Europe Surgical Sutures Market Research Report By Product, Application, End User & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis ( 2026 to 2034 )

Europe Surgical Sutures Market Summary

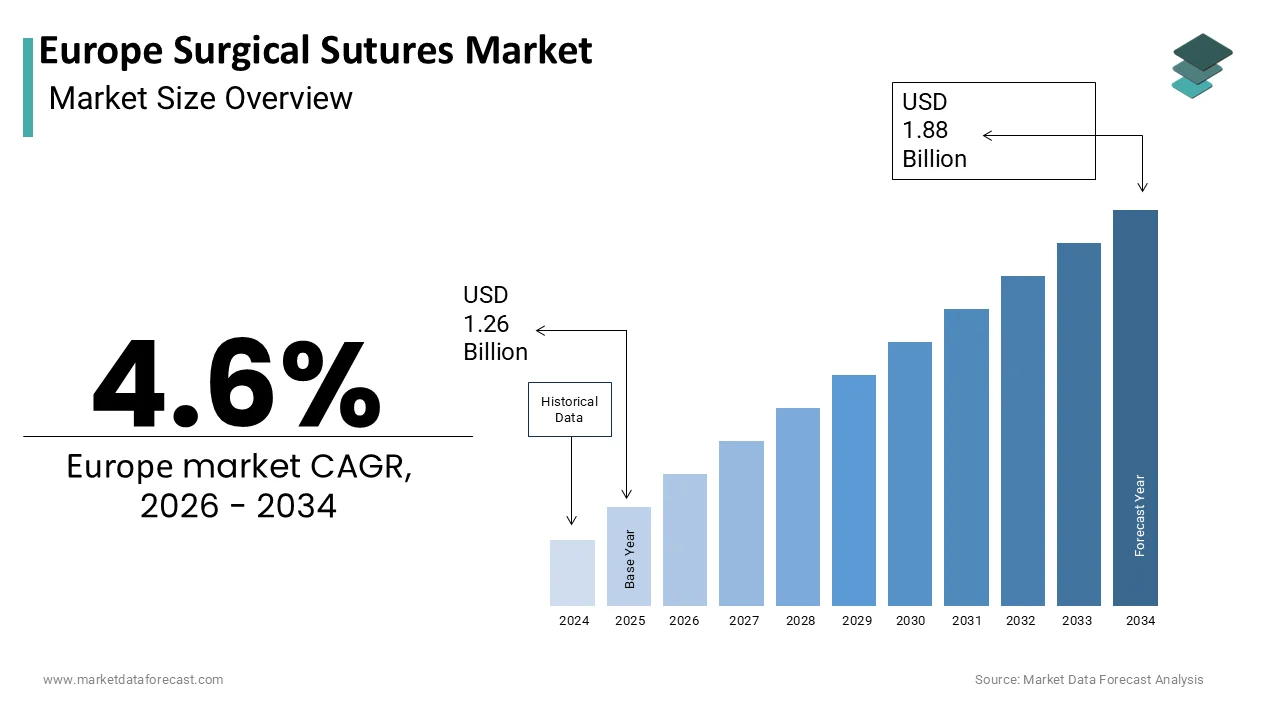

Europe surgical sutures market was valued at USD 1.20 billion in 2024, estimated at USD 1.26 billion in 2025, and is projected to reach USD 1.80 billion by 2033, growing at a CAGR of 4.6% from 2025 to 2033, driven by rising surgical volumes, rapid adoption of minimally invasive and robotic procedures, and increasing demand for absorbable, antimicrobial, and knotless suture technologies across European healthcare systems.

Market snapshot

- 2024 value: USD 1.20 billion

- 2025 (est): USD 1.26 billion

- 2033 forecast: USD 1.80 billion

- CAGR (2025–2033): 4.6%

Quick growth drivers

- Recovery and expansion of elective surgeries across orthopedics, general surgery, and gynecology.

- Rapid uptake of minimally invasive and robotic-assisted procedures is increasing demand for fine monofilament and barbed sutures.

- An aging European population is driving higher volumes of cardiovascular, oncological, and orthopedic surgeries.

- Rising focus on surgical site infection (SSI) prevention is accelerating the adoption of antimicrobial-coated sutures.

- Standardization of synthetic absorbable sutures in national clinical guidelines.

Principal restraints

- Stringent EU Medical Device Regulation (EU MDR 2017/745) is increasing compliance costs and approval timelines.

- Withdrawal of legacy and niche suture products unable to meet updated regulatory requirements.

- Price-focused public procurement systems are limiting the adoption of premium suture technologies.

- Budget constraints across public hospitals are reducing innovation-led purchasing decisions.

