Global Oncology Information System Market Size, Share, Trends & Growth Forecast Report By Products, and Services (Patient Information Systems, Treatment Planning Systems, Consulting/Optimization Services, Implementation Services and Post-Sale and Maintenance Services), Application (Surgical Oncology, Medical Oncology and Radiation Oncology), End Users and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Market Size, 2025

$3.25 BnMarket Estimate, 2026

$3.52 BnMarket Forecast, 2034

$6.72 BnCAGR, 2026–2034

8.41%Global Oncology Information System Market Report Summary

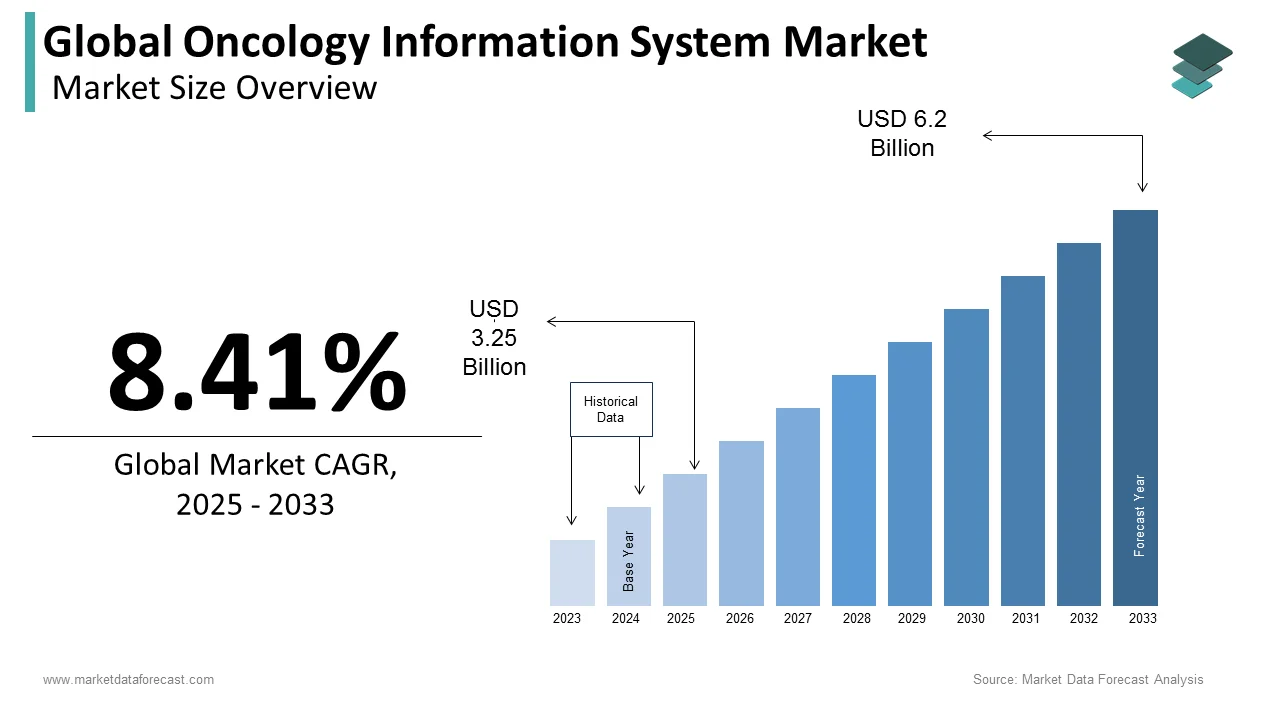

The global oncology information system market was valued at USD 3.25 billion in 2025, is estimated to reach USD 3.52 billion in 2026, and is projected to reach USD 6.72 billion by 2034, growing at a CAGR of 8.41% from 2026 to 2034. Market growth is driven by the increasing global burden of cancer, rising adoption of digital healthcare solutions, and the growing need for efficient data management in oncology care. Oncology information systems (OIS) play a critical role in streamlining patient data, treatment planning, and clinical workflows, particularly in radiation oncology. Additionally, advancements in healthcare IT, integration with electronic health records (EHRs), and increasing investments in cancer care infrastructure are supporting market expansion.

Key Market Trends

- Rising adoption of digital oncology workflows and data management systems.

- Increasing integration with electronic health records (EHRs).

- Growing demand for radiation oncology planning and management solutions.

- Expansion of healthcare IT infrastructure in cancer care.

- Increasing focus on personalized and data-driven oncology treatment.

Segmental Insights

- Based on products and services, the patient information systems segment dominated the global oncology information system market by capturing 45.1% share in 2025, driven by the need for centralized patient data management.

- Based on application, the radiation oncology segment led the market with 42.3% share in 2025, supported by increasing use of advanced radiation therapies.

- Based on end users, the hospitals and physician offices segment held the majority share in 2025 due to high patient volumes and the need for integrated oncology care systems.

Regional Insights

The global oncology information system market is witnessing steady growth across major regions due to increasing cancer prevalence and digital transformation in healthcare.

- North America led the market in 2025 with 44.4% share, supported by advanced healthcare IT infrastructure and high adoption of digital solutions.

- Europe followed with 26.5% share in 2025, driven by strong healthcare systems and government initiatives.

- Asia-Pacific is the fastest-growing region due to a large population base, rising cancer incidence, and increasing investments in healthcare modernization.

Competitive Landscape

The global oncology information system market is competitive, with key players focusing on technological innovation, system integration, and expanding their product offerings. Companies are investing in advanced analytics, cloud-based platforms, and interoperability solutions to enhance oncology care delivery.

