Global Textile Home Decor Market Size, Share, Trends & Growth Forecast Report By Product (Bed linen and Bedspread, Floor Coverings, Kitchen and Dining Linen, Bath/Toilet Linen, Upholstery, and Others), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail Stores, and Others), and Region (North America, Europe, APAC, Latin America, Middle East, and Africa) – Industry Analysis From 2026 to 2034

Market Size, 2025

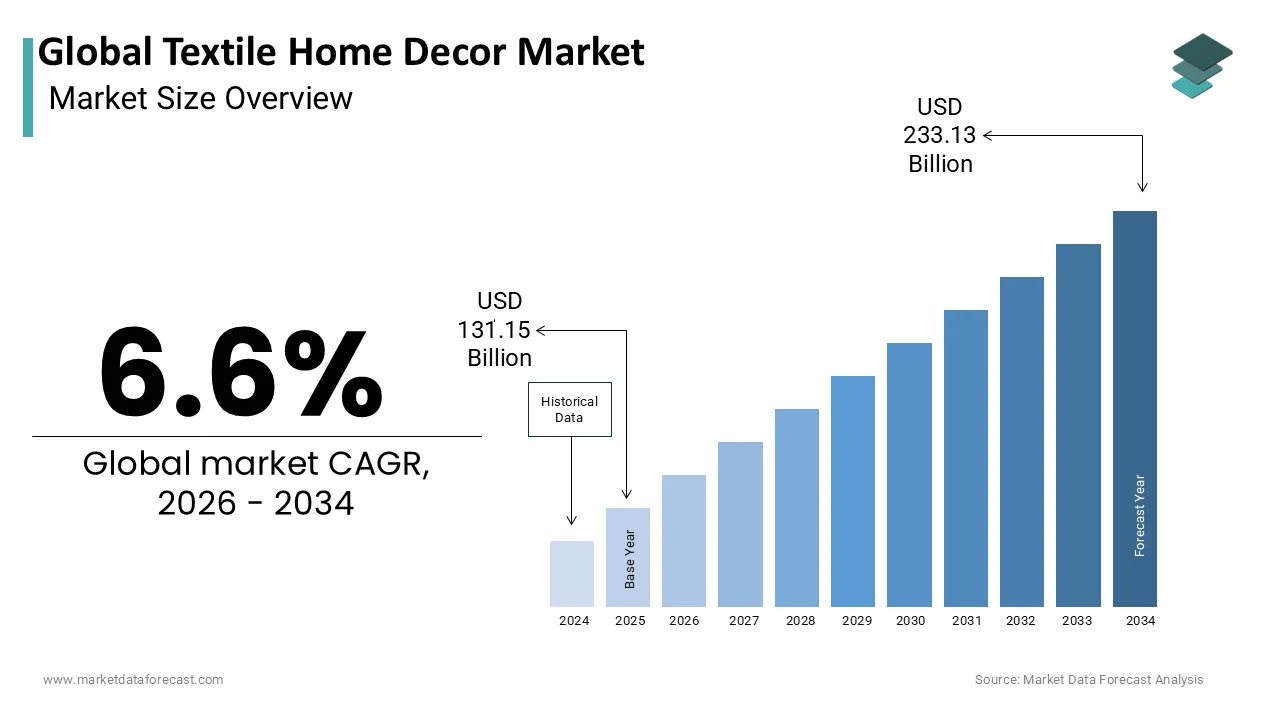

$131.15 BnMarket Estimate, 2026

$139.81 BnMarket Forecast, 2034

$233.13 BnCAGR, 2026–2034

6.6%Global Textile Home Decor Market Size

The global textile home decor market was valued at USD 131.15 billion in 2025, is expected to have a 6.6% CAGR from 2026 to 2034, and be worth USD 233.13 billion by 2034 from USD 139.81 billion in 2026.

Textile home decor refers to the use of woven, knitted, or synthetic fabrics to style, soften, and enhance the interior atmosphere of a living space. It acts as the perfect union of aesthetic design and everyday functionality, adding color, pattern, texture, and comfort to your home. This market represents the intersection of traditional craftsmanship and contemporary design trends, where materials such as cotto,n lin, en si, lk, and synthetic blends are transformed into decorative elements that define living environments. The market is deeply influenced by cultural preferences, seasonal trends, and evolving lifestyle choices that dictate consumer purchasing behavior across different regions. In Europe, the appreciation for high-quality textiles remains strong, with consumers increasingly valuing sustainability and ethical production methods alongside visual appeal. According to private market research, consumer interest in eco-friendly interior options is driving a steady expansion in the European sustainable home furniture market, though official Eurostat data focuses strictly on total household expenditure volumes. The global textile industry employs over 60 million people, according to the International Labour Organization,n highlighting the socioeconomic importance of this sector. Furthermore, ore the rise of remote work has led to increased investment in home office aesthetics. As per sources, remote work shifts since 2020 triggered a notable surge in household spending on interior updates, with European consumption of home textiles rising even as clothing sales fell. This transformation underscores how textile home decor has evolved from mere utility to a critical component of personal expression and well-being in modern living spaces.