High-value opportunities

- Antimicrobial and bioactive sutures integrated into infection prevention protocols.

- Barbed and knotless sutures are gaining adoption in aesthetic, reconstructive, and bariatric surgeries.

- Automated and robotic-compatible suturing devices address surgeon shortages and improve operating room efficiency.

- Demand for sustainable, single-use sterile packaging is aligned with European infection control and environmental policies.

Key operational challenges

- Dependence on non-EU raw material supply chains for absorbable polymer precursors.

- Exposure to geopolitical disruptions and material price volatility.

- Uneven surgeon training and familiarity with advanced suture technologies across regions.

- Complex hospital tendering processes are delaying the adoption of next-generation sutures.

Fastest-growing segments (short)

- Automated suturing devices: 13.8% CAGR — robotic surgery integration and workforce efficiency.

- Gynecological surgeries: 11.5% CAGR — rising cesarean sections and pelvic floor procedures.

- Barbed & antimicrobial sutures: fastest adoption in premium and outpatient procedures.

- Ambulatory & private clinics: 12.9% CAGR — decentralized procurement and faster innovation uptake.

Regional leadership & dynamics

- Germany (25.6% share): the largest market, driven by high surgical volume, domestic manufacturing strength, and early antimicrobial suture adoption.

- France: guideline-driven procurement and strong infection prevention mandates.

- United Kingdom: cost-effectiveness-focused NHS procurement with selective uptake of efficiency-driven sutures.

- Italy & Spain: strong growth in minimally invasive, cosmetic, and gynecological procedures.

What wins commercially

- EU MDR-compliant portfolios backed by strong clinical evidence.

- Integration of sutures into robotic and minimally invasive surgical ecosystems.

- Antimicrobial, barbed, and knotless designs that reduce operative time and complications.

- Surgeon education and training partnershipsare accelerating the adoption of premium products.

Top strategic ask for executives

Invest in EU MDR-ready product pipelines, expand antimicrobial and automated suturing portfolios, strengthen European supply-chain resilience, and scale surgeon training initiatives to accelerate premium product penetration.

Leading players

B. Braun · Ethicon (Johnson & Johnson) · Medtronic · Smith & Nephew · Boston Scientific · W.L. Gore · Conmed · 3M Healthcare · Demetech · Sutures Indi

Europe Surgical Sutures Market Size

The Europe Surgical Sutures Market is projected to grow from USD 1.26 billion in 2025 to USD 1.31 billion in 2026 and reach USD 1.88 billion by 2034, registering a CAGR of 4.6% during the forecast period from 2026 to 2034.

Surgical sutures refer to medical-grade threads used to approximate tissues and facilitate wound healing during surgical and trauma procedures. These are classified as absorbable or non-absorbable and further segmented by material origin, natural,l such as catg, ut, or synthetic, tic like polyglycolic acid, and by structure, monofilament or multifilament. The European medical device market operates under a comprehensive and stringent regulatory framework, with the EU Medical Device Regulation (EU) 2017/745 setting high standards for the safety and performance of all medical devices, including surgical sutures, throughout their lifecycle. Official European data indicate a significant volume of surgical procedures performed annually in EU hospitals, requiring a variety of suture products tailored to diverse clinical needs. Furthermore, an ongoing shift toward procedures that reduce the need for extended hospital stays is evident, with Eurostat data emphasizing a persistent increase in day surgeries and the use of minimally invasive surgery. National health systems across Germany, France, the UK,,ce and the UK prioritize cost-effective yet high-performance sutures due to budgetary constraints, while Nordic countries emphasize sustainability in single-use medical devices. The aging population also plays a role, which increases demand for cardiovascular, orthopedic,c and oncological surgeries that rely heavily on specialized suture materials. These demographic, ic clinical, and regulatory factors collectively define theEuropeane Surgical Sutures Market as a high precision segment within the broader medical device ecosystem.

MARKET DRIVERS

Rising Volume of Elective and Minimally Invasive Surgeries

The post pandemic recovery of elective procedures and the rapid adoption of minimally invasive techniques are primary drivers for the European surgical sutures market. According to research, surgical volumes in many EU hospitals continued their significant recovery trajectory in 2023, with ongoing efforts to address substantial backlogs of elective operations across specialties such as orthopedics, cataract surgery, and hernia repair. These procedures often require fine monofilament sutures that minimize tissue drag and inflammation. Laparoscopic and robotic surgeries are experiencing a continuous and significant increase in adoption due to enhanced techniques and improved patient outcomes, creating a steady demand for specialized surgical tools. In Germany, the adoption of robotic-assisted prostatectomies is increasing rapidly, becoming the predominant surgical approach due to demonstrated benefits such as reduced blood loss and shorter hospital stays. The UK's National Health Service has focused on increasing surgical activity and outpatient efficiency to tackle care backlogs, which in turn accelerates the demand for streamlined surgical supplies and products compatible with faster recovery protocols. This procedural resurgence, combined with technological shifts toward less invasive access, directly drives consumption of high-value engineered sutures across both public and private healthcare settings.

