Global Potato Market Size Share, Trends, and Growth Analysis Report, Segmented By End User (Individual, Commercial, Industrial), Distribution Channel, Type & Region (North America, Europe, Latin America, Asia Pacific, Middle East & Africa), Industry Forecast From 2025 to 2033

Global Potato Market Summary

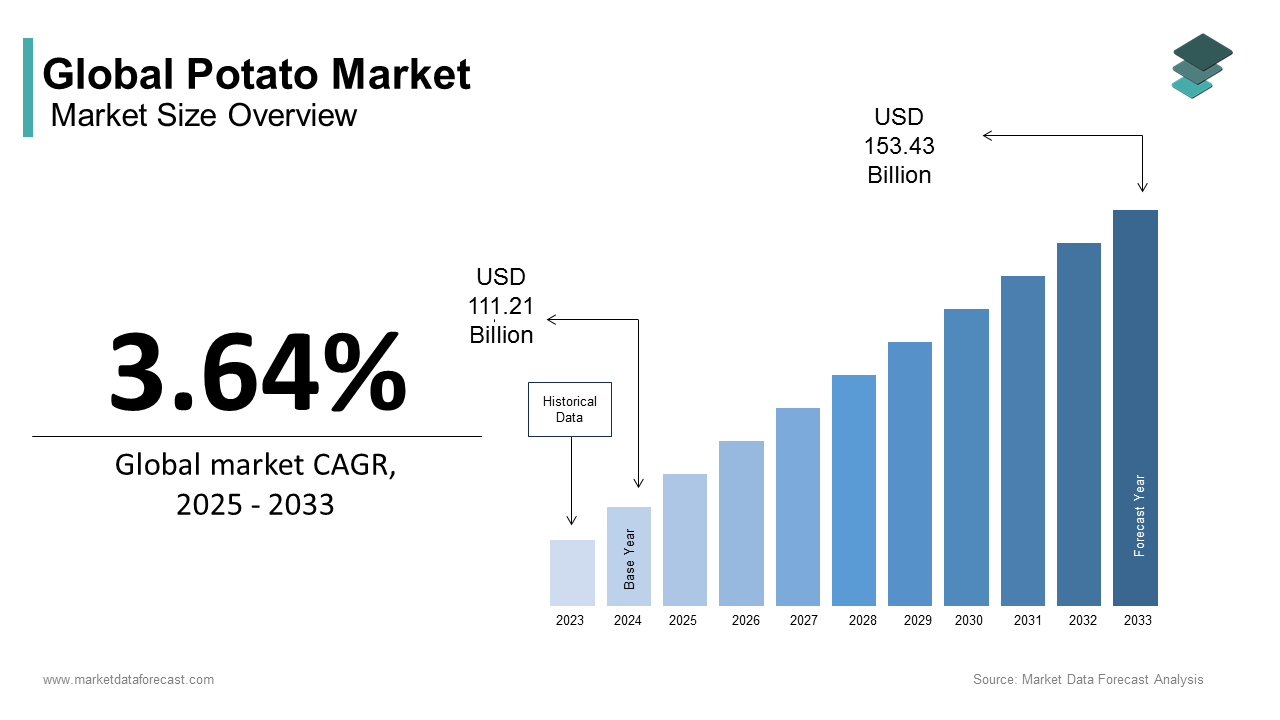

The global potato market was valued at USD 111.21 billion in 2024, is anticipated to reach USD 115.26 billion in 2025, and is projected to expand to USD 153.43 billion by 2033, growing at a CAGR of 3.64% from 2025 to 2033. The growth of the global potato market is driven by increasing demand from the food processing industry, rising consumption of frozen and processed potato products, and the crop’s versatility in both commercial and household applications. Expanding quick-service restaurants (QSRs), strong demand for snacks, and emerging applications in starch and bio-based products further support market growth.

Key Market Trends

- Growing consumption of frozen potato products such as fries, wedges, and hash browns.

