U.S. Home Decor Market Size, Share, Trends, and Growth Analysis Report, Segmented by Product Type, Material, Distribution Channel, Price Range, Room, and Country – Industry Forecast From 2026 to 2034

U.S. Home Decor Market Report Summary

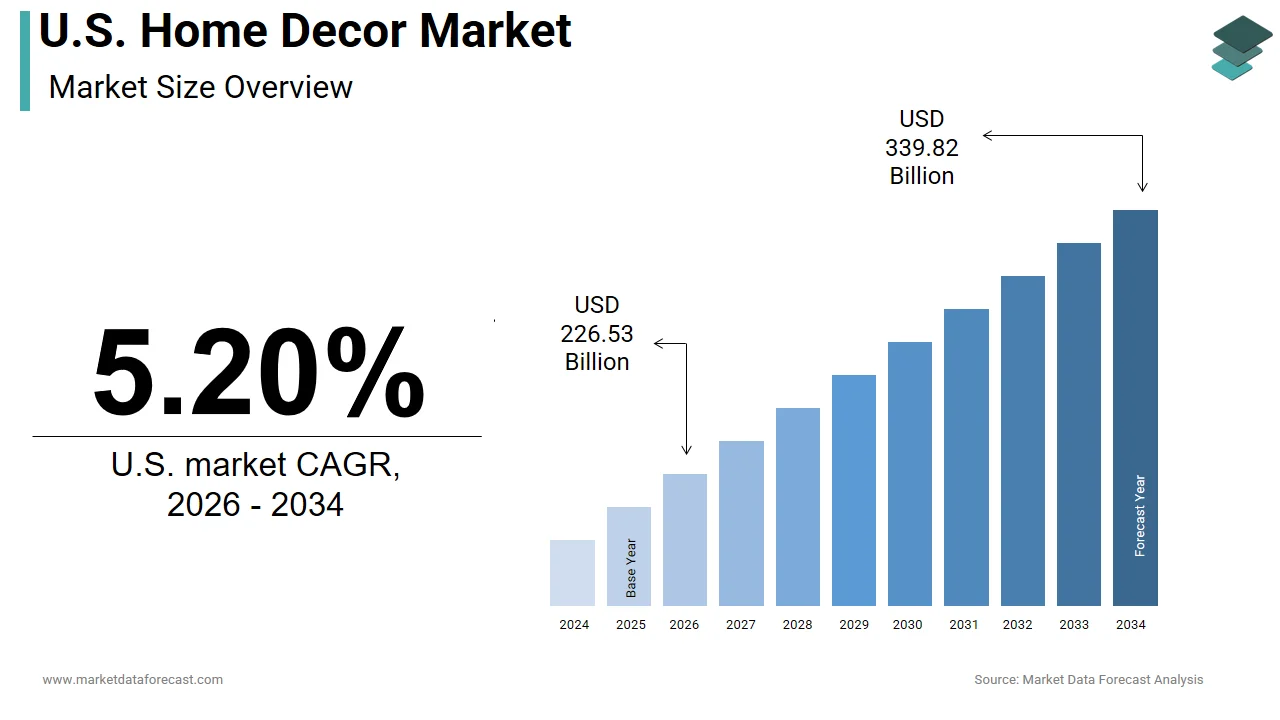

The U.S. home decor market was valued at USD 215.33 billion in 2025, is estimated to reach USD 226.53 billion in 2026, and is projected to reach USD 339.82 billion by 2034, growing at a CAGR of 5.20% from 2026 to 2034. Market growth is driven by rising consumer spending on home improvement, increasing interest in interior aesthetics, and growing demand for personalized living spaces. Consumers are increasingly investing in stylish furniture, decorative accessories, lighting, wall décor, and sustainable home furnishing products to enhance residential interiors. Additionally, rapid expansion of e-commerce platforms, rising urbanization, and growing popularity of smart and multifunctional home décor products are accelerating market growth across the United States.

Key Market Trends

- Rising demand for stylish and personalized home décor products.

- Increasing consumer spending on home renovation and interior design.

- Growth in sustainable and eco-friendly furniture materials.

- Expansion of online furniture and décor retail platforms.

- Increasing popularity of multifunctional and smart home décor solutions.

Segmental Insights

- Based on product type, the furniture segment dominated the United States home decor market by accounting for 47.3% share in 2025, driven by rising demand for premium and multifunctional household furniture.

