Europe Specialty Coffee Market Size, Share, Trends & Growth Forecast Report – Segmented By Age Group (18-24 Years, 25-39 Years, 40-59 Years, above 60), Distribution Channel, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Specialty Coffee Market Size

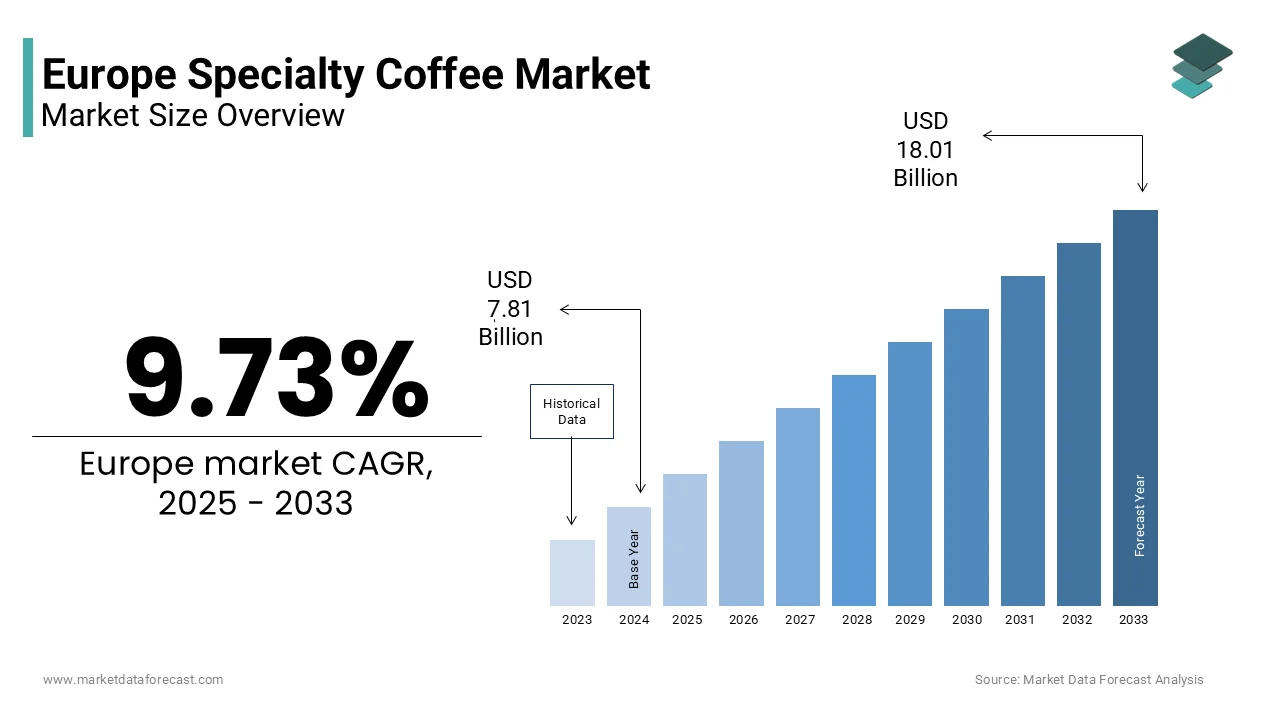

The European speciality coffee market size was valued at USD 7.81 billion in 2024 and is projected to reach USD 18.01 billion by 2033, growing at a CAGR of 9.73%.

Speciality coffee in Europe refers to high-quality Arabica beans that score 80 or above on the Speciality Coffee Association’s 100-point scale and are meticulously sourced, roasted, and brewed to origin characteristics and craftsmanship. According to the European Coffee Federation, over 28% of regular coffee drinkers in the European Union expressed willingness to pay a premium for certified speciality coffee in 2023. As per the E, imported 2.1 million metric tons of roasted coffee in 2023, with speciality-grade imports from Ethiopia, Colombia and Kenya growing at twice the rate of mainstream blends. The European Union’s Farm to Fork Strategy now includes provisions for ethical sourcing, which has accelerated direct trade relationships between European roasters and smallholder farms. Furthermore, the European Barista Championship and national competitions in countries like Germany and Sweden have elevated consumer awareness and professional standards. Drivers:

MARKET DRIVERS

Rising Consumer Preference for Traceable and Ethically Sourced Coffee

European consumers are increasingly prioritising transparency and ethical provenance in their coffee choices, which is a primary driver for the growth of the European speciality coffee market. The speciality coffee buyers in 2023 actively sought information on farm origin, processing method and producer compensation before making a purchase. This demand has spurred the adoption of blockchain and QR code traceability systems by roasters in the Netherlands and Denmark, with companies like Coffee Circle publishing annual impact reports detailing payments to cooperatives in Rwanda and Peru. Additionally, the EU Deforestation Regulation enacted in 2023 requires geolocation data for all imported coffee, which aligns naturally with speciality supply chains that already document parcel-level sourcing.