Prominent companies operating in the global oncology information system market include Accuray Incorporated, Altos Solutions, Inc., Cerner Corporation, Elekta AB, Epic Systems Corporation, Koninklijke Philips N.V., McKesson Corporation, and Varian Medical Systems, Inc.

Global Oncology Information System Market Size

The size of the global oncology information system market was worth USD 3.25 billion in 2025. The global market is anticipated to grow at a CAGR of 8.41% from 2026 to 2034 and be worth USD 6.72 billion by 2034 from USD 3.52 billion in 2026.

An Oncology Information System (OIS) is a specialized software platform designed to manage the entire "cancer journey" of a patient, from initial screening and diagnosis to treatment, follow-up, and palliative care. These systems facilitate precision medicine by enabling oncologists to track patient histories, monitor treatment responses, and adhere to evolving clinical guidelines with unprecedented accuracy. The definition extends beyond simple data storage to include advanced analytics for population health management and real-time decision support tools that mitigate medication errors. As per data from the World Health Organization, cancer remains a leading cause of death worldwide, accounting for nearly 10 million deaths in 2022, which necessitates a robust digital infrastructure to handle the increasing volume of cases. According to the American Cancer Society, approximately 2 million new cancer cases are diagnosed annually in the United States alone, creating an immense administrative burden that manual processes cannot sustain. The market operates at the intersection of clinical oncology and health informatics, driven by the need for interoperability between disparate hospital systems. Eurostat projections indicate that the population aged 65 and over in the European Union (EU-27) is expected to reach 29.4% of the total population by 2050, significantly expanding the demographic requiring chronic cancer management. This demographic shift forces healthcare providers to adopt scalable digital solutions that ensure continuity of care across multidisciplinary teams. The sector is increasingly focused on cloud-based architectures that support remote monitoring and tele-oncology, bridging gaps in access for rural patients. Unlike general hospital information systems, these platforms must accommodate highly specific workflows related to radiation dosing and complex drug regimens, making them indispensable for modern cancer centers striving for operational excellence and improved patient outcomes.

MARKET DRIVERS

Escalating Global Cancer Incidence and Complexity of Treatment Regimens

The relentless rise in cancer incidence in the world is one of the major drivers of the global oncology information system market. Furthermore, the increasing complexity of multimodal treatment protocols demands precise coordination and documentation. Modern oncology care often involves a combination of surgery, radiation, immunotherapy, and targeted agents, each requiring meticulous scheduling, dosing calculations, and toxicity monitoring that exceed human cognitive limits without digital assistance. According to statistics from the International Agency for Research on Cancer, the global burden of cancer is expected to rise to 28.4 million new cases by 2040, a 47 percent increase from 2020 figures, overwhelming traditional paper-based or fragmented digital records. Data from health surveillance and research indicate that a significant proportion of cancer patients receive multiple lines of therapy, necessitating seamless data exchange between radiologists, medical oncologists, and surgeons to prevent adverse events. This complexity is further exacerbated by the advent of personalized medicine, where treatment decisions rely on genomic profiling and biomarker analysis that generate vast amounts of unstructured data. As per guidelines issued by the Commission on Cancer in the United States, accredited programs must utilize standardized, certified software to capture and report specific data elements to the National Cancer Database for nearly all cases, forcing facilities to upgrade from generic electronic health records to dedicated oncology modules. The sheer volume of patient interactions and the critical nature of timing in chemotherapy administration create an inelastic demand for sophisticated information systems that can orchestrate these intricate workflows. As cancer becomes a chronic, manageable condition for many, the longitudinal tracking of survivorship care plans further entrenches the need for dedicated oncology platforms capable of managing decades of patient data.

Regulatory Mandates for Data Standardization and Quality Reporting

Tightening global regulatory frameworks is significantly accelerating the expansion of the global oncology information system market. They mandate rigorous data standards, quality reporting, and cancer registry participation to improve public health outcomes and accountability. Governments and accrediting bodies are increasingly requiring cancer centers to submit detailed treatment data to national registries to track survival rates and adherence to evidence-based guidelines, a task that is virtually impossible without specialized information systems. The European Union's Cross-Border Healthcare Directive similarly encourages the harmonization of cancer data to facilitate research and patient mobility across member states. Data from the Organisation for Economic Co-operation and Development suggests that countries with comprehensive cancer registration systems and mandatory data reporting demonstrate improved survival rates due to earlier detection and standardized care pathways, incentivizing governments to fund digital infrastructure. Furthermore, value-based care models tie reimbursement rates to quality metrics such as readmission rates and complication frequencies, compelling providers to leverage analytics within oncology systems to identify areas for improvement. The Food and Drug Administration also mandates strict tracking of adverse events for new oncology drugs, requiring systems that can automatically flag and report these incidents. This regulatory pressure transforms oncology information systems from optional tools into compliance necessities, driving widespread implementation across both large academic centers and community practices seeking to maintain accreditation and secure funding.

