for autonomous software-defined vehicles despite broader consumer market limitations.

COUNTRY LEVEL ANALYSIS

Germany Software-Defined Vehicles Market Analysis

Germany was the largest contributor in the Europe software-defined vehicles market with a 26.3% share in 2024, with its concentration of premium automotive OEMs such as Volkswagen, Mercedes-Benz, and BMW. Volkswagen’s CARIAD software unit alone employs over 5000 engineers across Wolfsburg and Berlin, which is developing the unified SSP platform for all group brands. Germany also hosts Europe’s most advanced testing infrastructure, including the digital test field on the A9 autobahn and the Aldenhoven Testing Center, which simulates real-world connectivity and edge computing scenarios. Furthermore, the German Federal Motor Transport Authority has approved more over-the-air update campaigns than any other EU nation, establishing a regulatory sandbox for rapid iteration.

United Kingdom Software-Defined Vehicles Market Analysis

The United Kingdom was positioned second by holding 14.3% of Europe's software-defined vehicles market share in 2024. The Centre for Connected and Autonomous Vehicles has allocated over 400 million pounds since 2021 to support software-defined vehicle trials, including the Smart Mobility Living Lab in London. British startups like Oxbotica and FiveAI have developed localization and perception software now integrated into European OEM platforms. The Zenzic CAM Scale Up programme further accelerates commercialization by connecting startups with OEMs and infrastructure providers.

France Software-Defined Vehicles Market Analysis

France's software-defined vehicles market growth is expected ot grow at a steady pace with new growth opportunities throughout the forecast period. The country’s software-defined vehicle strategy is anchored in its national AI plan and strong public-private collaboration. Renault Group’s AmpR Core and AmpR Cloud platforms are developed in partnership with Google Cloud and Qualcomm, which power its entire electric lineup with upgradable software features. The French government’s “Choose France” initiative has attracted over 2 billion euros in automotive software investment since 2022, thereby including Microsoft’s automotive cloud hub in Marseille. Moreover, France’s emphasis on data sovereignty through the Gaia-X alliance ensures that vehicle data processing remains within European jurisdiction.

COMPETITIVE LANDSCAPE

The Europe software-defined vehicles market features intense competition among legacy automakers racing to transform into software-driven technology companies while fending off new entrants and tech giants. Traditional OEMs leverage their manufacturing scale, brand trust, and regulatory expertise, but face challenges in cultural transformation and software talent acquisition. Competition is increasingly defined not by hardware specifications but by the richness of the software ecosystem, update frequency, cybersecurity robustness, and monetization models. Differentiation hinges on the ability to deliver seamless, personalized, and secure digital experiences that evolve post-purchase.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe software-defined vehicles market include

- Aptiv PLC

- General Motors Company

- Hyundai Motor Company

- Mercedes-Benz Group AG

- NVIDIA Corporation

- Qualcomm Technologies, Inc.

- Robert Bosch GmbH

- Stellantis

- Tesla, Inc.

- Toyota Motor Corporation

- Volkswagen Group

TOP PLAYERS IN THE MARKET

- Volkswagen Group is a European automotive leader actively transforming its portfolio through its CARIAD software division, which develops unified operating systems for all group brands, including Audi, Porsche, and Škoda. The company is pioneering the E³ 2.0 and SSP software-defined vehicle architectures to enable over-the-air updates, feature on demand, and advanced driver assistance across millions of vehicles. It also launched its first fully software-defined ID model with centralized compute and upgradable chassis controls. These initiatives reinforce Volkswagen’s global influence in scaling software-defined mobility while establishing a vertically integrated software stack that reduces reliance on external suppliers and strengthens long-term competitiveness in the digital automotive era.

- Mercedes-Benz Group has emerged as a frontrunner in the Europe software-defined vehicles market through its proprietary MB.OS operating system, designed to manage all vehicle domains from infotainment to autonomous driving on a single platform. The company delivers continuous feature enhancements via over-the-air updates and offers subscription-based services such as rear axle steering and ambient lighting. It also established a dedicated software campus in Stuttgart with over 1000 engineers focused on agile development. These actions position Mercedes-Benz as a premium innovator that blends luxury with cutting-edge software capabilities, thereby setting benchmarks for user experience and monetization in the global automotive software landscape.