Proliferation of Third Wave Cafes and Barista Culture

The expansion of third-wave coffee shops across European cities has fundamentally reshaped consumption patterns and elevated speciality coffee from niche to norm. This factor is also propelling the growth of the European speciality coffee market. According to the European Coffee Association, over 12000 independent speciality cafes operated in the EU in 2023,, ith GerGermanyFrance and the United Kingdom hosting the highest densities. These establishments function as experiential retail spaces where brewing methods such as aspour-overcold brew, and siphon are demonstrated, and sensory education is embedded in service. The World Barista Championship notes that European competitors have won five of the last ten global titles, highlighting the region’s technical excellence and influence. In cities like Lisbon and Warsaw, local governments have introduced “coffee tourism” trails to promote cultural districts centred on noasteriess and tasting rooms. As per the Eurofound Quality of Life Survey, 41% of urban Europeans aged 25 to 40 visit a speciality cafe at least once a week, viewing it as a social and cultural activity rather than mere caffeine consumption.

MARKET RESTRAINTS

High Volatility in Green Coffee Prices and Supply Disruptions

The persistent pressure from extreme fluctuations in global green coffee prices and climate-induced supply instability is restraining the growth of the European speciality coffee market. According to the International Coffee Organisation, the ICO composite indicator price for Arabica beans surged to 245 US cents per pound in December 2023, the highest in 14 years, due to drought in Brazil and frost damage in Central America. Speciality roasters who rely on single-origin lots often pay 30 to 100% above commodity price,,s making them especially vulnerable. Furthermore, the European Environment Agency reports that coffee farms in key origins like Colombia and Ethiopia are located in climate-vulnerable zones with yields projected to decline by up to 50% by 2050. In 2023, European importers experienced average lead time extensions of 22 days for speciality containers due to port congestion and shipping reroutes. These disruptions force small roasters to raise retail prices or reduce batch size,, es undermining customer retention and margin stability.

Stringent and Fragmented Food Safety and Labelling Regulation

Speciality coffee operators in Europe must navigate a complex and inconsistent web of national and EU-level regulations governing labels,ngg allergen declaration,,s and organic certificationnwhich increases compliance costs and limits scalability. According to the European Commission’s Food Information to Consumers Regulation, coffee is exempt from mandatory nutrition labelling but must declare allergens if processed in shared facilities, which is a requirement that varies in enforcement across member states. Additionally, the EU Organic Regulation requires full chain certification for any “organic” claim, with inspection fees ranging from 800 to 2500 euros annually per operator, as per the Organic Farmers Association of Europe. In Italy and Spain, local authorities have imposed additional municipal rules on café waste segregation and compostable packaging that indirectly affect coffee service models. This regulatory fragmentation disproportionately burdens micro roasters and independent cafes, which lack the legal resources to interpret and implement divergent standards.

MARKET OPPORTUNITIES

Growth of Direct Trade and Regenerative Agriculture Partnerships

The deepening of direct trade relationships that integrate regenerative agriculture practices and long-term price stability is escalating the growth of the European speciality coffee market. According to the European Speciality Coffee Association, over 60% top-tier roasters in Scandinavia and the Benelux region now source at least 40% of their beans through direct contracts that guarantee prices 25 to 50% above Fairtrade minimums. In 2023, a consortium of German roasters, including Five Elephant and The Barn, launched the “Soil to Cup” initiative, funding shade tree planting and soil health programs on 12 farms in Guatemala and Uganda. As per the Joint Research Centre of the European Commission, such partnerships reduce supply chain emissions compared to conventional trade due to fewer intermediaries and optimised logistics. Furthermore, the EU’s Carbon Border Adjustment Mechanism includes provisions for agricultural imports, which may soon reward carbon-neutral fees with tariff advantages.

Integration of Speciality Coffee into Workplace Wellness Programs

The corporate demand for premium coffee as part of employee wellness and sustainability initiatives presents a high-growth B2B opportunity in Europe. According to the European Foundation for the Improvement of Living and Working Conditions, multinational companies in the EU introduced enhanced food and beverage offerings in 2023 to improve workplace satisfaction amid hybrid work trends. Companies like Spotify in Stockholm and Siemens in Munich now contract speciality roasters to provide single-origin brews and barista training in office kitchens, replacing standard instant or pod systems. In the Netherlands, the government’s “Green Office Procurement” guideline explicitly encourages public agencies to source speciality coffee with verified social and environmental metrics.

