Global Pest Control Market Size, Share, Trends, COVID-19 Impact & Growth Forecast Report, Segmented By Type (Chemical Control, Mechanical Control and Biological Control), Availability (Commercial, Industrial, Residential and Agricultural), Pest Type (Insects, Termites, Rodents and Wildlife) and By Region (North America, Europe, Asia Pacific, Latin America, Middle East And Africa), Industry Analysis From 2026 to 2034

Market Size, 2025

$20.94 BnMarket Estimate, 2026

$22.05 BnMarket Forecast, 2034

$33.33 BnCAGR, 2026–2034

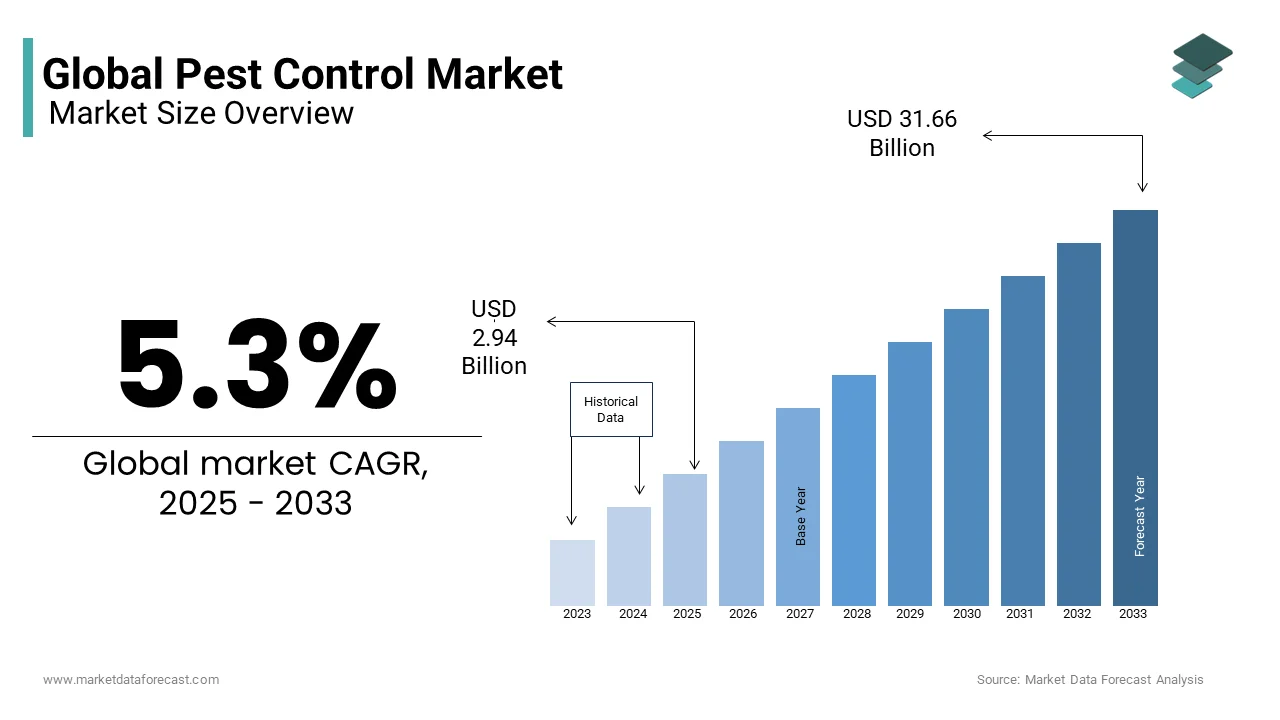

5.3%Global Pest Control Market Size

The global pest control market was valued at USD 20.94 billion in 2025 and is anticipated to reach USD 22.05 billion in 2026 from USD 33.33 billion by 2034, growing at a CAGR of 5.3% during the forecast period from 2026 to 2034.

Current Introduction of The Global Pest Control Market

Pest control is the systematic management and regulation of species defined as pests, such as insects, rodents, weeds, or fungi, that are detrimental to human health, property, or the environment. These include insects, rodents, birds, and other nuisance wildlife capable of transmitting diseases, contaminating food, or causing material degradation. The market serves residential, commercial, industrial, and agricultural sectors through a blend of preventive, reactive, and consultative models.