MARKET RESTRAINTS

Prohibitive Implementation Costs and Resource Intensiveness

The exorbitant cost associated with acquisition, customization, and ongoing maintenance hampers the widespread deployment of these systems and the growth of the global oncology information system market. This financial barrier places a severe strain on smaller community practices and resource-limited healthcare systems. Unlike general practice software, oncology platforms require extensive configuration to match specific institutional workflows, integration with legacy laboratory and imaging systems, and continuous updates to reflect changing treatment protocols, all of which demand significant capital investment. Research indicates that the total cost of ownership for comprehensive oncology information systems remains a significant barrier for mid-sized cancer centers, with expenses covering hardware, licensing, and consulting fees often straining capital budgets. Reports on independent medical practices confirm that a significant portion delay or forego technology upgrades due to budget constraints, as concerns persist that the return on investment will not materialize quickly enough to sustain independent operations. Additionally, the hidden costs of downtime during implementation and the need for temporary staff to manage the transition further inflate the financial burden. A study affirms that small practices often lack the necessary IT infrastructure to support modern cloud-based or on-premise solutions, frequently necessitating expensive network overhauls before implementation can occur. The scarcity of specialized IT personnel trained in oncology informatics drives up labor costs for system management and troubleshooting. Consequently, many smaller providers continue to rely on outdated or disjointed systems, limiting their ability to participate in advanced care networks and clinical trials, thereby creating a digital divide that restricts overall market penetration despite the clear clinical benefits.

Interoperability Challenges and Fragmented Data Ecosystems

Persistent lack of seamless interoperability between oncology information systems and other healthcare IT platforms is a critical restraint to the global oncology information system market. This failure creates data silos that diminish both care coordination and analytical utility. Despite advancements in health data standards like HL7 and FHIR, many oncology systems struggle to exchange structured data effectively with external electronic health records, pharmacy management systems, and genomic databases, resulting in fragmented patient profiles. Studies in clinical oncology informatics consistently show that the vast majority of critical patient data remains trapped in unstructured formats or incompatible systems, forcing clinicians to manually re-enter information and increasing the risk of transcription errors. The Office of the National Coordinator for Health Information Technology highlights that proprietary vendor standards create persistent barriers to data liquidity, preventing the creation of a unified, longitudinal view of the patient journey across care settings. This fragmentation impedes the ability to aggregate data for population health management and real-world evidence generation, which are key value propositions of these systems. Clinical oncology research indicates that poor interoperability and fragmented data access contribute to measurable delays in treatment initiation as care teams wait for complete medical records, which can negatively impact patient outcomes. Furthermore, the inability to seamlessly integrate with emerging digital health tools like wearable monitors and patient-reported outcome apps limits the holistic capabilities of current platforms. The full potential of oncology information systems to transform cancer care will remain unrealized, acting as a brake on market growth and user satisfaction. This will continue until vendors adopt universal connectivity protocols and prioritize open architecture.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Predictive Analytics and Precision Medicine

Deeply integrating artificial intelligence and machine learning algorithms into these systems offers a transformative opportunity for the global oncology information system market. This integration enables predictive analytics, early detection of recurrence, and personalized treatment recommendations. By leveraging vast repositories of historical patient data, genomic profiles, and treatment outcomes, AI-driven systems can identify subtle patterns that human clinicians might miss, facilitating truly precision-based care. Researchers at the Massachusetts Institute of Technology have utilized machine learning models to simulate and improve chemotherapy dosing schedules, aiming to minimize side effects and reduce toxicity by finding an optimal, personalized treatment plan. The National Cancer Institute and various hospital networks are using AI to streamline patient enrollment in clinical trials, allowing for more precise matching of patients to studies and increasing the overall efficiency of trial matching and recruitment. Furthermore, natural language processing capabilities allow these systems to extract valuable insights from unstructured clinical notes and pathology reports, enriching the data available for decision-making. Data tracking firms have reported substantial surges in investments within the AI-enabled oncology software sector, demonstrating high confidence in its ability to enhance drug development and precision diagnostics. Hospitals adopting these intelligent systems can differentiate themselves by offering superior outcomes and reduced trial-and-error prescribing. The ability to simulate treatment responses based on individual patient characteristics opens new revenue streams for software vendors through premium analytics modules. The synergy between oncology information systems and AI will redefine standard care as computational power increases and datasets grow. Consequently, this creates a lucrative niche for innovators delivering actionable intelligence at the point of care.

Expansion of Tele-Oncology and Remote Patient Monitoring Capabilities

The rapid evolution of tele-oncology and remote patient monitoring creates major possibilities for OIS vendors to expand their platforms beyond the clinic walls, which is likely to promote the expansion of the global oncology information system market. This addresses the growing demand for accessible and convenient cancer care. Cancer treatments are increasingly becoming oral and home-administered. Consequently, the need for digital tools that track adherence, monitor symptoms, and facilitate virtual consultations has become paramount, particularly for rural and underserved populations. Data from the American Telemedicine Association shows that tele-oncology services experienced a massive surge during the recent pandemic, leading to a permanent, sustained shift towards hybrid care models for cancer management. Oncology information systems that incorporate secure video conferencing, patient portals for symptom reporting, and integration with wearable devices for vital sign monitoring are poised to capture this expanding market segment. The Centers for Medicare and Medicaid Services has expanded reimbursement codes for remote therapeutic monitoring, providing a financial incentive for providers to adopt these technologies. Research into patient satisfaction suggests a high preference for hybrid cancer care, which balances in-person visits with virtual check-ins, reducing the travel burden and enhancing comfort. Vendors can leverage this trend by offering modular add-ons that transform static records into dynamic engagement platforms, fostering continuous care loops. Furthermore, remote monitoring allows for real-time data collection on quality of life and adverse events, enriching real-world evidence databases. Companies can unlock new customer bases by positioning their systems as the central hub for hybrid care delivery. Doing so drives recurring revenue through subscription-based remote monitoring services.

