Global Fruit Beer Market Size, Share, Trends & Growth Forecast Report Segmented By Flavour (Peach, Raspberry, Cherries, Blueberry, Plums And Others), Distribution Channel (Departmental Stores, Bars And Restaurants, Supermarkets, Speciality Stores And Online Retailers) , And Region(North America, Europe, APAC, Latin America, Middle East And Africa) - Industry Analysis 2026 To 2034

Global Fruit Beer Market Size

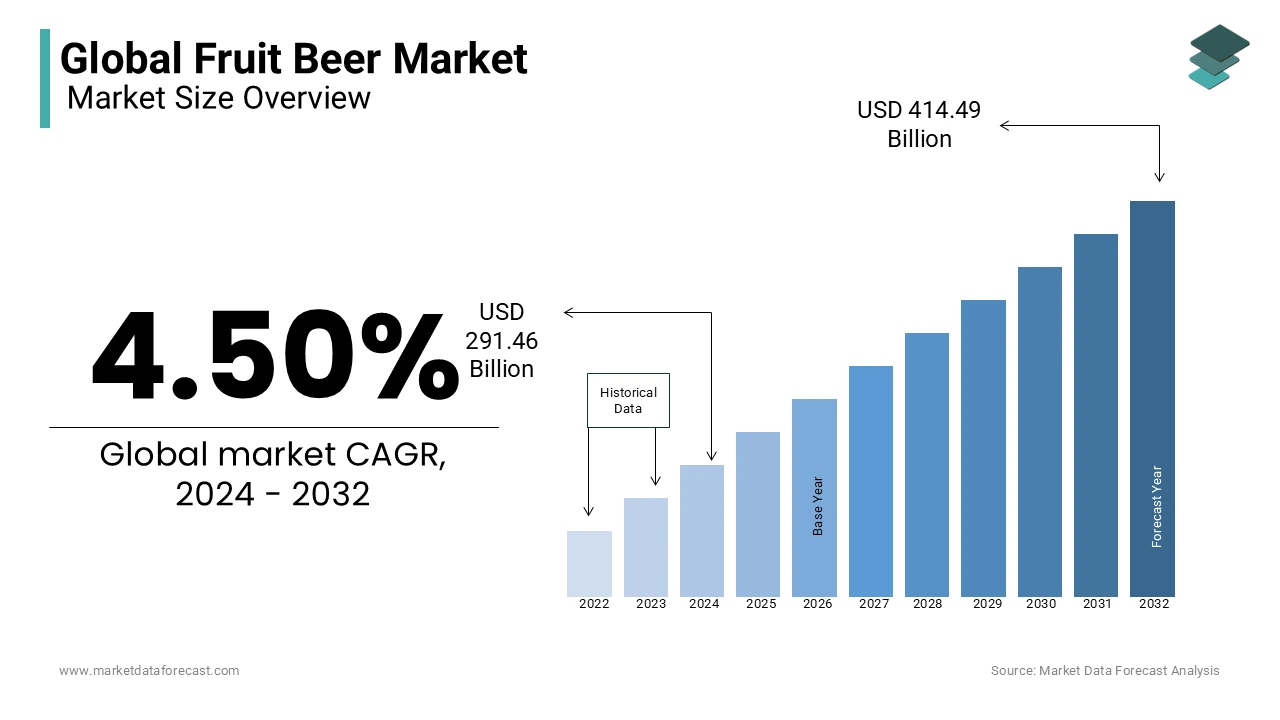

The global fruit beer market size is estimated to be USD 304.58 billion in 2025 and is anticipated to be worth USD 452.64 billion by 2034 from USD 318.29 billion in 2026, growing at a CAGR of 4.50% during the forecast period.

Fruit beer is any traditional or craft beer brewed with real fruit, fruit puree, or juice. This category diverges from traditional malt-forward beers by offering a diverse spectrum of flavor profiles ranging from tart and tangy to sweet and refreshing. The definition includes both craft-brewed varieties and mass-produced offerings that utilize fruits such as raspberry, lemon cherry, and passion fruit to enhance sensory appeal. According to the Brewers Association, the number of operating craft breweries in the United States reached 9,796 in 2024, an all-time high. To navigate a competitive market where volume has declined, many brewers are diversifying their revenue streams by expanding beyond traditional beer production to meet evolving consumer preferences. As per the International Organisation of Vine and Wine (OIV), global wine consumption fell to 214 million hectolitres in 2024, the lowest level since 1961, driven by inflation and generational changes in consumer behavior such as declining purchase frequency and a shift toward health-conscious choices like low-alcohol products. The market is defined by its appeal to consumers seeking novelty and approachability in their drinking experiences. Regulatory bodies in various jurisdictions classify these beverages differently, sometimes categorizing them as flavored malt beverages rather than traditional beer, which impacts taxation and labeling requirements. The rise of health consciousness has also influenced product formulation, with many brands reducing sugar content while maintaining fruit intensity. This sector represents a convergence of brewing tradition and modern flavor innovation, catering to evolving palates across diverse geographic regions.