MARKET DRIVERS

Rising Consumer Preference for Sustainable and Eco-Friendly Materials Drives Market Growth.

The escalating demand for sustainable and eco-friendly textile products is driving the growth in the textile home decor market. Consumers are increasingly aware of the environmental impact of their purchases, leading to a pronounced shift toward organic cotton, recycled polyester, and naturally dyed fabrics. According to European Commission Eurobarometer surveys, a significant portion of EU consumers value sustainability. This trend is further reinforced by stringent regulatory frameworks such as the European Green Deal, which mandates higher sustainability standards across all manufacturing sectors. Brands that adopt transparent supply chains and utilize biodegradable materials gain a significant competitive advantage. Additionally, the millennial and Generation Z demographics demonstrate a strong preference for brands that align with their environmental values. This demographic shift compels manufacturers to innovate with circular economy models, including take-back programs and upcycling initiatives. The integration of blockchain technology for traceability has also gained traction. These developments indicate that sustainability is no longer a niche preference but a fundamental driver shaping the future trajectory of the textile home decor market.

Increasing Urbanization and Residential Construction Activities Fuel Demand for Home Textiles

The rapid pace of urbanization, coupled with robust residential construction activities, creates substantial demand for textile home decor products across developed and emerging regions, which contributes to the expansion of the textile home decor market. As more individuals migrate to urban centers, the need for furnished living spaces intensifies, driving sales of ready-to-use home textile solutions. According to the United Nations Department of Economic and Social Affairs, the global urban population is projected to reach 68% by 2050, with Europe's urbanization rate expected to exceed 83%. This demographic transition necessitates the development of new housing units. Each new household represents a potential customer base for essential textile items such as curtains, bedding, and rugs. Moreover, the trend toward smaller urban apartments has spurred innovation in multifunctional and space-saving textile designs that maximize utility without compromising aesthetics. Real estate developers increasingly partner with home decor brands to offer staged interiors featuring coordinated textile collections, which influences buyer preferences and accelerates product adoption. The rental market also contributes significantly. This continuous cycle of occupancy and renovation ensures steady demand for textile home decor products, making urbanization a critical structural driver for market expansion.

MARKET RESTRAINTS

Volatility in Raw Material Prices Constricts Profit Margins for Manufacturers

Fluctuating prices of key raw materials such as cotton wool and synthetic fibers are impeding the growth of the textile home decor market. This creates uncertainty in production costs and pricing strategies. According to the International Cotton Advisory Committee (ICAC), the 2022 cotton market faced high volatility driven by a production deficit, where global consumption exceeded production by over 1 million tonnes. Such volatility directly impacts manufacturers who struggle to maintain consistent profit margins while remaining competitive in price-sensitive markets. Synthetic fibers derived from petroleum are equally susceptible to energy price fluctuations, with crude oil prices varying by 40 percent within a single year,r according to the International Energy Agency. These unpredictable cost structures force companies to either absorb losses or pass increased expenses to consumers, rs which can dampen demand,d particularly during economic downturns. Small and medium-sized enterprises are disproportionately affected as they lack the financial reserves and hedging capabilities of larger corporations. A 2022 survey by the European Textile Confederation (EURATEX) revealed that 96% of companies anticipated a drop in sales, with soaring energy costs threatening the viability of many manufacturers. Furthermore, the reliance on imported raw materials exposes European manufacturers to currency exchange risks and trade policy changes, adding another layer of complexity to cost management. Raw material price volatility will continue to constrain market growth and limit investment in innovation. This situation will persist until more stable sourcing mechanisms or alternative materials become widely available.