- Increasing demand from QSR chains and food service industries worldwide.

- Rising use of potatoes in starch production for food and industrial applications.

- Expansion of modern retail and B2B supply chains supporting wider availability.

- Shift toward sustainable farming and high-yield potato varieties.

Segmental Insights

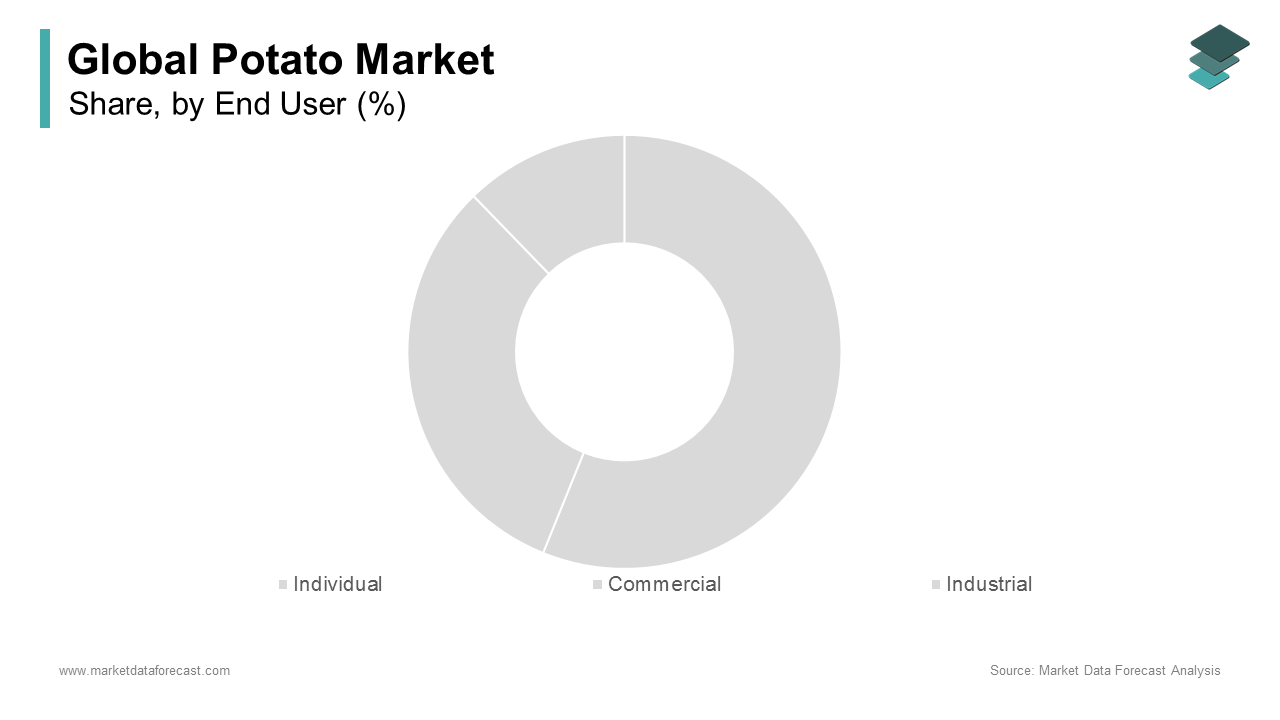

- Based on end-user, the commercial segment dominated the global potato market with 58.2% share in 2024, driven by strong demand from restaurants, hotels, and food processing industries.

- Based on distribution channel, the B2B (business-to-business) channel led the market with 63.1% share in 2024, reflecting bulk procurement by food processors and service providers.

- Based on type, the conventional potatoes segment captured the largest share in 2024, owing to their wide availability and cost-effectiveness.