- Stellantis is advancing its software-defined vehicle strategy across Europe through its STLA Brain and STLA SmartCockpit platforms, which power brands like Peugeot, Citroën, Opel, and Fiat with upgradable features and connected services. The company has committed to launching 30 software-defined vehicle models by 2026, all built on a centralized compute architecture with over-the-air update functionality. It also opened a software development center in Turin employing 500 engineers focused on agile coding and cybersecurity. These moves demonstrate Stellantis’ commitment to transforming from a volume manufacturer into a tech-driven mobility provider with scalable, secure, and consumer-centric software offerings across global markets.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe software-defined vehicles market are developing proprietary vehicle operating systems to achieve vertical integration and control over the user experience. They are forming strategic alliances with global cloud and semiconductor firms to access high-performance computing and scalable data infrastructure. Companies are establishing dedicated software campuses and hiring thousands of engineers to build in-house capabilities in agile development and functional safety. There is a strong emphasis on over-the-air update frameworks that comply with the EU Cyber Resilience Act and enable continuous feature delivery. Automakers are launching subscription-based feature on-demand services to create recurring revenue streams beyond vehicle sales. They are also investing in centralized electronic architectures that replace legacy distributed ECUs with domain controllers and system-on-chip processors. Additionally, they are participating in EU-funded testbeds and regulatory sandboxes to accelerate validation and type approval of software-defined functionalities across diverse operational environments.

MARKET SEGMENTATION

This research report on the Europe software-defined vehicles market has been segmented and sub-segmented into the following categories.

By Deployment Mode

- On-Board (Edge)

- Cloud-Based

By Type

- Autonomous Software-Defined Vehicles

- Connected Software-Defined Vehicles

- Electric Software-Defined Vehicles

- Infotainment and Comfort Software-Defined Vehicles

- Hybrid Software-Defined Vehicles

By Application

- Advanced Driver-Assistance Systems (ADAS)

- Autonomous Driving

- Infotainment Systems

- Electric Vehicle (EV) Management

- Vehicle-to-Everything (V2X) Communication

- Personalization

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

1. What drives the Europe Software Defined Vehicles Market growth?

Growth is driven by ADAS adoption, demand for OTA updates, EV sales, mobility startups, cloud integration, and digital vehicle architecture in Europe Software Defined Vehicles Market

2. Which segment leads the Europe Software Defined Vehicles Market?

On-board edge deployment is the largest and fastest-growing segment, enabling real-time processing, lower latency, and improved safety in Europe Software Defined Vehicles Market

3. What role do OTA updates play in the Europe Software Defined Vehicles Market?

OTA updates allow remote feature enhancements, bug fixes, security patches, and regulatory compliance, minimizing dealership visits

4. How do European regulations impact the Software Defined Vehicles Market?

EU data privacy laws, cyber standards, and functional safety mandates shape software design and SDV provider compliance in Europe

5. What are the main benefits of SDV architecture in the Europe market?

SDVs enable flexible upgrades, tailored driver experiences, predictive maintenance, and lower costs through software-driven features

6. How does edge computing influence SDVs in Europe?

Edge solutions allow real-time analytics, fast responses for ADAS, and reduced cloud latency, crucial for autonomous features in Europe

7. Which countries are major contributors in the Europe Software Defined Vehicles Market?

Germany, France, and the UK lead SDV adoption due to strong automotive OEMs, tech innovation, and supportive infrastructure

8. What impact does EV adoption have on the Europe Software Defined Vehicles Market?

High EV sales increase SDV adoption, as electric vehicles are built with centralized, software-defined architectures

9. How do SDVs change the automotive value chain in Europe?

Shift from hardware to software-centric features adds recurring revenue streams, ecosystem partnerships, and mobility service models

10. What is the role of ADAS in Europe Software Defined Vehicles Market?

ADAS modules powered by software provide emergency braking, lane keeping, collision avoidance, and driver assist features in Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com