MARKET CHALLENGES

Critical Shortage of Informatics-Trained Oncology Professionals

There is an acute shortage of healthcare professionals with dual expertise in clinical oncology and health informatics. This shortage is a paramount challenge for the global oncology information system market, which hinders effective system utilization and optimization. Vendors provide robust tools, but staff often struggle to fully leverage advanced features like clinical decision support, data analytics, and workflow automation. This inability limits the return on investment and can lead to user frustration. The complexity of cancer care requires users who understand both the nuances of treatment protocols and the technical capabilities of the software, a rare combination of skills. Without adequate training and support, clinicians often revert to workarounds that bypass system safeguards, reintroducing risks of errors and data inconsistencies. The lack of standardized curricula in medical schools regarding health IT further exacerbates this issue, leaving new graduates ill-prepared for digital-first environments. The market will struggle to realize the full potential of deployed systems until educational institutions and professional societies prioritize informatics training and certification programs. Consequently, these inactionable factors will hinder adoption rates and stifle innovation.

Heightened Cybersecurity Threats and Data Privacy Concerns

OISs are increasingly targeted by sophisticated cyberattacks, ransomware gangs, and identity thieves, which in turn limits the expansion of the global oncology information system market. These systems are particularly vulnerable because they house highly sensitive genetic, diagnostic, and treatment data. The centralized nature of these platforms, which aggregate comprehensive patient histories, creates a single point of failure that can cripple entire cancer centers if compromised, potentially delaying life-saving treatments. Oncology data is particularly valuable on the black market due to its richness and permanence, attracting state-sponsored actors and organized crime syndicates. The General Data Protection Regulation in Europe and the Health Insurance Portability and Accountability Act in the United States impose stringent penalties for data breaches, creating a high-stakes compliance environment. The fear of such breaches forces institutions to invest heavily in defensive measures, slowing down the adoption of cloud-based solutions and innovative features that might introduce new attack vectors. Balancing the need for open data access for research and care coordination with rigorous security postures remains a delicate and resource-intensive endeavor that threatens to stall market momentum.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Products and Services, Application, End-Users, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Accuray Incorporated (U.S.), Altos Solutions, Inc. (U.S.), Cerner Corporation (U.S.), Elekta AB (Sweden), Epic Systems Corporation (U.S.), Koninklijke Philips N.V. (The Netherlands), McKesson Corporation (U.S.), and Varian Medical Systems, Inc. (U.S.). |

SEGMENTAL ANALYSIS

By Products and Services Insights

The Patient Information Systems segment dominated the global oncology information system market and accounted for a 45.1% share in 2025. This dominance of the segment is driven by the fundamental necessity of maintaining comprehensive, longitudinal electronic health records. These records serve as the central repository for all patient data, from diagnosis through survivorship, forming the backbone of modern cancer care delivery. One key reason for sustaining the command of patient information systems is the critical need to consolidate vast amounts of fragmented clinical data into a single source of truth to manage the chronic and complex nature of cancer care. Unlike acute conditions, cancer treatment often spans years involving multiple specialists, modalities, and settings, requiring a unified view of pathology reports, imaging results, genomic profiles, and treatment histories to ensure safe and effective care. Furthermore, the shift toward value-based care mandates rigorous tracking of outcomes and quality metrics over the entire patient journey, which is only possible with a centralized database. The ability to generate real-time dashboards for tumor boards and multidisciplinary teams further cements the indispensability of these systems. As cancer incidence rises and treatments become more personalized, the reliance on comprehensive patient information systems to orchestrate care will only intensify, securing its dominant market position. A key factor supporting this segment is the stringent regulatory landscape that mandates detailed data capture and reporting for cancer registries, accreditation bodies, and government reimbursement programs, forcing healthcare providers to adopt sophisticated patient information systems. Accreditation from organizations like the Commission on Cancer requires facilities to abstract and submit specific data elements for nearly every cancer case, a process that is labor-intensive and error-prone without automated software support. As per compliance guidelines issued by the Centers for Medicare and Medicaid Services, failure to report quality measures accurately can result in significant financial penalties and reduced reimbursement rates, creating a powerful economic incentive for adoption. The European Union's General Data Protection Regulation also imposes strict requirements on how sensitive patient data is stored, accessed, and audited, necessitating systems with advanced security and governance features. Additionally, the push for interoperability under laws like the 21st Century Cures Act in the United States forces providers to use certified health IT modules that facilitate data exchange. The inability to meet these regulatory standards risks loss of accreditation and funding, making patient information systems not just a clinical tool but a compliance necessity. This regulatory pressure ensures consistent demand and high retention rates for these systems across all types of healthcare facilities.

The Consulting and Optimization Services segment is estimated to register the fastest CAGR of 12.8% from 2026 to 2034 due to the increasing complexity of system implementations, the need for workflow redesign to maximize return on investment, and the shortage of internal expertise required to manage these specialized platforms. The fast growth of this segment also comes from the extreme complexity of integrating oncology information systems into existing hospital ecosystems, which often involves reconciling disparate legacy systems, customizing workflows to match unique institutional protocols, and ensuring seamless data flow across departments. Off-the-shelf solutions rarely fit the highly specialized needs of cancer centers without significant configuration, requiring expert consultants to map out current processes, identify bottlenecks, and redesign workflows to leverage the full capabilities of the new software. The intricacy of oncology workflows, which involve precise timing for chemotherapy administration, radiation fractionation scheduling, and toxicity monitoring, demands a level of specialization that general IT staff typically lack. Furthermore, as systems evolve to include artificial intelligence and precision medicine modules, the need for ongoing strategic advice on how to best utilize these advanced features grows. Hospitals are increasingly recognizing that the software license is only part of the solution, and that expert guidance is essential to transform technology into tangible clinical improvements. This realization is driving a surge in demand for high-value consulting engagements that ensure successful deployment and sustained operational excellence. A further key driver is the acute shortage of qualified health informatics professionals within healthcare organizations who possess the dual expertise in clinical oncology and information technology required to manage and optimize these complex systems independently. The rapid pace of technological advancement in oncology IT outstrips the ability of internal teams to keep up, creating a heavy reliance on external vendors and consultants for training, system maintenance, and continuous improvement initiatives. The scarcity of skilled informaticians forces hospitals to engage consulting firms not just for initial setup but for long-term partnerships to handle system upgrades, user training, and performance tuning. Moreover, providers are shifting towards managed service models where consultants act as an extension of their IT department, providing on-demand expertise and reducing the burden on internal staff. The need for continuous education to keep clinicians proficient with evolving software features further amplifies the demand for training and optimization services. As the market matures, the value proposition of these services shifts from optional support to essential infrastructure, propelling the segment's rapid expansion.

