Asia Pacific Industrial Sensor Market Size, Share, Trends & Growth Forecast Report By Product Type (Pressure, Temperature, Level, Flow, Magnetic Field, Acceleration & Yaw Rate, Gas, Other Product Types), End-user Industry (Automotive, Aerospace & Military, Chemical & Petrochemical, Medical, Electronics & Semiconductor, Power Generation, Oil & Gas, Food & Beverage, Water & Wastewater, Other End Users), and Country (India, China, Japan, South Korea, Australia, New Zealand, Rest of APAC) – Industry Analysis, 2026 to 2034

Market Size, 2025

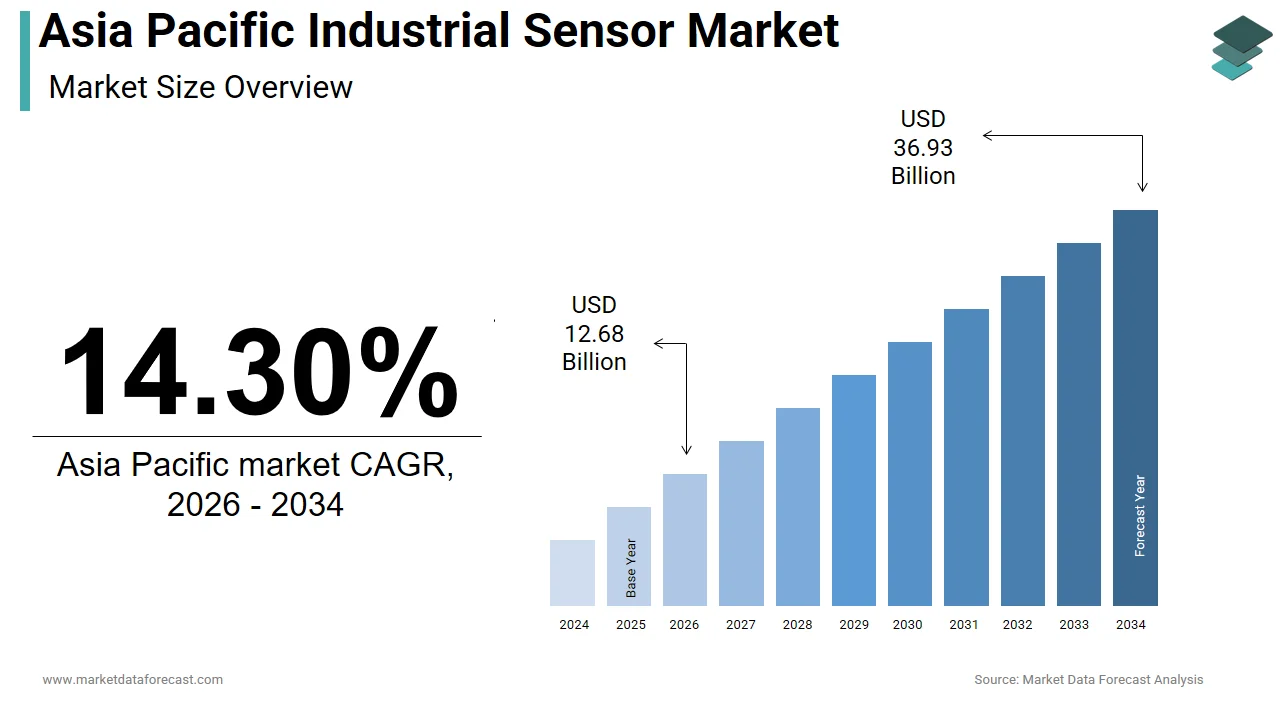

$11.09 BnMarket Estimate, 2026

$12.68 BnMarket Forecast, 2034

$36.93 BnCAGR, 2026–2034

14.30%Asia Pacific Industrial Sensor Market Size

The Asia Pacific industrial sensor market was valued at USD 11.09 billion in 2025, is estimated to reach USD 12.68 billion in 2026, and is projected to reach USD 36.93 billion by 2034, growing at a CAGR of 14.30% from 2026 to 2034.

