U.S. Packaging Market Size, Share, Trends, and Growth Analysis Report, Segmented By Material Type, Product Type, Packaging Format, End User, & Region (U.S.), Industry Forecast From 2026 to 2034

U.S Packaging Market Size

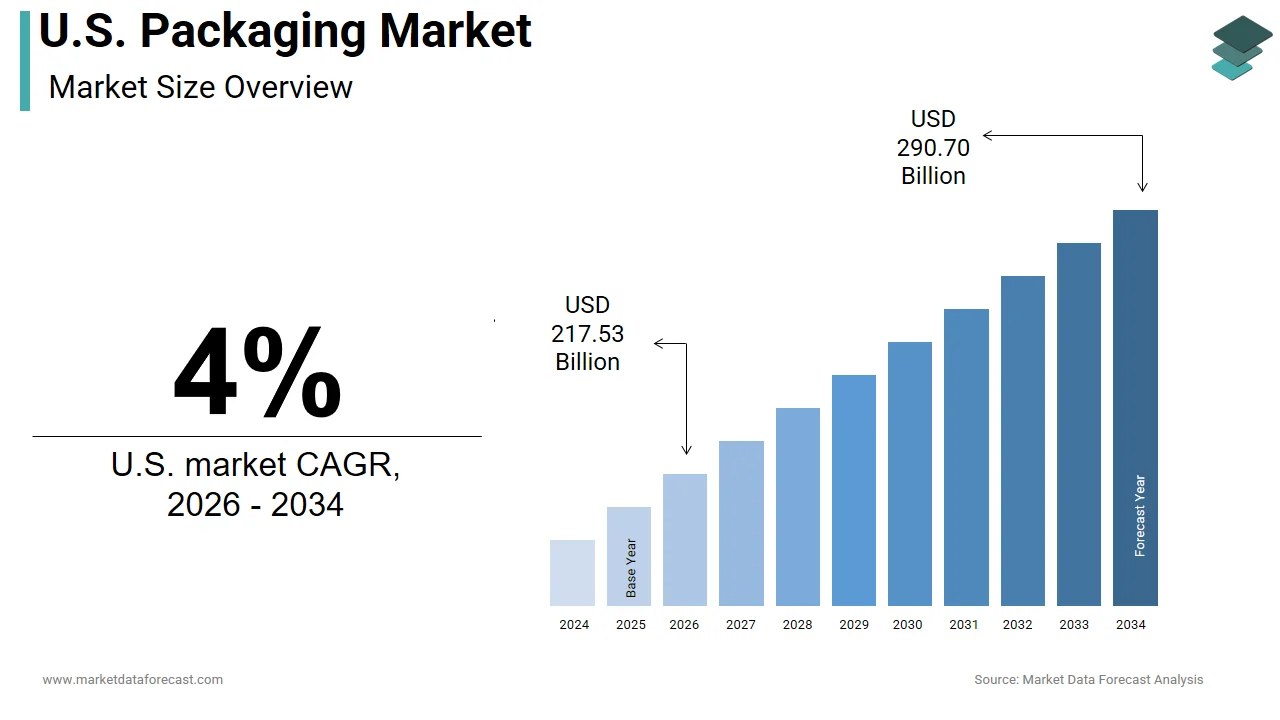

The U.S. packaging market was valued at USD 209.16 billion in 2025, is estimated to reach USD 217.53 billion in 2026, and is projected to reach USD 297.70 billion by 2034, growing at a CAGR of 4% from 2026 to 2034.

The packaging is an engineered interface between product integrity and consumer experience, evolving beyond mere containment to embody regulatory compliance, logistical efficiency, and brand signaling. Consumer purchasing behavior, as tracked by the Bureau of Labor Statistics, reveals that American households spent approximately $1,200 annually on packaged goods excluding food in 2021.

MARKET DRIVERS

Expansion of Online Retail and E-commerce

The meteoric expansion of online retail has reconfigured packaging demand from passive protection to dynamic, logistics-optimized architecture, which is one of the major driving factors for the growth of the U.S. packaging market. As per the U.S. Department of Commerce, e-commerce sales in the United States reached $1.03 trillion in 2023. This necessitates packaging that withstands multi-leg distribution, minimizes dimensional weight penalties, and integrates tamper evidence. Amazon’s 2023 Sustainability Report disclosed that 11.6% of its U.S. shipments utilized “frustration-free” packaging, reducing material use by 36% per unit. Retailers now demand modular, right-sized packaging; UPS found in its 2022 logistics audit that 24% of shipped boxes contained over 40% space, driving redesign mandates. Packaging is now engineered for algorithmic shipping efficiency.

