Europe Wound Debridement Products Market Size, Share, Trends & Growth Forecast Report By Method Of Debridement, Type Of Wound, Product and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe) – Industry Analysis From 2026 to 2034.

Europe Wound Debridement Products Market Report Summary

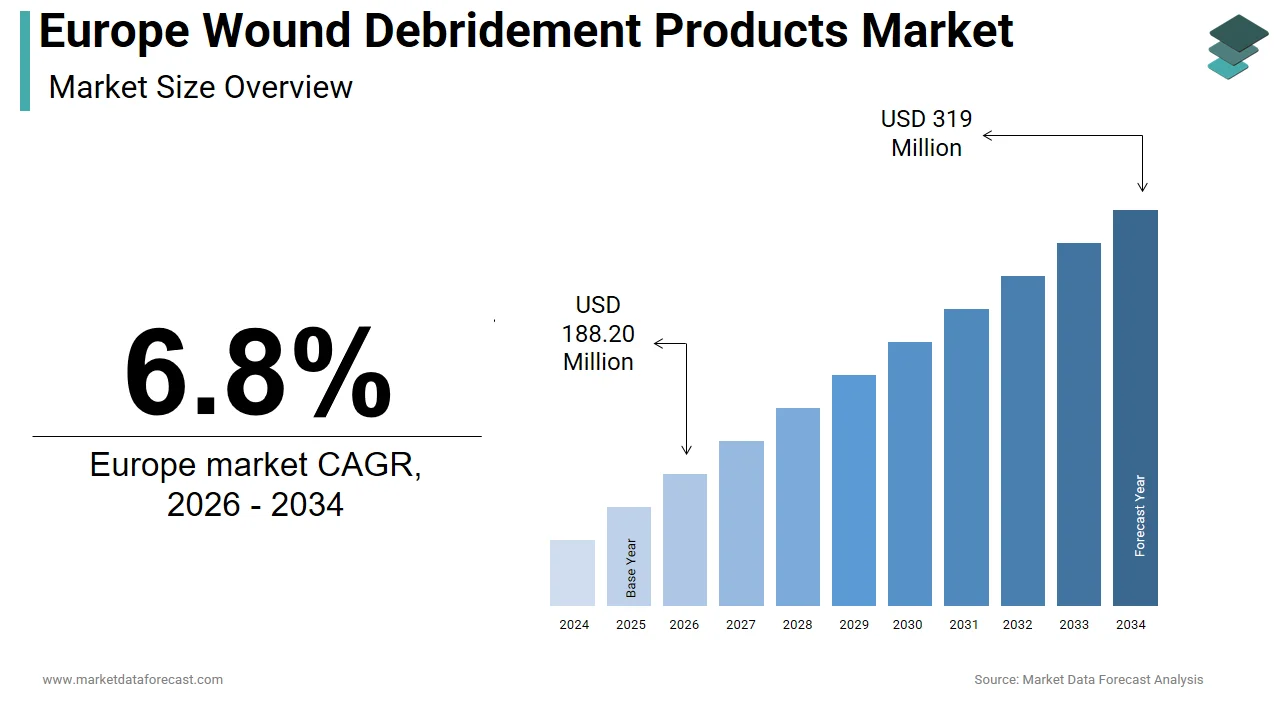

The Europe wound debridement products market was valued at USD 176.22 million in 2025, is anticipated to reach USD 188.20 million in 2026, and is projected to reach USD 319 million by 2034, growing at a CAGR of 6.8% from 2026 to 2034. Market growth is driven by the increasing prevalence of chronic wounds, rising incidence of diabetes and pressure ulcers, and growing demand for advanced wound care solutions. Wound debridement is a critical process in removing dead or infected tissue to promote healing and prevent complications. Additionally, advancements in wound care technologies, the expanding elderly population, and increasing healthcare investments are supporting steady market expansion across Europe.

Key Market Trends

- Rising prevalence of chronic wounds, including diabetic foot ulcers and pressure ulcers.

- Increasing adoption of advanced and minimally invasive debridement techniques.

- Growing demand for effective wound care solutions in aging populations.

- Expansion of hospital-based and specialized wound care centers.

- Increasing focus on improving patient outcomes and reducing healing time.

Segmental Insights

- Based on method of debridement, the sharp and surgical debridement segment dominated the Europe wound debridement products market by accounting for 43.6% share in 2025, driven by its effectiveness, precision, and widespread use in hospital settings.

