- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Market Size, 2025

$4.41 BnMarket Estimate, 2026

$4.57 BnMarket Forecast, 2034

$6.08 BnCAGR, 2026–2034

3.62%Europe Wound Care Management Devices Market Summary

Market Size & Growth

- The Europe Wound Care Management Devices Market was valued at USD 4.41 billion in 2025.

- Expected to reach USD 6.08 billion by 2034, growing at a CAGR of 3.62% from 2026 to 2034.

- Germany held the largest country share at 29.3% in 2025.

Key Market Segments

- By Product: Advanced Wound Management Products (48.2% share in 2025); Surgical Wound Care is the fastest-growing at a CAGR of 8.2%.

- By Type of Wound: Chronic Wounds led with 52.3% share in 2025; Burns are the fastest-growing at a CAGR of 9.6% from 2025 to 2033.

- By End User: Hospitals held 55.3% share in 2025; Home Care Settings is the fastest-growing at a CAGR of 10.4% from 2025 to 2033.

- By Country: Germany, United Kingdom, France, Italy, Netherlands, Spain, Sweden, Denmark, Switzerland, Russia, Turkey, Czech Republic, Rest of Europe.

Key Drivers

- The rising prevalence of chronic wounds is driven by aging populations and metabolic conditions, including diabetic foot ulcers, which precede lower limb amputations across Europe.

- EU health systems are adopting value-based healthcare frameworks that favor advanced wound care devices proven to reduce healing time and hospital readmissions.

- Expansion of home-based wound care services, with EU countries implementing formal home hospitalization programs between 2022 and 2025.

- Integration of digital health technologies, including biosensing smart dressings and AI-driven wound progression platforms, is reimbursed as telehealth services across 15 EU member states.

Key Restraints

- EU Medical Devices Regulation (MDR 2017/745) compliance: only 38% of legacy wound care devices had transitioned to MDR compliance as of early 2025.

- Reimbursement fragmentation: only 12 of 27 EU member states provide consistent public funding for silver-impregnated antimicrobial dressings as of 2025.

Key Players

Coloplast A/S, Baxter International Inc., Hollister Inc., Mölnlycke Health Care, 3M Company, Covidien PLC, Ethicon Inc., Derma Sciences Inc., Convatec Healthcare B.S.A.R.L., Acelity L.P., Smith & Nephew.

Country-Level Highlights

- Germany (29.3% share, 2025): Universal health coverage; GBA-approved smart antimicrobial dressings after trials showed reduced infection rates; hosts 3 of Europe's 10 certified burn centers.

- United Kingdom: Over 850,000 patients treated for chronic wounds in 2023 via NHS integrated community teams; NICE updated guidelines in 2025 recommending NPWT within 72 hours of debridement.

- France: 90 million euros allocated in 2023 for surgical wound protection upgrades across 800 public hospitals; over 200 advanced dressings approved for reimbursement as of 2025.

- Italy: Over 1.5 million Italians live with chronic wounds; 45 wound care devices fast-tracked for MDR certification in 2025.

- Netherlands: Digital wound documentation mandated in all home care agencies; advanced dressings prioritized under the 2025 value-based procurement framework.