Regulatory push for material accountability

Federal and state-level mandates are compelling material substitution, and lifecycle transparency is additionally leveraged to grow the growth of U.S. packaging market. As per the U.S. Food and Drug Administration, over 78 new packaging material clearances were issued in 2023 alone under its Food Contact Notification program for bio-based and recyclable substrates. California’s SB 54, enacted in 2022, requires all packaging to be recyclable or compostable by 2032 and mandates a 25% reduction in single-use plastic packaging by 2032.

MARKET RESTRAINTS

Material Cost Volatility Undermining Budget Certainty

Packaging manufacturers face acute exposure to commodity price swings, where feedstock costs dictate margin viability, which is degrading the growth of the U.S. packaging market. As per the American Chemistry Council, U.S. plastic resin output fell 4.1% year-over-year in Q1 2023 due to ethane supply constraints, which is exacerbating procurement instability.

Labor Shortages Disrupting Custom Packaging Workflows

The high-mix, low-volume custom packaging lines remain labor-intensive, and workforce scarcity is limiting the growth of the U.S. packaging market. As per the U.S. Bureau of Labor Statistics, the packaging manufacturing sector faced a 6.2% job vacancy rate in 2023. As per the Association for Packaging and Processing Technologies, 53% of U.S. packaging plants delayed client orders in 2023 due to insufficient skilled machine operators.

MARKET OPPORTUNITIES

AI-Driven Dynamic Packaging Personalization

The generative design and real-time consumer data now enable mass customization at scale, transforming packaging into a direct marketing channel, is creating new opportunities for the growth of the U.S. packaging market. As per McKinsey’s 2023 Consumer Packaged Goods Analytics Review, brands leveraging variable-data packaging saw a 19% uplift in repeat purchase rates. Coca-Cola’s “Freestyle” vending platform, deployed across 40,000 U.S. locations that allows consumers to customize bottle labels via app by generating 2.1 million unique designs monthly. Adobe’s 2023 Digital Experience Index confirmed that 64% of U.S. consumers are willing to pay 15% more for products with personalized packaging.

Circular Infrastructure Investment via EPR Legislation

The extended Producer Responsibility frameworks are a private investment in closed-loop systems, which is to substantially elevate the growth of the U.S. packaging market. As per the Product Stewardship Institute, 12 U.S. states enacted EPR packaging laws between 2021 and 2024, compelling brand owners to fund collection and reprocessing. Nestlé USA committed $25 million in 2023 to co-develop food-grade recycled polypropylene plants in Ohio and Texas.

MARKET CHALLENGES

Recyclability Claims vs. Reality in Multi-Material Laminates

The complex barrier packaging often evades municipal recovery systems due to incompatible polymer layers is one of the challenging factors for the growth of the U.S. packaging market. As per the Sustainable Packaging Coalition’s 2023 audit, only 9% of flexible multi-layer pouches placed into U.S. curbside bins were successfully recycled. The Ellen MacArthur Foundation’s U.S. Plastics Pact Tracker found that 63% of branded packaging labeled “recyclable” contained metallized films or adhesive laminates that conventional sorters cannot separate.

Cold Chain Packaging’s Carbon Intensity Under ESG Scrutiny

The temperature-sensitive logistics for biologics and premium perishables, which rely on expanded polystyrene and vacuum-insulated panels with high embedded emissions, are hindering the growth of the U.S. packaging market. As per the U.S. Department of Energy’s 2023 Cold Chain Efficiency Study, 41% of refrigerated packaging in transit exceeds required thermal thresholds, which indicates over-engineering.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Material Type, Product Type, Packaging Format, End User, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Amcor plc, International Paper Company, Mondi plc, Graphic Packaging Holding Company, Smurfit WestRock plc, and others. |

SEGMENTAL ANALYSIS

By Material Type Insights

The paper and paperboard segment held 38.7% of the U.S. packaging material market share in 2024. The U.S. Postal Service processed 7.6 billion parcels in 2023, 89% of which utilized corrugated paperboard, as per its internal logistics audit. Simultaneously, 42 states have introduced legislation restricting single-use plastics since 2021, per the National Conference of State Legislatures, accelerating brand migration to fiber-based alternatives. McDonald’s USA, for instance, transitioned 95% of its sandwich packaging to unbleached paperboard by Q4 2023, eliminating 3,200 metric tons of plastic annually.

