UK Tea Market Size, Share, Trends & Growth Forecast Report By Type, Packaging, End User, Price Point, Distribution Channel, and Country – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

$3.52 BnMarket Estimate, 2026

$3.74 BnMarket Forecast, 2034

$6.09 BnCAGR, 2026–2034

6.28%UK Tea Market Report Summary

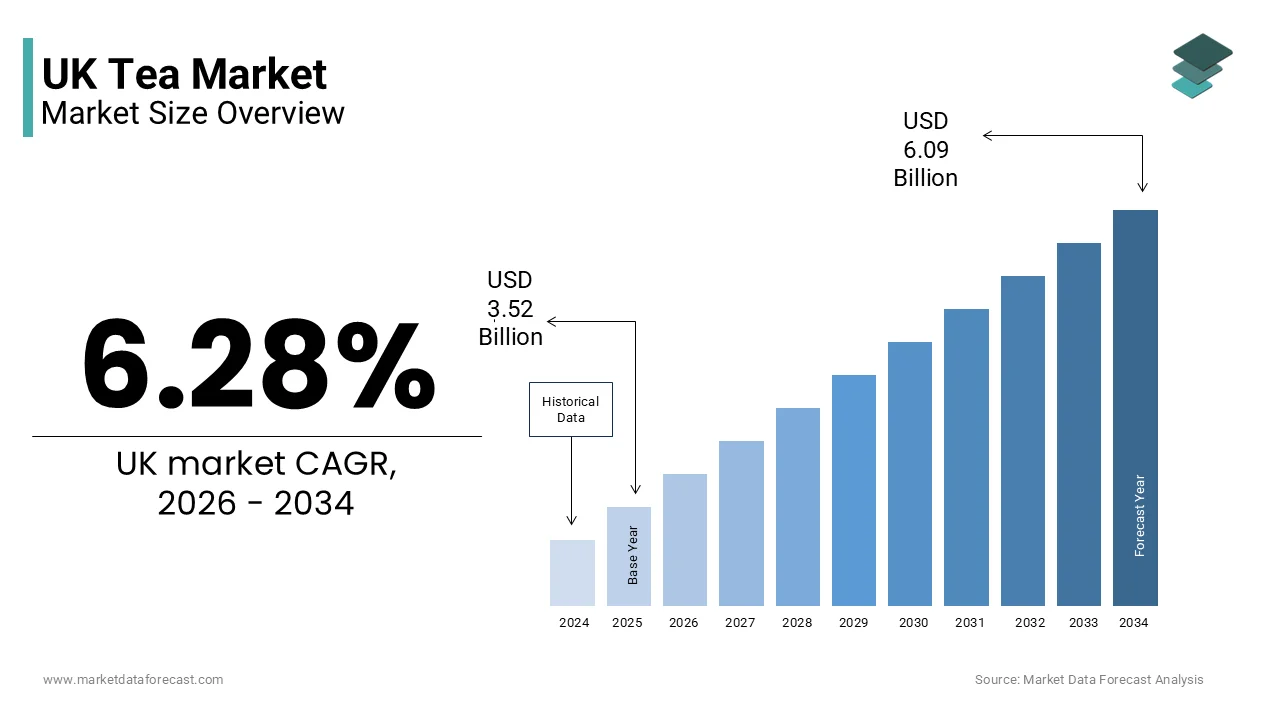

The UK tea market was valued at USD 3.52 billion in 2025, is estimated to reach USD 3.74 billion in 2026, and is projected to reach USD 6.09 billion by 2034, growing at a CAGR of 6.28% during the forecast period. Market growth is driven by the United Kingdom's strong tea drinking culture, increasing demand for premium and specialty tea products, and growing consumer interest in health and wellness beverages. Rising popularity of herbal, functional, and organic tea varieties, along with continuous product innovation, is further supporting market expansion across the country.

Key Market Trends

- Growing consumer demand for premium and specialty tea products is driving market growth.

- Increasing popularity of herbal, wellness, and functional teas is boosting market expansion.

- Rising interest in sustainable and ethically sourced tea products is supporting industry development.