- Based on type of wound, the chronic wounds segment held the largest share of 61.1% in 2025, supported by the rising prevalence of diabetes, vascular diseases, and aging-related wound complications.

- Based on product, the traditional wound debridement devices segment led the market by capturing 52.7% share in 2025, driven by widespread clinical adoption, affordability, and availability across healthcare facilities.

Regional Insights

The Europe wound debridement products market is witnessing steady growth across major countries, supported by increasing healthcare investments, rising chronic disease burden, and expanding wound care infrastructure.

- The United Kingdom holds a significant share of the market, supported by advanced healthcare infrastructure, increasing prevalence of chronic wounds, and strong adoption of advanced wound care technologies.

- Germany is expected to register significant growth during the forecast period, driven by rising incidence of diabetes, burns, and injuries, along with expanding healthcare infrastructure and increasing demand for effective wound care solutions.

- France maintains a notable position in the market, supported by strong public healthcare systems, growing elderly population, and increasing focus on improving chronic wound management.

Competitive Landscape

The Europe wound debridement products market is characterized by the presence of leading wound care product manufacturers focusing on innovation, product development, and expanding treatment options. Market participants are investing in advanced debridement technologies, strengthening distribution networks, and forming strategic partnerships with healthcare providers. Increasing emphasis on improving wound healing outcomes and reducing healthcare costs is shaping competitive dynamics.

Leading companies operating in the Europe wound debridement products market include Coloplast, ConvaTec, 3M, Smith & Nephew, Misonix, and MediWound.

Europe Wound Debridement Products Market Size

The Europe wound debridement products market was valued at USD 176.22 million in 2025, is estimated to reach USD 188.20 million in 2026, and is projected to reach USD 319 million by 2034, growing at a CAGR of 6.8% from 2026 to 2034.

Wound debridement products are medical devices and agents designed to remove necrotic tissue biofilm and foreign material from acute and chronic wounds to promote healing and prevent infection. In Europe, these include enzymatic formulations, autolytic dressings, mechanical tools such as curettes and scalpels, hydrotherapy systems, and advanced modalities like ultrasonic and hydrosurgical devices. The market is shaped by a high prevalence of hard-to-heal wounds driven by aging populations, diabetes, and vascular diseases alongside robust healthcare infrastructure and reimbursement frameworks. According to Eurostat, over 21 percent of the EU population is aged sixty-five or older, a demographic highly susceptible to pressure ulcers and diabetic foot complications. As per multiple studies, a significant and increasing number of Europeans suffer from chronic wounds, leading to a substantial economic burden on healthcare systems, primarily driven by the costs of nursing care and hospital treatments. The European Commission’s Strategic Agenda for Chronic Wound Care emphasizes early intervention and standardized protocols, which have elevated debridement from an optional step to a clinical necessity. Furthermore, the European Medicines Agency and notified bodies under the Medical Devices Regulation enforce stringent performance and biocompatibility standards, ensuring product safety and efficacy across diverse care settings from hospitals to home care.

MARKET DRIVERS

Rising Prevalence of Diabetes and Associated Foot Ulcers

The escalating burden of diabetes across Europe is a main reason for demand in advanced wound debridement solutions and the growth of the Europe wound debridement products market. According to the International Diabetes Federation, the number of adults living with diabetes in the European region is increasing and is expected to continue growing over the next decade, with the vast majority of these cases being type 2 diabetes. Medical experts indicate that a significant portion of the diabetic population will develop foot ulcers during their lifetime, a complication that remains a leading cause of hospital admissions and severe morbidity for these patients. These wounds are particularly prone to biofilm formation and delayed healing, requiring regular debridement to prevent amputation. Data from German statistical authorities show that a substantial number of lower limb amputations occur annually, frequently as a result of complications from non-healing ulcers in patients with underlying metabolic conditions. Clinical guidelines from the European Wound Management Association now mandate sharp or hydrosurgical debridement at every clinic visit for infected diabetic wounds. This protocol shift transforms debridement from episodic to routine care, driving sustained consumption of both single-use instruments and advanced irrigation systems across outpatient and home care channels.