Regional Insights

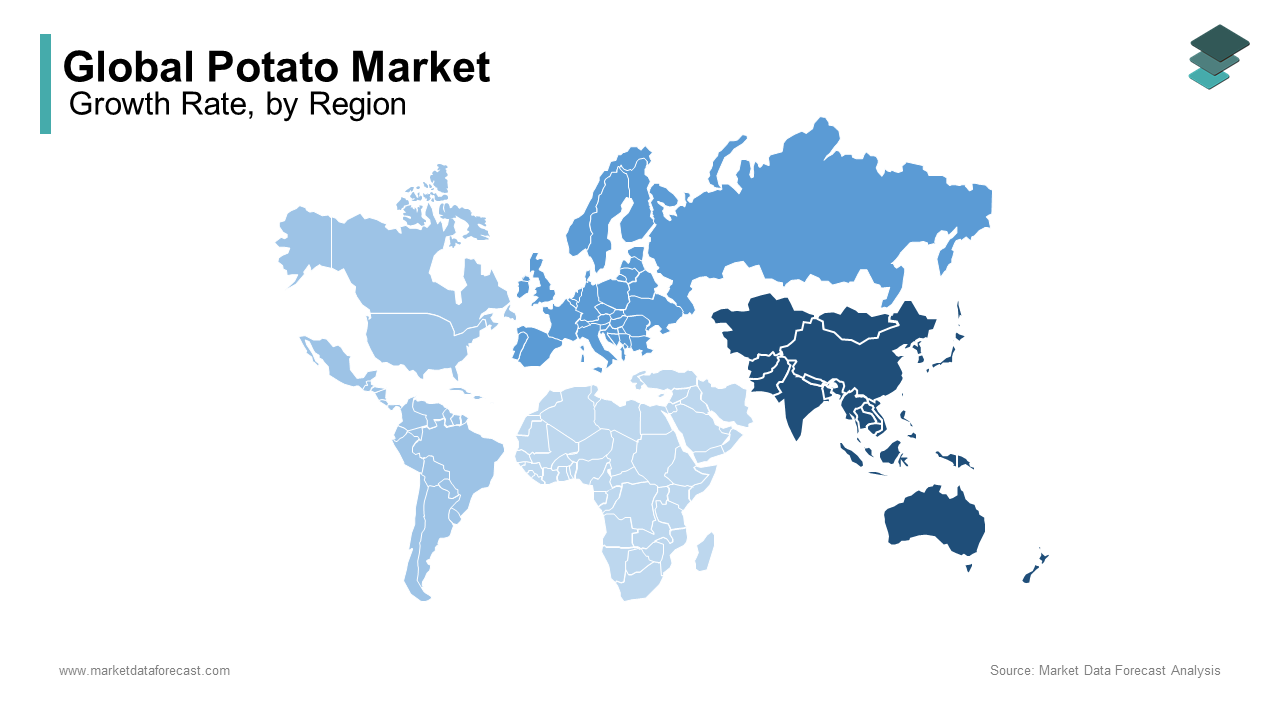

- Asia-Pacific was the top-performing region, accounting for 46.8% of the global potato market in 2024, supported by large-scale production in China and India, along with rising processed potato consumption.

- Europe shows steady growth, driven by strong demand for frozen and snack products.

- North America is witnessing robust demand from QSRs and packaged food companies.

- Latin America and the Middle East & Africa are emerging markets, supported by growing potato processing capacity and rising urban food consumption.

Competitive Landscape

Leading companies in the global potato market include McCain Foods Limited, Lamb Weston Holdings Inc., J.R. Simplot Company, Aviko, Agristo NV, Farm Frites International B.V., The Kraft Heinz Company, Intersnack Group GmbH & Co. KG, Ingredion Incorporated, Tereos, and Roquette Frères. These players are focusing on expanding frozen potato product lines, investing in supply chain efficiencies, and strengthening partnerships with QSRs and retail distributors to capture a larger share of the market.

