- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

North America Frozen Food Market Size

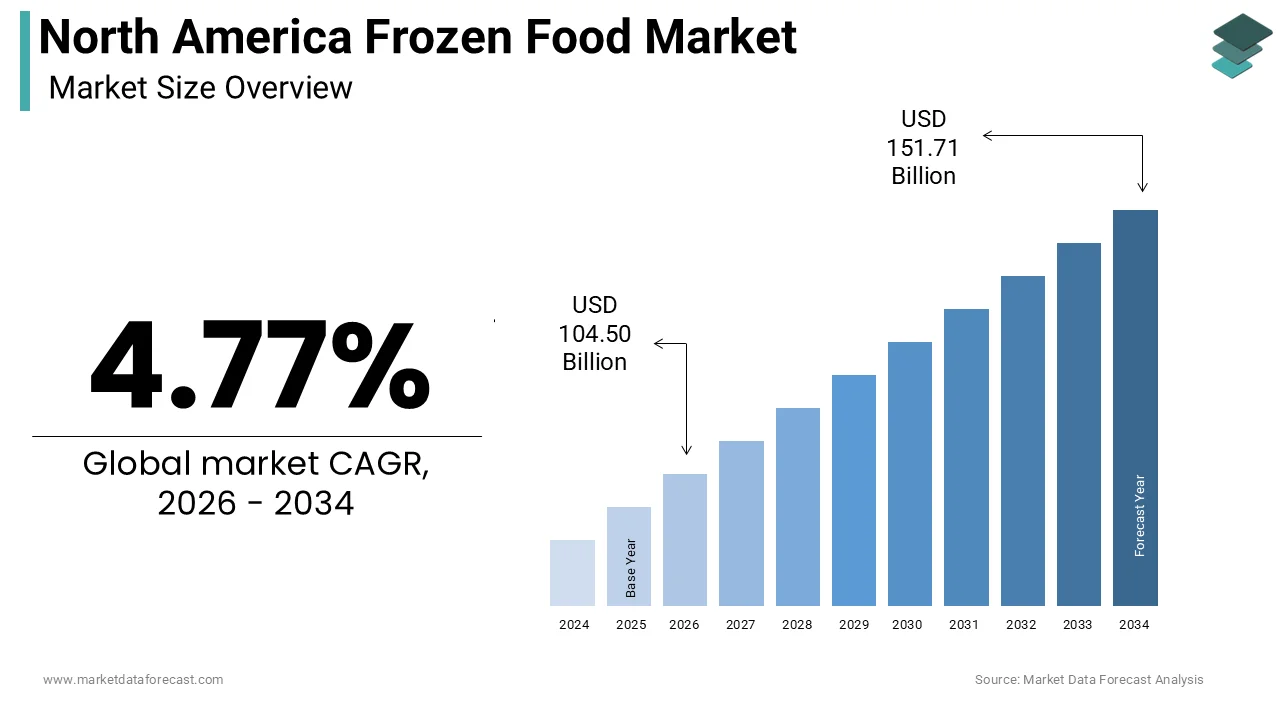

The size of the North American frozen food market was calculated to be USD 99.74 billion in 2025 and is anticipated to be worth USD 151.71 billion by 2034, from USD 104.50 billion in 2026, growing at a CAGR of 4.77% during the forecast period.

The North American frozen food market covers a wide range of pre-prepared, preserved, and ready-to-eat food products that are stored at sub-zero temperatures to extend shelf life while retaining nutritional value and texture. This market includes categories such as frozen vegetables, fruits, meats, seafood, ready meals, bakery items, and dairy-based frozen desserts. Over the past decade, the industry has evolved beyond convenience foods to include premium, organic, and health-focused offerings, aligning with shifting consumer preferences.

The sector benefits from increased urbanization, dual-income households, and growing demand for time-saving meal solutions. In addition, advancements in freezing technology have significantly improved product quality, making frozen produce sometimes fresher than its fresh counterpart due to immediate processing post-harvest.