Stringent Environmental Regulations Increase Compliance Costs for Industry Players

The implementation of increasingly stringent environmental regulations is also a major hurdle for manufacturers, as it imposes additional compliance costs and operational complexities, which slow down the expansion of the textile home decor market. The EU Strategy for Sustainable and Circular Textiles sets a vision that by 2030, all textile products placed on the EU market must be durable, repairable, and recyclable, a goal legally enforced through the Ecodesign for Sustainable Products Regulation (ESPR). Compliance with these requirements necessitates significant investments in the research and development process, redesign,n and certification procedures. According to industry estimates regarding Digital Product Passports (DPP), implementation costs can range from €15,000 to €50,000 for standard SME solutions, while highly customized systems for large enterprises may reach €500,000. These financial burdens are particularly challenging for smaller players who operate on thin margins and lack access to substantial capital resources. Additionally, ly the REACH regulation restricts the use of certain hazardous chemicals in textile production, requiring manufacturers to reformulate dyes and finishes, which often results in higher production costs and extended lead times. The Chemical Industries Association highlights that high regulatory and energy costs have severely impacted the chemical sector's competitiveness, with many firms facing rising operational expenses. The complexity of navigating varying regulatory frameworks across different countries further complicates international trade and market entry strategies. These regulations aim to promote sustainability; however, they inadvertently create barriers to entry and slow product innovation. As a result, they restrain overall market dynamism and competitiveness.

MARKET OPPORTUNITIES

Expansion of E-Commerce Platforms Creates New Avenues for Market Penetration

The rapid expansion of e-commerce platforms creates a pathway for brands to reach broader audiences and enhance customer engagement through digital channels, which propels the growth of the textile home decor market. Online retail sales of home furnishings in Europe grew steadily in 2023, with regional e-commerce trade reporting a resilient 6.21% uptick in total value despite widespread inflation. Digital platforms enable manufacturers to bypass traditional distribution intermediaries, thereby reducing costs and improving profit margins while offering competitive pricing to consumers. Advanced technologies such as augmented reality allow customers to visualize textile products in their own spaces before purchasing, which significantly reduces return rates and enhances satisfaction levels. Major online marketplaces report that products utilizing immersive 3D space visualization and augmented reality tools experience an average 30% higher conversion rate compared to standard text-and-image listings. Furthermore, social media integration facilitates targeted marketing campaigns that leverage user-generated content and influencer partnerships to build brand loyalty and drive sales. The direct-to-consumer model, empowered by e-commerce, enables brands to collect valuable customer data, which informs product development and personalized marketing strategies. Emerging markets in Eastern Europe show strong long-term expansion potential as internet penetration averages 92%–95%, though actual online purchasing activity lags significantly behind Western European baselines. Capitalizing on modern transformative trends requires textile home decor companies to embrace robust digital infrastructure and omnichannel retail. This strategic investment allows them to grow their market presence while fostering long-term loyalty with consumers.

Growing Trend of Personalization and Custom-Made Home Textiles Opens Premium Segments

The increasing consumer desire for personalized and custom-made home textile products offers a lucrative opportunity for manufacturers to differentiate themselves and capture premium market segments within the home textile decor market. Modern consumers view home decor as an extension of their identity, leading to heightened demand for bespoke items that reflect individual tastes and spatial requirements. According to interior design consumer trend mappings, modern buyers show an increasing desire for unique identities in their home decor, spurring demand for custom and made-to-measure textile items. Advances in digital printing technology have made small batch production economically viable, enabling brands to offer extensive customization options without prohibitive cost increases. Companies utilizing automated cutting and sewing systems can reduce lead times for custom orders from several weeks to just a few days,s enhancing customer satisfaction. The luxury segment particularly benefits from this trend with high-net-worth individuals seeking exclusive designs and premium materials that convey status and sophistication. Collaborations between textile manufacturers and interior designers further amplify this opportunity by creating limited edition collections that appeal to discerning clientele. Additionally, the rise of online configurators allows customers to design their own products, selecting from various fabrics, colors, and patterns, which enhances engagement and emotional connection to the brand. Personalization has become a key differentiator in today's crowded marketplace. Because of this, textile home decor companies that invest in flexible manufacturing and customer-centric design tools are well-positioned to thrive.

