North America Cider Market Research Report – Segmented Based on Type, Distribution Channels and Country (The U.S., Canada and Rest of North America) - Analysis on Size, Share, Trends, and Growth Forecasts (2026 to 2034)

North America Cider Market Size

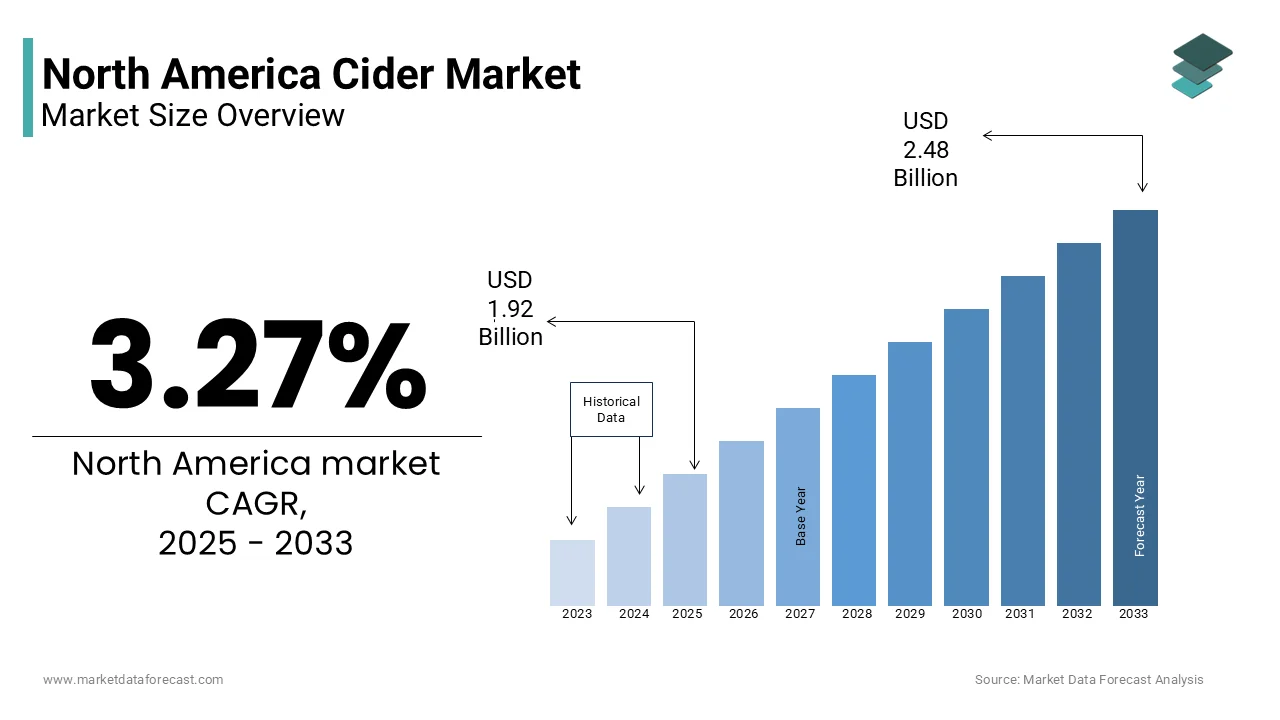

The cider market size in North America was valued at USD 1.92 billion in 2025 and is expected to reach USD 2.56 billion by 2034 from USD 1.98 billion in 2026, growing at a CAGR of 3.27% from 2026 to 2034.

Cider refers to the fermented beverages made primarily from apples, encompassing a spectrum of styles including traditional dry ciders, fruit-infused variants, hopped ciders, and hard ciders with added spirits or botanicals. Unlike beer or wine, cider occupies a distinct niche rooted in agricultural heritage, regional craftsmanship, and evolving consumer interest in low-hop, gluten-free alcoholic alternatives.

