Global Protein Bar Market Size, Share, Trends & Growth Forecast Report – Segmented By Product Type (Meal Replacement Bars, Energy Protein Bars, Low Carbohydrate Protein Bars And Womens Protein Bar), Protein Source (Plant Protein And Animal Protein), Protein Content (Low Protein, Medium Protein And High Protein) And Region (North America, Europe, Asia Pacific, Latin America, And Middle East & Africa) - Industry Analysis (2026 To 2034)

Global Protein Bar Market Summary

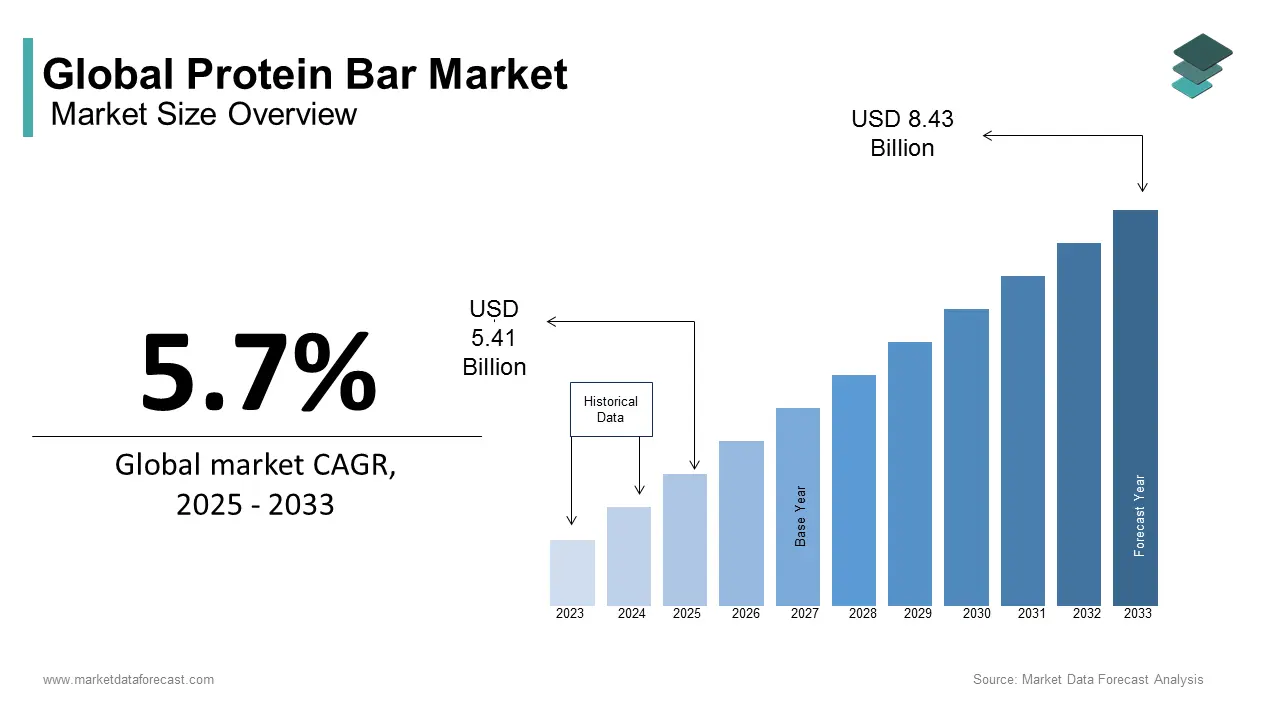

The size of the global protein bar market was valued at USD 5.41 billion in 2025. The global market size is expected to grow at a CAGR of 5.7% from 2026 to 2034 and be worth USD 8.91 billion by 2034 from USD 5.72 billion in 2026. Growth is fueled by the rising fitness culture, demand for convenient high-protein snacks, targeted product innovations for specific demographics, and expanding e-commerce distribution channels.