In Europe, the demand is increasingly shaped by stringent food safety mandates, urban densification, and climate-influenced pest behavior. According to research, the European Commission’s food and feed safety notification system continues to record a high volume of alerts regarding contaminated products, with pesticide residues and pathogens driving a significant portion of food safety interventions. According to the World Health Organization, diseases transmitted by pests, including mosquitoes and ticks, continue to cause a high, growing, and significant number of deaths worldwide, with outbreaks reaching historic highs. Additionally, the increasing concentration of Europe's population in urban centers expands built environments, creating prime, dense habitats that escalate pest proliferation risks. This confluence of demographic, regulatory, and ecological forces defines the current operational landscape of the pest control industry.

MARKET DRIVERS

Rising Incidence of Vector-Borne Diseases Amplifies Public Health Demand

The global surge in vector-borne illnesses continues to act as a key enabler for institutional and municipal pest control investments that boost the growth of the global pest control market. Pathogens transmitted by mosquitoes, ticks, and rodents, including dengue, Lyme disease, and West Nile virus, pose escalating public health burdens. Vector-borne diseases represent a significant fraction of infectious illnesses globally and are linked to a substantial number of worldwide fatalities. Reports from European areas indicate an increase in confirmed cases of infections transmitted by ticks. Trends suggest a gradual rise in the occurrence of specific tick-borne diseases in particular European regions over recent periods of observation. Climate anomalies have extended seasonal activity and enabled vectors to colonize regions like northern Germany and southern Sweden, previously considered low-risk. In response, national health agencies are commissioning large-scale vector abatement programs. This epidemiological pressure not only strengthens governmental procurement but also heightens household awareness, driving demand for professional interventions and embedding pest control within broader public health infrastructure.

Expansion of Global Food Supply Chains Elevates Hygiene Compliance Requirements

The complexity and scale of international food networks have intensified hygiene enforcement across all nodes of the supply chain, from farms to retail outlets, which further accelerates the expansion of the global pest control market. Regulatory regimes such as the European Union’s General Food Law enforce zero-tolerance policies toward pest presence in food-handling facilities. European Union border officials regularly reject large volumes of imported agri-food shipments due to significant hazards, including pest infestation and failure to meet strict phytosanitary documentation standards, primarily affecting fruits, vegetables, and spices. Certification schemes like the British Retail Consortium’s Global Standards mandate rigorous pest monitoring, where even minor evidence can trigger audit failures and facility shutdowns. Food contamination incidents, driven by issues like microbial growth or pest presence, pose major financial risks to companies, causing severe losses through product recalls, potential legal action, and damage to brand reputation. Consequently, food manufacturers are institutionalizing integrated pest management (IPM) as a core component of food safety. Major global food manufacturers, such as Nestlé, are increasingly implementing stringent, certified pest management and quality safety programs across their European manufacturing sites to meet international food safety standards. This systemic integration ensures consistent demand while accelerating innovation in non-intrusive monitoring and digital compliance tools.

MARKET RESTRAINTS

Stringent Regulatory Restrictions on Conventional Pesticides Limit Product Availability

Regulatory scrutiny over chemical pesticides, driven by environmental and toxicological concerns, has significantly curtailed the arsenal available to pest control professionals, especially in Europe, which hampers the growth of the global pest control market. Regulatory requirements in Europe have led to the removal of many active substances from commercial availability. A substantial quantity of pesticide active ingredients, including some widely utilized, have been discontinued or gradually phased out. Policy approaches within the European Union are designed to reduce the total amount of chemical pesticides used in farming. These measures disproportionately affect broad-spectrum insecticides that offer rapid, cost-effective results. Alternatives such as biopesticides often carry a cost premium. Moreover, the registration process for new active substances can require substantial amount in testing and documentation costs. This regulatory barrier restricts product diversity, increases service complexity, and elevates operational costs, particularly for small- and medium-sized enterprises lacking R&D capacity.