MARKET DRIVERS

Growing consumer preference for craft and regionally authentic alcoholic beverages is a pivotal driver shaping demand in the North America cider market. According to the Brewers Association, a large portion of adult craft alcohol consumers prioritize products made with locally sourced ingredients, a trend that aligns seamlessly with cider’s orchard-centric production model. Unlike mass-produced beers, many ciders are crafted in small batches using heirloom apple varieties such as Kingston Black, Dabinett, or Yarlington Mill, which are cultivated in specific microclimates across New England, the Pacific Northwest, and Ontario. The American Cider Association notes that many commercial cideries in the U.S. operate on-site orchards or source apples, reinforcing regional authenticity. This farm-to-bottle narrative resonates with millennial and Gen Z consumers.

MARKET RESTRAINTS

Expanding appeal among health-conscious and gluten-sensitive consumers is significantly boosting cider’s market penetration. According to the Celiac Disease Foundation, an estimated 3 million Americans have celiac disease, while another 18 million suffer from non-celiac gluten sensitivity, creating a substantial demand for gluten-free alcoholic alternatives. Cider, inherently gluten-free due to its fruit-based fermentation, has emerged as a preferred substitute for beer in social and dining settings. Like, some gluten-sensitive individuals selected hard cider as their top alcoholic beverage choice when dining out. Besides, the growing emphasis on clean labels has favored cider, as many producers avoid artificial additives and use only apple juice, yeast, and natural flavorings. The Alcohol and Tobacco Tax and Trade Bureau (TTB) recorded an increase in cider brands declaring “gluten-free” on labels in recent years, reflecting both regulatory clarity and consumer demand for dietary transparency.

Limited consumer awareness and persistent misperceptions about cider’s flavor profile remain significant restraints on broader market adoption. Like, a significant portion of adults in the U.S. associate cider primarily with overly sweet, soda-like beverages, often confusing it with apple juice or flavored malt drinks. This misconception limits trial among beer and wine enthusiasts seeking dry, complex, or tannic profiles. The Wine Market Council reports that only a portion of regular wine drinkers have ever purchased a dry cider, despite sensory similarities to white wine. Additionally, the absence of standardized flavor descriptors, unlike the well-established lexicons for wine or craft beer, hinders effective communication on shelves and menus. This knowledge gap is particularly pronounced among older demographics and in regions with limited craft beverage culture.

Stringent regulatory classification and taxation disparities pose structural challenges to cider producers. In the U.S., the Alcohol and Tobacco Tax and Trade Bureau (TTB) classifies cider based on apple content and fermentation method, but inconsistencies in labelling, such as whether a product is labeled as “hard cider” or “fruit wine”, affect tax rates and distribution eligibility. As of 2023, ciders with less than 7% ABV are taxed at $1.07 per gallon, while those above are taxed at wine rates, creating a disincentive for higher-alcohol traditional styles. The American Cider Association showcases that some of craft cideries avoid high ABV solely to remain in the lower tax bracket, constraining product innovation. Additionally, state-level regulations vary widely.

MARKET OPPORTUNITIES

Innovation in premium, low-sugar, and heritage-style ciders presents a significant growth opportunity. According to the American Cider Association, sales of dry and semi-dry ciders grew in recent years, signaling a shift toward wine-inspired palates. Producers such as Farnum Hill Ciders and Eve’s Cidery have gained acclaim for tannic, barrel-aged expressions that rival fine wine, attracting sommeliers and upscale restaurants. The James Beard Foundation notes that a notable portion of independent wine lists in major U.S. cities now feature artisanal ciders, often paired with charcuterie or seafood. Additionally, the rise of “skin-contact” and wild-fermented ciders, techniques borrowed from natural wine, has captivated adventurous drinkers.

Expansion into non-traditional retail and foodservice channels is unlocking new avenues for cider distribution. According to the National Restaurant Association, some of full-service restaurants added craft cider to their beverage menus, particularly in farm-to-table and New American cuisine establishments. Cider’s acidity and fruit-forward profile make it a versatile pairing for dishes ranging from pork belly to blue cheese, enhancing its culinary relevance. Additionally, the growth of beverage subscription boxes, such as Vinebox and Bespoke Post, has introduced curated cider selections to consumers unfamiliar with the category. In the USA, online alcohol sales grew, with cider experiencing a year-on-year increase in e-commerce penetration. Direct-to-consumer shipping is now legal in several states, enabling small cideries to bypass traditional distributors and build national followings through storytelling, virtual tastings, and limited releases.