Aging Population and Associated Comorbidities Driving Complex Surgical Needs

The region’s rapidly aging demographic intensifies demand for advanced sutures capable of managing compromised tissue integrity and prolonged healing, which in turn propels the expansion of the European surgical sutures market. According to research, the proportion of older people within the EU population has been steadily increasing for decades, driven by lower fertility rates and increased life expectancy. This cohort faces higher rates of cardiovascular disease, cancer, and osteoarthritis, all requiring intricate surgical interventions. As per sources, a large number of coronary artery bypass grafts and valve replacement procedures are performed in Europe annually, with surgical guidelines often recommending durable, non-absorbable sutures for vascular connections to ensure long-term integrity. Similarly, the incidence of colorectal cancer is increasing among younger adult populations in many European countries, prompting ongoing clinical discussion and research into optimal surgical techniques, including the appropriate type of suture material for different surgical conditions. Elderly patients often exhibit reduced collagen synthesis and impaired microcirculation, which requires sutures with minimal tissue reactivity. These clinical complexities elevate the need for premium suture materials that support secure wound closure in high-risk populations, sustaining market growth beyond basic procedural volume.

MARKET RESTRAINTS

Stringent Regulatory Requirements Under EU MDR 2017 745

The implementation of the European Union Medical Device Regulation has significantly increased the administrative and technical burden for suture manufacturers seeking market access. This impedes the growth of the European surgical sutures market. Under the EU Medical Devices Regulation (MDR), all surgical sutures, classified as Class IIa or higher medical devices, must undergo rigorous clinical evaluation and conformity assessment by independent Notified Bodies, a process that reflects a significant increase in review duration and complexity compared to the previous Medical Devices Directive (MDD). As per various studies, a considerable number of legacy suture products have been withdrawn from the EU market since 2021 due to manufacturers' inability to meet the updated, stricter biocompatibility, sterilization, and clinical documentation requirements of the EU MDR. Small and medium enterprises face disproportionate challenges. According to sources, many small and medium-sized enterprises (SMEs) have experienced significant delays in new surgical suture launches due to the substantial resource constraints and increased complexity involved in compiling the extensive MDR-compliant technical files. This regulatory friction extends time to market, increases compliance costs, and limits the availability of niche or specialized suture variants, particularly for rare surgical applications.

Cost Containment Pressures in Public Healthcare Systems

National health services across the region are implementing aggressive procurement strategies that prioritize price over innovation and thereby slow down the expansion of the European surgical sutures market. This constrains the adoption of premium suture technologies. According to sources, European healthcare systems increasingly utilize centralized procurement models and various price control mechanisms for medical devices and consumables to manage costs and improve efficiency. The UK’s NHS, like other national health systems, primarily uses cost-minimization strategies in procurement, but these processes prioritize modern, clinically effective synthetic suture materials over outdated natural options like catgut. Regional health authorities in Spain operate within budget constraints and implement strategies to consolidate product lines and manage the introduction of higher-cost, advanced surgical technologies. These austerity measures discourage investment in next-generation suture development and disincentivize the use of evidence-based premium products that could reduce long term complications and readmissions, which ultimately limits market value growth despite rising procedural volumes.

MARKET OPPORTUNITIES

Integration of Antimicrobial and Bioactive Sutures in Infection Prevention Protocols

The growing threat of surgical site infections offers a potential opportunity for the growth of the European surgical sutures market. This creates a new pathway for a high-value opportunity for advanced suture technologies embedded with antimicrobial agents. Surgical site infections represent a significant burden on healthcare systems, leading to increased morbidity, prolonged hospital stays, and elevated mortality risk across the EU. Evidence from various studies indicates that using triclosan-coated sutures may help reduce the risk of surgical site infections in patients. Health authorities in Germany emphasize adherence to evidence-based infection prevention bundles. These policy endorsements, combined with the EU’s One Health Action Plan against antimicrobial resistance, create a regulatory and clinical tailwind for bioactive sutures, which transforms infection control from a cost center into a quality and safety imperative.

