Europe Warehousing Market Size, Share, Trends and Growth Forecasts Research Report, Segmented By Warehouse Type, End-Use and Country – Industry Analysis (2026 to 2034)

Europe Warehousing Market Summary

Market Snapshot

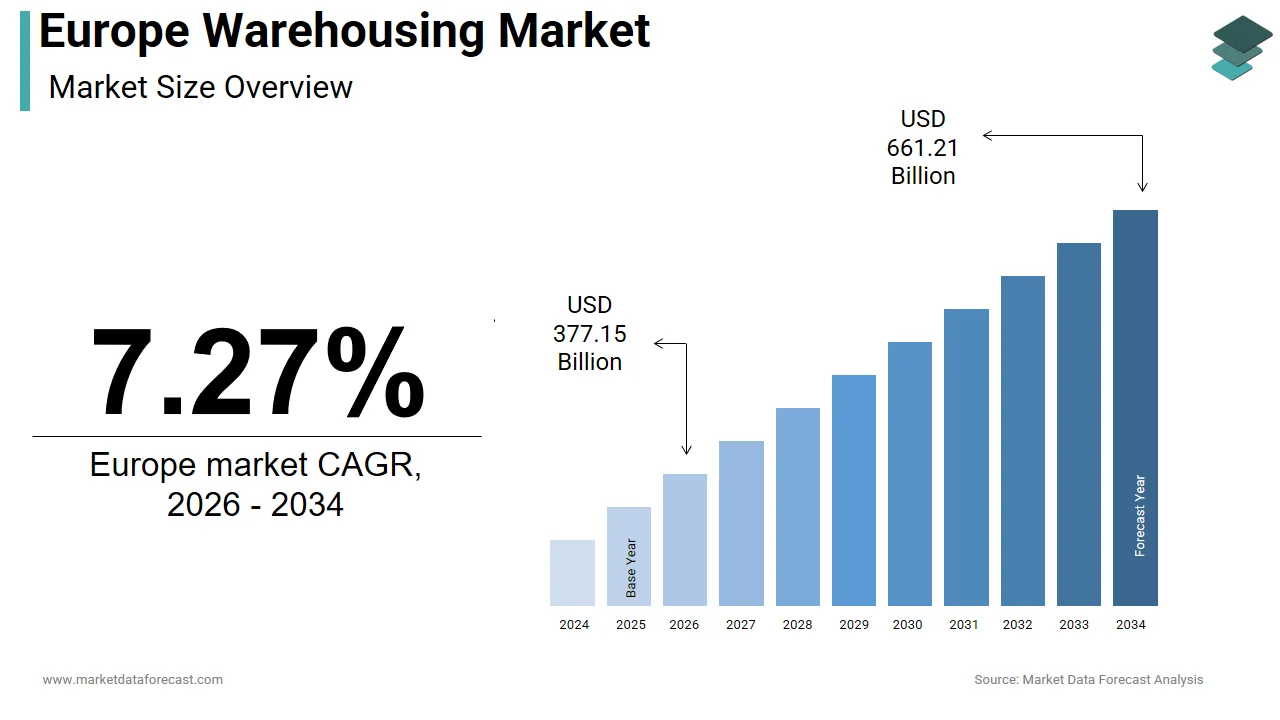

- Market size reached USD 377.15 billion in 2025

- Expected to expand to USD 661.21 billion by 2034

- Growth momentum sustained at 7.27% CAGR (2026 to 2034)

