Europe Tequila Market Size, Share, Trends & Growth Forecast Report, By Product Type (Blanco, Joven, Mixto Gold, Reposado, Anejo, Extra Anejo), Purity, Price Range, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis From (2025 To 2033)

Europe Tequila Market Size

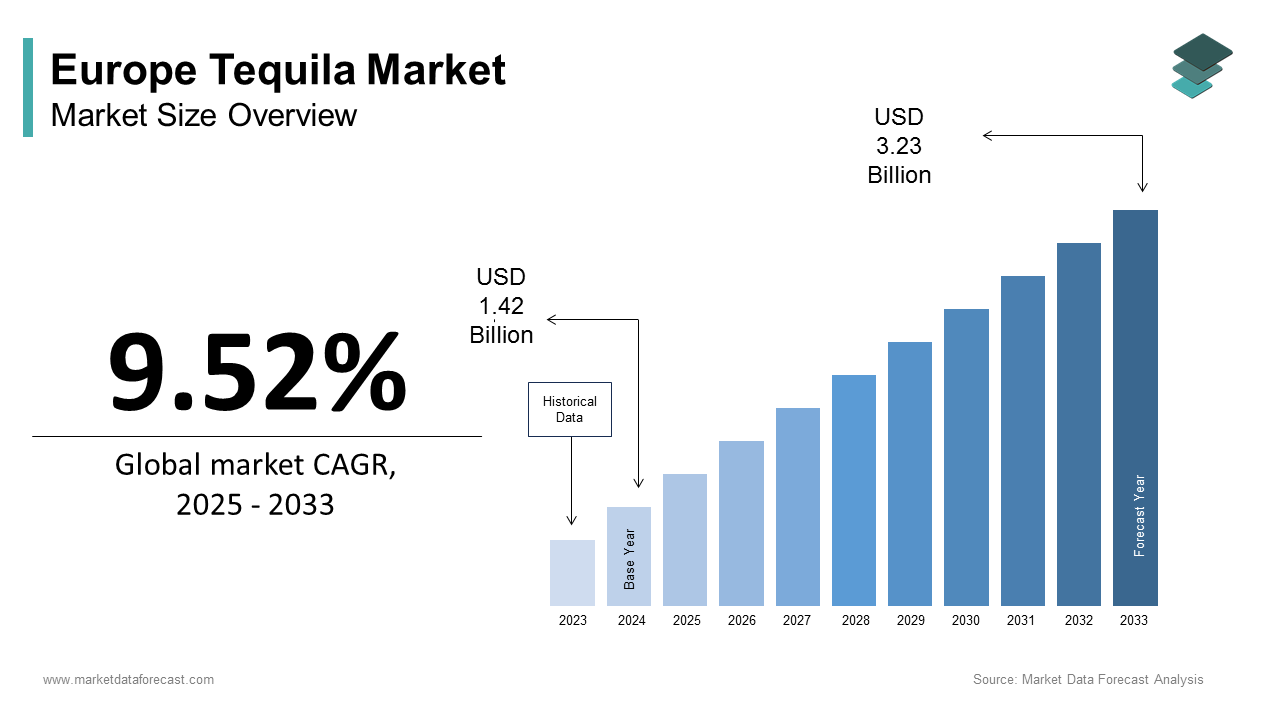

The Europe tequila market size was calculated to be USD 1.42 billion in 2024 and is anticipated to be worth USD 3.23 billion by 2033, from USD 1.56 billion in 2025, growing at a CAGR of 9.52% during the forecast period.