Adoption of Barbed and Knotless Sutures in Aesthetic and Reconstructive Surgery

The expansion of plastic reconstructive and bariatric surgery segments is accelerating the uptake of knotless barbed sutures that enhance procedural efficiency and aesthetic outcomes. This, in turn, generates fresh prospects for the expansion of the European surgical sutures market. The number of cosmetic surgical procedures is consistently increasing globally, with key organizations like the International Society of Aesthetic Plastic Surgery (ISAPS) reporting a steady rise in both surgical and nonsurgical interventions over recent years. Barbed sutures eliminate knot tying, reducing operative time. The field of post-bariatric body lifting procedures is a growing area of plastic surgery, with ongoing advancements and evolving surgical techniques, including the use of innovative suture materials, aimed at improving patient outcomes and scar appearance. Besides, the European Wound Management Association endorsed knotless sutures for diabetic foot reconstruction due to uniform tension distribution and reduced tissue necrosis. As patient expectations for minimal scarring and faster recovery rise, these advanced sutures are transitioning from niche to standard in high-visibility surgical fields.

MARKET CHALLENGES

Supply Chain Vulnerability to Raw Material Sourcing and Geopolitical Disruptions

Persistent risk from concentrated global supply chains for critical raw materials such as poliglecaprone and polydioxanone, which are synthesized from petrochemical derivatives primarily sourced from Asia, thereby hampering the growth of the European surgical sutures market. The European medical device industry recognizes a significant dependency on non-EU countries for critical raw materials and precursors used in products like absorbable sutures. Official EU assessments have increasingly emphasized the medical supply chain's susceptibility to global disruptions, identifying a strategic need to enhance domestic production capacity and diversify sourcing options. Geopolitical factors and stricter environmental policies in major producing nations, such as China, have been contributing to volatility in the supply and cost of key chemical intermediates used in medical manufacturing. European producers rely on just-in-time inventory models, leaving a minimal buffer against such disruptions. This dependency undermines supply security and complicates compliance with the EU’s push for resilient medical device supply chains under the Pharmaceutical Strategy for Europe.

Limited Surgeon Training on Advanced Suture Technologies

Inconsistent adoption persists due to gaps in surgical education and procedural familiarity, which holdback the expansion of the European surgical sutures market. General surgery residency programs are increasingly incorporating training on a variety of advanced synthetic suture materials, though the specific curriculum may still vary across institutions and regions. Surgeon preference for suture materials is influenced by a combination of factors, including clinical evidence, patient outcomes, procedure type, and individual surgeon familiarity or training with specific materials. In public hospitals across Italy and Greece, budget constraints limit access to simulation labs where new suture techniques could be practiced. This knowledge gap results in suboptimal suture selection, increasing risks of dehiscence infection or scarring, and slows market penetration of premium products. The successful integration of innovative surgical technologies, such as advanced sutures, into routine clinical practice generally depends on widespread, consistent education and practical training programs for surgical teams.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By ProductApplication, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Johnson & Johnson Inc., Braun Melsungen AG, Smith & Nephew PLC, Demetech Corporation, Conmed Corporation, W.L. Gore & Associates, Boston Scientific Corporation, 3M Healthcare, Medtronic Inc., and Sutures India Pvt Ltd. |

SEGMENTAL ANALYSIS

By Product Insights

The absorbable sutures segment dominated the European Surgical Sutures Market by holding a 42.5% share in 2025. The dominance of the absorbable sutures segment is driven by its essential role in internal tissue approximation, where suture removal is impractical or undesirable. Absorbable sutures are the standard of care for internal soft tissue closure in Europe due to their predictable degradation profile and reduced need for secondary interventions. These materials maintain tensile strength for several days, which aligns with the critical wound healing phase, before hydrolyzing into harmless metabolites. National clinical guidelines in Germany and France explicitly recommend synthetic absorbables over catgut due to superior consistency and lower inflammatory response. This entrenched clinical protocol, reinforced by decades of surgical training and outcome data, ensures sustained dominance acrosshigh-volumee procedural categories. Synthetic absorbable sutures offer superior batch-to-batch consistency and biocompatibility compared to traditional chromic catgut, aligning with EU Medical Device Regulation requirements. The European Pharmacopoeia establishes rigorous quality standards, including strict limits on bacterial endotoxins and residual monomers, for absorbable polymers and other materials used in medicinal products and medical devices. Adherence to these strict purity requirements necessitates robust quality control and advanced manufacturing processes across all material types, ensuring product safety and efficacy. These safety and regulatory advantages, coupled with the elimination of bovine sourcing concerns associated with catgut, have driven near universal adoption in public hospitals where risk mitigation is paramount.

