Asia Pacific Beer Market Size, Share, Trends & Growth Forecast Report, Segmented By Type, Distribution Channel, And Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC), Industry Analysis (2026 to 2034)

Market Size, 2025

$243.33 BnMarket Estimate, 2026

$256.30 BnMarket Forecast, 2034

$388.30 BnCAGR, 2026–2034

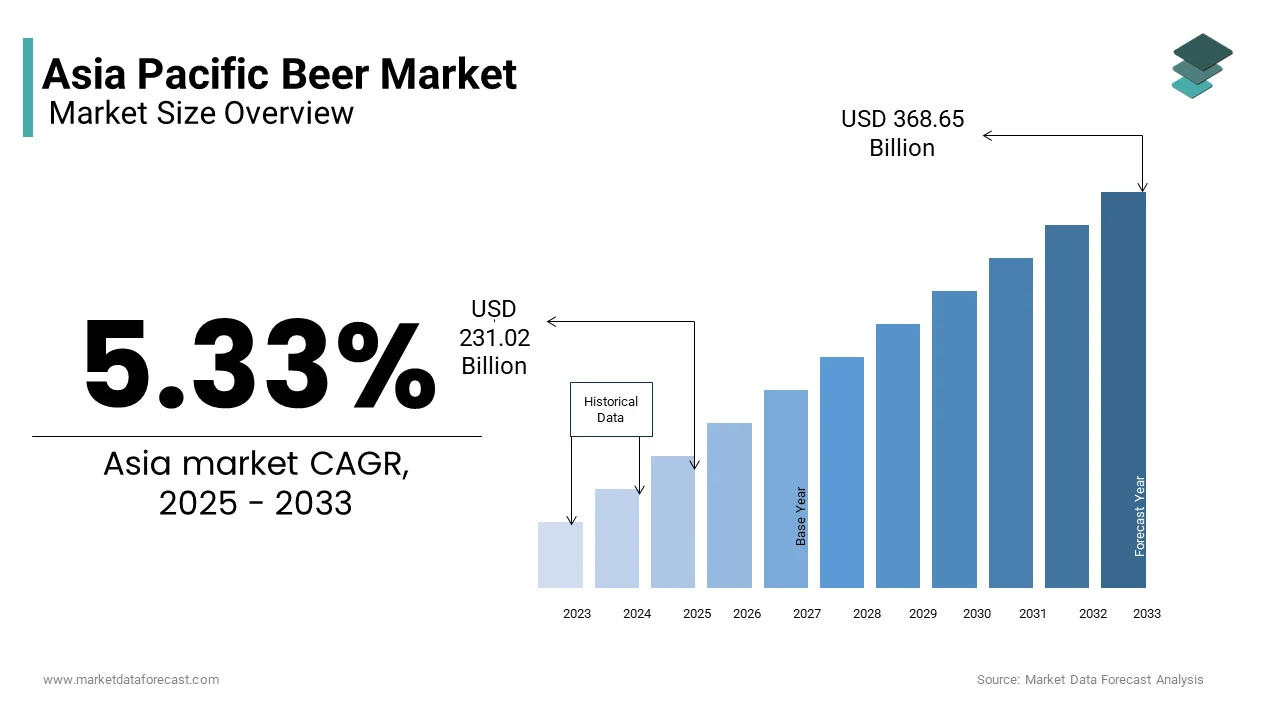

5.33%Asia Pacific Beer Market Size

The Asia Pacific beer market size was valued at USD 243.33 billion in 2025 and is anticipated to reach USD 256.30 billion in 2026 to reach USD 388.30 billion by 2034, growing at a CAGR of 5.33% during the forecast period from 2026 to 2034.

The beer is a diverse and dynamic landscape of brewing, consumption, and distribution across countries ranging from China and India to Australia and Japan. Characterized by a blend of traditional brewing cultures and modern consumer preferences, this market has evolved significantly over the past decade. It includes both mass-produced lagers that dominate volume sales and an emerging segment of craft and premium beers gaining traction among younger, urban demographics.

Beer in the Asia Pacific region is more than just a beverage as it is deeply embedded in social customs, festivals, and business interactions. In countries like Japan and South Korea, beer remains a staple at corporate dinners and casual gatherings, while in Southeast Asia, it plays a key role during celebrations and local festivities. The increasing influence of Western drinking habits, combined with rising disposable incomes and expanding retail infrastructure, has further fueled market growth.

