- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

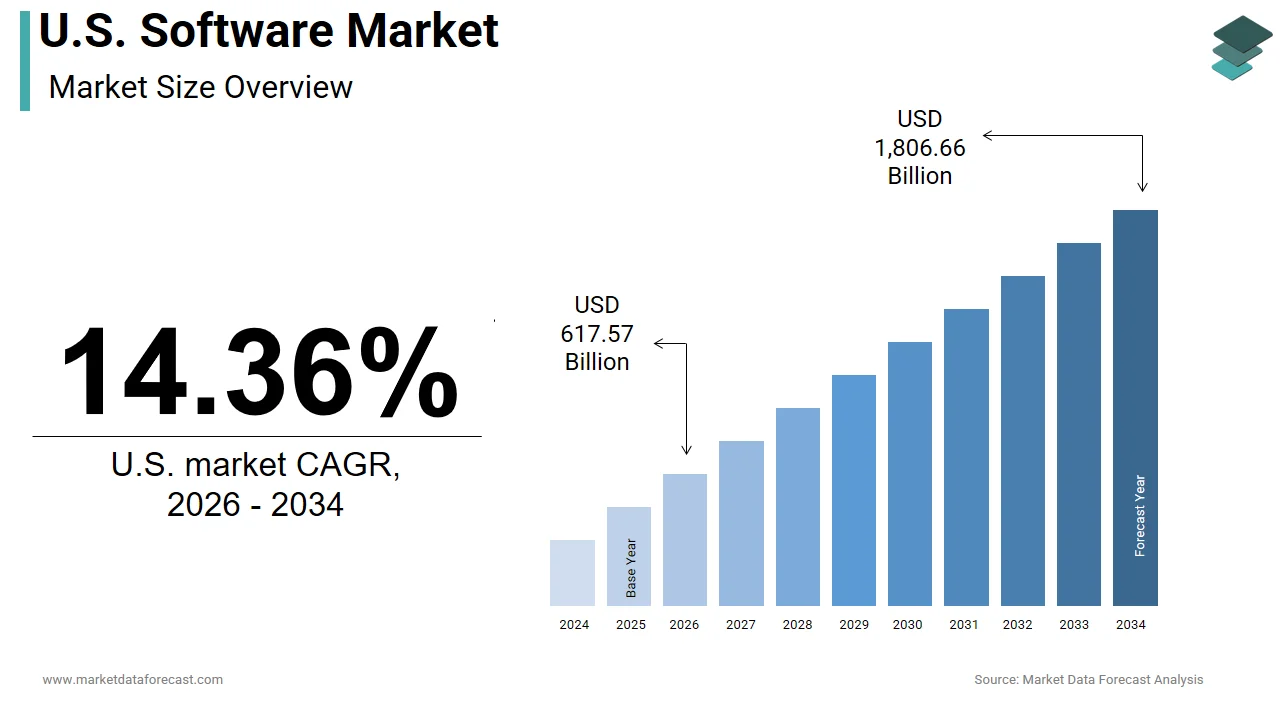

Market Size, 2025

$540.02 BnMarket Estimate, 2026

$617.57 BnMarket Forecast, 2034

$1,806.66 BnCAGR, 2026–2034

14.36%U.S. Software Market Report Summary

The U.S. software market was valued at USD 540.02 billion in 2025, is estimated to reach USD 617.57 billion in 2026, and is projected to reach USD 1,806.66 billion by 2034, growing at a CAGR of 14.36% from 2026 to 2034. Market growth is driven by rapid digital transformation across industries, increasing adoption of cloud computing, and the rising importance of data analytics and artificial intelligence. Businesses are investing heavily in enterprise software, cybersecurity, and automation tools to enhance operational efficiency and competitiveness. Additionally, the expansion of SaaS models and integration of AI-driven solutions are reshaping the software landscape in the United States.

Key Market Trends

- Rapid adoption of cloud computing and SaaS solutions.

- Increasing integration of AI, machine learning, and automation.

- Growing demand for cybersecurity and data protection software.

- Expansion of enterprise and financial software solutions.

- Rising investments in digital transformation initiatives.