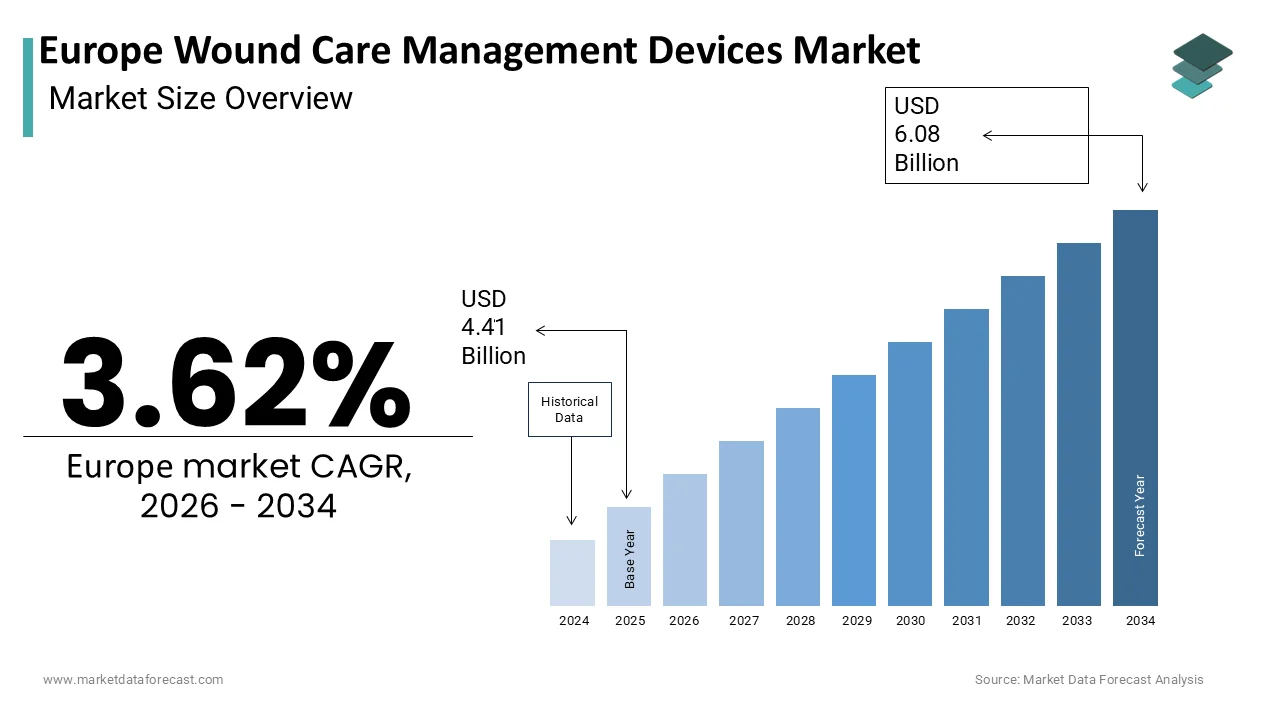

Europe Wound Care Management Devices Market Size

The Europe Wound Care Management Devices Market is projected to grow from USD 4.41 billion in 2025 to USD 4.57 billion in 2026 and reach USD 6.08 billion by 2034, registering a CAGR of 3.62% during the forecast period from 2026 to 2034.

Wound care management devices are a range of advanced medical technologies designed to support the healing of acute and chronic wounds through infection control, moisture balance, tissue regeneration, and exudate management. These include negative pressure wound therapy systems, antimicrobial dressings, gs hydrogel, els foam dressings, smart dressings with biosensing capabilities, and bioengineered skin substitutes. These devices are shaped by an aging population, rising prevalence of diabetes related complications, and stringent healthcare quality standards under the European Union Medical Devices Regulation. As per the International Diabetes Federation, Europe hosts more adults with diabetes, a condition directly linked to foot ulceration few cases during the patient’s lifetime. The European Wound Management Association estimates that chronic wounds affect some of the total EU population, translating to individuals requiring ongoing clinical intervention. This clinical and demographic reality underpins sustained demand for technologically advanced and clinically validated wound care solutions across hospital, outpatient, and home care settings.

MARKET DRIVERS

Escalating Burden of Chronic Wounds Linked to Age-Related and Metabolic Conditions

The growing incidence of chronic wounds is primarily propelled by demographic aging and the rising prevalence of metabolic disorders, such as diabetes and peripheral vascular disease is propelling the growth of the European wound care management devices market. According to Eurostat, the proportion of Europeans aged 80 years and above is projected to increase by 2035, significantly elevating the risk of pressure injuries and venous leg ulcers. Similarly, the International Diabetes Federation confirms that diabetic foot ulcers precede lower limb amputations in Europe, a region where diabetes prevalence continues to climb. These conditions require prolonged use of advanced wound care devices to prevent infection, accelerate granulation, and reduce hospitalization. National health systems, including those in Germany and the UK, now mandate structured wound care pathways that prioritize evidence-based devices over traditional gauze.

