Asia-Pacific Home Healthcare Market Size, Share, Trends & Growth Report By Product Type, Services Type, Software & Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC), Industry Analysis From 2026 to 2034

Asia-Pacific Home Healthcare Market Size

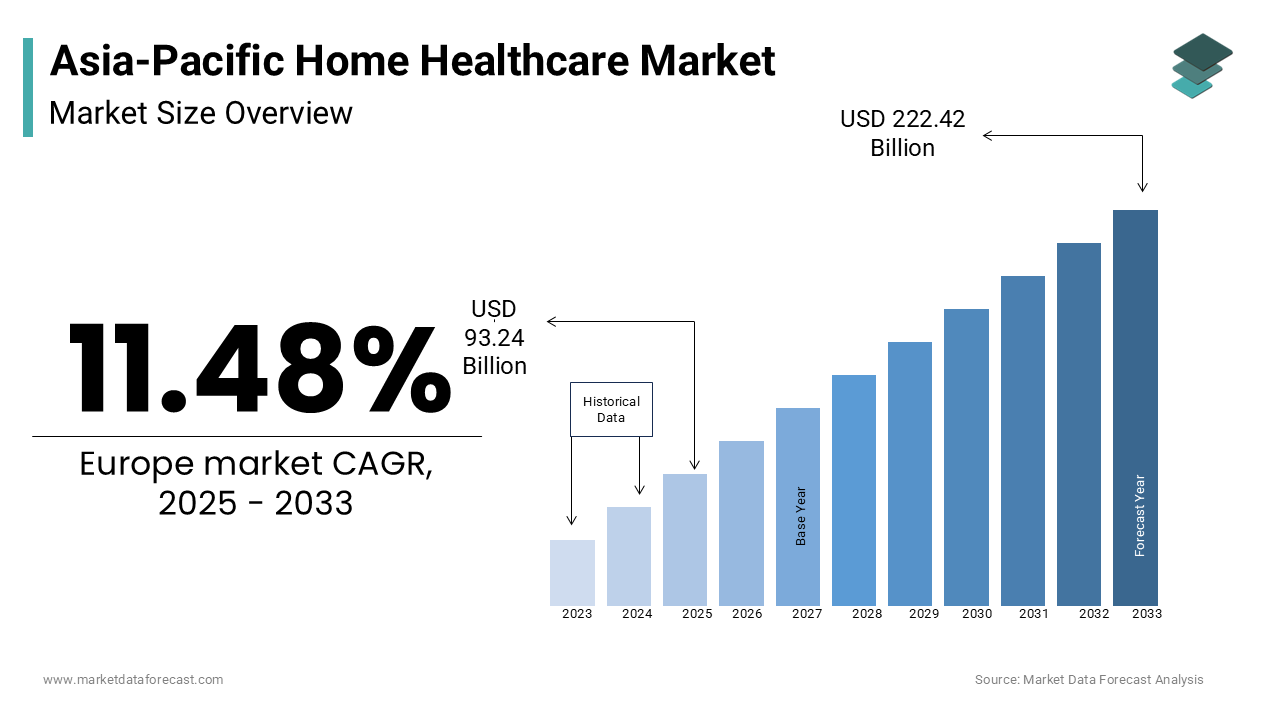

The size of the home healthcare market in the Asia Pacific was valued at USD 83.64 billion in 2024. The Asia-Pacific market is predicted to be growing at a CAGR of 11.48% from 2025 to 2033 and worth 222.42 billion by 2033 from USD 93.24 billion in 2025.

Home healthcare encompasses a broad spectrum of medical and non-medical services delivered within the patient residence rather than in institutional settings. This domain includes skilled nursing care, physical therapy, wound management, and chronic disease monitoring tailored for individuals requiring long-term support or post-acute recovery. The region is witnessing a profound demographic shift that fundamentally alters healthcare delivery models. According to the United Nations Department of Economic and Social Affairs, the population aged 60 years and older in Asia is projected to reach 1.3 billion by 2050, which represents a significant portion of the global elderly demographic. This aging cohort predominantly suffers from multiple chronic conditions necessitating continuous care outside hospital environments. Furthermore, as per the World Health Organization, non-communicable diseases account for 80% of all deaths in the South-East Asia Region and 77% in the Western Pacific Region. These health burdens drive the necessity for decentralized care solutions. The structural limitation of hospital infrastructure in densely populated nations further accelerates the transition toward home-based interventions. Governments across countries like Japan and Australia have already integrated home care into their national health insurance frameworks, recognizing it as a sustainable alternative to costly institutionalization. This evolving landscape reflects a strategic pivot toward patient-centric care models that prioritize comfort, accessibility, and cost efficiency, while addressing the escalating prevalence of age-related ailments and lifestyle disorders across the diverse economies of the Asia Pacific region.