MARKET CHALLENGES

Intense Competition from Low-Cost Imports Undermines Local Manufacturing Viability

Intense competition from low-cost Asian imports is a serious constraint for the textile home decor market. This massive influx directly threatens the survival of local European producers. Countries such as China, India, and Bangladesh benefit from lower labor costs, economies of scale, and an established supply chain, enabling them to offer products at prices that European manufacturers struggle to match. According to European market value chain analyses, imports from Asian manufacturing hubs have grown substantially over the last two decades, creating fierce competitive pricing pressure for local textile brands. This influx of inexpensive goods forces local companies to compete primarily on price rather than quality or innovation, eroding profit margins and limiting investment in sustainable practices. Small and medium-sized enterprises are particularly vulnerable as they lack the resources to achieve similar cost efficiencies or engage in aggressive marketing campaigns. The disparity in production costs is further exacerbated by differing environmental and labor standards, with some importing countries having less stringent regulations that reduce compliance expenses. Reports by industrial confederations indicate that European textile manufacturers have suffered structural pressure, with soaring energy and utility expenses heavily impacting domestic mill operations. While trade defense instruments exist, st they often prove insufficient in addressing the sheer volume and pricing advantages of imported goods. This competitive imbalance threatens the long-term sustainability of the European textile home decor industry and necessitates strategic interventions to support local innovation and value addition.

Supply Chain Disruptions and Logistical Bottlenecks Impede Timely Product Delivery

Persistent supply chain disruptions and logistical barriers are negatively impacting the textile home decor market. This impedes timely product delivery and increases operational uncertainties. Geopolitical re-routing across key maritime routes has periodically extended ocean freight transit timelines, requiring brands to expand lead times for seasonal interior shipments. These delays disrupt inventory management, forcing retailers to hold higher stock levels, which ties up capital and increases warehousing costs. The textile industry’s reliance on complex global supply chains involving multiple stages from raw material sourcing to finished product distribution makes it particularly susceptible to disruptions at any point in the process. Port congestion, container shortages, and fluctuating freight rates further compound these issues, with ocean freight costs varying by up to 300 percent during peak disruption periods, as reported by Drewry Maritime Research. European manufacturers face additional challenges due to their dependence on imported raw materials and components, which are subject to customs clearance delays and regulatory inspections. According to global logistics and supply chain trackers, international freight turbulence has intermittently caused significant delays in retail inventory arrivals, causing retail stockouts. The lack of visibility and predictability in supply chains hinders effective planning and responsiveness to market demands. Logistical challenges will continue to constrain market efficiency and growth potential. The only solution is to establish more resilient and localized supply networks.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Distribution Channel, and Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Market Leaders Profiled | Mannington Mills, Inc (U.S.), Companhia de Tecidos Norte de Minas (Brazil), Kurlon (India), American Textile Company. (U.S.), Leggett & Platt, Incorporated (U.S.), Nitori Holdings Co., Ltd. (Japan), Williams-Sonoma Inc. (U.S.), MOHAWK INDUSTRIES, INC. (U.S.), American Signature, Inc. (U.S.), Bombay Dyeing (India), Vescom B.V. (Netherlands), MITTAL INTERNATIONAL (India), Kimball International Inc. (U.S.) |

SEGMENTAL ANALYSIS

By Product Type Insights

The bedding and linens segment was the largest in the textile home decor market and occupied a 35.1% share in 2025. This prominence of the segment was supported by its fundamental role in daily living and high replacement frequency. Also, this category includes sheets, pillowcases d, duvets, nd mattress protectors, which are considered essential household items rather than discretionary purchases. The dominance of this segment is also driven by hygiene consciousness and the need for regular renewal, with consumers typically replacing bed linens every two to three years. According to private consumer retail tracking, household purchases of bedding sets fluctuate based on economic health, with the average consumer replacing linens every 3 to 5 years rather than on a strict biennial cycle. The proliferation of hospitality industries further amplifies this demand as hotels and short-term rental properties require large volumes of durable and aesthetically pleasing linens. As per hospitality procurement standards tracked by HOTREC, hotels maintain continuous inventory rotation models, replacing individual damaged linens as needed rather than discarding an entire property's stock simultaneously. Additionally, driven by post-pandemic wellness trends, market analysis indicates steady growth in the global hypoallergenic and antimicrobial textile sector, though official ISPA reports focus strictly on mattress and foundation wholesale metrics. The integration of smart textiles featuring temperature regulation and moisture-wicking properties also attracts tech-savvy consumers willing to pay premium prices. These factors combined ensure that bedding and linens remain the cornerstone of the textile home decor market, providing stable revenue streams for manufacturers and retailers alike.