MARKET DRIVERS

Urbanization and Changing Lifestyles

One of the primary drivers fueling the Asia Pacific beer market is rapid urbanization, which has transformed consumer behavior and spending patterns. In countries like India and Indonesia, urban centers have seen a rise in young working professionals who prefer socializing in pubs, cafes, and rooftop bars—venues where beer is a dominant beverage choice. According to the World Bank, urban populations in APAC countries grew by an average of 1.5% annually between 2015 and 2023, creating a larger base of potential beer consumers. Additionally, the growing influence of digital platforms and social media has played a crucial role in shaping beer consumption habits. Influencer marketing, online beer delivery services, and brand storytelling campaigns have made beer more accessible and appealing to millennials and Gen Z.

Growth of Premium and Craft Beer Segments

The emergence and expansion of the premium and craft beer segments represent a significant driver in the Asia Pacific beer market. Consumers in developed economies such as Australia, Japan, and South Korea are shifting away from mass-produced lagers in favor of high-quality, artisanal brews that offer unique flavors and locally inspired ingredients. This movement is being led by a younger, more adventurous consumer base that values authenticity, innovation, and experience. Moreover, governments in several APAC countries have introduced favorable policies to support small-scale brewers, including tax incentives and simplified licensing procedures. This regulatory easing has enabled entrepreneurs to enter the market and innovate freely, contributing to a richer and more diverse beer ecosystem.

MARKET RESTRAINTS

Regulatory Restrictions and Alcohol Control Policies

A major restraint affecting the Asia Pacific beer market is the presence of stringent alcohol control policies and regulatory restrictions across several countries. Governments in regions such as the Middle East and parts of South Asia have implemented strict laws governing the sale, advertising, and consumption of alcoholic beverages, which are limiting market expansion opportunities. Even within the broader Asia Pacific region, countries like India face fragmented regulations due to state-level excise policies, where some states enforce partial or complete prohibition. Similarly, in Malaysia, alcohol taxation and limited retail availability due to religious sensitivities constrain market growth. Furthermore, public health initiatives aimed at curbing alcohol-related illnesses have led to increased scrutiny and tighter controls in countries like Thailand and South Korea. These evolving policy landscapes present ongoing challenges for beer producers seeking stable and predictable operating conditions across the Asia Pacific region.

Health Awareness and Changing Consumer Attitudes

An emerging challenge for the Asia Pacific beer market is the growing awareness around health and wellness, leading to a shift in consumer attitudes toward alcohol consumption. This trend is particularly noticeable in urban centers across Australia, Japan, and Singapore, where health-conscious consumers are driving demand for lighter beverages such as hard seltzers, zero-alcohol beers, and functional drinks infused with vitamins or probiotics. Additionally, workplace wellness programs and corporate health initiatives are influencing professional drinking habits, especially among white-collar workers in metropolitan areas. Companies in countries like South Korea and India are promoting responsible drinking policies, further reinforcing this cultural shift. Media coverage and government-led anti-alcohol campaigns have also contributed to changing perceptions.

MARKET OPPORTUNITIES

Expansion of E-commerce and Direct-to-Consumer Sales

The rapid expansion of e-commerce and direct-to-consumer (DTC) sales channels is substantially to create huge growth opportunities for the Asia Pacific beer market. In China, for instance, platforms like JD.com and Tmall have become key distribution channels for both domestic and imported beers, offering consumers a wider selection and doorstep delivery. Similarly, in India, where off-trade remains the dominant sales channel due to regulatory restrictions, DTC models have gained traction in states like Goa and Maharashtra. Australia and Japan have also seen a rise in subscription-based beer services, where consumers receive curated selections of craft and seasonal brews at regular intervals.

Innovation in Product Development and Flavor Experimentation

Product innovation and flavor experimentation present a significant opportunity for growth in the Asia Pacific beer market. Craft breweries and multinational brands alike are investing in research and development to introduce new flavors, ingredient combinations, and brewing techniques tailored to regional palates. For example, in Southeast Asia, fruit-infused beers using tropical flavors like lychee, mango, and passionfruit have gained popularity among younger consumers. In Japan, brewers are experimenting with sake-infused beers and hop-forward IPAs to cater to a more sophisticated and adventurous drinker base. Additionally, health-focused innovations such as low-calorie, gluten-free, and plant-based beers are gaining traction, especially in Australia and New Zealand, where dietary consciousness is on the rise. These product advancements not only attract new consumers but also encourage repeat purchases and brand loyalty.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Cost Volatility

A significant challenge confronting the Asia Pacific beer market is the volatility in raw material prices and disruptions in the supply chain, which impact production costs and profit margins. Key ingredients such as barley, hops, and packaging materials have experienced price fluctuations due to climate change, geopolitical tensions, and transportation bottlenecks.