Aging Population and Increased Incidence of Pressure Injuries

The region’s rapidly aging demographic, which significantly increases the incidence of pressure injuries, is among the key forces behind the expansion of the Europe wound debridement products market. This is particularly true in long-term care and hospital settings where immobility and comorbidities converge. As per Eurostat, the proportion of the European Union population aged sixty-five or older has reached record highs, with Italy and several other member states having the highest shares of elderly residents. European studies indicate that hospital-acquired pressure ulcers are a significant safety concern for older patients, with a notable percentage of admitted individuals developing these wounds, which frequently require specialized debridement to remove necrotic tissue and allow for healing. Nursing homes in France manage a high volume of residents with limited mobility, making them high-risk environments where regular skin assessments are standard practice, as recommended by health authorities to detect and prevent severe wound progression. Autolytic and enzymatic debridement products are especially favored in these settings due to their non-invasive nature and compatibility with fragile skin. This demographic reality ensures consistent institutional demand for gentle yet effective debridement modalities that align with geriatric care principles and reduce caregiver burden.

MARKET RESTRAINTS

Stringent Regulatory Requirements Under the EU Medical Devices Regulation

The implementation of the European Union Medical Devices Regulation has introduced significant compliance complexities that affect the growth of the Europe wound debridement products market. These complexities delay market entry and increase development costs for wound debridement products. Enforced since May 2021, MDR mandates rigorous clinical evidence, post-market surveillance, and risk classification based on invasiveness and duration of contact. Many debridement devices, particularly powered systems like ultrasonic probes, fall under Class IIb, requiring extensive performance studies and notified body scrutiny. The number of authorized organizations available to certify medical devices has grown significantly since the regulation’s introduction. However, manufacturers still face substantial delays in securing approvals, with the certification process often taking well over a year. Recent industry findings highlight that smaller medical technology companies are disproportionately struggling with the new regulatory requirements, leading many to reduce their product offerings or delay the introduction of innovations to the European market. Additionally, reclassification of certain enzymatic gels as medical devices rather than cosmetics has forced reformulation and relabeling. These regulatory hurdles disproportionately impact innovative startups, limiting the diversity of solutions available to clinicians despite unmet clinical needs in complex wound management.

Limited Reimbursement for Advanced Debridement Modalities in Certain Member States

Reimbursement policies across the region remain fragmented with significant disparities in coverage for advanced modalities, which further slows down the expansion of the Europe wound debridement products market. This is the case despite clinical consensus on the importance of debridement. Reimbursement for advanced wound debridement in the EU varies significantly, with no evidence supporting a specific twelve-nation policy regarding hydrosurgical systems. In Southern and Eastern Europe, budget constraints often lead to restrictive formularies. Moreover, in Greece and other regions, budgetary constraints lead to restrictive, though not necessarily exclusive, coverage for specialized treatments. This patchwork discourages the adoption of cost-effective but higher upfront technologies that reduce long-term complications. Research indicates that while hydrosurgery improves wound preparation efficiency and reduces procedural time compared to conventional methods, its high cost often leads to cost-neutral outcomes rather than significant overall savings. Studies suggest that although advanced surgical technologies may be limited in some public hospitals, they are not completely unavailable in public systems. Patient access to optimal debridement will remain inequitable across the European Union. This will continue until harmonized value-based reimbursement frameworks emerge.

MARKET OPPORTUNITIES

Integration of Debridement into Home Care and Telemedicine Platforms

The expansion of home-based wound care supported by digital health technologies opens up major possibilities for user-friendly debridement products, which is likely to drive the growth of the Europe wound debridement products market. European healthcare systems, including those in Germany, France, and the Netherlands, are increasingly transitioning chronic wound management to primary and home care settings to improve patient quality of life and reduce hospital readmissions. This shift demands safe, easy-to-use debridement solutions suitable for caregiver or self-administration. Companies are responding with single-use pre-sterilized curettes, enzymatic gels with clear application instructions, and portable irrigation kits compatible with telehealth monitoring. Sweden utilizes digital health infrastructure to integrate clinical data, such as wound images and treatment records, into electronic systems to facilitate remote specialist assessment. The European Union funds digital healthcare, including initiatives aimed at modernizing care and improving treatment efficiency, often through initiatives like the Digital Europe Programme. Reimbursement changes are turning debridement into a decentralized, remote service, enhancing care continuity and accessibility.