The flexible plastic films segment is likely to experience a CAGR of 6.8% during the forecast period, with the lightweighting mandates and shelf-life extension imperatives. Walmart’s Project Gigaton recorded that switching rigid containers to stand-up pouches reduced per-unit shipping weight by 58% across 1,200 SKUs in 2023.

By Product Type Insights

The corrugated containers segment held 41.2% of the U.S. packaging product market share in 2024, with the omnichannel logistics resilience and automated handling compatibility. Amazon’s U.S. fulfillment network utilized 2.1 billion corrugated boxes in 2023, each engineered for robotic sortation and dimensional optimization, per its public sustainability metrics. Additionally, 96% of U.S. grocers, as per FMI’s Operational Benchmark, mandate corrugated for produce and dry goods due to stackability and moisture resistance.

The smart packaging systems segment is likely to grow with an expected CAGR of 12.4% during the forecast period, driven by the serialization mandates and real-time quality monitoring. The Drug Supply Chain Security Act requires full electronic traceability for pharmaceuticals by 2024, compelling 87% of top-50 U.S. drugmakers to embed NFC or RFID in primary packaging, per the Healthcare Distribution Alliance. In perishables, Zest Labs’ 2023 field trial demonstrated that time-temperature indicators reduced spoilage in berry shipments by 31%.

By End-User Insights

The food packaging segment was the largest and held 47.3% of the U.S. packaging market share in 2024. Its hegemony is sustained by portion control innovation and cold chain expansion. The U.S. frozen food market grew 5.8% in 2023, per the American Frozen Food Institute, demanding high-barrier multilayer pouches and vacuum skin packaging.

The pharmaceutical and medical packaging segment is growing lucratively with an expected CAGR of 9.1% during the forecast period, with biologics proliferation and anti-counterfeit regulation. Serialization compliance under DSCSA compelled 94% of U.S. drug packagers to adopt tamper-evident, trackable systems, as per the National Association of Boards of Pharmacy. Home healthcare trends amplify demand: Medicare data shows a 37% increase in self-administered injectables since 2020, which is necessitating auto-injector packaging with audible click confirmation and dose memory.

COUNTRY ANALYSIS

The United States packaging market was the largest contributor in the North America region, owing to the regulatory precocity and capital-intensive automation. Investment in Industry 4.0 infrastructure is unmatched, with the Association for Packaging and Processing Technologies recording $3.8 billion in robotics and vision system installations in U.S. plants in 2023 alone.

COMPETITIVE LANDSCAPE

Competition in the U.S. packaging market is a high-stakes convergence of material science, regulatory foresight, and logistical precision. Incumbents battle not for shelf space but for specification sheet embedding themselves into clients’ product development cycles, years ahead of launch. Rivalry manifests in patent races for mono-material laminates, proprietary coating chemistries, and AI-driven design automation. Regional converters compete on turnaround speed and customization depth, while multinationals leverage global compliance frameworks to standardize formats across borders. Talent wars intensify as packaging engineers become brand equity architects.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. packaging market include

- Amcor plc

- International Paper Company

- Mondi plc

- Graphic Packaging Holding Company

- Smurfit WestRock plc

Top Players in the U.S. Packaging Market

- International Paper anchors the U.S. fiber-based packaging ecosystem through vertically integrated mills and logistics-optimized containerboard networks. In the Asia Pacific, it operates coated paper and industrial packaging facilities in China, India, and Thailand, supplying multinational FMCG brands with region-specific sustainable substrates. The company commissioned a $300 million digital print integration center in Shanghai in Q1 2024, enabling real-time SKU customization for e-commerce clients across ASEAN with its innovation-led regional footprint without expanding its physical footprint.

- Amcor drives U.S. flexible and rigid plastic packaging innovation with a science-led approach to barrier performance and recyclability. In the Asia Pacific, it operates 27 manufacturing sites from Indonesia to South Korea, focusing on pharmaceutical and premium food segments. In late 2023, it inaugurated a Singapore-based Center for Packaging Excellence to co-develop shelf-life extending films with regional biotech firms. It also signed a long-term supply agreement with India’s Serum Institute for vaccine vial packaging compliant with WHO cold-chain standards.