Why the Market Is Expanding

- Warehousing demand is rising alongside e-commerce order volumes

- Urban logistics hubs are gaining importance for faster delivery timelines

- Intra-EU trade flows are increasing reliance on regional distribution centers

Structural Market Shifts

- Transition from traditional storage to high-throughput fulfillment centers

- Greater use of automation, digital inventory systems, and smart layouts

- Sustainability retrofits are becoming standard across logistics assets

Supply-Side Constraints

- Limited availability of developable land in Western Europe

- Persistently low vacancy rates in prime logistics corridors

- Skilled labor shortages are affecting warehouse productivity

Regulatory & Cost Pressures

- EU climate and energy regulations are increasing development costs

- Mandatory adoption of energy-efficient building standards

- Longer permitting timelines for large logistics facilities

Growth Pockets

- Rising investment in brownfield and legacy warehouse redevelopment

- Increasing integration of renewable energy infrastructure

- Expansion of cold chain and specialized logistics facilities

Regional Market Leaders

- Germany dominates due to its central location and industrial base

- United Kingdom is driven by high online retail penetration

- Netherlands benefits from port-centric and multimodal logistics

- Poland is emerging as a key Central European distribution hub

Competitive Landscape

- Market led by global logistics real estate developers and 3PL providers

- Competition focused on sustainability, strategic locations, and flexibility

- Long-term leases are common with e-commerce and retail tenants

- Leading players include: Prologis, Goodman Group, SEGRO, Deutsche Post AG, GEODIS, Kuehne+Nagel, P. Moller-Maersk, Lineage, Inc., XPO, Inc., and Ryder System, Inc.

Europe Warehousing Market Size

The size of the Europe warehousing market was worth USD 377.15 billion in 2025. The regional market is anticipated to grow at a CAGR of 7.27% from 2026 to 2034 and be worth USD 661.21 billion by 2034 from USD 377.15 billion in 2026.

Warehousing functions as a critical backbone of the continent’s integrated supply chain ecosystem, facilitating storage, inventory optimization, and rapid distribution across industrial and consumer sectors. As of early 2025, Savills’ European Logistics Market Overview (2024) reports that Europe’s modern logistics stock exceeds 100 million square meters, with a majority concentrated in Germany, the United Kingdom, France, and the Netherlands. Urban densification has driven the conversion of obsolete industrial zones into logistics hubs, while the EU Green Deal mandates have accelerated sustainability retrofits across the sector. According to CBRE’s Logistics Market Report, the prime logistics vacancy rate in Western Europe remained exceptionally low in Q4 2024, which is signalling a persistent demand‑supply imbalance. This evolving landscape reflects a shift from static storage facilities to dynamic, technology‑enabled distribution nodes embedded within responsive supply networks, positioning logistics real estate as a strategic backbone of Europe’s trade, e‑commerce, and industrial modernization.

MARKET DRIVERS

Accelerated E‑Commerce Penetration Fuels Demand for Last Mile Warehousing

The rapid expansion of online retail across Europe has fundamentally altered logistics architecture by necessitating proximity‑based warehousing near urban consumption hubs, which is primarily boosting the warehousing market growth in Europe. According to Statista (2024), online sales accounted for 15% of total retail trade in the EU, up from around 9% in 2019. This shift has driven the proliferation of micro‑fulfillment centers and urban logistics hubs, with cities like Berlin, Paris, and Madrid witnessing, as per JLL (2024), a 20% year‑on‑year rise in sub‑10,000 square meter lease transactions. According to the Universal Postal Union’s State of the Postal Sector Report (2023), parcel volumes in Europe exceeded 11 billion units, which reflects sustained growth in e‑commerce deliveries. Consequently, retailers and third‑party logistics providers are increasingly converting underutilized retail spaces and light industrial units into high‑throughput fulfillment nodes. The average lead time expectation for urban deliveries has contracted to under 24 hours in markets such as the Netherlands and Sweden, compelling operators to maintain buffer inventory closer to end consumers. This reconfiguration of inventory placement strategies has elevated demand for small‑scale, flexible warehousing solutions that support rapid order processing and returns handling.