Public Resistance to Chemical Treatments Undermines Service Adoption

Consumer aversion to synthetic chemical applications, especially in residential, educational, and healthcare settings, has emerged as a significant barrier to traditional pest control service models, and thereby hinders the expansion of the global pest control market. Heightened awareness of endocrine disruption, chemical residues, and ecological spillover effects has shifted preference toward “green” or non-chemical solutions. European citizens increasingly express substantial worry regarding exposure to pesticides in their surroundings and generally support environmentally sound pest management approaches. This sentiment directly impacts service delivery. In certain European regions, a notable portion of residential pest control service cancellations is attributed to consumer reluctance towards traditional spray-based application methods. Alternatives such as baiting, ultrasound, and heat treatment are popular but often entail extended treatment times and higher expenses. Furthermore, research indicates that non-chemical bed bug treatments often show lower initial success rates compared to integrated protocols that include chemical components. Balancing client expectations with functional reliability remains a persistent operational challenge.

MARKET OPPORTUNITIES

Integration of Digital Monitoring Technologies Creates New Service Models

The advent of connected devices and data analytics is redefining pest control from a reactive service to a predictive intelligence platform, which creates new opportunities for the global pest control market growth. Smart traps equipped with image recognition, motion sensors, and cloud connectivity now enable real-time pest surveillance and automated alerting. The global deployment of connected pest monitoring units is experiencing significant growth, driven by increasing adoption of IoT and AI technologies and demand for more environmentally conscious solutions. In Europe, major corporations like Unilever and IKEA have adopted digital pest management ecosystems that integrate trap data with facility management software to trigger preemptive interventions and generate audit-ready compliance reports. Companies that use advanced digital pest management systems often observe a meaningful reduction in the recurrence of pest issues compared to traditional, less frequent inspection methods. Regulatory bodies are also adapting. Strict government food safety and hygiene regulations are increasingly promoting the use of modern, data-driven pest monitoring and reporting systems to ensure compliance with quality control standards. Lowering hardware costs and mature AI analytics enable these platforms to provide scalable, transparent, and value-adding services that match sustainability and digital transformation goals.

The rapid institutionalization of urban farming across European cities has opened a potential niche for specialized, low-impact pest management, which is anticipated to drive the expansion of the global pest control market. Rooftop farms, vertical hydroponic units, and community gardens operate under strict organic principles and proximity constraints that prohibit conventional chemical use. European cities are increasingly expanding urban farming initiatives, with growing investment in local food production, community gardens, and vertical farming to enhance food security and sustainability, supported by EU-level research and planning initiatives. These operations are highly vulnerable to aphids, spider mites, and whiteflies, which can decimate yields within days. Traditional sprays are incompatible with pollinator conservation and residential adjacency, necessitating precision biocontrol methods such as pheromone disruption, predatory insect release, and UV-light traps. In line with EU environmental goals, there is a rising adoption of biological control products and natural pest management strategies across urban agricultural systems, aiming to reduce dependence on synthetic pesticides. Companies like Koppert and Biobest have responded with compact, user-friendly biocontrol kits tailored for small-scale urban growers. Municipal subsidies further accelerate adoption. This segment not only diversifies revenue streams but positions pest control providers as enablers of resilient, circular urban food systems.

MARKET CHALLENGES

Labor Shortages and Skill Gaps Impede Service Scalability

A critical workforce deficit, driven by aging demographics and insufficient vocational pipelines, is constraining the growth of the global pest control market. The European pest control industry is facing a significant workforce crisis, with a rapidly aging workforce in key nations like Germany and France, and a high rate of retirement outpacing the arrival of new professionals. This gap is compounded by rising technical demands: modern pest management now requires proficiency in digital diagnostics, regulatory documentation, and biological agent handling. Many pest management firms across Europe are experiencing significant operational challenges due to difficulties in hiring new staff, with open positions remaining unfilled for extended periods. The availability of standardized, nationally recognized training for pest control professionals is limited to only a few countries within the European Union. The shortage of qualified personnel appears to be impacting service availability, which is being linked to an increase in pest-related hygiene issues in regulated environments. Service scalability in regulated sectors will remain restricted unless we align our investments in apprenticeships, curriculum development, and workforce branding.