The industrial sensor market in the Asia Pacific region encompasses a wide range of sensing devices used to monitor and control physical parameters such as temperature, pressure, humidity, proximity, and motion across various manufacturing and process industries. These sensors play a critical role in automation systems, enabling real-time data acquisition, predictive maintenance, and enhanced operational efficiency. With rapid industrialization, growing adoption of Industry 4.0 technologies, and increasing investments in smart infrastructure, the demand for industrial sensors has seen a substantial rise across key economies such as China, Japan, India, and South Korea.

MARKET DRIVERS

Surge in Smart Manufacturing and Automation Adoption

The Asia Pacific is the widespread adoption of smart manufacturing and automation technologies is one of the primary drivers fueling the growth of the industrial sensor market. Governments and private enterprises across the region are investing heavily in automation to enhance productivity, reduce labor dependency, and improve product quality.

Also, as per Japan’s Robot Revolution Initiative Council, robot density in Japanese manufacturing plants reached 390 robots per 10,000 employees in 2023, up from 332 in 2020, necessitating extensive deployment of industrial sensors for precision control and safety.

Industrial sensors are integral to these automation frameworks, providing real-time feedback on variables such as temperature, pressure, and positioning. This trend is expected to continue as industries prioritize efficiency and agility in response to fluctuating global demand.

Expansion of Renewable Energy Infrastructure

The rapid expansion of renewable energy infrastructure, particularly in solar and wind power generation, is another significant driver of the Asia Pacific industrial sensor market. Industrial sensors are extensively deployed in renewable energy systems to monitor performance, ensure grid stability, and optimize energy output. As governments across the region commit to decarbonization targets and sustainable development goals, investments in clean energy have surged.

According to the International Renewable Energy Agency (IRENA), Asia Pacific added over 150 gigawatts of new renewable capacity in 2023 alone, accounting for nearly half of global additions.

Further, as per Wood Mackenzie, the Asia Pacific region accounted for 62% of global battery storage installations in 2023, where industrial sensors are crucial for monitoring voltage, current, and thermal conditions. This ongoing shift toward clean energy not only supports environmental goals but also stimulates sustained demand for industrial sensors across the energy value chain.

MARKET RESTRAINTS

High Capital Investment and Maintenance Costs

High initial capital investment and ongoing maintenance costs associated with advanced sensor systems continue to be a restraint for the Asia Pacific industrial sensor market. While industrial sensors offer long-term benefits in terms of efficiency and automation, the upfront expenses can be prohibitive for small and medium-sized enterprises (SMEs) that form a significant portion of the regional manufacturing base.

According to the Asian Development Bank, SMEs contribute to over 50% of employment and 40% of GDP in many Asia Pacific economies. However, a survey conducted by the Confederation of Indian Industry (CII) found that nearly 60% of Indian SMEs cited high equipment costs as a barrier to adopting automation technologies, including industrial sensors.

Moreover, the complexity of sensor integration and the need for skilled personnel add to the financial burden. As per a report by PwC, the average cost of deploying a full-scale industrial Internet of Things (IIoT) system including sensors, gateways, and analytics software ranges from $1 million to $5 million per facility in the Asia Pacific region. Moreover, ongoing calibration, replacement, and software updates require specialized expertise, which further escalates operational expenditures.

This economic reality hampers the widespread adoption of industrial sensors, particularly among smaller players, limiting overall market penetration.

Supply Chain Disruptions and Component Shortages

The persistent issue of supply chain disruptions and component shortages is another critical restraint affecting the Asia Pacific industrial sensor market. Over the past few years, geopolitical tensions, pandemic-related shutdowns, and logistical bottlenecks have significantly impacted the availability of essential electronic components such as microcontrollers, semiconductors, and printed circuit boards key elements in industrial sensor manufacturing.

Like, in Japan, as per the Nikkei Asian Review, major sensor producers like Omron and Keyence faced delays in production schedules due to unavailability of raw materials and prolonged shipping times from Southeast Asia.