Segmental Insights

- Based on type, the finance software segment dominated the United States software market by capturing 30.1% share in 2025, driven by strong demand for financial management, analytics, and compliance solutions.

Country-Level Insights

- The United States led the global software market by holding 45.3% share in 2025, supported by its advanced technological ecosystem, strong presence of leading software companies, and high enterprise IT spending. The country continues to dominate due to innovation in cloud computing, AI, and enterprise solutions.

Competitive Landscape

The U.S. software market is highly competitive, with companies focusing on innovation, cloud-based solutions, and AI-driven technologies. Strategic acquisitions, product development, and platform integration are key competitive strategies.

Prominent companies operating in the U.S. software market include Infor, Workday, Inc., Microsoft, Zoho Corporation Pvt. Ltd., Avid Technology, Inc., PreSonus Audio Electronics, Inc., Apple Inc., Adobe Inc., Cakewalk (BandLab Technologies), Oracle Corporation, Salesforce, Inc., Cockos Incorporated, MOTU, Inc., Verint Systems Inc., AxonSoft, and Honeywell International Inc..

U.S. Software Market Size

The U.S. software market reached USD 540.02 billion in 2025 and is expected to grow to USD 617.57 billion in 2026, and is anticipated to touch USD 1,806.66 billion by 2034, at a CAGR of 14.36% from 2026 to 2034.

Software is a collection of instructions, data, or programs used to operate computers and execute specific tasks. This market is the backbone of the digital economy, facilitating automation, data analysis, and connectivity across all industries. The market is characterized by a rapid shift toward cloud-based delivery models and subscription-based licensing, which has transformed how organizations procure and utilize technology. According to the U.S. Bureau of Labor Statistics, employment in computer and information technology occupations is projected to grow by 9% from 2023 to 2033, much faster than the average for all occupations. This growth is expected to result in about 356,700 net new jobs, though the industry will see an average of 377,500 openings each year due to growth and the need to replace workers who leave these occupations. This labor trend underscores the critical dependence of the US economy on software development and maintenance. Furthermore, according to the National Science Foundation’s (NSF) latest Business Enterprise Research and Development (BERD) survey data, domestic R&D performed by the software publishing industry (NAICS 5132/5112) reached $96.3 billion in 2022. This represents 14% of all U.S. business R&D and reflects a R&D-to-sales intensity of 13.7%, confirming a massive and sustained commitment to innovation. The integration of artificial intelligence and machine learning into standard software suites is redefining productivity benchmarks and operational efficiencies. Regulatory frameworks concerning data privacy and cybersecurity are increasingly shaping product development requirements. This dynamic environment reflects a mature yet rapidly evolving landscape where technological agility and continuous innovation determine competitive advantage and market leadership.

MARKET DRIVERS

Accelerated Digital Transformation Across Industries

Accelerated digital transformation across various industries is one of the major drivers of the United States software market. This compels organizations to adopt advanced software solutions to enhance operational efficiency and customer engagement. Companies are increasingly relying on cloud computing, enterprise resource planning, and customer relationship management software to streamline processes and gain competitive advantages. As per sources, spending on digital transformation technologies and services in the United States is expected to reach hundreds of billions of dollars as businesses prioritize modernization initiatives. The need for real-time data analytics and automated workflows drives demand for specialized software tools that can handle complex datasets and integrate disparate systems. Remote work trends have further accelerated this shift, requiring robust collaboration and communication platforms to maintain productivity. Industries such as healthcare, finance, and manufacturing are leveraging software to optimize supply chains, improve patient outcomes, and enhance financial security. The urgency to adapt to changing market conditions and consumer expectations forces organizations to continuously update their technology stacks. So, the widespread imperative for digital modernization fuels sustained growth in the software sector as enterprises seek scalable and flexible solutions to navigate the complexities of the modern business environment.