Global Potato Market Size

The global potato market size was valued at USD 111.21 billion in 2024 and is anticipated to reach USD 115.26 billion in 2025 and USD 153.43 billion by 2033, growing at a CAGR of 3.64% during the forecast period from 2025 to 2033.

Potato is one of the world’s most vital non-cereal food crops. According to the Food and Agriculture Organization of the United Nations, more than 383 million metric tons of potatoes were harvested globally in 2023, with China and India collectively contributing over 40% of total production. The crop plays an important role in food security, particularly in mountainous and temperate regions where other staples struggle to thrive. In Ethiopia, potatoes are cultivated at elevations above sea level which providies a reliable food source for highland communities.

MARKET DRIVERS

Urbanization and Rising Demand for Convenience Food Products

The rapid expansion of urban population, particularly in Asia and Africa, has intensified demand for ready-to-eat and processed potato-based foods, that drives the growth of potato market. According to the research, a portion of the global population resides in urban centers, a figure projected to rise by 2030, increasing reliance on time-saving food options. In India, consumption of processed potatoes rose which is driven by the proliferation of quick-service restaurants like McDonald’s and Domino’s by require consistent supplies of frozen French fries, as per research. Similarly, in Nigeria, urban fast-food chains have increased potato procurement over the past years, according to the research. Cold chain development and investment in industrial peelers, slicers, and freezers have enabled processors to meet this demand. The integration of potatoes into modern foodservice menus is transforming the tuber from a subsistence crop into a commercial commodity with scalable downstream applications.

Government-Led Food Security and Crop Diversification Initiatives

National agricultural policies in several countries are actively promoting potato cultivation as a strategy to enhance food security and reduce dependence on cereal imports, which propels the growth of potato market. The initiative includes subsidized seeds, irrigation support, and training for off-season farming using raised beds and mulching. Similarly, in Kenya, as per study, potato output increased due to state-backed distribution of disease-resistant varieties. These state-driven efforts are boosting yields as well as improving farmer incomes and stabilizing food supplies in regions vulnerable to climate-induced cereal shortages.

MARKET RESTRAINTS

High Susceptibility to Late Blight and Other Pathogenic Diseases

The potato cultivation is severely constrained by Phytophthora infestans, the pathogen responsible for late blight, which hampers the growth of potato market. The late blight affects hectares of potato farms annually, resulting in significant global yield losses. In Uganda, where smallholder farming dominates, a portion of potato harvests are lost to blight and bacterial wilt, as per the study. The disease spreads rapidly in humid conditions, which are common in tropical highlands, and resistant strains have emerged due to overreliance on chemical fungicides. In India, farmers in Himachal Pradesh apply fungicides up to multiple times per season, increasing production costs and environmental degradation, according to the research. The lack of affordable as well as certified disease-free seed tubers further exacerbates the problem in low-income countries where informal seed systems prevail which weakens productivity and food security.

Post-Harvest Losses Due to Inadequate Storage Infrastructure

The potato production is lost after harvest due to poor storage conditions, which hinders the growth of potato market. According to the study, post-harvest losses in sub-Saharan Africa and South Asia were notable primarily due to sprouting, rotting, and pest infestation. In Pakistan, where large metric tons are produced annually, losses were notable due to the absence of climate-controlled warehouses, as per the study. Traditional storage methods, such as underground pits, offer limited protection against temperature fluctuations and humidity. Even in China, where production was significant metric tons, according to the study, a portion of potatoes degrade before reaching markets due to inadequate cold storage. These losses not only reduce farmer incomes but also destabilize supply chains. This leads to price volatility and seasonal shortages, particularly during off-crop periods.

MARKET OPPORTUNITIES

Development and Adoption of Climate-Resilient and Biofortified Varieties

The advancements in plant breeding are enabling the deployment of potato varieties, which is setting up new opportunities for the growth of potato market. These variestes withstand drought, heat, and nutrient-poor soils while offering enhanced nutritional profiles. These innovations are supported by public-private partnerships and digital extension services that deliver seedlings and agronomic advice via mobile platforms. Thus, such resilient cultivars are becoming essential for sustaining production in vulnerable regions as climate change is threatening traditional growing zones which transforms the potato into a tool for both adaptation and malnutrition mitigation.