The automated suturing devices segment is expected to exhibit a noteworthy CAGR of 13.8% from 2025 to 2033 due to integration into robotic and minimally invasive surgical platforms, and addressing surgical workforce shortages through procedural efficiency. Automated suturing systems are increasingly embedded in robotic surgery ecosystems to enhance precision and reduce operative time. These devices are particularly valuable in confined anatomical spaces, such as pelvic reconstructive surgery, where manual dexterity is limited. Europe faces a critical shortage of experienced surgeons. Automated suturing devices mitigate this gap by standardizing complex closure techniques and reducing reliance on manual skill. In public hospitals across Italy and Spain, these systems enable faster turnover without compromising outcomes. This convergence of workforce constraints, training efficiency, and policy support positions automated devices as a strategic response to Europe’s evolving surgical care demands.

By Application Insights

The general surgeries segment held the largest share of 38.2% of the European surgical sutures market in 2025. The leading position of the general surgeries segment is credited to the high volume of abdominal soft tissue and gastrointestinal procedures performed annually across the region. General surgery encompasses a wide range of high-frequency interventions, including appendectomies, herniarepairss, and colorectal resections, all of which require multiple suture types. These procedures typically use a combination of non-absorbable sutures for fascial closure and absorbable sutures for subcuticular layers. Besides, the rising prevalence of obesity drives demand for bariatric and reflux surgeries that require specialized high-strength sutures. This procedural volume, combined with standardized suture protocols, ensures general surgery remains the cornerstone of suture consumption. Unlike specialized applications, general surgeries benefit from comprehensive and consistent reimbursement across all EU health systems. According to sources, a number of member states provide full coverage for essential general surgical procedures under statutory health insurance. This financial accessibility sustains high procedural volumes even during economic downturns. National clinical pathways specify suture types by procedure, creating predictable demand patterns for manufacturers. This institutionalization of suture selection within publicly funded care systems guarantees stable and substantial consumption in the general surgery segment.

The gynecological surgeries segment is predicted to witness the highest CAGR of 11.5% during the forecast period, owing to demographic and clinical trends. Cesarean delivery rates continue to climb across Europe. Each cesarean requires multiple suture types, typically absorbable for uterine closure and subcuticular skin closure. Besides, the aging female population drives demand for pelvic organ prolapse and stress urinary incontinence surgeries. These procedures rely onhigh-strength non-absorbablee sutures like polyester for ligament fixation. This dual demographic and procedural momentum fuels accelerated suture demand in gynecology. Modern gynecological care emphasizes minimal scarring, rapid recovery, and preservation of fertility, which favors advanced suture technologies. In aesthetic gynecology, a rapidly emerging field, barbed poliglecaprone sutures are used for labiaplasty and vaginal rejuvenation to eliminate knots and improve cosmesis. Evolving patient demands and the rise of outpatient gynecological procedures drive the increasing need for outcome-focused suture options, which in turnpropels market expansion in this area.

By End User Insights

The hospitals segment led the European surgical sutures market by accounting for a substantial share in 2025. The supremacy of the hospitals segment is because of the central role of hospitals as the primary site for surgical care across publicly funded European health systems. National health services in Germany, France, and the UK operate centralized procurement systems that bundle suture purchases across hospital networks, creating massive scale demand. Even in countries with robust ambulatory surgery centers, complex and high-risk procedures, such as cardiovascular or oncological resections, remaihospital-boundnd due to regulatory and safety requirements. This institutional concentration ensures that hospitals dictate suture specifications, drive formulary decisions, and represent the primary channel for new product adoption across the region. Hospitals operate under strict EU and national mandates for sterility traceability and infection prevention that shape suture selection. Besides, the EU Medical Device Regulation requires hospitals to maintain full implant registers, including suture lot numbers for post market surveillance, a requirement that favors pre-sterilized single-use kits over bulk supplies. National health authorities in Sweden and the Netherlands have banned reusable suture reels in operating rooms, which mandates individually packaged sterile units to reduce cross-contamination risk. These regulatory frameworks make hospitals not just volume leaders but also quality and compliance gatekeepers in the suture market.

The other end-usersegment is estimated to register the fastest CAGR of 12.9% over the forecast period. The swift growth of the other end-usersegment is fuelled by a shift toward outpatient and aesthetic surgical procedures, and regulatory flexibility and direct procurement models. Ambulatory surgery centers across Western and Northern Europe are expanding rapidly to accommodate demand for same-day procedures. These facilities favor premium preloaded sutures with integrated needles for efficiency and sterility assurance. In aesthetic medicine, specialized clinics in Spain and Italy use barbed and monofilament sutures for facelifts and body contouring, often purchasing directly from distributors due to the absence of centralized procurement. This decentralization of surgical care, driven by patient convenience and cost containment, is reshaping suture distribution and product preferences. Unlike public hospitals bound by tender restrictions, ambulatory centers and private clinics exercise greater autonomy in suture selection. The direct procurement bypasses price-focused group purchasing organizations, enabling faster adoption of high-value products. Besides, EU regulations permit specialized clinics to use CE-marked sutures without the extensive documentation required in hospitals, lowering entry barriers for premium brands. The healthcare industry continues to delegate low-risk procedures to non-hospital settings, and this trend is driving rapid growth in the agile and innovative segment that caters to these procedures.