Integration of Artificial Intelligence and Machine Learning

The integration of artificial intelligence and machine learning also accelerates the growth of the United States software market. This enables the development of intelligent applications that offer predictive insights and autonomous decision-making capabilities. Software vendors are embedding AI algorithms into their products to enhance functionality, automate routine tasks, and personalize user experiences. As per a study, the adoption of artificial intelligence has doubled in recent years, with companies reporting substantial improvements in revenue and cost savings through AI-enabled software solutions. These technologies allow businesses to analyze vast amounts of data quickly, identifying patterns and anomalies that human analysts might miss. In sectors like cybersecurity, AI-driven software detects threats in real time, while in marketing, it optimizes ad targeting and content delivery. The availability of advanced development frameworks and cloud-based AI services lowers the barrier for software creators to incorporate these features. Consumers increasingly expect smart functionalities such as voice recognition and recommendation engines in their daily applications. This demand for intelligent automation and enhanced interactivity pushes software developers to innovate continuously. Thus, the pervasive adoption of AI and machine learning technologies drives substantial investment and growth in the software market as organizations strive to leverage data for strategic advantage.

MARKET RESTRAINTS

Cybersecurity Threats and Data Privacy Concerns

Cybersecurity threats and data privacy concerns continue to be a significant restraint on the United States software market. This increases the complexity and cost of software development and deployment. As software becomes more interconnected and reliant on cloud infrastructure, it becomes a prime target for cyberattacks, including ransomware, data breaches, and identity theft. According to the FBI Internet Crime Complaint Center (IC3) 2023 Annual Report, total potential losses from internet crime exceeded $12.5 billion in 2023, a 22% increase from the $10.3 billion reported in 2022. Investment fraud was the costliest category, accounting for $4.57 billion of those losses. Software companies must invest heavily in security protocols, encryption, and compliance measures to protect user data and maintain trust. Strict regulations such as the California Consumer Privacy Act impose rigorous standards for data handling, requiring companies to implement robust privacy controls. Non-compliance can result in hefty fines and reputational damage, discouraging rapid innovation and deployment. The constant evolution of threat vectors necessitates continuous updates and patches, which can disrupt service and increase operational burdens. Users are becoming more cautious about sharing personal information, leading to resistance against data-intensive applications. Hence, the heightened focus on security and privacy creates barriers to entry and slows down the adoption of new software solutions as organizations prioritize risk mitigation over feature expansion.

High Costs of Implementation and Maintenance

High costs of implementation and maintenance serve as a major restraint to the United States software market. This limits accessibility for small and medium-sized enterprises with constrained budgets. Enterprise-level software solutions often require significant upfront investment for licensing, customization, and integration with existing systems. As per the Small Business Administration, many small businesses struggle to allocate sufficient resources for technology upgrades due to competing financial priorities. The ongoing costs of subscription fees, technical support, and staff training add to the total cost of ownership, making it difficult for smaller organizations to sustain advanced software usage. Complex implementations often lead to downtime and productivity losses during the transition period, further discouraging adoption. Additionally, the rapid pace of technological obsolescence forces companies to frequently upgrade their software to remain compatible with new hardware and standards. This continuous cycle of investment strains financial resources and creates uncertainty regarding return on investment. Lack of in-house technical expertise necessitates hiring external consultants, which increases expenses. Consequently, the financial burden associated with acquiring and maintaining sophisticated software solutions restricts market penetration among smaller businesses, slowing overall growth despite the clear benefits of digital tools.

MARKET OPPORTUNITIES

Expansion of Cloud-Based Software as a Service Models

The expansion of cloud-based Software as a Service models offers new pathways for the United States software market. This offers flexible, scalable, and cost-effective solutions to businesses of all sizes. SaaS allows users to access software applications over the internet without the need for local installation or hardware maintenance, reducing initial capital expenditures. As per the Gartner Group, worldwide end-user spending on public cloud services is projected to grow substantially, with SaaS representing the largest segment of this market. This model enables companies to scale their software usage up or down based on demand, ensuring optimal resource utilization. Subscription-based pricing provides predictable costs and facilitates easier budget management for organizations. The ability to access data and applications from any location supports remote work and global collaboration, enhancing productivity. SaaS providers can deliver continuous updates and new features seamlessly, ensuring that users always have access to the latest technology. The lower barrier to entry encourages small businesses to adopt enterprise-grade tools that were previously inaccessible. Furthermore, the integration of AI and analytics into SaaS platforms adds value by providing actionable insights. Therefore, the shift toward cloud-based delivery models drives market growth by making software more accessible, adaptable, and efficient for diverse organizational needs.