For example, extreme weather events in major barley-producing regions like Australia and Canada have affected crop yields, leading to shortages and cost increases. Packaging materials, particularly aluminum cans and glass bottles, have also seen sharp price increases. Rising energy costs and environmental regulations have further compounded the issue, making sustainable packaging solutions expensive to implement.

Intensifying Competition from Non-Alcoholic and Alternative Beverages

Intensifying competition from non-alcoholic and alternative beverages poses a growing challenge to the Asia Pacific beer market. Consumers are increasingly opting for healthier, low-calorie, or functional beverages such as kombucha, sparkling water, ready-to-drink teas, and mocktails, which mimic the sensory experience of beer without the alcohol content. This shift is particularly pronounced in urban markets like Singapore, South Korea, and Australia, where health-conscious millennials and Gen Z consumers are driving demand for alternatives that align with fitness goals and sober-curious lifestyles. Beverage giants like Coca-Cola and PepsiCo have capitalized on this trend by launching their lines of functional and fermented non-alcoholic drinks, intensifying competition for traditional beer brands. Even within the beer category, innovations such as zero-alcohol lagers and flavoured malt beverages are blurring boundaries and fragmenting consumer attention.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.33% |

| Segments Covered | By Type, Distribution Channel, And Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of APAC |

| Market Leaders Profiled | Anheuser-Busch InBev, Beijing Yanjing Brewery Ltd, Carlsberg Group, China Resources Enterprise, Heineken NV, Kirin Holdings Co. Ltd, Asahi Breweries Ltd, Tsingtao Brewery, SABMiller PLC, United Breweries Group (UB Group). |

SEGMENTAL ANALYSIS

By Type Insights

The lager segment dominated the Asia Pacific beer market by holding a dominant share in 2025 with its widespread consumer preference across major markets like China, India, and Southeast Asia. Lagers are known for their crisp, clean taste and lower bitterness compared to other types such as ale or stout, making them more palatable to a broader demographic. Another key driver is the strong presence of large-scale brewing companies such as Anheuser-Busch InBev and Kirin Brewery Company, which have heavily invested in lager production due to its scalability and longer shelf life. For instance, in China alone, Tsingtao Brewery, one of the largest producers of lager-style beers, reported a revenue of over CNY 30 billion in 2023, reflecting robust domestic demand.

The ale segment is projected to grow with a CAGR of 8.2% in the coming years, with the increasing disposable income among millennials and Gen Z consumers who are willing to pay a premium for unique, high-quality products. In Japan, for example, the craft beer market was valued at JPY 200 billion in 202, with a significant portion attributed to ale varieties, as reported by Japan External Trade Organization (JETRO). These consumers are increasingly seeking out flavorsome, artisanal, and locally brewed options that offer a differentiated experience compared to mass-produced lagers. Additionally, government support and easing regulations around microbreweries have encouraged entrepreneurship in this space.

By Distribution Channel Insights

The off-trade segment accounted for a prominent share of the Asia Pacific beer market in 2025, with the rising trend of home consumption in densely populated urban areas, where people prefer drinking in private settings. In India, for instance, off-trade channels accounted for over 70% of beer sales in 2023 due to strict alcohol laws in certain states that limit public drinking, as noted by IWSR Drinks Market Analysis. Similarly, in Malaysia, where alcohol consumption is restricted in Muslim-majority regions, off-trade remains the preferred channel for legal buyers. Furthermore, promotional activities and bulk purchasing discounts offered by off-trade retailers enhance consumer attraction. In Australia, Woolworths and Coles frequently run beer promotions, which contribute to higher household purchases, especially during sporting events and holidays.

The on-trade distribution segment is poised to grow with a CAGR of 6.8% in the coming years. Post-pandemic recovery in hospitality sectors across the region has significantly boosted on-trade sales. In Japan, for example, bar and restaurant footfall increased by over 40% in 2023, according to the Japan Food Service Association, leading to higher beer consumption in these venues. The reopening of pubs and gastropubs in India, especially in metropolitan cities like Mumbai and Bangalore, has also contributed to a 12% YoY increase in on-trade beer sales as reported Craft beer bars and brewpubs are playing a pivotal role in driving this growth. Cities like Bangkok, Sydney, and Seoul have seen a surge in specialized beer bars that serve local and international ale variants, creating a niche yet rapidly expanding market. In South Korea, the number of craft beer cafes increased by more than 20% in 2023, per the Korea Craft Beer Association.