Development of Biofilm-Targeted and Antimicrobial Debridement Agents

The growing recognition of biofilm as a key barrier to wound healing is driving innovation in debridement products, which boosts expansion potential for the Europe wound debridement products market. These products are engineered to disrupt microbial communities and prevent reinfection. According to the European Wound Management Association, over eighty percent of chronic wounds harbor polymicrobial biofilms that resist conventional antibiotics and impede tissue regeneration. This insight has spurred the development of debridement agents combining mechanical removal with antimicrobial action. For instance, polyhexamethylene biguanide impregnated dressings and iodine-based hydrogels not only soften necrotic tissue but also penetrate biofilm matrices. Studies involving dispersin B formulations indicate a significant reduction in biofilm biomass, showing potential to combat chronic wound infections by breaking down protective biofilm structures. The European Centre for Disease Prevention and Control supports these advances under its One Health Action Plan to combat antimicrobial resistance by promoting non-antibiotic strategies. The maturing MDR framework for combination products highlights biofilm-targeted debridement as a crucial innovation, simultaneously improving clinical outcomes and meeting public health demands.

MARKET CHALLENGES

Shortage of Trained Wound Care Specialists Across Primary and Community Settings

The effective use of advanced debridement techniques requires specialized training, but the scarcity of this training across the region’s overstretched healthcare workforce is challenging the growth of the Europe wound debridement products market. The European Wound Management Association indicates that a significant shortage of specialized wound care professionals exists across Europe, leaving a growing population of patients with complex wounds with limited access to expert care. The European Observatory on Health Systems and Policies emphasizes that rural areas in Spain and Poland face significant challenges in providing equitable access to specialized health services, resulting in a higher burden on primary care and reduced availability of specialized professionals compared to urban centers. This deficit leads to inconsistent debridement practices, with general practitioners often avoiding sharp techniques due to legal and skill concerns. Consequently, wounds remain inadequately managed, progressing to severe stages that necessitate hospitalization. Vocational training programs are insufficient, with only a few EU countries offering accredited wound care curricula, as per sources. The full potential of advanced debridement products will remain unrealized due to human capital gaps in frontline care delivery. To bridge these gaps, coordinated upskilling under initiatives like the EU Pact for Skills is required.

High Cost of Single-Use Advanced Debridement Devices in Resource-Constrained Settings

The economic burden of adopting single-use advanced debridement systems remains prohibitive for many public hospitals and long-term care facilities, which in turn constrains the expansion of the Europe wound debridement products market. This is particularly true in Southern and Eastern Europe. Advanced disposable surgical tools like hydrosurgical probes and ultrasonic tips represent a high cost per procedure compared to traditional instruments. Conventional manual surgical tools, such as scalpels and gauze, are highly cost-effective, with low per-procedure costs. Studies confirm long-term savings through reduced healing time and infection rates. However, the high upfront expense deters procurement committees operating under annual budget caps. In Italy, regional health authorities in Sicily and Calabria have explicitly excluded powered debridement from tender lists, citing cost inefficiency despite national guidelines endorsing their use. Similarly, Romanian public hospitals rely almost exclusively on autolytic methods due to import restrictions on high-value medical devices. This financial barrier creates a two-tier system where only affluent private clinics or university hospitals can offer state-of-the-art debridement, perpetuating disparities in wound care outcomes across socioeconomic and geographic lines.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Method of Debridement, Type of Wound, Product, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Coloplast A/S, ArthroCare Corporation, ConvaTec Group plc, Misonix, Inc., 3M Company, MediWound Ltd, Derma Sciences, Inc., PuriCore plc, and Smith & Nephew Plc. |

SEGMENTAL ANALYSIS

By Method of Debridement Insights

The sharp and surgical debridement segment led the Europe wound debridement products market and accounted for a 43.6% share in 2025. The leading position of the segment is driven by its status as the gold standard for rapid and precise removal of necrotic tissue biofilm and non-viable margins, particularly in infected or critically colonized wounds. Evidence-based guidelines recommend that the frequency of sharp debridement for chronic wounds, such as diabetic foot ulcers and pressure ulcers, be determined by a clinician based on the presence of necrotic tissue or bioburden, rather than as a strict mandate for every visit. Sharp debridement is considered a foundational part of standard chronic wound care in Germany, though frequency varies based on individual patient assessment. The method’s efficacy is unmatched. Evidence suggests that, compared to autolytic methods, sharp debridement can accelerate the healing process of venous leg ulcers by enabling faster removal of necrotic tissue. Additionally, the availability of single-use sterile scalpels, curettes, and forceps ensures safety and compliance with infection control standards across hospital, outpatient, and home care settings, reinforcing its entrenched position in European wound management pathways.