Growth in Internet of Things and Edge Computing Applications

The growth in Internet of Things and edge computing applications sets the stage for the expansion of the United States software market. This creates demand for specialized software that manages and analyzes data from connected devices. As the number of IoT devices increases across industries such as manufacturing, healthcare, and logistics, there is a growing need for software that can process data in real time at the edge of the network. As per the International Data Corporation, the number of connected IoT devices worldwide is expected to reach tens of billions, generating massive volumes of data that require efficient management. Edge computing software reduces latency by processing data closer to the source, enabling faster decision-making and improved operational efficiency. This technology is critical for applications requiring immediate responses, such as autonomous vehicles and industrial automation. Software developers have the opportunity to create innovative solutions that integrate IoT devices with cloud platforms, providing comprehensive visibility and control. The ability to derive insights from decentralized data sources enhances predictive maintenance and resource optimization. Furthermore, the convergence of 5G technology with edge computing expands the potential for high-speed, low-latency applications. Consequently, the proliferation of IoT and edge computing drives demand for specialized software solutions that enable smarter and more responsive connected ecosystems.

MARKET CHALLENGES

Shortage of Skilled Technical Workforce

The shortage of skilled technical workforce is a serious impediment to the United States software market. This hampers the ability of companies to develop, maintain, and innovate software solutions effectively. The demand for software developers, data scientists, and cybersecurity experts far exceeds the available supply of qualified professionals. As per the United States Bureau of Labor Statistics, there are hundreds of thousands of unfilled job openings in the technology sector, creating intense competition for talent. This scarcity drives up salary expectations and increases recruitment costs for software firms, impacting profitability. The rapid evolution of technology requires continuous learning and upskilling, which many existing employees struggle to keep pace with. Companies face difficulties in finding candidates with expertise in emerging technologies such as artificial intelligence, blockchain, and cloud architecture. The lack of diverse talent pools further limits innovation and problem-solving capabilities within teams. Educational institutions often lag behind industry needs, resulting in graduates who lack the practical skills required for immediate contribution. So, the workforce gap slows down project timelines and limits the capacity for innovation, forcing companies to rely on outsourcing or automation, which may not fully address the complexity of custom software development.

Rapid Technological Obsolescence and Compatibility Issues

Rapid technological obsolescence and compatibility issues negatively impact the growth of the United States software market. These hurdles create uncertainty and increase the complexity of software management. The fast pace of innovation means that software versions and platforms become outdated quickly, requiring frequent updates and migrations. As per the Standish Group, a significant percentage of software projects fail to meet their original goals due to changing requirements and technological shifts. Maintaining compatibility between legacy systems and new software applications is a persistent struggle for organizations, leading to integration challenges and data silos. Users often face disruptions when software updates introduce bugs or change interfaces, requiring retraining and adjustment. The fragmentation of operating systems and devices complicates the development process as software must be tested across multiple environments. Vendor lock-in situations make it difficult for companies to switch providers without incurring high conversion costs. The inability to seamlessly integrate diverse software tools hinders workflow efficiency and data consistency. Thus, the constant need to adapt to new technologies and resolve compatibility issues creates operational friction and increases the total cost of ownership for software users.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Infor, Workday, Inc., Microsoft, Zoho Corporation Pvt. Ltd., Avid Technology, Inc., PreSonus Audio Electronics, Inc., Apple Inc., Adobe Inc., Cakewalk (BandLab Technologies), Oracle Corporation, Salesforce Inc., Cockos Incorporated, MOTU, Inc., Verint Systems Inc., AxonSoft, Honeywell International Inc., and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The finance software segment led the United States software market and captured a 30.1% share in 2025. This leading position of the segment is attributed to the critical necessity for accurate financial management, regulatory compliance, and strategic decision-making across all business sectors. Also, this segment includes enterprise resource planning, accounting, tax preparation, and financial analysis tools that are indispensable for operational continuity. As per the United States Bureau of Labor Statistics, the finance and insurance sector employs millions of individuals who rely heavily on specialized software to process transactions, manage risks, and generate reports. A key driver for this domination is the increasing complexity of financial regulations, such as the Sarbanes-Oxley Act and Generally Accepted Accounting Principles, which mandate rigorous data tracking and auditing capabilities. Organizations invest significantly in finance software to automate these processes, reducing human error and ensuring compliance. Furthermore, the shift toward real-time financial reporting enables executives to make informed decisions quickly, enhancing competitive advantage. The integration of artificial intelligence for fraud detection and predictive analytics further solidifies the value proposition of finance software. Small and medium enterprises also contribute to this dominance by adopting cloud-based accounting solutions that offer affordability and scalability. The universal need for financial transparency and efficiency ensures that finance software remains a foundational component of the software ecosystem. Consequently, the regulatory, operational, and strategic imperatives facing businesses cement finance software as the largest and most stable segment in the market.