MARKET DRIVERS

Increasing Demand for Convenience and Ready-to-Eat Meals

One of the primary drivers of the North American frozen food market is the growing consumer preference for convenience-oriented and ready-to-eat meal options. With rising urbanization, increasing work hours, and a surge in dual-income households, consumers are seeking time-saving yet nutritious food alternatives that fit into fast-paced lifestyles. According to the Bureau of Labor Statistics (BLS), the average American spent just under 38 minutes per day on food preparation and cleanup in 2023, reflecting a steady decline over the past two decades. This shift has led to greater reliance on pre-prepared and easy-to-cook meals, many of which are found in the frozen food aisle. Additionally, the rise of single-person households and smaller family units has contributed to this trend, as individuals increasingly opt for portion-controlled, quick-prep meals. Retailers and manufacturers have responded by expanding their offerings of gourmet, ethnic, and plant-based frozen meals tailored to evolving tastes and dietary preferences, thereby fueling sustained growth in the frozen food segment.

Advancements in Freezing Technology and Nutritional Awareness

Technological improvements in freezing methods have played a crucial role in reshaping consumer perceptions and boosting demand for frozen foods across North America. Innovations such as flash freezing, individually quick freezing (IQF), and vacuum sealing have enhanced the texture, flavor retention, and nutritional integrity of frozen products, making them competitive with fresh alternatives. This scientific backing has helped dispel long-standing misconceptions about the inferiority of frozen foods, encouraging health-conscious consumers to integrate them into balanced diets. Furthermore, organizations like the American Frozen Food Institute (AFFI) have actively promoted research-backed messaging around the benefits of frozen foods, influencing public opinion and dietary recommendations. These developments have been instrumental in driving both retail and food service adoption, supporting the sustained expansion of the frozen food market across North America.

MARKET RESTRAINTS

Consumer Perception Concerns Regarding Additives and Preservatives

Despite technological advancements, one major restraint affecting the North American frozen food market is the lingering consumer skepticism regarding the use of additives, preservatives, and artificial ingredients in frozen food products. Many consumers still associate frozen meals with high sodium content, chemical stabilizers, and lower overall quality compared to fresh alternatives. According to the International Food Information Council (IFIC), nearly 60% of U.S. consumers in 2023 expressed concerns about the presence of unfamiliar or synthetic ingredients in processed and frozen foods. This perception is particularly strong among millennials and Gen Z, who prioritize clean-label products and scrutinize ingredient lists before purchasing decisions. In response, several brands have reformulated their frozen food lines to remove artificial preservatives and enhance transparency through labeling initiatives. However, these changes often come with higher production costs, which can lead to elevated retail prices and reduced affordability for budget-conscious shoppers.

Volatility in Raw Material and Energy Costs

Another significant challenge impeding the growth of the North American frozen food market is the fluctuation in raw material and energy costs, which directly impacts production expenses and pricing stability. Ingredients such as meat, dairy, grains, and vegetables are subject to seasonal availability, climate conditions, and global trade dynamics, leading to price volatility. According to the U.S. Department of Agriculture (USDA), agricultural commodity prices saw a sharp increase in 2023 due to supply chain disruptions, extreme weather events, and geopolitical tensions affecting key exporting regions. Moreover, the energy-intensive nature of freezing and cold storage operations makes the industry highly sensitive to electricity and natural gas price fluctuations.

MARKET OPPORTUNITIES

Expansion of Premium and Organic Frozen Food Lines

A major opportunity emerging in the North American frozen food market is the growing demand for premium and organic frozen products that cater to health-conscious and environmentally aware consumers. Shoppers are increasingly prioritizing clean-label, sustainably sourced, and minimally processed frozen meals, prompting manufacturers to expand their high-end offerings. Consumers are showing strong interest in certified organic vegetables, plant-based proteins, and gluten-free frozen meals that align with specific dietary needs and wellness goals. This shift is being driven by younger generations—particularly millennials and Gen Z—who seek convenience without compromising on health or ethical sourcing. Companies such as Amy’s Kitchen, Birds Eye, and Green Giant have capitalized on this trend by introducing organic frozen entrees, smoothie packs, and functional snacks fortified with vitamins and probiotics. Retailers are also expanding frozen organic sections in supermarkets and online grocery platforms, further enhancing accessibility.