Implementation of Value-Based Healthcare Frameworks Across EU Health Systems

European healthcare systems are increasingly adopting value-based care models that tie reimbursement to clinical outcomes, patient experience, and cost efficiency rather than volume of services. The implementation of value-based healthcare frameworks across EU health systems is additionally escalating the growth of the European wound care management devices market. This shift strongly favors advanced wound care management devices that demonstrate reduced healing time, fewer dressing changes, and lower overall treatment costs. According to the Organisation for Economic Co-operation and Development, value-based procurement now influences a few of the public health expenditures in countries like Sweden, the Netherlands, and Denmark. In the United Kingdom, the National Health Service’s Getting It Right First Time program identified that standardized use of negative pressure wound therapy reduced hospital readmissions for complex wounds between 2021 and 2023. Similarly, Germany’s GBA Joint Federal Committee approved coverage for smart antimicrobial dressings after trials showed a reduction in wound infection rates in home care settings. These policy-driven incentives encourage clinicians and procurement bodies to select high-performance devices even at higher upfront costs as they yield measurable savings across the care continuum.

MARKET RESTRAINTS

Stringent Regulatory Requirements Under EU Medical Devices Regulation MDR 2017 745

The enforcement of the European Union Medical Devices Regulation has introduced significant compliance hurdles for wound care device manufacturers, particularly for novel or combination products. The stringent regulatory requirements under the EU medical devices regulation MDR 2017 745 are one of the factors hampering the growth of the European wound care management devices market. Unlike the previous directive, MDR mandates rigorous clinical evidence post-market surveillance and unique device identification for all classes of wound care products, including basic dressings, if they claim therapeutic effects. According to the European Commission, as of early 2025, only 38% of legacy wound care devices originally certified under the Medical Devices Directive had successfully transitioned to MDR compliance due to data gaps or insufficient clinical evaluation. The European Wound Management Association reported that small and medium enterprises face average conformity assessment costs exceeding 500000 euros per product line, a barrier that stifles innovation and delays market access. These regulatory complexities disproportionately impact emerging biotech firms and limit the diversity of advanced solutions available to European clinicians despite clear clinical need.

Fragmented Reimbursement Policies Across European Member States

The absence of a harmonized reimbursement framework for advanced wound care devices creates significant access disparities and commercial uncertainty, which is additionally degrading the growth of the European wound care management devices market. While Germany and the Netherlands maintain structured coverage for negative pressure wound therapy and bioengineered skin substitutes, countries such as Greece, Romania, and Bulgaria often restrict reimbursement to basic dressings due to fiscal constraints. According to the European Observatory on Health Systems and Policies, national health technology assessment timelines for wound care devices vary in the Netherlands, Southern and Eastern Europe. The European Federation of Wound Healing Societies documented in 2025 that only 12 of 27 EU member states provide consistent public funding for silver-impregnated antimicrobial dressings despite clinical guidelines recommending their use in infected wounds. This fragmentation forces manufacturers to navigate 20-plus distinct pricing and evidence submission processes, thereby increasing market entry costs and delaying patient access. Clinicians in underfunded systems frequently resort to off-label use or out-of-pocket purchases, undermining treatment efficacy and equity.

MARKET OPPORTUNITIES

Integration of Digital Health Technologies and Remote Monitoring Capabilities

The emergence of wound care devices with digital health platforms is evolving care delivery, which is creating new opportunities for the growth of the European wound care management devices market. Smart dressings embedded with biosensors can now monitor pH, temperature, exudate volume, and bacterial load, transmitting real-time data to clinicians via mobile applications. According to the European Connected Health Alliance, EU countries launched national telehealth strategies between 2022 and 2025 that include remote wound assessment as a reimbursable service. In Sweden, the national eHealth Agency integrated a wound imaging and analytics platform into primary care workflows, reducing specialist referral times in a 2023 pilot. Similarly, France’s Health Data Hub approved a multicenter study in early 2025 evaluating AI-driven wound progression prediction using data from connected dressings. These digital ecosystems not only enhance clinical decision-making but also align with EU priorities for integrated care and reduced hospital burden. Manufacturers that embed interoperability with national electronic health records and comply with the EU’s Digital Health and Care Strategy will gain first-mover advantage in this high-growth segment.