MARKET DRIVERS

Escalating Prevalence of Chronic Diseases Drives Sustained Demand for Continuous Home Monitoring

The rising incidence of chronic illnesses, such as diabetes, cardiovascular disorders, and respiratory conditions is driving the expansion of home healthcare services in the Asia Pacific region. Chronic diseases require long-term management and regular monitoring, which are often more effectively and comfortably administered in a home setting. According to the International Diabetes Federation, the Western Pacific Region had approximately 206 million adults living with diabetes in 2021, which accounts for nearly half of the global total. This staggering figure underscores the urgent need for accessible healthcare solutions that do not rely solely on hospital visits. Home healthcare enables patients to receive consistent treatment, including insulin administration, blood glucose monitoring, and dietary counselling, without the burden of frequent travel to medical facilities. Additionally, the World Heart Federation states that cardiovascular diseases cause 20.5 million deaths annually worldwide, with a disproportionate impact on low and middle-income countries in Asia. The ability to manage these conditions at home reduces the risk of hospital-acquired infections and lowers overall healthcare expenditure. Patients benefit from personalized care plans that adapt to their daily routines, thereby improving adherence to medication and lifestyle modifications. The integration of remote patient monitoring technologies further enhances this driver by allowing healthcare providers to track vital signs in real time. This continuous data flow facilitates early intervention and prevents complications that could lead to emergency hospitalizations. Consequently, the growing burden of chronic diseases directly fuels the demand for comprehensive home healthcare services that offer both clinical efficacy and patient convenience.

Rapidly Aging Population Creates Urgent Need for Long Term Care Solutions

The demographic transition toward an older population structure is further boosting the growth of the home healthcare market across Asia Pacific. Nations such as Japan, China, and South Korea are experiencing unprecedented rates of aging, which strains traditional hospital systems and family care structures. According to the United Nations Department of Economic and Social Affairs, the number of persons aged 65 years or over in Eastern and South-Eastern Asia is expected to reach 573 million by 2050. This demographic shift creates a substantial demand for long-term care services that are specifically designed to address the complex needs of the elderly, including mobility assistance, palliative care, and dementia management. In Japan, where 29% of the population was aged 65 or older in 2023, according to the Statistics Bureau of Japan, the government has actively promoted home care services to alleviate the pressure on nursing homes and hospitals. Elderly individuals often prefer to age in place, maintaining their independence and dignity within familiar surroundings. Home healthcare providers offer specialized services, such as physical therapy to prevent falls and occupational therapy to enhance daily living skills. Furthermore, the decline in family sizes and increasing participation of women in the workforce reduce the availability of informal family caregivers. This societal change necessitates professional home care interventions to fill the gap. The convergence of these demographic and social trends ensures a robust and expanding customer base for home healthcare providers who can deliver high-quality, compassionate care to the aging population.

MARKET RESTRAINTS

Shortage of Skilled Healthcare Professionals Limits Service Scalability

A critical restraint hindering the growth of the Asia Pacific home healthcare market is the acute shortage of trained medical personnel capable of delivering specialized care in domestic environments. Providing effective home healthcare requires nurses, therapists, and caregivers who possess not only clinical expertise but also the ability to work independently and manage diverse patient needs without immediate supervisory support. According to the World Health Organization, the global healthcare sector faces a projected shortfall of 10 million health workers by 2030, with a significant deficit occurring in the South-East Asia Region. This shortfall is particularly pronounced in rural and semi-urban areas, where the demand for home care is rising due to limited access to hospitals. The lack of standardized training programs for home healthcare workers further exacerbates the issue. In many developing nations within the region, there is no formal certification process for home care aides, leading to variability in service quality and patient safety concerns. Additionally, the migration of skilled healthcare professionals from Asian countries to developed nations in Europe and North America for better employment opportunities depletes the local talent pool. For instance, the Philippines and India are major sources of exported nursing labor, which leaves domestic healthcare systems understaffed. This brain drain impedes the ability of home healthcare agencies to recruit and retain qualified staff. Without a sufficient workforce of competent professionals, the industry cannot scale its operations to meet the growing demand. Consequently, the scarcity of skilled labor remains a significant bottleneck that restricts market expansion and compromises the consistency of care delivery across the region.