Expansion of Cross‑Border Trade Within the EU Reinforces Regional Distribution Requirements

The deepening integration of European supply chains has amplified demand for strategically located transshipment and consolidation centers that facilitate seamless intra‑EU trade, which is further propelling the European warehousing market growth. According to the European Commission’s Annual Trade Report (2024), more than two‑thirds of goods produced within the bloc cross at least one internal border before reaching final consumers. This interdependence has elevated the importance of logistics nodes in Central and Eastern Europe, where countries like Poland and the Czech Republic recorded, as per the International Transport Forum (2024), an 18% increase in cross‑border freight traffic between 2022 and 2024. The Pan‑European Transport Corridors, particularly Corridor X connecting Salzburg to Thessaloniki, have become critical arteries for inventory movement, prompting developers to construct multimodal logistics parks within 30 kilometers of key interchanges. According to Cushman & Wakefield (2024), Poland recorded nearly 6 million square meters of leased warehouse space, accounting for 59% of all agreements finalized in Central and Eastern Europe. Such developments highlight how regulatory harmonization, customs simplification, and infrastructure alignment under the EU Single Market continue to drive structural demand for warehousing assets that support agile, multi‑country fulfillment strategies.

MARKET RESTRAINTS

Chronic Shortage of Skilled Logistics Labor Constrains Operational Scalability

Despite robust capital investment in warehouse infrastructure, Europe faces a persistent deficit in qualified logistics personnel, which is directly limiting throughput capacity and automation adoption and hampering the European market growth. According to the European Labour Authority (2025), transport and storage are among the top five sectors facing acute shortages, with Germany and Italy accounting for a significant share of the gap. High employee turnover rates, averaging as per the International Labour Organization’s World Employment Outlook (2024) close to 30% annually in Southern Europe, further exacerbate operational instability. This labor constraint discourages operators from fully leveraging complex automated systems that demand specialized technical oversight. Vocational education pipelines have not kept pace with technological advancements, according to CEDEFOP (2024). Fewer than 20% of logistics training programs across the EU incorporate digital warehouse management competencies. Without coordinated public‑private upskilling initiatives, labor scarcity will continue to cap productivity gains and delay the transition toward next‑generation fulfillment models.

Stringent Environmental Regulations Impose Cost and Design Limitations on New Developments

Europe’s ambitious climate mitigation agenda has introduced significant compliance burdens for warehousing developers seeking planning permissions and operational certifications, which further impede the regional market growth. According to Directive (EU) 2024/1275 on the Energy Performance of Buildings, all new non‑residential buildings must meet nearly zero‑energy standards. Meeting these benchmarks requires extensive integration of photovoltaic panels, heat recovery systems, and electric vehicle charging infrastructure, increasing upfront construction costs as per RICS Global Construction Monitor (2024) by 10–15% compared to conventional builds. Moreover, several countries, including the Netherlands and Denmark, have implemented binding circularity requirements that compel developers to source at least 30% of building materials from recycled or bio‑based origins. These stipulations lengthen permitting timelines and restrict site selection to locations with adequate renewable energy access and waste diversion capacity. In France, for instance, new logistics projects exceeding 10,000 square meters must undergo a full life‑cycle assessment before approval according to the AGEC Law (2024).

MARKET OPPORTUNITIES

Retrofitting Legacy Warehouses for Modern E‑Commerce Fulfillment Presents a Strategic Growth Avenue

A vast inventory of underutilized industrial buildings across Europe offers untapped potential for the European warehousing market. According to the European Environment Agency (2024), more than 230 million square meters of post‑war industrial real estate remains in use or vacant, with over 40% structurally adaptable for logistics repurposing. Cities such as Turin, Lyon, and Rotterdam have launched brownfield redevelopment incentives that reduce permitting fees by up to 30% for projects incorporating sustainability upgrades. Retailers like Zalando and Ocado have already capitalized on this trend, converting former manufacturing plants into automated micro‑fulfillment facilities in Milan and Brussels, respectively. According to the World Green Building Council (2024), the reuse of existing foundations and roof structures can lower embodied carbon by up to 50% compared to new builds.