Expansion of Industrial Utilization in Starch and Bio-Based Product Manufacturing

The increased usage in industrial applications as feedstock, including starch extraction, bioethanol, and biodegradable packaging, will provide new opportunities for the potato market. In Germany, companies process large tons of potatoes annually into functional ingredients for adhesives and bioplastics. In China, it has classified potato starch as a strategic material for reducing reliance on imported corn-based polymers. Apart from these, startups in the Netherlands are developing mycelium-composite materials using potato waste. These non-food applications diversify demand, enhance farmgate value, and align with circular economy principles which positions the potato as a multi-sectoral resource.

MARKET CHALLENGES

Dependence on Vegetative Propagation and Seed Degeneration

The potatoes are predominantly grown from seed tubers rather than true seeds, which is leading to the accumulation of viruses and pathogens over successive planting cycles, which challenges the growth of potato market. In Nepal, a portion of farmers reuse their own tubers as seed, perpetuating diseases, as per the study. The lack of formal seed systems and high cost of certified seed limit access to clean planting material. In sub-Saharan Africa, only a portion of potato seed is certified, according to the study. Establishing decentralized mini-tuber production units and tissue culture labs is important, but requires sustained investment and technical capacity. Therefore, seed degeneration will continue to weaken productivity gains and food security efforts due to lack of systemic reforms.

Water Intensity and Competition for Irrigation Resources

The potato cultivation requires substantial water input by making it vulnerable to water scarcity and competition from other sectors, challenges the growth of potato market. The potato farming accounts for a portion of irrigated land in northern China’s Hebei Province, a region facing severe groundwater depletion. The water table in this area is declining, as per the research. In Peru, where potatoes originated, farmers in the Andean highlands are experiencing reduced glacial meltwater which affects dry-season irrigation. As per the study, a portion of potato farms in the Mantaro Valley face water shortages during important growth stages. Balancing agricultural demand with ecological sustainability is becoming a defining challenge for the sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.64% |

| Segments Covered | By End User, Distribution Channel, Type, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | McCain Foods Limited, Lamb Weston Holdings Inc., J.R. Simplot Company, Aviko, Agristo NV, Farm Frites International B.V., The Kraft Heinz Company, Intersnack Group GmbH & Co. KG, Ingredion Incorporated, Tereos, and Roquette Frères |

SEGMENTAL ANALYSIS

By End-User Insights

The commercial segment dominated the potato market by capturing 58.2% of share in 2024. The explosive rise of the quick-service restaurant (QSR) industry is propelling the growth of the commercial segment. In addition, the global QSR sector generated significant revenue, with fries and potato-based sides being among the most popular menu items. McDonald’s alone serves millions of pounds of fries daily worldwide, as per the research. The scalability of potato use in standardized menus across international chains strengthens bulk procurement patterns which favors commercial buyers over individual consumers. Apart from these, the rise of cloud kitchens and delivery-focused dining models has amplified demand. These operations prioritize low-cost, high-margin staples like potatoes, further entrenching the commercial segment’s lead.

The industrial segment is estimated to register the fastest CAGR of 6.8% during the forecast period owing to the rising demand for processed potato products such as frozen fries, dehydrated flakes, and potato starch. Unlike raw potato consumption, industrial use involves value-added transformation, which aligns with broader food manufacturing trends. The surge in convenience food consumption is also accelerating the growth of industrial segmnet. The global business of frozen potato products is expected to grow at annually, according to research. This is supported by changing lifestyles, especially in urban centers, where time-poor consumers opt for ready-to-cook or ready-to-eat meals. For instance, as per research, a portion of consumers in North America and Western Europe purchase frozen meals regularly, with potato-based items dominating freezer sections. The expanding use of potato starch in non-food industries is further boosting the growth of this segment. Its biodegradability and functional properties make it a preferred alternative to synthetic polymers, especially under EU green regulations.