The low-frequency ultrasound debridement segment is expected to exhibit a noteworthy CAGR of 11.8% between 2026 and 2034 due to its unique ability to selectively remove devitalized tissue while preserving healthy granulation through controlled cavitation and microstreaming effects. Unlike mechanical methods, it minimizes pain and bleeding, making it ideal for fragile patients with comorbidities such as diabetes or vascular insufficiency. Evidence indicates that ultrasound-assisted wound debridement may be more effective and efficient at removing slough in diabetic foot ulcers than traditional sharp debridement alone. Additionally, the European Commission’s Horizon Europe program supports the adoption of advanced, non-invasive wound care technologies to enhance community-based management and reduce hospital admissions for chronic wounds. Furthermore, devices like MIST Therapy are now integrated into home care protocols in Sweden and the Netherlands, enabling weekly treatments without clinic visits. Reimbursement is expanding, and training programs are proliferating. As a result, this modality is transitioning from a niche innovation to a mainstream standard of care.

By Type of Wound Insights

In 2025, the chronic wounds segment was the largest segment in the Europe wound debridement products market and captured a 61.1% share. The supremacy of the segment is attributed to the high prevalence of hard-to-heal ulcers driven by aging populations, diabetes, and venous insufficiency. According to Eurostat, over 21 percent of the EU population is aged sixty-five or older, a demographic highly susceptible to pressure injuries and diabetic foot complications. The International Diabetes Federation notes that a significant percentage of Europeans with diabetes are expected to develop foot ulcers in their lifetime, requiring regular, specialized care. Venous leg ulcers affect a significant portion of the European population, with high recurrence rates observed without proper, ongoing wound management. National health systems in Germany, France, and the UK have institutionalized debridement as a mandatory step in chronic wound protocols under integrated care pathways. This structural embedding ensures consistent demand for both enzymatic gels and powered devices across primary, secondary, and home care settings, making chronic wounds the cornerstone of debridement product consumption.

The diabetic ulcers segment is predicted to witness the highest CAGR of 10.4% over the forecast period, owing to the rising incidence of type 2 diabetes and associated neuropathy across Europe. The International Diabetes Federation indicates that the number of adults living with diabetes in the European Region is rising, with projections suggesting continued growth in the coming years, primarily driven by obesity and sedentary lifestyles. Diabetic foot ulcers are particularly challenging due to impaired circulation, reduced immune response, and high biofilm burden, necessitating frequent and aggressive debridement. Clinical guidelines now recommend debridement at every visit, a shift that transforms episodic care into continuous intervention. Following the implementation of updated clinical practice guidelines for the treatment of diabetic foot syndrome in Italy, specialized clinics have continued to refine and standardize wound management procedures. Innovations like hydrosurgery and ultrasound offer selective tissue removal, critical for preserving limited tissue viability in these patients. With amputation prevention as a core healthcare priority, diabetic ulcers drive the sustained adoption of advanced debridement solutions. Consequently, these technologies are seeing increased, consistent use across the continent.

By Product Insights

The traditional wound debridement devices segment dominated the Europe wound debridement products market and held a 52.7% share in 2025. The dominance of the segment is supported by universal accessibility, low cost, and integration into standard clinical workflows across all care settings. These single-use sterile instruments are essential for sharp debridement, which remains the first-line intervention for infected necrotic or heavily exudating wounds per European Wound Management Association guidelines. In public hospitals across Spain, Poland, and Romania, where budget constraints limit access to powered systems, traditional tools are the only viable option, ensuring baseline care continuity. Even in advanced clinics, they serve as indispensable complements to high-tech modalities for fine margin refinement. Procurement is increasingly streamlined through national, electronic tender systems and central purchasing bodies, which aim to leverage bulk purchasing to reduce unit costs and improve efficiency. Their simplicity, reliability, and regulatory familiarity make them the backbone of debridement practice despite the rise of innovative alternatives.

The low-frequency ultrasound devices segment is estimated to register the fastest CAGR of 12.1% between 2026 and 2034. The rapid growth of the segment is fuelled by its dual action of debridement and biostimulation, which accelerates healing while minimizing tissue trauma. Devices emit sound waves at 20 to 40 kilohertz, creating microbubbles that disrupt biofilm and loosen necrotic material without damaging viable cells. Randomized controlled trials indicate that low-frequency ultrasound debridement is an effective, less painful, and generally faster alternative for healing chronic wounds compared to standard surgical care, often resulting in lower pain scores. The European Commission is funding digital technology and tele-health initiatives, which include, in certain regions, pilot projects aimed at enhancing home-based treatment through remote supervision. Reimbursement is expanding, too. The Federal Joint Committee (G-BA) in Germany continues to regulate and evaluate the reimbursement of various wound care devices and methods, with ongoing discussions about the coverage of advanced therapeutic technologies. Increasing evidence and broader training are transforming this technology from an optional tool into an essential part of wound management.