Inadequate Reimbursement Policies and Regulatory Fragmentation Impede Market Penetration

The absence of comprehensive reimbursement frameworks and fragmented regulatory landscapes across Asia Pacific countries poses a substantial restraint to the widespread adoption of home healthcare services, which is further hindering the regional market expansion. In many nations, patients are required to pay out-of-pocket for home care services, which limits accessibility primarily to affluent segments of the population. According to the World Bank, out-of-pocket expenditure as a percentage of current health expenditure remains high in the region, exceeding 50% in nations like India and Bangladesh. This financial burden discourages middle and lower-income households from utilizing professional home healthcare services, even when medically necessary. Unlike hospital care, which is often covered by national health insurance schemes or private insurance policies, home healthcare services frequently fall outside these coverage parameters. The lack of clear guidelines on which services are reimbursable creates uncertainty for both providers and patients. Furthermore, the regulatory environment for home healthcare is inconsistent across the region. Some countries have well-defined licensing requirements for home care agencies, while others lack specific regulations, leading to an unorganized market sector with varying standards of practice. This regulatory ambiguity hinders the entry of international players and restricts the growth of domestic firms seeking to standardize their operations. The absence of unified policies also complicates the integration of home care data into national health records, affecting continuity of care. Until governments establish robust reimbursement mechanisms and harmonized regulatory standards, the market will struggle to achieve its full potential and ensure equitable access to quality home healthcare services for all citizens.

MARKET OPPORTUNITIES

Integration of Digital Health Technologies Offers Transformative Growth Avenues

The rapid advancement and adoption of digital health technologies present a significant opportunity for the Asia Pacific home healthcare market to enhance service delivery and operational efficiency. Telemedicine, remote patient monitoring, and mobile health applications enable healthcare providers to extend their reach beyond geographical constraints and offer continuous care to patients in remote areas. According to the Asian Development Bank, the digital health market in Asia is expected to reach 100 billion USD by 2025, facilitating early diagnosis and timely intervention. The proliferation of smartphones and internet connectivity in countries like India, Indonesia, and Vietnam provides a robust infrastructure for deploying digital health solutions. Remote monitoring devices can track vital signs, such as blood pressure, heart rate, and oxygen saturation, transmitting data directly to healthcare providers for analysis. This real-time information allows for proactive management of chronic conditions and reduces the need for unnecessary hospital visits. Furthermore, artificial intelligence-driven platforms can analyze patient data to predict health deteriorations and recommend personalized care plans. The integration of these technologies not only improves patient engagement but also optimizes resource allocation for healthcare providers. Governments in the region are increasingly supporting digital health innovations through policy initiatives and funding. For example, the Chinese government has promoted the development of internet-based medical services to modernize the healthcare system. By leveraging digital tools, home healthcare providers can offer more precise, efficient, and scalable services, thereby capturing a larger share of the market and improving overall patient satisfaction.

Expansion of Medical Tourism and Cross Border Healthcare Services Creates New Revenue Streams

The growing prominence of medical tourism in the Asia Pacific region offers a unique opportunity for home healthcare providers to diversify their revenue streams and expand their service offerings. Countries such as Thailand, Singapore, Malaysia, and India have established themselves as global hubs for medical tourism, attracting millions of international patients annually for affordable and high-quality treatments. According to the Tourism Authority of Thailand, the country serves as a major destination for medical travelers, contributing significantly to the national healthcare economy. Post-treatment recovery and rehabilitation are critical components of the medical tourism experience, and many patients prefer to recuperate in the comfort of their accommodation or a dedicated home care setting rather than staying in a hospital. Home healthcare agencies can partner with hospitals and medical tourism facilitators to provide specialized post-operative care, physiotherapy, and nursing services to these international patients. This collaboration not only enhances the overall patient experience but also creates a lucrative niche market for home care providers. Additionally, the rise of cross-border healthcare agreements within the region facilitates the movement of patients and healthcare professionals. Home healthcare firms can leverage these agreements to offer services to expatriates and foreign residents who require ongoing medical support. By tailoring their services to meet the diverse cultural and linguistic needs of international patients, providers can differentiate themselves in a competitive market. This strategic expansion into the medical tourism sector allows home healthcare companies to tap into a high-value customer base and drive sustainable growth.