Key Market Trends & Insights

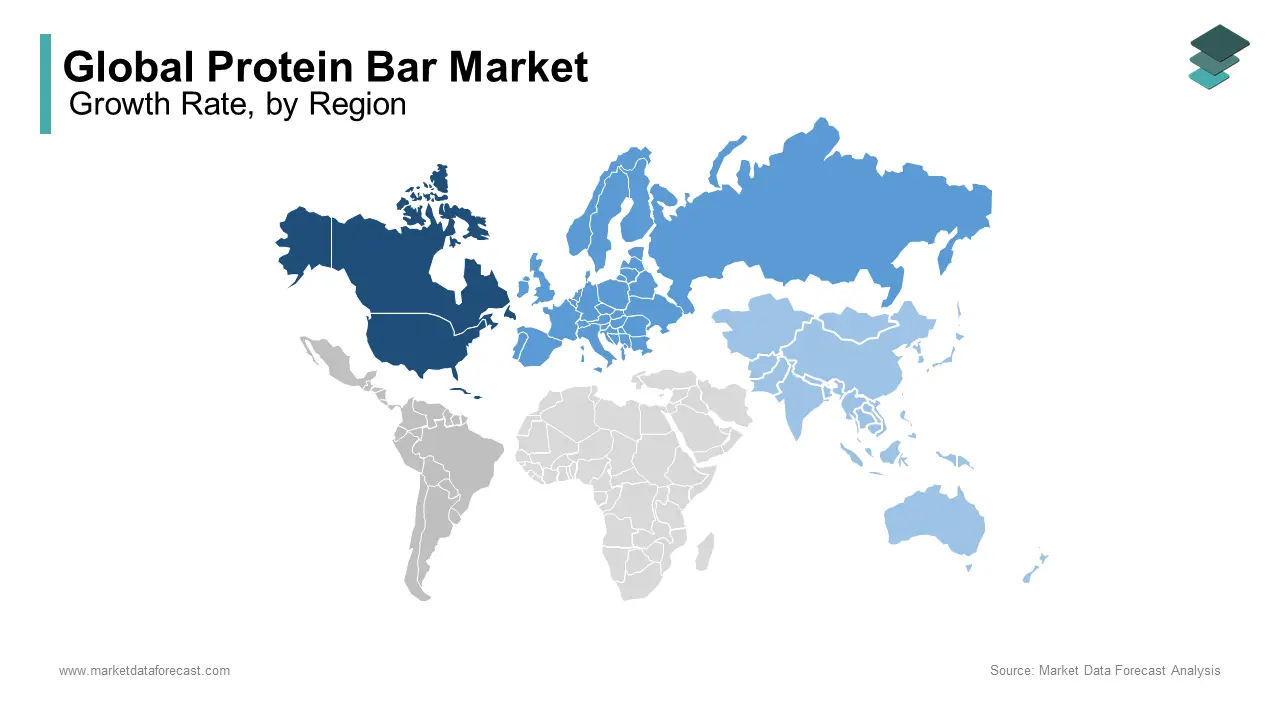

- North America is the largest market in 2025 (44.1% share), driven by a mature fitness culture, strong brand presence (Clif Bar, Quest, RXBAR), and high consumer health awareness.

- Asia Pacific is the fastest-growing region, boosted by urbanization, rising disposable incomes, and increasing adoption of fitness and preventive health habits in China, India, Japan, and South Korea.

- By Product Type: Energy protein bars dominated in 2025 (42% share) due to their dual role as performance-enhancing snacks and meal replacements.

- By Protein Source: Animal protein-based bars led with 61.5% share in 2025, supported by whey and casein’s complete amino acid profile and rapid digestibility.

- By Protein Content: High protein bars dominated in 2025 (56.3% share), favored for muscle maintenance, satiety, and performance nutrition.

Market Size & Forecast

- 2025 Market Size: USD 5.14 Billion

- 2034 Projected Market Size: USD 8.91 Billion

- CAGR (2026–2034): 5.7%

- North America: Largest market in 2025

- Asia Pacific: Strong growth region

Global Protein Bar Market Size

The size of the global protein bar market was valued at USD 5.41 billion in 2025. The global market size is expected to grow at a CAGR of 5.7% from 2026 to 2034 and be worth USD 8.91 billion by 2034 from USD 5.72 billion in 2026.