Integration of Renewable Energy Infrastructure Within Warehousing Assets Enhances Long‑Term Viability

On‑site renewable energy generation is emerging as a critical value driver for warehousing operators seeking to mitigate volatile utility costs and satisfy tenant sustainability criteria, and can be a potential opportunity for the European warehousing market. According to Prologis (2024), more than 65% of new logistics leases in Germany and the Netherlands included clauses requiring landlords to provide verified renewable power. Solar photovoltaic systems installed on warehouse rooftops now achieve, as per SolarPower Europe (2024), average generation capacities of 1–1.2 MW per 30,000 square meter facility, sufficient to power all internal operations and electric yard equipment. Major logistics landlords such as Goodman and Logicor have committed to equipping 100% of their European portfolios with rooftop solar by 2027, a move projected to offset, according to SolarPower Europe (2024), more than 1 million metric tons of CO2 annually.

MARKET CHALLENGES

Fragmented National Land Use Policies Hinder Pan‑European Network Optimization

The absence of harmonized zoning regulations across European countries is a major challenge to the European warehousing market growth. While the EU promotes free movement of goods, land allocation for logistics remains governed by divergent national and municipal frameworks that impose inconsistent density, height, and environmental thresholds. According to the European Landowners’ Organization (2024), warehouse height restrictions range from 12 meters in parts of southern Italy to 24 meters in the Netherlands. In France, a single logistics development may require clearances from up to seven different administrative bodies, extending project timelines by 9 to 14 months as per CBRE France (2024).

Geopolitical Instability and Energy Volatility Undermine Operational Continuity and Cost Predictability

Ongoing geopolitical tensions, particularly those affecting Eastern Europe and critical maritime chokepoints, have introduced new layers of risk into warehousing operations through energy supply disruption and cost inflation, which is further challenging the warehousing market growth in Europe. According to the European Commission’s Quarterly Gas Market Report (Q4 2024), EU natural gas prices averaged €50/MWh at year‑end, around 40% higher than the 2019 baseline. Countries bordering conflict zones have experienced intermittent grid instability, prompting logistics operators in Romania and Slovakia to invest in backup diesel generators at an average cost of €200,000 per site as per the European Investment Bank’s Supply Chain Resilience Report (2024). Additionally, insurance premiums for warehouse assets in high‑risk corridors have risen by 20–30% since 2023, according to Lloyd’s of London (2024).

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Warehouse Type, End-use, and County. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Deutsche Post AG, BrightKey, Inc., GEODIS, Goodman Group, NIPPON EXPRESS HOLDINGS, INC., FedEx, RXO Inc., XPO, Inc., Ryder System, Inc., Prologis, Mitsubishi Logistics Corporation, H. Robinson Worldwide, Inc., SEGRO, Americold Logistics, Inc., Lineage, Inc., Kuehne+Nagel, P. Moller – Maersk, NewCold, and Others. |

SEGMENTAL ANALYSIS

By Warehouse Type Insights

The general warehousing segment dominated the Europe warehousing market and held 65.4% of the European warehousing market share in 2024. The dominance of the general warehousing segment in the European warehousing market can be credited to the segment’s versatility in accommodating a broad spectrum of goods across diverse sectors, including retail, automotive, and consumer electronics, which do not require temperature control or specialized handling infrastructure. General warehouses serve as foundational nodes for industries dealing with durable and non-perishable goods, which represent the majority of Europe’s industrial output. According to Eurostat, non-food consumer goods comprised a majority share of intra-EU trade volume in 2024, which is reinforcing reliance on flexible and multi-tenant logistics spaces. The rise of omnichannel retail has further amplified demand, according to the European Retail Roundtable. A large majority of European retailers operate hybrid fulfillment models that blend store inventory with centralized warehouse stock. This operational model favours general-purpose facilities capable of handling mixed SKUs with scalable racking systems. Additionally, the relatively lower capital expenditure for constructing non-climate-controlled spaces makes general warehousing economically attractive for both developers and tenants seeking rapid deployment.