Furthermore, according to the China Semiconductor Industry Association, the country’s domestic semiconductor production met only 15% of internal demand in 2023, forcing manufacturers to import the remaining from overseas suppliers. This dependency exposes the industrial sensor industry to risks stemming from trade restrictions and export controls, especially from the United States.

These disruptions not only slow down production but also inflate costs, making it difficult for companies to meet rising demand efficiently. As a result, project timelines are extended, and some potential buyers delay procurement, creating a ripple effect across the market.

MARKET OPPORTUNITIES

Integration of AI and Edge Computing in Sensor Systems

The integration of artificial intelligence (AI) and edge computing within sensor systems is a transformative opportunity emerging in the Asia Pacific industrial sensor market. This technological convergence allows for real-time data processing at the source, reducing latency, improving decision-making accuracy, and enhancing overall system responsiveness. As industries increasingly adopt AI-driven analytics, the demand for intelligent sensor networks capable of autonomous decision-making is rising sharply.

Edge computing complements this evolution by enabling localized data analysis, minimizing bandwidth usage, and enhancing cybersecurity. Companies like Bosch and Yokogawa are actively embedding edge capabilities into their industrial sensor portfolios, unlocking new applications in smart cities, agriculture, and logistics.

This shift toward intelligent, decentralized sensor ecosystems presents a compelling growth avenue for the Asia Pacific industrial sensor market, offering enhanced functionality and scalability across diverse industrial verticals.

Growth of Smart Cities and Urban Infrastructure Projects

The proliferation of smart city initiatives and large-scale urban infrastructure development programs across the Asia Pacific region is creating significant opportunities for the industrial sensor market. Governments are increasingly investing in intelligent transportation systems, smart grids, waste management solutions, and environmental monitoring networks, all of which rely heavily on industrial sensors for real-time data collection and control.

Also, South Korea’s Ministry of the Interior and Safety announced in 2023 that over 100,000 IoT-enabled sensors had been installed in Seoul to monitor air quality, noise levels, and seismic activity. These deployments not only enhance urban livability but also create recurring demand for industrial sensors in both public and private sectors.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Connected Sensor Networks

The growing risk of cybersecurity threats targeting connected sensor networks is a pressing challenge confronting the Asia Pacific industrial sensor market. As industrial sensors become increasingly integrated with the Industrial Internet of Things (IIoT) and cloud-based analytics platforms, they expose vulnerabilities that malicious actors can exploit to disrupt operations, steal sensitive data, or compromise safety systems.

According to the Ponemon Institute, in 2023, 68% of industrial organizations in the Asia Pacific region experienced at least one cyberattack targeting their operational technology (OT) environments, many of which involved sensor-based control systems. The lack of standardized security protocols in legacy sensor infrastructure makes these systems particularly susceptible to breaches.

As per South Korea’s Korea Internet & Security Agency (KISA), ransomware attacks on manufacturing facilities increased by 42% in 2023, with compromised sensor nodes serving as entry points for broader network infiltration. In one notable case, a semiconductor plant was forced to halt production temporarily after unauthorized access to its temperature and pressure monitoring sensors disrupted fabrication processes.

Besides, the growing use of wireless and Bluetooth-enabled industrial sensors introduces further exposure to eavesdropping and data manipulation. Addressing these vulnerabilities requires significant investment in secure firmware updates, network segmentation, and intrusion detection systems, adding complexity and cost to sensor deployment strategies.

Regulatory and Standardization Hurdles Across Diverse Markets

The Asia Pacific industrial sensor market faces considerable regulatory and standardization challenges due to the region’s vast diversity in compliance requirements, certification procedures, and technical specifications. Unlike the European Union or North America, where harmonized standards simplify cross-border trade, the Asia Pacific lacks a unified framework for industrial sensor certifications, leading to fragmented market access conditions.

For instance, in China, the Certification and Accreditation Administration of China (CNCA) mandates compulsory product certification (CCC) for most industrial electronics, including sensors, while Japan follows the JIS (Japanese Industrial Standards) system, which often requires separate testing and documentation.