MARKET CHALLENGES

Data Privacy and Security Concerns Pose Significant Operational Risks

The increasing reliance on digital technologies and electronic health records in home healthcare introduces substantial challenges related to data privacy and security. As home care providers collect and transmit sensitive patient information, including medical histories, vital signs, and personal identifiers, they become attractive targets for cyberattacks. According to the IBM Cost of a Data Breach Report, the average cost of a data breach in the healthcare industry reached 10.93 million USD in 2023, which is the highest among all sectors. In the Asia Pacific region, where cybersecurity infrastructure varies significantly across countries, protecting patient data remains a critical concern. Many home healthcare agencies lack robust cybersecurity measures, making them vulnerable to data breaches, ransomware attacks, and unauthorized access. The implementation of strict data protection regulations, such as the Personal Data Protection Act in Thailand and the Personal Information Protection Law in China, adds another layer of complexity for operators. Compliance with these regulations requires significant investment in secure IT systems, staff training, and regular audits. Failure to adhere to these standards can result in severe financial penalties, reputational damage, and loss of patient trust. Furthermore, the use of interconnected devices in remote patient monitoring increases the attack surface for potential security threats. Ensuring the confidentiality, integrity, and availability of patient data is paramount for maintaining credibility in the home healthcare sector. Providers must prioritize cybersecurity investments and adopt best practices to mitigate these risks. Without adequate safeguards, the threat of data breaches will continue to hinder the adoption of digital health solutions and erode confidence in home healthcare services.

Cultural Preferences and Family Dynamics Influence Service Acceptance

Cultural norms and traditional family dynamics in many Asia Pacific countries present a nuanced challenge to the widespread acceptance of professional home healthcare services. In societies such as China, India, and Korea, there is a strong cultural expectation that family members, particularly children, will care for their elderly parents at home. This filial piety is deeply ingrained in the social fabric, and relying on external caregivers can be perceived as a failure of familial duty or a lack of respect. According to research published in the journal BMC Geriatrics, cultural values and family support play a decisive role in the utilization of formal home care services among Asian elderly populations. This cultural preference limits the willingness of families to engage professional home healthcare providers, even when such services are medically advisable. Additionally, there is often a stigma associated with bringing strangers into the home, particularly for intimate care tasks. Overcoming these cultural barriers requires extensive community education and awareness campaigns to demonstrate the benefits of professional care in complementing family support. Home healthcare providers must also adapt their service models to involve family members in the care process, thereby respecting cultural values while ensuring professional standards. The challenge is further compounded by the diversity of cultural practices across the region, requiring localized strategies for market entry and customer engagement. Without addressing these deep-seated cultural attitudes, home healthcare companies may face resistance and slow adoption rates despite the growing need for such services.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 11.48% |

| Segments Covered | By Product Type, Type, Services Type and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, the Philippines, Indonesia, Singapore, and the rest of APAC. |

| Key Market Players | Almost Family Inc., Amedisys Inc., General Electric Company (GE), Kinnser Software Inc., Linde Group, Omron Corporation, Roche Holding AG, Philips Healthcare, Mckesson Corporation, LHC Group Inc., Kindred Healthcare, Fresenius Se & Co KGaA, Abbott Laboratories, and Apria Healthcare Group. |

SEGMENTAL ANALYSIS

By Product Type Insights

The testing, screening, and monitoring products segment led the market by commanding for 36.5% of the Asia-Pacific market share in 2025. The dominance of testing, screening and monitoring products segment in the Asia-Pacific market is attributed to the escalating prevalence of chronic diseases that demand regular physiological assessment outside clinical settings. The increasing adoption of point-of-care testing devices allows patients to manage conditions such as diabetes and hypertension effectively from home. According to the International Diabetes Federation, the Western Pacific Region is home to 206 million adults with diabetes, which creates a sustained demand for blood glucose monitoring systems. These devices are essential for daily management and prevention of acute complications. Furthermore, the rising geriatric population contributes significantly to this segment's leadership. According to the United Nations Department of Economic and Social Affairs, the number of people aged 60 years or older in Asia is projected to reach 1.3 billion by 2050. This demographic is prone to multiple comorbidities requiring continuous monitoring of vital signs, such as blood pressure and oxygen saturation. The integration of smart sensors in monitoring devices enables real-time data transmission to healthcare providers, facilitating timely interventions. Government initiatives promoting preventive healthcare also boost the uptake of screening products. For instance, the Healthy China 2030 plan emphasizes early detection and management of chronic diseases through accessible diagnostic tools. Consequently, the combination of high disease burden, aging demographics, and technological advancements solidifies the leading position of this segment in the regional market.