COUNTRY LEVEL ANALYSIS

Germany Wound Debridement Products Market Analysis

Germany was the top performer in the Europe Wound Debridement Products Market and accounted for a 23.5% share in 2025. The dominance of the German market is attributed to its sophisticated healthcare infrastructure and high prevalence of chronic wounds. The country's position is reinforced by an aging demographic that drives significant demand for treatments targeting diabetic foot ulcers and pressure injuries. As per the German Federal Statistical Office, over twenty percent of the population is aged sixty five or older, creating a vast patient pool requiring regular debridement to prevent infection and promote healing. The German healthcare system mandates strict quality standards for wound care, encouraging the adoption of advanced enzymatic and autolytic debridement agents over traditional surgical methods. According to research, there is a strong clinical consensus on the importance of early and effective debridement, which fuels consistent consumption of premium products. Furthermore, the presence of leading medical device manufacturers and research institutions fosters a culture of innovation where new debridement technologies are rapidly validated and integrated into clinical practice. The robust reimbursement framework ensures that patients have access to high-cost-effective therapies, removing financial barriers to optimal care. This synergy of demographic necessity, clinical rigor, and industrial capability ensures Germany maintains its top position as the primary driver of market volume and technological advancement in the European region.

United Kingdom Wound Debridement Products Market Analysis

The United Kingdom followed closely in the Europe Wound Debridement Products Market because of its centralized National Health Service, which drives standardized adoption of evidence-based debridement guidelines across the nation. The British market is showing a strong shift towards community-based care, where district nurses perform the majority of wound debridement procedures outside hospital settings. Rising rates of diabetes and obesity are contributing to an increased prevalence of chronic wounds, creating a need for effective, comfortable, and self-care-friendly wound management solutions. The National Institute for Health and Care Excellence provides clear recommendations on wound management that prioritize autolytic and enzymatic methods to reduce patient trauma and accelerate healing times. There is a noticeable shift in clinical practice toward using gentle mechanical and/or moist-based methods to enhance patient comfort during wound management. The government's focus on reducing hospital admissions through effective community care has boosted procurement of advanced debridement kits for primary care trusts. Additionally, the UK serves as a key testing ground for new digital wound assessment tools that guide debridement frequency and technique. This combination of structured clinical governance, demographic pressure, and a mature home care sector solidifies the UK's role as a critical and dynamic market for wound debridement innovations.

France Wound Debridement Products Market Analysis

France is another key player in the Europe Wound Debridement Products Market due to its excellence in specialized burn centers, trauma care units, and a strong emphasis on aesthetic outcomes in wound healing. The French market is also supported by a network of highly specialized hospitals that treat complex wounds requiring aggressive yet precise debridement strategies to minimize scarring and functional loss. As per sources, there is a growing international consensus, supported by expert Italian users and European studies, favoring bromelain-based enzymatic debridement for early, selective eschar removal in burns, often leading to reduced surgery and grafting. The country's robust public health insurance system ensures comprehensive coverage for advanced wound care products, enabling widespread access to high-quality debridement therapies. Modern burn care is shifting toward faster, selective, and less invasive debridement techniques, including enzymatics and hydrodissection, to improve scar quality and reduce surgical trauma. The aging population in France also contributes to the demand for pressure ulcer management in long-term care facilities, where regular debridement is essential to prevent sepsis. Furthermore, the presence of major pharmaceutical companies fosters local research into novel enzyme formulations tailored for specific wound types. The convergence of specialized medical expertise, supportive reimbursement policies, and a focus on quality of life ensures France remains a key driver of value and sophistication in the European wound debridement landscape.