MARKET CHALLENGES

Intensifying Competition from Premiumized Mainstream Brands

Established mass market coffee companies are blurring category boundaries by launching “premium” or “craft-inspired” sub-brands that mimic speciality attributes at lower price points, which threatens independent roasters’ differentiation. These products leverage extensive retail distribution and marketing budgets to capture mid-tier consumers who desire quality but are price sensitive. The European Coffee Monitor found that 39% of occasional speciality buyers switched to these mainstream premium options in 2023 due to convenience and promotional pricing. Furthermore, supermarket chains like Carrefour in France and Edeka in Germany now operate in-house roasting facilities producing private label speciality style coffee at 30% lower cost than independent brands. This commoditization of craft aesthetics without equivalent ethical or quality standards creates confusion and price pressure, particularly for micro roasters without scale or digital reac

Labourbor Shortages and Rising Operational Costs in Urban Cafes..

Speciality coffee businesses in Europe are grappling with acute staffing shortages and escalating fixed costs that undermine profitability and expansion. According to Eurostat, the hospitality sector in the EU faced a 12.3% vacancy rate in 20,23, with barista positions among the hardest to fill in cities like London and Amsterdam due to low wages and high skill requirements. These compounding pressures force man speciality cafes to reduce operating hours, limit training investments, or exit high-visibility districts, thereby weakening brand presence and customer engagement in key markets.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 9.73% |

| Segments Covered | By Age Group, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Starbucks Corporation, Inspire Brands, Inc., F. Gavina and Sons, Inc., Barista Coffee, Coffee Day Enterprises Ltd., Blue Bottle Coffee, Inc. (Nestle S.A.), Eight O'Clock Coffee Company (Tata Consumer Products Limited), Keurig Dr Pepper, Inc., Costa Coffee (The Coca-Cola Company), and The J.M. Smucker Company |

SEGMENTAL ANALYSIS

By Age Group Insights

The 25–39 years age group segment was the largest by accounting for 47.3% of the European speciality coffee market share in 2024, with a confluence of disposable income, urban lifestyles and digital engagement with coffee culture. According to the European Commission’s Digital Economy and Society Index, this demographic spends 12.4 hours per week on social media, where coffee aesthetics, cs lattear t, single origin labels and brewing tutorials are heavily curated and shared. In Germany and Sweden, national barista championships attract over 70% of their audience from this segment as per event attendance data from the Speciality Coffee Association Europe. Their willingness to pay premiums for traceability and experience sustains the economic model of independent roasteries across the continent.

The 18–24 years age group segment is likely to grow with an anticipated CAGR of 11.2% from 2025 to 2033, with early exposure to third wave culture through education, employment and digital immersion. As per the Eurostat Youth Survey 2023, Europeans aged 18 to 24 prioritise ethical consumption, with coffee being the most frequently cited product where they verify farm origin and labour practices. In the Netherlands and Denmark, national youth councils have integrated coffee literacy into civic education workshops focusing on climate justice and fair trade. Additionally, platforms like TikTok and Instagram Reels have made brewing techniques such as AeroPress and cold drip viral among this cohort, with the hashtag #SpecialtyCoffee amassing over 2.3 billion views in Europe in 2023 as tracked by the European Social Media Observatory.

By Distribution Channel Insights

The away-from-home channel segment was the largest by accounting for a dominant share of the European speciality coffee market in 2024, with the experiential and social value embedded in cafe culture. According to the European Coffee Association, over 12500 independent speciality cafes operated across the EU in 2, with average weekly footfall of 1800 customers in metropolitan hubs like London, Berlin and Lisbon. According to the European Foundation for the Improvement of Living and Working Conditions, 52% of remote workers aged 25 to 45 prefer cafes over home offices for productivity and ambient stimulation. Municipal policies also reinforce this trend in Paris and Copenhagen local zoning laws prioritise small food and beverage operators in mixed-use districts to enhance street vitality. This ecosystem of place, skill, and ritual ensures that physical venues remain the primary gateway for speciality coffee engagement.

