Latin America E-Commerce Market Size, Share, Trends & Growth Forecast Report By Model Type, By Product, and By Country (Mexico, Brazil, Argentina, Chile & Rest of Latin America) – Industry Analysis and Forecast, 2026 to 2034

Latin America E-Commerce Market Report Summary

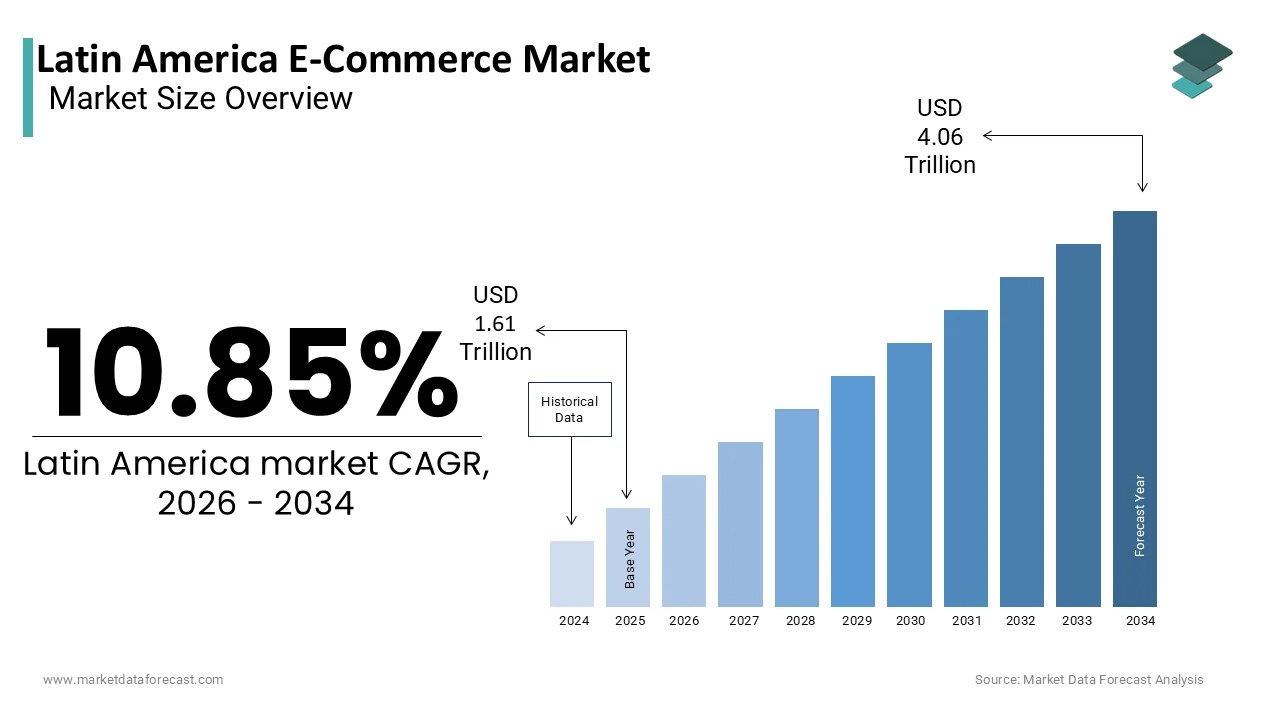

The Latin America E-Commerce Market was valued at USD 1.61 trillion in 2025 and is projected to reach USD 4.06 trillion by 2034, growing from USD 1.78 trillion in 2026 at a CAGR of 10.85% during the forecast period. Growth is driven by increasing smartphone penetration, expansion of digital payment infrastructure, rising internet accessibility, and growing adoption of mobile commerce across the region. Logistical infrastructure gaps in rural areas and regulatory fragmentation across countries are shaping market dynamics.

Key Market Trends

- Rising adoption of mobile commerce driven by increasing smartphone penetration and affordable mobile internet.

- Growing integration of digital payment platforms and fintech solutions to improve financial inclusion.

- Increasing adoption of artificial intelligence for personalized shopping experiences and customer engagement.

- Expansion of social commerce through Instagram, TikTok, WhatsApp, and influencer-led marketing.

- Rising investments in logistics infrastructure and fulfillment networks to improve delivery efficiency across the region.