- Based on material type, the wood segment led the market with 42.5% share in 2025, supported by strong consumer preference for durable, aesthetic, and sustainable furniture materials.

Country-Level Insights

The United States dominated the North American home decor market by capturing 81.2% share in 2025, supported by high consumer spending power, strong housing infrastructure, and increasing investments in residential interior enhancement.

Competitive Landscape

The U.S. home decor market is highly competitive, with companies focusing on premium product offerings, omnichannel retail expansion, and sustainable product innovation. Investments in digital shopping experiences, customizable furniture, and eco-friendly materials are shaping the competitive landscape.

Prominent companies operating in the U.S. home decor market include The Home Depot, Lowe's Companies Inc., IKEA, Williams-Sonoma Inc., and Wayfair Inc

U.S. Home Decor Market Size

The size of the U.S. home decor market was worth USD 215.33 billion in 2025. The market is anticipated to grow at a CAGR of 5.20% from 2026 to 2034 and be worth USD 339.82 billion by 2034 from USD 226.53 billion in 2026.

Home decor, or home decoration, refers to the art and practice of styling, furnishing, and accessorizing a living space to enhance its aesthetic appeal, functionality, and comfort. This market is deeply influenced by housing trends, consumer lifestyle shifts, and the psychological need for personalized living environments. The fundamental desire for comfort and self-expression drives consistent demand across diverse demographic segments. According to the U.S. Census Bureau, the total national housing inventory has surpassed 146 million units, creating a massive and expanding infrastructure for home decor and renovation consumption. The aging housing stock further amplifies the need for renovation and refreshment as homeowners seek to modernize outdated interiors. Moreover, the Joint Center for Housing Studies of Harvard University reveals that over 60% of the U.S. owner-occupied housing stock was built before 1980, driving a critical, sustained market demand for structural repairs and modernizing renovations. Additionally, the rise of remote work has transformed homes into multifunctional spaces, necessitating decor that balances professionalism with comfort. The Bureau of Labor Statistics indicates that in 2023, approximately 22.5% of employed persons worked from home at least some of the time, cementing a permanent, albeit normalized, demand for home office setups and ergonomic furniture. Social media platforms also play a crucial role in shaping trends, with millions of users seeking inspiration for DIY projects and interior makeovers. This digital influence accelerates the adoption of new styles and encourages frequent updates to living spaces. The market is thus defined by a convergence of practical necessity and artistic expression, where consumer choices are increasingly driven by the desire for sanctuary and identity rather than mere utility.

MARKET DRIVERS

Surge in Homeownership and Renovation Activities

The sustained surge in homeownership rates and subsequent renovation activities is a major reason for the expansion of the United States home decor market. Owning a home often inspires individuals to invest in personalizing their spaces through decor upgrades and structural improvements. According to U.S. Census Bureau data, the national homeownership rate has stabilized at approximately 66.4%, reflecting a massive, resilient base of consumers with long-term financial and investment interests in their properties. New homeowners typically allocate significant portions of their budgets to immediate decor changes such as painting, flooring, and window treatments to align the space with their personal tastes. The Joint Center for Housing Studies of Harvard University highlights that while home remodeling reached historic peaks in the early 2020s, spending has since stabilized, with homeowners navigating a tight housing inventory by prioritizing necessary maintenance over massive discretionary overhauls. This trend is further supported by the aging of the housing stock, which requires regular updates to remain functional and aesthetically pleasing. Additionally, the increase in home equity allows owners to finance larger renovation projects that include high-end decor elements. The National Association of Home Builders (NAHB) indicates that while macroeconomic pressures have created a more cautious remodeling environment, consumers continue to value home improvements to preserve both residential utility and long-term equity. So, the home decor sector benefits from this continuous cycle of acquisition and improvement, driving demand for a wide range of products from basic accessories to luxury furnishings.