- Expansion of flavored and organic tea offerings is enhancing market opportunities.

- Innovation in packaging formats and ready to drink tea products is influencing market advancement.

Segmental Insights

- Based on type, the black tea segment accounted for 45.6% of the UK tea market share in 2025. This dominance is attributed to the country's long established tea consumption habits and strong consumer preference for traditional black tea varieties.

- Based on packaging, the tea bags segment held a substantial share of the UK tea market in 2025 due to convenience, ease of preparation, and widespread household adoption.

- Based on end user, the residential segment accounted for the largest share of the UK tea market in 2025, driven by high daily tea consumption across households.

- Based on distribution channel, the supermarkets and hypermarkets segment held 44.3% of the UK tea market share in 2025, supported by extensive product availability, promotional activities, and strong retail penetration.

Regional Insights

- The United Kingdom accounted for 25.5% of the European tea market share in 2025 and maintained its position as the leading tea market in the region. Strong cultural affinity toward tea consumption, premium product demand, and continuous innovation continue to support market growth.

Competitive Landscape

The UK tea market is highly competitive, with manufacturers focusing on premiumization, sustainable sourcing, health oriented formulations, and product innovation to strengthen their market position. Companies continue to invest in organic teas, functional ingredients, and environmentally friendly packaging solutions to meet evolving consumer preferences. Key companies operating in the UK tea market include The Republic of Tea, Harris Tea, Caraway Tea, Bigelow Tea, Dilmah, Twinings, Starbucks Corp, Unilever PLC, and PepsiCo Inc..

UK Tea Market Size

The UK tea market size was valued at USD 3.52 billion in 2025, and is projected to reach USD 6.09 billion by 2034 from USD 3.74 billion in 2026, growing at a CAGR of 6.28%.

Tea is historically and culturally the most popular hot drink in Britain. This market includes black tea, green tea, herbal infusions and specialty blends that cater to diverse consumer preferences ranging from traditional breakfast blends to wellness oriented botanicals. Tea serves as a social lubricant and a source of comfort deeply embedded in the national identity. According to the UK Tea and Infusions Association approximately 100 million cups of tea are consumed daily across the nation underscoring its pervasive presence in household routines. The market is evolving as consumers shift towards premium and ethically sourced products reflecting broader societal values regarding sustainability and health. According to HM Revenue and Customs and International Tea Committee data, the UK imports approximately 84,000 to 100,000 tonnes of tea annually, drawing primarily from Kenya and India to feed its international supply chains. The rise of independent tea houses and artisanal blenders has diversified the landscape offering unique flavor profiles and experiential retail opportunities. Consumer behavior is increasingly influenced by transparency in sourcing with demands for fair trade and organic certifications gaining prominence. The integration of tea into modern lifestyles through ready to drink formats and innovative packaging further expands its reach. Thus, the UK tea market is not merely a commodity sector but a dynamic industry adapting to changing demographics environmental concerns and lifestyle trends while maintaining its status as a national staple.

MARKET DRIVERS

Health Consciousness and Demand for Functional Beverages

The increasing awareness of health and wellness among the consumers is among the major drivers for the tea market. This trend is especially evident in the rapid growth of green, herbal, and functional teas. Consumers are actively seeking beverages that offer health benefits beyond hydration such as improved digestion enhanced immunity and stress relief. According to Public Health England (now OHID), campaigns like Sugar Smart and the Soft Drinks Industry Levy successfully reduced sugar intake from beverages, primarily driving consumers toward reformulated lower-sugar soft drinks and water rather than specifically to unsweetened tea. This shift is supported by scientific evidence highlighting the antioxidant properties of tea which contribute to overall well being. Ingredients like chamomile peppermint and ginger are popular for their soothing effects appealing to those managing anxiety and insomnia. The aging population also contributes to this trend as older adults prioritize heart health and cognitive function which are associated with regular tea consumption. Retailers have responded by expanding their ranges to include specialized blends targeting specific health needs such as detox or energy boosting. The perception of tea as a clean label product free from artificial additives aligns with the clean eating movement. Furthermore the availability of organic options caters to environmentally conscious shoppers who value purity and sustainability. This health driven demand ensures that tea remains a relevant and growing category within the broader beverage landscape.