Tequila is a distilled spirit made exclusively from blue agave, specifically the Weber variety, grown in designated regions of Mexico and certified by the Tequila Regulatory Council. Unlike generic agave spirits, genuine tequila carries a protected geographical indication recognized by the European Union since 1997 to ensure strict production and labeling standards. Europe’s engagement with tequila has evolved from niche bar curiosity to mainstream premium spirits category, driven by cocktail culture, experiential consumption, and growing consumer literacy about agave terroir. According to Eurostat, the European Union imported tens of millions of liters of tequila in 2023, which reflects sustained double‑digit growth over the past five years. This rise coincides with broader shifts in drinking behaviour. As per the World Health Organization’s European Health Report, per‑capita alcohol consumption in high‑income EU countries has declined since 2010, yet premium spirit categories such as tequila have expanded, signaling a quality‑over‑quantity trend. Furthermore, the European Commission’s Geographical Indications Register (2023) lists tequila among the top non‑European products subject to frequent enforcement actions against counterfeit goods, which indicates both strong demand and regulatory vigilance. These dynamics position tequila not merely as an imported spirit but as a culturally resonant, legally protected, and increasingly sophisticated segment of Europe’s premium beverage landscape, where consumer preference, regulatory frameworks, and authenticity converge to drive growth.

MARKET DRIVERS

Premiumization and Cocktail Culture Drive Demand Among Urban Consumers

The premiumization trend across Europe is one of the key factors propelling the growth of the European tequila market. The expansion of high‑end cocktail bars and consumer interest in craft mixology have fundamentally reshaped tequila’s perception in Europe from a party shot to a sippable and terroir‑driven spirit. According to the European Bartenders Federation, cities like London, Berlin, and Barcelona now host over 1,200 bars certified by the Tequila Matchmakers Guild, which is elevating consumer expectations and driving tequila’s premium positioning. As per a 2024 study by the University of Gastronomic Sciences in Italy, 68% of European consumers aged 25 to 40 associate reposado and añejo tequilas with complexity and authenticity, preferring them neat or in minimal cocktails, which strengthens demand for premium variants. According to the International Wine and Spirit Record, the premium segment now accounts for 52% of all tequila value sales in Western Europe, highlighting the shift toward premiumization. As per HM Revenue and Customs, premium tequila volumes in the UK grew by 29% in 2023, outpacing all other spirit categories, which indicates its rapid adoption. Spain’s Ministry of Agriculture documented a 40% increase in tequila‑based cocktail mentions on restaurant menus between 2021 and 2023, positioning Madrid as a hub for agave innovation. This cultural repositioning, fueled by education, urban nightlife, and sensory sophistication, transforms tequila into a symbol of informed consumption rather than casual indulgence.

Growing Consumer Awareness of Authenticity and Geographical Indication Protection

The growing consumer emphasis on authenticity is another key driver supporting the expansion of the European tequila market. European consumers are increasingly discerning about product origin and authenticity, a trend amplified by the EU’s robust geographical indication framework. According to the European Commission’s 2024 Intellectual Property Enforcement Report, customs authorities seized over 1,200,000 liters of counterfeit “tequila‑style” spirits in 2023, up 18% from 2022, which demonstrates both illicit demand and institutional protection. As per surveys by the European Consumer Organisation, 74% of spirits purchasers in Germany and France now check for the official “Tequila” NOM number and certified seal before buying, reinforcing consumer vigilance and trust. Carrefour France reported a 33% sales uplift in certified 100% agave bottles after introducing shelf labeling that explains agave content, showing the direct impact of educational campaigns on consumer purchasing behavior. This convergence of regulatory clarity, consumer vigilance, and brand transparency strengthens demand for legitimate tequila while marginalizing imitations and reinforcing its premium positioning across European markets.

MARKET RESTRAINTS

Stringent EU Alcohol Labeling and Health Warning Regulations Increase Compliance Burden

One of the primary restraints facing the European tequila market is the stringent regulatory standards governing alcohol labeling and health warnings, which impose substantial compliance costs on brand owners. The European Union’s evolving alcohol labeling regime imposes significant operational and financial constraints on tequila importers and producers. According to Regulation (EU) No 1169/2011, mandatory ingredient listing and nutritional declarations for all alcoholic beverages above 1.2% ABV took full effect in December 2023, which requires tequila producers to reformulate labels for each market. As per the European Spirits Organisation, adapting packaging for 27 national languages and regulatory interpretations costs an average of €185,000 per brand annually, creating a substantial compliance burden. Moreover, Ireland’s Public Health (Alcohol) Act 2018 mandates cancer risk warnings and calorie counts on all alcohol containers, serving as a template for similar laws in France and the Netherlands. These requirements conflict with Mexico’s Denomination of Origin regulations that prohibit health claims on tequila labels, forcing costly dual labeling or market withdrawal. This regulatory fragmentation undermines standardization and inflates go‑to‑market expenses, particularly for small and midsize producers. The high compliance costs and regulatory inconsistencies act as significant restraints on tequila’s European market expansion.