Influence of Digital Media and Interior Design Trends

The pervasive influence of digital media and rapidly evolving interior design trends significantly drives the growth of the United States home decor market. Social media platforms such as Pinterest, Instagram, and TikTok have become primary sources of inspiration for consumers seeking to update their living spaces. Research highlights near-universal digital connectivity, with a vast majority of American adults utilizing social media platforms—providing an omnipresent digital ecosystem where design influencers and home decor content drive massive consumer engagement. These platforms democratize design knowledge, allowing users to discover new styles, DIY techniques, and product recommendations instantly. The viral nature of trends such as cottagecore maximalism or minimalist aesthetics creates sudden spikes in demand for specific decor items. Influencers and interior designers share curated looks that encourage followers to replicate these styles in their own homes. This digital engagement shortens the decision-making process and increases impulse purchases of decorative accessories. Furthermore, augmented reality tools provided by retailers allow users to visualize decor items in their spaces before buying, reducing hesitation and returns. The constant flow of fresh content keeps consumers engaged and eager to refresh their environments to stay current with trends. This dynamic interaction between digital inspiration and physical consumption ensures that the home decor market remains vibrant and responsive to cultural shifts.

MARKET RESTRAINTS

Economic Volatility and Inflationary Pressures

Economic volatility and persistent inflationary pressures are major restraints on the United States home decor market. This reduces consumer discretionary spending power. Home decor is often considered a non-essential expense that can be deferred during times of financial uncertainty. The Bureau of Labor Statistics (BLS) shows that while household furnishings faced intense inflationary spikes during global supply chain imbalances, the category has since experienced price stabilization and deflationary corrections. This increase in prices for materials, labor, and finished goods forces consumers to prioritize essential needs over aesthetic upgrades. The Federal Reserve Bank of New York confirms that household debt levels remain elevated, and massive gains in residential home equity continue to act as a primary financial buffer for major remodeling investments. High interest rates on mortgages and home equity loans also discourage large-scale renovations that typically drive demand for extensive decor purchases. Many consumers are opting to delay major updates or choose lower-cost alternatives such as DIY fixes instead of hiring professionals or buying premium items. This cautious spending behavior limits the growth potential for higher-end decor brands and retailers who rely on premium pricing strategies. Thus, the market faces challenges in maintaining volume and value growth as economic headwinds persist, affecting both new home buyers and existing homeowners.

Supply Chain Disruptions and Material Shortages

Supply chain disruptions and shortages of key raw materials are constraining the availability and pricing of home decor products in the country, which hampers the expansion of the United States home décor market. The global nature of the supply chain means that components such as wood, metals, fabrics, and glass are sourced from various international suppliers, making the industry vulnerable to logistical bottlenecks. These disruptions result in inventory stockouts and an inability to meet consumer demand, particularly during peak seasons. According to the Bureau of Labor Statistics, the Producer Price Index for intermediate materials has retrenched from its pandemic-era peaks, easing raw material cost pressures for domestic home goods manufacturers. These cost increases are often passed on to consumers, leading to higher retail prices, which can dampen demand. Additionally, the shortage of skilled labor in manufacturing and logistics further exacerbates production delays. The National Association of Manufacturers (NAM) emphasizes that persistent structural workforce shortages impact operational capacities, forcing companies to automate production lines to maintain efficiency in a highly competitive retail market. Furthermore, geopolitical tensions and trade policies affect the availability of imported materials, adding another layer of complexity. These factors create uncertainty in production planning and pricing strategies, making it difficult for retailers to maintain consistent product offerings. Consequently, the market faces operational challenges that hinder growth and customer satisfaction.

MARKET OPPORTUNITIES

Expansion of E-Commerce and Augmented Reality Shopping

The proliferation of e-commerce and the integration of augmented reality shopping experiences offer significant opportunities for growth in the United States home decor market. Online platforms offer consumers convenience, extensive variety, and competitive pricing, which appeals to modern shoppers. The ability to browse thousands of products from home eliminates geographical barriers and allows access to niche and international brands. Augmented reality tools enable users to visualize how furniture and decor items will look in their spaces using smartphone cameras. This innovation reduces the uncertainty associated with online purchases and lowers return rates. Additionally, personalized recommendations powered by artificial intelligence help consumers discover products that match their style preferences. The convenience of home delivery and easy return policies further enhances the online shopping experience. As internet penetration and digital literacy increase, the online channel offers a lucrative avenue for retailers to reach broader audiences. Brands that invest in seamless digital experiences and virtual visualization tools can capture market share and build stronger customer relationships in the evolving retail landscape.