MARKET CHALLENGES

Climate variability and apple crop yield instability present persistent challenges to consistent production. The Cornell University School of Integrative Plant Science notes that climate change has shortened chilling periods essential for apple tree dormancy, threatening long-term orchard viability. Smaller cideries, lacking long-term supply contracts, are particularly vulnerable to price spikes and ingredient shortages.

Intense competition from alternative fermented beverages and flavored malt drinks undermines cider’s market share growth. Brands like White Claw and Truly have leveraged aggressive marketing, broad distribution, and lower price points to dominate shelf space traditionally allocated to cider. RTD products now occupy a notable share of cooler space in convenience stores, often displacing craft ciders. Additionally, wine-based spritzers and kombucha hard drinks are gaining traction among health-focused consumers, further fragmenting the low-alcohol segment. This competitive pressure forces cider producers to invest heavily in branding and education to differentiate their products, despite often operating with limited marketing budgets compared to multinational beverage conglomerates.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.27% |

| Segments Covered | By Type, Distributional Channels, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United States, Canada & Mexico |

|

Market Leaders Profiled | Aston Manor Brewery, C&C Group Plc, Carlberg A/S, Distell Group, Halewood International Holdings Plc, Heineken UK Ltd., SABMiller Plc, Carlton & United Breweries Limited, The Boston Beer Company Inc |

SEGMENTAL ANALYSIS

By Type Insights

The Sparkling Cider segment dominated the North America cider market by capturing a 57.5% of total value in 2025. Characterized by effervescence achieved through natural fermentation or forced carbonation, sparkling cider aligns closely with consumer expectations for a refreshing, celebratory, or social drinking experience, distinguishing it from still or wine-style variants. The strong consumer association between carbonation and refreshment in social and casual drinking contexts is a primary driver of its dominance. The American Cider Association notes that trend of commercial cider releases were carbonated, reflecting producer confidence in market preference. Additionally, the sensory profile of sparkling cider, bright acidity, lively mouthfeel, and aromatic lift, makes it ideal for pairing with a wide range of cuisines, from barbecue to seafood, enhancing its versatility in both retail and foodservice environments. A further critical factor is the dominance of sparkling cider in mass-market and national brand portfolios. Major players produce sparkling variants as their flagship offerings, leveraging large-scale distribution and marketing. The format also lends itself well to canning and portable packaging, making it a staple at festivals, outdoor events, and casual gatherings.

The Still Cider segment is the fastest-growing and is projected to expand at a CAGR of 9.6% from 2026 to 2034. Still cider, which lacks carbonation, is gaining traction among consumers seeking wine-like alternatives with greater complexity and lower perceived sweetness. The rising interest in artisanal, dry, and terroir-driven cider expressions is a key driver. Producers in regions like Vermont, Ontario, and Washington State are crafting still ciders using traditional methods such as barrel aging and wild fermentation, appealing to connoisseurs and sommeliers. A different critical factor is the expansion of still cider into upscale dining and specialty retail. Its still nature allows for nuanced flavor development and pairing with delicate dishes such as roasted poultry and soft cheeses. Additionally, the absence of carbonation reduces gastric discomfort for some consumers, making it preferable in formal or prolonged dining settings.

By Distribution Channel Insights

The Supermarkets segment holds the largest share of the distribution channel at 47.3% of total cider sales in 2025. These mid-to-large format grocery retailers, including Kroger, Safeway, and Publix, offer broad consumer access, consistent shelf presence, and integration within the beer and wine sections, making them the primary point of purchase for mainstream and regional cider brands. Their strategic placement in dedicated alcohol aisles with high visibility and cross-category adjacency, is a major factor behind supermarket dominance. Additionally, private-label cider programs from retailers have captured a portion of supermarket cider sales, offering competitive pricing and localized branding that appeal to budget-conscious consumers. An additional critical driver is the integration of supermarkets into omnichannel retail ecosystems. Like, online grocery orders alcoholic beverage is growing. Supermarkets leverage loyalty programs, such as Kroger Rewards and Safeway for U, to personalize promotions and collect consumer data. This seamless blend of physical and digital access ensures supermarkets maintain their stronghold despite the rise of alternative retail models.