MARKET DRIVERS

Rising Preference for Low Alcohol and Sessionable Beverages Among Younger Demographics

The shifting consumption patterns among millennials and Generation Z towards moderate alcohol intake are propelling the growth of the Fruit Beer Market. These demographics prioritize sessionability and flavor complexity over high alcohol by volume level,s seeking beverages that allow for social engagement without excessive intoxication. According to data from the National Institute on Alcohol Abuse and Alcoholism, there has been a notable long-term decrease in heavy drinking episodes among young adults in the United States. In tandem, wider market data shows this demographic shift is aligning with a growing consumer preference for low-alcohol and sessionable options. Fruit beers often feature lower alcohol content compared to traditional stouts or IPAs, making them ideal for extended social gatherings. The perception of fruit beers as refreshing and less filling further enhances their appeal during daytime events and outdoor activities. Breweries respond by launching sessionabfruit-infusedsed lagers and wheat beers that align with these lifestyle preferences. The trend towards mindful drinking is not merely a temporary fad but a structural shift in consumer behavior driven by health awareness and wellness trends. This driver is reinforced by the availability of non alcoholic fruit beer variants, which cater to those abstaining from alcohol entirely while still desiring the sensory experience of a crafted beverage. The versatility of fruit flavors allows manufacturers to create unique taste profiles that resonate with adventurous drinkers seeking new experiences without the commitment of high alcohol content.

Expansion of Craft Brewing Culture and Flavor Innovation

The proliferation of craft brewing culture globally has significantly accelerated the expansion of the Fruit Beer Market. This encourages experimentation and diversification of flavor profiles. Craft brewers consistently seek to differentiate their products in a saturated market by incorporating unconventional ingredients, including exotic fruits and local produce. Reports from the Brewers Association highlight that while the overall U.S. craft beer market volume has leveled off and faced maturation pressures, flavored, innovative, and specialty beers continue to represent a vital, high-interest segment of the industry. The creativity inherent in craft brewing allows for the integration of seasonal fruits such as pea, cherry, cot, and berry varieties, which appeal to consumers seeking limited edition and artisanal experiences. European consumer and market observations show that the diversity of beer styles across the continent has expanded dramatically. While fruit beers remain a historic staple in Belgium, they are increasingly gaining traction as an innovative category in traditional brewing markets like Germany. This innovation extends beyond simple flavor addition to include complex brewing techniques such as barrel aging with fruit infusions, which adds depth and sophistication to the final product. Social media platforms play a crucial role in amplifying these innovations, as visually appealing and uniquely flavored beers generate significant online engagement. Consumers are increasingly educated about brewing processes and ingredient sourcing, leading to a higher appreciation for quality fruit beers. This driver is supported by the willingness of craft breweries to collaborate with local farmers, ensuring fresh and sustainable fruit supplies. The continuous introduction of novel combinations keeps the market dynamic and attracts both beer enthusiasts and casual drinkers looking for distinctive taste experiences.

MARKET RESTRAINTS

Regulatory Classification and Taxation Discrepancies

Inconsistent regulatory classifications and varying taxation structures across different jurisdictions are hampering the growth of the fruit beer market. In many countries, beverages containing fruit additives are categorized differently from traditional beers, leading to higher excise taxes and stricter labeling requirements. Regulations from the Alcohol and Tobacco Tax and Trade Bureau stipulate that flavored malt beverages must adhere to strict ingredient and formulation thresholds to be taxed as beer. Deviating from these specific limits triggers reclassification into significantly higher distilled spirit tax brackets, imposing clear financial parameters for producers. This regulatory ambiguity increases compliance costs and complicates market entry for smaller breweries lacking legal resources. The European Commission maintains a single trade market. However, regulatory discrepancies in how individual member states define and tax traditional beer versus fruit-flavored alcoholic beverages create administrative complexity and compliance friction for producers. Manufacturers must navigate a complex web of local laws, which often require reformulation or repackaging to meet specific regional standards. These barriers limit the ability of brands to scale efficiently and maintain consistent pricing strategies across markets. Additionally, some regions impose restrictions on the use of certain natural flavorings or preservatives in alcoholic beverages, further constraining product development. The lack of harmonized standards creates operational inefficiencies and discourages investment in innovation. Small and medium-sized enterprises are disproportionately affected as they struggle to absorb the additional administrative and financial burdens. This restraint stifles market growth by limiting product availability and increasing consumer prices, ultimately reducing competitiveness against other alcoholic beverage categories with clearer regulatory frameworks.