Limited Consumer Understanding of Agave Spirit Categories Beyond Tequila

The lack of consumer education on agave spirits is another restraint impeding the growth of the European tequila market. Despite rising tequila consumption, European consumers exhibit significant confusion between tequila, mezcal, and other agave spirits, leading to misattribution and market distortion. According to a 2024 pan‑European survey by the European Beverage Association, 61% of consumers believe mezcal is a subtype of tequila, while 44% assume any smoky agave spirit is tequila, showing widespread misconceptions. As per the UK’s Wine and Spirit Education Trust, only 12% of certified mixologists can accurately distinguish between blanco tequila and joven mezcal in blind tastings, highlighting structural gaps in sensory education. Without coordinated EU‑level classification standards or mandatory category separation at the point of sale, tequila risks being subsumed into a generic “agave spirit” bucket, eroding its distinct identity and value proposition. The consumer confusion and lack of education restrain tequila’s premiumization potential in Europe.

MARKET OPPORTUNITIES

Expansion of E‑commerce and Direct‑to‑Consumer Channels for Premium Bottles

The growing adoption of e‑commerce and direct‑to‑consumer channels is a significant opportunity for the European tequila market. The liberalization of alcohol e‑commerce across Europe has unlocked new avenues for premium tequila brands to bypass traditional retail gatekeepers and engage directly with connoisseurs. According to the European Court of Justice’s 2023 ruling in Case C‑215/22, licensed online retailers can ship spirits across member states, provided they comply with excise and age verification rules. As per Eurostat, online spirits sales in the EU grew by 22% in 2023, with tequila outperforming the category average at 37% growth, which indicates its digital momentum. Germany’s Alko Online reported that customers who purchase premium tequila online spend 2.8 times more per transaction than in physical stores, highlighting higher engagement levels. This channel democratizes access to authentic, high‑end tequila while fostering a community of informed enthusiasts across borders. The rapid growth of e‑commerce channels that provide tequila brands with direct consumer engagement and expansion opportunities for the European tequila market.

Integration into Sustainable and Ethical Consumption Narratives

The development of sustainability and ethical consumption narratives offers another promising avenue for European tequila market expansion. Tequila producers are increasingly aligning with Europe’s strong ethical consumption ethos by emphasizing agave sustainability, water stewardship, and fair labor practices. According to the European Commission’s 2023 Sustainable Food System Framework, consumers are encouraged to support products with verifiable environmental and social credentials, which tequila brands leverage through certifications like B Corp and Fair Trade. Patrón Spirits achieved B Corp status in 2023 after reducing water usage by 42% per liter of tequila, verified by the Rainforest Alliance, demonstrating a measurable sustainability impact. Systembolaget in Sweden reported a 28% sales increase for certified tequila brands in 2023, prioritizing shelf placement for spirits with third‑party sustainability validation. The Tequila Regulatory Council’s “Agave Sustainability Program” has enrolled over 1,200 producers in soil conservation and biodiversity initiatives, strengthening transparency for EU importers. As European shoppers increasingly link indulgence with responsibility, these narratives transform tequila from a luxury import into a conscious choice, opening premium pricing power and brand loyalty.