COUNTRY-LEVEL ANALYSIS

China Beer Market Analysis

China was the largest contributor in the Asia Pacific beer market by accounting for 30.3% of the share in 2025. Urbanization and rising disposable incomes have led to increased beer consumption, particularly among young professionals and middle-class consumers. Domestic brands like Snow Beer and Tsingtao continue to dominate, but there's also a growing appetite for imported and premium beers, especially in first-tier cities like Shanghai and Beijing. The government’s relaxation of licensing norms for microbreweries has spurred innovation and diversity in the market. By 2023, the number of craft breweries in China had grown to over 2,000, up from just a few hundred in 2018, as reported by China Daily.

India Beer Market Analysis

India's beer market held 15.4% of the share in 2024, with the rapid urbanization and modernization of lifestyles, particularly among the youth demographic. The 18–35 age group constitutes the largest consumer base, with rising disposable incomes and exposure to global drinking trends fueling demand for premium and craft beers. However, state-level excise policies remain a critical factor shaping the market. States like Goa and Kerala allow relatively liberal alcohol sales, while others like Bihar and Gujarat enforce partial or full prohibition. The entry of international players like Carlsberg and Heineken into the Indian market has intensified competition and raised product quality standards. Additionally, the emergence of local craft breweries such as Bira 91 and White Owl has diversified the market, appealing to niche segments and contributing to double-digit growth in premium beer categories.

Japan Beer Market Analysis

Japan beer market is expected to grow with the highest CAGR in the coming years. Beer remains a staple beverage in Japanese culture, especially during social gatherings and business dinners. A notable trend is the revival of draft beer consumption, particularly in izakayas (Japanese pubs), which saw a 15% rebound in sales post-pandemic, according to JETRO. Domestic giants like Asahi, Kirin, and Sapporo have responded by introducing innovative flavors and eco-friendly packaging to attract environmentally conscious consumers.

Australia Beer Market Analysis

The Australian beer market is poised to have significant growth opportunities in the coming years. Government support for small brewers through tax incentives and reduced licensing barriers has spurred innovation and diversification. By 2023, Australia had over 700 craft breweries, up from fewer than 500 in 2020. This proliferation has been accompanied by rising consumer interest in locally sourced, sustainable, and flavor-rich products.

South Korea Beer Market Analysis

South Korea's beer market is expected to have a steady pace with a blend of traditional preferences for mass-produced lagers and a growing inclination toward craft and premium beer varieties. The rise of craft breweries and beer cafés in cities like Seoul and Busan has created a vibrant beer culture, reminiscent of Western trends. By 2023, the number of registered microbreweries in South Korea had surpassed 300, doubling since 2019, per the Korea Craft Beer Association. Alcohol consumption is deeply embedded in Korean social customs, especially in corporate and familial settings. The easing of import tariffs and increased exposure to global beer styles have also contributed to a more diverse and competitive market landscape.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific beer market is highly dynamic, shaped by a mix of global giants, regional leaders, and emerging craft breweries. While multinational corporations dominate with their vast resources, established distribution networks, and strong brand recognition, they face increasing pressure from local players who understand regional tastes and regulatory environments better. Consumer preferences are rapidly evolving, with a growing demand for premium, craft, and health-conscious beer options, prompting both large and small brewers to innovate continuously. Additionally, the rise of microbreweries and taproom concepts has introduced new levels of competition, especially in urban centers where experiential consumption is gaining traction. Regulatory challenges, such as alcohol taxes and restrictions in certain countries, further complicate market entry and expansion strategies. Companies must balance between mass-market appeal and niche offerings to remain relevant. Sustainability and digital engagement have become critical differentiators, with leading players investing heavily in eco-friendly production and data-driven marketing.

KEY MARKET PLAYERS

These are the market players that are dominating the Asia paPacificeer market, including

- Anheuser-Busch InBev

- Beijing Yanjing Brewery Ltd

- Carlsberg Group

- China Resources Enterprise

- Heineken NV

- Kirin Holdings Co. Ltd

- Asahi Breweries Ltd

- Tsingtao Brewery

- SABMiller PLC

- United Breweries Group (UB Group).

Top Players In The Market

- AB InBev is a dominant global brewing giant with a strong presence across the Asia Pacific region. The company leverages its extensive brand portfolio, including global names like Budweiser and Corona, to maintain relevance in diverse markets such as China, India, and Southeast Asia. Its operations in the region are supported by local partnerships and acquisitions by enabling it to adapt to regional tastes while maintaining global standards. AB InBev plays a pivotal role in shaping consumption trends through innovation, sustainability initiatives, and digital transformation in supply chain management. Its influence extends beyond volume sales, impacting industry practices and regulatory frameworks.