The specialized warehousing segment is emerging as the fastest-growing segment in the Europe warehousing market and is predicted to expand at a CAGR of 8.24% over the forecast period, owing to the stringent regulatory demands and consumer preferences favouring perishable, temperature-sensitive, and high-value goods. Automated systems are essential to maintaining temperature-controlled environments without human intervention, which risks thermal breaches. According to the European Commission’s Directorate General for Health and Food Safety, a substantial share of food sold in the EU is classified as chilled or frozen, representing hundreds of billions of euros in retail value. This necessitates expanded cold chain capacity, according to the Global Cold Chain Alliance, and additional temperature-controlled space required across the EU over the medium term. Pharmaceutical logistics further intensify demand, according to the World Health Organization and the European Medicines Agency, vaccine and biologics distribution requiring 2-to-8-degree Celsius storage throughout the supply chain. These compliance imperatives render specialized warehousing non-optimal for critical sectors.

By End Use Insights

The retail segment commanded the highest share of 40.8% of the regional market in 2024. The growth of the retail segment in the European market is attributed to the sector’s high inventory turnover, extensive SKU diversity, and dependence on rapid replenishment systems. Retailers across Europe have aggressively adopted omnichannel strategies that integrate physical stores with digital storefronts, necessitating dense warehousing networks to support same-day and next-day delivery promises. According to the European Retail Consortium, more than four-fifths of major European retailers operated store-based fulfillment or micro hubs alongside regional distribution centers in 2024. This hybrid approach has increased warehouse dependency per sales euro by according to the European Commission’s retail logistics insights, which is a significant margin versus pre-2020 levels. For example, H and M and Zara now maintain dedicated urban fulfillment centers in over 30 European cities, each occupying 5000 to 15000 square meters of retail-aligned logistics space. The need for rapid sortation and reverse logistics for returns, which is further entrenches retail’s reliance on warehousing capacity.

The food and beverages segment is the fastest-growing end-use category in the Europe warehousing market and is estimated to grow at a CAGR of 8.84% over the forecast period due to the growing demand for fresh and perishable food products. European consumers are increasingly prioritizing fresh, unprocessed, and locally sourced food, driving up the volume of temperature-sensitive goods requiring specialized storage. According to the European Commission’s Agricultural Market Report, EU fresh produce sales reached hundreds of billions of euros in 2024, with mid-single-digit annual growth. This trend necessitates extensive cold chain infrastructure, according to the Global Cold Chain Alliance and national cold chain federations, as a majority of fresh food volumes move through refrigerated warehouses before reaching shelves. Urbanization further accelerates this need, as city dwellers rely on frequent, small-volume deliveries that demand regional cold storage nodes. According to the French National Federation of Cold Chain Operators, the number of urban cold hubs in France and Germany expanded in 2024, which reflects stronger regional distribution requirements.

COUNTRY-LEVEL ANALYSIS

Germany Warehousing Market Analysis

Germany stood as the largest national market for warehousing in Europe in 2025. The central geographic position, advanced transport connectivity, and role as Europe’s manufacturing and export engine are propelling the dominance of Germany in the European market. According to BNP Paribas Real Estate, total logistics take‑up in Germany reached around 5.3 million square meters in 2024, though this was below the ten‑year average due to subdued macroeconomic conditions. As per Destatis, industrial production contributes over 21% to Germany’s GDP, sustaining demand for just‑in‑time warehousing near clusters such as Stuttgart and Wolfsburg. According to the Federal Ministry for Digital and Transport, Germany’s infrastructure benefits from the Rhine River, the TEN‑T network, and more than 30 autobahn intersections, enabling same‑day delivery to most Western European consumers.

United Kingdom Warehousing Market Analysis

The United Kingdom held the second-largest share of the warehousing market in Europe in 2025. The growth of the UK in the European market is driven by consumer‑driven e‑commerce and pharmaceutical logistics despite Brexit‑related trade adjustments. According to the Office for National Statistics, online retail penetration in the UK remained the highest in Europe in 2024, driving demand for regional fulfillment centers. As per Savills and the UK Warehousing Association, the UK warehousing sector continues to expand, with vacancy rates in prime regions such as the southeast remaining below 2%. According to the Association of the British Pharmaceutical Industry, the UK is one of Europe’s largest pharmaceutical producers, requiring GMP‑certified warehouses with 24/7 temperature monitoring.