Italy Wound Debridement Products Market Analysis

Italy is moving ahead steadfastly in the Europe wound debridement products market owing to the urgent need to manage non-healing wounds in an elderly population, particularly in the southern regions where diabetes rates are elevated. The country has a high prevalence of chronic venous leg ulcers and a healthcare system that is increasingly harmonizing standards across its diverse regions. As per the Italian National Institute of Statistics, the proportion of citizens over sixty-five continues to rise, correlating directly with the increased incidence of vascular complications that require frequent debridement. The Italian Ministry of Health has launched initiatives to standardize wound care protocols nationwide, promoting the adoption of modern autolytic and enzymatic debridement techniques over outdated surgical practices. According to multiple studies, there is a growing awareness among clinicians regarding the benefits of moisture-balanced debridement that reduces pain and accelerates epithelialization. The decentralized nature of the healthcare system leads to varied procurement patterns, yet the overall demand remains robust due to the sheer volume of chronic cases. Additionally, the strong tradition of dermatological research in Italy supports the clinical evaluation of new debridement matrices and gels. The interplay of demographic challenges, regulatory harmonization efforts, and clinical dedication ensures Italy remains a significant and evolving market for wound debridement solutions.

Spain Wound Debridement Products Market Analysis

Spain is an emerging player in the Europe Wound Debridement Products Market due to its expanding network of wound care units, rising diabetes prevalence, and increasing adoption of integrated care models for chronic patients. The Spanish market exhibits a proactive approach to managing complex wounds within primary care settings, reducing the burden on specialized hospitals. As per research, the rate of diabetes mellitus has reached alarming levels, making diabetic foot ulcers a major public health concern that necessitates effective debridement strategies to prevent amputations. The Spanish Ministry of Health has implemented national strategies for the care of chronic wounds, encouraging the use of advanced debridement products that offer selectivity and ease of use. There is a significant, evidence-based shift towards adopting rapid, selective, non-invasive debridement methods like hydrosurgical devices and enzyme-based therapies to enhance outpatient efficiency. The growing emphasis on telemedicine allows remote specialists to guide local nurses in performing appropriate debridement, expanding access to expert care in rural areas. Furthermore, the economic recovery has led to increased investment in public health infrastructure, facilitating the procurement of modern wound care supplies. The combination of rising disease burden, strategic policy interventions, and technological integration ensures Spain represents a vital and rapidly growing opportunity for the wound debridement industry in Europe.

COMPETITIVE LANDSCAPE

The Europe wound debridement products market features intense competition among multinational medtech leaders, regional specialists, and emerging innovators vying for adoption in a clinically complex and regulation-heavy environment. Global players like Smith & Nephew, 3M, and ConvaTec dominate through integrated portfolios, robust clinical evidence, and established hospital relationships. Niche firms such as Lohmann & Rauscher and B. Braun compete on specialized offerings like single-use instruments or larval therapy, catering to specific clinical preferences. The implementation of the EU Medical Devices Regulation has raised entry barriers favoring companies with resources to navigate conformity assessments, yet it has also spurred partnerships between startups and larger distributors. Reimbursement disparities across member states create a two-tier market where advanced modalities thrive in wealthier nations while basic tools prevail in resource-constrained regions. Despite these challenges, innovation in biofilm-targeted agents, portable ultrasound, and telehealth integration continues to reshape the competitive landscape, rewarding those who align clinical efficacy with operational practicality and regulatory foresight.

KEY MARKET PLAYERS

The leading companies operating in the Europe wound debridement products market include:

- Coloplast A/S

- ArthroCare Corporation

- ConvaTec Group plc

- Misonix, Inc.

- 3M Company

- MediWound Ltd

- Derma Sciences, Inc.

- PuriCore plc

- Smith & Nephew Plc

TOP PLAYERS IN THE MARKET

- Smith & Nephew plc, a UK-based global medical technology company, is a leader in advanced wound management with a comprehensive portfolio of debridement solutions, including the VERSAJET Hydrosurgery System and enzymatic debriding gels. The company plays a pivotal role in European clinical practice by supporting evidence-based protocols through partnerships with wound care societies and national health systems. Smith & Nephew has enhanced its wound care portfolio by integrating digital monitoring capabilities, such as the LEAF patient monitoring system, to assist in pressure injury prevention and management. Smith & Nephew continues to expand its medical education initiatives through the Smith & Nephew Academy, providing training in advanced techniques like hydrosurgery to address workforce skill gaps across Europe.

- 3M Company leverages its materials science expertise to deliver innovative wound debridement products, including mechanical debridement pads, antimicrobial dressings, and single-use surgical instruments, widely used in European hospitals and clinics. The company strengthens its position through localized manufacturing in Germany and the Netherlands, ensuring supply chain resilience and regulatory compliance under the EU Medical Devices Regulation. A collaboration was announced for a next-generation enzymatic debridement agent based on bromelain, aimed at efficiently removing necrotic tissue in chronic wounds without impacting viable tissue. It also enhanced its clinician education programs across Southern Europe, focusing on biofilm recognition and selective debridement strategies to improve outcomes in chronic wounds.