In India, the Bureau of Indian Standards (BIS) introduced mandatory conformity assessments for certain categories of industrial sensors in 2023, increasing time-to-market for foreign manufacturers. These overlapping and sometimes conflicting regulations create compliance complexities for multinational sensor vendors.

Furthermore, discrepancies in environmental and safety regulations complicate product design and localization efforts. The absence of a coordinated regulatory ecosystem hampers the seamless deployment of industrial sensors across borders, discouraging smaller firms from entering niche markets.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, End-user Industry, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | Texas Instruments Incorporated, STMicroelectronics N.V., Emerson Electric Co, Rockwell Automation Inc., ABB Limited, and others. |

SEGMENTAL ANALYSIS

By Product Insights

The temperature sensors segment represented the largest product in the Asia Pacific industrial sensor market by accounting for 23.5% of total revenue in 2024. Expansion of process industries, particularly in China and India, is one key driver behind the strong performance of temperature sensors. Apart from these, the rise in smart building automation systems has further fueled demand for temperature sensorsMoreover, the adoption of IoT-enabled temperature sensors in agriculture and cold chain logistics has expanded their application base

The magnetic field sensors segment is projected to register the highest CAGR of 10.6% between 2026 and 2034 in the Asia Pacific industrial sensor market. Their increasing deployment in automotive electrification and industrial automation applications, particularly in countries like China, South Korea, and Japan, is fuelling the rapid expansion of the magnetic field sensors segment. According to McKinsey, electric vehicle (EV) production in the Asia Pacific region accounted for over 60% of global output in 2023, with magnetic field sensors playing a crucial role in motor control, battery management, and steering systems. Another significant growth driver is the adoption of magnetic sensors in robotics and automated guided vehicles (AGVs). Further, in South Korea, as per the Korea Institute of Machinery & Materials (KIMM), magnetic field sensors were increasingly used in semiconductor manufacturing tools to detect misalignments and ensure precision handling of wafers. Furthermore, advancements in contactless current sensing technology have enhanced the appeal of magnetic field sensors in energy infrastructure.

By End-user Industry Insights

The automotive industry held the largest share of the Asia Pacific industrial sensor market with 21.4% of total value in 2023. China remains the world’s largest automobile producer, having manufactured over 28 million vehicles in 2023, as reported by the China Association of Automobile Manufacturers (CAAM). Each modern vehicle incorporates between 60 and 100 sensors, including pressure, acceleration, and magnetic field sensors, to support functions such as engine control, braking, and driver assistance systems.

In addition, the accelerated adoption of electric and autonomous vehicles has significantly boosted sensor demand. These vehicles rely heavily on sensors for battery management, thermal regulation, and environmental perception, particularly in Level 2+ autonomous driving features. Japan also plays a pivotal role in sustaining this segment’s growth. Moreover, South Korea’s automotive supply chain, led by companies like Hyundai Mobis and LG Magna e-Powertrain, is integrating sensor-based ADAS (Advanced Driver Assistance Systems) at an unprecedented pace.

The medical sector segment is emerging as the fastest-growing end-user segment in the Asia Pacific industrial sensor market, recording a CAGR of 12.3% between 2025 and 2033. This surge is primarily driven by the Increasing demand for diagnostic and patient monitoring devices, especially in response to aging populations and post-pandemic healthcare investments is primarily driving the rise of the medical sector segment. According to the World Health Organization (WHO), the proportion of the population aged 65 and above in the Asia Pacific is expected to rise from 12% in 2023 to over 20% by 2035, necessitating greater reliance on home healthcare and wearable monitoring systems equipped with industrial-grade sensors. With increasing hospital automation and AI-assisted diagnostics, the medical sector is set to continue its rapid ascent, reinforcing its position as a key growth engine for the industrial sensor market in the Asia Pacific.