Growth of E-Commerce and Direct-to-Consumer Frozen Food Sales

The rapid expansion of e-commerce and direct-to-consumer (DTC) frozen food delivery services presents a compelling opportunity for the NortAmericanca frozen food market. With digital shopping becoming increasingly ingrained in consumer behavior, companies are leveraging online platforms to reach wider audiences and offer specialized frozen food options. Online retailers such as Amazon Fresh, Instacart, and regional DTC startups have introduced temperature-controlled logistics and same-day delivery models that ensure frozen food quality is maintained throughout the supply chain. Additionally, meal kit providers like HelloFresh and Factor have incorporated frozen components into their offerings, blending convenience with freshness. These services appeal to consumers looking for curated, portion-controlled meals that minimize food waste and save preparation time. As last-mile delivery infrastructure improves and cold storage logistics become more efficient, the frozen food industry is well-positioned to capitalize on this digital transformation, opening new revenue streams and enhancing customer engagement across North America.

MARKET CHALLENGES

Logistical Complexity in Cold Chain Management

One of the most pressing challenges facing the North American frozen food market is the complexity and cost associated with maintaining an uninterrupted cold chain from production to final delivery. Unlike ambient or refrigerated goods, frozen foods require consistent sub-zero temperatures throughout storage, transportation, and retail display to preserve quality and safety. According to the International Institute of Refrigeration (IIR), even minor temperature fluctuations during transit can lead to ice crystal formation, texture degradation, and diminished nutritional value. This necessitates specialized equipment such as blast freezers, insulated containers, and temperature-monitored trucks, all of which add to operational expenditures. Moreover, the rise of direct-to-consumer frozen food delivery has intensified logistical demands, requiring companies to invest in advanced cold chain technologies and real-time tracking systems. These complexities not only impact profit margins but also pose barriers to market expansion, particularly for smaller brands attempting to scale without robust logistics partnerships.

Regulatory Compliance and Labeling Standards

Navigating regulatory compliance and adhering to evolving labeling standards present another significant challenge for the North American frozen food market. Manufacturers must contend with stringent food safety regulations, ingredient disclosure requirements, and nutritional claims oversight from agencies such as the U.S. Food and Drug Administration (FDA) and Health Canada.

According to the FDA’s 2023 guidance updates, food labels now require more detailed information on added sugars, trans fats, and serving sizes, compelling frozen food producers to reformulate products or modify packaging. Additionally, the implementation of the U.S. Food Safety Modernization Act (FSMA) has heightened preventive controls for food manufacturing facilities, increasing compliance costs and operational complexity. These regulatory shifts require continuous investment in quality assurance, legal consultation, and consumer education efforts.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.77% |

| Segments Covered | By Product, User, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | The US, Canada, and the rest of North America |

| Market Leaders Profiled | Aryzta AG, General Mills Inc., Kraft Foods Group Inc., Ajinomoto Co. Inc., Cargill Incorporated, Europastry S.A., JBS S.A., Kellogg’s Company, Nestle S.A., and Flower Foods. |

SEGMENTAL ANALYSIS

By Product Insights

The frozen vegetables and fruits segment held the largest share of the North America frozen food market by accounting for approximately 28.4% of total market revenue in 2025. This dominance is primarily attributed to increasing consumer focus on health, convenience, and year-round availability of produce. This scientific backing has helped shift perceptions, especially among health-conscious consumers who seek nutrient-dense meal options without compromising on time or quality. With rising demand for plant-based diets and clean-label ingredients, this segment continues to maintain its leadership position in the frozen food landscape.

The frozen ready meals segment is emerging as the fastest-growing within the North American frozen food market, projected to expand at a CAGR of 6.4%. This rapid growth is primarily fueled by changing lifestyles, increased urbanization, and a growing preference for quick yet nutritious meal solutions. This trend has led to a surge in demand for pre-prepared meals that offer convenience without sacrificing flavor or nutrition. Moreover, manufacturers have expanded their offerings to include premium, organic, and ethnic-inspired frozen meals tailored to evolving tastes. Retailers are also enhancing frozen meal sections in supermarkets and online grocery platforms, further boosting accessibility and consumer adoption across North America.