Segmental Insights

- Based on model type, Business-to-Consumer (B2C) held the majority share in 2025, driven by increasing consumer preference for online shopping, cross-border marketplaces, and mobile-first retail platforms.

- Based on product, fashion and apparel held the largest share in 2025, supported by high purchase frequency, fast-fashion trends, and strong social media influence on buying behavior.

- Food and beverages is the fastest-growing product segment, driven by increasing online grocery adoption, expansion of rapid delivery services, and growing demand for health and wellness products.

Regional Insights

- Brazil led the market in 2025, supported by its mature digital payment ecosystem, widespread Pix adoption, and strong presence of leading e-commerce platforms.

- Mexico holds a significant share, driven by expanding logistics infrastructure, cross-border trade, and increasing online consumer spending.

- Argentina is a prominent market, supported by growing digital commerce adoption, installment-based payment systems, and resilient domestic e-commerce platforms.

- Chile contributes notably due to its high internet penetration, advanced retail ecosystem, and increasing digital payment adoption.

- Consumer-to-Consumer (C2C) is the fastest-growing model type segment, driven by increasing peer-to-peer commerce, expanding second-hand marketplaces, and widespread use of social commerce platforms.

Competitive Landscape

The market is highly competitive, with regional e-commerce leaders, global marketplace operators, and omnichannel retailers competing on pricing, logistics capabilities, digital payment integration, customer experience, and technology innovation. Companies are investing heavily in AI-driven personalization, fulfillment centers, fintech services, social commerce, and localized digital ecosystems to strengthen their market presence and improve customer retention across Latin America.Prominent players in the market include MercadoLibre, Amazon, B2W Digital, Magazine Luiza, Americanas.com, OLX, Falabella, Cencosud, Linio, and Netshoes.

Latin America E-Commerce Market Size

The Latin America E-Commerce Market was valued at USD 1.61 trillion in 2025 and is estimated to reach USD 1.78 trillion in 2026. The market is projected to grow to USD 4.06 trillion by 2034, registering a CAGR of 10.85% during the forecast period from 2026 to 2034.

The Latin America e-commerce market represents a dynamic and rapidly evolving digital landscape characterized by increasing internet penetration and a youthful demographic profile. This sector encompasses the buying and selling of goods and services through online platforms across countries such as Brazil, Mexico, Argentina, Colombia, and Chile. The region has witnessed a structural shift in consumer behavior, accelerated by global health crises that necessitated remote transactions and digital engagement. According to World Bank data, internet usage in Latin America reached 77.2% of the population in 2024, creating a vast addressable base for digital retailers. Mobile connectivity serves as the primary gateway, with smartphone adoption outpacing desktop access in many urban centers. The market is defined by its diversity, ranging from sophisticated financial ecosystems in Brazil to emerging digital infrastructures in Central America. Social commerce plays a pivotal role, with platforms like Instagram and WhatsApp facilitating direct transactions between sellers and buyers. According to the Economic Commission for Latin America and the Caribbean, the digital economy contributes significantly to regional GDP growth, driven by small and medium enterprises adopting online sales channels. Logistics networks are expanding beyond major metropolitan areas, although rural connectivity remains a work in progress. The integration of local payment methods and cross-border trade agreements further shapes the competitive environment. This market continues to mature as regulatory frameworks adapt to protect consumer rights and ensure data privacy, fostering a more secure environment for digital commerce expansion across the continent.

MARKET DRIVERS

Rising Smartphone Penetration and Mobile Internet Accessibility Driving Adoption

The proliferation of smartphones and affordable mobile data plans is a key factor propelling the e-commerce market growth in Latin America. Mobile devices have become the primary tool for internet access, bypassing the need for traditional broadband infrastructure in many regions. According to GSMA Intelligence, mobile connections in Latin America reached approximately 450 million in 2023, with 4G networks covering over 80% of the population in major economies like Brazil and Mexico. This widespread accessibility allows consumers in tier two and tier three cities to participate in the digital economy for the first time. The convenience of mobile shopping apps enables users to browse, compare prices, and make purchases anytime, removing geographical barriers to retail access. Social media platforms integrated with shopping features further amplify this trend, as users discover products through influencers and peer recommendations on their mobile feeds. The user interface of e-commerce applications has become increasingly intuitive, catering to first-time digital shoppers who may lack technical expertise. Payment gateways optimized for mobile devices simplify the checkout process, reducing cart abandonment rates. As per Statista, mobile commerce accounts for nearly 60% of all online transactions in the region, reflecting a strong preference for handheld devices over desktop computers. This mobile-first approach encourages retailers to prioritize app development and mobile-responsive designs. The continuous improvement in network speed and reliability supports richer media content, such as video product demonstrations, enhancing the overall shopping experience and driving higher conversion rates across diverse demographic segments.

