Global Cider Market Size, Share, Trends & Growth Forecast Report - Segmented By Type (Still Cider, Sparkling Cider, Draft Cider, Apple Wine), Distribution Channels (Hypermarkets, Supermarkets, Departmental Stores, Convenience Stores, Online Stores), and Region (North America, Europe, Asia Pacific, Latin America, Middle East and Africa, and Rest of the World) - Industry Analysis 2026 to 2034

Global Cider Market Report Summary

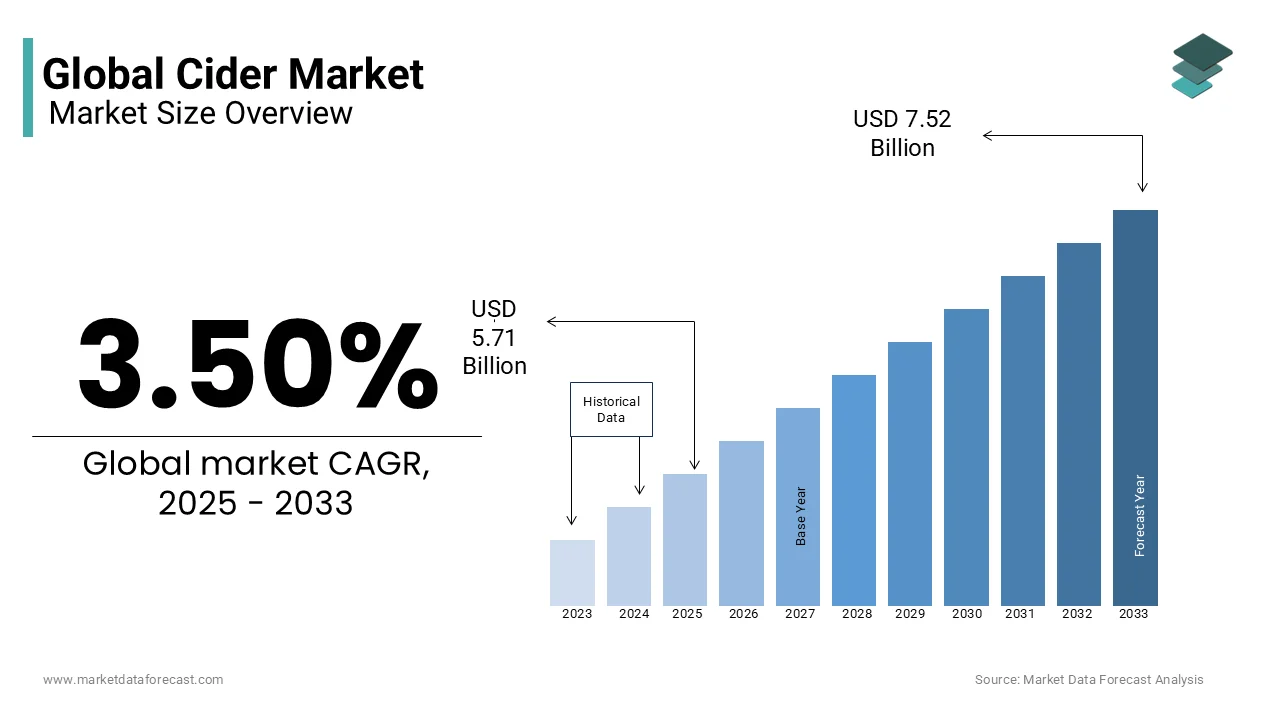

The global cider market size was valued at USD 5.74 billion in 2025, is projected to reach USD 5.94 billion in 2026, and is expected to grow to USD 7.82 billion by 2034, registering a CAGR of 3.50% during the forecast period. Market growth is driven by the rising popularity of fruit-based alcoholic beverages, increased consumer preference for low-ABV drinks, and growing demand for flavored and premium ciders. Expansion of modern retail formats, strong consumption in Europe, and continued product innovation further contribute to market development.

Key Market Trends

- Increasing consumer preference for low-alcohol, refreshing, and fruit-forward beverages.

- Strong shift toward sparkling and flavored cider varieties.

- Rising global penetration of cider through supermarkets and modern retail chains.

- Expansion of artisanal and craft cider brands appealing to premium consumers.

- Growing interest in natural, organic, and locally sourced cider products.

- Innovation in apple blends, fruit infusions, and packaging formats enhancing consumer appeal.