Climate-Driven Pest Range Expansion Complicates Treatment Protocols

Climate change is accelerating the northward and altitudinal spread of invasive pest species, disrupting established control paradigms, which slows down the expansion of the global pest control market. Rising temperatures, reduced frost days, and erratic rainfall have enabled organisms like the Asian hornet and brown marmorated stink bug to establish self-sustaining populations across northern Europe. According to the European Environment Agency and related EU scientific bodies, the number of established invasive alien species in the EU has continued to rise, with a significant number of new species establishing themselves annually, representing a persistent threat to biodiversity. These newcomers often exhibit novel behaviors, resistance profiles, and ecological interactions that render traditional baiting, spraying, or trapping ineffective. For example, studies on insecticide resistance suggest that standard gel baits formulated for German cockroaches may show diminished effectiveness against other cockroach species, such as oriental cockroaches, indicating a need for targeted management. Regulatory approvals for new control agents lag significantly behind invasion timelines, leaving practitioners with limited legal options. The European Commission is implementing stricter regulations, including a, move toward Integrated Pest Management, which is projected to increase operational costs for farmers and professional users as they adopt more sustainable alternative methods by 2030. Sustained efficacy now demands dynamic surveillance, cross-border data sharing, and rapid-response research frameworks, an operational paradigm still in its infancy.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.3% |

| Segments Covered | By Type of Pest Control, Availability, Type of Pest, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Rollins Inc., Rentokil Initial plc, Ecolab Inc., Terminix Global Holdings, Inc., Anticimex Group, Arrow Exterminators, Massey Services, BASF SE, Syngenta, Bayer AG, Bird-X, Pelsis Group, Bird B Gone, Rentokil Steritech, Wil-Kil Pest Control, Dodson Pest Control, The Home Depot (Orkin), Western Exterminator Company, Truly Nolen of America. |

SEGMENTAL ANALYSIS

By Type Insights

The chemical control segment led the global pest control market by occupying a 58.2% share in 2025 because of its immediate efficacy, broad-spectrum action, and cost efficiency, particularly in large-scale agricultural and industrial applications. Chemical pesticides deliver rapid knockdown of pest populations which is critical in time sensitive scenarios such as post harvest storage or disease outbreak containment. In emerging economies such as India and Brazil where smallholder farming constitutes a significant portion of food production chemical solutions remain the default due to affordability and accessibility. Additionally chemical formulations are often integrated into seed treatments and irrigation systems enabling seamless deployment. Despite ongoing environmental concerns, the advancement of microencapsulated and slow-release chemistries has reduced off-target impacts, sustaining institutional reliance on this modality.

The biological control segment is predicted to witness the highest CAGR of 11.3% from 2026 to 2034 due to intensifying regulatory bans on synthetic pesticides rising consumer demand for residue free food and advancements in biopesticide formulation stability. Policy initiatives aimed at reducing chemical pesticide use appear to be stimulating greater public and private investment in alternative pest control methods. The worldwide market for biological control products is expanding, with one region accounting for a considerable share. Improvements in application techniques and the creation of microbial insecticides are enhancing the efficiency and scalability of biological options. Regulatory agencies are showing quicker approval processes for new biopesticide active ingredients. Major food retailers are encouraging the adoption of biological pest management among their produce providers. These converging policy commercial and technological forces are transforming biological control from a niche supplement into a mainstream pest mitigation pillar.

By Availability Insights

The agricultural segment was the largest segment in the global pest control market by capturing a 42.1% share in 2025. The leading position of the agricultural segment is driven by the non negotiable need to safeguard global food production against pre and post harvest losses. Plant pests and diseases cause significant annual reductions in global crop yields, leading to substantial economic consequences. In Asia and Latin America where rice maize and soy dominate agricultural output pest pressure from stem borers fall armyworms and locusts necessitates frequent interventions. ndia utilizes a notable quantity of the world's pesticides across its extensive agricultural land. Furthermore, global export standards enforced by bodies like the Codex Alimentarius compel producers to maintain pest free certification triggering routine professional services. The rise of contract farming and agri tech platforms has also formalized pest management as a bundled service enhancing adoption. Unlike residential or commercial segments where pest issues are episodic agriculture demands year round surveillance and intervention thereby anchoring consistent high volume demand.