By Application Insights

The Radiation Oncology segment led the global oncology information system market and captured a share of 42.3% in 2025. Moreover, the highly technical, data-intensive, and safety-critical nature of radiation therapy propels this position of the segment. It requires specialized software for treatment planning, dose calculation, machine control, and quality assurance that general oncology systems cannot provide. The main factor driving the domination of radiation oncology systems is the absolute imperative for millimeter-level precision in radiation delivery and rigorous dose verification to prevent catastrophic harm to healthy tissues while maximizing tumor control. Radiation therapy involves complex physics calculations, 3D modeling of patient anatomy, and dynamic beam modulation that must be executed flawlessly, necessitating dedicated information systems that integrate directly with linear accelerators and imaging devices. The complexity of modern techniques like Intensity Modulated Radiation Therapy and Stereotactic Body Radiation Therapy generates terabytes of imaging and planning data per patient, requiring robust databases and high-performance computing integration that only specialized systems can handle. Furthermore, regulatory bodies mandate strict documentation of every fraction delivered, including machine parameters and patient positioning data, which these systems automate effortlessly. The inability to operate high-end radiation equipment without compatible information software creates a locked-in ecosystem where specialized solutions are non-negotiable. This technical dependency and the high stakes of treatment accuracy ensure that radiation oncology remains the largest application segment, commanding significant investment in advanced planning and management platforms. Also strengthening this segment is the deep integration of radiation oncology information systems with advanced imaging modalities such as MRI, CT, and PET scans to enable adaptive radiotherapy workflows where treatment plans are modified in real-time based on daily anatomical changes. Modern radiation therapy is no longer a static process but a dynamic one that requires daily image guidance and plan adaptation to account for tumor shrinkage or organ movement, a capability that relies entirely on sophisticated information systems to manage the data flux. The sheer volume of image data generated daily necessitates high-speed networks and intelligent archiving solutions that are native to radiation oncology platforms. Additionally, the push for hypofractionation, where higher doses are delivered in fewer sessions, increases the complexity and risk of each treatment, further elevating the need for precise planning and verification tools. The requirement for seamless data exchange between imaging, planning, and delivery components creates a closed loop that generic systems cannot replicate. This technological synergy ensures that radiation oncology information systems remain indispensable, driving sustained revenue and market leadership through continuous innovation in imaging integration and adaptive capabilities.

The Medical Oncology segment is anticipated to witness the fastest CAGR of 11.5% over the forecast period, owing to the explosion of targeted therapies and immunotherapies, the shift toward oral oncolytics administered at home, and the increasing complexity of managing systemic treatment regimens. The rapid expansion of the medical oncology segment is largely driven by the paradigm shift from cytotoxic chemotherapy to targeted therapies and immunotherapies, which rely heavily on genomic profiling and biomarker data to determine eligibility and predict response, necessitating information systems capable of handling complex molecular datasets. Unlike traditional chemotherapy, which follows standardized protocols based on body surface area, targeted treatments require matching specific genetic mutations to drugs, creating a massive data management challenge that legacy systems cannot address. Furthermore, the rapid evolution of treatment guidelines for these novel agents requires systems that can update decision support rules in real-time to ensure adherence to the latest evidence. As precision medicine becomes the standard of care, the demand for systems that bridge the gap between the lab bench and the bedside will skyrocket, fueling the segment's accelerated growth. The quick rise in this segment is powered by the dramatic increase in the prescription of oral oncolytics, which shifts the locus of care from the infusion center to the patient's home, creating an urgent need for information systems that support remote monitoring, adherence tracking, and virtual symptom management. Traditional systems designed for chair-side administration lack the tools to track pill counts, monitor patient-reported outcomes via mobile apps, or trigger alerts for adverse events in real-time, creating a dangerous gap in care continuity. Medical oncology information systems are evolving to fill this void by integrating telehealth platforms, wearable device data, and patient portals that allow for continuous engagement. The Centers for Medicare and Medicaid Services has introduced new reimbursement codes for remote therapeutic monitoring, providing a financial incentive for practices to adopt these advanced capabilities. The ability to proactively manage side effects and prevent emergency room visits through remote monitoring not only improves outcomes but also reduces the overall costs of care. This transformation of medical oncology into a hybrid care model is unlocking new value propositions for information system vendors, propelling the segment to the forefront of market growth.