Protein Bar Market refers to a specialized segment of the functional food industry comprising ready-to-eat snack bars formulated with elevated protein content, typically ranging from 10 to 20 grams per unit, designed to support muscle maintenance, satiety, and active lifestyles. These products are engineered using diverse protein sources such as whey, casein, soy, pea, rice, and collagen, often combined with fibers, healthy fats, and low-glycemic sweeteners to balance macronutrient profiles. Unlike conventional confectionery bars, protein bars are positioned as performance or wellness-oriented foods, consumed pre- or post-exercise, as meal replacements, or for appetite control. Their formulation adheres to evolving nutritional standards, with increasing emphasis on clean labels, allergen transparency, and minimal processing.

According to the World Health Organization, global physical inactivity affects over 1.4 billion adults, contributing to rising metabolic disorders and prompting interest in dietary solutions that support metabolic health. The International Society of Sports Nutrition highlights that protein intake above the RDA (0.8g/kg/day) is beneficial for active individuals, with optimal muscle synthesis occurring at intakes of 1.6–2.2g/kg/day—demanding convenient sources beyond whole foods. As consumer behavior shifts toward preventive health and time-efficient nutrition, protein bars have transitioned from niche athletic supplements to mainstream dietary staples across diverse demographics.

MARKET DRIVERS

Rising Participation in Fitness and Structured Exercise Regimens

The surge in gym memberships, home workouts, and organized fitness activities is a primary catalyst for increased demand for protein bars as convenient, on-the-go sources of high-quality protein. This behavioral change is mirrored in digital fitness adoption. Protein bars are increasingly consumed immediately post-workout to support muscle protein synthesis, a practice reinforced by sports nutrition guidelines recommending 20–25 grams of protein within 30–60 minutes after exercise. Additionally, the normalization of fitness among women has expanded the consumer base. Brands like Clif Bar, Quest Nutrition, and RXBAR have capitalized on this trend by aligning product messaging with performance outcomes, sponsoring fitness events, and collaborating with trainers. As structured exercise becomes a routine aspect of modern life, protein bars are evolving into essential tools for nutritional recovery and consistency.

Increasing Prevalence of Protein-Deficient Diets Among Specific Demographics

A growing awareness of inadequate protein intake, particularly among aging populations, vegetarians, and busy professionals, is driving demand for fortified, portable protein sources such as protein bars. The European Society for Clinical Nutrition and Metabolism estimates that over 30% of elderly individuals in developed nations are protein-deficient, contributing to prolonged recovery from illness and reduced mobility. Similarly, plant-based diets, while rising in popularity, often lack complete amino acid profiles. In fast-paced urban environments, time constraints further exacerbate poor dietary habits. These products offer a balanced compromise between convenience and nutrition, with many brands now offering vegan, gluten-free, and low-sugar variants to cater to dietary restrictions. As public health messaging emphasizes protein’s role in satiety, weight management, and metabolic health, protein bars are gaining recognition not just as fitness aids but as essential components of balanced, modern diets.

MARKET RESTRAINTS

High Sugar and Additive Content in Many Commercial Formulations

Despite their health-oriented positioning, many protein bars contain excessive levels of added sugars, artificial sweeteners, and preservatives, undermining their nutritional credibility and deterring health-conscious consumers. Additionally, sugar alcohols such as erythritol and maltitol, commonly used in “low-sugar” variants, have been linked to gastrointestinal discomfort. As consumers increasingly scrutinize ingredient lists, brands with opaque or chemically complex formulations face reputational damage. In addition, retailers like Whole Foods and Thrive Market have implemented strict clean-label standards, delisting products with artificial ingredients. Until the industry standardizes transparent, minimally processed formulations, consumer trust will remain fragmented, constraining market expansion among discerning demographics.

Consumer Skepticism Due to Misleading Health Claims and Greenwashing

The protein bar market faces growing resistance from informed consumers who question the validity of marketing claims such as “all-natural,” “keto-friendly,” or “high-protein” when not substantiated by independent verification or regulatory oversight. Furthermore, terms like “plant-based” or “clean label” are often used without standardized definitions, leading to consumer confusion. Social media amplifies scrutiny; platforms like Reddit and YouTube host extensive user-led testing and ingredient analysis, exposing discrepancies between branding and reality. This erosion of trust is particularly acute among younger consumers. As regulatory bodies tighten labeling requirements—such as the FDA’s proposed update to the “healthy” claim definition—brands must align marketing with scientific rigor or risk losing credibility in an increasingly transparent marketplace.