COUNTRY-LEVEL ANALYSIS

China Industrial Sensor Market Insights

China stood as the largest contributor to the Asia Pacific industrial sensor market by holding a 35.2% share in 2024. This lead position is underpinned by the country’s massive industrial base, rapid digital transformation, and aggressive push toward smart manufacturing and electric mobility. The Chinese government has been instrumental in fostering sensor adoption through initiatives like “Made in China 2025” and the “14th Five-Year Plan”, which prioritize automation, robotics, and advanced sensor integration in industries. Moreover, the country’s electric vehicle boom has created a substantial demand for sensors. Companies like BYD and NIO are leading the charge, integrating sensor networks for battery management, thermal regulation, and autonomous driving features. Beyond automotive, the semiconductor and electronics manufacturing sectors remain major consumers of industrial sensors. As per SEMI, China accounted for nearly 20% of global semiconductor manufacturing capacity in 2023, with sensor-based inspection systems ensuring high yields and product reliability.

Japan Industrial Sensor Market Insights

Japan is known for its advanced manufacturing capabilities and early adoption of automation technologies. Japan continues to be a key market for high-precision industrial sensors. The country’s industrial robotics sector serves as a major driver of sensor demand. Companies like Fanuc and Yaskawa Electric are embedding sensor arrays into robotic arms to enhance flexibility and safety in production lines. Moreover, Japan’s aging population and focus on elderly care have spurred innovation in sensor-based assistive technologies. The automotive industry, particularly in hybrid and electric vehicles, also contributes significantly to sensor demand. Toyota and Honda together produced over 6 million vehicles in 2023, many of which featured advanced driver assistance systems (ADAS) utilizing radar, lidar, and ultrasonic sensors.

India Industrial Sensor Market Insights

India is a fast-growing region in the Asia Pacific industrial sensor market. The country’s market is being propelled by rapid industrialization, government-backed digitization efforts, and surging investments in infrastructure and clean energy. One of the primary drivers of sensor adoption in India is the expansion of the renewable energy sector. The Solar Energy Corporation of India (SECI) noted that every 10 MW solar plant requires an average of 1,200 sensors for real-time monitoring and maintenance. Simultaneously, the Make in India initiative has catalyzed growth in domestic manufacturing, particularly in electronics and automotive segments. The smart city program is another major growth lever.

South Korea Industrial Sensor Market Insights

South Korea is a major contributor to the market. The country’s advanced industrial structure, particularly in semiconductors, automotive, and consumer electronics, fuels consistent demand for high-performance industrial sensors. The semiconductor industry remains a cornerstone of sensor adoption in South Korea. According to the Korea Semiconductor Industry Association (KSIA), the country accounted for around 18% of global memory chip production in 2023, with fabrication plants relying on ultra-sensitive pressure and flow sensors to maintain process purity and yield efficiency. In the automotive sector, South Korea is witnessing a surge in electric and autonomous vehicle development. As per the Korea Automobile Manufacturers Association (KAMA), EV production in the country rose by 33% in 2023, with each model integrating over 100 sensors for battery management, climate control, and ADAS functionalities. LG Magna e-Powertrain, a joint venture between LG Electronics and Magna International, launched several sensor-integrated drive systems tailored for EV platforms. Besides, the government’s push for smart factories has accelerated sensor integration in SMEs. South Korea’s technological prowess and strategic investments in next-generation industries ensure its continued prominence in the regional industrial sensor market.