Cultural Tradition and Social Rituals

The enduring cultural significance of tea in the country is also a key accelerator for consistent demand in the UK tea market. Tea drinking is deeply ingrained in British social fabric functioning as a ritual for hospitality comfort and community bonding. According to the UK Tea and Infusions Association's 2024 Census, 98% of UK residents drink tea daily, surpassing the 80% figure, confirming its status as the nation's favorite hot beverage with over 100 million cups consumed each day. This habitual consumption creates a stable baseline demand that is resilient to economic fluctuations. The tradition of afternoon tea continues to thrive in both domestic and commercial settings providing a sense of continuity and nostalgia. As per Visit Britain the hospitality sector leverages this tradition by offering premium afternoon tea experiences which attract tourists and locals alike generating significant revenue for hotels and cafes. The role of tea in workplace culture as a break time staple further reinforces its daily usage. Social media platforms have revitalized interest in tea aesthetics with influencers sharing brewing techniques and pairing suggestions that inspire younger generations. The emotional connection to tea as a source of solace during stressful times enhances its psychological value. Additionally the diversity of regional preferences allows for localized marketing strategies that resonate with specific communities. This cultural embeddedness ensures that tea remains a central element of British life driving steady consumption and fostering brand loyalty across generations.

MARKET RESTRAINTS

Competition from Coffee and Specialty Beverages

The rising popularity of coffee and specialty beverages is restricting the growth of the UK tea market. Coffee culture has expanded rapidly with the proliferation of café chains and artisanal roasters offering diverse and customizable drinks that appeal to younger demographics. According to the British Coffee Association, overall UK coffee consumption has risen by roughly 35% over the past two decades to roughly 98 million cups daily. While older demographics dominate at-home instant coffee use, millennials and Generation Z are driving a distinct shift toward premium pods, ground coffee, and high-street café culture. The perception of coffee as a more sophisticated and energizing option challenges the traditional dominance of tea. Moreover, the variety of coffee based drinks such as lattes cappuccinos and cold brews offers sensory experiences that traditional tea may lack. Marketing efforts by coffee brands emphasize lifestyle and status attracting consumers who view their beverage choice as a form of self expression. Additionally the convenience of mobile ordering and delivery services favors coffee chains that have invested heavily in digital infrastructure. Tea retailers often struggle to match this level of innovation and engagement leading to a loss of market share in the out of home sector. The higher average spend on coffee compared to tea also impacts revenue potential for tea establishments. This competitive pressure forces tea brands to innovate and differentiate themselves to retain relevance in a changing beverage landscape.

Supply Chain Vulnerabilities and Climate Change Impacts

Supply chain vulnerabilities and the impacts of climate change are limiting the expansion of the UK tea market. This affects availability and pricing. The UK relies heavily on imports from countries such as Kenya India and Sri Lanka where tea production is susceptible to weather extremes and political instability. According to the Intergovernmental Panel on Climate Change changing rainfall patterns and rising temperatures threaten tea yields and quality in key producing regions. Droughts and floods can lead to significant crop failures causing supply shortages and price volatility. Auction prices have historically remained stagnant or low for decades due to overproduction, meaning environmental stress is actively compressing the profit margins of smallholder farmers and producers, while global importers and retailers have largely been insulated from high raw material costs. The reliance on long distance transportation also exposes the supply chain to logistical disruptions such as port congestion and shipping delays. Geopolitical tensions and trade policies further complicate procurement processes increasing costs and uncertainty. Smallholder farmers who produce a significant portion of the world’s tea are particularly vulnerable to these challenges lacking resources to adapt to changing conditions. The ethical imperative to support sustainable farming practices adds complexity to sourcing strategies. Brands face pressure to ensure fair wages and environmental stewardship which can increase operational costs. These factors collectively constrain the stability and growth potential of the tea market requiring strategic adaptations to mitigate risks and ensure long term supply security.