By Distribution Channel Insights

The B2B (business-to-business) channel led the potato market by capturing 63.1% of the global market share in 2024. The growth of B2B segment is propelled by the structural reliance of large-scale food processors, restaurant chains, and institutional buyers on direct procurement from farmers, cooperatives, and wholesale aggregators. The scale of institutional procurement is main factor behind the growth of B2B segment. For example, in the United States, a portion of potato production is contracted before harvest through forward agreements between growers and processors like McCain Foods and Lamb Weston, according to the research. These contracts ensure supply chain stability and reduce price volatility which makes B2B the preferred route for high-volume users. Furthermore, cold chain infrastructure favours bulk movement. The global business of agricultural cold chain is optimized for palletized and temperature-controlled shipments to central kitchens and processing plants rather than individual retail units.

The B2C (business-to-consumer) segment is predicted to witness the highest CAGR of 7.1% from 2025 to 2033 due to the shifting consumer behaviors, digital transformation, and heightened focus on food quality and origin. The rise of e-grocery platforms is also propelling the growth of B2C segment. The online business of grocery surged, with fresh produce as the fastest-growing category. In India, for instance, an increase in potato sales via direct-to-home delivery, attributing it to urban consumers seeking fresher, traceable produce. The rising preference for premium and specialty potato varieties is further escalating the growth of this segment. In Germany, sales of colored and heirloom potatoes in retail surged, according to the study. Consumers are increasingly willing to pay a premium for organic, locally grown, or nutritionally enhanced options, trends that B2C channels are better equipped to serve through branding and storytelling.

By Type Insights

The conventional potatoes segment dominated the potato market by capturing significant share in 2024. The growth of the conventional segment is driven by the established farming systems, lower production costs, and widespread availability across both developed and developing economies. Economic efficiency is primary factor propelling the growth of conventional segment. Conventional potato farming yields metric tons per hectare which significantly higher than organic yields. This productivity gap makes conventional potatoes the default choice for large-scale processors and food manufacturers seeking cost stability. Apart from these, supply chain infrastructure is overwhelmingly geared toward conventional production. In the Netherlands, the world’s second-largest potato exporter, a notable share of exported potatoes are conventionally grown, as per study. The country’s advanced seed certification, storage, and processing facilities are calibrated for high-volume, consistent output, conditions less compatible with organic variability.

The organic potato segment is predicted to witness the highest CAGR of 9.3% from 2025 to 2033 owing to the deepening consumer awareness about health, environmental sustainability, and food transparency. Rising health consciousness is also boosting the growth of organic potato segment. As per the study, a portion of U.S. consumers actively avoid pesticide residues in food, with potatoes frequently cited due to their position on the Environmental Working Group’s Dirty Dozen list. This concern is translating into purchasing behaviour. Environmental regulations are also accelerating adoption. Furthermore, retailers like Tesco and Carrefour have committed to expanding organic produce shelf space, per their corporate sustainability disclosures.

REGIONAL ANALYSIS

Asia Pacific Potato Market Insights

Asia Pacific was the top performer in the global potato market in 2024 and accounted for 46.8% of the global market share in 2024. China and India alone account for a portion of global output, with China producing millions of metric tons and India with millions of metric tons annually. The region’s dominance is rooted in population-driven staple demand and government-backed agricultural programs. In India, it has allocated substantial share to boost potato productivity in states like Uttar Pradesh and West Bengal. Urbanization and rising fast-food penetration, KFC expanded to notable number of outlets in China by 2023, as per study, further fuel industrial use. However, post-harvest losses remain high which limits value realization.