The Online Stores segment is the fastest-growing distribution channel and is projected to expand at a CAGR of 12.8% from 2026 to 2034. This growth is driven by the increasing consumer preference for convenience, subscription models, and direct access to niche and premium brands. The expansion of direct-to-consumer (DTC) sales by craft and regional cideries is a key driver. Platforms enable small cider producers to reach national audiences, with combined DTC sales growing fast. Brands have built loyal followings through limited releases, virtual tastings, and storytelling, emphasizing orchard heritage and fermentation artistry. A further critical factor is the growing integration of online alcohol marketplaces with curated discovery and gifting platforms. Subscription services like Cider Crate and First Sip Cider Club have gained popularity, offering monthly deliveries of rare and international ciders. The convenience of home delivery, combined with educational content and personalized recommendations, positions online stores as the most dynamic and scalable channel for premium and specialty cider growth.

REGIONAL ANALYSIS

The United States held a commanding position in the North America cider market by capturing a substantial share of total regional value in 2025. As the largest producer and consumer of hard cider in the region, the U.S. benefits from a mature craft beverage ecosystem, extensive apple cultivation, and strong consumer interest in alternative alcoholic drinks. The country is home to over 900 commercial cideries, concentrated in states like New York, Vermont, and Washington, where heirloom apple orchards support artisanal production.

Canada is establishing itself as a significant player with a growing emphasis on premium and craft cider production. British Columbia and Ontario are the nation’s cider hubs, with over 220 licensed cideries as of 2023, according to the Canadian Association of Cider Makers. Canadian consumers exhibit a strong preference for dry and semi-dry styles. The federal government’s Small Winery Tax Credit has been extended to cider producers, incentivizing small-batch innovation.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Aston Manor Brewery, C&C Group Plc, Carlsberg A/S, Distell Group, Halewood International Holdings Plc, Heineken UK Ltd., SABMiller Plc, Carlton & United Breweries Limited, The Boston Beer Company Inc. are some of the key players in the North America cider market.

The competitive landscape of the North America cider market is marked by a coexistence of large beverage conglomerates and independent craft producers, each vying for relevance in a category still defining its identity. Established players like Angry Orchard, Woodchuck, and Crispin dominate through scale, marketing, and retail penetration, while hundreds of regional cideries compete on authenticity, varietal depth, and local sourcing. Competition is intensifying around flavor differentiation, with brands moving beyond sweet profiles to dry, tannic, and wild-fermented styles that appeal to sophisticated palates. The rise of online sales and DTC models enables small producers to bypass traditional gatekeepers, increasing fragmentation. Retail shelf space is contested by RTD seltzers and flavored malt beverages, forcing cider brands to emphasize craftsmanship, agricultural heritage, and culinary versatility to maintain consumer interest and loyalty.

TOP PLAYERS IN THE MARKET

Angry Orchard

Angry Orchard, a pioneer in the modern North American cider movement, has played a transformative role in mainstreaming hard cider through accessible flavor profiles, national distribution, and consumer education. Owned by the Boston Beer Company, Angry Orchard has invested heavily in orchard development, including its 60-acre research orchard in New York’s Hudson Valley, where it cultivates over 80 heirloom and bittersweet apple varieties to refine flavor complexity. The company also strengthened its sustainability profile by renewable electricity use across its production facilities and introducing lightweight glass bottles to reduce carbon emissions. Through partnerships with culinary festivals and farm-to-table events, Angry Orchard has positioned cider as a sophisticated, food-friendly beverage.