Australia Industrial Sensor Market Insights

Australia captures a modest but stable share of the Asia Pacific industrial sensor market. While not as large as other markets, Australia’s industrial sensor demand is characterized by high-value applications in mining, energy, and environmental monitoring. The mining industry is a key driver of sensor deployment, given the country’s vast natural resource reserves and reliance on automation for safety and efficiency. Companies like Rio Tinto and BHP have invested heavily in autonomous haulage systems, which depend on accelerometers, GPS, and proximity sensors. The energy sector, particularly renewables, is another major growth area. As per the Clean Energy Council of Australia, the country installed over 5 GW of new solar and wind capacity in 2023, with sensor networks playing a crucial role in turbine diagnostics, panel efficiency tracking, and grid synchronization. The Australian Renewable Energy Agency (ARENA) supported several pilot projects involving AI-enhanced sensor systems for predictive maintenance in wind farms. Apart from these, environmental monitoring initiatives are expanding sensor usage in water treatment, air quality assessment, and agricultural irrigation. Despite its smaller size, Australia’s industrial sensor market is distinguished by high-tech applications and a focus on sustainability, positioning it as a steady performer in the regional landscape.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific industrial sensor market is marked by intense rivalry among global and regional players striving to capture market share through innovation, strategic expansion, and localized offerings. With rapid industrialization and increasing automation across sectors like automotive, electronics, and energy, the demand for high-performance sensors continues to rise, prompting companies to differentiate themselves through product versatility and application-specific solutions. Established international brands leverage their technological expertise and brand reputation, while domestic players capitalize on cost advantages and deep-rooted supply chain relationships. The market also witnesses growing convergence between sensor manufacturers and software developers, especially in the context of Industry 4.0 and smart manufacturing ecosystems. As a result, firms are not only focusing on hardware excellence but also on integrating digital platforms that offer analytics and remote monitoring capabilities. This dynamic environment fosters continuous evolution, where agility, innovation, and strategic positioning determine long-term competitiveness.

KEY MARKET PLAYERS

Some of the noteworthy companies in the Asia Pacific industrial sensor market profiled in this report are

- Texas Instruments Incorporated

- STMicroelectronics N.V.

- Emerson Electric Co.

- Rockwell Automation Inc.

- ABB Limited

TOP LEADING PLAYERS IN THE MARKET

One of the leading players in the Asia Pacific industrial sensor market is Honeywell International Inc. The company has a strong foothold in the region, offering a wide range of industrial sensors including pressure, temperature, and gas sensors. Honeywell plays a crucial role in driving innovation through its advanced sensing technologies tailored for aerospace, automotive, and manufacturing applications. Its regional R&D centers focus on developing customized sensor solutions that cater to the evolving needs of Asian industries.

Another major player is TE Connectivity Ltd., known for its robust portfolio of high-performance sensors used across diverse sectors such as automotive, healthcare, and industrial automation. TE Connectivity’s strategic partnerships with local manufacturers and its emphasis on miniaturization and durability have positioned it strongly in the Asia Pacific market. The company consistently invests in localized production facilities to meet growing demand and support supply chain resilience.

The third key player is Omron Corporation, a Japanese multinational with deep expertise in automation and control systems. Omron specializes in proximity, pressure, and temperature sensors widely used in factory automation and robotics. The company's presence in emerging markets within the Asia Pacific is expanding rapidly due to its focus on smart manufacturing and Industry 4.0 integration. Omron’s commitment to precision engineering and adaptive sensor technologies makes it a dominant force in the region’s industrial ecosystem.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

A primary strategy adopted by key players in the Asia Pacific industrial sensor market is product innovation and technological advancement. Companies are continuously investing in research and development to design more accurate, durable, and compact sensors that can operate under extreme conditions. This includes integrating AI and IoT capabilities into sensor systems to enable real-time monitoring and predictive maintenance across various industries.

Another critical approach is strategic partnerships and collaborations. Leading firms are forming alliances with local manufacturers, system integrators, and technology providers to enhance their regional presence and better serve industry-specific applications. These collaborations help in adapting global technologies to local requirements while accelerating time-to-market for new sensor solutions.

Lastly, expansion through localized manufacturing and distribution networks is a key growth strategy. By establishing or expanding production units and service centers in emerging markets, companies aim to reduce logistics costs, comply with regulatory standards, and improve customer responsiveness. This localization also supports customization efforts, enabling firms to address specific industrial demands across different countries in the Asia Pacific region.

RECENT MARKET DEVELOPMENTS

- In January 2024, Honeywell announced the launch of its next-generation wireless pressure sensor, specifically designed for harsh industrial environments in the Asia Pacific region. This product aims to enhance operational efficiency in oil & gas and chemical processing industries by providing real-time data transmission without the need for complex wiring systems.