MARKET CHALLENGES

Vulnerability to Agave Supply Volatility and Climate‑Related Production Risks

The vulnerability of agave supply to climate volatility is primarily challenging the European tequila market. Blue Weber agave requires 7 to 10 years to mature, making supply planning highly inflexible, and recent climate disruptions have exacerbated shortages. According to Mexico’s Ministry of Agriculture, prolonged droughts in Jalisco reduced agave yields by 23% in 2023, the lowest harvest since 2017. Agave piña prices have surged by 68% over two years, forcing producers to raise retail prices or compromise on aging, which risks alienating European consumers accustomed to stable quality. As per the European Spirits Association’s 2024 risk bulletin, prolonged agave shortages could lead to increased use of diffuser technology, which some connoisseurs argue undermines traditional flavor profiles. Without diversified cultivation or climate‑resilient agave variants, Europe’s growing demand remains tethered to ecological fragility in a single Mexican region, creating structural supply chain risk. Justification: The climate‑driven agave shortages are directly challenging tequila’s supply stability and pricing in Europe and challenging the expansion of this regional market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 9.52% |

| Segments Covered | By Product Type, Purity, Price Range, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | José Cuervo, Patrón Spirits International, Don Julio, Sauza Tequila, Olmeca Tequila, Herradura, Espolon Tequila, 1800 Tequila, Casamigos Tequila, El Jimador |

SEGMENTAL ANALYSIS

By Product Type Insights

The blanco segment dominated the Europe tequila market by holding 38.7% of the market in 2024. The dominance of the blanco segment in this European market is attributed to its dual appeal as both a cocktail foundation and a pure expression of agave terroir. According to the European Bartenders Federation, more than 70% of tequila‑based cocktails served in certified craft bars in London, Berlin, and Madrid use blanco as the base spirit. As per the UK’s Wine and Spirit Trade Association, 100% agave blanco sales grew by over 30% in 2023, driven by demand for transparency and authenticity. Blanco requires no aging, enabling producers to meet surging demand without inventory lag, ensuring a consistent supply to Europe’s dynamic on‑trade and off‑trade channels. This segment is expected to remain dominant over the forecast period as mixology trends and consumer preference for authenticity sustain growth.

The extra añejo segment is anticipated to grow at a promising CAGR of 14.2% over the forecast period in the European market. The repositioning of extra añejo from niche curiosity to the luxury sipping category is supporting the growth of this segment in this European market. According to Mexico’s Tequila Regulatory Council, less than 3% of total tequila production qualifies as extra añejo, creating natural exclusivity. As per Swiss trade data, sales of extra añejo tequilas priced above €120 increased significantly in 2023, reflecting demand among affluent consumers. Luxury brands such as Don Julio 1942 and Clase Azul have invested in artisanal decanters and storytelling around master distillers, aligning with Europe’s luxury gifting culture. This segment is expected to expand rapidly over the forecast period as rarity, craftsmanship, and premium positioning drive adoption.

By Purity Insights

The 100% agave tequila segment held the leading position in the Europe tequila market in 2024 and occupied 82.5% of the regional market share. The dominance of the 100% agave segment in this European market is driven by consumer preference for transparency and authenticity, reinforced by EU labeling laws. According to the European Consumer Organisation, more than three‑quarters of spirits purchasers in France and Germany actively avoid mixto products, associating them with artificial additives. As per major importers such as La Maison du Whisky and The Whisky Exchange, only 100% agave expressions are stocked due to customer demand for purity. Regulatory alignment also plays a role; the EU’s Protected Geographical Indication for tequila mandates that only 100% agave products can be labeled simply as “tequila.” This segment is expected to remain dominant over the forecast period as legal frameworks and cultural consensus sustain demand.

The 100% agave tequila segment is expected to register the fastest CAGR of 12.8% over the forecast period in the European market. The collapse of the mixto segment and continuous elevation of 100% agave into higher price tiers are propelling the growth of this segment in this European market. According to Spain’s Ministry of Agriculture, 94% of tequila imports in 2023 were 100% agave, up from 76% in 2019. As per Eurostat, tequila tasting rooms and specialty bars across Europe have expanded, normalizing 100% agave as a sipping spirit. Sustainability narratives also center on agave purity, with producers emphasizing support for traditional jimadores and avoidance of industrial neutral spirits. This segment is expected to expand robustly over the forecast period as regulatory legitimacy and consumer preference reinforce growth.