The antivirus and security software segment is likely to experience the fastest CAGR of 12% from 2026 to 2034 due to the escalating frequency and sophistication of cyber threats. Moreover, the attack surface for malicious actors expands as digital transformation accelerates. Therefore, robust protective measures are necessary for individuals and organizations alike. According to the FBI Internet Crime Complaint Center (IC3) 2024 State of the Web Report, total potential losses from internet crime reached $13.8 billion in 2024, a notable increase from the $12.5 billion reported in 2023. This trend underscores the escalating financial toll of security breaches and the critical demand for advanced AI-driven cybersecurity defenses. The primary factor driving this growth is the rise in ransomware attacks, phishing schemes, and data breaches targeting sensitive personal and corporate information. Remote work trends have further exacerbated vulnerabilities as employees access corporate networks from unsecured home environments, requiring comprehensive endpoint security solutions. Government mandates and industry standards, such as the Health Insurance Portability and Accountability Act, compel organizations to implement stringent cybersecurity protocols, driving demand for compliant antivirus software. Additionally, the proliferation of Internet of Things devices creates new entry points for attacks, necessitating specialized security tools. Consumers are increasingly aware of digital privacy risks, leading to higher adoption of personal security suites. Consequently, the persistent threat landscape and regulatory pressures accelerate the rapid expansion of the antivirus and security software segment.

COUNTRY LEVEL ANALYSIS

U.S. Software Market Analysis

The United States dominated the global software market and accounted for a 45.3% share in 2025. This growth trajectory of the US market is supported by its robust technological infrastructure, high innovation capacity, and substantial investment in research and development. The country’s market status is characterized by a mature and highly competitive ecosystem where leading global software corporations originate and operate. As per the National Science Foundation, business expenditure on research and development in the software publishing industry exceeds 50 billion dollars annually, reflecting a strong commitment to innovation and product advancement. The presence of major technology hubs such as Silicon Valley, Seattle, and Boston fosters a culture of entrepreneurship and talent attraction that fuels continuous growth. High levels of digital literacy and broadband penetration ensure widespread adoption of software solutions across consumer and enterprise segments. Regulatory frameworks regarding intellectual property protection and data privacy provide a stable environment for business operations and investment. The United States serves as a trendsetter for global software standards, influencing development practices and consumer expectations worldwide. The convergence of artificial intelligence, cloud computing, and big data analytics within the US market drives significant advancements that are exported globally. The combination of economic strength, technological leadership, and supportive policy environments solidifies the United States position as the dominant force in the global software industry.

COMPETITIVE LANDSCAPE

The competition in the United States software market is intense and characterized by the presence of established technology giants, agile startups, and specialized niche providers vying for dominance. Major players compete based on innovation, feature richness, ease of use, and integration capabilities to attract and retain customers. Differentiation is achieved through proprietary algorithms, superior user experience, and comprehensive ecosystem support. Price competition is moderate as enterprises prioritize value, reliability, and security over initial cost savings. The market sees continuous disruption from new entrants leveraging open source technologies and low-code platforms to democratize software development. Customer loyalty is driven by seamless integration with existing workflows and robust customer support services. Regulatory compliance and data sovereignty requirements influence competitive dynamics as firms navigate complex legal landscapes. Strategic partnerships and alliances are common to expand market reach and enhance product offerings. The rapid pace of technological change requires constant adaptation and investment in research and development. Success depends on balancing innovation with stability and addressing evolving customer needs effectively.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. software market include

- Infor (U.S.)