By User Insights

The retail segment accounted for the majority of the North American frozen food market in 2025. This dominance is due to widespread consumer adoption of frozen foods for household consumption, supported by strong supermarket and e-commerce distribution networks. Major retailers such as Walmart, Kroger, and Albertsons have expanded their frozen food aisles to include a broader range of premium, organic, and ready-to-eat options catering to diverse dietary preferences. The combination of affordability, convenience, and nutritional benefits makes frozen food a staple in modern retail shopping, reinforcing the segment’s leading position in the market.

The food service industry is a booming segment within the North American frozen food market, expanding at a CAGR of 6.1%. This growth is primarily driven by increasing reliance on frozen ingredients in commercial kitchens, including restaurants, hotels, and institutional catering operations. Quick-service restaurants (QSRs) and fast-casual chains increasingly depend on frozen ready-to-cook items such as patties, nuggets, and pre-cut vegetables to maintain efficiency and scalability. Furthermore, post-pandemic recovery in the hospitality sector has accelerated demand for cost-effective and time-saving food solutions. Technomic reports that off-premise dining, including takeout and delivery, remains a dominant trend, encouraging operators to integrate high-quality frozen entrees into their menus.

REGIONAL ANALYSIS

The United States maintained the dominant position in the North American frozen food market. This is underpinned by high consumer penetration, well-established retail infrastructure, and a strong presence of major frozen food manufacturers. Consumer demand is driven by convenience, affordability, and improved perceptions regarding the nutritional value of frozen produce. Additionally, the U.S. food services sector has increasingly adopted frozen ingredients to enhance operational efficiency, particularly in quick-service and full-service restaurants.

Canada represented a significant and steadily growing contributor to the North American frozen food market. The country's market expansion is largely driven by urbanization, changing dietary habits, and increasing reliance on convenient meal solutions among working professionals and single-person households. Moreover, the rise of e-commerce and online grocery delivery services such as Amazon Fresh and Instacart has made frozen foods more accessible to rural and suburban populations. As major brands expand their frozen food portfolios and introduce premium, plant-based, and functional frozen options, Canada’s frozen food market is expected to continue its upward trajectory.

The "Rest of North America" segment, primarily comprising Mexico and select Caribbean territories, will contribute a decent share of the total regional market value in 2025. Though relatively smaller in scale compared to the U.S. and Canada, this segment is showing promising growth due to improving economic conditions, increasing urbanization, and rising disposable incomes. This economic momentum has translated into higher investments in food processing, retail infrastructure, and frozen food imports. Additionally, tourism-driven economies in the Caribbean, such as Puerto Rico and the Bahamas, have seen increased adoption of frozen food products in both retail and hospitality sectors.

TOP PLAYERS IN THE NORTH AMERICAN FROZEN FOOD MARKET

Nestlé S.A.

Nestlé is a global leader in the frozen food industry, with a strong presence across North America through its diverse portfolio of frozen meals, vegetables, and desserts. The company's commitment to innovation has led to the development of premium, nutritious, and sustainable frozen products tailored to evolving consumer preferences. Known for brands like Stouffer’s and Lean Cuisine, Nestlé continues to influence market trends by introducing healthier formulations, plant-based options, and convenient meal solutions that cater to modern lifestyles.

Conagra Brands, Inc.

Conagra is one of the most prominent players in the North American frozen food landscape, offering a wide range of products under well-established brands such as Birds Eye, Healthy Choice, and Banquet. The company has consistently focused on product diversification, quality enhancement, and strategic brand positioning to meet changing dietary demands. Its emphasis on convenience, affordability, and nutritional transparency has helped solidify its reputation among both retail consumers and food service operators.

General Mills, Inc.