Woodchuck Hard Cider

Woodchuck Hard Cider, one of the oldest and most established cider producers in the U.S., has shaped the category through innovation, broad portfolio diversification, and deep integration into the craft beverage ecosystem. Based in Vermont and owned by Anheuser-Busch InBev, Woodchuck has leveraged its scale to expand distribution while maintaining a craft identity. It also launched a limited-edition collaboration with Ben & Jerry’s, creating a cider inspired by the “Hazed & Confused” ice cream flavor, blending apple and blueberry with a creamy finish. Woodchuck intensified its presence in foodservice by partnering with regional barbecue chains and gastropubs to develop cider-pairing menus. Its investment in canning line efficiency reduced production waste, enhancing both sustainability and cost competitiveness.

Crispin Cider Company

Crispin Cider Company, known for its dry, English-style ciders, has carved a niche by aligning with wine and craft beer connoisseurs who value authenticity and minimal intervention. Acquired by MillerCoors (now Molson Coors Beverage Company), Crispin has maintained its artisanal ethos while expanding national reach. Crispin also deepened its commitment to regenerative agriculture by sourcing apples from certified organic orchards in Washington and Michigan, with a goal of 90% sustainable sourcing. The company launched a direct-to-consumer e-commerce platform with curated tasting kits and virtual experiences, enhancing engagement with loyal customers. Its participation in sommelier-led tastings and wine fairs has further elevated cider’s status as a serious fermented beverage.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Key players in the North America cider market are deploying a range of strategic initiatives to strengthen brand positioning and capture evolving consumer preferences. Major companies are expanding into premium, dry, and heritage-style ciders to appeal to wine and craft beer drinkers. Product innovation focuses on low-sugar, organic, and fruit-infused variants that align with health and wellness trends. Strategic collaborations with food brands, restaurants, and cultural events enhance visibility and culinary integration. Sustainability initiatives, including orchard conservation, renewable energy use, and lightweight packaging, are becoming central to brand identity. Direct-to-consumer e-commerce and subscription models enable personalized engagement and data collection. Additionally, national brands are leveraging their distribution networks to support craft partnerships, while smaller producers focus on storytelling, terroir, and limited releases to differentiate in a competitive landscape.

RECENT HAPPENINGS IN THE MARKET

- Asahi has completed the acquisition of Carlton and United Breweries, Australia's largest brewers. With the addition of some of Australia's most popular and well-loved beer brands, Asahi Beverages will be able to provide customers and consumers with an even broader selection of great-tasting beverages.

- Weston’s, a family-run cider company, has developed a raspberry and cucumber variation to their Rosie's Pig line.

MARKET SEGMENTATION

This research report on the North American cider market has been segmented and sub-segmented into the following categories.

By Type

- Still Cider

- Sparkling Cider

- Draft Cider

- Apple Wine

- Others

By Distribution Channels

- Hypermarkets

- Supermarkets

- Departmental Stores

- Convenience Stores

- Online Stores

By Country

- The U.S.

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

1. What is the North America Cider Market?

The market includes alcoholic beverages made from fermented apple juice and other fruits, consumed across the U.S., Canada, and Mexico.

2. What drives growth in the North America Cider Market?

Growing demand for craft beverages, rising health-conscious consumers, and preference for gluten-free drinks fuel market growth.

3. Which countries dominate the North America Cider Market?

The United States leads cider consumption, followed by Canada and Mexico with increasing popularity.

4. Which distribution channels are key in the North America Cider Market?

Bars, restaurants, supermarkets, liquor stores, and online sales platforms are major distribution channels.

5. Who are the leading players in the North America Cider Market?

Key players include Angry Orchard, Woodchuck Cider, Boston Beer Company, Strongbow, and Ace Cider.

6. What consumer trends shape the North America Cider Market?

Trends include low-alcohol options, fruit-flavored varieties, organic ciders, and sustainable packaging.

7. What challenges face the North America Cider Market?

Challenges include competition from beer and wine, seasonal demand, and regulatory complexities.

8. Which consumer segments drive the North America Cider Market?

Millennials, health-conscious drinkers, and consumers seeking gluten-free alcoholic options drive demand.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com