Growing Demand for Sustainable and Eco-Friendly Decor

The growing consumer preference for sustainable and eco-friendly home decor products creates a strong opening for manufacturers and retailers to differentiate their offerings, which is expected to boost the expansion of the United States home décor market. Environmental consciousness is increasingly influencing purchasing decisions, particularly among millennials and Generation Z consumers who prioritize ethical production practices. In response, several home decor brands have introduced products made from recycled materials, reclaimed wood, organic cotton,, and biodegradable components. Brands that communicate their sustainability efforts effectively often enjoy higher brand loyalty and willingness to pay premium prices. Additionally, regulatory pressures regarding waste and carbon emissions are expected to tighten, which makes early adoption of sustainable practices a strategic advantage. By investing in circular economy principles, such as take-back programs and recyclable packaging, companies can appeal to this discerning demographic. This shift not only mitigates environmental impact but also opens new avenues for innovation and brand storytelling in the competitive home decor market.

MARKET CHALLENGES

Intense Competition and Market Saturation

Intense competition and saturation are challenging the growth of the United States home decor market. This makes it challenging for new entrants and established players alike to differentiate their offerings. The market is fragmented with numerous players ranging from large big box retailers to small independent boutiques and online startups. This high level of competition leads to price wars and aggressive marketing campaigns, which erode profit margins. Large retailers leverage economies of scale to offer lower prices while niche brands focus on unique designs and personalized service. The rise of private label products from major retailers further intensifies competition by offering affordable alternatives that mimic trending styles. Differentiation through innovation becomes difficult as design trends are quickly replicated across the industry. Additionally, consumer switching costs are low, allowing shoppers to easily try new brands based on promotions or social media recommendations. This dynamic forces companies to continuously innovate and invest in brand building to maintain relevance. The saturation of traditional retail spaces also limits physical expansion opportunities, pushing brands to compete fiercely in the digital arena where customer acquisition costs are rising. Thus, maintaining market share requires significant strategic effort and financial investment.

Changing Consumer Preferences and Trend Volatility

The rapid pace of changing consumer preferences and trend volatility is a significant challenge for home decor manufacturers and retailers in the country, which negatively impacts the expansion of the United States home décor market. Interior design trends evolve quickly, influenced by social media celebrity endorsements and cultural shifts, making it difficult for companies to predict demand accurately. Products that are popular one month may become obsolete the next, leading to excess inventory and markdowns. The fast fashion model has influenced the home decor sector, with consumers expecting frequent new arrivals and low prices. This pressure strains manufacturing capabilities and increases the risk of overproduction. Additionally, the diversity of consumer tastes means that no single style dominates the market for long, requiring brands to offer wide assortments. Companies must balance the need for trend responsiveness with the costs of rapid product development and distribution. Failure to anticipate shifts in preference can result in significant financial losses and brand irrelevance. Hence, the market faces the ongoing challenge of staying ahead of curves while managing operational efficiency and profitability in an unpredictable market environment.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Material, Distribution Channel, Price Range, Room, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | The Home Depot Inc., Lowe’s Companies Inc., IKEA, Williams-Sonoma Inc., Wayfair Inc., and Others. |

SEGMENTAL ANALYSIS

By Product Type Insights

The furniture segment dominated the United States home decor market and accounted for a 47.3% share in 2025. This dominance of the segment was driven by its fundamental role in establishing functional living spaces. Unlike decorative accessories, which are optional furniture items, such as sofas, beds, and dining tables, are essential for daily habitation and comfort. This structural necessity ensures a consistent and substantial demand regardless of economic fluctuations or changing design trends. The National Association of Realtors (NAR) indicates that while homeowner tenure has extended to a historic average of 10 to 13 years, residential turnover remains a major catalyst for predictable, highly cyclical surges in furniture and home decor procurement. Furthermore, the rise of remote work has increased the need for specialized furniture such as ergonomic desks and supportive chairs. According to the Bureau of Labor Statistics, approximately 22.5% of employed persons continue to work from home at least part of the time, cementing permanent structural demand for home office furnishings and ergonomic design adaptations. This functional requirement creates a stable revenue base for manufacturers and retailers. Additionally, furniture pieces often serve as anchor items around which other decor elements are styled, making them the primary purchase in any interior design project. The high ticket value of furniture compared to textiles or accessories also contributes to its dominance in terms of total market revenue.

Furthermore, the domination of the furniture segment is further reinforced by the natural wear and tear associated with daily use, which necessitates periodic replacement. Furniture items are subject to physical degradation over time, including fabric fading, cushion sagging, and structural weakening. This finite lifecycle creates a predictable replacement market that drives continuous sales volume. Consumers often replace furniture not only due to damage but also to update the aesthetic of their homes as styles evolve. The trend towards larger sectional sofas and modular seating arrangements also boosts unit values. Furthermore, the availability of financing options through major retailers allows consumers to spread the cost of high-value furniture purchases, making them more accessible. These factors collectively ensure that the furniture segment maintains its leadership position by combining essential utility with regular replacement needs.