The residential segment is estimated to register the fastest CAGR of 9.7% over the forecast period owing to rising urban infestations, heightened health awareness, and digital service accessibility. Urbanization has intensified human pest cohabitation. A majority of the global population is currently living in urban areas, with this proportion projected to increase in the coming years. Municipalities in European regions have noted a rise in rodent sightings, particularly in large city centers. These increases in urban rodent presence are often associated with challenges in maintaining older infrastructure. Issues related to waste management have also been identified as contributing factors to the heightened rodent activity. Simultaneously consumer behavior has shifted toward on demand service models with mobile apps enabling instant booking and transparent pricing. Companies reported year on year growth in residential digital bookings. Furthermore the post pandemic focus on indoor hygiene has elevated pest control from a reactive fix to a preventive wellness measure. This behavioral shift supported by subscription based pricing and eco friendly service options is driving sustained residential market expansion.

By Pest Insights

The insects segment dominated the global pest control market by holding a 65.1% share in 2025. The prominence of the insects segment is credited to its vast species diversity rapid reproductive cycles and role as vectors for human and animal diseases. Mosquitoes alone transmit pathogens causing malaria dengue and Zika affecting hundreds of millions annually. In agriculture insect pests such as aphids whiteflies and beetles inflict continuous damage across fruit vegetable and cereal crops. Urban environments also face persistent challenges from cockroaches ants and bed bugs which compromise hygiene and trigger allergic responses. The United States Environmental Protection Agency identifies indoor cockroach allergens as a leading cause of asthma in children particularly in low income housing. Given the omnipresence of insects across ecological residential and agricultural domains and their direct linkage to health and economic outcomes this segment maintains structural dominance in service volume and revenue.

The rodent control segment is estimated to register the fastest CAGR of 10.1% from 2026 to 2034. The swift expansion of this segment is fuelled by escalating urban rodent populations food safety enforcement and zoonotic disease risks. Rodents are recognized as a major factor in the degradation and contamination of global food supplies. These pests are known carriers of numerous diseases that pose risks to human health. Urban areas across Europe, including major cities, have reported significant increases in rodent activity. Municipal records in specific European locations have shown a notable rise in citizen complaints regarding rat sightings. The upward trend in rodent reports suggests a growing management challenge for city authorities. The European Food Safety Authority mandates zero tolerance for rodent evidence in food processing facilities with non-compliance resulting in immediate shutdowns. Consequently, food retailers and logistics firms are investing in integrated rodent monitoring including tamper proof bait stations and AI powered trap alerts. Climate induced habitat displacement and aging urban sewer systems further exacerbate infestations creating persistent demand for professional rodent abatement services.

REGIONAL ANALYSIS

North America Market Analysis

North America outperformed other regions in the global pest control market by accounting for a 29.1% share in 2025. The supremacy of the North American market is supported by highly regulated food safety protocols advanced service infrastructure and robust residential demand. A significant portion of regional revenue is generated within the United States due to regulatory requirements necessitating third-party pest audits for food handling establishments. A high percentage of food manufacturers in the United States engage certified pest control providers for their facilities annually. Residential demand for pest control services remains elevated, with a notable portion of homeowners reporting encounters with pests. Technological adoption is another differentiator US firms lead in deploying thermal imaging drone surveillance and automated reporting platforms. Additionally, the rise of bed bug infestations in multi unit housing has spurred specialized treatment services generating substantial amount of annual revenue. This blend of regulatory rigor consumer awareness and service innovation sustains North America’s market leadership.

Europe Market Analysis

Europe was the next prominent region in the global pest control market by capturing a share of 25.7% in 2025. The growth of the European market is driven by its emphasis on integrated pest management sustainability mandates and public health driven vector control. Stringent regional chemical frameworks are encouraging a transition away from traditional synthetic substances. Regulatory pressure is increasingly favoring the adoption of biological and mechanical solutions for crop protection. Heightened focus on food safety serves as a primary motivator for shifts in agricultural practices. Monitoring systems continue to track and report incidents related to pests and safety standards to maintain market integrity. Urban centers face mounting rodent and insect pressures with cities like Paris and Amsterdam investing millions in smart waste systems and public baiting programs. Germany leads regional revenue accounting for a portion of Europe’s market due to its dense industrial and food processing base. Additionally, the EU’s Green Deal and Farm to Fork Strategy are institutionalizing non chemical pest control in public procurement creating long term structural demand for eco compliant services.