MARKET OPPORTUNITIES

Expansion of Plant-Based and Allergen-Free Protein Bar Offerings

The development of plant-based, allergen-conscious, and specialty-diet protein bars presents a significant growth avenue, driven by rising demand for inclusive and ethically aligned nutrition. Plant-based protein bars, formulated with pea, brown rice, hemp, or pumpkin seed protein, cater to vegans, environmentally conscious consumers, and those with dairy allergies. Companies like No Cow and GoMacro have gained traction with soy-free, nut-free, and gluten-free options certified under GFCO and NSF standards. Additionally, sustainability concerns are influencing choices. Brands are responding with transparent sourcing, recyclable packaging, and carbon labeling. As dietary diversity becomes a norm rather than an exception, protein bars that align with ethical, environmental, and medical needs are poised to capture underserved market segments.

Integration with Digital Health and Personalized Nutrition Platforms

The convergence of protein bars with digital health technologies and personalized nutrition services offers a transformative opportunity to shift from mass-market products to tailored dietary solutions. Wearable fitness trackers, DNA testing kits, and AI-driven nutrition apps are generating vast amounts of individual health data, enabling customized macronutrient recommendations. Companies like Zoe and InsideTracker provide personalized nutrition plans that include specific protein bar recommendations based on blood markers, gut microbiome, and lifestyle. Additionally, subscription models powered by AI, such as those from Gainful and Care/Of, allow consumers to customize protein bar flavors, macronutrient ratios, and ingredient sensitivities. These models report higher customer retention than standard e-commerce. As healthcare shifts toward preventive, data-driven models, protein bars integrated into digital wellness ecosystems can transition from generic snacks to precision nutrition tools, enhancing efficacy, adherence, and brand loyalty in a competitive marketplace.

MARKET CHALLENGES

Ingredient Sourcing Volatility and Supply Chain Fragility

The protein bar industry is increasingly vulnerable to disruptions in the supply of key ingredients, particularly dairy-derived proteins and plant-based isolates, due to climate change, geopolitical instability, and agricultural constraints. Whey protein, a primary ingredient in many bars, is a byproduct of cheese production, making it susceptible to dairy industry fluctuations. Similarly, pea protein, a cornerstone of plant-based bars, is concentrated in Canada and France. Additionally, supply chain bottlenecks, exacerbated by port congestion and container shortages, have increased lead times and inventory costs. These vulnerabilities force brands to either absorb cost increases or reformulate products, risking consistency and consumer trust. To mitigate risks, companies are investing in vertical integration, alternative protein sources like mycoprotein, and regional sourcing, but scalability remains a challenge in a rapidly growing market.

Saturation and Differentiation Difficulties in a Crowded Market

The protein bar market is marked by intense competition and product homogeneity, making brand differentiation increasingly difficult despite growing consumer demand. The saturation reduces shelf space availability and increases marketing costs. Additionally, private-label brands from retailers like Kroger, Amazon, and Costco are gaining share with lower-priced alternatives, eroding margins for established players. Smaller brands struggle with distribution access, as major chains prioritize national brands with proven turnover. Digital channels offer some relief, but customer acquisition costs on platforms like Amazon and Instagram have risen since 2021. Without clear differentiation in taste, texture, ingredient quality, or mission, even innovative products risk being lost in the noise, making sustainable brand building a formidable challenge in an oversaturated landscape.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.7% |

| Segments Covered | By Product Type, Protein Source, Protein Content and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Small Planet Foods, Inc., The WhiteWave Foods Company, The Kellogg Company, General Mills, Inc., Premier Nutrition Corporation, Caveman Foods LLC, MARS, Incorporated, and Others. |

SEGMENTAL ANALYSIS

By Product Type Insights

The Energy protein bars segment commanded the largest share of the global protein bar market at 42% of total revenue in 2025. This dominance is due to their dual positioning as both performance-enhancing snacks and convenient meal supplements, appealing to athletes, fitness enthusiasts, and time-constrained professionals. A key driver is their formulation, which combines moderate-to-high protein (12–20g) with complex carbohydrates and healthy fats to deliver sustained energy. The popularity of endurance sports has surged. Additionally, the integration of these bars into corporate wellness programs has broadened their reach. Brands such as Clif Bar and KIND have capitalized on this trend by aligning with marathons, triathlons, and outdoor adventure communities. With formulations designed for both immediate fuel and recovery, energy protein bars have become indispensable in active lifestyles, reinforcing their market leadership.