Expansion of Digital Payment Infrastructure and Financial Inclusion Initiatives

The development of robust digital payment systems and increased financial inclusion is further boosting the Latin American e-commerce market expansion. Historically, a large portion of the population remained unbanked, relying on cash transactions, which hindered online shopping growth. However, the introduction of instant payment systems has revolutionized this landscape. In Brazil, the Pix system launched by the Central Bank has transformed digital transactions, processing billions of payments monthly since its inception. According to the Central Bank of Brazil, Pix adoption covers 80% of the adult population, enabling seamless real-time transfers without traditional banking fees. Similar initiatives in other countries, such as CoDi in Mexico and Plin in Peru, are reducing reliance on cash and credit cards. Fintech companies have expanded access to digital wallets and buy now, pay later services, allowing consumers with limited credit history to make purchases. These solutions address trust issues by offering secure and transparent transaction methods. As per the Global Findex Database 2025, financial inclusion rates in the region have improved,d as 70% of adults owned a financial account in 2024, marking significant progress due to digital banking innovations. Retailers benefit from reduced fraud risks and faster settlement times compared to traditional card processing. The integration of these payment options into e-commerce platforms lowers entry barriers for new customers, particularly among lower-income groups. This financial ecosystem evolution creates a more inclusive market where millions of previously excluded consumers can now participate confidently in online commerce, driving volume growth and market expansion.

MARKET RESTRAINTS

Logistical Infrastructure Deficiencies in Rural and Remote Areas

Inadequate logistical infrastructure in rural and remote regions serves as a significant restraint on the Latin American e-commerce market. While urban centers enjoy relatively efficient delivery networks, vast geographical areas suffer from poor road conditions, limited warehousing facilities, and unreliable postal services. According to the World Bank Logistics Performance Index, several Latin American countries rank below the global average in infrastructure quality, impacting last-mile delivery efficiency. High transportation costs result from these inefficiencies, making free or low-cost shipping difficult for retailers to offer outside major cities. Delivery times in remote areas can extend to weeks, discouraging consumers who expect rapid fulfillment similar to urban standards. Security concerns also plague logistics operations, with cargo theft remaining a persistent issue in certain corridors, leading to higher insurance premiums and operational risks. As per IMAP, logistics costs in Brazil reached 15.5% of GDP in 2025, higher than in many developed economies. This burden is passed on to consumers through higher product prices or shipping fees, reducing the competitiveness of online offers against local brick-and-mortar stores. Small and medium-sized sellers struggle to manage complex distribution networks, limiting their market reach. The lack of standardized addressing systems in informal settlements further complicates delivery accuracy. Until substantial investments are made in road networks, regional distribution hubs, and technology-driven logistics solutions, the e-commerce market will remain concentrated in urban pockets, excluding a significant portion of the potential customer base in rural communities.

Regulatory Fragmentation and Cross-Border Trade Complexities

Regulatory fragmentation across Latin American countries creates substantial barriers for e-commerce operators seeking regional expansion. Each nation maintains distinct tax laws, customs regulations, and consumer protection standards, complicating cross-border trade operations. Import duties and value-added taxes vary significantly, creating uncertainty for both sellers and buyers regarding final costs. According to the OECD, non-tariff barriers and bureaucratic delays increase the cost of cross-border transactions by up to 20% in some cases. Customs clearance processes are often slow and opaque, leading to prolonged delivery times and frustrated customers. Data privacy regulations also differ, with some countries implementing strict laws similar to the European General Data Protection Regulation while others lag, creating compliance challenges for multinational platforms. Local content requirements and restrictions on foreign ownership in certain sectors further limit market entry strategies. As per the Inter American Association of Intellectual Property, inconsistencies in intellectual property enforcement expose brands to counterfeiting risks when operating across borders. These regulatory hurdles discourage small and medium enterprises from engaging in international e-commerce, limiting product variety for consumers. Harmonizing these regulations through regional trade agreements remains a slow process, hindering the creation of a unified digital market. Companies must invest heavily in legal and compliance teams to navigate this complex landscape, increasing operational overheads. Until greater regulatory alignment is achieved, the full potential of regional e-commerce integration will remain constrained by administrative and legal friction.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Personalized Shopping Experiences