Perception of Artificial Ingredients and Quality Concerns

Consumer skepticism regarding the use of artificial flavors and concentrates in these beers is a major restraint on the fruit beer market expansion. Many mass-produced fruit beers rely on synthetic flavorings to achieve consistent taste profiles, which detracts from the perceived authenticity and quality of the product. Surveys by the International Food Information Council indicate a strong consumer preference for clean-label products, with a significant portion of respondents stating they prefer foods and beverages free from artificial additives or synthetic ingredients. This preference poses a challenge for manufacturers who struggle to balance cost efficiency with the use of real fruit purees or juices, which are more expensive and perishable. General beverage market analysis shows that consumer complaints regarding overly sweet or chemical-tasting flavor formulations lead to negative word-of-mouth, which can rapidly damage a brand's reputation and stifle repeat purchases. The association of fruit beers with sugary sodas or low-quality alcoholic drinks further alienates discerning beer enthusiasts who prioritize traditional brewing values. Educating consumers about the distinction between artificially flavored and naturally infused beers requires significant marketing investment, which many brands find prohibitive. Additionally, the stability of natural fruit flavors during storage and transportation remains a technical challenge, leading to potential inconsistencies in taste. This perception issue limits the premiumization potential of the category and restricts its appeal to health-conscious and quality-driven segments. Manufacturers must first consistently deliver high-quality natural fruit beers at accessible price points. Until then, this restraint will continue to impede broader market acceptance and growth.

MARKET OPPORTUNITIES

Integration of Functional Ingredients and Health Benefits

The incorporation of functional ingredients, such as probiotics, antioxidants, and vitamins, into fruit beers provides a clear path for market differentiation and growth in the global fruit beer market. Consumers are increasingly seeking beverages that offer health benefits beyond mere hydration or intoxication, driving demand for functional alcoholic drinks. Data from the Global Wellness Institute confirms that the global wellness economy is experiencing rapid expansion as consumer prioritization of health increases. Concurrently, independent retail studies indicate that a growing segment of health-conscious consumers demonstrates a higher willingness to pay a premium for targeted physical and mental well-being products. Fruit beers infused with ingredients like ginger, turmeric, or elderberry can leverage the natural health properties of these components to appeal to health-conscious drinkers. Research published in the Journal of Functional Foods demonstrates that the antioxidant properties of fruits like berries and citrus significantly enhance the nutritional and bioactive profile of beverages. In consumer markets, these scientifically backed nutritional profiles are increasingly leveraged to attract fitness-oriented and health-conscious demographics. Breweries can collaborate with nutritionists to develop formulations that align with dietary trends such as keto-friendly or gluten-free options. This opportunity allows brands to position fruit beers as part of a balanced lifestyle rather than an indulgent treat. The use of organic and locally sourced fruits further enhances the appeal to environmentally and health-aware consumers. Marketing campaigns emphasizing transparency and ingredient benefits can build trust and loyalty among target audiences. Additionally, the development of low-sugar and low-calorie fruit beers addresses concerns about weight management and metabolic health. By tapping into the functional beverage trend, manufacturers can expand their customer base and command higher price points. This strategic shift transforms fruit beer from a niche novelty into a viable option for health-focused consumers.

Expansion into Emerging Markets with a Growing Middle Class

Emerging markets in the Asia Pacific, Latin America, and Africa offer significant growth opportunities for the Fruit Beer Market. This is due to rising disposable incomes and changing consumer preferences. As the middle class expands in these regions, there is increased exposure to international beverage trends and a growing appetite for premium and diversified alcoholic options. According to the World Bank, sustained economic growth in emerging nations such as India, Vietnam, and Brazil has significantly expanded their middle-class populations. Parallel consumer research indicates this macroeconomic growth is driving higher disposable income and increased discretionary spending on leisure, entertainment, and hospitality. Fruit beers with their approachable flavors and lower bitterness are well-suited to introduce new consumers to the beer category who may find traditional lagers or ales too intense. Local breweries can leverage indigenous fruits to create unique products that resonate with cultural tastes and preferences. Partnerships with international brands can facilitate knowledge transfer and technology adoption, enhancing product quality and consistency. The rise of modern retail channels and e-commerce platforms improves accessibility and visibility for fruit beer brands. Government initiatives promoting tourism and hospitality also contribute to market expansion by increasing demand for diverse beverage offerings in hotels and restaurants. By tailoring products to local palates and investing in distribution infrastructure, manufacturers can capture significant market share in these high-growth regions. This opportunity enables global players to diversify their revenue streams and reduce dependency on mature markets.