The retail channel segment is expected to witness the fastest CAGR of 13.5% from 2025 to 2033 with the integration of e-commerce convenience and at-home brewing innovation. According to Eurostat, online grocery and speciality food sales grew by 19.3% in the EU in 2023, with coffee among the top five categories. Brands like Difference Coffee and Kaffeina have partnered with Amazon Fresh and Picnic to offer single-origin capsules and whole beans with QR code traceability. Furthermore, the European Home Appliance Federation notes that sales of precision grinders and pour-over kettles rose by 27% in 2023 as consumers replicate cafe experiences domestically. The European Commission’s Green Public Procurement guidelines now encourage public institutions to source retail-packed speciality coffee for staff rooms, further expanding B2B retail avenues. This shift transforms speciality coffee from an out-of-home indulgence into a daily at-home ritual.

REGIONAL ANALYSIS

Germany Market Analysis

Germany was the top performer of the European speciality coffee market by holding 21.3% of the share in 2024, with its dense urban cafe networks, technical brewing standards and strong import infrastructure. According to the survey, over 2800 speciality cafes operated in Germany in 20,23, with Berlin alone hosting more than 650 certified establishments. The German Barista Championship has produced three world finalists since 2,018, reinforcing a culture of excellence. Additionally, the Federal Environment Agency includes coffee in its circular economy pilot programs with Berlin and Hamburg mandating compostable packaging for all takeaway beverages. Major roasteries such as Five Elephant and Flying Roasters have pioneered direct trade with farms in Guatemala using blockchain for real-time payment verification.

United Kingdom Market Analysis

The United Kingdom speciality coffee market grows with h prominent CAGR during the forecast period. According to the UK Coffee Association, over 4200 speciality cafes operated across the country in 2023, with 68% single-origin pour-over or batch brew options. The Office for National Statistics reports that UK consumers spent 3.1 billion pounds on speciality coffee in 2023, marking a 12% increase from the previous year. London alone hosts seven SCA-certified training campuses and has produced two World Barista Champions. The UK’s post-Brexit Trade and Cooperation Agreement includes streamlined customs for green coffee imports, which benefits small roasters reliant on air freight for freshness.

France Market Analysis

France's speciality coffee market growth is driven by a renaissance in third wave culture, challenging traditional espresso norms. As per the French Coffee Federation, over 210 speciality cafes operated in 2023, many converting historic boulangeries and bookshops into minimalist tasting spaces. French roasters such as Cafés Lomi and Belledonne have pioneered “zero emission” roasting using electric infrared technology powered by renewable grids. Additionally, the Institut National de la Jeunesse reports that 58% of French adults under 35 now prefer filter coffee over traditional espresso. This cultural shift from ritual to exploration defines France’s dynamic speciality trajectory.

Italy Market Analysis

Italy's speciality coffee market growth is likely to grow with a gradual but determined evolution beyond its espresso heritage. The Ministry of Agricultural Policies launched the “Nuovo Caffè Italiano” initiative in 2022 to certify roasters meeting SCA standards and promote origin transparency. Furthermore, the Italian Barista Guild reports that women now represent 52% of certified baristas, with a shift from traditional gender norms.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the notable key players in the European speciality coffee market are

- Starbucks Corporation

- Inspire Brands, Inc.

- F.Gavina and Sons, Inc.

- Barista Coffee

- Coffee Day Enterprises Ltd.

- Blue Bottle Coffee, Inc. (Nestlé S.A.)

- Eight O'Clock Coffee Company (Tata Consumer Products Limited)

- Keurig Dr Pepper, Inc.

- Costa Coffee (The Coca-Cola Company)

- The J.M.. Smucker Company

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the European speciality coffee market are prioritising direct trade relationships that ensure transparency, premium pricing for farmers, and batch-level traceability. Companies are investing in renewable energy-powered roasting facilities and compostable or reusable packaging to align with EU sustainability mandates. Educational initiatives, including barista academies and consumer workshops, are being scaled to build brand loyalty and elevate industry standards. Digital engagement through subscription e-commerce platforms and QR code-enabled storytelling enhances at-home experiences and repeat purchases. Participation in regenerative agriculture projects and carbon insetting programs allows brands to claim verified climate action beyond offsetting. Collaborations with airlines, hotels, and workplaces extend premium coffee into B2B channels while maintaining craft integrity. These strategies collectively shift competition from price to provenance quality and purpose.

COMPETITION OVERVIEW

Competition in the European speciality coffee market is highly fragmented yet intensifying as independent micro roasteries compete with premiumized mainstream brands and digitally native startups. While no single player dominates the landscape, reputation for ethical sourcing, roast precision, and sensory quality determines influence more than volume. The entry barriers are relatively low, ow enabling new cafes to emerge in urban centres, but scaling profitably remains difficult due to rising rent, labour or shortages, and green compliance costs. Differentiation hinges on storytelling, traceability certification, and consumer education, withh leaders investing in training labs, sustainability reports, and origin travel content. At the same time, large foodservice and FMCG companies are launching pseudo craft lines that mimic speciality aesthetics without equivalent supply chain depth, creating market confusion.