The adoption of artificial intelligence and machine learning technologies presents a major opportunity for the Latin American e-commerce market growth. AI-driven algorithms enable retailers to analyze vast amounts of consumer data to provide personalized product recommendations, targeted marketing, and dynamic pricing strategies. According to McKinsey and Company, personalization can deliver five to eight times the return on investment for marketers and lift sales by 10% or more. In Latin America, where brand loyalty is often influenced by relevance and convenience, tailored shopping experiences foster deeper customer relationships. Chatbots powered by natural language processing handle customer inquiries in local dialects and slang, improving service accessibility and response times. These tools operate twenty-four seven, addressing the needs of consumers in different time zones without additional labor costs. Inventory management systems utilizing predictive analytics help retailers optimize stock levels, reducing overstock and stockouts. As per IBM, businesses using AI for supply chain management report a 20% reduction in inventory costs. Visual search technologies allow users to upload images to find similar products, enhancing discovery for fashion and home decor items. Voice commerce is also emerging as Spanish and Portuguese language recognition improves. By leveraging these technologies, e-commerce platforms can differentiate themselves in a crowded market, offering superior convenience and relevance that drive repeat purchases and increase average order values across the region.

Growth of Social Commerce and Influencer-Led Marketing Channels

Social commerce represents a burgeoning opportunity for the Latin American e-commerce market, leveraging the high engagement levels on social media platforms to drive direct sales. Platforms such as Instagram, TikTok, and Facebook have integrated shopping features that allow users to purchase products without leaving the app, streamlining the buyer journey. According to Latam Intersect PR, over 23% of Latin American online consumers use Instagram for product research and discovery. Influencers play a crucial role in this ecosystem, building trust and credibility with their followers through authentic content and recommendations. Live streaming shopping events have gained popularity, enabling real-time interaction between sellers and buyers, which mimics the traditional market experience in a digital format. This format is particularly effective in cultures that value personal connection and social validation in purchasing decisions. As per eMarketer, social commerce sales in Latin America are projected to grow at a double-digit annual rate, outpacing traditional e-commerce growth. Small businesses and artisans benefit significantly from this model, as it lowers entry barriers by eliminating the need for standalone websites. User-generated content such as reviews and unboxing videos further amplifies brand visibility organically. Retailers who effectively integrate social commerce strategies can tap into viral trends and community-driven demand. This channel offers a cost-effective alternative to traditional advertising, providing measurable returns through direct conversion tracking. Embracing social commerce allows brands to meet consumers where they already spend significant time, creating seamless and engaging shopping opportunities.

MARKET CHALLENGES

Cybersecurity Threats and Data Privacy Concerns

Cybersecurity threats pose a critical challenge to the Latin American e-commerce market, eroding consumer trust and increasing operational risks for businesses. The region has seen a surge in cyberattacks, including phishing, ransomware, and data breaches targeting online retailers and payment processors. According to Kaspersky, Latin America experienced a 30% increase in cyberattacks on e-commerce platforms in the past year, highlighting the vulnerability of digital infrastructure. Consumers are increasingly aware of these risks, leading to hesitation in sharing personal and financial information online. High-profile data breaches damage brand reputation and result in significant financial losses due to regulatory fines and compensation claims. The lack of uniform cybersecurity standards across countries complicates defense strategies for multinational operators. Small and medium-sized enterprises often lack the resources to implement robust security measures, making them easy targets for attackers. As per the Inter American Development Bank, only 40% of small businesses in the region have basic cybersecurity protocols in place. Fraudulent activities such as identity theft and credit card fraud further exacerbate the problem, leading to higher transaction rejection rates and increased costs for verification processes. Building a secure digital environment requires continuous investment in encryption, multi-factor authentication, and employee training. Without addressing these security gaps, the market risks stagnation as consumers revert to cash-based transactions or trusted local vendors, limiting the growth potential of online commerce.