- Workday, Inc. (U.S.)

- Microsoft (U.S.)

- Zoho Corporation Pvt. Ltd. (India)

- Avid Technology, Inc. (U.S.)

- Presonus Audio Electronics, Inc. (U.S.)

- Apple Inc. (U.S.)

- Adobe Inc. (U.S.)

- Cakewalk (BandLab Technologies)

- Oracle Corporation

- Salesforce Inc

- Cockos Incorporated (U.S.)

- MOTU, Inc. (U.S.)

- Verint Systems Inc. (U.S.)

- AxonSoft (U.S.)

- Honeywell International Inc. (U.S.)

TOP PLAYERS IN THE MARKET

- Microsoft Corporation is a dominant entity in the United States software market, offering a comprehensive suite of productivity cloud and enterprise solutions. The company leverages its Azure cloud platform and Office 365 suite to serve millions of users globally. Recent actions include significant investments in artificial intelligence integration across its product lines, enhancing user productivity and automation capabilities. Microsoft has expanded its cybersecurity offerings to address growing threats, ensuring robust protection for enterprise clients. The company focuses on hybrid work solutions, enabling seamless collaboration and data access. By prioritizing interoperability and open standards, Microsoft strengthens its ecosystem. These initiatives reinforce its position as a leader in digital transformation, providing scalable and secure software infrastructure for businesses and individuals alike.

- Oracle Corporation contributes significantly to the United States software market through its extensive database management systems and enterprise resource planning applications. The company provides critical infrastructure for data storage, analytics, and business operations across various industries. Recent actions involve the expansion of its cloud infrastructure services to support high-performance computing and artificial intelligence workloads. Oracle has enhanced its autonomous database capabilities, reducing manual management tasks for clients. The company focuses on industry-specific cloud solutions catering to healthcare, finance, and retail sectors. By integrating advanced security features and compliance tools, Oracle ensures data integrity. These efforts strengthen its market presence by delivering reliable and efficient software solutions that drive operational excellence and innovation for enterprise customers.

- Salesforce Inc plays a pivotal role in the United States software market by leading the customer relationship management sector with its cloud-based platforms. The company offers a wide array of tools for sales, marketing, service, and commerce, enabling businesses to connect with customers effectively. Recent actions include the acquisition of specialized AI firms to enhance its Einstein AI capabilities, providing predictive insights and automation. Salesforce has expanded its industry clouds to address specific vertical needs such as healthcare and financial services. The company emphasizes sustainability and social responsibility within its software offerings. By fostering a robust ecosystem of partners and developers, Salesforce drives innovation. These strategies solidify its position as a key enabler of digital customer engagement and business growth.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States software market primarily focus on integrating artificial intelligence and machine learning to enhance product functionality and automate complex tasks. Companies are increasingly adopting cloud native architectures to ensure scalability, flexibility, and remote accessibility for users. Strategic acquisitions of niche technology firms enable rapid expansion into emerging sectors and the acquisition of specialized talent. Emphasis on cybersecurity and data privacy builds trust and ensures compliance with evolving regulatory standards. The development of industry-specific solutions addresses unique operational challenges and drives deeper customer engagement. Subscription-based pricing models provide predictable revenue streams and improve customer retention rates. Partnerships with hardware manufacturers and telecommunications providers facilitate seamless integration and broader market reach. Continuous investment in research and development fosters innovation and maintains competitive advantage in a rapidly evolving technological landscape.

U.S. SOFTWARE MARKET NEWS

- In March 2024, Microsoft Corporation integrated advanced AI features into Office 365 to enhance productivity and strengthen its software market presence in the US

- In May 2024, Oracle Corporation expanded its cloud infrastructure services to support AI workloads and strengthen the Us software market presence

- In November 2024, Oracle Corporation introduced industry-specific cloud solutions for healthcare to address unique needs and strengthen its software market presence in the US.

MARKET SEGMENTATION

This research report on the U.S. software market has been segmented and sub-segmented into the following categories.

By Type

- Finance

- Video

- Antivirus

- Music

- Resume

- Ad Spam

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.