The women’s protein bars segment is the fastest-growing in the protein bar market and is projected to expand at a CAGR of 10.8% in the coming years. This acceleration is driven by targeted product development that addresses the unique nutritional and hormonal needs of women across life stages. A primary factor is the rising participation of women in strength training and functional fitness. Women-specific bars often contain added iron, collagen, B vitamins, and lower caffeine levels to support menstrual health, bone density, and skin integrity. Brands like Premier Protein’s Women’s Series and Bobbie’s Women’s Fuel Bars have introduced formulations with 15g of protein, 8mg of iron, and adaptogens to reduce fatigue. Additionally, marketing strategies now emphasize body positivity and holistic wellness rather than weight loss alone, resonating with younger demographics. As gender-specific nutrition gains scientific and cultural legitimacy, women’s protein bars are evolving into a distinct and rapidly expanding category.

By Protein Source Insights

The animal protein-based bars segment led the protein bar market by capturing 61.5% of global revenue in 2025. This dominance is rooted in the high biological value, complete amino acid profile, and rapid digestibility of animal-derived proteins such as whey, casein, and egg white. Whey protein, in particular, is widely regarded as the gold standard for muscle protein synthesis due to its rich leucine content. Additionally, consumer familiarity and trust in dairy-based nutrition remain strong. Major brands such as Quest Nutrition, Optimum Nutrition, and RXBAR have built their reputations on animal protein formulations, leveraging clinical research to validate efficacy. Furthermore, advancements in processing, such as cold-filtration and hydrolysis, have improved taste and reduced lactose content, expanding accessibility to sensitive consumers. Despite rising interest in plant-based options, animal protein bars continue to dominate due to their proven performance benefits, sensory appeal, and established supply chains.

The plant protein-based bars segment is the fastest-growing in the protein bar market by projected to grow at a CAGR of 11.2% from 2026 to 2034. This surge is fueled by shifting consumer preferences toward sustainable, ethical, and allergen-conscious diets. A key driver is the global rise in plant-based eating. Plant protein bars, typically formulated with pea, brown rice, hemp, or soy isolates, cater to vegans, environmentally aware consumers, and those with dairy or egg allergies. Additionally, sustainability concerns are influencing choices. Brands like No Cow, CLIF’s Plant Bar, and Ripple have gained traction with transparent sourcing and recyclable packaging. Regulatory support is also growing. As plant protein technologies improve—enhancing taste, texture, and amino acid completeness—this segment is poised to challenge the dominance of animal-based products.

By Protein Content Insights

The high protein bars segment dominated the market by accounting for 56.3% of global revenue in 2025. This position is driven by their alignment with evidence-based nutrition guidelines for muscle maintenance, satiety, and metabolic health. High protein bars efficiently deliver this macronutrient density. The aging population further amplifies demand. Additionally, weight management remains a key motivator. Brands like Quest, Premier Protein, and Built Bar have built their identity around high protein content, often exceeding 20g per bar. Retailers prioritize these products in fitness and health sections, reinforcing consumer perception of efficacy. As scientific consensus strengthens around protein’s role in long-term health, high protein bars remain the preferred choice for performance and preventive nutrition.

The medium protein bars segment is emerging as the fastest-growing segment, with a projected CAGR of 9.7% in the future. This growth is driven by their positioning as balanced, everyday snacks suitable for broader demographics beyond hardcore athletes. A key factor is their appeal to consumers seeking moderate protein intake without the dense texture or chalky aftertaste often associated with high-protein formulations. These products are increasingly consumed as mid-morning or afternoon snacks to stabilize energy and curb cravings. Brands like KIND, Lärabar, and GoMacro have gained traction by combining protein with whole food ingredients, fiber, and healthy fats, appealing to clean-label advocates. Additionally, parents are adopting medium protein bars for children and teens. With lower formulation costs and broader flavor versatility, medium protein bars are expanding into mainstream retail and convenience channels, positioning them for sustained growth.