- In March 2024, TE Connectivity expanded its manufacturing facility in Malaysia, reinforcing its commitment to the Asia Pacific market. The upgraded plant focuses on producing high-precision sensors for automotive and consumer electronics applications, supporting faster delivery times and improved supply chain reliability.

- In June 2024, Omron Corporation partnered with a Singapore-based AI startup to integrate machine learning algorithms into its sensor systems, enhancing predictive maintenance capabilities for smart factories across Southeast Asia. This collaboration aligns with the broader trend of digital transformation in industrial automation.

- In September 2024, Siemens opened a new regional innovation hub in Shanghai, dedicated to developing advanced sensor technologies for smart infrastructure and energy management. The center serves as a collaborative platform for local engineers, startups, and academic institutions to co-develop cutting-edge industrial sensing solutions.

- In December 2024, Bosch Sensortec entered into a joint venture with a South Korean semiconductor firm to develop ultra-compact MEMS sensors for next-generation electric vehicles and wearable medical devices. This move strengthens Bosch’s position in the rapidly growing mobility and healthcare segments of the Asia Pacific market.

MARKET SEGMENTATION

This Asia Pacific industrial sensor market research report is segmented and sub-segmented into the following categories.

By Product Type

- Pressure

- Temperature

- Level

- Flow

- Magnetic Field

- Acceleration & Yaw Rate

- Gas

- Other Product Types

By End-user Industry

- Automotive

- Aerospace & Military

- Chemical & Petrochemical

- Medical

- Electronics & Semiconductor

- Power Generation

- Oil & Gas

- Food & Beverage

- Water & Wastewater

- Other End Users

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Rest Of APAC

Frequently Asked Questions

1. What are the main drivers for industrial sensor adoption in Asia Pacific?

Key drivers include industrial automation, rapid manufacturing expansion, government Industry 4.0 initiatives, the rise of IoT, and widespread deployment of smart and wireless sensors for productivity and compliance

2. Who are the top industrial sensor vendors in the Asia Pacific region?

Leading manufacturers include Honeywell International, Rockwell Automation, Texas Instruments, Panasonic Holdings, TE Connectivity, Siemens AG, Amphenol Corporation, Bosch Sensortec, STMicroelectronics, and ABB

3. Which countries are major contributors to the Asia Pacific industrial sensors market?

China, Japan, and India are the largest markets, driven by strong manufacturing bases, rising electronics and automotive output, and rapid adoption of automation technologies

4. What types of industrial sensors are most in demand?

Major sensor types include pressure sensors, temperature sensors, position sensors, image sensors, flow sensors, force sensors, and accelerometers, with growth in both contact and non-contact categories

5. How is Industry 4.0 impacting the industrial sensor market in APAC?

Industry 4.0 fosters the integration of AI, machine learning, and industrial IoT, resulting in the deployment of more intelligent, miniaturized, and networked sensors for smart manufacturing and predictive maintenance

6.What are the key end-user industries for industrial sensors in Asia Pacific?

Key sectors include manufacturing, automotive, oil & gas, chemical, pharmaceuticals, energy & power, mining, and semiconductor production

7. What are the main challenges in the Asia Pacific industrial sensor market?

Key challenges include integration complexity, high initial deployment costs, skill gaps for advanced automation, and ensuring interoperability across legacy and new systems

8. How is AI and edge computing influencing industrial sensing in APAC?

AI, machine learning, and edge computing enable real-time analytics, smarter sensors, reduced data latency, and better process optimization in smart factories

9. How has the adoption of 5G technology impacted industrial sensors in Asia Pacific?

5G increases sensor-to-cloud connectivity, supports larger-scale automation, and enables advanced smart factory setups with faster, more reliable data transmission

10. What are the trends in wireless and battery-free sensors in the region?

Wireless and battery-free sensors are gaining momentum, especially in difficult-to-access or hostile environments, and are poised for rapid growth through 2033

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com