The home textiles segment is anticipated to witness the fastest CAGR of 6.8% from 2026 to 2034, owing to the rising trend of seasonal decor updates where consumers refresh their living spaces using affordable soft furnishings. Unlike furniture, which represents a long-term investment, textiles such as throw pillows, curtains, rugs, and bedding allow for quick and cost-effective style changes. The Home Furnishings Association (HFA) confirms that decorative home textile categories experience significant sales surges during spring cleaning and holiday seasons as consumers refresh their living spaces. A study indicates that the average household allocates under $180 annually to household textiles, validating the category's status as a highly accessible, low-barrier entry point for interior decorating compared to major furniture investments. Social media platforms like Instagram and Pinterest amplify this trend by showcasing styled rooms that feature coordinated textile patterns and colors. A survey reveals that a strong consumer appetite for seasonal updates, revealing that nearly half of design-conscious homeowners refresh their home textiles at least once a year to align with changing seasons and styling trends. This frequent turnover drives high-volume sales for retailers. Additionally, the ease of online shopping for textiles that do not require complex assembly or delivery logistics further accelerates market growth. Consumers can easily compare fabrics and read reviews, leading to confident purchasing decisions. The ability to mix and match textures and patterns also encourages multiple purchases within a single transaction, boosting overall segment performance.

A different factor driving the rapid growth of the home textiles segment is the heightened focus on comfort and hygiene in the post-pandemic era. Consumers are placing greater emphasis on creating cozy and sanitary living environments, which has boosted demand for high-quality bedding, towels, and bath mats. The pandemic led to a surge in time spent indoors, prompting investments in plush rugs, soft throws, and premium sheet sets that enhance tactile comfort. Additionally, the trend towards spa-like bathrooms has driven demand for luxury towels and bath accessories. Consumers are willing to pay premium prices for organic cotton, bamboo, and other sustainable materials that offer both comfort and environmental benefits. The home textiles segment continues to experience robust growth, with health and well-being remaining top priorities. This market expansion is driven by the desire for safe, comfortable, and hygienic home environments.

By Material Type Insights

The wood segment led the United States home decor market and captured a 42.5% share in 2025. This leading position of the segment was attributed to its unparalleled versatility, durability, and timeless aesthetic appeal. It is used extensively in furniture, flooring, cabinetry, and decorative accents across various design styles from rustic to contemporary. The U.S. Department of Agriculture (USDA) and the U.S. Forest Service confirm that the United States produces tens of billions of board feet of timber annually, sustaining a robust domestic supply chain for both structural construction and finish manufacturing. Wood's natural grain and warmth create a welcoming atmosphere that resonates with American consumers who value authenticity and craftsmanship. The National Wood Flooring Association (NWFA) indicates that premium wood flooring remains a highly coveted residential standard, consistently commanding a premium market share due to its unmatched longevity and proven ability to enhance property value. Additionally, wood can be easily stained, painted, or carved, allowing for extensive customization to match diverse interior themes. Major furniture retailers consistently feature wood-based collections as core offerings because of their broad consumer acceptance. The durability of solid wood furniture means it can last for generations, making it a preferred choice for heirloom pieces. Furthermore, the integration of wood with other materials such as metal and glass enhances its design flexibility. These factors collectively sustain the dominance of wood as the primary material in the home decor sector.

In addition, the spearheading of the wood segment is further reinforced by a strong cultural preference for natural and organic materials in American homes. Consumers increasingly seek to connect with nature through biophilic design principles, which emphasize the use of natural elements to improve well-being. This psychological benefit drives demand for wooden furniture and decor items that bring the outdoors inside. Reclaimed and salvaged wood has also gained popularity as consumers look for unique stories and sustainability in their purchases. Additionally, the perception of wood as a premium and high-quality material justifies higher price points, contributing to its revenue leadership. This trust ensures that wood continues to be the material of choice for discerning homeowners who value both aesthetics and environmental responsibility.