REGIONAL ANALYSIS

North America

North America spearheaded the global protein bar market by accounting for 44.1% of revenue in 2025. The region’s growtg is anchored in a deeply entrenched fitness culture, high health awareness, and robust retail infrastructure. The United States, in particular, has a mature market supported by widespread gym participation. Additionally, the prevalence of sedentary lifestyles and obesity has spurred demand for convenient, nutrient-dense snacks. The rise of meal replacement trends and intermittent fasting has further boosted protein bar consumption as a tool for appetite control. Major brands such as Clif Bar, Quest, and RXBAR originated in the U.S., benefiting from early-mover advantage and strong distribution networks. E-commerce platforms like Amazon and Thrive Market have expanded access, while digital marketing and influencer partnerships drive brand loyalty. Regulatory clarity from the FDA on labeling and health claims also supports innovation. With high disposable income and a culture of preventive health, North America remains the most developed and influential market for protein bar innovation and consumption.

Europe

Europe holds a significant share of the protein bar market. The region’s market is characterized by increasing health consciousness, rising fitness participation, and growing regulatory support for functional foods. Countries such as Germany, the UK, and Sweden lead in adoption. The European Commission’s focus on nutrition and sustainability through the Farm to Fork strategy has encouraged the development of clean-label, plant-based, and low-sugar protein bars. Consumer demand for transparency is high. Additionally, the rise of active aging programs in countries like Italy and France has increased protein bar use among seniors. Retailers such as Tesco, Carrefour, and REWE have expanded dedicated health snack aisles, improving visibility. However, regulatory fragmentation across nations affects labeling and claims, requiring brands to adapt regionally. Despite this, the integration of protein bars into workplace wellness programs and sports nutrition plans is accelerating adoption. With strong scientific backing and evolving consumer preferences, Europe is a dynamic and rapidly expanding market.

Asia Pacific

Asia-Pacific is the fastest-growing region in the protein bar market. The region’s ascent is driven by rising disposable incomes, urbanization, and increasing awareness of fitness and nutrition, particularly in China, India, Japan, and South Korea. In India, the number of fitness centers increased between 2019 and 2023, reflecting a cultural shift toward active lifestyles. In Japan, where a portion of the population is over 65, protein bars are gaining traction as tools to combat sarcopenia, supported by government-endorsed nutrition guidelines. China’s growing middle class is embracing Western-style health trends, with online searches for “protein bar” increasing from 2020 to 2023. Local brands like Oatside and MuscleBlaze are competing with global players by offering regionally adapted flavors and pricing. E-commerce platforms such as Alibaba, JD.com, and Flipkart have enabled rapid distribution. Additionally, the expansion of convenience stores and health food retailers in urban centers has improved accessibility. With increasing digital health engagement and fitness app adoption, APAC is transitioning from a nascent to a high-potential market for protein bars.

Latin America

Latin America is reflecting a market in early but accelerating development. Brazil and Mexico are the primary growth engines, driven by rising health awareness, urbanization, and the expansion of private healthcare and fitness sectors. In Mexico, it has launched public campaigns promoting balanced diets, indirectly supporting functional food adoption. However, affordability remains a barrier. To address this, companies like Nutrabay and Max Titanium are introducing cost-optimized local brands. Additionally, e-commerce is expanding access. Cultural preferences for natural ingredients are shaping formulations, with brands incorporating native superfoods like chia and maca. While regulatory frameworks are still evolving, the growing middle class and fitness culture suggest strong long-term potential for market expansion.

Middle East and Africa (MEA)

The Middle East and Africa collectively represent small share of the global protein bar market, with growth concentrated in the Gulf Cooperation Council (GCC) nations. The UAE and Saudi Arabia are leading the transformation, supported by high disposable incomes, government-backed health initiatives, and a youthful population. In Saudi Arabia, Vision 2030 includes a focus on reducing obesity and promoting physical activity, driving demand for performance nutrition. The number of health-conscious consumers has risen sharply. However, in sub-Saharan Africa, access remains limited due to low disposable income and underdeveloped retail infrastructure. Nigeria and South Africa are emerging as regional hubs, with local brands like Nuzone and PowerBar SA introducing affordable, fortified bars. The rise of online grocery platforms like Jumia and Noon is improving distribution. With increasing urbanization and digital health adoption, MEA is evolving into a fragmented yet strategically growing market for protein bar innovation.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a key role in the global protein bar market include Small Planet Foods, Inc., The WhiteWave Foods Company, The Kellogg Company, General Mills, Inc., Premier Nutrition Corporation, Caveman Foods LLC and MARS, Incorporated.

