Global Full Body Scanners Market Size, Share, Trends & Growth Forecast Report By Technology, By Type, By End Use, and By Region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa) – Industry Analysis and Forecast, 2026 to 2034

Global Full Body Scanners Market Report Summary

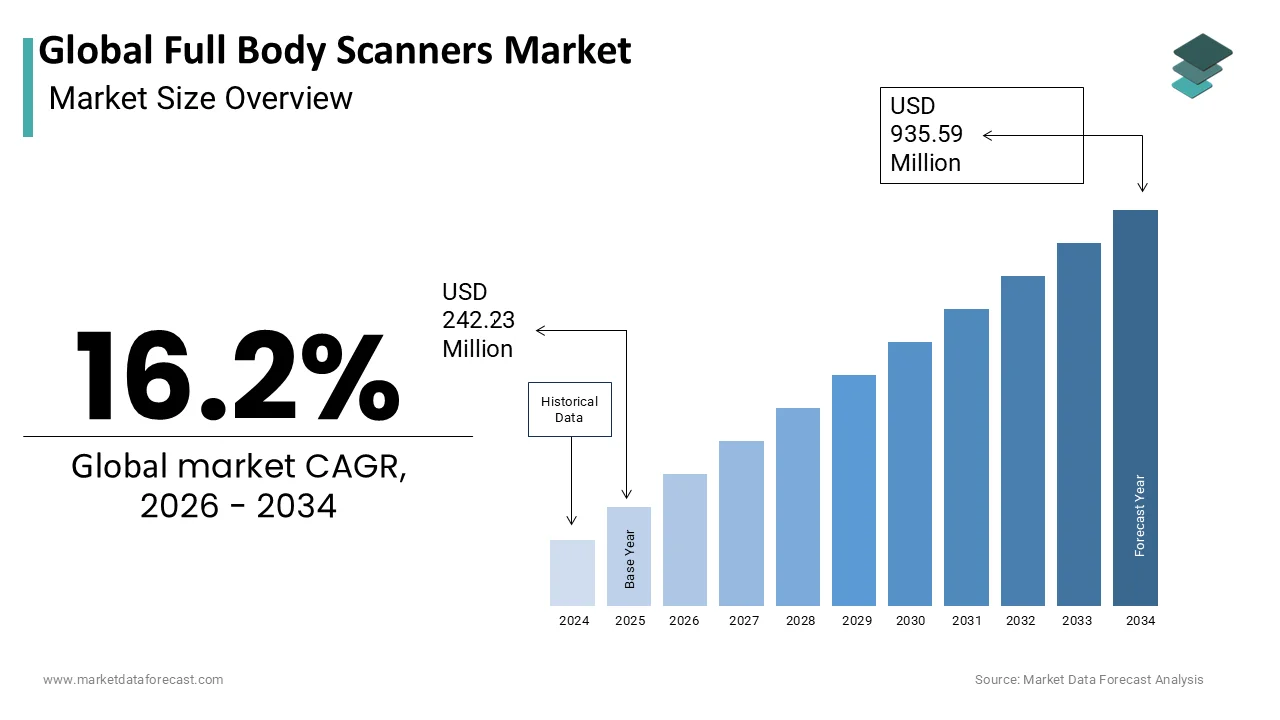

The Global Full-Body Scanner Market was valued at USD 242.23 million in 2025 and is projected to reach USD 935.59 million by 2034, growing from USD 281.47 million in 2026 at a CAGR of 16.20% during the forecast period. Growth is driven by rising global air passenger traffic, stringent aviation security mandates requiring advanced imaging technology, and expansion into non-aviation sectors like prisons and government buildings. Privacy concerns and high capital costs are shaping market dynamics.

Key Market Trends

- Rising integration of AI-assisted image analysis to reduce false alarm rates

- Growing adoption of millimeter-wave scanners over legacy X-ray backscatter systems

- Increasing deployment of full-body scanners in prisons and critical infrastructure