On the other hand, the therapeutic products segment is projected to be the fastest-growing segment and register a CAGR of 8.02% over the forecast period owing to the increasing preference for minimally invasive treatments and home-based administration of complex therapies. Patients are increasingly opting for home infusion therapy and respiratory care devices to avoid prolonged hospital stays and reduce the risk of nosocomial infections. According to the World Health Organization, chronic obstructive pulmonary disease is one of the leading causes of death in the region, with environmental factors being a significant contributor. This has led to a surge in the demand for home oxygen concentrators and nebulizers. Additionally, the advancement in drug delivery systems has made it feasible to administer biologics and other specialized medications at home. The growing awareness about patient-centric care models further supports this trend. In Japan, for example, the Long-Term Care Insurance system covers various therapeutic equipment rentals, encouraging widespread adoption among the elderly. Moreover, the rise in post-surgical recovery at home drives the demand for pain management devices and wound care products. According to the Global Burden of Disease Study, cardiovascular diseases remain a primary health challenge in Asia, necessitating long-term therapeutic interventions. The convergence of these factors, including technological innovation in drug delivery and supportive reimbursement policies in key markets, ensures that therapeutic products remain the fastest growing segment in the Asia Pacific home healthcare landscape.

By Type Insights

The home telehealth monitoring devices segment held the dominant position in the Asia Pacific home healthcare market by type and captured 40.9% of the regional market share in 2025. The dominating position of home telehealth monitoring devices segment in the regional market is attributed to the widespread proliferation of connected health devices that enable continuous remote patient monitoring. The ability to track vital parameters, such as heart rate, blood glucose, and electrocardiogram readings, in real time has revolutionized chronic disease management. According to the Asian Development Bank, approximately 50% of the population in many Asian countries now has access to high-speed internet, which has facilitated the adoption of Internet of Things enabled medical devices. These devices provide healthcare professionals with accurate data to make informed decisions without the need for physical visits. The aging population in countries like Japan and South Korea further accelerates the demand for these devices. According to the Statistics Bureau of Japan, nearly 29% of the population is aged 65 or older, creating a substantial user base for remote monitoring solutions. Additionally, the increasing incidence of lifestyle disorders, such as hypertension and diabetes, necessitates regular monitoring, which these devices efficiently provide. The integration of artificial intelligence in these devices enhances their predictive capabilities, allowing for early detection of health anomalies. Governments across the region are also promoting the use of telehealth devices to alleviate the burden on overcrowded hospitals. For instance, the Chinese government has supported the expansion of remote monitoring within its national health strategy. These factors collectively sustain the dominance of home telehealth monitoring devices in the regional market.

However, the home telehealth software segment is identified as the fastest growing segment and is estimated to grow at a CAGR of 10.5% over the forecast period owing to the increasing need for integrated platforms that connect patients, providers, and payers seamlessly. The software facilitates secure data exchange, appointment scheduling, and virtual consultations, which are critical components of modern home healthcare delivery. According to the World Health Organization, the adoption of digital health solutions in the South-East Asia Region is experiencing robust growth due to increased smartphone penetration and internet accessibility. The software segment benefits from the shift towards value-based care models, where outcomes are prioritized over volume. Advanced analytics and machine learning algorithms embedded in these platforms help in predicting patient deterioration and optimizing care plans. In Australia, the My Health Record system serves as a foundational infrastructure that supports the integration of various telehealth applications. Furthermore, the regulatory support for digital health innovations is strengthening across the region. The Indian government launched the Ayushman Bharat Digital Mission to create a unified digital health ecosystem, which significantly boosts the adoption of telehealth software. The COVID-19 pandemic also acted as a catalyst, accelerating the acceptance of virtual care platforms among both providers and patients. As healthcare systems strive for greater efficiency and cost-effectiveness, the demand for sophisticated software solutions that streamline operations and enhance patient engagement continues to surge, making it the fastest expanding segment.