Competition in the protein bar market is intense and multifaceted, characterized by a blend of global corporations, regional specialists, and digitally native startups vying for consumer attention in a saturated yet growing sector. Established players like Clif Bar, Kellogg, and Nestlé compete on brand equity, distribution strength, and scientific validation, while challenger brands such as No Cow and RXBAR leverage niche positioning and clean-label appeal. The battleground spans product formulation, flavor innovation, packaging sustainability, and digital engagement, with differentiation increasingly dependent on authenticity and mission-driven branding. Retail shelf space is highly contested, prompting brands to invest heavily in in-store promotions and private-label alternatives. E-commerce has become a critical front, with Amazon, Shopify, and regional platforms enabling rapid scaling but also intensifying price competition. Consumer skepticism toward exaggerated health claims has elevated the importance of transparency, third-party testing, and ingredient traceability. Mergers and acquisitions, such as Post Holdings’ acquisition of Premier Nutrition, reflect consolidation to expand portfolio breadth. As consumer expectations shift from mere convenience to holistic wellness, competition is evolving beyond protein content to encompass taste, ethical sourcing, and personalized nutrition integration, making innovation and agility essential for sustained relevance.

TOP PLAYERS IN THE MARKET

Clif Bar & Company

Clif Bar has established a strong presence in the Asia Pacific protein bar market by positioning its products as performance and lifestyle staples for active consumers. The company’s flagship Clif Builder’s and Clif Energy bars are widely distributed in Australia, Japan, and South Korea through premium gyms, outdoor retailers, and e-commerce platforms. The company also launched region-specific marketing campaigns featuring local athletes and yoga influencers to resonate with culturally diverse fitness communities. Clif reinforced its sustainability credentials by introducing recyclable wrappers across its APAC portfolio and committing to carbon-neutral operations in the region by 2027. Additionally, it collaborated with sports nutritionists in New Zealand to develop educational content on fueling active lifestyles. By combining brand authenticity, environmental responsibility, and strategic retail partnerships, Clif Bar continues to strengthen its foothold in the rapidly evolving Asia Pacific market.

Kellogg Company (Premier Protein)

Kellogg’s Premier Protein brand has significantly expanded its footprint in the Asia Pacific region by leveraging its reputation for quality and scientific backing in sports nutrition. The brand entered key markets such as Australia, Singapore, and the Philippines with a focus on high-protein, low-sugar bars tailored to fitness-conscious consumers. In 2023, Kellogg launched a digital-first campaign in Japan emphasizing muscle health for aging populations, aligning with national wellness initiatives. It also introduced single-serve packs in convenience stores across Thailand and Malaysia to improve on-the-go accessibility. The company strengthened its e-commerce presence by listing Premier Protein bars on platforms like Lazada and Flipkart, supported by targeted social media advertising. Additionally, Kellogg partnered with fitness apps such as Fittr and Sweat to integrate its products into personalized nutrition plans. By combining clinical messaging with digital engagement and localized distribution, Kellogg is positioning Premier Protein as a trusted, science-led option in a competitive and fragmented market.

Nestlé (PowerBar, Carnation, and BOOST)