- Expansion of 3D imaging systems to eliminate blind spots in threat detection

- Growing public education efforts to address radiation exposure misconceptions

Segmental Insights

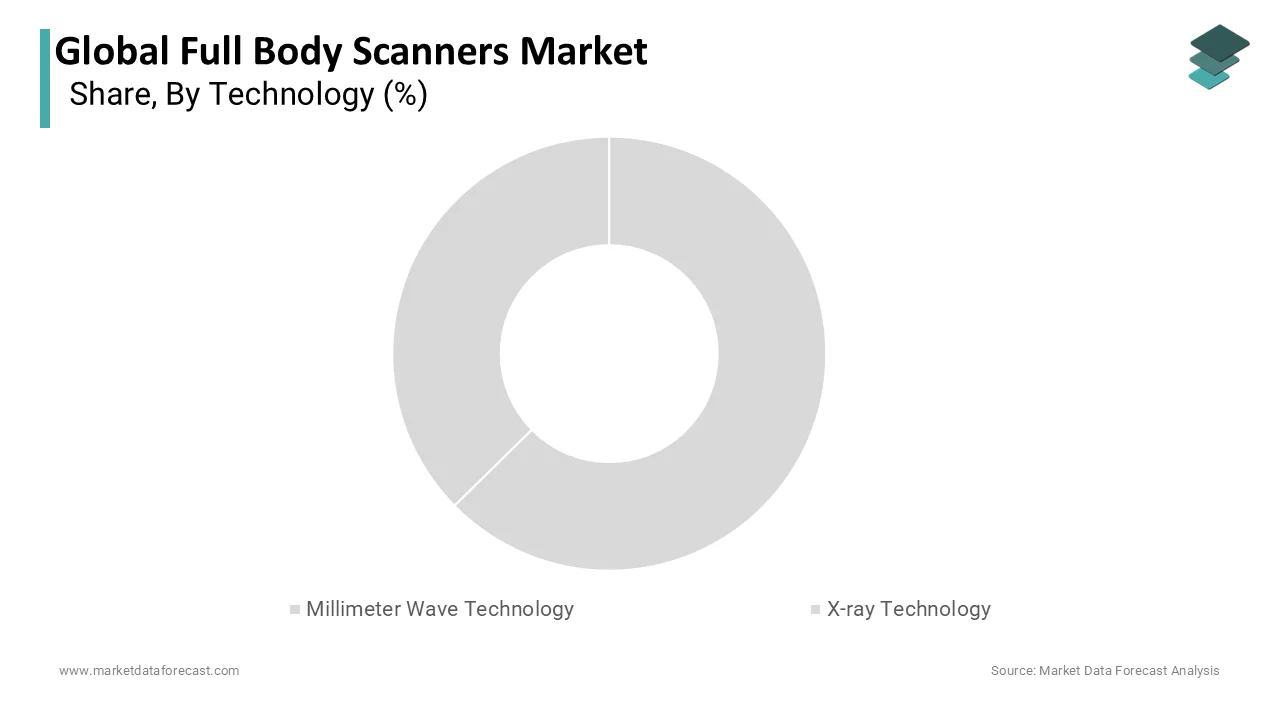

- Based on technology, millimeter wave held the largest share in 2025 at 54.3%, driven by its superior safety profile and non-ionizing radiation.

- Based on type, 3D view scanners captured the largest share in 2026 at 46.4%, driven by comprehensive spatial threat detection from any angle.

- Based on end-use, airports held a significant share in 2025, driven by mandatory regulatory requirements and massive passenger volumes.

Regional Insights

- North America led the market in 2025 by holding 35.3% of the global market share, supported by early technology adoption and stringent regulatory frameworks.

- Europe holds a significant share at 21.3%, driven by EU Aviation Safety Agency mandates and GDPR-influenced privacy requirements.

- Asia Pacific is expected to witness the fastest growth during the forecast period, driven by massive airport construction in China and rising middle-class travel demand.

Competitive Landscape

The market is highly competitive, with companies focusing on imaging resolution, privacy protection features, and integration with existing security infrastructure. Companies are investing in AI-driven threat detection and modular scalable systems to serve airports and government clients globally.

Prominent players in the market include OSI Systems Inc. (Rapiscan Systems), Smiths Detection Group Ltd., Leidos Holdings Inc., Rohde & Schwarz GmbH & Co. KG, Nuctech Company Limited, Thales Group, L3Harris Technologies Inc., Tek84 Inc., Westminster Group plc, Analogic Corporation, Bruker Corporation, and Astrophysics Inc.

Global Full Body Scanners Market Size

The Global Full-body Scanner Market is projected to grow from USD 242.23 million in 2025 to USD 281.47 million in 2026 and reach USD 935.59 million by 2034, registering a CAGR of 16.2% during the forecast period from 2026 to 2034.