Expansion of Home-Based and Community Wound Care Services

Shifting care delivery from hospitals to community and home settings is creating robust demand for user-friendly portable and self-managed devices is another factor boosting the growth of the European wound care management devices market. Driven by cost containment goals and patient preference, national health systems are increasingly delegating chronic wound management to district nurses, home care agencies, and even trained patients. According to the European Centre for Disease Prevention and Control, chronic wound care episodes in the EU now occur outside acute hospitals, a trend accelerated by post-pandemic care redesign. The United Kingdom’s National Wound Care Strategy 2023 mandates that leg ulcer patients receive care within four weeks in community settings, reducing pressure on surgical beds. This transition necessitates devices that are easy to apply, require fewer changes, and minimize caregiver dependency. Single-use negative pressure systems and pre-hydrated hydrocolloid dressings have seen rapid uptake in Germany and the Netherlands, where home care coverage includes advanced wound products. Companies that design for usability, durability, and caregiver training will capture significant value in this decentralized care model.

MARKET CHALLENGES

Shortage of Specialized Wound Care Clinicians and Training Gaps

Despite technological advances, the shortage of healthcare professionals trained in modern wound management principles, which directly impedes optimal device utilization, is a challenge for the growth of the European wound care management devices market. According to the European Wound Management Association, few nurses in primary care across Southern and Eastern Europe have received formal certification in wound care as of 2025. In Italy, a 2023 Ministry of Health audit revealed that district nurses could correctly identify the appropriate dressing type for a sloughy venous ulcer, often leading to inappropriate gauze use and delayed healing. This knowledge gap is exacerbated by the rapid pace of device innovation, where new products with specific indications require precise application protocols. Bridging this competency divide is essential to unlock the full clinical and economic value of modern wound care technologies.

High-Cost Sensitivity in Public Procurement and Budget Constraints

Public healthcare budget limitations, particularly in Southern and Eastern Europe, continue to restrict the adoption of premium-priced advanced wound care devices. Despite their long-termcost-effectivenessh cost sensitivity in public procurement and budget constraints are other factors declining the growth of the European wound care management devices market. According to Eurostat, total health expenditure per capita in countries like Romania and Bulgaria remains below that in Germany or Sweden. The European Commission’s 2025 Health at a Glance report noted that price is the dominant criterion in public tenders for medical consumables in these regions, often excluding innovative but higher-cost devices from procurement lists. This forces clinicians to use suboptimal alternatives or request patient co-payments, which are unaffordable for many.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Type of Wound, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Coloplast A/S, Baxter International Inc., Hollister Inc., Mölnlycke Health Care, 3M Company, Covidien PLC, Ethicon Inc., Derma Sciences Inc., Convatec Healthcare B.S.A.R.L., Acelity L.P./, and Smith & Nephew. |

SEGMENTAL ANALYSIS

By Product Insights

The advanced wound management segment held 48.2% of the European wound care management devices market share in 2025, owing to the clinical superiority of these products in managing complex chronic wounds and their alignment with white evidence-based treatment protocols endorsed across the region. According to the European Wound Management Association, many of the national clinical guidelines in Western Europe now recommend advanced dressings, such as hydrogels, alginate,s, and antimicrobial silver dressings as first-line therapy for diabetic foot ulcers and venous leg ulcers. The European Society for Vascular Surgery reported in 2025 that the use of moisture-retentive advanced dressings reduced healing time for venous ulcers by an average of 22 days compared to traditional gauze. Furthermore, public health agencies increasingly recognize the cost-effectiveness of these technologies. This emergence of clinical efficacy policy endorsement and economic validation solidifies the dominance of advanced wound management products across European healthcare systems.

The surgical wound care segment is anticipated to witness the fastest CAGR of 8.2% throughout the forecast period by rising surgical volumes, post-operative infection prevention mandates, and integration of antimicrobial technologies. As per Eurostat, many inpatient surgical procedures were performed across the EU in 202,3, with an additional outpatient interventions reflecting sustained demand for sterile high-performance wound closure and protection products. The European Centre for Disease Prevention and Control reported that surgical site infections remain the second most common healthcare-associated infection in acute care hospitals, affecting a few procedures despite preventive efforts. In response, the European Commission’s 2023 Healthcare-Associated Infection Strategy prioritized antimicrobial incision dressings and absorbable hemostats as core components of surgical safety bundles. Countries like Sweden and the Netherlands now require the use of iodine or silver-impregnated sponges for high-risk procedures, such as colorectal and orthopedic surgeries.