Nestlé has leveraged its extensive healthcare and nutrition portfolio to expand its protein bar offerings across Asia Pacific, particularly in Japan, China, and Australia. Through brands like PowerBar, historically associated with endurance sports, and Carnation Instant Breakfast bars, Nestlé targets both athletes and older adults seeking nutritional support. In 2023, the company introduced a new line of plant-based protein bars in Singapore under the PowerBar brand, formulated with pea and rice protein to cater to vegan and allergen-sensitive consumers. It also enhanced its hospital and pharmacy distribution network in South Korea to position protein bars as part of clinical nutrition pathways for recovery and aging. Nestlé invested in localized R&D at its Singapore Innovation Center to develop flavors such as matcha and red bean that align with regional palates. Furthermore, it collaborated with sports federations in Australia to sponsor marathons and triathlons, reinforcing brand visibility. By integrating performance, health, and cultural relevance, Nestlé is building a multifaceted presence in the Asia Pacific protein bar landscape.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the protein bar market are deploying a range of strategic initiatives to consolidate their market position, including product innovation, digital engagement, regional expansion, sustainability integration, and strategic partnerships. Companies are reformulating products to improve taste, texture, and nutritional profiles, with a focus on clean labels, plant-based proteins, and reduced sugar. Digital marketing and influencer collaborations are being leveraged to reach younger, health-conscious consumers on platforms like Instagram, TikTok, and fitness apps. Expansion into high-growth regions such as Asia Pacific and Latin America is being accelerated through localized distribution, flavor adaptation, and e-commerce optimization. Sustainability is a growing priority, with brands adopting recyclable packaging and carbon-neutral production claims to appeal to environmentally aware buyers. Strategic partnerships with gyms, sports organizations, and telehealth platforms are enhancing brand credibility and usage context. Additionally, companies are investing in direct-to-consumer models and subscription services to improve customer retention. These strategies collectively enable firms to differentiate in a crowded market, build long-term loyalty, and align with evolving consumer values around health, ethics, and convenience.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Clif Bar partnered with Cult.fit in India to offer exclusive Clif Builder’s bars at fitness centers and through the Cultsport app, enhancing direct access to health-conscious urban consumers.

- In March 2023, Kellogg launched a digital fitness campaign in Japan featuring local influencers, promoting Premier Protein bars as part of an active aging strategy to support muscle maintenance in adults over 50.

- In June 2023, Nestlé introduced a plant-based PowerBar variant in Singapore, formulated with pea and rice protein and packaged in recyclable materials, targeting environmentally conscious and vegan consumers.

- In September 2023, Quest Nutrition expanded its e-commerce presence in Australia by listing its protein bars on major platforms including Chemist Warehouse Online and Woolworths.com.au, improving nationwide accessibility.

- In April 2025, DynaTouch, a kiosk solutions provider, acquired KioWare, a kiosk management software company. This acquisition is anticipated to allow DynaTouch to offer more comprehensive kiosk solutions and strengthen their market presence.

MARKET SEGMENTATION

This research report on the global protein bar market has been segmented and sub-segmented based on product type, protein source, protein content and region.

By Product Type

- Energy Protein Bars

- Women's Protein Bar

- Meal Replacement Bars

- Low Carbohydrate Protein Bars

By Protein Source

- Plant Protein

- Animal Protein

By Protein Content

- Low

- Medium

- High

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What factors drive the growth of the protein bar market?

Factors driving market growth include increasing consumer health and fitness awareness, growing demand for convenient and nutritious snack options, rising interest in protein-rich diets, expanding product innovations, and the influence of social media and fitness trends.

2. What are the challenges facing the protein bar market?

Challenges include competition from other protein-rich snacks, consumer concerns about artificial ingredients, sugar content, and taste preferences, regulatory considerations related to labeling and health claims, and the need for continuous product differentiation and innovation.

3. What are the key ingredients typically found in protein bars?

Protein bars typically contain protein sources such as whey, soy, pea, or other plant-based proteins. Depending on the specific product and target audience, they may also include carbohydrates, fats, fibers, vitamins, and minerals.

4. Which regions lead the global protein bar market?

North America dominates, while Asia-Pacific is showing rapid growth.

5. Who are the key players in the protein bar market?

Major brands include Clif Bar, Quest Nutrition, RXBAR, Optimum Nutrition, and Kind LLC.

6. What types of protein bars are available?

Whey-based, plant-based, dairy-free, gluten-free, and low-carb bars.

7. Which consumer segments buy protein bars the most?

Athletes, gym-goers, busy professionals, and health-conscious consumers.

8. How does e-commerce influence protein bar sales?

Online channels expand product variety and enable direct-to-consumer sales.

9. What challenges does the protein bar market face?

High competition, pricing pressure, and sugar content concerns.

10. How are companies innovating in the protein bar space?

New flavors, functional ingredients, and sustainable packaging solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com