MARKET OPPORTUNITIES

Premiumization and Artisanal Blends

The trend towards premiumization and artisanal blends offers a significant opportunity for the UK tea market. This growth is driven by consumers actively seeking high-quality and unique tasting experiences. Shoppers are increasingly willing to pay more for single origin loose leaf teas and expertly crafted blends that offer distinct flavor profiles. According to sources, the premium tea segment has shown resilience and growth with consumers viewing tea as a luxury item rather than a commodity. This shift is driven by the desire for authenticity and craftsmanship similar to the specialty coffee movement. As per the Speciality Tea Institute educated consumers are exploring terroir and processing methods leading to greater appreciation for rare and exotic varieties. Independent tea blenders and boutique brands are capitalizing on this by offering limited edition releases and personalized subscriptions. The rise of tea sommeliers and tasting events enhances the educational aspect of tea consumption fostering deeper engagement. Retailers can differentiate themselves by curating exclusive collections and providing detailed information about sourcing and production. Packaging innovation also plays a crucial role with elegant and sustainable designs appealing to gift buyers and collectors. The integration of tea into fine dining and mixology opens new avenues for experimentation and exposure. By focusing on quality and storytelling brands can build loyal customer bases and command higher price points. This opportunity allows the market to evolve beyond mass produced bags into a sophisticated and diverse industry.

Expansion of Ready to Drink and Cold Tea Formats

The expansion of ready to drink (RTD) and cold tea formats is paving the way for UK tea market growth. This trend is particularly appealing to younger and health-conscious consumers. As lifestyles become busier there is growing demand for convenient and refreshing beverage options that can be consumed on the go. Cold brew teas and sparkling tea infusions offer a modern twist on traditional flavors appealing to those seeking alternatives to sugary sodas and energy drinks. Brands can innovate with functional ingredients such as vitamins adaptogens and probiotics to enhance health benefits. The use of natural sweeteners and fruit extracts improves taste profiles making these products more accessible to mainstream audiences. Retailers are dedicating more shelf space to RTD teas in convenience stores and supermarkets ensuring visibility and accessibility. Partnerships with fitness centers and cafes can further drive trial and adoption. The versatility of cold tea allows for creative marketing campaigns targeting summer seasons and active lifestyles. Tea companies can tap into new usage occasions by embracing convenience and innovation. Doing so allows them to expand their reach beyond traditional hot beverage consumers.

MARKET CHALLENGES

Regulatory Pressures and Plastic Packaging Bans

Regulatory pressures and plastic packaging bans are significantly challenging the UK tea market. As a result, manufacturers are working hard to comply with environmental standards. Many traditional tea bags contain polypropylene a plastic sealant that prevents them from being fully biodegradable. The Department for Environment, Food & Rural Affairs (DEFRA) has implemented strict bans on many single-use plastics (such as cutlery and plates), creating a regulatory climate that, alongside consumer pressure, has prompted tea manufacturers to voluntarily accelerate the shift to biodegradable, plastic-free materials. Transitioning to plant based or compostable materials requires substantial investment in research and development as well as changes in manufacturing processes. Consumers are becoming more aware of microplastics in tea bags influencing purchasing decisions and demanding transparency from brands. The lack of standardized certification for compostable packaging can lead to consumer confusion and improper disposal. Retailers are also under pressure to reduce plastic waste in their supply chains affecting how tea products are displayed and sold. Compliance with varying international regulations adds complexity for brands that export or import ingredients. The shift away from plastic must balance functionality with sustainability ensuring that tea freshness and quality are maintained. Failure to adapt quickly can result in reputational damage and loss of market share to eco friendly competitors. This regulatory landscape requires continuous innovation and collaboration across the industry.