Europe Potato Market Insights

Europe potato market was ranked second 22.1% of the global market share in 2024. Value addition and technological advancement are the factors propelling the growth of Europe in the global market. The region produces millions of tons annually, with countries like Germany, France, and the Netherlands excelling in seed potato exports and frozen processing. The Netherlands exports significant tons of seed potatoes yearly which makes it the world’s top exporter, according to study. The EU’s strict quality standards and investment in cold storage, a portion of potatoes are stored under climate-controlled conditions, enable year-round supply.

North America Potato Market Insights

North America potato market is anticipated to have lucrative CAGR during the forecast period with the dominance in per capita consumption and retail value. The U.S. produces notable million tons annually, with Idaho contributing a portion of national output. Americans consume a significant amount of potatoes each year, their consumption of wheat flour (used to make bread) is much higher, according to the study. The region’s strength lies in integrated supply chains and brand-driven marketing. A portion of U.S. potatoes are processed, with frozen fries making a notable share of that, as per the research. Canada’s investment in disease-resistant varieties through Agriculture and Agri-Food Canada has also improved yield stability.

Latin America Potato Market Insights

Latin America is expected to be the most lucrative region in the potato market. Brazil produces notable million tons annually, while Colombia and Peru are expanding cultivation. Peru hosts numerous native varieties, according to the study, and is leveraging this biodiversity for niche export markets. Chile has become a key off-season supplier and exporting significant tons of fresh potatoes annually, as per study. Urbanization and rising middle-class incomes are increasing demand for processed forms. In Mexico, potato chip sales grew, as per study, signaling a shift in consumption patterns.

Middle East & Africa Potato Market Insights

The Middle East and Africa is likely to grow in the potato market. The region is the most import-dependent market. Egypt is the key producer in Africa with millions of tons annually, according to research, while Nigeria and South Africa are scaling up. Gulf countries like Saudi Arabia and the UAE import significant tons of potatoes yearly, primarily from India, Egypt, and Jordan, as per the study. Rapid urbanization and a booming foodservice sector, Dubai hosts number of restaurants, are driving demand. Therefore, the region’s potato demand is expected to double by 2035, per IFPRI projections.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global potato market include

- McCain Foods Limited

- Lamb Weston Holdings Inc.

- J.R. Simplot Company

- Aviko

- Agristo NV

- Farm Frites International B.V.

- The Kraft Heinz Company

- Intersnack Group GmbH & Co. KG

- Ingredion Incorporated

- Tereos

- Roquette Frères

Top Strategies Used By Key Market Participants

Key players in the potato market are deploying vertical integration, product innovation, geographic expansion, sustainability initiatives, and digital transformation to strengthen their positions. Companies are investing in farm-to-fork control by partnering with farmers for contract cultivation, ensuring raw material quality and supply stability. Product diversification, such as launching flavored fries, plant-based potato snacks, and organic variants, caters to evolving consumer preferences. Expansion into emerging markets like India, Indonesia, and Vietnam allows access to growing middle-class populations. Sustainability efforts include water-efficient farming, biodegradable packaging, and carbon-neutral processing. Digital tools like AI-driven yield prediction, blockchain traceability, and e-commerce platforms enhance efficiency and transparency. These strategies collectively enable firms to build resilience, differentiate offerings, and capture long-term value in a competitive global landscape.

COMPETITION OVERVIEW

The global potato market is highly competitive, characterized by the presence of large multinational processors, regional agribusinesses, and emerging local brands. Competition is driven by scale, innovation, supply chain efficiency, and brand recognition. Multinational companies like McCain, Lamb Weston, and J.R. Simplot dominate through advanced processing technologies and global distribution networks. However, regional players in Asia, Eastern Europe, and Latin America are gaining ground by offering cost-effective, locally adapted products. Price sensitivity, fluctuating raw material costs, and logistical challenges intensify rivalry. Differentiation occurs through product variety, sustainability claims, and private-label partnerships with retailers. The rise of health-conscious consumers has spurred innovation in organic, non-GMO, and functional potato products. As demand for convenience foods grows, companies are investing heavily in R&D and automation to maintain margins and market dominance in an increasingly dynamic and fragmented landscape.