Segmental Insights

- Based on type, the sparkling cider segment held the largest share of the global cider market in 2025, accounting for 68% of total cider volume sales due to its widespread popularity, refreshing taste, and strong presence across retail and on-trade channels.

- Based on distribution channel, the supermarkets segment represented the largest distribution channel in 2025, capturing 44.5% of total global retail cider sales owing to wide product visibility, convenient access, and extensive brand assortment.

Regional Insights

- Europe remained the most mature and dominant cider-producing and cider-consuming region, holding 52.6% of the global cider market share in 2025. The region’s strong cider heritage, well-established brands, and growing preference for flavored and craft variants support ongoing market leadership.

Competitive Landscape

The global cider market is competitive, with major beverage companies and regional producers focusing on flavor innovation, product diversification, and stronger retail penetration. Leading players in the global cider market include Asahi Premium Beverages, Aston Manor, C&C Group plc, Carlsberg Breweries A/S, Carlton & United Breweries (CUB), Heineken UK Limited, The Boston Beer Company, Anheuser-Busch Companies LLC, and Distell Group

Global Cider Market Size

The global cider market size was valued at USD 5.74 billion in 2025. The market size is expected to reach USD 7.82 billion by 2034 from USD 5.94 billion in 2026. The market's promising CAGR for the predicted period is 3.50%.

Cider refers to fermented beverages derived predominantly from apples, including both traditional and modern interpretations such as hard cider, flavored variants, and low-alcohol or non-alcoholic versions. While rooted in historical European brewing practices, cider has evolved into a globally recognized alcoholic beverage category, particularly gaining traction in North America and parts of Western Europe. Additionally, as per data published by the British Apple and Pear Association, approximately 20% of the UK’s apple crop is dedicated exclusively to cider production annually, underscoring the agricultural integration of this sector. The beverage’s identity straddles rural heritage and contemporary craft trends, with increasing consumer interest in natural ingredients and region-specific terroir influencing its modern positioning.

MARKET DRIVERS

The growing consumer preference for natural and minimally processed alcoholic beverages is one pivotal driver of the cider market. Modern drinkers, particularly millennials and Gen Z, exhibit a marked inclination toward drinks with transparent ingredient lists, free from artificial additives. Cider, traditionally made from fermented apple juice, aligns with this clean-label movement. Furthermore, a portion of craft cider consumers in North America cited “fewer additives” as a primary reason for choosing cider over beer or spirits. This shift is reinforced by the rising popularity of heritage apple varieties and spontaneous fermentation techniques, which enhance perceived authenticity. The alignment of cider with broader wellness-oriented consumption patterns, without compromising on flavor or alcohol content, has solidified its appeal among health-conscious yet socially active demographics.

The expansion of craft beverage culture and experiential consumption trends is another significant demand driver. Consumers are increasingly seeking unique tasting experiences, brewery tours, and limited-edition releases, which cider producers are adept at delivering through small-batch production and regional storytelling. According to the American Cider Association, the number of licensed cideries in the United States grew from just 150 in 2010 to over 1,000 by 2023, indicating a robust artisanal movement. This proliferation enables hyper-local engagement, with many cideries integrating orchards, tasting rooms, and agritourism activities. The experiential aspect, ranging from apple harvest festivals to barrel-aging tastings, fosters brand loyalty and word-of-mouth marketing, differentiating cider from mass-produced alcoholic alternatives and fueling sustained demand.

MARKET RESTRAINTS

The volatility of apple supply due to climate change and agricultural challenges is a major restraint impacting the cider market. Apple cultivation for cider requires specific varietals, such as Dabinett, Yarlington Mill, or Kingston Black, that are less resilient and require specific growing conditions than dessert apples. The UK experienced a decline in cider apple yields in 2021 due to unseasonal frost and prolonged drought, marking one of the worst harvests in two decades. Similarly, in France, where traditional cidre is produced in Normandy and Brittany, Météo-France reported that erratic blooming cycles caused by rising spring temperatures reduced apple availability. These disruptions not only increase production costs but also limit the consistency of flavor profiles, undermining brand reliability. Moreover, as cider-specific orchards take 5–7 years to mature, replanting in response to climate stress is a long-term and capital-intensive endeavor, constraining scalability.