Changing Consumer Preferences and Declining Youth Interest

Changing consumer preferences and a decline in interest among younger generations further limit the expansion of the UK tea market. While tea remains popular among older demographics younger consumers are increasingly drawn to coffee energy drinks and functional beverages. The perception of tea as an old fashioned or boring beverage hinders its appeal to this demographic. Marketing efforts often fail to resonate with younger audiences who prioritize convenience and digital engagement. The rise of alternative wellness trends such as kombucha and matcha lattes competes for attention and spending. Tea brands struggle to modernize their image without alienating their core customer base. The lack of innovation in mass market products further exacerbates this issue making tea less competitive in the dynamic beverage sector. Engaging younger consumers requires creative strategies including social media campaigns influencer partnerships and novel product formats. Without successful rejuvenation the market faces the risk of long term decline as older consumers age out. Addressing this challenge is critical for sustaining future growth and relevance.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.28% |

| Segments Covered | By Type, Packaging, End User, Price Point, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Market Leaders Profiled | The Republic of Tea (U.S.), Harris Tea (U.S.), Caraway Tea (U.S.), Bigelow Tea (U.S.), Dilmah (Sri Lanka), Twinings (U.K.), Starbucks Corp (U.S.), Unilever PLC (U.K.), and PepsiCo Inc. (U.S.) |

SEGMENTAL ANALYSIS

By Type Insights

The black tea segment dominated the UK tea market and accounted for a 45.6% share in 2025. This dominance of the segment was driven by its deep cultural integration and status as the traditional choice for daily consumption. According to the UK Tea and Infusions Association, standard black tea accounts for approximately 90% of all tea consumed in the UK, reflecting its continued dominance despite the growing popularity of herbal alternatives. The main driver is the familiarity and comfort associated with strong robust flavors that pair well with milk and sugar which are staples in British households. The affordability of standard black tea blends makes them accessible to all income groups sustaining high volume sales. Major brands continue to innovate within this category by offering ethically sourced and premium variants to retain consumer interest. The widespread availability in supermarkets and convenience stores ensures that black tea remains the default option for most shoppers. Additionally the perception of black tea as a reliable source of caffeine for morning routines reinforces its daily usage. The segment benefits from strong brand loyalty towards established names that have been part of British culture for generations. This enduring popularity ensures that black tea remains the cornerstone of the UK tea industry driving the bulk of revenue and volume.

However, the fruit and herbal tea segment is anticipated to witness the fastest CAGR of 7.5% between 2026 and 2034 due to increasing health consciousness and the demand for caffeine-free alternatives. The expansion is propelled by consumers seeking natural remedies for stress sleep and digestion without the stimulant effects of caffeine. The variety of flavors available appeals to younger demographics who view tea as a wellness beverage rather than just a hot drink. Retailers are expanding their shelves to include diverse herbal blends catering to specific health needs such as immunity boosting or detoxifying. The perception of herbal tea as a hydrating and healthy alternative to sugary soft drinks further drives adoption. Social media influencers promote herbal teas as part of self care routines enhancing their appeal. The availability of organic and sustainably sourced options aligns with environmental values attracting conscious consumers. This segment’s ability to offer both taste and health benefits positions it for sustained rapid growth in the evolving UK tea landscape.

By Packaging Insights

The tea bags segment led the UK tea market and captured a substantial share in 2025 because of its unparalleled convenience and ease of use. This format dominates because it eliminates the need for measuring straining or cleaning up loose leaves making it ideal for fast paced lifestyles. According to the UK Tea and Infusions Association (UKTIA), tea bags account for approximately 96% of the British market, demonstrating an overwhelming national preference for convenience over loose-leaf preparation. The primary driver is the time saving aspect which appeals to office workers students and families who require quick preparation. As per research, the average British consumer prepares multiple cups of tea daily with tea bags being the preferred method for efficiency. The standardization of tea bag sizes ensures consistent flavor strength which consumers rely on for their daily routine. Manufacturers have improved the quality of tea bags by using pyramid shapes that allow better leaf expansion enhancing the taste experience. The widespread availability of tea bags in various formats including string and tag envelope and double chamber ensures broad accessibility. The cost effectiveness of mass produced tea bags makes them an affordable option for budget conscious shoppers. Additionally the portability of individual tea bags facilitates consumption outside the home in workplaces and travel settings. This combination of convenience consistency and affordability ensures that tea bags remain the primary packaging choice for the majority of UK tea drinkers.