The full-body scanners are advanced security screening technologies designed to detect concealed weapons, explosives,s and contraband on individuals without physical contact. These systems utilize millimeter-wave technology or backscatter X-ray imaging to create detailed three-dimensional representations of the human body, allowing security personnel to identify threats hidden under clothing. The deployment of these devices has become standard practice at major international airports following regulatory mandates that prioritize non-invasive yet thorough screening protocols. The European Union Aviation Safety Agency enforces strict standards requiring member states to implement approved security equipment that balances passenger privacy with threat detection capabilities. Airports, such as Heathrow and Dubai International, handle tens of millions of passengers each year,r relying heavily on automated scanning solutions to minimize queue times. The technology has evolved from controversial early models to privacy-preserving systems that display generic avatars rather than explicit images, addressing public concerns. Government agencies worldwide continue to invest in next-generation scanners capable of detecting non-metallic threats that traditional metal detectors miss.

MARKET DRIVERS

Rising Global Air Passenger Traffic Drives Equipment Demand

Global air travel is positively impacting the growth of the full-body scanners market. Airlines and airport authorities face increasing pressure to process larger crowds efficiently while maintaining stringent security checks that prevent unauthorized items from entering secure areas. Manual screening processes are labor-intensive and time-consuming, often requiring several minutes per passenger, whereas automated scanners can process individuals in seconds. Heathrow Airport in London reported processing over 80 million passengers in recent years, illustrating the sheer volume that necessitates technological intervention to prevent excessive queuing times. The World Tourism Organization states that international tourist arrivals exceeded 1.3 billion globally,y placing immense strain on border and security infrastructure in popular destinations. Airport operators recognize that prolonged wait times negatively impact customer satisfaction and operational efficiency,cy driving investment in high-throughput screening solutions. Full-body scanners allow security agencies to reallocate human resources to complex cases requiring detailed scrutiny rather than routine verification tasks. This shift improves overall security posture by enabling officers to focus on high-risk individuals while low-risk travelers experience expedited clearance. The scalability of these systems allows airports to adjust capacity dynamically based on flight schedules and seasonal demand fluctuations, ensuring consistent service levels during peak travel periods.

Stringent Regulatory Mandates Enforce Advanced Screening Standards

Governments worldwide are implementing stricter aviation security mandates that require advanced imaging technology capabilities only achievable through modern full-body scanners. The stringent regulatory mandates enforce advanced screening standards, which is also a prominent factor boosting the growth of the full body scanners market. Regulatory bodies demand higher accuracy in threat detection to combat sophisticated concealment methods used by malicious actors, including non-metallic explosives and ceramic weapons. The United States Transportation Security Administration mandated the deployment of Advanced Imaging Technology at all major commercial airports, ts replacing older metal detector systems that failed to detect many modern threats. According to the study, the transition to millimeter wave scanners was completed across hundreds of checkpoints to ensure uniform security standards nationwide. The regulations require member states to use approved security equipment that meets specific performance criteria for detecting prohibited articles. The new annexes to the Convention on International Civil Aviation encourage the adoption of standardized screening technologies to facilitate interoperability between different national systems. These regulatory frameworks compel airports and security agencies to upgrade legacy equipment to meet compliance deadlines or face penalties and operational restrictions. The push for harmonized security standards also drives the adoption of scanners that can integrate with central monitoring systems and provide real-time data analytics. Security agencies prioritize systems that offer audit trails and remote management capabilities, features inherent in modern digital scanning solutions.

MARKET RESTRAINTS

High Capital Expenditure and Maintenance Costs Restrict Adoption

The substantial capital expenditure required for deploying advanced features is hindering the growth of the full-body scanners market. A single advanced imaging unit involves sophisticated hardware, including sensitive sensors, high-performance computing modules,s and specialized shielding, along with complex installation costs. Smaller regional airports often lack the financial resources to undertake such investments without external funding or government subsidies. The total cost of ownership includes ongoing maintenance, software updates, and calibration, which further strains operational budgets. As per the research, many airports in Africa and Latin America operate with tight margins, making large upfront technology investments challenging despite long-term security benefits. Budget constraints force these facilities to rely on older metal detection systems or manual pat downs that do not offer the same level of threat detection or throughput efficiency. The complexity of integrating scanners with existing security infrastructure and baggage handling systems adds to the implementation burden, requiring specialized expertise that may not be locally available. Financial institutions and leasing options exist but often come with high interest rates or stringent conditions that deter potential buyers.