The lack of standardized regulatory definitions and labeling clarity across key markets, which creates consumer confusion and hampers international trade, is another critical restraint. In the United States, the Alcohol and Tobacco Tax and Trade Bureau (TTB) permits the use of concentrate, added sugar, and even non-apple fermentables in products labeled as “cider,”. This ambiguity dilutes brand equity and discourages premiumization.

MARKET OPPORTUNITIES

The development of non-alcoholic and functional ciders targeting health-conscious demographics is one emerging opportunity. With global demand for alcohol-free beverages expanding rapidly, cider producers are leveraging fermentation expertise to create complex, alcohol-removed variants. Brands like Sheppy’s and Brothers Cider in the UK have launched alcohol-free lines that retain tannic depth and fruit character, appealing to drivers, fitness enthusiasts, and non-drinkers. Also, a significant number of British adults reduced alcohol intake for wellness reasons, creating a receptive market. Moreover, early experimentation with probiotic-infused ciders and vitamin-enriched formulations is underway. This convergence of functional health and sensory pleasure positions non-alcoholic cider as a high-growth niche.

The integration of sustainable production practices and carbon-neutral branding, which resonates with environmentally aware consumers, is another strategic opportunity. Cider’s inherent connection to orchards offers a natural platform for carbon sequestration, biodiversity enhancement, and regenerative agriculture. As per the Soil Association, a single hectare of traditional cider orchard can support over 300 species of flora and fauna, including endangered pollinators. Leading producers have committed to net-zero operations, investing in solar-powered pressing facilities and biogas generation from pomace waste. Such initiatives not only lower operational costs but also strengthen consumer trust, particularly among eco-literate buyers who prioritize environmental accountability in their purchasing decisions.

MARKET CHALLENGES

The intensifying competition from alternative fermented beverages, particularly craft beer, kombucha, and ready-to-drink (RTD) cocktails, is a principal challenge facing the cider market. Unlike cider, many of these products are not constrained by seasonal apple harvests and can be produced year-round at scale. Furthermore, their alignment with low-calorie, portable consumption models appeals to younger demographics, forcing cider brands to reposition or risk marginalization in an increasingly crowded and fast-evolving beverage landscape.

The limited consumer awareness and education regarding cider’s diversity and quality tiers, which impedes premiumization and export potential is another pressing challenge. Unlike wine or whisky, cider lacks a widely recognized classification system, leading many consumers to perceive it as a homogeneous, sweet, mass-market drink. This misperception limits pricing power and discourages sommelier adoption in fine dining. Without broader cultural validation and sensory education, the market struggles to elevate beyond commodity status.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.50% |

| Segments Covered | By Type, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Asahi Premium Beverages, Aston Manor, C&C Group plc, Carlsberg Breweries A/S, Carlton & United Breweries (CUB), Heineken UK Limited, The Boston Beer Company, Anheuser-Busch Companies LLC, and Distell Group. |

SEGMENTAL ANALYSIS

By Type Insights

The sparkling cider segment holds the largest share of the global market of 68% of total cider volume sales in 2025. Its dominance is because of primarily from strong consumer alignment with celebratory and social drinking occasions, where effervescence is culturally associated with festivity and refreshment. The effervescent texture and crisp finish of sparkling cider make it a preferred substitute for champagne and prosecco in casual settings. Furthermore, major producers such as Kopparberg and Strongbow have heavily invested in premium sparkling variants with sleek packaging, amplifying shelf appeal. The rapid expansion of sparkling cider is also fueled by product innovation and flavor diversification, particularly in mature markets like North America and Western Europe. Flavored sparkling ciders, especially those infused with berries, citrus, and tropical fruits, have gained widespread traction among younger consumers seeking novelty and sensory variety. The adaptability of carbonation to both high-strength and low-alcohol formulations further broadens its demographic reach, enabling penetration into wellness-oriented and moderate-drinking segments, thus reinforcing its market leadership.

The still cider segment is emerging as the fastest-growing within the cider market and is projected to expand at a CAGR of 9.3% from 2026 to 2034. This surge is driven by a rising appreciation for artisanal, terroir-driven beverages that mirror the complexity of wine. Still ciders, which lack carbonation, offer a fuller mouthfeel and enhanced tannic structure, appealing to connoisseurs and sommeliers seeking nuanced flavor profiles. Unlike sparkling variants, still ciders are often aged in oak barrels and produced in small batches, reinforcing their premium image and justifying higher price points. A further key factor propelling the growth of still cider is its alignment with the slow beverage movement and food pairing culture. Consumers increasingly view still cider as a sophisticated alternative to white wine, particularly when paired with cheese, charcuterie, or regional cuisine. A notable share of wine-educated consumers preferred dry still cider over sparkling cider in formal dining contexts due to its lower pressure and greater aromatic complexity. Moreover, traditional producers in regions like Asturias (Spain) and Normandy (France) have successfully exported still cidre and sidra as cultural heritage products, supported by EU Protected Geographical Indication (PGI) status.