General Mills plays a crucial role in shaping the frozen food market in North America through its well-known brands, including Totino’s, Pillsbury, and Betty Crocker. The company leverages strong brand equity and extensive distribution networks to maintain a competitive edge. With a focus on innovation, sustainability, and expanding into premium and organic frozen categories, General Mills continues to drive growth and consumer engagement across multiple frozen food segments.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by key players in the North American frozen food market is continuous product innovatio,n and companies are investing heavily in developing healthier, clean-label, and functional frozen foods that align with shifting consumer health trends and regulatory expectations. This includes reducing sodium, eliminating artificial additives, and incorporating plant-based and organic ingredients.

Another critical approach is enhancing digital engagement and e-commerce integration. Leading manufacturers are strengthening their online presence through direct-to-consumer platforms, partnerships with grocery delivery services, and data-driven marketing strategies. This allows them to reach a broader customer base and improve supply chain responsiveness to fluctuating demand patterns.

Lastly, firms are increasingly engaging in strategic brand acquisitions and collaborations to expand their product portfolios and enter new consumer segments. These moves help companies diversify offerings, strengthen market position, and respond more effectively to competitive pressures within the dynamic frozen food sector.

KEY MARKET PLAYERS AND COMPETITIVE OVERVIEW

Major Players in the North American frozen food market include Aryzta AG, General Mills Inc., Kraft Foods Group Inc., Ajinomoto Co. Inc., Cargill Incorporated, Europastry S.A., JBS S.A., Kellogg’s Company, Nestle S.A., and Flower Foods.

The competition in the North American frozen food market is highly dynamic, characterized by the presence of large multinational corporations, regional players, and emerging private-label brands vying for consumer preference and shelf space. Established industry leaders dominate due to their strong brand recognition, extensive distribution networks, and ability to invest in continuous product innovation. However, mid-tier and niche-market companies are gaining traction by focusing on specialized offerings such as organic, plant-based, and functional frozen foods tailored to specific dietary needs.

Retailers also play a pivotal role in shaping market dynamics, with private-label frozen food lines becoming increasingly sophisticated and competitive against branded products. Consumer expectations around transparency, sustainability, and health-conscious ingredients have intensified pressure on manufacturers to reformulate products and enhance packaging claims. At the same ttimeservicece operators are leveraging frozen ingredients to streamline kitchen operations and maintain consistency in taste and portion control.

Digital transformation is another key battleground, with companies investing in e-commerce platforms, subscription models, and smart logistics to ensure product availability and convenience. As the frozen food market evolves, agility, innovation, and strategic branding will remain essential for companies seeking to maintain or enhance their market positions.

RECENT HAPPENINGS IN THE MARKET

- In February 2023, Nestlé launched a new line of plant-based frozen meals under its Lean Cuisine brand, targeting health-conscious consumers looking for sustainable protein alternatives. This initiative aimed to capitalize on the growing demand for eco-friendly and low-calorie meal options while reinforcing Nestlé’s leadership in nutrition-focused frozen food innovation.

- In July 2023, Conagra introduced an expanded clean-label initiative across its Birds Eye frozen vegetable line, removing artificial preservatives and enhancing ingredient transparency. This move was designed to align with consumer demand for minimally processed foods and reinforce trust in the brand’s quality and safety standards.

- In January 2025, General Mills partnered with a leading online grocery delivery service to increase the accessibility of its frozen products through digital platforms. This collaboration aimed to boost direct-to-consumer sales and improve last-mile delivery efficiency for frozen food items.

- In September 2023, Tyson Foods expanded its portfolio of frozen ready-to-cook meals by launching a new ethnic-inspired product line featuring global flavors and quick-prep formats. This expansion targeted younger consumers seeking variety and convenience without compromising on taste.

- In May 2025, McCain Foods invested in a state-of-the-art freezing facility in Canada to enhance production capacity and support the growing demand for frozen potato products in both retail and foodservice sectors. This strategic move strengthened the company’s supply chain resilience and product availability across North America.

DETAILED SEGMENTATION OF THE NORTH AMERICA FROZEN FOOD MARKET IS INCLUDED IN THIS REPORT

This research report on the North America Frozen Food Market has been segmented and sub-segmented based on product, user & region.

By Product

- Frozen Vegetables & Fruits

- Frozen Ready Meals

By User

- Retail

- Food Service Industry

By Region

- US

- Canada

- Mexico

- Rest of North America