The metal material segment is likely to experience the fastest CAGR of 7.2% over the forecast period, owing to the popularity of industrial chic and modern minimalist design trends, which heavily feature metal elements. Metals such as steel, iron, brass, and gold are used in lighting fixtures, furniture frames, shelving, and decorative accents to create sleek and sophisticated looks. Architectural design indices show a distinct surge in contemporary interior trends incorporating metallic finishes, driving increased cross-industry procurement for both ferrous and non-ferrous decorative metal products in residential construction. The versatility of metal allows for thin profiles and intricate designs that are difficult to achieve with wood or plastic. This aesthetic flexibility appeals to younger demographics who favor clean lines and urban aesthetics. The National Association of Home Builders notes that metal accents are increasingly specified in new home constructions, particularly in kitchens and bathrooms, for hardware and fixtures. Additionally, the durability and low maintenance requirements of metal make it an attractive option for high-traffic areas. Powder coating and other finishing technologies have expanded the color palette of metal decor beyond traditional silver and black to include vibrant hues and textured finishes. These innovations keep the material fresh and relevant in evolving design landscapes. As urban living spaces become smaller, the lightweight and space-efficient nature of metal furniture further boosts its adoption.

The segment moves ahead quickly, driven by its durability and strong sustainability credentials, particularly regarding recycled content. Metals are infinitely recyclable without loss of quality, which aligns with the growing consumer demand for circular economy products. Eco-conscious consumers prefer metal decor items made from recycled sources as they reduce the environmental impact of mining and processing raw materials. Additionally, metal furniture and decor are highly durable and resistant to pests, moisture, and warping, which extends their lifespan compared to some organic materials. This longevity reduces the frequency of replacement and overall waste generation. Furthermore, the industrial aesthetic of metal pairs well with other sustainable materials like reclaimed wood and bamboo, creating hybrid designs that appeal to broader audiences. As regulatory pressures on waste management increase, the inherent recyclability of metal positions it as a future-proof material choice. These environmental and practical advantages ensure the continued rapid expansion of the metal segment in the home decor market.

By Distribution Channel and Price Range Insights

The home improvement and furniture stores segment held the majority share of 56.8% of the United States home decor market in 2025 because of the convenience of one-stop shopping and immediate product availability. Large retailers such as Home Depot, Lowe's, IKEA, and Wayfair offer extensive assortments of furniture, textiles, and accessories under one roof, allowing consumers to complete their decor projects efficiently. The ability to see and touch products reduces the uncertainty associated with online buying and minimizes return rates. Additionally, these stores often provide immediate pickup options for in-stock items, which appeals to customers who need decor solutions quickly. These retailers also offer professional design services and installation support, which adds value for customers undertaking complex renovations. The established trust and brand recognition of major chains further drive foot traffic and sales volume. Promotional events and seasonal sales attract bargain hunters who seek value for money. The integration of online and offline channels through buy online, pick up in store services enhances the customer experience. These factors collectively sustain the dominance of home improvement and furniture stores as the primary conduit for home decor distribution.

Moreover, the leadership of the home improvement and furniture store segment is further reinforced by their extensive physical presence and robust supply chain infrastructure. Major retailers have thousands of locations across the United States, ensuring widespread accessibility for consumers in urban, suburban, and rural areas. This physical network allows for efficient logistics and inventory management, reducing shipping costs and delivery times. Established relationships with manufacturers enable these retailers to negotiate favorable pricing and secure exclusive product lines. Additionally, these stores invest heavily in visual merchandising and showroom displays that inspire customers and demonstrate product usage. The tactile experience of sitting on a sofa or feeling a fabric texture is crucial for high involvement purchases, which physical stores facilitate effectively. Loyalty programs and credit financing options further enhance customer retention and average order values. The ability to handle returns and exchanges in-store provides a safety net for consumers that pure play online retailers struggle to match. These operational strengths ensure that home improvement and furniture stores maintain their leading position in the market.

Online Stores

The online stores segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 9.5% between 2026 and 2034. This rapid expansion of the segment is propelled by the digital convenience and expanded product selection that e-commerce platforms offer. Consumers can browse millions of items from the comfort of their homes, accessing niche and international brands that are not available in local stores. The ability to compare prices, read reviews, and view user-generated photos helps consumers make informed decisions. Amazon and Wayfair have revolutionized the sector by offering fast shipping and easy return policies, which mitigate the risks of online buying. Augmented reality tools allow users to visualize products in their spaces, enhancing confidence in purchase decisions. Additionally, online retailers often offer lower prices due to reduced overhead costs, attracting budget-conscious shoppers. The convenience of home delivery eliminates the need for transportation and handling of bulky items. As logistics networks become more efficient, delivery times continue to shrink, making online shopping a viable alternative for urgent needs. These factors collectively fuel the rapid growth of the online channel.