Talent Shortage in Digital Skills and Technical Expertise

A significant shortage of professionals with advanced digital skills and technical expertise hampers the growth and innovation capacity of the Latin American e-commerce market. The rapid digitization of the economy has outpaced the development of educational programs and training initiatives needed to supply qualified talent. According to the World Economic Forum, there is a growing skills gap in areas such as data science, software engineering, and digital marketing across the region. Companies struggle to find employees capable of managing complex e-commerce platforms, analyzing big data, and implementing cybersecurity measures. This scarcity drives up salary costs, straining the budgets of startups and small businesses that are key drivers of innovation. Brain drain further exacerbates the issue, as skilled professionals migrate to North America or Europe in search of better opportunities and higher wages. As per LinkedIn data, demand for digital tech roles in Latin America has grown by 25% annually, while the supply of qualified candidates has increased by only 10%. This imbalance limits the ability of firms to adopt advanced technologies and optimize operations efficiently. Educational institutions are slowly adapting curricula, but the pace of change remains insufficient to meet immediate industry needs. Corporate training programs are becoming essential, yet they require significant investment. Without a robust pipeline of digital talent, the market faces constraints in scaling operations, improving customer experiences, and maintaining competitiveness in the global digital economy, ultimately slowing down overall sector advancement.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Model Type, Product, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | Mexico, Brazil, Argentina, Chile, Rest of Latin America |

| Market Leaders Profiled | MercadoLibre, Amazon, B2W Digital, Magazine Luiza, Americanas.com, OLX, Falabella, Cencosud, Linio, Netshoes. |

SEGMENTAL ANALYSIS

By Model Type Insights

The Business-to-Consumer model segment captured the largest share of the Latin American market in 2025 and is expected to maintain its dominance in the Latin American e-commerce market over the forecast period as it continues to capitalize on the increasing digital engagement of regional consumers. This segment captures the majority of transaction volume as consumers increasingly prefer online channels for daily purchases ranging from electronics to groceries. According to industry projections, the B2C e-commerce revenue in Latin America is expected to reach 173.2 billion US dollars by 2025, reflecting deep consumer integration into digital retail. A primary driver is the expansion of cross-border marketplaces that offer international product variety at competitive prices, attracting price-sensitive buyers who previously lacked access to global brands. The second major factor is the proliferation of mobile-first retail platforms optimized for smartphone users, which aligns with regional connectivity trends where mobile devices serve as the primary internet gateway. As per GSMA Intelligence, over 70% of online retail traffic in the region originates from mobile devices, compelling retailers to prioritize app-based shopping experiences that streamline discovery and checkout. These platforms leverage data analytics to personalize recommendations, enhancing conversion rates and customer retention. The dominance of B2C is further reinforced by improved last-mile delivery networks in urban centers, reducing fulfillment times and building consumer trust in online transactions. This combination of accessibility, variety, and convenience solidifies B2C as the cornerstone of regional digital commerce.

The Consumer to Consumer segment is poised for significant expansion and is estimated to record a promising CAGR in the Latin American market during the forecast period as more individuals utilize digital platforms for peer-to-peer trading. This accelerated growth stems from economic pressures that drive consumers toward secondhand goods and peer-to-peer exchanges as cost-saving measures. Inflation and currency volatility in countries like Argentina and Brazil have made preowned items attractive alternatives to new products, fueling platform activity. According to the Economic Commission for Latin America and the Caribbean, the secondhand market in the region grew by 25% year on year in 2023 as households sought to maintain consumption levels amid financial constraints. Another critical driver is the rise of social commerce platforms that facilitate informal C2C transactions through messaging apps and social media feeds. As per Meta, over 60% of Latin American social media users have engaged in buying or selling goods through platforms like Facebook Marketplace or WhatsApp groups, bypassing traditional listing fees and formal registration barriers. These decentralized channels lower entry thresholds for individual sellers while providing buyers with localized, negotiable options. The convergence of economic necessity and accessible digital tools creates a fertile environment for C2C expansion, outpacing traditional retail models in growth velocity.