Privacy Concerns and Public Acceptance Issues Hinder Deployment

The growing public awareness regarding personal privacy and bodily integrity that generates detailed images of passengers is also impeding the growth of the full-body scanners market. Travelers express apprehension about how their bodily images are captured, stored,d and viewed by security personnel, el raising ethical and legal questions. According to a survey, nearly 40% of passengers cite privacy invasion as a major concern when undergoing advanced imaging screening. The American Civil Liberties Union has historically challenged the use of certain scanning technologies, arguing that they constitute unreasonable searches under constitutional protections. The strict limitations on the processing of biometric and personal data require explicit consent and robust security measures that complicate system deployment. Incidents of image leakage or misuse in other sectors heighten skepticism about the safety of databases managed by government agencies or private vendors. As per privacy advocates, the lack of transparency in how images are deleted after screening raises fears of unauthorized retention and potential abuse. Legal challenges in various jurisdictions have delayed or halted scanner projects due to insufficient safeguards for individual rights. Public trust is essential for the smooth operation of these systems, and negative publicity surrounding privacy violations can lead to boycotts or political pressure to remove installed equipment.

MARKET OPPORTUNITIES

Integration with Artificial Intelligence Enhances Detection Capabilities

The emergence of full-body scanners with artificial intelligence and machine learning algorithms creates innovative opportunities for improved threat detection and operational efficiency. The integration with artificial intelligence is expected to fuel the growth of the full-body scanners market. Modern scanners generate vast amounts of data that can be analyzed by AI systems to identify subtle anomalies indicative of concealed threats with greater accuracy than human operators. The pilot programs using AI-assisted image analysis have shown significant improvements in detection rates for non-metallic weapons and explosives. This technology reduces the cognitive load on security officers who no longer need to interpret complex images manually, allowing them to focus on decision-making and passenger interaction. AI integration can reduce false alarm rates by up to 30%, minimizing unnecessary secondary screenings and improving passenger flow, as per the study. The ability of machine learning models to continuously learn from new threat patterns ensures that scanning systems remain effective against evolving concealment techniques. Governments are increasingly interested in smart security ecosystems where scanners communicate with other sensors and databases to provide a comprehensive risk assessment for each passenger. This trend supports the development of automated lanes where multiple biometric and scanning technologies work in concert to verify identity and screen for threats simultaneously. Technology providers that successfully integrate AI capabilities into their scanner solutions gain a competitive advantage by offering superior performance metrics and lower operational costs for clients.

Expansion into Non-Aviation Security Sectors Presents Growth Potential.

The application of full-body scanners is expanding beyond airports to prisons, courthouses,s government buildings, gs and infrastructure sites, opening new revenue streams for technology providers. The expansion into non-aviation security sectors is in addition to leveraging the growth of the full-body scanners market. Traditional security measures in these environments often rely on metal detectors and manual searches, which are ineffective against modern non-metallic threats. Prisons face significant challenges with drugs and weapons being smuggled in by visitors or staff, creating demand for thorough non-invasive screening solutions. Courthouses and legislative buildings also present opportunities for high-profile incidents, amplifying vulnerabilities in existing security protocols. The federal facilities are increasingly adopting advanced imaging technology to protect judges, lawyers,s and public servants from armed threats. Corporate campuses and data centers are another emerging segment where protection of intellectual property and personnel drives investment in high-security screening. These diverse applications require ruggedized hardware designs capable of withstanding high usage frequencies and varying environmental conditions, offering manufacturers chances to develop specialized product lines. Government initiatives to enhance public safety and reduce crime often include funding for security upgrades, providing financial incentives for adoption in these emerging segments.

MARKET CHALLENGES

Operational Complexity and False Alarm Rates Affect Efficiency

Full-body scanners face operational challenges related to false alarm rates and the complexity of interpreting scan results, which can disrupt passenger flow and increase staffing requirements. The operational complexity and false alarm rates affect efficiency, which is a major factor hindering the growth of the full-body scanners market. Each false alarm requires a security officer to perform a targeted pat-down or additional inspection, consuming valuable time and resources. Training personnel to accurately distinguish between genuine threats and benign anomalies is a continuous challenge requiring regular recertification and skill maintenance. The psychological stress on operators who must maintain high levels of concentration while viewing numerous images daily can lead to fatigue and decreased performance over time. System downtime due to technical glitches or calibration issues can cause significant backlogs, negating the efficiency benefits of automation. Operators must maintain sufficient staff to handle exceptions and failures,s limiting the extent to which human resources can be reduced. Balancing sensitivity to detect small threats with specificity to avoid false alarms remains a critical engineering challenge that impacts user satisfaction and security effectiveness. Continuous software updates and hardware maintenance are required to keep false alarm rates within acceptable limits, ts adding to the operational burden.