By Type of Wound Insights

The chronic wounds segment was the largest by accounting for 52.3% of the European wound care management devices market share in 2025, owing to their high prevalence, prolonged treatment duration, and resource intensity. Conditions, such as diabetic foot ulcers, venous leg ulcers, and pressure injuries, affect millions and require ongoing use of advanced devices for effective management. The European Pressure Ulcer Advisory Panel confirmed in 2025 that pressure injuries affect some of the hospitalized elderly patients and nursing home residents. National strategies increasingly prioritize early intervention. The United Kingdom’s National Wound Care Strategy mandates multidisciplinary assessment within 48 hours of ulcer identification and recommends advanced dressings as standard care. Similarly, Germany’s Disease Management Programs for diabetes include comprehensive foot screening and wound care pathways reimbursed under statutory health insurance. These systemic approaches ensure sustained device utilization over months or even years per patient, thereby anchoring chronic wounds as the dominant therapeutic segment.

The burns segment is projected to witness the fastest CAGR of 9.6% from 2025 to 2033, with technological advances in bioengineered skin substitutes, improved emergency response systems, and increasing thermal injury incidents linked to energy transitions. According to the European Burns Association, many burn cases requiring medical attention were recorded across the EU in 2023, with domestic accidents and industrial incidents representing the leading causes. Recent policy developments have intensified focus on specialized burn care. The European Commission’s 2025 Civil Protection Mechanism allocated huge funds to enhance regional burn center capacity, including procurement of advanced wound matrices. Switzerland’s University Hospital Zurich reported in 2025 that the use of autologous skin cell spray technologies reduced hospital stays for partial thickness burns, compared to conventional dressings. Additionally, the shift toward renewable energy infrastructure has raised occupational burn risks, with the European Agency for Safety and Health at Work documenting a rise in thermal injuries in battery manufacturing and hydrogen facilities since 2021.

By End User Insights

The hospitals segment was the largest by holding 55.3% of the European wound care management devices market share in 2025 due to their role as primary sites for complex acute and surgical wound management. These institutions handle the majority of high acuity cases, including trauma, burns post post-operative complications, and infected chronic wounds requiring multidisciplinary intervention. According to the European Hospital and Healthcare Employers Association, many negative pressure wound therapy systems and bioengineered skin substitutes are administered within hospital settings where sterile environments and specialist staff ensure optimal outcomes. National health systems reinforce this concentration. In France, the 2023 Hospital Quality and Safety Directive mandated that all tertiary hospitals establish dedicated wound care units equipped with advanced devices as part of accreditation standards. Similarly, Italy’s National Health Service reimburses only hospital-based use of growth factor-based therapies for diabetic foot ulcers.

The home care settings segment is anticipated to grow at the fastest CAGR of 10.4% from 2025 to 2033, driven by policy-led dehospitalization cost containment strategies and patient preference for care in familiar environments. According to the Organisation for Economic Co-operation and Development, EU countries implemented formal home hospitalization programs between 2022 and 2025, enabling complex wound management outside acute facilities. The Netherlands’ Home First initiative reported that some venous leg ulcer patients received full treatment at home in 2023 using telehealth-supported protocols and nurse-delivered advanced dressings. Similarly, Germany’s Statutory Health Insurance expanded reimbursement in 2025 to cover single-use negative pressure devices for home use in patients with stage three or four pressure injuries, reducing readmission rates. The European Connected Health Alliance confirmed that digital wound assessment tools are now integrated into home care workflows in 15 EU member states, facilitating remote monitoring and timely intervention. These systemic shifts transform the home into a viable and increasingly preferred site for advanced wound therapy delivery.