MARKET CHALLENGES

Supply Chain Volatility and Seasonality of Fruit Ingredients

Supply chain volatility and seasonality challenges are slowing down the growth of the fruit beer market. These constraints impact production consistency and cost stability. Fruit harvests are highly dependent on weather conditions, pest outbreaks, and climate change effects, leading to fluctuations in availability and pricing. As per the Food and Agriculture Organization (FAO) of the United Nations, the increasing frequency of extreme weather events, such as intense rainfall patterns, droughts, and severe temperature fluctuations, increasingly exerts severe pressure on global agricultural systems, introducing systemic volatility across regional fresh fruit and high-value horticultural supply chains. This unpredictability forces breweries to secure long-term contracts or invest in preservation technologies such as freezing or pureeing, which add to operational costs. According to the International Society of Horticultural Science, the shelf life of fresh fruits is limited, requiring efficient logistics and cold chain management to maintain quality during transport. Any disruption in the supply chain can result in production delays or compromised product quality, damaging brand reputation. Additionally, the cost of importing exotic fruits for year-round production subjects manufacturers to currency fluctuations and trade tariffs. Small breweries with limited bargaining power are particularly vulnerable to price spikes and supply shortages. This challenge necessitates robust risk management strategies, including diversification of supplier bases and investment in sustainable farming practices. The inability to guarantee consistent flavor profiles due to variations in fruit quality can also alienate consumers who expect uniformity. Addressing these supply chain complexities requires significant capital investment and strategic planning, which may be prohibitive for smaller market participants.

Intense Competition from Ready-to-Drink Cocktails and Hard Seltzers

Intense competition from the rapidly growing segments of ready-to-drink cocktails and hard seltzers is holding back the expansion of the fruit beer market. These alternatives offer consumers similar flavor profiles and convenience. These alternative beverages have gained significant popularity among consumers seeking light, refreshing, and low-calorie alcoholic options. The marketing prowess of major beverage corporations behind these products has amplified their visibility and appeal, particularly among younger demographics. According to market tracking from the Beverage Marketing Corporation (BMC), a permanent consumer shift toward the convenience of single-serve packaging and the health-conscious positioning of hard seltzers and RTD cocktails has significantly transformed the alcohol landscape, posing a direct market-share threat to traditional premium, craft, and flavored beer categories. Consumers often perceive hard seltzers as having fewer calories and carbohydrates compared to fruit beers, which may contain residual sugars from fruit additions. This perception drives switching behavior, especially among health-conscious individuals. Fruit beer manufacturers must invest heavily in branding and innovation to differentiate their products and highlight the craftsmanship and natural ingredients associated with brewing. The saturation of the flavored alcoholic beverage market makes it difficult for new fruit beer launches to gain traction without substantial marketing budgets. Additionally, the rapid pace of trend cycles in the beverage industry requires continuous product innovation to maintain relevance. Failure to adapt to these competitive pressures can result in declining sales and reduced market presence for fruit beer brands.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.50% |

| Segments Covered | By Flavour, Distribution Channel, And Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Joseph James Brewing Company, Inc., New Belgium Brewing Company, Brewery Ommegang, All Saints’ Brewery, Lindemans Brewery, Lost Coast Brewery, Magic Hat Brewing Company, Shipyard Brewing Company, Unibroue, Wells & Young's Ltd., Brouwerij Van Honsebrouck N.V., Abita Brewing Co., and Pyramid Breweries, Inc. |

SEGMENTAL ANALYSIS

By Flavour Insights

The raspberry segment dominated the Fruit Beer Market and accounted for a 29.3% share in 2025. This dominance of the segment was driven by its exceptional versatility in pairing with various beer styles and its widespread consumer appeal across different demographics. The tartness and aromatic profile of raspberries complement both light lagers and robust ales, making it a preferred choice for brewers seeking balanced flavor profiles. As per the United States Department of Agriculture, raspberry production has seen steady growth in key agricultural regions, ensuring a consistent supply of high-quality fruit for beverage manufacturers. The natural acidity of raspberries helps cut through the sweetness of malt, creating a refreshing finish that appeals to modern palates. According to the Brewers Association, fruit beers featuring berry flavors account for a significant portion of specialty beer sales, with raspberry being the most frequently cited ingredient in craft brewing surveys. The visual appeal of raspberry-infused beers, which often exhibit a vibrant red or pink hue, also enhances their marketability on social media platforms, driving organic marketing. Consumers associate raspberries with health benefits due to their high antioxidant content, which aligns with the growing trend of functional beverages. This perception encourages trial among health-conscious drinkers who view raspberry beer as a lighter alternative to sugary cocktails. The availability of raspberry puree and concentrate allows breweries to maintain consistent flavor year-round, overcoming seasonal limitations. Major commercial brands have also adopted raspberry as a flagship flavor, further cementing its dominance through extensive distribution and advertising campaigns. The familiarity of the flavor reduces the barrier to entry for new consumers who may be hesitant to try more exotic fruit combinations.