Health and Safety Perceptions Create Public Resistance

The persistent public misconceptions regarding the health effects of radiation exposure from full-body scanners create resistance and reluctance among certain passenger demographics. The health and safety perceptions are also limiting the growth of the full-body scanners market. Although millimeter wave technology uses non-ionizing radio waves similar to those used in mobile phones, public perception often conflates it with ionizingX-rayy radiation, which carries known health risks. The millimeter wave scanners emit energy levels thousands of times lower than safety limits and pose no known health risks,s yet anecdotal fears persist. Backscatter X-ray systems, which were previously more common, have been largely phased out in favor of millimeter wave due to these concerns, but historical stigma remains. This hesitation can lead to passengers opting out of scanning in favor of manual pat-downs,s which are more intrusive and time-consuming, thereby reducing the overall efficiency of the security checkpoint. Airport authorities must invest in public education campaigns to clarify the safety profile of modern scanners,s but changing deeply held beliefs is difficult. Legal requirements in some jurisdictions mandate that alternative screening methods be available for those who refuse scanning, ng further complicating operations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Technology, Type, End Use, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | OSI Systems, Inc. (Rapiscan Systems), Smiths Detection Group Ltd., Leidos Holdings, Inc., Rohde & Schwarz GmbH & Co. KG, Nuctech Company Limited, Thales Group, L3Harris Technologies, Inc., Tek84 Inc., Westminster Group plc, Analogic Corporation, Bruker Corporation, Astrophysics Inc. |

SEGMENTAL ANALYSIS

By Technology Insights

The millimeter wave technology segment was the largest by holding 54.3% of the full body scanners market share in 2025 due to its superior safety profile and enhanced privacy features compared to X-ray-based systems. This technology utilizes non-ionizing radio waves that pose no known health risks to passengers, making it highly acceptable for high-volume public screening environments. The millimeter wave scanners emit energy levels significantly lower than international safety limits, ensuring passenger safety during frequent exposure. The advanced imaging technology units deployed in United States airports now utilize millimeter wave technology,y reflecting a decisive industry shift away from backscatter X-ray systems. The ability of millimeter wave scanners to detect both metallic and non-metallic threats, including ceramics, plastics, and liquids,s provides comprehensive security coverage that traditional metal detectors cannot match. Regulatory mandates in North America and Europe have effectively standardized this technology as the preferred solution for aviation security checkpoints. Manufacturers have invested heavily in improving the resolution and speed of millimeter wave sensors,ors allowing for faster processing times that meet the demands of busy international hubs.

The X-ray technology segment is lucratively growing at the fastest CAGR of 4.2% from 2026 to 2034, with applications in correctional facilities and high-security government buildings where privacy concerns are secondary to threat detection precision. While largely phased out in commercial aviation due to radiation concerns, X-ray backscatter technology offers superior image clarity for detecting thin materials and organic substances that millimeter wave systems might miss. Many federal prisons and detention centers continue to rely on X-ray-based full-body scanners because they provide detailed visual evidence required for contraband investigations and legal proceedings. The Bureau of Prisons reports that contraband smuggling remains an issue with thousands of incidents reported annually, necessitating high-resolution imaging capabilities that X-ray systems provide. In industrial settings, such as nuclear power plants and military bases, X-ray scanners are preferred for their ability to penetrate thicker clothing and protective gear worn by workers. The technology is also gaining traction in cargo screening applications where detailed internal views of packages and vehicles are essential for identifying hidden explosives or narcotics. Advances in low-dose X-ray technology have mitigated some health concerns, allowing for safer deployment in controlled environments where operators can maintain safe distances.

By Type Insights

The 3D view scanners segment was the largest by capturing 46.4% of the full body scanners market share in 2026 due to their ability to provide comprehensive spatial analysis and eliminate blind spots inherent in single- or dual-view systems. These advanced systems rotate around the subject or utilize multiple sensor arrays to create a complete three-dimensional model of the individual, enabling security personnel to detect threats from any angle. The next generation security standards encourage the adoption of 3D imaging technologies to improve detection accuracy for complex concealment methods. Major airports, such as Changi in Singapore and Heathrow in London, have deployed 3D-capable scanners to handle high passenger volumes while maintaining rigorous security protocols. 3D visualization allows operators to manipulate images digitally, zooming in on specific areas of interest without requiring the passenger to undergo additional physical screening. This capability significantly reduces secondary inspection rates and improves overall checkpoint efficiency. The integration of 3D data with artificial intelligence algorithms enhances automated threat recognition by providing richer datasets for machine learning models to analyze. Manufacturers report that 3D scanners have higher initial costs but offer better long-term value through reduced false alarms and faster processing times. The technology’s ability to distinguish between harmless items like medical devices and actual threats reduces passenger inconvenience and enhances the travel experience.