COUNTRY LEVEL ANALYSIS

Germany Wound Care Management Devices Market Analysis

Germany was the largest contributor in the European wound care management devices market by capturing 29.3% of the market share in 2025. This position reflects its universal health coverage, dense network of specialized wound clinics, and proactive integration of advanced devices into statutory reimbursement frameworks. The German Federal Joint Committee regularly updates its catalog of reimbursable wound care products, ensuring timely access to innovations, such as antimicrobial and negative pressure systems. The country’s Disease Management Programs for diabetes include mandatory evaluations and structured wound pathways covered under public insurance. Furthermore, Germany hosts three of Europe’s ten certified burn centers and maintains strict hospital hygiene standards under the Infection Protection Act, which mandates advanced dressings for high-risk surgical patients.

United Kingdom Wound Care Management Devices Market Analysis

The UniKingdom's wound care management devices market growth is likely to grow with its centralized National Health Service, strong clinical governance, and pioneering national wound care strategy. Launched in 2022, the NHS England Wound Care Strategy established standardized pathways for venous leg ulcers, diabetic foot ulcers, and pressure injuries across primary and secondary care. According to NHS Digital, over 850000 patients received treatment for chronic wounds in 2023 through integrated community teams using advanced dressings. The National Institute for Health and Care Excellence updated its clinical guidelines in 2025 to recommend negative pressure wound therapy for complex surgical wounds within 72 hours of debridement. Additionally, the UK’s Medicines and Healthcare products Regulatory Agency operates one of Europe’s fastest conformity assessment routes under MDR, facilitating quicker access to innovative devices. These coordinated policy, clinical, and regulatory mechanisms ensure consistent demand and serve as a model for integrated wound care delivery.

France Wound Care Management Devices Market Analysis

France's wound care management devices market growth is likely to grow with its extensive public hospital network, robust social security reimbursement, and national focus on infection control. The French Ministry of Health’s 2023 National Plan Against Healthcare-Associated Infections allocated 90 million euros to upgrade surgical wound protection protocols across 800 public hospitals, mandating antimicrobial dressings for high-risk procedures. The country’s Haute Autorité de Santé actively evaluates wound care technologies for inclusion in the List of ReReimbursable Productswith over 200 advanced dressings approved as of 2025. Furthermore, France maintains a dense network of specialized diabetic foot centers with 120 units integrated into hospital outpatient departments, ensuring early intervention. These structural and policy advantages position France high-compliance market with strong uptake of evidence-based devices.

Italy Wound Care Management Devices Market Analysis

Italy's wound care management devices market growth is likely to grow with the high chronic wound prevalence, regional healthcare autonomy, and growing adoption of advanced therapies. According to the Italian National Institute of Health, over 1.5 million Italians live with chronic wounds primarily due to aging and diabetes, with regional disparities in care access. The 2023 National Chronic Wound Registry initiative standardized data collection across 18 regions, enabling better resource allocation and technology assessment. Regions like Lombardy and Emilia Romagna lead adoption with local health authorities reimbursing bioengineered skin substitutes for diabetic foot ulcers since 2022. The Italian Medicines Agency also alsofast-trackedd MDR certification for 45 wound care devices in 2025 to address legacy product shortages.

Netherlands Wound Care Management Devices Market Analysis

Netherlands care management devices market growth is likely to grow with integrated care models, value-based procurement, and leadership in home-based wound management. The Dutch Healthcare Authority’s 2025 procurement framework prioritizes devices that demonstrate reduced healing time and lower total cost of care, with advanced dressings and single-use negative pressure systems receiving preferential pricing. The country also mandates the use of digital wound documentation in all home care agencies, enabling real-time monitoring and protocol adherence. Additionally, the Netherlands hosts leading wound research centers at Erasmus MC and Radboud University, driving clinical validation and innovation adoption.

COMPETITIVE LANDSCAPE

The European wound care management devices market features a competitive landscape shaped by a mix of multinational medtech corporations, specialized wound care firms, and regional innovators. Competition is driven less by price and more by clinical efficacy, regulatory compliance, ease of use, and integration into care pathways. Leading companies differentiate through robust clinical trials, data digital connectivity, and alignment with national wound strategies. The implementation of the EU Medical Devices Regulation has raised entry barriers favoring established players with strong quality management systems, yet also creating opportunities for agile firms with novel technologies. Reimbursement fragmentation across countries necessitates tailored market access strategies. Additionally, the shift toward home and community care demands products that are user-friendly and supported by training infrastructure. This environment encourages continuous innovation while requiring a deep understanding of clinical workflows and policy dynamics across diverse European health systems.