By Product Insights

The fashion and apparel segment led the market by accounting for the largest share of the Latin American market in 2025. The growth of the fashion and apparel segment in the regional market can be credited to high purchase frequency and strong cultural emphasis on personal appearance. This category benefits from seasonal turnover, trend cycles, and the universal need for clothing across demographics. According to data from 2025, fashion accounted for approximately 28.9% of online retail revenue in Latin America, surpassing other verticals in transaction volume. A key driver is the dominance of fast fashion retailers offering affordable, trend-responsive collections tailored to local tastes and body types. Brands like Shein and Zara have invested heavily in regional logistics hubs, enabling faster delivery and easier returns that mitigate sizing uncertainties inherent in online apparel shopping. The second driving factor is the integration of social influence into purchasing decisions, where influencers and user-generated content shape trends and validate style choices. As per a survey by Kantar, 65% of Latin American Gen Z consumers report discovering new fashion brands through TikTok or Instagram, creating direct pathways from inspiration to purchase. Visual platforms allow detailed product showcasing through videos and try-on hauls, reducing perceived risk. Additionally, flexible payment options such as installments make higher-value fashion items accessible to broader income segments. This synergy of affordability, social validation, and financial flexibility ensures fashion remains the top-performing product category in regional e-commerce.

On the other side, the food and beverages segment is anticipated to witness robust performance in the next few years as consumers continue to integrate online grocery shopping into their regular routines. This surge is driven by the normalization of online grocery shopping post-pandemic, transforming what was once a niche service into a mainstream habit for urban households. Consumers now expect the same convenience for perishables as they do for durable goods, prompting retailers to invest in cold chain infrastructure and rapid delivery fleets. According to NielsenIQ, online grocery penetration in major Latin American cities reached 15% in 2023, up from just 3% in 2019, indicating a sustained behavioral shift beyond emergency lockdowns. Another pivotal driver is the emergence of specialized health and wellness food platforms catering to dietary preferences such as vegan, gluten-free, and organic products that are often unavailable in traditional brick-and-mortar stores. As per the Pan American Health Organization, 40% of urban consumers in the region actively seek functional foods for preventive health, creating demand for curated online assortments. Subscription models for staples and meal kits further lock in recurring revenue while reducing decision fatigue for busy professionals. The combination of habitual adoption and niche product accessibility propels this segment’s exceptional growth trajectory, redefining food retail dynamics across the continent.

COUNTRY LEVEL ANALYSIS

Brazil E-Commerce Market Analysis

Brazil led the market by capturing the highest share of the Latin American market in 2025 and is expected to maintain its status as the regional leader in e-commerce, with continued innovation and market expansion projected for the next few years. The country serves as the primary testing ground for innovative business models and attracts significant foreign investment in logistics and fintech. According to ABComm, Brazilian e-commerce revenue reached 180 billion reais in 2023, supported by the world-leading instant payment system Pix, which processed over 3 billion transactions monthly. A major driving factor is the high level of banking digitization that enables seamless online payments even among lower-income populations who previously relied on cash. The Central Bank of Brazil reports that Pix adoption covers 80% of the adult population, removing friction from checkout processes and boosting conversion rates significantly. Another critical factor is the maturity of domestic marketplace giants like Mercado Libre and Magazine Luiza that have built integrated ecosystems combining retail, payments, credit, and logistics. These platforms offer end-to-end solutions that small merchants can leverage without heavy capital expenditure, fostering a vibrant seller base. Government initiatives to reduce import taxes on e-commerce parcels under 50 dollars have also stimulated cross-border trade. Despite logistical challenges in remote areas, Brazil’s scale and innovation capacity ensure its continued leadership in shaping regional e-commerce trends and standards.

Mexico E-Commerce Market Analysis

Mexico held the second-largest share of the Latin America e-commerce market in 2025 due to its strategic proximity to North America and robust manufacturing base that supports both domestic and cross-border commerce. The country benefits from integrated supply chains established under trade agreements, facilitating efficient movement of goods. According to the Mexican Online Sales Association, e-commerce sales in Mexico grew by 16% in 2024 to reach 790 billion pesos, driven by rising middle-class consumption. A primary driver is the expansion of cash-on-delivery and convenience store payment networks that accommodate the unbanked population while maintaining digital transaction records. As per Condusef, over 35 million Mexicans use OXXO stores to pay for online purchases, bridging the gap between digital intent and physical payment capability. Another significant factor is the influx of international players establishing local fulfillment centers to serve both Mexican consumers and US-based Latino markets. Amazon and Walmart have invested billions in Mexican warehousing infrastructure, reducing delivery times to same-day standards in major metropolitan areas. The government’s digital tax reforms have also formalized many informal sellers, increasing taxable transaction volumes. Mexico’s unique position as a nearshoring hub combined with adaptive payment solutions creates a resilient e-commerce ecosystem poised for sustained expansion.

Argentina E-Commerce Market Analysis

Argentina is poised to navigate its complex economic landscape with continued digital innovation, with e-commerce likely to serve as a vital consumer tool over the next few years. E-commerce here functions as a hedge against depreciation, with consumers accelerating purchases to lock in prices before further devaluation. According to CACE, Argentine e-commerce transactions increased by 30% in nominal terms during 2023, though real growth adjusted for inflation was more modest at 8%. A key driver is the widespread use of installment payment plans that allow consumers to preserve purchasing power in an inflationary environment. As per the Argentine Central Bank, over 70% of online purchases are made in multiple interest-free installments, making expensive items attainable despite eroded wages. Another critical factor is the resilience of domestic platforms that adapt quickly to regulatory changes and currency fluctuations, offering dynamic pricing and alternative payment methods like cryptocurrency or barter systems. Local players have developed sophisticated hedging mechanisms to manage inventory costs amid exchange rate volatility. While cross-border trade faces restrictions, domestic e-commerce thrives on necessity-driven consumption patterns. Argentina’s market demonstrates how digital commerce can persist and even grow under adverse economic conditions through financial innovation and adaptive consumer behavior.

COMPETITIVE LANDSCAPE

Competition in the Latin American e-commerce market is intense and characterized by a mix of regional giants and global entrants vying for consumer attention and loyalty. Mercado Libre holds a strong position due to its early entry and comprehensive ecosystem,m but faces increasing pressure from Amazon, which leverages its global scale and logistical expertise. Local players in specific countries like Falabella in Chile and Magazine Luiza in Brazil compete fiercely by offering specialized services and deep community integration. Price wars are common as retailers attempt to attract price-sensitive consumers through discounts and promotional events. Differentiation occurs through superior customer service, faster delivery times,s and exclusive product offerings. Fintech integration has become a critical battleground with companies developing proprietary payment solutions to capture transaction data and enhance user stickiness. Regulatory compliance varies across borders, requiring agile adaptation to local laws regarding taxation and data privacy. The rise of social commerce introduces new competitors from informal sectors who leverage social media platforms for direct sales. Innovation in logistics,s including drone deliveries and pickup points, ts helps overcome infrastructure deficits. Overall, the market remains dynamic with constant evolution driven by technological advancements and shifting consumer expectations.

KEY MARKET PLAYERS

Key players operating in the Latin American e-commerce market include

- MercadoLibre

- Amazon

- B2W Digital

- Magazine Luiza

- Americanas.com

- OLX

- Falabella

- Cencosud

- Linio

- Netshoes

TOP LEADING PLAYERS IN THE MARKET

- Mercado Libre operates as the dominant digital commerce ecosystem in Latin America, providing integrated solutions for online retail, payments, and logistics. The company facilitates millions of transactions daily through its marketplace platform while supporting small businesses with credit and fulfillment services. Recent actions include expanding its logistics network by opening new distribution centers in Colombia and Chile to reduce delivery times significantly. The firm has also enhanced its fintech arm, Mercado Pago, by integrating cryptocurrency trading features and instant payment options like Pix in Brazil. These initiatives strengthen user retention and increase transaction frequency across the region. By investing heavily in technology infrastructure and customer service automation, Mercado Libre continues to set industry standards for speed and reliability. Its comprehensive approach connects buyers and sellers seamlessly, fostering trust and driving sustained growth in diverse local markets throughout Latin America.

- Amazon maintains a strong presence in Latin America by leveraging its global supply chain expertise and technological prowess to serve key markets like Brazil and Mexico. The company focuses on offering a vast product selection and rapid delivery through its Prime membership program,m which attracts loyal subscribers. Recent actions involve launching dedicated local websites in additional countries and establishing fulfillment centers in strategic urban hubs to optimize last-mile logistics. Amazon has also introduced localized payment methods and cash on delivery options to cater to unbanked populations. Investments in cloud computing services through AWS support local enterprises in digitizing their operations. By prioritizing customer experience and operational efficiency, Amazon strengthens its competitive position against regional rivals. Its continuous expansion of product categories and enhancement of mobile app functionalities ensure it remains a preferred destination for online shoppers seeking convenience and variety across the continent.