On the other hand, the rugs and carpets segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 6.8% between 2026 and 2034. This accelerated growth of the segment is primarily fueled by evolving interior design trends that emphasize floor coverings as central aesthetic elements rather than mere functional accessories. Contemporary design philosophies encourage layering textures and patterns, making rugs pivotal in defining spatial zones within open-plan living areas. According to residential renovation market surveys, soft furnishings like area rugs are increasingly used to optimize acoustic comfort in homes featuring hard surface flooring, though no centralized pan-European design federation tracks these exact project percentages. The availability of diverse materials ranging from traditional wool to innovative recycled synthetics allows consumers to align purchases with sustainability goals and budget constraints. Customization options have also expanded with digital printing technology,s enabling bespoke designs that cater to individual preferences. The commercial sector contributes significantly to this growth as offices and retail spaces increasingly use branded carpets to reinforce corporate identity and improve employee well-being. Furthermore, the ease of online purchasing and virtual visualization tools has reduced barriers to entry, allowing consumers to experiment with bold patterns and colors confidently. These dynamics position rugs and carpets as the most dynamic growth engine within the textile home decor landscape.

By Material Type Insights

In 2025, the synthetic fibers segment held the majority share of 37.2% of the textile home decor market because of its superior cost efficiency, durability, and versatility. These materials offer significant advantages over natural fibers in terms of resistance to stains, fading, and wear, making them ideal for high-traffic areas and households with children or pets. According to data compiled by the Textile Exchange, synthetic materials represent approximately 64% of the global fiber market, highlighting their massive scale across commercial home furnishing lines. The manufacturing processes for synthetic materials are highly scalable, allowing producers to meet large volume demands consistently while maintaining competitive pricing structures. Polyester in particular dominates this category due to its ability to mimic the look and feel of natural fabrics like silk and cotton at a fraction of the cost. Advances in polymer technology have also enhanced the environmental profile of synthetics. This shift addresses consumer concerns about plastic waste while preserving the performance benefits of synthetic materials. Additionally, our synthetic fibers require less water and energy during production compared to cotton cultivation, aligning with broader sustainability initiatives. The combination of affordability, its low maintenance requirements, and improving eco credentials ensures that synthetic fibers remain the material of choice for mass market textile home decor products.

However, the natural fibers segment is expected to exhibit a noteworthy CAGR of 7.2% over the forecast period due to heightened consumer preference for sustainable and biodegradable materials. This segment benefits from the global movement toward ethical consumption, where buyers prioritize transparency and environmental responsibility in their purchasing decisions. Cotton remains the most popular natural fiber due to its breathability,y softness, and ease of care. According to Textile Exchange market indicators, the certified organic cotton sector continues to expand steadily with a multi-year projected market value growth rate of roughly 7.6% annually. Linen is also gaining traction, particularly in European markets where its rustic aesthetic and exceptional durability resonate with contemporary design trends. The Alliance for European Flax-Linen & Hemp reports that while European flax cultivation acreage has more than doubled over the past decade, actual annual fiber yields remain highly subject to weather volatility. Wool is valued for its insulating properties and luxurious texture, making it a preferred choice for rugs and throws in colder climates. Consumers are increasingly willing to pay premium prices for certified natural fibers that guarantee fair labor practices and minimal chemical usage. Certification schemes such as GOTS and Oeko-Tex assure quality and sustainability, further boosting consumer confidence. As awareness of the environmental impact of synthetic materials grows, the demand for natural alternatives continues to accelerate, positioning this segment as the primary beneficiary of the green transition in home furnishings.

By Distribution Channel Insights

The brick-and-mortar stores segment continued to dominate the textile home decor market and accounted for a 65.6% share in 2025. They achieve this by offering tangible shopping experiences and immediate product availability. Despite the rise of e-commerce, physical stores remain crucial for customers who wish to assess fabric texture, re-color accuracy, and overall quality before making purchases. According to research, brick-and-mortar storefronts continue to secure the majority of home product transactions, as consumers value tactile evaluation before buying home textiles. Department stores leverage their established brand reputation and extensive floor space to showcase coordinated collections that inspire customers and drive incremental sales. The ability to provide personalized assistance from knowledgeable staff enhances customer satisfaction and builds loyalty,oyalty particularly for high-value items such as custom curtains and upholstery. Furthermore, physical retailers offer immediate gratification by allowing customers to take products home instantly, which is appealing for uneeds or last-minutenuteee decorating projects. Promotional events and seasonal displays in stores create immersive shopping environments that stimulate impulse buys and increase basket sizes. Many brick-and-mortar retailers have also integrated omnichannel strategies, such as click and collect services, which combine the convenience of online browsing with the reliability of physical pickup. This hybrid approach strengthens the position of physical stores by addressing modern consumer expectations for flexibility and speed while preserving the tactile advantages that define the textile shopping experience.