France Warehousing Market Analysis

France commands a strong share of Europe’s warehousing market due to its strategic location linking Southern and Northern Europe and strong domestic consumption. According to the Ministry of the Economy, the National Logistics Strategy launched in 2023 earmarked €1.7 billion for warehouse modernization near ports such as Le Havre and Marseille. As per Agence Bio, France led Europe in organic food consumption, with sales exceeding €13 billion in 2023, necessitating dedicated cold storage. According to RTE, France’s electricity mix is dominated by nuclear and hydro power, providing stable, low‑carbon energy for cold storage operations.

Netherlands Warehousing Market Analysis

The Netherlands plays a pivotal role in Europe’s warehousing market owing to its multimodal connectivity and gateway role via the Port of Rotterdam. According to the Port of Rotterdam Authority, more than 14 million TEUs of containerized goods were processed in 2023, necessitating extensive transshipment and bonded warehouses. As per the Dutch Green Building Council, nearly 80% of new warehouses achieve BREEAM Excellent or Outstanding ratings, underscoring leadership in sustainable logistics. According to the Dutch government’s Logistics Corridor Program, permits for warehouses near rail freight terminals have been fast‑tracked to accelerate development in zones such as Venlo and Tilburg.

Poland Warehousing Market Analysis

Poland has emerged as one of Europe’s fastest‑growing warehousing markets. The growth of Poland in the European market is attributed to the low operating costs, strategic location bordering Germany and Ukraine, and strong foreign investment. According to CBRE Poland, total warehouse and logistics stock reached 33.9 million square meters at the end of 2024, an increase of 9.2% compared to 2023. As per Eurostat, Polish labor costs remain significantly below the EU average, attracting multinational distributors serving pan‑European markets. According to the European Commission, Warsaw and Rzeszów have been designated as critical relief distribution nodes since 2022, reinforcing Poland’s humanitarian and commercial logistics role.

COMPETITIVE LANDSCAPE

Competition in the Europe warehousing market is intensifying as global real estate investment trusts, regional developers, and institutional investors vie for prime logistics locations amid acute space scarcity. The market is characterized by a dual focus on sustainability and technological integration, with leading players differentiating through energy-efficient building certifications and digital asset management platforms. Urban infill development and brownfield redevelopment have become critical battlegrounds as greenfield land availability dwindles in Western Europe. Meanwhile, Central and Eastern Europe is witnessing aggressive entry by international capital seeking higher yields and scalable portfolios. Tenant demands for flexible lease structures, ESG-aligned operations, and proximity-based fulfillment are reshaping development priorities. This competitive landscape fosters innovation in building design, operational resilience, and customer-centric logistics solutions while pressuring developers to accelerate delivery timelines and ensure regulatory compliance across fragmented national frameworks.

KEY MARKET PLAYERS

The leading companies operating in the Europe warehousing market include:

- Deutsche Post AG

- BrightKey, Inc.

- GEODIS

- Goodman Group

- NIPPON EXPRESS HOLDINGS, INC.

- FedEx

- RXO Inc.

- XPO, Inc.

- Ryder System, Inc.

- Prologis

- Mitsubishi Logistics Corporation

- H. Robinson Worldwide, Inc.

- SEGRO

- Americold Logistics, Inc.

- Lineage, Inc.