LEADING PLAYERS IN THE POTATO MARKET

McCain Foods

McCain Foods, a global leader in frozen potato products, has significantly expanded its footprint in the Asia Pacific region through localized production and strategic partnerships. The company operates multiple processing facilities in India, China, and Australia, enabling it to meet rising demand for frozen fries in fast-food and retail sectors. It also launched region-specific products like masala-flavored fries to cater to local tastes. Collaborating with farmers on contract farming models, McCain ensures consistent potato quality while boosting rural incomes. Its innovation in packaging and cold chain logistics has strengthened distribution across urban and semi-urban markets, positioning it as a key driver of processed potato consumption in the region.

J.R. SIMPLOT COMPANY

J.R. Simplot has deepened its presence in Asia Pacific by leveraging its integrated agricultural and food processing expertise. The company supplies frozen potato products to major QSR chains in Japan, South Korea, and Southeast Asia, supported by its advanced processing plant in China. Simplot has invested heavily in sustainable farming practices, partnering with local growers in Australia and Indonesia to improve yield and reduce environmental impact. It also launched a digital farm monitoring system in Thailand to optimize irrigation and pest control.

Lamb Weston

Lamb Weston has intensified its focus on Asia Pacific by expanding distribution networks and launching tailored product lines for diverse culinary preferences. The company established a joint venture in China and strengthened logistics partnerships in Indonesia and Vietnam to improve market reach. It also introduced sustainable packaging solutions across its APAC portfolio, aligning with regional environmental regulations. Its investment in cold chain infrastructure and digital sales platforms has enhanced supply reliability, making it a preferred supplier for both multinational and regional food businesses seeking consistent, high-quality frozen potato solutions.

MARKET SEGMENTATION

This research report on the global potato market is segmented and sub-segmented into the following categories.

By End User

- Individual

- Commercial

- Industrial

By Distribution Channel

- B2C

- B2B

By Type

- Conventional

- Organic

By Region

- North America

- Europe

- Latin America

- Asia Pacific

- Middle East & Africa

Frequently Asked Questions

1. What are the key factors driving the growth of the potato market?

Rising consumption of processed foods, increasing demand for frozen fries and chips, growing quick-service restaurants (QSRs), and the versatility of potatoes across cuisines.

2. Which regions dominate the global potato market?

Asia-Pacific leads in production (China and India are the largest producers), while Europe and North America dominate in processed and frozen potato consumption.

3. Who are the major players in the potato market?

Key players include McCain Foods, Lamb Weston, J.R. Simplot Company, Aviko, Agristo, Farm Frites, Kraft Heinz, and Intersnack Group.

4. How is the demand for frozen potato products evolving?

Frozen potato products (fries, wedges, hash browns) are witnessing strong growth due to fast-food chains, convenience, and longer shelf life.

5. What role does potato starch play in the market?

Potato starch is widely used in food processing, adhesives, textiles, pharmaceuticals, and as a gluten-free alternative.

6. What are the key challenges faced by the potato market?

Price volatility, climate change affecting yields, storage challenges, and competition from alternative snacks and staple crops.

7. How does the health trend affect potato consumption?

While potatoes are nutrient-rich, growing health-conscious consumers may limit fried potato intake, boosting demand for healthier potato-based products.

8. What is the outlook for potato production in Asia-Pacific?

Asia-Pacific will continue to dominate due to large-scale production in China, India, and Pakistan, supported by rising domestic consumption.

9. How is technology influencing the potato industry?

Advances in cold storage, precision farming, processing automation, and new potato varieties are improving yields and product quality.

10. What is the future growth outlook for the global potato market?

The market is expected to grow steadily, driven by increasing demand for frozen, convenience, and snack products, alongside expanding foodservice industries.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com