On the contrary, the online retailers segment is predicted to witness the highest CAGR of 9.5% from 2026 to 2034, owing to digital convenience, extensive product selection, and competitive pricing. The proliferation of smartphones and high-speed internet has made online shopping accessible to a broader demographic, enabling consumers to browse thousands of products from the comfort of their homes. Advanced features such as augmented reality allow customers to visualize how fabrics and patterns will look in their specific spaces, reducing uncertainty and return rates. Major online platforms invest heavily in logistics infrastructure, ensuring fast and reliable delivery, which enhances customer trust and repeat purchases. The direct-to-consumer model eliminates intermediaries, allowing brands to offer lower prices and exclusive deals that attract price-sensitive shoppers. Social media integration facilitates discovery and inspiration with influencer endorsements and user-generated content, driving traffic to online stores. Additionally, online retailers leverage data analytics to personalize recommendations and marketing messages, thereby increasing conversion rates and customer lifetime value. The ability to operate without geographical constraints enables online players to reach niche markets and underserved regions, expanding their customer base rapidly. These technological and operational advantages position online retailers as the primary engine of distribution growth in the textile home decor sector.

COUNTRY LEVEL ANALYSIS

North America Textile Home Decor Market Analysis

North America was positioned second in the global textile home decor market and captured a 28.5% share in 2025. This growth of the North American market was fuelled by high disposable income levels and robust residential renovation activities. The United States serves as the primary contributor within this region, with consumers demonstrating a strong willingness to invest in premium home furnishings that reflect personal style and comfort. The prevalence of single-family homes with larger living spaces creates greater demand for window treatments, rugs, and upholstery compared to densely populated regions. Cultural emphasis on hospitality and frequent home entertaining further stimulates purchases of decorative textiles that enhance aesthetic appeal. The presence of major retail chains and established e-commerce platforms ensures wide product availability and competitive pricing. Additionally, the trend toward smart homes has influenced textile choices with consumers seeking fabrics that complement integrated technology and modern design aesthetics. Trade policies favoring domestic production have also supported local manufacturers,s although imports from Asia remain significant. The mature nature of the North American market means growth is driven primarily by replacement cycles and upgrades rather than new household formation. Nevertheless, ss the continuous innovation in sustainable materials and digital retail experiences keeps the region at the forefront of global market developments.

Europe Textile Home Decor Market Analysis

Europe plays a major role in the global textile home decor market due to its rich heritage in textile craftsmanship and leadership in sustainability standards. Countries such as Italy, France,e and Germany are renowned for high-quality production and innovative design, influencing global trends and consumer preferences. However, according to EURATEX and Eurostat data, EU textile and clothing trade decreased by 13% in 2023, reflecting a slowdown in demand rather than a vibrant expansion. European consumers are highly discerning, prioritizing durability,y ethical sourcing, and environmental certifications when making purchasing decisions. The European Green Deal has accelerated the adoption of circular economy principles, with many brands implementing take-back schemes and using recycled materials. Northern European countries lead in minimalist and functional design, while Southern Europe excels in luxury and ornate style, creating a diverse market landscape. The region benefits from well-developed retail infrastructure, including specialized boutiques, department stores, and robust online platforms. Government support for artisanal industries helps preserve traditional techniques while fostering innovation in modern applications. Tourism also plays a role, as visitors often purchase local textiles as souvenirs, supporting small businesses and regional economies. Although faced with competition from low-cost imports, Europe retains its premium positioning through quality differentiation and strong brand equity.

Asia Pacific Textile Home Decor Market Analysis

Asia Pacific was the top performer in the global textile home decor market and accounted for a 35.8% share in 2025. China, India, and Vietnam serve as manufacturing hubs, leveraging low labor costs and established supply chains to produce vast quantities of home textiles for domestic and export markets. According to OECD and Brookings Institution projections, the global middle class, led by Asia, is expected to reach 3.5 billion people by 2030, creating potential demand for consumer goods. Urbanization rates in countries such as Indonesia, the Philippines, and Thailand are accelerating, leading to increased construction of residential complexes that require interior furnishing. Rising disposable incomes enable consumers to upgrade from necessities to decorative and premium textile products. E-commerce penetration is expanding rapidly, with platforms like Alibaba and Lazada facilitating access to diverse product ranges. Local manufacturers are increasingly focusing on branding and design innovation to capture higher value segments rather than competing solely on price. Government initiatives promoting domestic consumption and infrastructure development further support market growth. Cultural festivals and traditions involving home decoration also contribute to seasonal spikes in demand. While the region faces challenges related to environmental regulations and labor standards, due to its sheer scale and dynamic economic growth,th it positionsitself ass the most influential force in the global textile home decor industry.