- Kuehne+Nagel

- P. Moller - Maersk

- NewCold

TOP PLAYERS IN THE MARKET

- Prologis is a leading global provider of logistics real estate with a significant footprint across Europe. The company develops and manages state-of-the-art warehouse facilities that support e-commerce retailers, third-party logistics providers, and industrial enterprises. In recent years, Prologis has accelerated its sustainability initiatives by equipping new developments with rooftop solar panels and smart energy management systems. It also launched a customer-centric logistics operating platform that integrates data analytics and automation to enhance supply chain visibility. These efforts reinforce its strategic relevance in Europe, where demand for energy-efficient and technologically advanced warehousing continues to rise amid tightening environmental regulations and digital transformation trends.

- Goodman Group maintains a strong presence in Europe through its focus on developing sustainable logistics hubs in key urban and intermodal locations. The company actively partners with multinational occupiers to design customized facilities that align with their net-zero commitments. Recently, Goodman expanded its European development pipeline by securing planning approvals for multiple large-scale logistics parks in Germany and the Netherlands. It also enhanced its digital asset management capabilities by deploying AI-driven building performance monitoring tools across its portfolio. These actions position Goodman to meet the growing demand for high specification warehouses that support resilient and agile supply chains across the continent.

- SEGRO is a UK-based real estate investment trust specializing in urban logistics and industrial space across Europe. The company has been instrumental in transforming underutilized urban sites into modern distribution centers that serve last-mile delivery networks. SEGRO recently intensified its focus on sustainability by committing to achieving net-zero operational carbon across its entire European portfolio by 2030. It has also invested in modular construction techniques to accelerate delivery timelines for new facilities. In addition, SEGRO has deepened collaborations with local authorities to repurpose brownfield land in cities like Paris and Milan. These initiatives solidify its role as a strategic enabler of urban supply chain efficiency and environmental compliance.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe warehousing market are actively pursuing sustainability-driven development by integrating renewable energy systems and circular design principles into new facilities. They are investing heavily in digital infrastructure, including warehouse automation, Internet of Things sensors, and AI-powered logistics platforms to enhance operational efficiency. Strategic land banking near major transport corridors and urban centers ensures proximity to demand hubs. Companies are also forming long-term partnerships with e-commerce retailers and third-party logistics providers to secure anchor tenancy and de-risk development pipelines. Finally, they are adopting modular and flexible building designs to accommodate evolving tenant requirements and enable rapid reconfiguration of storage layouts without structural overhauls.

MARKET SEGMENTATION

This research report on the Europe warehousing market has been segmented and sub-segmented into the following categories.

By Warehouse Type

- General Warehousing

- Specialized Warehousing

- Cold Storage Warehousing

By End-use

- Retail

- Food & Beverages

- Chemicals

- Others

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

1. What is the size of the Europe warehousing market?

The Europe warehousing market is expected to reach USD 377.15 billion in 2026, projected to reach USD 661.21 billion by 2034. Growth reflects e-commerce expansion.

2. What drives growth in the Europe warehousing market?

E-commerce surge, nearshoring, and automation propel the Europe warehousing market. Demand for prime locations boosts development.

3. Who are key players in the Europe warehousing market?

Leaders in the Europe warehousing market include DHL, Prologis, Goodman, Segro, and Logicor. They dominate modern facilities.

4. What is the CAGR of the Europe warehousing market?

The Europe warehousing market expects a 7.27% CAGR from 2026-2034, driven by cold chain and specialized needs.

5. Which countries dominate the Europe warehousing market?

Germany and UK lead the Europe warehousing market, with France growing fastest via logistics hubs.

6. What is general warehousing in the Europe warehousing market?

General warehousing holds largest share in the Europe warehousing market for diverse goods storage.

7. How does e-commerce impact the Europe warehousing market?

E-commerce drives 40% demand in the Europe warehousing market through urban micro-fulfillment centers.

8. What trends shape the Europe warehousing market?

Automation and green buildings trend in the Europe warehousing market for efficiency and ESG compliance.

9. Is cold storage key in the Europe warehousing market?

Cold storage grows fastest in the Europe warehousing market amid food/pharma logistics needs.

10. How competitive is the Europe warehousing market?

Institutional investors dominate the Europe warehousing market, creating supply shortages in prime areas.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com