By End Users Insights

The Hospitals and Physician Offices segment held the majority share of the oncology information system market in 2025 because of the fact that the vast majority of cancer diagnosis, treatment planning, and administration occurs within these settings, making them the primary consumers of clinical workflow and data management solutions. A main factor pushing the domination of hospitals and physician offices is the sheer volume of patient encounters and the critical need for coordinated multidisciplinary care that characterizes modern cancer treatment delivery. Cancer care inherently involves a team of surgeons, medical oncologists, radiation oncologists, pathologists, and nurses who must collaborate closely, sharing real-time data to make time-sensitive decisions, a process that is impossible without a unified information system. The complexity of coordinating care across these diverse specialties necessitates robust platforms that facilitate tumor boards, shared care plans, and seamless communication, reducing the risk of fragmentation and errors. Furthermore, the financial pressure on hospitals to optimize throughput and reduce length of stay drives the adoption of systems that streamline scheduling, billing, and resource allocation. The concentration of high-acuity cases in hospital settings ensures that they remain the largest purchasers of comprehensive oncology IT solutions, as the cost of inefficiency or error in this environment is prohibitively high. This operational necessity secures the segment's dominant position as the core engine of market demand. This segment is further shaped by the dependence of hospitals and large physician groups on oncology information systems to maintain accreditation status and secure favorable reimbursement rates from payers and government programs. Accreditation bodies like the Commission on Cancer mandate the use of certified software for data abstraction and quality reporting, making these systems a prerequisite for operation. As per regulations from the Centers for Medicare and Medicaid Services, participation in value-based payment models such as the Oncology Care Model requires detailed reporting on cost, quality, and patient experience metrics that can only be reliably extracted from advanced information systems. The ability to demonstrate compliance with meaningful use criteria and interoperability standards is also tied to financial incentives, further compelling adoption. Additionally, the legal liability associated with cancer care drives hospitals to invest in systems with robust audit trails and decision support features to mitigate malpractice risks. The convergence of regulatory mandates, financial incentives, and risk management needs creates an inelastic demand for oncology information systems among hospitals and physician offices, ensuring their continued dominance as the primary end-user segment in the global market.

The Research Centres segment is likely to experience the fastest CAGR of 13.2% between 2026 and 2034. This growth is fueled by the accelerating pace of translational research, the rise of precision medicine trials, and the increasing need to aggregate real-world evidence for drug development. The segment’s rise is largely caused by the exponential increase in precision medicine clinical trials that require sophisticated data management systems to handle complex genomic datasets, patient stratification criteria, and longitudinal outcome tracking. Unlike traditional trials, modern oncology studies often involve multiple cohorts based on specific genetic mutations, requiring flexible and powerful information systems to manage eligibility screening, sample tracking, and data analysis efficiently. Furthermore, the push for master protocol trials like basket and umbrella studies, which test multiple drugs against multiple mutations simultaneously, adds layers of complexity that legacy systems cannot support. As the focus of oncology research shifts toward rare mutations and personalized combinations, the need for agile, data-rich information systems becomes paramount. Research centres are investing heavily in these platforms to remain competitive in securing grants and industry partnerships, propelling the segment's rapid expansion. This segment is also gaining from the growing reliance on real-world evidence generated from routine clinical practice to support regulatory approvals, label expansions, and health technology assessments, prompting research centres to deploy systems capable of aggregating and harmonizing data from diverse sources. Regulatory agencies like the Food and Drug Administration and the European Medicines Agency are increasingly accepting real-world data as supplementary evidence for drug efficacy and safety, transforming clinical data repositories into valuable assets for drug development. The ability to pool data across multiple institutions through federated learning networks allows for larger sample sizes and more robust statistical power, enhancing the validity of findings. Furthermore, patient advocacy groups are demanding faster access to experimental therapies, pressuring research centres to streamline trial operations through better data management. The convergence of regulatory acceptance, industry investment, and patient advocacy is creating a fertile environment for the adoption of advanced research information systems, driving the segment's status as the fastest-growing end-user market.

REGIONAL ANALYSIS

North America Oncology Information System Market Analysis

North America was the top performer in the global oncology information system market and occupied a 44.4% share in 2025. The demand for these systems in North America is supported by its advanced healthcare infrastructure, high adoption rates of electronic health records, substantial funding for cancer research, and a regulatory environment that strongly incentivizes digitization and data interoperability. In addition, the United States is leading the market in growth, driven by a confluence of factors including the widespread implementation of value-based care models, the presence of major health IT vendors, and a high prevalence of cancer that necessitates efficient care management. The Centers for Medicare and Medicaid Services continues to refine payment models like the Enhancing Oncology Model, which rewards providers for using data analytics to improve outcomes and reduce costs, directly stimulating demand for advanced information systems. Furthermore, the National Cancer Institute designates numerous comprehensive cancer centers that serve as early adopters of cutting-edge technologies, setting trends for the rest of the market. The strong presence of venture capital and private equity in the US health tech sector also fuels innovation and rapid commercialization of new solutions. Despite challenges related to data privacy and interoperability, the relentless drive for quality improvement and operational efficiency ensures that North America remains the largest and most sophisticated market for oncology information systems globally.

Europe Oncology Information System Market Analysis

Europe was the second-largest region in the global oncology information system market and captured a 26.5% share in 2025 because of a fragmented but harmonizing landscape driven by cross-border health initiatives, strong public healthcare systems, and increasing focus on cancer registry standardization. The region offers a unique dynamic where national policies dictate adoption rates, yet EU-wide directives are fostering greater cohesion and data sharing. The European market is distinguished by the influence of the European Code Against Cancer and the EU Mission on Cancer, which prioritize the creation of a unified European Health Data Space to facilitate research and improve care across member states. Countries like Germany, France, and the United Kingdom are leading the adoption, supported by well-funded national health services that are modernizing their digital infrastructure to handle the aging population's growing cancer burden. The General Data Protection Regulation imposes strict requirements on data handling, pushing vendors to develop highly secure and compliant solutions tailored to the European context. Furthermore, the rise of personalized medicine initiatives in countries like the Netherlands and Sweden is spurring demand for systems capable of handling genomic data. While fragmentation remains a challenge, the overarching push for digital sovereignty and collaborative research is creating a robust growth trajectory, making Europe a critical hub for innovation and adoption in the oncology IT sector.