A big reason for the fast growth is the use of personalization and data-driven marketing strategies that enhance customer engagement. E-commerce platforms leverage artificial intelligence and machine learning to analyze browsing behavior and purchase history, providing tailored product recommendations. Online retailers send targeted emails and notifications about sales and new arrivals, keeping brands top of mind for shoppers. Social media integration allows for seamless shopping experiences where users can purchase items directly from ads and posts. Subscription services for decor boxes and curated collections also drive recurring revenue and customer loyalty. Online platforms gather valuable feedback through reviews and ratings, which helps them refine their offerings and improve customer satisfaction. The ability to track inventory in real time ensures that popular items are restocked quickly, reducing lost sales opportunities. As technology advances, the online shopping experience becomes more immersive and convenient, attracting a broader audience. This strategic use of data and technology ensures that online stores continue to outpace traditional channels in growth rate.

COUNTRY ANALYSIS

U.S. Home Decor Market Analysis

The United States outperformed other countries in the North American home decor market and accounted for a 81.2% share in 2025. This dominance was attributed to the country's large population, high homeownership rates, and strong culture of interior design and personalization. The market status is characterized by a mature yet dynamic environment where consumer preferences drive continuous innovation and trend adoption. According to U.S. Census Bureau estimates, the national housing stock has surpassed 146 million units, providing an expansive and continuously growing infrastructure for home decor and residential furnishings consumption. The high prevalence of home renovation activities further amplifies demand as homeowners seek to update and personalize their living spaces. Additionally, the United States has a robust retail infrastructure with a mix of large big box stores, specialty boutiques, and advanced e-commerce platforms, ensuring wide product availability. High disposable income levels allow consumers to invest in premium and luxury decor items, contributing to market value growth. The influence of social media and digital platforms accelerates trend cycles and encourages frequent updates to home aesthetics. Furthermore, the emphasis on sustainability and eco-friendly materials is shaping product development and consumer choices. These structural, demographic, and economic factors solidify the United States as the leading market for home decor in the region, with sustained growth potential driven by lifestyle evolution and technological integration.

COMPETITIVE LANDSCAPE

The competition in the United States home decor market is intense and characterized by a mix of established big box retailers, specialized chains, and agile e-commerce platforms. Major players leverage their extensive distribution networks and brand recognition to maintain dominance while newer entrants disrupt the market with niche designs and direct-to-consumer models. The rivalry is further amplified by the rapid pace of trend cycles influenced by social media, which requires companies to be highly responsive to changing consumer preferences. Price competition is fierce, particularly in the mass market segment, where private labels offer affordable alternatives to branded goods. Traditional retailers face pressure to enhance their digital capabilities and omnichannel services to retain customers who value convenience. The threat of substitution from DIY projects and second-hand markets also influences competitive dynamics. Brand loyalty is cultivated through consistent quality, superior customer service, and unique design aesthetics. Regulatory compliance regarding sustainability and labor practices serves as a differentiator for ethical brands. Overall, the market demands continuous innovation and strategic agility to sustain competitive advantage and profitability in this fragmented and evolving industry landscape.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. home decor market include

- The Home Depot Inc.

- Lowe’s Companies Inc.

- IKEA

- Williams-Sonoma Inc.

- Wayfair Inc.

TOP PLAYERS IN THE MARKET

- Wayfair Inc is a dominant force in the United States home decor market by operating as a pure play e-commerce retailer with an extensive catalog of furniture and home goods. The company leverages advanced technology and data analytics to provide personalized shopping experiences and efficient logistics solutions. Recently, Wayfair has invested heavily in augmented reality tools, allowing customers to visualize products in their homes before purchasing. This innovation reduces return rates and enhances customer confidence. The corporation also expanded its private label offerings to improve margins and differentiate its product assortment. By focusing on supply chain optimization and faster delivery times, Wayfair strengthens its competitive position. Their commitment to customer service and flexible financing options further drives loyalty. These strategic initiatives ensure that Wayfair remains a preferred destination for online home decor shopping while adapting to evolving consumer preferences for convenience and digital integration in the retail landscape.