Asia Pacific Market Analysis

Asia Pacific maintains a significant share of the global pest control market due to agricultural intensity rapid urbanization and rising middle class awareness. The market for pest control in Asia is heavily driven by demand in China and India. China's pest control sector is experiencing notable annual growth, reflecting increased demand for services. In India, a substantial portion of the labor force is involved in agriculture, where pests cause significant losses to major food crops. Rapid urban expansion across Asia is significantly increasing the need for pest control services in both residential and commercial spaces. Countries like Thailand and Vietnam are also emerging as hubs for food exports requiring strict pest compliance to access Western markets. Furthermore, dengue and chikungunya outbreaks in Southeast Asia have prompted government funded mosquito abatement campaigns. This dual pressure from food security and public health ensures Asia Pacific’s rapid market ascent.

Latin America Market Analysis

Latin America grew steadily in the global pest control market, with Brazil and Mexico as primary growth engines. The region’s dominance in tropical agriculture particularly soybeans coffee and sugarcane creates relentless pest pressure requiring continuous intervention. Agricultural production in Brazil is characterized by a high volume of pesticide application. The fall armyworm represents a significant economic challenge to maize cultivation in Latin America, resulting in substantial crop losses. Urban residential pest control services are experiencing increased demand in certain metropolitan areas, driven by density and health concerns. Regulatory modernization is another catalyst Colombia and Chile have recently updated their pest control licensing frameworks to align with WHO standards enhancing service professionalism. Additionally, the rise of contract farming and supermarket supply chains has institutionalized pest audits for small producers. These agricultural imperatives coupled with urban health concerns position Latin America as a high growth resilient market.

Middle East and Africa Market Analysis

The Middle East and Africa region is likely to expand in the global pest control market from 2026 to 2034 owing to stark contrasts between Gulf state sophistication and Sub Saharan public health urgency. In the Gulf Cooperation Council countries particularly Saudi Arabia and the United Arab Emirates stringent food import laws and luxury hospitality standards drive premium service adoption. Regulatory bodies in certain regions are increasing oversight of food service establishments by implementing mandatory, documented pest management protocols. In various regions, including sub-Saharan Africa, there is a continued, significant challenge regarding the health impact of diseases transmitted by insects. Public health monitoring in specific African regions indicates a high mortality rate associated with malaria. Pest management approaches differ significantly between areas focused on food safety inspections and those combating endemic vector-borne diseases. Countries like Nigeria and Kenya are scaling up indoor residual spraying and larvicide programs often funded by international agencies such as the Global Fund. Agricultural losses are equally severe the International Institute of Tropical Agriculture estimates that stored grain pests destroy a notable share of post harvest cereals in West Africa. Urbanization is adding pressure Lagos and Nairobi are experiencing rodent infestations linked to informal settlement growth. Though fragmented the region’s market is expanding annually driven by health imperatives and regulatory catch up

COMPETITIVE LANDSCAPE

The Pest Control Market features a highly fragmented competitive landscape characterized by the coexistence of global enterprises regional specialists and local operators. While multinational firms leverage technology scale and brand recognition to serve large commercial and industrial clients local providers often dominate residential segments through personalized service and community presence. Competition is intensifying due to rising client expectations for eco friendly solutions digital transparency and regulatory compliance. Key differentiators include speed of response treatment efficacy service integration and sustainability credentials. The market also witnesses frequent consolidation as larger players acquire regional firms to access new territories and specialized expertise. Simultaneously technological innovation particularly in smart monitoring and biological control is lowering entry barriers for agile start ups. Despite fragmentation the trend toward professionalization standardization and digitalization is steadily raising the competitive threshold requiring continuous investment in both human capital and technological infrastructure to maintain relevance and reliability.

KEY MARKET PLAYERS

Some major players are involved in the global pest control market.

- Rollins Inc.

- Rentokil Initial plc

- Ecolab Inc.

- Terminix Global Holdings, Inc.