- ConvaTec Group plc, headquartered in the United Kingdom, is a key player in the European wound debridement market through its AQUACEL Ag+ Extra and Debrisoft products, which combine autolytic and mechanical debridement with infection control. The company actively collaborates with national wound care networks in France, Italy, and Sweden to embed its solutions into standardized treatment pathways. ConvaTec continues to promote its "Wound Hygiene" protocol for clinical practice, which is designed to improve wound management, including debridement and cleansing, supporting improved patient outcomes in various care settings. Also, ConvaTec is working towards MDR certification of its portfolio, adhering to the updated EU timelines to ensure compliance and maintain confidence among clinicians.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe wound debridement products market focus on clinical evidence generation, regulatory compliance, digital integration, and workforce education to sustain a competitive advantage. Companies are investing in randomized controlled trials and real-world data studies to validate the cost-effectiveness and healing acceleration of their debridement modalities. Full compliance with the EU Medical Devices Regulation is prioritized through early certification and transparent technical documentation. Digital platforms that link debridement procedures to electronic health records enhance documentation accuracy and support value-based reimbursement. Strategic collaborations with wound care associations and national health services embed products into standardized protocols. Additionally, firms are expanding training academies and e learning modules to address the shortage of skilled practitioners, ensuring proper technique and consistent outcomes across diverse care settings.

MARKET SEGMENTATION

This research report Europe wound debridement products market has been segmented and sub-segmented into the following categories.

By Method of Debridement

- Selective Methods

- Larvae Debridement Therapy Or Bio-Surgical Debridement

- Enzymatic Or Chemical Debridement

- Autolytic Debridement

- Non-Selective Methods

- Mechanical Debridement

- Ultrasound

- Sharp And Surgical Debridement

By Type of Wound

- Acute Wounds

- Surgical Wounds

- Traumatic Wounds

- Abrasions

- Necrotizing Fasciitis

- Lacerations

- Contusions

- Toxic Epidermal Necrolysis

- Burn Wounds

- Chemical Burns

- Electrical Burns

- Flash Burns

- Radiation Burns

- Thermal Burns

- Chronic Wounds

- Diabetic Ulcers

- Venous Ulcers

- Pressure Ulcers

By Product

- Hydrological Debridement Devices

- Low-Frequency Ultrasound Devices

- Surgical Wound Debridement Devices

- Mechanical Debridement Pads

- Traditional Wound Debridement Devices

- Larval Therapy

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe wound debridement products market?

The Europe wound debridement products market supplies tools removing necrotic tissue from chronic wounds like diabetic ulcers. Hydrosurgical and ultrasound options lead adoption.

Why is the Europe wound debridement products market growing?

Growth in the Europe wound debridement products market stems from rising diabetes, burns, and aging populations. Reimbursement boosts access in hospitals and clinics.

Which country dominates the Europe wound debridement products market?

UK dominates the Europe wound debridement products market with high chronic wound incidence. Germany grows via diabetes prevalence and advanced care infrastructure.

What product types lead the Europe wound debridement products market?

Hydrosurgical devices lead the Europe wound debridement products market for precise tissue removal. Mechanical, ultrasound, and gels support diverse wound needs.

How do hospitals use the Europe wound debridement products market?

Hospitals apply the Europe wound debridement products market for treating surgical wounds and ulcers. Devices speed healing and reduce infection risks effectively.

What trends shape the Europe wound debridement products market?

Trends in the Europe wound debridement products market include minimally invasive tech and bioactive agents. Focus on outpatient care expands product accessibility.

How does diabetes drive the Europe wound debridement products market?

Diabetes fuels the Europe wound debridement products market via foot ulcer prevalence. Products target necrotic removal for faster recovery in affected patients.

What challenges exist in the Europe wound debridement products market?

Challenges in the Europe wound debridement products market involve high device costs and training needs. Standardization efforts aid wider clinical adoption.

Which companies influence the Europe wound debridement products market?

Companies like Smith & Nephew and Coloplast shape the Europe wound debridement products market with innovative hydrosurgical and enzymatic solutions.

How has aging impacted the Europe wound debridement products market?

Aging populations boost the Europe wound debridement products market with more chronic wounds. Home care shifts increase demand for user-friendly devices.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com