By Price Range Insights

The premium and super premium tequila segment captured 54.1% of the Europe tequila market share in 2024. The dominance of this segment in the European market is attributed to the shift toward quality over quantity consumption, where drinkers prioritize craftsmanship and provenance. According to HM Revenue and Customs, more than 60% of tequila value sales in the UK in 2023 fell within the €30–75 price range. As per the German Bartenders Association, most certified cocktail venues stock multiple super premium tequilas for mixing and neat service. France’s Caves Legrand reported that the majority of tequila sales by value occur between €35 and €65, where consumers perceive maximum flavor return per euro. This segment is expected to remain dominant over the forecast period as accessibility and prestige sustain demand.

Theultra-premiumm tequila segment is anticipated to exhibit a CAGR of 15.6% over the forecast period in the European market. Luxury gifting, collector behavior, and experiential consumption are favoring the growth of the ultra premium segment in this European market. According to Swiss and Swedish customs data, ultra premium tequila sales doubled between 2021 and 2023, with collectible editions gaining traction among high net worth consumers. As per luxury retailers such as Harrods and KaDeWe, dedicated tequila sections and masterclasses have been introduced to cater to demand. Handcrafted bottles, numbered editions, and artisanal presentation reinforce tequila’s positioning as a luxury collectible. This segment is expected to expand rapidly over the forecast period as wealth resilience and cultural capital drive premiumization.

REGIONAL ANALYSIS

United Kingdom Tequila Market Analysis

The United Kingdom led the market and accounted for 22.4% of the European market share in 2024. The dominance of the UK in the European market is driven by its cocktail culture, open import regime, and dynamic retail landscape. According to HM Revenue & Customs, UK tequila imports rose sharply in 2023, reflecting strong demand for premium agave spirits. London’s vibrant bar scene, with hundreds of craft cocktail venues, has elevated tequila’s profile, while major retailers such as Waitrose and Selfridges promote the category through tasting events and pairing guides. The UK Tequila Importers Association confirms that the majority of imports are 100% agave, underscoring consumer preference for authenticity. This ecosystem of professional advocacy, retail education, and regulatory agility positions the UK as Europe’s tequila gateway.

Spain Tequila Market Analysis

Spain had a substantial share of the European tequila market in 2024 owing to the cultural ties to Mexico, culinary integration, and supportive regulation. According to the Spanish Ministry of Culture, tequila festivals and agave‑focused bars in Madrid and Barcelona highlight Spain’s role as a consumption hub. Customs data show reposado and añejo tequilas account for a higher share of imports compared to the EU average, reflecting consumer preference for sipping styles. Spanish chefs increasingly integrate tequila into modern cuisine, expanding its role beyond cocktails. The Spanish Agency for Consumer Affairs enforces strict labeling rules, ensuring only authentic tequila reaches consumers. Spain is expected to remain both a large and qualitative benchmark for tequila consumption in Europe.

Germany Tequila Market Analysis

Germany is expected to account for a prominent share of the European tequila market over the forecast period due to its large population, rising cocktail sophistication, and strong ethical consumption values. According to Destatis, tequila imports into Germany grew significantly in 2023, with most being 100% agave. A survey by the German Consumer Protection Agency found that sustainability factors such as water use and farming practices influence purchasing decisions among premium spirit buyers. Organic retailers like Alnatura highlight brands with B Corp certification or carbon‑neutral distillation. Germany’s hospitality schools also incorporate spirits training, ensuring bartenders understand tequila’s nuances. Germany is expected to remain a volume leader with premium integrity.

France Tequila Market Analysis

France accounted for a considerable share of the European tequila market in 2024. The connoisseurship, terroir appreciation, and luxury positioning are propelling the French tequila market expansion. According to La Maison du Whisky, France stocks hundreds of tequila expressions, with strong growth in single‑estate highland blancos. Michelin‑starred restaurants in Paris increasingly offer tequila pairings, aligning the spirit with fine dining. France’s DGCCRF enforces strict geographical indication compliance, blocking counterfeit products at ports. French media outlets such as Revue du Vin de France regularly feature agave spirits, legitimizing tequila within the national oenological discourse. France is expected to sustain its role as a luxury‑driven market for tequila.