TOP PLAYERS IN THE MARKET

- Tim Wendelboe is a pioneering Norwegian speciality coffee company known globally for its uncompromising quality, direct trade model, and influential role in shaping European third wave standards. Based in Oslo, the company operates a roastery cafe and SSCA-certified training campus that attracts professionals from across the continent. Tim Wendelboe sources exclusively from single farms and microlo, ts often visiting producers multiple times per year to co-develop processing methods. In 2,023, the company launched a blockchain-enabled traceability platform, allowing European consumers to view harvest dates, fermentation protocols, and payment details for each bag. It also partnered with Scandinavian Airlines to serve its single-origin brews in premium cabins, enhancing brand visibility across Northern Europe. These initiatives reinforce its reputation as a benchmark for transparency and excellence in the European speciality coffee landscape.

- The Barn is a Berlin-based speciality coffee roastery that has significantly influenced Germany’s craft coffee evolution and served as a catalyst for Central European barista culture. Founded by former World Barista Champion Sophia Hoffmann, the company emphasises light roasting, precision bbrewingand regenerative sourcing. The Barn operates multiple cafes, traininglabss and a central roastery powered entirely by renewable energy. The company also co-founded the European Coffee Equality Collective to promote gender equity in sourcing and hiring. Through its educational outreach and ethicarigouror The Barn has positioned itself as both a commercial brand and a thought leader advancing sustainability and professionalism across the European market.

- Kaffeine is a London-based speciality coffee brand that has played a formative role in the UK’s third wave movement and expanded its influence across Western Europe through training and retail innovation. Originally a flagship cafe on Great Titchfield Street, it now supplies premium beans to over 300 hospitality venues in the UK, France, and the Netherlands. Kaffeine is renowned for its single-origin curation and commitment to female coffee producers, with over 60% of its 2023 lots sourced from wwomen-led cooperatives It also introduced compostable retail packaging lined with plant-based barrier films compliant with the EU Single Use Plastics Directive. These actions demonstrate Kaffeine’s dual focus on education, inclinclusivityand environmental responsibility.

MARKET SEGMENTATION

This research report on the European speciality coffee market has been segmented and sub-segmented based on categories.

By Age Group

- 18–24 Years

- 25–39 Years

- 40–59 Years

- Above 60

By Distribution Channel

- Retail

- Away From Home

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe specialty coffee market?

The Europe specialty coffee market focuses on high-quality, premium-grade coffee beans that score above 80 points, offering unique flavors, origins, and brewing experiences.

2. What factors are driving the growth of the specialty coffee market in Europe?

Key drivers include rising café culture, increasing consumer preference for premium products, growth in home-brewing equipment, and awareness of sustainable and ethical sourcing.

3. Which countries dominate the Europe specialty coffee market?

Germany, the U.K., Italy, France, and the Netherlands are the leading markets due to strong café networks and high per-capita coffee consumption.

4. What types of specialty coffee are popular in Europe?

Popular types include single-origin coffee, Arabica specialty blends, cold brew, organic coffee, and high-scoring micro-lot beans.

5. Which distribution channels are widely used in the Europe specialty coffee market?

The main channels include specialty cafés, coffee roasters, online retail platforms, supermarkets, and subscription-based services.

6. How is sustainability impacting the specialty coffee market in Europe?

Consumers increasingly prefer coffee that is ethically sourced, Fair Trade certified, organic, and produced with transparent supply chains, boosting demand for sustainably produced beans.

7. Who are the major players in the Europe specialty coffee market?

Key players include Starbucks Reserve, Costa Coffee, Nestlé (Blue Bottle Coffee), Lavazza, Tchibo, and various independent specialty roasters across Europe.

8. What role do specialty coffee shops play in market growth?

Specialty cafés educate consumers, promote artisanal brewing methods, and serve as key touchpoints for discovering premium coffee varieties.

9. How is home brewing influencing the specialty coffee market?

The adoption of home espresso machines, grinders, pour-over kits, and pod systems has significantly increased demand for specialty coffee beans and capsules.

10. What challenges does the Europe specialty coffee market face?

Rising raw coffee prices, supply chain disruptions, competition from mainstream brands, and the need for consistent quality standards are major challenges.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com