KEY MARKET PLAYERS

Notable companies operating in the europe wound care management devices market are

- Coloplast A/S

- Baxter International Inc.

- Hollister Inc.

- Mölnlycke Health Care

- 3M Company

- Covidien PLC

- Ethicon Inc.

- Derma Sciences Inc.

- Convatec Healthcare B.S.A.R.L.

- Acelity L.P.

- Smith & Nephew

TOP LEADING PLAYERS IN THE MARKET

- Smith & Nephew is a globally recognized leader in advanced wound management with a strong foothold in Europe through its comprehensive portfolio, including negative pressure wound therapy systems, antimicrobial dressings, and bioactive technologies. The company contributes significantly to global innovation by investing in clinical research and digital wound care solutions. Recently, Smith & Nephew expanded its Wound Care Digital Platform across Germany, France, and the UK by enabling real-time wound assessment and treatment tracking in both hospital and home settings. It also launched a next-generation silver alginate dressing with enhanced exudate handling in early 2025, with its commitment to infection control and andpatient-centricc design without reliance on legacy technologies.

- 3M plays a pivotal role in the European wound care management devices market through its advanced wound closure and infection prevention portfolio, including antimicrobial incision dressings and hydrocolloid technologies. Globally, the company leverages its materials science expertise to develop breathable yet protective barriers that support moist wound healing. 3M partnered with major European hospital networks to integrate its surgical site infection prevention bundles into perioperative protocols. It also enhanced its manufacturing capacity in Germany to ensure a consistent supply of sterile dressings compliant with the EU Medical Devices Regulation. These actions demonstrate its strategic alignment with European clinical standards and public health priorities.

- Braun is a key European-based participant in the wound care devices market, offering a focused range of surgical and chronic wound solutions grounded in its heritage in hospital care and sterility assurance. The company contributes to global best practices through its emphasis on single-use sterile products and compatibility with hospital infection control policies. B. Braun introduced a new line of silicone-based soft dressings designed for fragile skin in elderly patients across its EU distribution network. It also collaborated with nursing associations in Italy and Spain to deliver training programs on modern wound assessment and dressing selection. These initiatives strengthen its clinical credibility and reinforce deep integration within European healthcare ecosystems.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European wound care management devices market primarily pursue strategies centered on clinical evidence generation, regulatory compliance under MD, R digital health integrations, strategic partnerships with healthcare ers, product portfolio diversification, training and education initiatives for clinicians, and targeted expansion of home care compatible solutions. These companies also invest in localized manufacturing to ensure supply chain resilience and align product development with national wound care guidelines and reimbursement policies across diverse EU member states.

MARKET SEGMENTATION

This research report on the europe wound care management devices market has been segmented & sub-segmented into the following categories.

By Product

-

Advanced Wound Management Products

- Advanced Wound Dressings

- Foam Dressings

- Hydrocolloid Dressings

- Film Dressings

- Alginate Dressings

- Hydrogel Dressings

- Collagen Dressings

- Other Dressings

- Therapy Devices

- Negative Pressure Wound Therapy

- Pressure Relief Devices

- Oxygen and Hyperbaric Oxygen Devices

- Electrical Stimulation Devices

- Other Therapy Devices

- Active Wound Care

- Artificial Skin and Skin Substitutes

- Topical Agents

- Advanced Wound Dressings

- Surgical Wound Care

- Tissue Adhesives, Sealants & Glues

- Anti-infective Dressings

- Traditional/Basic Wound Care

- Medical Tapes

- Dressings

- Cleansing Agents

By Type of Wound

- Chronic Wounds

- Diabetic Foot Ulcers (DFU)

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

- Acute Wounds

- Surgical & traumatic wounds

- Burns

By End User

- Hospitals

- Clinical

- Home Care Settings

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe