- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

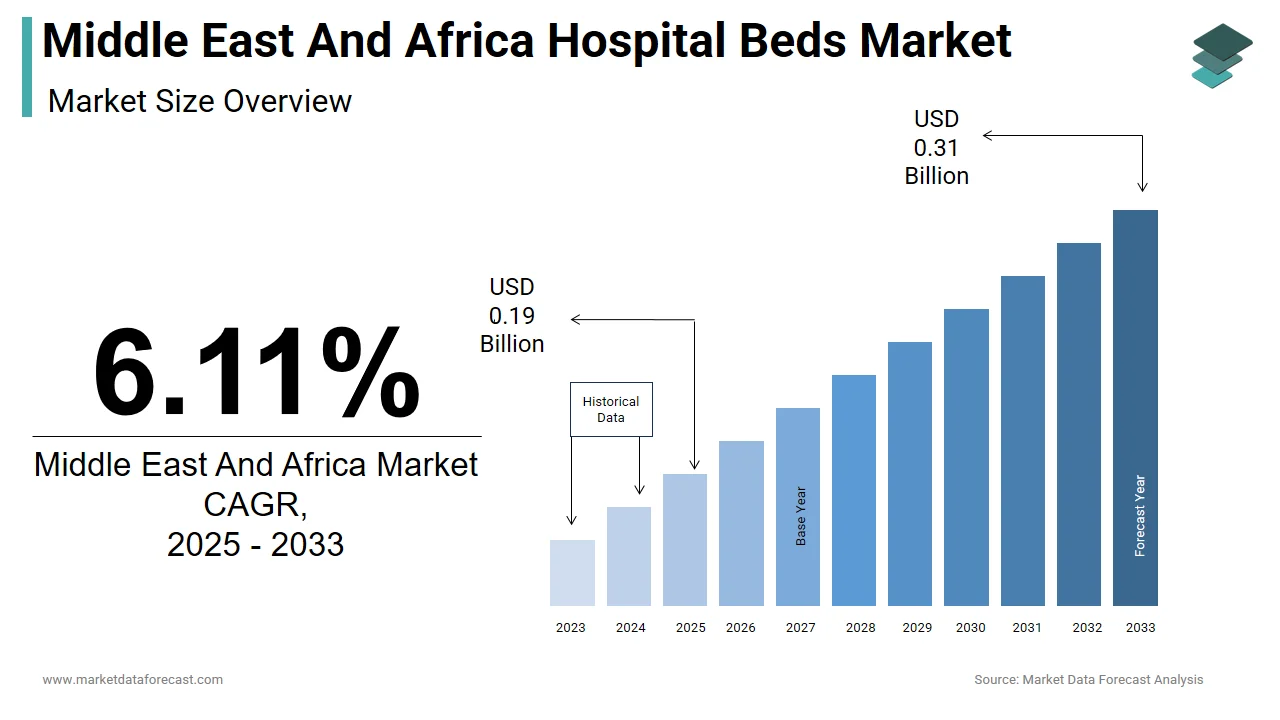

Middle East and Africa Hospital Beds Market Size

The size of the Middle East and Africa hospital beds market was worth USD 0.18 billion in 2024. The market is anticipated to grow at a CAGR of 6.11% from 2025 to 2033 and be worth USD 0.31 billion by 2033 from USD 0.19 billion in 2025.

MARKET DRIVERS

Rising Chronic Diseases and Hospital Growth Boosting Market Expansion

The growth of the hospital beds market in the Middle East and Africa is attributed to key factors such as the growing number of chronic diseases, the growing number of hospitals and clinics, and the growing number of public-private partnerships in the healthcare sector. The growth of the hospital supplies market in the Middle East and Africa is mainly driven by the growing number of hospitals, the aging population, and the increasing emergence of community-based illnesses. The GCC countries have robust global demand for medical devices and, due to this increasing demand, the healthcare sector is on the rise. Due to the growth of the healthcare sector, the market for hospital supplies in GCC countries is also growing.

The Middle East and Africa region rely heavily on imported hospital supplies for most medical products, including beds. Other factors driving the market are rising healthcare spending, increasing cases of community-based illnesses, and growing awareness of hospital infections (HAIs).

The price of beds and a reduction in the average length of stay for patients are likely to constrain market growth. The Middle East and Africa region are heavily dependent on imported hospital supplies for most products. Saudi Arabia is estimated to have a total imported value of hospital supplies of around US $ 125 million in 2015, which increased to around the US $ 315 million in 2019. Many imported products have a high cost which is an obstacle to the growing market in this region. Other factors hamper the growth of the MEA hospital beds market, including the emergence of home care services and strict regulatory bodies.

SEGMENTAL ANALYSIS

By Usage Insights

REGIONAL ANALYSIS

Geographically, the Middle East is forecasted to account for the largest share in the Middle East and Africa region. At the same time, Africa predicts to have a lower share during the forecast period. The total public and private health expenditure of the Gulf Cooperation Council (GCC) countries amounted to the US $ 66.9 billion in 2020. The rest of the GCC countries are expected to experience healthy growth rates during the forecast period.

The Saudi Arabian hospital beds market is estimated to register healthy CAGR from 2024 to 2029. The government of Saudi Arabia has a transformation plan to develop and improve health services. As part of this plan, the government announced initiatives among which the participation of the private sector is vital. Extended Care is one of 9 initiatives in the Private Sector Engagement Program and represents an excellent growth opportunity for Saudi Arabia.

KEY MARKET PLAYERS

Invacare Corporation, Paramount Bed Holdings Co. Ltd., Gendron Inc., Medline Industries Inc., LINET spol. S r.o., Savaria Corporation, Savion Industries, Hill-Rom Holdings Inc., Stryker Corporation, and Getinge Group are prominent companies in the MEA hospital beds market.

MARKET SEGMENTATION

This Middle East and Africa hospital beds market research report is segmented and sub-segmented into the following categories.

By Usage

- Acute care beds

- Long-term care beds

- Psychiatric care beds

- Others (maternity, etc.)

By Power

- Electric Bed

- Semi-Electric Bed

- Manual Bed

By End-User

- Hospitals

- Clinics

- Ambulatory services

- Others

By Country

- KSA

- UAE

- Israel

- Rest of the GCC countries

- South Africa

- Ethiopia

- Kenya

- Egypt

- Sudan

- rest of MEA