Latin America Textile Home Decor Market Analysis

Latin America is an emerging player in the textile home decor market, owing to sustained urban expansion and rising middle-class aspirations. Brazil and Mexico represent the largest markets within the region, benefiting from relatively industrialized economies and established retail networks. Urban migration continues to drive demand for affordable and functional textile products as new residents furnish apartments and smaller living spaces. The region has a strong cultural appreciation for vibrant colors and patterns, influencing local design preferences and product offerings. Local manufacturers compete with imports from Asia and North America, striving to balance quality and affordability. E-commerce is gaining traction, although logistical challenges and limited banking infrastructure hinder widespread adoption in rural areas. Political instability and currency fluctuations create uncertainty for investors and retailers, affecting inventory planning and pricing strategies. Nevertheless,s the youthful demographic profile and increasing connectivity suggest long-term growth opportunities. Brands that offer flexible payment options and localized designs are better positioned to succeed in this complex market. Sustainability awareness is gradually increasing, prompting some companies to explore eco-friendly materials, although price sensitivity remains a dominant factor in purchasing decisions.

Middle East and Africa Textile Home Decor Market Analysis

The Middle East and Africa region is predicted to expand notably in the textile home decor market during the forecast period due to luxury demand in Gulf states and infrastructure development in emerging African economies. Countries such as the United Arab Emirates, Saudi Arabia, and Qatar exhibit strong demand for high-end textiles due to affluent populations and ambitious construction projects, including hotels and residential towers. According to industry market analysis, the GCC luxury furniture market is projected to see growth. The hospitality sector is a key driver with new hotels requiring extensive quantities of bespoke curtains b, bedding, and carpets. In Africa, rapid urbanization in nations like Nigeria, Kenya, and South Africa is creating a nascent but growing market for affordable home textiles. Limited local manufacturing capacity means reliance on imports primarily from Asia and Europe. Challenges include inconsistent electricity supply, logistical bottlenecks, and varying regulatory environments across countries. However, increasing mobile phone penetration and digital payment solutions are facilitating e-commerce growth. Cultural preferences for rich textures and intricate designs influence product selection, requiring suppliers to adapt their offerings. While the overall market size remains smaller compared to other regions, the high-value nature of transactions in the Middle East and the untapped potential in Africa make this region an attractive frontier for strategic expansion.

COMPETITIVE LANDSCAPE

The competition in the textile home decor market is characterized by intense rivalry among established multinational corporations and emerging regional players who vie for consumer attention through differentiation and innovation. Market participants face pressure to balance cost efficiency with high-quality standards while adhering to stringent environmental regulations. The fragmentation of the industry allows niche brands to thrive by focusing on specific segments, such as luxury bespoke items or sustainable, eco-friendly collections. Price competition remains fierce, particularly in the mass market segment, where low-cost imports from Asia exert significant downward pressure on margins. Established companies leverage their brand equity, extensive distribution networks, and economies of scale to maintain leadership positions. However, agile startups disrupt traditional models by utilizing direct-to-consumer channels and social media marketing to build loyal communities. Technological advancements in digital printing and smart textiles create new battlegrounds for innovation where companies must continuously invest to stay relevant. The threat of substitution from alternative materials and changing consumer tastes further complicates the competitive landscape, requiring constant adaptation and strategic foresight from all industry participants to sustain profitability and growth.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Global Home Furnishings Market include

- Mannington Mills, Inc. (U.S.)

- Companhia de Tecidos Norte de Minas (Coteminas) (Brazil)

- Kurlon Enterprise Ltd. (India)

- American Textile Company (U.S.)

- Leggett & Platt, Incorporated (U.S.)

- Nitori Holdings Co., Ltd. (Japan)

- Williams-Sonoma, Inc. (U.S.)

- Mohawk Industries, Inc. (U.S.)

- American Signature, Inc. (U.S.)

- Bombay Dyeing & Manufacturing Company Limited (India)

- Vescom B.V. (Netherlands)

- Mittal International (India)

- Kimball International, Inc. (U.S.)