- Ball Corporation dominates U.S. metal packaging with aerospace-grade precision in beverage and aerosol can manufacturing. In the Asia Pacific, it serves premium beverage and personal care brands through plants in China, India, and Japan. In 2023, it retrofitted its Kunshan facility with inert-gas-lined canning lines to serve oxygen-sensitive Japanese tea exporters. It co-developed lightweight, embossed aluminum bottles with Korean beauty brands to replace glass in e-commerce channels.

Top Strategies Used by Key Market Participants

Key players deploy material science innovation to preempt regulatory shifts, embedding recyclability and bio-sourcing into core R&D. They vertically integrate supply chains to lock in resin and fiber cost advantages, while digitalizing production for SKU agility. Strategic acquisitions target niche converters with regional compliance expertise, particularly in the Asia Pacific. Co-development labs with CPG giants accelerate time-to-market for sustainable formats.

MARKET SEGMENTATION

This research report on the U.S. packaging market has been segmented and sub-segmented into the following categories.

By Material Type

- Paper and Paperboard

- Plastics

- Polyethylene Terephthalate (PET)

- High-density Polyethylene (HDPE) and Low-density Polyethylene (LDPE)

- Polyvinyl Chloride (PVC)

- Polypropylene (PP)

- Other Plastics

- Metal

- Container Glass

By Product Type

- Paper and Paperboard Product Type

- Folding Cartons and Rigid Boxes

- Corrugated Boxes and Containers

- Shipping Bags and Pouches

- Other Paper and Paperboard Product Types

- Plastic Product Type

- Rigid Plastics

- Bottles and Jars

- Cups and Closures

- Trays and Pots

- Other Rigid Plastic Product Types

- Flexible Plastics

- Pouches

- Bags

- Wraps

- Other Flexible Plastic Product Types

- Rigid Plastics

- Metal Product Type

- Cans

- Caps and Closures

- Aerosol Containers

- Other Metal Product Types

- Container Glass Product Type

- Bottles

- Jars

By Packaging Format

- Flexible Packaging Format

- Rigid Packaging Format

By End User

- Food and Beverages

- Personal Care

- Pharmaceutical and Medical

- Household and Industrial

- Agriculture

- Other End Users

By Country

- U.S

Frequently Asked Questions

1. What is the U.S. Packaging Market and what factors are driving its growth?

The U.S. Packaging Market includes all materials, formats, and technologies used to protect, transport, and display products for industrial and consumer use, and its growth is fueled by e-commerce expansion, sustainability demand, and advanced manufacturing infrastructure

2. Which packaging materials dominate the U.S. Packaging Market?

Rigid plastics are the largest segment, while paper & paperboard is the fastest-growing segment due to the push toward eco-friendly packaging options

3. How is sustainability influencing the U.S. Packaging Market?

Sustainability drives packaging innovation, with companies adopting recyclable materials, biodegradable solutions, and meeting regulatory targets for waste reduction

4. What sectors are leading demand in the U.S. Packaging Market?

Food & beverage, healthcare, personal care, and e-commerce industries are the primary end-use sectors boosting packaging demand

5. What are some recent technological advancements in the U.S. Packaging Market?

Recent advances include smart packaging, improved barrier materials, digital printing, and automation in packaging lines

6. How is the e-commerce boom affecting the U.S. Packaging Market?

Surge in online shopping has led to increased demand for durable, branded, and innovative packaging to ensure product safety during transit and enhance customer experience

7. Who are the leading companies in the U.S. Packaging Market?

Major players include International Paper Co, WestRock Co, Amcor PLC, Berry Global, Mondi, Sealed Air Corp, Tetra Pak, Sonoco Products, and Graham Packaging

8. What challenges does the U.S. Packaging Market face?

Challenges include adapting to changing consumer preferences, rising material costs, stringent recycling regulations, and evolving sustainability standards

9. How are regulatory standards shaping the U.S. Packaging Market?

Regulatory mandates on packaging material recycling, labeling accuracy, and hazardous substance restriction force companies to continuously innovate and comply

10. What role does packaging play in branding and marketing in the U.S. Packaging Market?

Packaging enhances product visibility, communicates brand values, and directly influences consumer purchasing decisions through innovative designs and labeling

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com