By Services Type Insights

The skilled nursing care services segment had the major share of 33.6% of the Asia-Pacific market in 2025. The prominence of skilled nursing care services segment in the Asia-Pacific market is driven by the critical need for professional medical attention for patients with acute and chronic conditions who require specialized care at home. The shortage of hospital beds and the high cost of institutional care have shifted the focus toward home-based nursing services. According to the World Health Organization, the South-East Asia Region faces a significant shortfall of health workers, which intensifies the reliance on efficient home care models to maximize resource utilization. Skilled nurses provide essential services, such as wound care, medication administration, and post-operative monitoring, which are vital for patient recovery. The aging population in developed economies like Japan and Australia further fuels this demand. According to the Australian Institute of Health and Welfare, 17% of Australians were aged 65 and over in 2022, a proportion that is expected to increase substantially. These individuals often require complex medical management that can only be provided by trained nursing professionals. Additionally, the rising prevalence of non-communicable diseases necessitates long-term skilled care to prevent complications. Government initiatives in countries like Singapore support home nursing through subsidies and integrated care programs. The home nursing subsidy scheme in Singapore exemplifies such efforts to make skilled care accessible. These dynamics ensure that skilled nursing remains the cornerstone of the home healthcare service landscape in the region.

The respiratory therapy services segment is emerging as the fastest growing segment and is predicted to register a CAGR of 9.2% over the forecast period due to the increasing burden of respiratory diseases exacerbated by environmental factors, such as air pollution and smoking. According to the Global Burden of Disease Study, chronic obstructive pulmonary disease is a leading cause of mortality in the Asia Pacific region. The deteriorating air quality in major urban centers like New Delhi and Beijing has led to a higher incidence of respiratory ailments, necessitating ongoing therapeutic support. Home-based respiratory therapy offers patients the convenience of receiving treatment, such as oxygen therapy and ventilator management, in a comfortable environment. This approach reduces the frequency of hospital admissions and improves quality of life. The aging population is particularly vulnerable to respiratory issues, further driving demand. According to the United Nations, the number of elderly individuals in Asia is rising rapidly, increasing the pool of patients requiring respiratory care. Technological advancements in portable respiratory devices have also made home therapy more feasible and effective. In China, the government has implemented air quality improvement plans, but the legacy effects of pollution continue to impact public health. Additionally, the awareness about sleep apnea and other respiratory disorders is increasing, leading to higher diagnosis rates. These factors, combined with the convenience of home-based care, contribute to the rapid expansion of the respiratory therapy services segment.

REGIONAL ANALYSIS

China Home Healthcare Market Analysis

China demonstrated a robust performance in 2025 as the region’s primary engine of industrialization, and is expected to maintain its leading position through the forecast period by transitioning toward innovative drug development. The market status in China is characterized by rapid expansion driven by government reforms and a massive aging population. The Chinese government has prioritized healthy aging through initiatives such as the Healthy China 2030 blueprint, which aims to improve health outcomes and expand healthcare access. According to the National Bureau of Statistics of China, the population aged 60 and above reached 296.97 million by the end of 2023, representing approximately 21% of the total population. This demographic shift creates an immense demand for home-based medical services. The prevalence of chronic diseases, such as hypertension and diabetes, is also high, with the International Diabetes Federation reporting over 140 million diabetic adults in China. The government is actively promoting the integration of medical and elderly care services to address these challenges. Furthermore, the rapid urbanization and changing family structures have reduced the availability of informal caregivers, increasing the reliance on professional home healthcare. The adoption of digital health technologies is also accelerating, with telemedicine platforms gaining traction in tier 1 and tier 2 cities. The combination of policy support, demographic pressures, and technological adoption positions China as the dominant force in the regional home healthcare landscape, driving significant investment and innovation.

Japan Home Healthcare Market Analysis

Japan maintained a steady and mature performance in 2025, and is projected to experience consistent expansion during the forecast period as it focuses on high-value regenerative medicines and therapies for its aging population. The market status in Japan is defined by maturity and high per capita expenditure on home healthcare services, supported by a robust social insurance framework. The country has the oldest population in the world, with the Statistics Bureau of Japan reporting that 29% of its citizens were aged 65 or older in 2023. This extreme aging demographic necessitates comprehensive long-term care solutions. The Long-Term Care Insurance system, introduced in 2000, has been instrumental in formalizing and funding home care services. According to the Ministry of Health, Labour and Welfare of Japan, the number of individuals certified as needing care has reached approximately 7 million, with a significant portion receiving home-based services. The government continues to reform the system to ensure sustainability, focusing on community-based integrated care systems. These systems aim to allow elderly individuals to live in their own homes for as long as possible. The high level of technological adoption in Japan also supports the market, with advanced robotics and monitoring devices being widely used. The cultural preference for aging in place further reinforces the demand for home healthcare. Despite the mature nature of the market, continuous innovation and policy adjustments ensure steady growth and high service standards, making Japan a critical pillar of the regional market.