Netherlands Tequila Market Analysis

The Netherlands is anticipated to account for a noteworthy share of the European tequila market over the forecast period due to its role as a logistics hub, progressive drinking culture, and retail education. According to the Dutch Ministry of Infrastructure and Water Management, Rotterdam’s port handles a significant share of tequila imports into the EU, enabling efficient distribution. Statistics Netherlands reports high trial rates among younger adults, reflecting openness to new spirits. Amsterdam’s cocktail scene emphasizes agave tastings, while liberal advertising laws allow brands to engage directly with consumers. Retailers such as Gall & Gall provide detailed tasting notes and agave maps, demystifying tequila for newcomers. The Netherlands is expected to remain a critical launchpad for tequila brands entering Northern and Central Europe.

COMPETITION OVERVIEW

The Europe tequila market features intense yet nuanced competition among multinational spirits conglomerates, independent premium brands, and Mexican producers seeking direct entry. Unlike volume-driven markets, European success hinges on authenticity, storytelling, and alignment with local drinking cultures—favoring brands that invest in education, sustainability, and sensory sophistication over aggressive pricing. Multinationals like Bacardi and Diageo dominate through distribution scale and luxury positioning, while agile players such as Clase Azul or Don Julio gain traction via artisanal narratives and limited editions. Regulatory compliance—particularly around labeling, ingredients, and geographical indication—is non-negotiable, creating high barriers for uncertified entrants. Competition is further shaped by national preferences: Spain values sipping culture, the UK drives cocktail innovation, and Germany prioritizes ethical production. As consumer literacy grows, the market rewards transparency, terroir expression, and cultural respect, making authenticity the ultimate differentiator in an increasingly discerning landscape.

KEY MARKET PLAYERS

A few major players of the Europe tequila market include

- Jose Cuervo

- Patrón Spirits International

- Don Julio

- Sauza Tequila

- Olmeca Tequila

- Herradura

- Espolòn Tequila

- 1800 Tequila

- Casamigos Tequila

- El Jimador

Top Strategies Used by the Key Market Participants

Key players in the Europe tequila market are investing in bartender education and mixology partnerships to embed tequila in premium cocktail culture across major urban centers. They are emphasizing 100% agave authenticity through transparent labeling aligned with EU geographical indication standards to build consumer trust. Companies are leveraging sustainability narratives by highlighting water conservation, agave farming, G ethics, and carbon-neutral logistics to resonate with environmentally conscious European buyers. Strategic collaborations with luxury retailers duty duty-free operators, and fine dining establishments position tequila as a sophisticated sipping spirit rather than a casual shot. Additionally, brands are tailoring ultra-premium and limited-edition offerings to Europe’s gifting and collector segments, reinforcing exclusivity and cultural relevance.

Leading Players in the Europe Tequila Market

Bacardi Limited

Bacardi Limited is a global spirits leader that significantly influences the Europe tequila market through its ownership of Patrón and its strategic distribution network across the continent. The company has elevated tequila’s premium positioning by aligning Patrón with luxury experiences, sustainability, and craftsmanship. In Europe, Bacardi partners with high-end bars, Michelin restaurants, and duty-free retailers to showcase Patrón’s 100% agave heritage. In 2024, the company achieved B Corp certification for Patrón’s Jalisco distillery, emphasizing water stewardship and ethical labor practices, a move that resonated strongly with environmentally conscious European consumers. Bacardi also launched immersive agave education programs for bartenders in London, Paris, and Madrid, reinforcing authenticity and driving category growth. These initiatives solidify Bacardi’s role as both a commercial force and a cultural ambassador for premium tequila in Europe.