The loose tea segment is likely to experience the fastest CAGR of 6.2% over the forecast period owing to the premiumization trend and the desire for higher quality experiences. Connoisseurs and enthusiasts are fueling the segment's growth. They prefer loose leaf tea, viewing it as superior in flavor and aroma to bagged varieties. The rise of independent tea shops and online retailers has made loose tea more accessible providing education on brewing techniques and origins. In addition, the environmental benefit of reduced packaging waste also appeals to eco conscious shoppers who prefer buying in bulk or using reusable containers. Specialty blends and single origin teas are often available only in loose form attracting those seeking unique and exotic flavors. The social aspect of sharing loose tea during gatherings enhances its appeal as a hospitality item. Retailers are responding by offering stylish storage solutions and brewing accessories that complement the loose tea experience. This segment’s growth reflects a shift towards quality and sustainability positioning it as a key area for innovation and expansion.

By End User Insights

In 2025, the residential segment held the majority share of the UK tea market. This leading position of the segment was attributed to the cultural norm of offering tea to guests and family members which sustains high domestic demand. The habit of drinking tea at home during meal breaks and social interactions is highly popular. According to Office for National Statistics (ONS) projections, there are approximately 28.6 million households in the UK, with industry data estimating that roughly 80% of these households regularly purchase tea. The comfort and relaxation associated with home brewing encourage frequent consumption throughout the day. Retailers cater to this segment by offering family sized packs and value bundles that ensure steady supply. The rise of remote work has further increased residential consumption as individuals prepare tea at home instead of purchasing it outside. Consumers prefer the cost savings and customization options available when brewing at home. The emotional connection to tea as a source of warmth and security reinforces its place in daily domestic life. Marketing campaigns often target homemakers and families emphasizing tradition and quality. This segment’s stability is underpinned by the ingrained nature of tea drinking in British home life ensuring consistent and predictable revenue for manufacturers.

The food service segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 8.1% during the forecast period. This swift growth of the segment is propelled by the recovery of the hospitality industry and the rising popularity of specialty tea offerings. Expanded hospitality tea menus drive this segment's growth through premium blends that attract discerning customers. The trend towards experiential consumption encourages patrons to try unique tea pairings and tasting flights. As per Visit Britain tourism plays a significant role in driving demand for traditional afternoon tea experiences which showcase high quality loose leaf and specialty teas. Hotels are investing in tea sommeliers and curated selections to enhance guest satisfaction and differentiate their services. The integration of tea into cocktail menus and dessert pairings creates new usage occasions. Independent tea houses are gaining popularity by offering educational workshops and cozy atmospheres that appeal to locals and tourists alike. This segment’s growth reflects the evolving role of tea as a premium hospitality product that enhances the overall dining experience.

By Distribution Channel Insights

The supermarkets and hypermarkets segment was the largest in the UK tea market and occupied a 44.3% share in 2025. Factors such as its extensive reach and one stop shopping convenience have supported the prominence of this segment. These retail giants command the largest share of tea sales as they offer a wide variety of brands and types under one roof. A key factor behind this segment’s top position is the competitive pricing and frequent promotions that attract budget conscious consumers. The strategic placement of tea aisles near other breakfast items encourages cross selling and impulse buys. Major chains invest in private label teas that offer quality at lower prices appealing to value seekers. The physical presence of supermarkets in nearly every community ensures broad accessibility for all demographics. Loyalty programs and digital apps provide personalized offers that drive repeat purchases. The ability to buy tea alongside weekly groceries simplifies the shopping experience for busy families. This channel’s scale and marketing power solidify its position as the primary driver of tea consumption in the UK.

However, the online stores segment is expected to exhibit a noteworthy CAGR of 10.5% from 2026 to 2034. This quick surge is driven by the convenience of home delivery and access to niche products. The segment’s growth is also supported by the increasing adoption of e commerce and the desire for specialized teas that are not available in physical stores. According to the Office for National Statistics online grocery sales have stabilized at higher levels indicating a permanent shift in consumer behavior. Direct to consumer brands offer subscription services and curated boxes that enhance customer engagement and loyalty. As per The Drum digital marketing efforts by tea companies have increased visibility and driven traffic to online platforms. The ability to read reviews and compare products online empowers consumers to make informed choices. Online retailers often provide detailed information about sourcing and brewing which educates customers and builds trust. The convenience of having heavy bulk orders delivered to the doorstep appeals to regular drinkers. This channel’s agility and reach enable it to capture a growing share of the market particularly among younger demographics who prioritize ease and variety.