On the contrary, the peach segment is likely to experience the fastest CAGR of 9.2% over the forecast period, owing to its strong association with summer consumption and its naturally sweet profile that masks the bitterness of hops. The juicy and aromatic characteristics of peach resonate well with consumers seeking approachable and refreshing alcoholic beverages, particularly during warm weather seasons. Data compiled by the Food and Agriculture Organization (FAO) demonstrates a steady upward trajectory in global peach production volume, expanding the baseline raw material pipeline for food and beverage processors looking to leverage stone-fruit flavors. The versatility of peach allows it to be paired with wheat beers, IPAs, and sours, creating a diverse range of products that cater to varying taste preferences. The rise of hazy IPAs and New England-style ales, which emphasize fruity and juicy notes, has further accelerated the adoption of peach as a key ingredient. Breweries are leveraging local peach harvests to create limited-edition seasonal releases that generate buzz and urgency among consumers. Marketing campaigns often highlight the natural and wholesome aspects of the peach, appealing to those seeking clean-label products. The integration of peach into hard seltzers and malt beverages has also cross-pollinated demand for peach-flavored beers. This segment benefits from the nostalgia and comfort associated with peach flavors, making it a safe yet exciting choice for experimental drinkers. The ability of the peach to blend seamlessly with other fruits, such as mango or lemon, also fosters innovation and product differentiation.

By Distribution Channel Insights

The supermarkets segment led the Fruit Beer Market and captured a 46.5% share in 2025. Their widespread accessibility, competitive pricing, and ability to offer a broad selection of brands under one roof are the main factors behind the leading position of this segment. These retail outlets serve as the primary point of purchase for mainstream consumers who prioritize convenience and value when buying alcoholic beverages. Research confirms that supermarkets and large-scale grocery stores command the largest share of off-premise alcohol volume sales in the United States, providing fruit beer manufacturers with a mission-critical, high-volume sales channel. The prominent shelf placement and promotional activities such as discounts and bundle offers in supermarkets drive impulse purchases and encourage trial among shoppers. The ability of supermarkets to stock both domestic and imported varieties caters to diverse consumer preferences and expands market reach. Private-label fruit beers offered by major supermarket chains also contribute to segment dominance by providing affordable alternatives to premium brands. The integration of loyalty programs and digital coupons further enhances customer retention and drives repeat purchases. Supermarkets also benefit from extended operating hours and multiple locations, making them the most convenient option for regular household stocking. The trust associated with established retail giants ensures product quality and safety, which is crucial for food and beverage items. This channel remains resilient despite the growth of e-commerce due to the immediate gratification of physical shopping.

However, the online retailers segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 11.5% from 2026 to 2034, fueled by the increasing adoption of e-commerce platforms and the demand for niche and craft products. The convenience of home delivery and the ability to access a wider variety of brands than available in local stores drive this rapid expansion. As per Statista, online alcohol sales have surged globally, with younger demographics, particularly millennials and Generation Z, preferring digital channels for purchasing beverages. The ability of online platforms to provide detailed product descriptions, reviews, and ratings helps consumers make informed decisions about unfamiliar fruit beer brands. According to the Beverage Information Group, the direct-to-consumer model allows craft breweries to bypass traditional distribution barriers and reach customers in remote or underserved areas. Subscription services offering curated selections of fruit beers have gained popularity, providing a recurring revenue stream for retailers and enhancing customer loyalty. The use of data analytics enables online retailers to personalize recommendations and target specific consumer segments with relevant promotions. Social media integration and influencer marketing further drive traffic to online stores, creating a seamless shopping experience. The pandemic accelerated the shift towards online shopping, establishing habits that persist post-lockdown. Regulatory changes in various regions allowing for the legal shipment of alcohol have also facilitated this growth. Online retailers offer competitive pricing and exclusive deals that attract price-sensitive consumers. The ease of comparing prices and reading feedback empowers buyers and enhances satisfaction.