By Distribution Channel Insights

The supermarkets segment represented the largest distribution channel for cider by capturing an estimated 44.5% of total retail cider sales globally in 2025. Their dominance is due to widespread accessibility, consistent product availability, and strategic placement in the alcoholic beverage aisles, often adjacent to beer and wine. In countries like the UK and Germany, where off-premise alcohol consumption exceeds on-trade sales, supermarkets serve as the primary procurement point for household cider purchases. The integration of promotional pricing, multi-pack discounts, and seasonal displays further amplifies consumer uptake, particularly during summer and holiday periods. A different critical factor reinforcing supermarket dominance is the consolidation of private-label cider offerings by major grocery chains. Retailers such as Tesco, Sainsbury’s, and Aldi have introduced their own branded ciders, leveraging economies of scale to offer competitive pricing while maintaining quality. The in-house brands often source from established producers under contract, ensuring consistency and reducing marketing costs. Additionally, supermarkets benefit from cold chain infrastructure and dedicated chilled sections, essential for preserving cider’s flavor integrity.

Conversely, the online stores segment is the fastest-growing distribution channel in the cider market and is registering a CAGR of 13.7% between 2051 and 2026. This acceleration is largely attributed to the increasing consumer preference for convenience, doorstep delivery, and access to niche or regional cider varieties unavailable in physical stores. During the post-pandemic period, e-commerce platforms such as Master of Malt, Cider Union, and Barnivore saw a rise in transaction volume for craft and heritage ciders. The ability to offer detailed product descriptions, tasting notes, and producer stories enhances consumer engagement, particularly among digitally native buyers. A further driver of online growth is the rise of direct-to-consumer (DTC) models adopted by independent cideries. Many small-scale producers, lacking the resources for national retail distribution, now utilize e-commerce platforms to reach global audiences. This shift enables producers to retain higher margins and cultivate brand loyalty through subscription services and limited releases. Moreover, platforms like Shopify and WooCommerce have simplified online storefront creation, allowing even rural orchard-based producers to participate in the digital economy.

REGIONAL ANALYSIS

Europe Market Analysis

Europe stood as the most mature and dominant cider-producing and consuming region by holding a 52.6% share of the global cider market in 2025. Anchored by deep-rooted traditions in countries like the UK, France, and Spain, Europe’s cider culture is both regionally diverse and institutionally preserved. The sector benefits from protected designations which safeguard production methods and enhance export credibility. Additionally, the European Union’s Common Agricultural Policy provides subsidies for orchard maintenance, ensuring a stable supply of cider-specific apple varieties. The region’s position is further sustained by strong integration of cider into gastronomy and rural tourism. These cultural ecosystems elevate cider beyond a beverage into a heritage experience, fostering both domestic consumption and international interest. Moreover, European producers lead in sustainability innovation, with organic cider production increasing across the EU between 2020 and 2023. This blend of tradition, regulation, and experiential engagement solidifies Europe’s preeminence in the global cider landscape.

North America Market Analysis

North America is key major player in the global cider market. The United States drives the majority of demand, with retail cider sales surging. While historically overshadowed by beer, cider has carved a distinct niche through craft innovation and demographic targeting. The proliferation of micro-cideries has fostered regional diversity, from New England’s heirloom apple ciders to Pacific Northwest fruit-infused variants. This artisanal expansion parallels the earlier craft beer revolution, enabling differentiation in a saturated alcohol market. A key growth catalyst in North America is the strategic alignment of cider with health and lifestyle trends. Many brands emphasize gluten-free, vegan, and low-sugar formulations, appealing to wellness-focused consumers. Furthermore, as per the Alcohol Marketing Review, cider’s average calorie count (180 per 12 oz) is lower than many craft beers, enhancing its appeal. The rise of hard seltzer initially disrupted cider sales, but producers have responded with lighter, sparkling variants that compete directly in the same category. This adaptive innovation ensures cider remains relevant in a dynamic and health-conscious marketplace.