The single-view scanners segment is likely to register the fastest CAGR of 2.8% from 2026 to 2034, with the replacement cycles in smaller airports and budget-constrained facilities that do not require the advanced capabilities of 3D systems. These units provide a two-dimensional image from a single perspective, which is sufficient for basic threat detection in low-risk environments. Many regional airports in developing countries continue to operate single-view scanners due to their lower acquisition and maintenance costs. The simplicity of single-view technology makes it easier to train operators and maintain equipment, requiring less specialized technical support. Single-view scanners are often used as supplementary screening tools in conjunction with metal detectors rather than primary screening devices in high-traffic hubs. Their compact footprint allows for installation in space-constrained areas such as small terminal buildings or temporary security checkpoints. While they lack the comprehensive coverage of 3D systems, single-view scanners remain effective for detecting larger concealed items and metallic objects. Government subsidy programs in emerging markets often fund the purchase of basic scanning equipment to improve baseline security standards across national airport networks. The steady demand for these units ensures a consistent revenue stream for manufacturers offering cost-effective solutions for entry-level security requirements.

By End-use Insights

The airports segment held a significant share of the full-body scanners market in 2025 due to mandatory regulatory requirements and massive passenger volumes. International aviation security regulations compel airports to deploy advanced imaging technology at all passenger screening checkpoints to detect non-metallic threats. Major hubs like Dubai International and Los Angeles International process tens of millions of passengers annually, requiring extensive networks of full-body scanners to prevent hurdles. The United States alone operates over 5000 advanced imaging units across its commercial airports, representing a significant portion of global installations. The high value of aviation assets and the catastrophic potential of security breaches justify substantial investment in premium scanning technologies. Airport authorities prioritize systems that offer high throughput and low false alarm rates to maintain schedule reliability and passenger satisfaction. Government funding and airport improvement fees often subsidize the procurement of these expensive systems,s ensuring widespread adoption. The continuous expansion of airport infrastructure in emerging markets further drives demand as new terminals are equipped with state-of-the-art security screening lanes.

The critical infrastructure segment is likely to grow at the fastest CAGR of 6.5% from 2026 to 2034, with increasing geopolitical tensions and domestic security threats. These facilities require robust screening measures to protect sensitive assets and personnel from insider threats and unauthorized access. The federal facilities in the United States have upgraded security protocols following several high-profile incidents, resulting in increased procurement of full-body scanners. The Department of Energy mandates strict access control measures for nuclear power plants and research facilities where conventional metal detectors are insufficient for detecting non-metallic explosives. As per the General Services Administration, numerous federal office buildings have installed advanced imaging technology to screen visitors and employees entering secure zones. The rise in corporate espionage and intellectual property theft has also prompted private sector critical infrastructure owners such as data centers and pharmaceutical manufacturing plants to adopt similar screening technologies. Government initiatives to harden critical infrastructure against terrorism and sabotage provide funding opportunities for security upgrades. The specialized nature of these installations requires ruggedized and highly secure scanner models that can integrate with existing access control systems.

COUNTRY LEVEL ANALYSIS

North America Full Body Scanners Market Analysis

North America was the largest contributor by holding 35.3% of the global full-body scanners market share in 2025, owing to the early adoption of advanced technologies and stringent regulatory frameworks. The US operates the largest network of full-body scanners globally, with thousands of units deployed across hundreds of airports. Canada Border Services Agency has also implemented advanced screening technologies at major international airports to align with US security standards and facilitate cross-border travel. The region benefits from the presence of major scanner manufacturers and technology developers who drive innovation in biometric integration and artificial intelligence. Strong government funding for homeland security ensures continuous upgrades and replacements of aging equipment. Privacy regulations in the region have shaped the development of automated target recognition software that protects passenger identity while maintaining security effectiveness. Collaboration between government agencies and private sector vendors facilitates the rapid deployment of next-generation screening capabilities.

Europe Full Body Scanners Market Analysis

Europe full body scanners market was next, holding 21.3% of the share in 2025, with the European Union Aviation Safety Agency regulations that mandate standardized security equipment across member states. The region has largely adopted millimeter wave technology due to strict General Data Protection Regulation requirements that prioritize passenger privacy and data protection. All EU member states must comply with common basic standards for aviation security, which include the use of approved advanced imaging technology. Major airports have deployed extensive scanner networks to handle high volumes of international transit passengers. European airports processed over 900 million passengers in recent years,s necessitating efficient screening solutions to maintain competitiveness, as per the study. The United Kingdom continues to invest in advanced security technologies post Brexit to maintain its status as a global aviation hub. Regional manufacturers like Smiths Detection benefit from home market advantages and a deep understanding of local regulatory requirements. Government funding through the Connecting Europe Facility supports infrastructure modernization projects, including security upgrades at smaller regional airports. The focus on harmonized security standards facilitates interoperability and mutual recognition of screening results across borders. Ongoing threats from terrorism and organized crime maintain political support for continued investment in advanced screening technologies.