COUNTRY LEVEL ANALYSIS

Germany Surgical Sutures Market Analysis

Germany was the top performer in the European surgical sutures market and accounted for a 25.6% share in 2025. The supremacy of the German market is driven by its status as the region’s most populous nation and a leader in surgical volume and medical technology adoption. The country performs millions of surgical procedures annually, with a high proportion of complex cardiovascular and oncological interventions that demand premium suture materials. Germany’s statutory health insurance system covers a portion of the population and enforces stringent quality standards through the Federal Joint Committee’s benefit assessments, which influence the formularies nationwide. Leading manufacturers like B Braun and Ethicon maintain major R&D and production facilities in Germany, ensuring close alignment with clinical needs. The National Antibiotic Resistance Strategy also promotes antimicrobial sutures in high-risk surgeries, which drives the adoption of advanced products. This combination of procedural scale, regulatory sophistication, and domestic manufacturing presence solidifies Germany’s position as the anchor market for surgical sutures in Europe.

France Surgical Sutures Market Analysis

France was the next prominent country in the European surgical sutures market and held a 18.6% share in 2025. The growth of the French market is propelled by its centralized healthcare system and strong emphasis on clinical guidelines. The National Authority for Health issues binding recommendations on suture selection, such as the mandatory use of triclosan-coated sutures in colorectal operations, which directly shape national procurement. France also hosts major suture innovators like Medtronic’s surgical division, which collaborates with academic hospitals on clinical trials for next-generation materials. The country’s universal health coverage ensures consistent surgical access, while its aging population sustains demand for high complexity procedures. These institutional and demographic factors make France a high-volume, guideline-driven market with significant influence on EU-wide suture standards.

United Kingdom Surgical Sutures Market Analysis

The United Kingdom is another key player in the European surgical sutures market, owing to a publicly funded National Health Service that prioritizes cost-effectiveness alongside clinical outcomes. The National Institute for Health and Care Excellence provides evidence-based guidance on suture use, recently endorsing barbed sutures for abdominal wall closure due to reduced operative time. The UK’s exit from the EU has led to dual regulatory compliance requirements under UKCA and CE marking, increasing complexity for suppliers but also creating opportunities for tailored product offerings. Apart from these, the UK has a high density of specialized surgical centers in oncology and trauma, driving demand for niche suture types. Budget limitations are an obstacle to premium product uptake, but the drive to decrease surgical site infections and readmissions offers a strategic entry point for cost-effective suture solutions.

Italy Surgical Sutures Market Analysis

Italy is moving ahead steadfastly in the European surgical sutures market, with regional disparities in healthcare delivery and a growing emphasis on surgical innovation in the North. The national health service reimburses all essential surgeries, but regional authorities manage procurement independently, leading to varied suture formularies. Northern hospitals increasingly adopt robotic and laparoscopic techniques, accelerating demand for fine monofilament and barbed sutures. Italy also has a high rate of cosmetic and reconstructive surgery, creating a robust private market for premium sutures. This duapublic-privatete dynamic, combined with rising surgical volumes in an aging population, ensures steady suture demand with growing sophistication in advanced segments.

Spain Surgical Sutures Market Analysis

Spain is likely to grow notably in the European surgical sutures market from 2025 to 2033 due to a universal public healthcare system and expanding private surgical care. Regional health services manage procurement through centralized tenders that prioritize price, yet tertiary hospitals in Madrid and Barcelona lead in adopting antimicrobial and high-strength sutures for complex cases. Spain also exhibits one of Europe’s highest cesarean section rates, which sustains demand for absorbable sutures in obstetrics. The private clinic sector, particularly in aesthetic and dental surgery, is growing rapidly. This blend of public volume and private innovation positions Spain as a dynamic and evolving market with strong growth potential in specialized suture categories.

TOP LEADING PLAYERS IN THE MARKET

- B Braun is a German multinational medical technology company with deep roots in the European Surgical Sutures Market. The company offers a comprehensive portfolio of absorbable and non-absorbable sutures under its Aesculap brand, known for high precision and biocompatibility. B Braun emphasizes innovation in monofilament and antimicrobial sutures tailored to European surgical standards and regulatory expectations. In recent years, the company has strengthened its position by launching triclosan-coated polydioxanone sutures compliant with EU MDR and expanding its single-use sterile packaging to meet hospital infection control protocols. Globally, B. Braun supplies surgical sutures to over 60 countries and integrates suture solutions into its broader surgical portfolio, including instruments and energy devices,s enhancing its value proposition in operating rooms worldwide.