India Home Healthcare Market Analysis

India showcased significant growth momentum in 2025, and is likely to emerge as the fastest growing regional segment during the forecast period by leveraging its status as a global powerhouse for biosimilars. The market status in India is characterized by increasing current penetration and immense growth potential driven by increasing healthcare awareness and rising income levels. The country faces a dual burden of communicable and non-communicable diseases, with the World Health Organization indicating that non-communicable diseases account for 66% of all deaths in India. This epidemiological transition is driving the demand for chronic disease management services at home. The aging population is also growing, although at a slower pace than East Asia, with the United Nations projecting that the number of elderly people in India will reach 194 million by 2030. The private sector plays a dominant role in healthcare delivery, and home healthcare startups are gaining momentum in urban centers. According to the National Sample Survey Office, out-of-pocket expenditure on health remains a major challenge in India, which makes cost-effective home care an attractive alternative to hospitalization. The government initiatives, such as Ayushman Bharat, aim to strengthen primary healthcare, which indirectly supports home-based services. The increasing availability of skilled nursing staff and the expansion of digital health platforms further facilitate market growth.

Top Players in the Market

Amedisys Inc

Amedisys Inc stands as a prominent provider of home health and hospice care services with a significant footprint in the Asia Pacific region through strategic partnerships. The company focuses on delivering high quality patient centric care that improves clinical outcomes and reduces hospital readmissions. Recently Amedisys has invested heavily in digital health technologies to enhance remote patient monitoring capabilities. These initiatives allow for real time data collection and analysis which supports proactive care management. The company also emphasizes workforce development by training skilled nurses and therapists to meet the growing demand for home based services. By integrating advanced analytics into their care models Amedisys ensures personalized treatment plans for chronic disease patients. Their commitment to operational excellence and patient satisfaction strengthens their position as a key player in the evolving home healthcare landscape across diverse markets in the region.

B Braun Melsungen AG

B Braun Melsungen AG is a leading international healthcare company that provides essential therapeutic products and services for home healthcare settings. In the Asia Pacific market the company offers a wide range of infusion therapy pain management and wound care solutions tailored for home use. B Braun actively collaborates with local healthcare providers to establish comprehensive home care programs that ensure safe and effective treatment administration. The company recently expanded its manufacturing facilities in the region to improve supply chain efficiency and product availability. They also focus on educating healthcare professionals and patients on the proper use of home medical devices. Through continuous innovation in drug delivery systems and digital health integration B Braun enhances the quality of life for patients requiring long term care. Their strong emphasis on sustainability and corporate social responsibility further solidifies their reputation as a trusted partner in the Asia Pacific home healthcare sector.

Fresenius SE and Co KGaA

Fresenius SE and Co KGaA operates as a global healthcare group with a robust presence in the Asia Pacific home healthcare market particularly in renal care. The company provides dialysis products and services that enable patients to receive treatment at home thereby improving convenience and quality of life. Fresenius has been expanding its home dialysis programs across countries like Australia and Japan by offering comprehensive training and support to patients and caregivers. Recent initiatives include the launch of innovative portable dialysis machines that are easier to use and maintain in domestic settings. The company also invests in digital platforms that facilitate remote monitoring and communication between patients and medical teams. By focusing on patient empowerment and clinical excellence Fresenius aims to make home dialysis a preferred option for individuals with kidney failure. Their strategic collaborations with local healthcare systems help in scaling these services and addressing the rising prevalence of chronic kidney disease in the region.