- Alibaba Group influences the Latin America e-commerce landscape primarily through its cross-border platforms AliExpress and Alibaba.com, which connect regional buyers with global suppliers. The company enables access to affordable goods from Asia while supporting local exporters in reaching international markets. Recent actions include partnering with local logistics providers in Brazil and Mexico to streamline customs clearance and improve delivery speeds. Alibaba has also invested in digital payment collaborations to facilitate smoother transactions for consumers unfamiliar with international banking systems. The introduction of localized language support and customer service teams enhances user experience and trust. By focusing oncross-borderr trade facilitation and supplier empowerment, Alibaba strengthens its role as a critical bridge between Latin American consumers and global manufacturing hubs. Its strategic partnerships and technology investments continue to expand its footprint and influence in the rapidly growing regional digital economy.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Latin American e-commerce market employ vertical integration to control supply chains and reduce dependency onthird-partyy logistics providers. They invest heavily in proprietary fulfillment networks to ensure faster delivery times and better quality control. Localization strategies are crucial as companies adapt interfaces, payment methods,s and marketing campaigns to suit cultural nuances and linguistic preferences in each country. Partnerships with local fintech firms enable seamless financial transactions for unbanked populations through digital wallets and buy now, ow pay later services. Data analytics drive personalized shopping experiences that increase conversion rates and customer loyalty. Mobile-firstt development ensures accessibility for users who rely primarily on smartphones for internet access. Cross-border expansion allows retailers to tap into neighboring markets with similar consumer behaviors. Sustainability initiatives such as eco-friendly packaging and carbon-neutral delivery options appeal to environmentally conscious shoppers. Continuous innovation in artificial intelligence enhances customer service through chatbots and recommendation engines. These strategies collectively help participants navigate regulatory complexities and logistical challenges while capturing growing digital demand.

RECENT MARKET DEVELOPMENTS

- In January 2025, Mercado Libre announced a major expansion of its logistics network in Brazil, launching new fulfillment centers aimed at reducing delivery times and improving customer experience across densely populated urban areas.

- In August 2025, Amazon introduced a localized version of its Prime subscription in Mexico, offering exclusive benefits tailored to regional shopping habits and reinforcing its long-term commitment to the Latin American market.

- In March 2025, Falabella launched an integrated digital wallet across its e-commerce platforms in Colombia and Peru, enhancing payment flexibility and encouraging higher transaction volumes among users.

- In November 2025, Mercado Pago partnered with a leading Brazilian bank to offer no-interest installment plans, making online purchases more accessible to a broader demographic and boosting conversion rates.

- In May 2025, Amazon expanded its cross-border seller program to include more small businesses in Brazil, enabling them to reach global customers and strengthening the company’s role as a facilitator of international trade.

MARKET SEGMENTATION

This research report on the LatinAmericana e-commerce market is segmented and sub-segmented into the following categories.

By Model Type

- B2C

- B2B

- C2C

By Product

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY, and Media

- Other Product Categories

By Country

- Mexico

- Brazil

- Argentina

- Chile

- Rest of Latin America

Frequently Asked Questions

What are the major factors driving the growth of e-commerce in Latin America?

The growth of e-commerce in Latin America is driven by increasing internet and smartphone penetration, rising digital payment adoption, a growing middle-class population, improved consumer trust in online shopping, and enhancements in logistics and last-mile delivery systems.

What challenges does the e-commerce sector face in Latin America?

Some of the major challenges in the Latin American e-commerce market include infrastructure limitations in rural areas, cybersecurity threats, delivery and logistics inefficiencies, complex regulatory environments, and limited access to digital payment solutions for some consumers.

What is the future outlook for the Latin America e-commerce market?

The future of the Latin American e-commerce market looks promising, with strong projected growth supported by greater digital inclusion, fintech innovations, and the expansion of delivery infrastructure in less developed areas.

Which emerging technologies are impacting e-commerce in Latin America?

Emerging technologies such as artificial intelligence (AI), chatbots, big data analytics, augmented reality (AR), and blockchain are transforming the e-commerce landscape in Latin America by improving personalization, security, and the overall shopping experience.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com