COUNTRY LEVEL ANALYSIS

The United Kingdom was the top performer in the European tea market and captured a 25.5% share in 2025. This expansion of the country’s market was fuelled by high per capita consumption and a strong cultural heritage. A mature regulatory environment and a long-standing tradition of tea consumption define the UK market landscape. Key market drivers include the deep-rooted presence of tea in households and the traditional importance of tea breaks. According to the UK Tea and Infusions Association, the British public consumes over 100 million cups of tea daily. This translates to an average of about 3.5 cups per person per day, reflecting a deep-rooted cultural habit. Consumer preferences are shifting towards sustainable and ethical products influencing sourcing and production practices. Global market trends monitored by organizations like Fairtrade International indicate a growing consumer preference for ethically sourced and environmentally friendly teas. The increasing availability and sales of fair trade certified teas demonstrate a shift towards responsible and conscious consumption. The presence of major international brands alongside local blenders ensures a competitive and diverse landscape. Retailers play a crucial role in shaping trends through promotions and private label developments. The aging population contributes to steady demand while younger generations drive innovation in flavors and formats. The UK’s leadership in setting standards for tea quality and sustainability influences regional markets. These factors combined ensure that the UK remains a key player in the global tea industry driving growth and setting benchmarks for excellence.

COMPETITIVE LANDSCAPE

The competition in the United Kingdom tea market is intense and characterized by the presence of established multinational corporations alongside agile independent blenders. Major brands leverage their extensive distribution networks and marketing budgets to dominate shelf space in supermarkets. These entities continuously innovate with new flavors and sustainable packaging to retain consumer interest. Independent producers compete by offering unique artisanal products that appeal to niche markets seeking authenticity and quality. The market sees fierce rivalry in the premium segment where provenance and ethical credentials play crucial roles in decision making. Price competition remains significant in the standard category prompting retailers to offer frequent promotions and discounts. Regulatory pressures regarding environmental impact add complexity to competitive dynamics requiring strategic agility. The rise of herbal and functional teas introduces new competitors from the wellness sector diversifying the landscape. Collaboration between brands and hospitality partners is common to enhance consumer experiences and drive sales. Overall the market demands continuous adaptation to changing consumer trends and sustainability goals to sustain growth and profitability in this evolving industry.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the UK tea market are

- The Republic of Tea (U.S.)

- Harris Tea (U.S.)

- Caraway Tea (U.S.)

- Bigelow Tea (U.S.)

- Dilmah (Sri Lanka)

- Twinings (U.K.)

- Starbucks Corp (U.S.)

- Unilever PLC (U.K.)

- PepsiCo Inc. (U.S.)

Top Players in the Market

- Taylors of Harrogate is a prominent family owned business that significantly contributes to the UK tea market through its iconic Yorkshire Tea and Bettys Café Tea Rooms brands. The company is deeply involved in sustainable sourcing initiatives ensuring ethical practices across its supply chain. Recent actions include substantial investments in water conservation projects in tea growing regions to mitigate climate change impacts. Taylors has also expanded its range of organic and fair trade options to meet evolving consumer demands for transparency. The firm strengthens its position by engaging directly with farmers to improve livelihoods and crop quality. Their commitment to environmental stewardship and community support enhances brand loyalty among conscious consumers. Taylors of Harrogate maintains high quality standards and fosters long-term partnerships. Through this approach, the company solidifies its reputation as a trusted and responsible leader in the British tea industry.

- Unilever PLC plays a pivotal role in the UK tea market with its extensive portfolio including PG Tips and Lipton brands. The company leverages its global scale to drive innovation and accessibility in tea consumption. Recent strategies involve transitioning to fully recyclable packaging materials to address environmental concerns and reduce plastic waste. Unilever has also focused on digital marketing campaigns that resonate with younger audiences emphasizing versatility and modern lifestyles. The corporation invests in research and development to create new blends that cater to health conscious preferences. By optimizing supply chain efficiency Unilever ensures consistent product availability and competitive pricing. Their dedication to sustainability and continuous product innovation helps maintain strong brand recognition. These efforts enable Unilever to adapt to changing market dynamics while reinforcing its position as a key contributor to the UK tea sector.