Asia-Pacific Oncology Information System Market Analysis

The Asia-Pacific region is the fastest-growing market for oncology information systems due to the massive populations of China, India, and Japan, rapid economic development, and government-led initiatives to modernize healthcare infrastructure and combat rising cancer rates. The region is witnessing an explosive uptake of health IT solutions driven by necessity and strategic investment. This follows a history of lagging in digitization. China and India are spearheading this transformation, driven by government mandates to improve cancer care accessibility and quality in the face of soaring incidence rates. In India, the Ayushman Bharat Digital Mission aims to create unique health IDs and electronic health records for millions, creating a fertile ground for oncology module adoption. Japan, with its super-aged society and high cancer prevalence, drives demand for advanced systems to manage complex geriatric oncology cases and integrate with its universal health insurance system. The rising middle class is demanding higher standards of care, pushing private hospitals to adopt international best practices and technologies. Furthermore, collaborations with Western research institutions are accelerating the transfer of knowledge and technology. Challenges related to infrastructure gaps and varying regulatory frameworks persist in the Asia-Pacific region. However, the sheer scale of the unmet need and strong political commitment to digital health position it as the primary growth engine for the future of the oncology information system market.

Latin America Oncology Information System Market Analysis

Latin America occupies a noteworthy position in the global market by expanding private healthcare sectors, and government efforts to strengthen public health systems are beginning to unlock demand for oncology information systems. It is primarily driven by Brazil and Mexico, where growing cancer burdens. The region benefits from increasing awareness but faces hurdles related to economic volatility and uneven infrastructure distribution. Brazil is the dominant force in the region, boasting the largest healthcare market in Latin America and a proactive public health system (SUS) that is gradually digitizing its oncology care pathways to improve efficiency and transparency. In Mexico, the proximity to the United States facilitates the flow of medical technologies and best practices, with private hospitals increasingly adopting US-standard oncology IT solutions to attract medical tourism and serve affluent patients. However, budget constraints and bureaucratic hurdles often slow down large-scale public sector implementations. Despite these challenges, the growing presence of multinational pharmaceutical companies and contract research organizations is stimulating demand for clinical trial management systems in the region. The increasing penetration of internet connectivity and mobile health technologies is also enabling innovative solutions for remote areas. As economic stability improves and healthcare reforms take hold, Latin America is poised to see accelerated adoption of oncology information systems, particularly in the private sector and major urban centers.

Middle East and Africa Oncology Information System Market Analysis

The Middle East and Africa region is predicted to grow significantly in the global oncology information system market during the forecast period by displaying pockets of high potential in Gulf Cooperation Council countries and South Africa. This growth is driven by strategic investments in healthcare modernization, despite being constrained by infrastructure deficits and varying economic development. The region represents a long-term frontier where gradual improvements in digital literacy and infrastructure could unleash substantial demand. South Africa and the Gulf states serve as the anchors of advancement in the region, with nations like Saudi Arabia and the UAE implementing ambitious vision plans that include massive investments in smart healthcare and cancer control strategies. In South Africa, the private healthcare sector maintains high standards and utilizes advanced information systems, while the public sector struggles with resource limitations but is benefiting from international aid focused on cancer registry development. However, the broader African continent faces significant challenges, with the World Health Organization estimating that many countries lack basic cancer registration capabilities, let alone advanced information systems. Efforts by organizations like the African Organization for Research and Training in Cancer are slowly building capacity and promoting the adoption of low-cost, cloud-based solutions. The Middle East and Africa are expected to transition from a marginal player to a meaningful contributor to the global market, driven by top-down government mandates and the urgent need to address rising cancer mortality rates. This transition is being enabled by improvements in political stability and increased foreign direct investment, particularly in the Gulf.

COMPETITIVE LANDSCAPE

The competition in the oncology information system market is characterized by intense rivalry among specialized medical device giants and dedicated health IT vendors striving to offer the most comprehensive and interoperable solutions. Major players compete fiercely on the depth of clinical functionality, particularly in radiation oncology, where integration with treatment delivery hardware creates high switching costs and strong vendor lock-in. The landscape is shifting as companies increasingly differentiate themselves through advanced artificial intelligence capabilities that promise to automate routine tasks and provide predictive insights for personalized medicine. Rivalry often manifests through strategic partnerships with electronic health record providers to ensure seamless data flow and avoid silos that hinder care coordination. Smaller niche firms challenge incumbents by offering agile cloud-native platforms tailored specifically for community practices that find enterprise solutions too complex or costly. Pricing pressure is moderate due to the critical nature of these systems, but value-based contracting is becoming more common as providers seek proof of improved outcomes. Regulatory compliance and data security remain paramount battlegrounds as vendors must navigate complex global privacy laws. Ultimately, the competitive dynamic is driven by the ability to deliver integrated ecosystems that enhance clinical efficiency and support the transition to precision oncology.

KEY MARKET PARTICIPANTS

Notable companies dominating the global oncology information system market profiled in this report are

- Accuray Incorporated (U.S.)

- Altos Solutions, Inc. (U.S.)

- Cerner Corporation (U.S.)

- Elekta AB (Sweden)

- Epic Systems Corporation (U.S.)

- Koninklijke Philips N.V. (The Netherlands)

- McKesson Corporation (U.S.)

- Varian Medical Systems, Inc. (U.S.)