REGIONAL ANALYSIS

North America Fruit Beer Market Analysis

North America was the top performer in the global Fruit Beer Market and occupied a 35.2% share in 2025. This position of the regional market was driven by a mature craft brewing industry and a consumer base that actively seeks novel and diverse flavor experiences. The region is characterized by a high density of microbreweries and craft breweries that continuously innovate with fruit infusions to differentiate their offerings. According to the Brewers Association, the United States is home to thousands of active craft breweries. In parallel, retail tracking shows that a substantial number of these establishments frequently produce fruit-flavored beers to capture seasonal consumer interest and cater to localized flavor preferences. The cultural acceptance of beer as a versatile beverage suitable for various occasions supports robust demand. The presence of major beverage conglomerates investing in craft brands further amplifies market visibility and distribution reach. Regulatory frameworks in states like California and Colorado support local brewing initiatives, fostering a competitive and dynamic market environment. The influence of social media and food tourism drives consumers to seek out unique and Instagram-worthy beer experiences. The availability of fresh local fruits in regions like the Pacific Northwest and Florida provides brewers with high-quality ingredients for authentic flavors. The trend towards health consciousness has also spurred the development of low-calorie and organic fruit beers. The strong e-commerce infrastructure facilitates direct-to-consumer sales, enhancing market penetration. North America remains a trendsetter in the global fruit beer landscape, influencing product development and marketing strategies worldwide.

Europe Fruit Beer Market Analysis

Europe followed closely behind in the Fruit Beer Market and captured a significant share in 2025. This growth of the European market was supported by traditional brewing cultures in countries like Belgium and Germany that have long embraced fruit-infused beers. The region benefits from a deep-seated appreciation for beer diversity and quality, which supports the continued popularity of classic fruit beer styles such as Lambic and Kriek. A study confirms that Europe accounts for a substantial portion of global beer consumption. Concurrently, regional market tracking indicates that fruit beers maintain a highly steady and loyal customer base, anchored deeply in traditional brewing heritage. The strict adherence to brewing standards and quality regulations ensures high product integrity, which builds consumer trust. The integration of modern brewing techniques with traditional recipes allows breweries to appeal to both older traditionalists and younger adventurous drinkers. The prevalence of beer festivals and cultural events provides platforms for breweries to showcase new fruit beer varieties and engage directly with consumers. Sustainability initiatives and the use of organic ingredients are increasingly important to European consumers, influencing purchasing decisions. The regional trade agreements facilitate the cross-border movement of beer products, expanding market access for smaller breweries. The rise of craft beer bars and specialized retail outlets enhances the visibility and availability of niche fruit beers. Europe's commitment to brewing heritage, combined with innovation, ensures its continued prominence in the global market.

Asia Pacific Fruit Beer Market Analysis

The Asia Pacific region is the fastest-growing region in the fruit beer market due to rapid urbanization, rising disposable incomes, and the expanding middle class in countries such as China, Japan, and Australia. The region is witnessing a shift from traditional spirits and baijiu to western-style alcoholic beverages, including beer with fruit flavors appealing to younger consumers. Reports from the World Bank show that sustained economic growth in the Asia-Pacific region has significantly raised disposable incomes. Commercial market research indicates that this financial growth is boosting discretionary spending on leisure and entertainment, subsequently driving demand for premium and flavored beers. The introduction of international craft beer brands and the establishment of local breweries have diversified the market offerings. The influence of Western culture and travel has exposed consumers to diverse beer styles, fostering curiosity and experimentation. Local fruits such as lychee, mango, and yuzu are being incorporated into beers, creating unique regional variants that resonate with local palates. The growth of e-commerce and food delivery platforms enhances accessibility and convenience for consumers. Government initiatives promoting tourism and hospitality also contribute to market growth by increasing demand in bars and restaurants. The young demographic profile of the region ensures a large potential customer base for future growth. Marketing efforts focusing on lifestyle and social engagement are effective in driving brand awareness and adoption.