Diageo plc

Diageo plc plays a pivotal role in the Europe tequila market through its ownership of Casamigos, the brand co-founded by George Clooney, which has become a symbol of approachable luxury. Diageo leverages its extensive pan-European logistics and retail relationships to ensure Casamigos is available from premium supermarkets to airport lounges. Recognizing Europe’s emphasis on transparency, Diageo has enhanced Casamigos’ labeling with clear agave origin and production details tailored to EU regulatory expectations. In 2023, the company expanded its ultra-premium Casamigos Añejo offering across Germany and the Nordics in response to rising demand for sipping tequilas. Diageo also collaborates with European mixologists to develop region-specific cocktails, blending local flavors with tequila’s profile. These localized, premium-focused strategies position Casamigos as a lifestyle brand deeply integrated into Europe’s social and culinary fabric.

Pernod Ricard SA

Pernod Ricard SA contributes to the Europe tequila market through its strategic partnership with the Avión tequila brand and its commitment to responsible premiumization. The French group utilizes its deep-rooted relationships with European regulators, retailers, and hospitality groups to promote Avión as a refined 100% agave spirit suited for both cocktails and neat consumption. In 2024, Pernod Ricard integrated Avión into its “Good Times from a Good Place” sustainability platform, highlighting agave conservation and carbon-neutral shipping to EU markets. The company also launched limited edition bottles in collaboration with European artists, strengthening emotional connection with urban consumers in cities like Barcelona and Berlin. By aligning tequila with European values of craftsmanship, sustainability, and moderation, Pernod Ricard bridges Mexican tradition with continental sensibilities, enhancing tequila’s long-term appeal beyond fleeting trends.

MARKET SEGMENTATION

This research report on the Europe tequila market has been segmented and sub-segmented based on product type, purity, price range, and region.

By Product Type

- Blanco

- Joven

- Mixto Gold

- Reposado

- Anejo

- Extra Anejo

By Purity

- 100% Tequila

- 60% Tequila

By Price Range

- Premium Tequila

- Value Tequila

- Premium and Super-Premium Tequila

- Ultra-Premium Tequila

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe tequila market?

The Europe tequila market refers to the production, import, distribution, and consumption of tequila across European countries, driven mainly by premium spirit demand.

2. What factors drive the growth of the Europe tequila market?

Rising consumer preference for premium and super-premium spirits, cocktail culture expansion, and increasing interest in agave-based alcoholic beverages support market growth.

3. Which countries lead tequila consumption in Europe?

The United Kingdom, Germany, Spain, France, and Italy are the leading tequila-consuming countries in Europe.

4. Which tequila type dominates the Europe market?

100% agave tequila holds a dominant share due to growing consumer awareness of quality and authenticity.

5. What are the key distribution channels in the Europe tequila market?

On-trade channels, such as bars and restaurants, and off-trade channels, including supermarkets, specialty liquor stores, and online platforms.

6. What role does premiumization play in market growth?

Premiumization drives higher value sales as consumers shift toward aged and craft tequila varieties.

7. How does cocktail culture influence the Europe tequila market?

The rising popularity of tequila-based cocktails in urban nightlife and hospitality venues significantly boosts demand.

8. What challenges affect the Europe tequila market?

Supply constraints of blue agave, price volatility, and strict labeling and import regulations impact market expansion.

9. What impact do regulations have on tequila sales in Europe?

Protected designation of origin rules and EU alcohol regulations ensure product authenticity but can increase compliance costs.

10. How does sustainability affect tequila demand in Europe?

Eco-friendly production practices and sustainable agave sourcing positively influence purchasing decisions among environmentally conscious consumers.

11. What role does e-commerce play in the Europe tequila market?

Online retail channels enhance accessibility, brand visibility, and premium product availability across regions.

12. Which end-use segment contributes most to market revenue?

The hospitality sector contributes significantly due to high tequila consumption in bars, clubs, and restaurants.

13. How does brand awareness impact the market?

Strong brand heritage and marketing strategies improve consumer trust and drive repeat purchases.

14. What trends are shaping the Europe tequila market?

Growth in flavored tequila, craft distilleries, celebrity-backed brands, and low-additive premium offerings.

15. What is the future outlook for the Europe tequila market?

The market is expected to grow steadily, supported by premium spirit trends, evolving consumer tastes, and expanding distribution networks.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com