TOP LEADING PLAYERS IN THE MARKET

- Mohawk Industries stands as a dominant force in the global textile home decor sector with extensive manufacturing capabilities and a diverse product portfolio. The company produces high-quality carpets, rugs, and upholstery fabrics that cater to both residential and commercial segments worldwide. Mohawk has recently focused on sustainability by investing in recycling technologies and developing eco-friendly fiber solutions. Their acquisition of various regional brands has expanded their geographic reach and distribution network significantly. The company leverages advanced digital printing techniques to offer customized designs that meet evolving consumer preferences. By integrating vertical supply chain operations, Mohawk ensures cost efficiency and consistent product quality. Their commitment to innovation is evident in the launch of smart textile products that enhance durability and aesthetic appeal. Strategic partnerships with interior designers and retailers further strengthen their market presence and brand visibility across key global regions.

- Welspun India Limited is a leading global player specializing in hotextilesile,s includintowelssel,s bed linen,s and rug,s with a strong emphasis on innovation and sustainability. The company serves major international retailers and hospitality chains through its robust manufacturing infrastructure and design capabilities. Welspun has invested heavily in digital transformation using artificial intelligence and data analytics to optimize production and enhance customer experience. Their recent initiatives include launching proprietary technologies for antimicrobial and moisture-wicking fabrics that address health-conscious consumer needs. The company actively promotes circular economy practices by incorporating recycled materials into its product lines. Welspun’s strategic focus on direct-to-consumer channels has enabled it to build stronger brand loyalty and capture higher margins. Collaborations with global fashion houses have elevated its design profile and attracted premium clientele seeking unique and stylish home decor solutions.

- Tate & Lyle PLC contributes significantly to the textile home decor market through its specialized ingredients and functional solutions that enhance fabric performance and sustainability. Although primarily known for food ingredients, the company has expanded into textile applications by providing bio-based polymers and finishing agents. These innovations help manufacturers create durable, stain-resistant,t and eco-friendly textiles that align with modern environmental standards. Tate & Lyle has recently partnered with textile producers to develop biodegradable fibers that reduce plastic waste in home furnishings. Their research and development efforts focus on improving the tactile qualities and longevity of natural and synthetic blends. By offering technical expertise and sustainable alternatives, Tate & Lyle supports brands in meeting regulatory requirements and consumer expectations. This strategic diversification strengthens their position as a key enabler of innovation within the global textile home decor supply chain and industry value network.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the textile home decor market primarily employ product innovation and sustainability integration to maintain a competitive advantage. Companies invest heavily in research and development to create eco-friendly materials such as organic cotton and recycled polyester that appeal to environmentally conscious consumers. Strategic acquisitions and mergers allow firms to expand their geographic footprint and diversify product offerings efficiently. Digital transformation is another critical strategy with businesses leveraging e-commerce platforms, augmented reality, and data analytics to enhance customer engagement and streamline operations. Partnerships with interior designers and influencers help brands reach targeted audiences and build credibility through authentic endorsements. Vertical integration enables manufacturers to control supply chains, reduce costs,s and ensure consistent quality from raw material sourcing to final delivery. Customization services are increasingly offered to meet individual consumer preferences and differentiate products in a saturated marketplace. These combined strategies foster resilience, adaptability, and long-term growth in a dynamic global environment.

RECENT HAPPENINGS IN THE MARKET

- In 2025, Kroger acquired Bed Bath & Beyond to create a new online marketplace. This partnership allows both companies to expand their offerings on Kroger's Ship marketplace by including products from Bed Bath & Beyond and Buybuy Baby. Customers can now find storage, bedding, and baby furniture from these brands. Kroger shoppers will also have access to Bed Bath & Beyond's store brands and popular national brands.

- Also, in 2025, Kimball International Inc., a company specializing in commercial furniture, announced plans to enhance its warehousing operations. They intend to build a 220,000-square-foot warehouse at their industrial complex in Dubois County.

MARKET SEGMENTATION

This research report on the global textile home decor market has been segmented and sub-segmented based on product type, distribution channel, and region.

By Product Type

- Bed linen and Bedspread

- Floor Coverings

- Kitchen and Dining Linen

- Bath/Toilet Linen

- Upholstery

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail Stores

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the size of the textile home decor market?

The textile home decor market is expected to reach USD 175.53 billion by 2028, which is USD 105.27 billion in 2022.

Who are the key market players in the textile home decor market?

Mannington Mills, Inc (U.S.), Companhia de Tecidos Norte de Minas (Brazil), Kurlon (India), American Textile Company. (U.S.), Leggett & Platt, Incorporated (U.S.), Nitori Holdings Co., Ltd. (Japan), etc.

Which region dominates the textile home decor market?

North America dominates the textile home decor market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com