Asia Pacific Full Body Scanners Market Analysis

Asia Pacific full-body scanners market is anticipated to grow at the fastest CAGR in the coming years, with the massive infrastructure development and rising middle-class travel demand. China leads regional expansion with plans to construct over 200 new airports by 2035, according to the study. India’s Airport Authority of India is upgrading security infrastructure at major hubs like Delhi and Mumbai to handle growing passenger volumes and meet international safety standards. Southeast Asian nations, including Singapore, Thailand, and Malaysia, are investing in smart airport initiatives that include advanced full-body scanners as core components. Government initiatives to boost tourism and facilitate trade drive the adoption of efficient screening technologies that minimize wait times. Local partnerships with international vendors facilitate technology transfer and local assembly, reducing costs and improving service support. The region’s diverse regulatory landscape requires vendors to offer flexible solutions that comply with varying national standards. Increasing awareness of aviation security threats among regional governments supports sustained investment in advanced screening capabilities.

Latin America Full Body Scanners Market Analysis

Latin America full body scanners market growth is driven by tourism recovery and infrastructure concession programs. Mexico’s airport privatization program has triggered security upgrades at Cancun and Mexico City International Airport to improve the passenger experience and meet US security pre-clearance requirements. Chile serves as a regional hub connecting South America with Asia Pacific and Oceania, driving scanner deployment at Santiago’s Arturo Merino Benitez Airport. Government tourism promotion strategies emphasize security and facilitation as competitive advantages for attracting international visitors. Infrastructure concessions to private operators often include mandatory security upgrade commitments that guarantee scanner procurement. Regional integration initiatives aim to harmonize security procedures and technology standards across neighboring countries. Economic volatility and currency fluctuations create procurement challenges,s but long-term growth fundamentals remain positive. Local partnerships with international vendors facilitate maintenance capability development and technical support.

Middle East and Africa Full Body Scanners Market Analysis

The Middle East and Africa full-body scanners market growth is driven by the significant strategic development opportunities driven by mega projects and regional connectivity initiatives. Gulf Cooperation Council states lead regional adoption through ambitious airport expansion programs and smart city developments. Saudi Arabia’s Vision 2030 includes massive aviation infrastructure investments with new airports and terminal expansions requiring comprehensive security systems. South Africa operates advanced screening systems at OR Tambo and Cape Town international airports, serving as regional hubs for sub-Saharan Africa. Qatar’s Hamad International Airport features state-of-the-art scanning technology supporting its status as a major global transit hub. Oil-rich nations leverage sovereign wealth funds to finance cutting-edge technology deployments as part of economic diversification strategies. Regional security cooperation initiatives drive interoperability requirements and joint procurement opportunities.

COMPETITIVE LANDSCAPE

The full-body scanners market features intense competition among established technology giants and specialized security firms vying for government contracts and airport modernization projects. Market participants differentiate themselves through superior imaging resolution, robust privacy protection features,s and seamless integration capabilities with existing security infrastructure. High barriers to entry due to stringent regulatory requirements and complex procurement processes limit new competitors but encourage continuous innovation among existing players. Companies compete based on technical performance, reliability,y and ability to meet strict data protection standards mandated by governments worldwide. Pricing pressure exists but is mitigated by the critical nature of security infrastructure, where quality and compliance often outweigh cost considerations. Technological adoption varies across competitors,ors with leaders investing heavily in artificial intelligence and machine learning to improve verification speeds and reduce error rates. Service quality,lity including installation, support,upport maintenance, and software updates,s serves as a key differentiator in securing long-term contracts with public sector entities. Geographic reach determines the ability to serve multinational clients requiring consistent technology standards across different jurisdictions. Regulatory compliance capabilities also distinguish competitors as adherence to evolving international standards becomes increasingly complex. The concentration of market power among a few major players creates an oligopolistic structure where collaboration on industry standards coexists with fierce competition for individual high-value projects.

KEY MARKET PLAYERS

Some of the companies that are playing a dominant role in the Global Full Body Scanners Market include

- OSI Systems, Inc. (Rapiscan Systems)

- Smiths Detection Group Ltd.

- Leidos Holdings, Inc.