Latin America Fruit Beer Market Analysis

Latin America is moving ahead steadfastly in the fruit beer market owing to cultural preferences for sweet and fruity flavors and evolving economic dynamics. Countries like Brazil, Mexico, and Argentina have strong traditions of consuming fruit-based beverages, which translates well to the acceptance of fruit-infused beers. Data from the Inter-American Development Bank highlights an expanding middle-class population across Latin America due to shifting regional economic dynamics. Parallel retail studies indicate this growing demographic is increasingly driving market demand for premium and differentiated alcoholic beverages. The hot climate in many parts of the region makes refreshing and light fruit beers particularly appealing for casual consumption. The availability of tropical fruits such as passion fruit, guava, and pineapple provides local brewers with abundant and cost-effective ingredients for innovative formulations. The rise of craft beer festivals and specialized bars in cities like São Paulo and Mexico City is educating consumers and expanding the market. Economic volatility can impact purchasing power, but the affordability of local craft beers helps maintain demand. The influence of international trends and tourism introduces new flavors and styles to the market. Regulatory environments vary by country, affecting distribution and taxation, but overall trends are positive for growth. The emphasis on social drinking and community events supports the cultural integration of fruit beers. Local breweries are increasingly focusing on quality and branding to compete with imports.

Middle East And Africa Fruit Beer Market Analysis

The Middle East and Africa region is likely to expand notably in the Fruit Beer Market over the forecast period due to regulatory constraints in certain countries and emerging demand in others. In non alcoholic beer friendly markets such as South Africa and some Gulf Cooperation Council countries, fruit flavored non alcoholic beers are gaining popularity as socially acceptable alternatives. Global status reports from the World Health Organization show that alcohol consumption patterns vary drastically across the Middle East and Africa. This variance aligns with diverse regional frameworks, ranging from strict, faith-based total prohibitions in certain nations to regulated legal markets in others. In South Africa, the craft beer scene is expanding with fruit beers appealing to a diverse and multicultural population. Fruit flavors help mask the taste differences in non alcoholic beers, making them more palatable to consumers. The tourism sector in countries like Dubai and Cape Town drives demand for international and local beer varieties in hotels and restaurants. The availability of imported fruit beers in specialized stores caters to expatriate and tourist populations. Local breweries are exploring fruit infusions to create unique products that align with regional tastes. Economic development and urbanization are slowly changing consumption habits in select markets. The challenge lies in navigating complex regulatory landscapes and cultural sensitivities. However, the potential for growth in non alcoholic fruit beers remains significant as health and wellness trends gain traction.

COMPETITION OVERVIEW

The competitive landscape of the Fruit Beer Market is characterized by intense rivalry between multinational beverage conglomerates and independent craft breweries. Large corporations leverage their extensive distribution networks and marketing budgets to dominate mainstream channels, while craft brewers differentiate themselves through innovation and authenticity. Competition is driven by the continuous introduction of novel fruit flavors and seasonal variations that capture consumer interest. Brand loyalty is increasingly influenced by sustainability practices and ethical sourcing initiatives, which resonate with modern consumers. Price competition remains significant in the mass market segment, whereas premium brands focus on quality and exclusivity. The rise of hard seltzers and ready-to-drink cocktails poses a substantial threat requiring fruit beer producers to adapt their offerings. Regulatory differences across regions impact market entry and expansion strategies for global players. Digital presence and e-commerce capabilities are becoming critical factors in reaching direct-to-consumer segments. Collaborations with local artists and influencers help brands build cultural relevance and community engagement. The market is dynamic with frequent product launches and shifting consumer preferences, demanding agility and responsiveness from all participants. Success depends on balancing tradition with innovation to meet diverse global demands.

KEY MARKET PLAYERS

A few major players of the global fruit beer market include

- Joseph James Brewing Company, Inc

- New Belgium Brewing Company

- Brewery Ommegang

- All Saints’ Brewery

- Lindemans Brewery

- Lost Coast Brewery

- Magic Hat Brewing Company

- Shipyard Brewing Company

- Unibroue

- Wells & Young's Ltd

- Brouwerij Van Honsebrouck N.V

- Abita Brewing Co

- Pyramid Breweries, Inc

Top Strategies Used by Key Market Participants

Key players in the Fruit Beer Market primarily employ product innovation and strategic branding to maintain a competitive advantage. Companies invest heavily in research and development to create unique fruit flavor combinations that appeal to evolving consumer tastes. Limited edition seasonal releases are frequently used to generate buzz and encourage trial among adventurous drinkers. Partnerships with local fruit suppliers ensure high-quality ingredients and support sustainability initiatives. Digital marketing campaigns targeting younger demographics through social media platforms enhance brand visibility and engagement. Expansion into emerging markets with growing middle classes provides new revenue opportunities. Mergers and acquisitions allow larger corporations to integrate craft breweries and diversify their portfolios. Pricing strategies focus on premiumization to position fruit beers as high-value lifestyle products. Educational initiatives inform consumers about brewing processes and ingredient benefits, building trust and loyalty. These combined approaches enable manufacturers to navigate market dynamics and sustain long-term growth in the global beverage industry.