- Ethicon is a global leader in surgical care and a major force in the European Surgical Sutures Market with a legacy of pioneering synthetic absorbable and barbed suture technologies. The company’s portfolio includes Vicryl Polysorb and PDS II sutures, widely used in European hospitals for their predictable absorption profiles and strength retention. Ethicon has reinforced its European presence by aligning its product labeling and clinical documentation with EU Medical Device Regulation requirements and by conducting multicenter trials across Germany, France, and the UK to validate infection reduction claims for its antimicrobial sutures. Globally, hiThicon’snovations in knotless and rrobotic-compliant suturesset industry benchmarks, and its distribution network ensures rapid access to advanced suture solutions in both developed and emerging markets.

- Medtronic is a leading global healthcare technology company with a significant footprint in the European Surgical Sutures Market through its Surgical Innovations division. The company provides a range of high-performance sutures, including specialized products for cardiovascular, eurosurgical a, nd minimally invasive procedures. Medtronic has enhanced its European competitiveness by integrating sutures into its broader ecosystem of surgical staplers, energy devices,s and robotics, enabling seamless procedural workflows. Recent actions include updating its suture sterilization and traceability systems to comply with EU MDR and launching educational programs for surgeons on advanced suturing techniques in collaboration with European surgical societies. Medtronic’s global scale and commitment to outcome-driven solutions position it as a key contributor to suture innovation and adoption across diverse clinical settings worldwide.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European Surgical Sutures Market focus on regulatory compliance by aligning product documentation and clinical evidence with the EU Medical Device Regulation 2017 745 requirements. They invest in antimicrobial and barbed suture technologies to address surgical site infection prevention and procedural efficiency. Companies integrate sutures into broader surgical ecosystems, including robotics and energy devices, to enhance workflow compatibility. Strategic collaborations with European surgical societies and teaching hospitals support clinical validation and surgeon training. Additionally,lly they prioritize sustainable sterile packaging and digital traceability to meet hospital procurement and infection control mandates across national health systems.

COMPETITIVE LANDSCAPE

The European Surgical Sutures Market features intense competition among a few global leaders and specialized regional manufacturers. Differentiation is driven not by price but by clinical performance and regulatory compliance with modern surgical workflows. Multinational companies leverage extensive clinical data portfolios and established hospital relationships to maintain formulary positions while navigating stringent EU MDR requirements. Barriers to entry remain high due to the need for long term biocompatibility studies, es notified body certification, and hospital tender participation. However, niche players thrive in segments like aesthetic surgery or veterinary sutures where agility and customization matter more than scale. Competition is further shaped by national procurement policies that balance cost containment with quality mandates, especially in infection prevention. As robotic and minimally invasive surgeries grow,w companies that offer compatible advanced sutures gain a strategic advantage, fostering continuous innovation in material science and delivery systems across the European landscape.

KEY MARKET PLAYERS

Companies playing a leading role in the europe surgical sutures market profiled in the report are

- Johnson & Johnson Inc.

- Braun Melsungen AG

- Smith & Nephew PLC

- Demetech Corporation

- Conmed Corporation

- W.L. Gore & Associates

- Boston Scientific Corporation

- 3M Healthcare

- Medtronic Inc.

- Sutures India Pvt Ltd.

MARKET SEGMENTATION

This research report on the European surgical sutures market has been segmented and sub-segmented into the following categories.

By Product

- Sutures

- Absorbable Sutures

- Non-Absorbable Sutures

- Automated Suturing Devices

By Application

- Surgeries

- General Surgeries

- Gynecological Surgeries

- Orthopedic Surgeries

- Ophthalmic Surgeries

- Other Applications

By End User

- Hospitals

- Other End-Users

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What are the key drivers of the Europe Surgical Sutures Market and why is demand for the Europe Surgical Sutures Market increasing?

The Europe Surgical Sutures Market is primarily driven by demographic aging, the growing burden of chronic diseases, and the corresponding rise in cardiovascular, orthopedic, and general surgeries requiring reliable wound closure. In addition, higher healthcare expenditure, technological advancements in suture materials, and increasing awareness about the role of sutures in reducing post‑operative complications are pushing hospitals and surgical centers to purchase more advanced products, thereby accelerating demand in the Europe Surgical Sutures Market.

2. Which countries dominate the Europe Surgical Sutures Market and how is the Europe Surgical Sutures Market distributed regionally?