Asia Pacific Market Analysis

Asia Pacific holds a modest but rapidly expanding position in the global cider market. While traditional cider consumption remains limited, urban centers in Japan, South Korea, and Australia are emerging as key adoption hubs. This growth is concentrated among younger, cosmopolitan drinkers seeking novel, low-abv alternatives to beer. The region’s expansion is fueled by increasing exposure to Western drinking cultures and premiumization of social consumption. In cities like Tokyo and Seoul, cider is increasingly featured in craft bars and rooftop lounges, often marketed as a sophisticated, imported beverage. Additionally, local producers in New Zealand and Tasmania are cultivating cider-specific orchards, reducing reliance on imports. With rising disposable incomes and evolving palates, the Asia Pacific region is poised for sustained cider market development.

Asia Pacific Market Analysis

Latin America occupies a significant share of the global cider market, with Brazil and Mexico leading regional demand. Though cider remains a niche category compared to beer and spirits, its presence is growing in urban and expatriate communities. This growth is largely driven by the introduction of international brands into major supermarket chains. Domestic production is still limited, but micro-cideries are emerging in southern Brazil’s apple-growing regions, such as Fraiburgo in Santa Catarina. A critical factor shaping Latin America’s cider trajectory is the rising influence of craft beverage culture and import liberalization. Additionally, craft beer festivals in Mexico City and São Paulo have begun featuring cider tastings, exposing new audiences to the category. While cultural familiarity remains low, the region’s youthful population and increasing openness to global trends suggest latent potential for future market expansion.

Middle East and Africa Market Analysis

Middle East and Africa collectively account for small share of the global cider market. Consumption is highly concentrated in non-Muslim populations and expatriate communities, particularly in the Gulf Cooperation Council (GCC) countries and South Africa. In the UAE, duty-free imports and cosmopolitan dining scenes have enabled premium cider brands to establish a foothold. The primary constraint in this region is religious and regulatory restrictions on alcohol, which limit mass-market penetration. However, the rise of non-alcoholic cider presents a viable growth avenue. These products mimic the taste and fizz of traditional cider without violating cultural norms. In South Africa, where alcohol regulations are more permissive, cider is gaining traction among younger demographics seeking premium alternatives to beer. While the overall market remains small, innovation in alcohol-free formats could unlock broader acceptance across the region.

COMPETITIVE LANDSCAPE

The cider market exhibits a dynamic and increasingly fragmented competitive landscape, characterized by the coexistence of multinational beverage conglomerates and a growing number of independent craft producers. Global players leverage scale, distribution networks, and marketing budgets to maintain visibility, while regional and artisanal brands differentiate through authenticity, heritage, and innovation in flavor and fermentation techniques. Competition is intensifying as cider overlaps with the RTD, craft beer, and wine sectors, prompting brands to sharpen positioning. Price, packaging, sustainability claims, and experiential engagement—such as orchard tours and limited releases—serve as key differentiators. In Asia Pacific and Latin America, market entry strategies focus on premium import branding and localization, whereas in Europe and North America, competition centers on shelf space, innovation speed, and consumer loyalty.

KEY MARKET PLAYERS

Some of the leading players in the global cider market are

-

Asahi Premium Beverages

-

Aston Manor

-

C&C Group plc

-

Carlsberg Breweries A/S

-

Carlton & United Breweries (CUB)

-

Heineken UK Limited

-

The Boston Beer Company

-

Anheuser-Busch Companies LLC

-

Distell Group

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Key players in the cider market are deploying a combination of product innovation, geographic expansion, sustainability integration, digital transformation, and strategic partnerships to consolidate their positions. Companies are reformulating offerings to include low-alcohol, non-alcoholic, and functional variants to align with health-conscious consumer trends. Premiumization through heritage branding and limited editions is being leveraged to differentiate in saturated markets. Expansion into emerging regions via local production and joint ventures enhances accessibility and reduces logistical barriers. E-commerce integration and direct-to-consumer models are being scaled to capture online demand. Additionally, investment in sustainable packaging, carbon-neutral production, and regenerative agriculture strengthens brand equity and meets evolving regulatory and consumer expectations across global markets.