Leading Players in the Fruit Beer Market

- Anheuser Busch InBev leverages its vast global distribution network to dominate the fruit beer segment through brands like Shock Top and Hoegaarden. The company focuses on mass market appeal by producing consistent and accessible fruit-infused wheat beers. Recent actions include expanding production capacities in key markets to meet rising demand for flavored beverages. Anheuser-Busch InBev invests heavily in marketing campaigns that highlight the refreshing nature of their fruit beers, targeting younger demographics. The firm actively collaborates with local suppliers to source high-quality fruits, ensuring authentic flavors. Their strategic acquisitions of craft breweries allow them to integrate innovative fruit beer recipes into their portfolio. This approach strengthens their position by combining scale with creativity. The company also emphasizes sustainability in sourcing, which resonates with environmentally conscious consumers. By utilizing advanced brewing technologies, they maintain product quality across diverse regions. These efforts ensure sustained relevance and growth in the competitive global beverage landscape.

- Heineken N.V. contributes significantly to the global fruit beer market through its premium brand portfolio, including Desperados and local fruit-infused variants. The company emphasizes innovation by introducing unique flavor combinations that appeal to adventurous drinkers. Recent strategies involve launching limited-edition fruit beers in European and Asian markets to test consumer preferences. Heineken invests in digital marketing platforms to engage directly with consumers and build brand loyalty. The firm partners with music festivals and lifestyle events to promote its fruit beer offerings as social beverages. Their focus on premiumization ensures higher profit margins and brand prestige. Heineken also prioritizes sustainable brewing practices, reducing water usage and carbon emissions. This commitment enhances their corporate image and attracts ethical consumers. By leveraging data analytics, they optimize supply chain efficiency and product availability. These initiatives reinforce Heineken's leadership in the global alcoholic beverage sector.

- Boston Beer Company is a key player in the fruit beer market, known for its Samuel Adams and Angry Orchard brands. The company pioneers craft brewing techniques to create complex and flavorful fruit beers. Recent actions include expanding the Angry Orchard cider line with new fruit infusions such as pear and berry blends. Boston Beer Company focuses on education and transparency, informing consumers about ingredient sourcing and brewing processes. The firm collaborates with local orchards to secure fresh and high-quality fruits for production. Their emphasis on seasonal releases creates urgency and drives repeat purchases. Boston Beer Company also invests in research and development to innovate with new fruit varieties. This commitment to quality and creativity distinguishes them from mass market competitors. By maintaining strong relationships with distributors, they ensure wide product availability. These strategies solidify their reputation as a leader in the craft beverage industry.

DETAILED SEGMENTATION OF THE GLOBAL FRUIT BEER MARKET IS INCLUDED IN THIS REPORT

This research report on the global fruit beer market has been segmented and sub-segmented based on flavor, distribution channel, & region.

By Flavor

- Peach

- Raspberry

- Cherries

- Blueberry

- Plums

- Other flavors

By Distribution Channel

- Departmental Stores

- Bars and Restaurants

- Supermarkets

- Specialty Stores

- Online Retailers

By Region

- North America

- Europe

- Asia Pacifica

- Latin America

- Middle East and Africa

Frequently Asked Questions

2. What are the major types of fruit beers available in the market?

Fruit beers are available in several flavors including raspberry, strawberry, peach, blueberry, cherry, mango, and grapefruit, offering diverse taste experiences for consumers.

3. Which distribution channels dominate the fruit beer market?

Supermarkets, hypermarkets, specialty stores, bars, restaurants, and online retail platforms are the major distribution channels through which fruit beer products are marketed and sold.

4. How is the craft beer trend influencing the fruit beer market?

The increasing number of microbreweries and the growing popularity of craft beer products are significantly boosting demand for fruit beer worldwide.

5. Which region holds the largest share of the fruit beer market?

Europe holds a dominant share of the global fruit beer market due to a strong tradition of flavored beer consumption and a well-established brewing industry.

7. What role does innovation play in the fruit beer market?

Manufacturers are introducing new fruit combinations and experimenting with unique brewing techniques to create innovative flavors and enhance product differentiation.

8. What challenges does the fruit beer market face?

The market faces challenges such as high production costs, regulatory constraints on alcoholic beverages, and competition from traditional beers and other flavored alcoholic drinks.

9. What are the key applications of fruit beer?

Fruit beer is widely consumed in social gatherings, restaurants, pubs, and recreational settings due to its refreshing flavor and moderate alcohol content.

10. What is the future outlook of the fruit beer market?

The fruit beer market is expected to witness steady growth due to increasing consumer demand for flavored alcoholic beverages, rising innovation in craft brewing, and expanding distribution channels worldwide.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com