Within the Europe Surgical Sutures Market, countries such as Germany, the U.K., France, Italy, and Spain account for a major share due to their large patient populations, developed hospital networks, and strong presence of global medical device manufacturers. Germany and the U.K. often lead the Europe Surgical Sutures Market in terms of revenue and procedure volume, while emerging markets in Eastern and Southern Europe show rising demand as healthcare infrastructure and insurance coverage improve.

3. What product segments are included in the Europe Surgical Sutures Market and how do they shape the Europe Surgical Sutures Market outlook?

The Europe Surgical Sutures Market typically includes absorbable sutures, non‑absorbable sutures, monofilament and multifilament products, as well as synthetic and natural materials tailored for specific types of tissue and procedures. Growth in the Europe Surgical Sutures Market is especially strong for advanced absorbable and antimicrobial sutures that support faster healing, reduced infection risk, and better handling characteristics in minimally invasive and conventional surgeries.

4. How do minimally invasive and robotic surgeries impact the Europe Surgical Sutures Market and future demand in the Europe Surgical Sutures Market?

The rising adoption of minimally invasive and robotic‑assisted procedures increases the need for precise, high‑performance sutures, positively influencing the Europe Surgical Sutures Market by pushing demand for thinner, stronger, and more biocompatible materials. As hospitals upgrade surgical capabilities, the Europe Surgical Sutures Market benefits from a shift toward premium products that enable smaller incisions, shorter recovery times, and lower complication rates, supporting both clinical outcomes and economic efficiency.

5. Who are the major players in the Europe Surgical Sutures Market and how do they compete within the Europe Surgical Sutures Market?

Key companies in the Europe Surgical Sutures Market include multinational leaders such as Johnson & Johnson’s Ethicon, B. Braun Melsungen AG, Medtronic, and Smith & Nephew, alongside several regional manufacturers. Competition in the Europe Surgical Sutures Market centers on product performance, innovation in absorbable and antimicrobial sutures, pricing strategies, distribution strength, and the ability to navigate diverse regulatory and tendering environments across European countries.

6. What are the main challenges and restraints facing the Europe Surgical Sutures Market and how do they affect the Europe Surgical Sutures Market growth?

The Europe Surgical Sutures Market faces challenges from stringent EU MDR regulations, complex national reimbursement systems, price pressure from competitive tenders, and raw material cost volatility. These factors can delay product launches and compress margins in the Europe Surgical Sutures Market, while the availability of alternative wound closure methods, such as staples and tissue adhesives, creates additional competitive pressure even though sutures remain the preferred standard in many procedures.

7. How is the aging population influencing the Europe Surgical Sutures Market and long‑term demand in the Europe Surgical Sutures Market?

Europe’s aging population leads to higher incidence of chronic diseases such as cardiovascular disorders, osteoarthritis, and cancers, which in turn drive more surgical interventions and directly increase consumption in the Europe Surgical Sutures Market. Over the long term, this demographic shift ensures a stable pipeline of elective and emergency surgeries, making the Europe Surgical Sutures Market structurally attractive as hospitals plan for sustained demand in cardiac, orthopedic, and general surgery departments.

8. What role do regulations and EU MDR play in the Europe Surgical Sutures Market and how do they shape the Europe Surgical Sutures Market landscape?

The Europe Surgical Sutures Market is governed by strict medical device regulations and the EU MDR framework, which impose rigorous clinical, safety, and quality requirements for all suture products sold in the region. While compliance costs can be high, these regulations increase trust and transparency in the Europe Surgical Sutures Market, favoring established manufacturers with strong quality systems and supporting widespread adoption of advanced, clinically validated products.

9. What are the major trends in materials and technology within the Europe Surgical Sutures Market and how are they transforming the Europe Surgical Sutures Market?

Technological innovation in the Europe Surgical Sutures Market includes the development of bioabsorbable polymers, coated sutures, antimicrobial threads, and products designed to minimize tissue trauma and improve knot security. These advancements not only enhance clinical performance but also help hospitals in the Europe Surgical Sutures Market reduce infection rates, shorten hospital stays, and align with value‑based healthcare initiatives focusing on quality and cost efficiency.

10. How do alternative closure technologies affect the Europe Surgical Sutures Market and competitive dynamics in the Europe Surgical Sutures Market?

Alternatives such as surgical staples, clips, and tissue adhesives exert competitive pressure on the Europe Surgical Sutures Market, especially in specific procedures where speed or cosmetic outcomes are prioritized. Nonetheless, the Europe Surgical Sutures Market continues to grow because sutures offer versatility, cost‑effectiveness, and proven reliability across a wide variety of open and minimally invasive surgeries, keeping them integral to standard surgical practice.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com