TOP PLAYERS IN THE MARKET

- Heineken N.V. has established a prominent footprint in the Asia Pacific cider market through its globally recognized cider brand, Strongbow. The company has strategically expanded its presence by localizing production and tailoring flavor profiles to suit regional palates, particularly in India, Japan, and Australia. The company also invested in cold-chain logistics and partnered with e-commerce platforms like Rakuten and BigBasket to enhance distribution. Heineken’s “Brew a Better World” sustainability initiative has been extended to its cider operations, incorporating recyclable packaging and water-efficient production methods, reinforcing brand credibility among environmentally conscious consumers in urban Asia Pacific markets.

- Aspall Cyder has emerged as a key influencer in the premium cider segment across Asia Pacific, leveraging its centuries-old heritage and artisanal production methods. The Suffolk-based producer has focused on positioning its still and sparkling ciders as luxury imports, available in high-end restaurants and hotels in Singapore, Sydney, and Seoul. The company also introduced limited-edition oak-aged ciders in the region, emphasizing terroir and craftsmanship. Aspall’s commitment to organic certification and single-estate apple sourcing has resonated with discerning consumers seeking authenticity, enabling the brand to carve a niche in the premium on-trade sector and strengthen its reputation as a purveyor of heritage cider in Asia Pacific.

- Carlsberg Group has intensified its engagement in the Asia Pacific cider landscape through its Somersby brand, one of the most widely distributed cider labels in the region. Known for its fruit-forward flavors such as peach, blackberry, and rosé, Somersby has gained traction among younger consumers in markets like Thailand, Vietnam, and South Korea. Carlsberg has localized production in Thailand and India to reduce import costs and improve supply efficiency. Additionally, Carlsberg integrated Somersby into its broader “Together Towards Zero” sustainability framework, reducing carbon emissions in cider production by 35% since 2020, enhancing brand appeal in eco-sensitive markets.

RECENT HAPPENINGS IN THE MARKET

- In June 2023, Heineken launched Strongbow Ultra in Japan, a low-carbohydrate, 4% ABV sparkling cider, targeting health-conscious urban consumers and expanding its presence in the premium ready-to-drink segment.

- In September 2022, Aspall Cyder partnered with Fortnum & Mason in Singapore to introduce an exclusive range of oak-matured ciders, enhancing its visibility in luxury retail and high-end hospitality channels across Southeast Asia.

- In January 2025, Carlsberg Group inaugurated a new Somersby-dedicated production line at its ThaiBev joint venture facility in Thailand, optimizing supply for Southeast Asian markets and reducing lead times by 30%.

- In November 2023, Accolade Wines, owner of the Island Bay cider brand, acquired an orchard in Tasmania to secure premium apple supply and vertically integrate production for its Australia and New Zealand distribution.

- In March 2025, Boston Beer Company collaborated with Japanese retailer Don Quijote to launch a sake-infused limited-edition cider, blending Western fermentation with Eastern flavors to capture novelty-driven consumers in Japan.

MARKET SEGMENTATION

This research report on the global cider market has been segmented, and sub-segmented based on source, product, and region.

By Type

- Still Cider

- Sparkling Cider

- Draft Cider

- Apple Wine

By Distribution Channels

- Hypermarkets

- Supermarkets

- Departmental Stores

- Convenience Stores

- Online Stores

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East, and Africa

Frequently Asked Questions

1. What is the Cider Market?

The cider market includes alcoholic beverages made from fermented apple juice and other fruits, available in still, sparkling, and flavored varieties.

2. What drives growth in the Cider Market?

Rising demand for low-alcohol drinks, fruit-based beverages, and innovative flavors drive global cider consumption.

3. Which regions dominate the Cider Market?

Europe leads due to high traditional consumption, while North America and Asia-Pacific show strong growth.

4. What types of cider are popular in the Cider Market?

Popular types include apple cider, pear cider, fruit-flavored cider, and craft artisanal cider.

5. Which distribution channels are key in the Cider Market?

Supermarkets, liquor stores, pubs, restaurants, and online retail drive cider sales.

6. Who are the leading players in the Cider Market?

Key players include Heineken, Anheuser-Busch InBev, Carlsberg, Aston Manor, and C&C Group.

7. What consumer trends shape the Cider Market?

Trends include craft cider popularity, seasonal launches, premiumization, and eco-friendly packaging.

8. What challenges face the Cider Market?

Challenges include competition from beer and wine, taxation on alcohol, and raw material fluctuations.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com