TOP PLAYERS IN THE MARKET

- Varian Medical Systems stands as a global pioneer in oncology information systems, renowned for its ARIA oncology information platform, which integrates radiation therapy, medical oncology, and proton therapy workflows. The company plays a pivotal role in digitizing cancer care by connecting treatment planning systems with delivery machines to ensure precision and safety. Recent actions include the full integration of Varian into Siemens Healthineers, creating a comprehensive portfolio that spans imaging, diagnostics, and therapy. This strategic move allows Varian to offer end-to-end solutions that streamline data flow from diagnosis to treatment. The firm continues to invest heavily in artificial intelligence capabilities within its software to automate contouring and optimize treatment plans. By leveraging the vast resources of Siemens, Varian is expanding its global reach and enhancing interoperability with electronic health records. These initiatives solidify its position as a leader dedicated to improving clinical outcomes through advanced digital innovation and seamless workflow integration for cancer centers worldwide.

- Elekta AB is a leading provider of precise radiation therapy solutions and oncology informatics, offering the MOSAIQ oncology information system, which is widely used globally to manage complex radiotherapy and chemotherapy processes. The company focuses on empowering clinicians with data-driven insights to personalize treatment and improve patient safety across diverse healthcare settings. Recent actions involve strategic partnerships with major technology firms to integrate cloud-based analytics and machine learning tools into its informatics platform. Elekta has also launched initiatives to enhance interoperability, ensuring its systems communicate effectively with third-party electronic health records and imaging archives. The firm is actively expanding its presence in emerging markets by tailoring solutions to local infrastructure needs while maintaining high global standards. By prioritizing user-centric design and continuous software updates, Elekta ensures its platforms adapt to evolving clinical guidelines. These efforts demonstrate its commitment to transforming cancer care through connected ecosystems that facilitate collaboration among multidisciplinary teams and support value-based healthcare models globally.

- McKesson Corporation operates as a critical backbone in the oncology information landscape through its iKnowMed system, a specialized electronic health record designed specifically for community oncology practices. The company leverages its extensive distribution network and data analytics expertise to provide practices with tools for clinical decision support, practice management, and quality reporting. Recent actions include enhancing the artificial intelligence features within iKnowMed to predict patient risks and optimize resource allocation. McKesson has also strengthened its data aggregation capabilities to support real-world evidence generation for pharmaceutical partners and researchers. The firm actively assists practices in navigating complex regulatory requirements and value-based care contracts through robust reporting modules. By integrating financial and clinical data, McKesson helps independent practices remain viable amidst industry consolidation. Its focus on delivering actionable insights and operational efficiency allows community providers to offer high-quality care comparable to large academic centers. This dedication to supporting the unique needs of outpatient oncology solidifies McKesson's role as an essential partner in the global cancer care ecosystem.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the oncology information system market primarily employ strategic acquisitions and mergers to expand their product portfolios and integrate complementary technologies such as artificial intelligence and genomic data analytics. Companies frequently invest heavily in research and development to enhance interoperability standards, ensuring seamless data exchange between oncology platforms and broader electronic health record systems. Another major strategy involves forming strategic alliances with pharmaceutical companies and research institutions to leverage real-world data for drug development and clinical trial recruitment. Market participants are also focusing on transitioning to cloud-based deployment models to offer scalable solutions that reduce upfront costs for smaller practices. Building comprehensive training and support ecosystems helps firms drive user adoption and minimize workflow disruptions during implementation. Additionally, companies are expanding their global footprint by entering emerging markets where healthcare digitization is accelerating rapidly. These strategies collectively enable leaders to drive innovation and capture significant market opportunities.

MARKET SEGMENTATION

This market research report on the global oncology information system market has been segmented and sub-segmented based on the products and services, application, end-users, and region.

By Products and Services

- Patient Information Systems

- Treatment Planning Systems

- Consulting/Optimization Services

- Implementation Services

- Post-Sale and Maintenance Services

By Application

- Surgical Oncology

- Medical Oncology

- Radiation Oncology

By End Users

- Hospitals & Physician’s Offices

- Research Centres

- Government Institutions

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. How do oncology information systems improve cancer treatment?

Oncology information systems streamline patient data management, support personalized treatment planning, and enhance clinical decision-making in the global oncology information system market

2. Which regions lead the global oncology information system market?

North America leads the global oncology information system market, with Asia Pacific emerging as the fastest-growing region due to healthcare infrastructure expansion

3. What are the key drivers for growth in the global oncology information system market?

Drivers include rising cancer prevalence, demand for real-time clinical data, government initiatives, and advancements in AI and cloud-based oncology platforms

4. How do technology advancements impact the global oncology information system market?

AI integration, cloud deployment, and mobile accessibility boost efficiency and interoperability in the global oncology information system market

5. What are common applications of oncology information systems?

They are used for treatment planning, electronic health records integration, clinical trial management, and patient outcome tracking in the global oncology information system market

6. How important is data interoperability in the global oncology information system market?

Interoperability ensures seamless data exchange between oncology systems and other healthcare IT, a critical factor in the global oncology information system market

7. What challenges does the global oncology information system market face?

Challenges include high implementation costs, data security concerns, regulatory compliance, and integration complexities in the global oncology information system market

8. How do oncology information systems support precision medicine?

They enable detailed patient data analysis and treatment customization, advancing precision medicine in the global oncology information system market

9. What role do government initiatives play in the global oncology information system market?

Governments promote adoption through funding, digital health policies, and cancer registries, bolstering the global oncology information system market

10. How do oncology information systems enhance patient outcomes?

By supporting accurate treatment plans, monitoring progress, and facilitating multidisciplinary care, oncology information systems improve outcomes in the global oncology information system market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com