- IKEA maintains a significant presence in the United States home decor market through its unique combination of affordable pricing, functional design, and sustainable practices. The company operates large-format stores that offer immersive shopping experiences alongside a robust online platform. Recently, IKEA has focused on expanding its urban footprint with smaller planning studios and pickup points to increase accessibility in major cities. The brand actively promotes circular economy principles by introducing buyback programs and using renewable materials in product manufacturing. IKEA also enhances its digital capabilities with improved mobile applications and virtual design services. These efforts align with growing consumer demand for eco-friendly and convenient home solutions. By balancing cost efficiency with innovative design, IKEA continues to attract a broad demographic. Their strategic investments in sustainability and omnichannel retailing strengthen their market position and reinforce their reputation as a leader in accessible and responsible home furnishing.

- Williams Sonoma Inc contributes significantly to the United States home decor market through its portfolio of premium brands, including Pottery Barn, West Elm, and Williams Sonoma. The company targets middle to upper income consumers seeking high-quality furniture and decorative accessories with distinct styles. Recently, Williams Sonoma has accelerated its digital transformation by integrating artificial intelligence into its customer engagement strategies. The corporation focuses on sustainable sourcing and ethical production practices, which resonate with environmentally conscious shoppers. They have also expanded their professional services, such as interior design consultations, to enhance customer value. By leveraging strong brand equity and exclusive product collections, Williams Sonoma differentiates itself from mass market competitors. Their investment in supply chain resilience ensures consistent product availability. These actions foster deep customer loyalty and drive repeat purchases. The company’s ability to blend traditional retail excellence with modern digital innovations solidifies its position as a key player in the premium home decor segment.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States home decor market employ several strategic initiatives to maintain competitiveness and drive growth. Product diversification remains a primary strategy with companies expanding their private label offerings to improve margins and brand loyalty. Brands are increasingly adopting omnichannel retail models that seamlessly integrate online and offline experiences to enhance customer convenience. Sustainability is a critical focus as manufacturers adopt eco-friendly materials and circular economy practices to appeal to environmentally conscious consumers. Digital innovation through augmented reality and artificial intelligence helps personalize shopping experiences and reduce return rates. Strategic partnerships with designers and influencers create exclusive collections that drive trend adoption. Companies also invest in supply chain optimization to ensure faster delivery and inventory efficiency. Price competitiveness is maintained through dynamic pricing strategies and promotional events. These strategies collectively enable companies to adapt to evolving consumer preferences and strengthen their market presence effectively in a dynamic retail environment.

MARKET SEGMENTATION

This research report on the U.S. home decor market has been segmented and sub-segmented into the following categories.

By Product Type

- Furniture

- Home Textiles

By Material

- Wood

- Metal

By Distribution Channel

- Home-Improvement & Furniture Stores

- Specialty Decor Stores

By Price Range

- Mass

- Premium / Luxury

By Room

- Living Room

- Bedroom

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. home decor market?

The U.S. home decor market covers accessories, furnishings, and decorative items used to improve home aesthetics and reflect personal style.

How does the U.S. home decor market function?

The U.S. home decor market operates through brands, retailers, and online stores selling products for every room and style preference.

What drives growth in the U.S. home decor market?

The U.S. home decor market grows from personalization demand, home improvement spending, and interest in stylish living spaces.

Which product categories lead the U.S. home decor market?

Wall decor, lighting, rugs, mirrors, and decorative accessories lead the U.S. home decor market due to broad household use.

How important is personalization in the U.S. home decor market?

Personalization is central to the U.S. home decor market because consumers want spaces that reflect individuality and taste.

What role does sustainability play in the U.S. home decor market?

Sustainable materials and eco-friendly products are gaining traction in the U.S. home decor market as buyers seek responsible choices.

How does e-commerce affect the U.S. home decor market?

E-commerce expands the U.S. home decor market by offering wider selection, convenience, and easier comparison shopping.

What trends shape the U.S. home decor market?

The U.S. home decor market is shaped by customizable items, artisanal products, and style-led room upgrades.

How do seasonal trends influence the U.S. home decor market?

Seasonal updates drive the U.S. home decor market through changes in color themes, accent pieces, and holiday decoration demand.

What is the role of wall decor in the U.S. home decor market?

Wall decor is a high-visibility category in the U.S. home decor market, helping consumers personalize rooms quickly.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com