Top Strategies Used by the Key Market Participants

Key players in the Asia Pacific Home Healthcare Market primarily employ strategic partnerships and collaborations to expand their geographic reach and service offerings. Companies frequently engage in mergers and acquisitions to integrate complementary technologies and strengthen their competitive position. Investment in digital health technologies such as telemedicine and remote patient monitoring is a common strategy to enhance service efficiency and patient engagement. Firms also focus on product innovation by developing user friendly medical devices tailored for home use. Additionally expanding the skilled workforce through training programs ensures high quality care delivery. Many organizations prioritize regulatory compliance and adherence to local standards to build trust with stakeholders. Marketing efforts often emphasize the cost effectiveness and convenience of home based care compared to institutional settings. These strategies collectively drive growth and enable companies to address the diverse needs of the aging population and chronic disease patients across the region effectively and sustainably over time.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific Home Healthcare Market is characterized by a mix of global giants and regional players striving to capture market share through innovation and service differentiation. Global companies leverage their extensive resources and technological expertise to introduce advanced home care solutions while local firms capitalize on their understanding of cultural nuances and regulatory landscapes. The market is moderately fragmented with numerous small and medium sized enterprises offering specialized services such as nursing care and physical therapy. Competitive intensity is increasing as companies invest in digital health platforms to enhance patient monitoring and engagement. Strategic alliances with hospitals and insurance providers are common tactics to secure referral networks and reimbursement pathways. Price competition remains relevant in price sensitive markets but quality and reliability are becoming key differentiators. The entry of technology startups focusing on telehealth and artificial intelligence further disrupts traditional models. Companies must continuously adapt to changing regulatory requirements and patient expectations to maintain their competitive edge. This dynamic environment fosters innovation and drives improvements in care delivery standards across the diverse Asia Pacific region ensuring better outcomes for patients.

RECENT MARKET DEVELOPMENTS

- In March 2023, B Braun Melsungen AG launched a new home infusion therapy program in Singapore. This initiative is anticipated to allow B Braun to offer more comprehensive home care solutions and strengthen the Asia Pacific Home Healthcare Market presence.

- In June 2023, Fresenius SE and Co KGaA expanded its home dialysis services in Australia. This expansion is anticipated to allow Fresenius to reach more patients with kidney failure and strengthen the Asia Pacific Home Healthcare Market presence.

- In September 2023, Amedisys Inc partnered with a leading telehealth provider in Japan. This partnership is anticipated to allow Amedisys to integrate remote monitoring tools and strengthen the Asia Pacific Home Healthcare Market presence.

- In January 2024, B Braun Melsungen AG opened a new manufacturing facility in India. This investment is anticipated to allow B Braun to improve supply chain efficiency and strengthen the Asia Pacific Home Healthcare Market presence.

- In May 2024, Fresenius SE and Co KGaA introduced a portable dialysis device in South Korea. This launch is anticipated to allow Fresenius to enhance patient convenience and strengthen the Asia Pacific Home Healthcare Market presence

KEY MARKET PLAYERS

Companies that play a key role in the Asia Pacific home healthcare market include

- Almost Family Inc.

- Amedisys Inc.

- General Electric Company (GE)

- Kinnser Software Inc.

- Linde Group

- Omron Corporation

- Roche Holding AG

- Philips Healthcare

- McKesson Corporation

- LHC Group Inc.

- Kindred Healthcare

- Fresenius SE & Co. KGaA

- Abbott Laboratories

- Apria Healthcare Group

MARKET SEGMENTATION

This research report on the Asia Pacific home healthcare market has been segmented and sub-segmented into the following categories.

By Product Type

- Testing, Screening, & Monitoring Products

- Therapeutic Products

- Mobility Care Products

By Type

- Home Telehealth Monitoring Devices

- Home Telehealth Services

- Home Telehealth Software

By Services Type

- Rehabilitation Therapy Services

- Infusion Therapy Services

- Unskilled Care Services

- Respiratory Therapy Services

- Pregnancy Care Services

- Skilled Nursing Care Services

- Hospice

- Palliative Care Services

By Software

- Agency Software

- Clinical Management Systems

- Hospice Solutions

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What are the major trends in the APAC Home Healthcare Market?

The growing adoption of telehealth services, the rise of mobile health apps, and the development of IoT-based healthcare devices are some of the major trends in the APAC home healthcare market.

What are the opportunities for investors in the APAC Home Healthcare Market?

Investors can explore opportunities in telehealth startups, medical device manufacturing, and home healthcare service providers in the APAC region.

How is the COVID-19 pandemic impacting the APAC Home Healthcare Market?

The COVID-19 pandemic has accelerated the adoption of telehealth and home healthcare services in APAC, making it a growing sector.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com