- Anticimex Group

- Arrow Exterminators

- Massey Services

- BASF SE

- Syngenta

- Bayer AG

- Bird-X

- Pelsis Group

- Bird B Gone

- Rentokil Steritech

- Wil-Kil Pest Control

- Dodson Pest Control

- The Home Depot (Orkin)

- Western Exterminator Company

- Truly Nolen of America

Top Players In The Market

- Rentokil Initial operates as a global leader in pest control with a presence spanning numerous countries. The company delivers integrated pest management solutions across commercial food processing healthcare and residential sectors. In recent years Rentokil Initial has prioritized digital transformation launching its PestConnect platform which uses connected sensors and real time data analytics to enable predictive pest control. The company has also expanded its sustainability initiatives aligning services with global environmental standards and enhancing client compliance reporting. Through strategic acquisitions such as the purchase of Western Exterminator Company in the United States Rentokil Initial continues to consolidate its footprint and deepen service capabilities in high growth markets.

- Terminix Global Holdings provides comprehensive pest control services with a strong emphasis on residential and commercial segments primarily in North America. The company is known for its science based treatment protocols and customer centric service model. Recently Terminix strengthened its market position by completing the acquisition of United Pest Solutions which extended its reach in the Western United States. The firm also launched an enhanced digital booking and monitoring platform enabling clients to schedule services track technician visits and receive electronic compliance documentation. Terminix continues to invest in technician training and eco friendly treatment options to meet evolving consumer and regulatory expectations.

- Anticimex Group headquartered in Sweden offers innovative pest control solutions with a distinct focus on sustainability and smart technology. The company serves clients across Europe North America and parts of Asia leveraging its proprietary SMART digital monitoring system that minimizes chemical use through early detection and data driven intervention. Anticimex has intensified its commitment to non chemical pest management by expanding its biological control offerings and achieving certified green service status in multiple jurisdictions. Its initiatives reinforce Anticimex’s reputation as a forward looking leader in environmentally responsible pest control.

Top Stratagies Used By The Key Market Participants

Key players in the Pest Control Market consistently deploy five core strategies to reinforce competitive advantage. First they invest heavily in digital transformation integrating Internet of Things enabled monitoring systems and cloud based reporting platforms to enhance service precision and client transparency. Second they pursue strategic acquisitions to expand geographic footprint and diversify service portfolios particularly in underserved urban and agricultural zones. Third they prioritize sustainability by developing and promoting non chemical biological and mechanical control methods in alignment with tightening global regulations. Fourth they enhance workforce capabilities through certified training programs technician upskilling and standardized service protocols. Fifth they deepen client relationships by offering subscription based models predictive maintenance contracts and real time compliance documentation tailored to industry specific regulatory demands. These strategies collectively drive differentiation scalability and long term market resilience in a fragmented and evolving landscape.

MARKET SEGMENTATION

This research report on the pest control market has been segmented and sub-segmented based on pest control, availability, type of pest, and region.

By Pest Control

- Chemical

- Mechanical

- Biological control

By Availability

- Commercial

- Industrial

- Agricultural

- Residential control

By Type of Pest

- Terminates

- Insects

- Rodents

- Wildlife

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the pest control market?

It includes services and products used to manage, prevent, and eliminate pests in residential, commercial, and industrial settings.

What is driving the growth of the pest control market?

Rising health and hygiene awareness, urbanization, and increasing pest-related diseases.

Which pests are commonly targeted in the market?

Insects, rodents, termites, mosquitoes, cockroaches, and bed bugs.

How does climate change impact the pest control market?

Warmer temperatures increase pest populations and expand their geographic spread, boosting demand for control services.

What role does regulation play in the pest control market?

Strict environmental and pesticide regulations influence product usage and encourage eco-friendly solutions.

Which sectors drive demand for pest control services?

Residential, commercial, industrial, healthcare, hospitality, and agriculture sectors.

What are the major challenges in the pest control market?

Regulatory restrictions, rising operational costs, and limited chemical options.

How is sustainability influencing pest control practices?

There is growing adoption of integrated pest management (IPM) and non-toxic, eco-friendly solutions.

What opportunities exist in the pest control market?

Growth in green pest control, smart monitoring technologies, and preventive pest management services.

`What is the future outlook of the pest control market?

The market is expected to grow steadily due to climate change, urban expansion, and health-driven demand.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com