- Kirin is one of Japan’s most iconic brewing companies and a key player in the Asia Pacific beer market. With a deep-rooted legacy in Japanese beer culture, Kirin has expanded its footprint across Southeast Asia through strategic investments and acquisitions. The company owns several regional breweries and brands, allowing it to cater to both mainstream and premium segments. Kirin's emphasis on quality, product diversification, and sustainable brewing practices has strengthened its position. It also contributes significantly to the global beer market through research and development in brewing technologies and health-conscious formulations, which is influencing broader market dynamics.

- Carlsberg maintains a strong foothold in the Asia Pacific region, particularly in markets like China, Vietnam, and India. Known for its eponymous flagship brand, Carlsberg has successfully localized its offerings to suit regional preferences while upholding international brewing standards. The company's "Carlsberg Green” sustainability strategy has set benchmarks in eco-friendly brewing practices globally. Through joint ventures and local partnerships, Carlsberg has built a resilient distribution network that supports both urban and rural market penetration. Its commitment to innovation, responsible drinking campaigns, and digital marketing strategies enhances its competitive edge in the evolving beer landscape.

Top Major Strategies Used by Key Players in the Market

Product Diversification and Premiumization

Leading players are expanding their portfolios to include craft, flavored, and low-alcohol beers to cater to changing consumer preferences. Companies aim to capture high-value segments and attract younger, more adventurous drinkers who seek unique experiences and better quality by introducing premium variants and limited-edition brews.

Strategic Partnerships and Local Acquisitions

To strengthen their regional presence and navigate complex regulatory landscapes, major brewers are forming joint ventures or acquiring local breweries. These moves help them gain market access, reduce operational costs, and tailor products to local tastes while leveraging global brand equity and distribution networks.

Digital Transformation and E-commerce Expansion

Brewers are investing in digital platforms to enhance consumer engagement, streamline supply chains, and boost online sales. From AI-driven marketing to direct-to-consumer models, digital tools are being used to improve customer experience, track consumption trends, and optimize inventory management across both on-trade and off-trade channels.

RECENT MARKET NEWS

- In March 2024, Carlsberg Group launched a new line of low-alcohol beers across Southeast Asia, targeting health-conscious consumers and aligning with shifting lifestyle trends. This move was aimed at capturing the growing segment of drinkers seeking lighter alternatives without compromising on taste.

- In July 2023, Kirin Brewery Company expanded its presence in Vietnam through the acquisition of a majority stake in a local craft brewery by enhancing its product diversity and strengthening its foothold in the country's rising premium beer market.

- In November 2023, Anheuser-Busch InBev (AB InBev) partnered with a leading e-commerce platform in India to boost its digital retail reach by aiming to expand its consumer base through direct-to-consumer sales and personalized marketing strategies.

- In February 2024, Tsingtao Brewery announced a major investment in sustainable packaging solutions, introducing recyclable cans and reducing carbon emissions across its production facilities in China, which is reinforcing its commitment to environmental responsibility.

- In September 2023, Lion Beer & Drinks (a subsidiary of Kirin) opened a new craft beer taproom in Sydney, Australia, focusing on localized flavors and experiential dining to engage directly with craft beer enthusiasts and build brand loyalty.

MARKET SEGMENTATION

This research report on the Asia Pacific Beer market is segmented and sub-segmented into the following categories.

By Type

- Lager

- Ale

- Other Types

By Distribution Channel

- On-trade

- Off-trade

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of APAC

Frequently Asked Questions

What is the Asia Pacific beer market?

The Asia Pacific beer market includes the production, distribution, and consumption of beer products across the region.

Why is the Asia Pacific beer market growing rapidly?

The market is growing due to rising disposable incomes and increasing demand for alcoholic beverages among young consumers.

What types of beer are commonly consumed in Asia Pacific?

Common beer types include lager, ale, stout, wheat beer, and craft beer products.

Which beer segment leads the Asia Pacific market?

Lager beer dominates the market due to its widespread popularity and high consumer preference.

Who are the primary consumers in the Asia Pacific beer market?

Young adults, urban consumers, and social drinkers are the main users of beer products.

How is consumer preference influencing the Asia Pacific beer market?

Consumers are increasingly choosing premium and flavored beer products for unique drinking experiences.

Why is craft beer gaining popularity in Asia Pacific?

Craft beer is gaining demand due to rising interest in premium, locally brewed, and innovative beverage options.

What challenges does the Asia Pacific beer market face?

Strict alcohol regulations and fluctuating raw material prices can affect market growth.

How is technology influencing the Asia Pacific beer market?

Advanced brewing technologies and innovative packaging solutions are improving beer quality and distribution efficiency.

What is the future outlook for the Asia Pacific beer market?

The market is expected to grow steadily with increasing urbanization and rising demand for premium alcoholic beverages.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com