- Rohde & Schwarz GmbH & Co. KG

- Nuctech Company Limited

- Thales Group

- L3Harris Technologies, Inc.

- Tek84 Inc.

- Westminster Group plc

- Analogic Corporation

- Bruker Corporation

- Astrophysics Inc.

TOP LEADING PLAYERS IN THE MARKET

- Leidos Holdings Inc is a premier provider of advanced security screening solutions with a strong focus on millimeter wave technology for aviation and public transport sectors. The company manufactures the ProVision series of full-body scanners, which are widely deployed at major international airports globally. Leidos recently enhanced its product line by integrating artificial intelligence algorithms to improve threat detection accuracy and reduce false alarm rates significantly. This technological advancement allows security agencies to process passengers more efficiently while maintaining high security standards. The firm actively collaborates with government bodies to ensure compliance with evolving privacy regulations and safety standards. Leidos continues to invest in research and development to create next-generation scanners that offer faster processing times and improved user experience. Their global service network ensures reliable maintenance and support for security infrastructure at high-traffic transportation hubs worldwide.

- Smiths Detection Group Ltd stands as a global leader in threat detection and security screening technologies, offering a comprehensive portfolio of full-body scanners. The company provides both millimeter wave and backscatter X-ray solutions tailored for diverse applications, including airports, prisons, and government facilities. Smiths Detection recently launched its Hi Scan series featuring advanced imaging capabilities and automated target recognition software to streamline security operations. This innovation strengthens their market position by addressing key operational challenges such as operator fatigue and screening disruptions. The firm has secured multiple contracts for deploying smart security lanes in Europe athe nd Asia Pacific regions. Smiths Detection focuses on interoperability, ensuring its systems integrate seamlessly with existing airport infrastructure and central monitoring platforms. Their commitment to sustainability includes developing energy-efficient scanners that reduce operational costs for clients while minimizing environmental impact.

- Rohde and Schwarz GmbH and Co KG is a renowned technology group specializing in secure communications and cybersecurity with a significant presence in the security screening market. The company offers the QPS201 millimeter wave people scanner, which is designed forhigh-throughputt environments requiring strict privacy protection. Rohde and Schwarz recently expanded its manufacturing capacity to meet growing global demand for advanced security screening equipment. This expansion enables the company to deliver products faster and support large-scale deployment projects in emerging markets. The firm emphasizes data privacy by design, ensuring that all scanned images are processed locally and deleted immediately after analysis. Rohde and Schwarz partners with leading system integrators to provide end-to-end security solutions for infrastructure protection. Their robust engineering approach ensures high reliability and durability of scanners in challenging operational conditions.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the full-body scanners market employ several strategic approaches to maintain competitive advantages and drive growth. Product innovation remains a primary strategy as companies develop advanced millimeter-wave sensors and artificial intelligence algorithms to enhance detection accuracy and speed. Strategic partnerships with government agencies and airport authorities facilitate large-scale deployments and ensure compliance with regional regulatory requirements. Geographic expansion into emerging markets allows participants to capture growth opportunities in regions with expanding aviation infrastructure and rising passenger volumes. Mergers and acquisitions enable firms to consolidate technical expertise and broaden their product portfolios to offer comprehensive security solutions. Investment in cybersecurity measures protects sensitive biometric data and builds trust among public sector clients concerned about privacy and data breaches. Development of modular and scalable systems offers flexible solutions for smaller airports and border crossings with limited space and budgets. Focusing on interoperability ensures systems can integrate with diverse national databases and legacy infrastructure, reducing implementation complexity for clients.

MARKET SEGMENTATION

This research report on the global full-body scanners market is segmented and sub-segmented into the following categories.

By Technology

- Millimeter Wave Technology

- X-ray Technology

By Type

- Single View Scanners

- Dual View Scanners

- 3D View Scanners

By End Use

- Airports

- Critical Infrastructure

- Correctional Facilities

- Government Buildings

- Military & Defense

- Others

By Country

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. Where are they used most?

Main applications include airports, railway stations, metro systems, borders, government buildings, stadiums, and other high‑security venues

2. Which technology segment leads the market?

Millimeter‑wave scanners are a leading technology segment, valued for safety and image quality compared with older X‑ray‑based systems.

3. Which system type is important?

Image processing and modelling systems, along with 3D body scanners, form key system categories in the market.

4. Which region leads the market?

North America is a major market because of early adoption and large airport and border‑security programs.

5. Which region is growing fast?

Asia‑Pacific and other emerging regions are growing quickly as new airports, rail networks, and security projects expand.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com