- Twinings is a historic brand that contributes significantly to the UK tea market by offering a diverse range of herbal fruit and black teas. The company is renowned for its heritage and commitment to quality blending techniques. Recent actions include the launch of premium loose leaf collections and innovative ready to drink formats to capture new usage occasions. Twinings has strengthened its market position by partnering with wellness influencers to promote the health benefits of its herbal infusions. The brand actively supports sustainable agriculture through its Sourcing with Respect program which aids farming communities. Twinings also enhances customer engagement through interactive digital platforms and educational content about tea origins. By balancing tradition with modern trends Twinings appeals to both loyal customers and new demographics. Their focus on flavor innovation and ethical sourcing ensures continued relevance and growth in the competitive UK tea landscape.

Top Strategies Used by Key Market Participants

Key players in the UK tea market primarily employ sustainability strategies to enhance brand reputation and meet consumer expectations. Companies focus on ethical sourcing and environmentally friendly packaging to reduce their ecological footprint. Product innovation is another major strategy with firms developing functional blends that offer health benefits such as improved digestion or relaxation. Digital engagement is crucial as brands utilize social media to connect with younger demographics and share brewing tips. Partnerships with certified organizations help validate claims regarding fair trade and organic practices. Retailers optimize shelf space for premium and specialty teas to capture higher margins. Private label development allows supermarkets to offer competitive alternatives to established brands. Customer loyalty programs are used to encourage repeat purchases and gather data on preferences. These multifaceted approaches enable participants to differentiate themselves and maintain competitiveness in a mature market.

MARKET SEGMENTATION

This research report on the UK tea market is segmented and sub-segmented into the following categories.

By Type

- Black Tea

- Green Tea

- Fruit/Herbal Tea

- Oolong Tea

- Others

By Packaging

- Loose Tea

- Paperboards

- Tea Bags

- Plastic Containers

- Aluminum Tins

By End User

- Residential

- Food Service

- Institutional

By Price Point

- Economy

- Mid Range

- Premium and Luxury

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Convenience Stores

- Online Stores

- Bulk Suppliers

- Others

Frequently Asked Questions

1. What is driving the growth of the UK tea market?

The UK tea market is growing due to increasing consumer demand for premium teas, herbal infusions, specialty blends, and health focused beverages.

2. Which type of tea is most popular in the UK?

Black tea remains the most widely consumed tea in the UK, driven by the country's long standing tea drinking culture.

3. How are health trends influencing the UK tea market?

Consumers are increasingly choosing green tea, herbal tea, and functional tea products that offer benefits such as relaxation, immunity support, and weight management

4. What role does premiumization play in the UK tea market?

Premium and specialty teas, including organic and ethically sourced varieties, are gaining popularity as consumers seek higher quality products.

5. Which distribution channels are important in the UK tea market?

Supermarkets, hypermarkets, convenience stores, online retail platforms, and specialty tea shops are key distribution channels.

6. How is e commerce impacting tea sales in the UK?

Online platforms are expanding consumer access to a wide range of tea products, subscription services, and premium international brands.

7. What are the major challenges facing the UK tea market?

Challenges include fluctuating raw material prices, supply chain disruptions, changing consumer preferences, and competition from other beverages.

8. Are sustainable and ethical sourcing practices important in the UK tea market?

Yes, consumers increasingly prefer tea products that are sustainably produced, ethically sourced, and certified by recognized environmental standards.

9. What is the demand for herbal and fruit teas in the UK?

Demand for herbal and fruit teas is rising as consumers look for caffeine free and wellness oriented beverage options.

10. How are manufacturers innovating in the UK tea market?

Manufacturers are introducing new flavors, functional ingredients, eco friendly packaging, and ready to drink tea products to attract consumers.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com