Asia Pacific Speed Sensor Market Size, Share, Trends & Growth Forecast Report By Type (Hall Effect, Magneto Resistive, Variable Reluctance, Others), Application (Automotive, Industrial, Aerospace & Defense, Consumer Electronics, Others), and Country (India, China, Japan, South Korea, Rest of APAC) – Industry Analysis, 2026 to 2034

Asia Pacific Speed Sensor Market Size

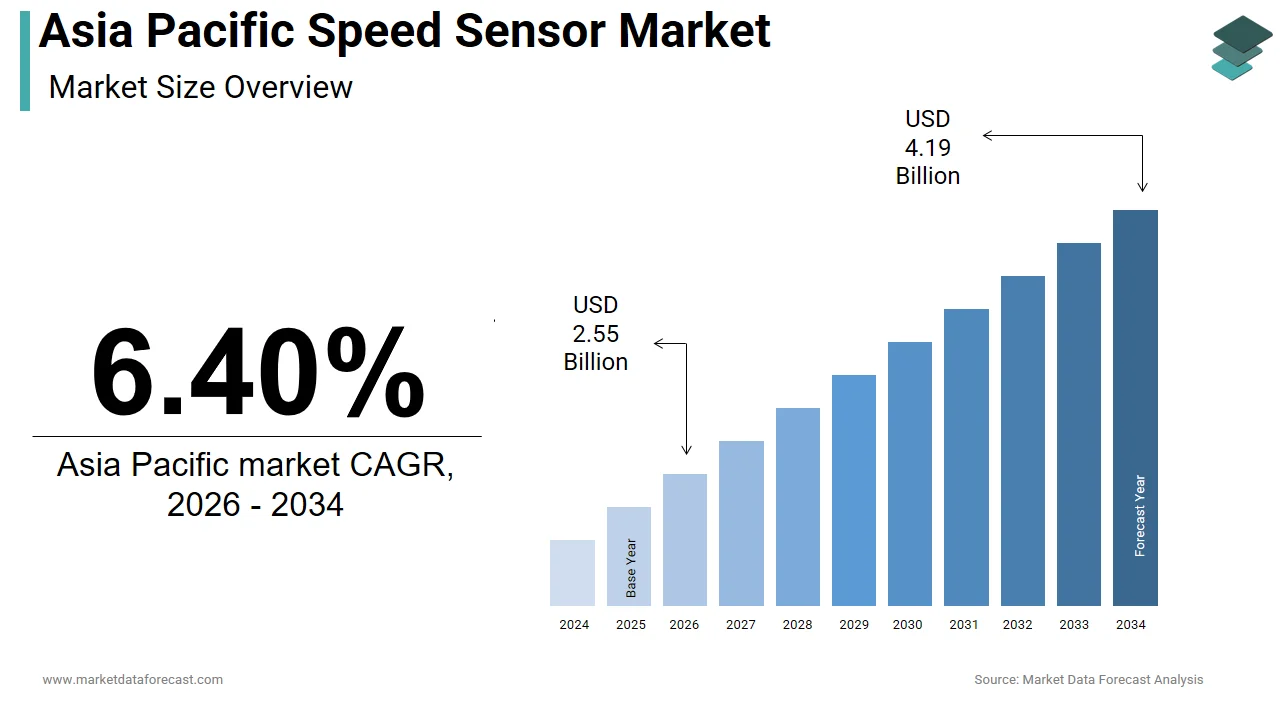

The Asia Pacific speed sensor market was valued at USD 2.40 billion in 2025, is estimated to reach USD 2.55 billion in 2026, and is projected to reach USD 4.19 billion by 2034, growing at a CAGR of 6.40% from 2026 to 2034.

Speed sensor is a device designed to measure rotational or linear velocity across a wide range of industrial, automotive, and consumer applications. These sensors operate on various principles such as magnetic, optical, and Hall-effect technologies, enabling precise monitoring and control in systems ranging from electric motors to transportation infrastructure. As industries increasingly prioritize automation and real-time data analytics, the demand for accurate and reliable speed sensing mechanisms has surged across the region.

In recent years, rapid urbanization, coupled with advancements in Industry 4.0 technologies, has significantly influenced the adoption of speed sensors in countries like China, Japan, India, and South Korea. This expansion underscores the growing reliance on precision components such as speed sensors in manufacturing ecosystems.

Moreover, government initiatives aimed at enhancing energy efficiency and promoting smart mobility solutions have further stimulated the integration of speed sensors in transportation and renewable energy sectors.

MARKET DRIVERS

Expansion of Industrial Automation Across Key Manufacturing Hubs

The rapid expansion of industrial automation across major manufacturing economies is one of the primary drivers fueling the growth of the Asia Pacific speed sensor market. Countries such as China, India, and South Korea are witnessing a significant shift towards automated production lines to enhance efficiency, reduce labor dependency, and improve product consistency. As per the Ministry of Industry and Information Technology of China, the country’s industrial robotics density reached 322 robots per 10,000 employees in 2023, up from just 97 in 2015. This exponential growth highlights the increasing need for precision components like speed sensors to monitor motor speeds, conveyor belts, and robotic arms in real time. Speed sensors play a crucial role in ensuring seamless operation within programmable logic controllers (PLCs) and supervisory control and data acquisition (SCADA) systems, which are integral to modern factories. Moreover, the Indian government’s "Make in India" initiative has spurred investments in automation infrastructure, leading to increased deployment of smart sensors.

Surge in Electric Vehicle Production and Adoption

The accelerating adoption of electric vehicles (EVs) across the Asia Pacific region serves as another critical driver for the speed sensor market. Speed sensors are indispensable components in EVs, used primarily for monitoring wheel rotation, motor performance, and regenerative braking systems. With governments across the region implementing stringent emission norms and offering subsidies to promote green mobility, EV sales have witnessed unprecedented growth.

According to the International Energy Agency, EV sales in China reached over 9 million units in 2023, accounting for nearly 60% of global EV sales. Similarly, India recorded a 46% year-on-year increase in EV sales during the same period, driven by policy support under the Faster Adoption and Manufacturing of Electric Vehicles (FAME II) scheme. In Japan and South Korea, hybrid and battery electric vehicle penetration continues to rise steadily, with companies like Toyota and Hyundai investing heavily in next-generation electric drivetrains.

Each EV typically integrates multiple speed sensors to ensure optimal performance and safety. For instance, a typical electric car may feature four wheel-speed sensors and an additional motor speed sensor. As per BloombergNEF, EV penetration in Southeast Asia is expected to grow fivefold by 2030, further amplifying demand for speed sensors in automotive applications. This trend is not limited to passenger vehicles; it also extends to e-bikes, commercial EVs, and autonomous delivery platforms, all of which rely on accurate speed measurements.

MARKET RESTRAINTS

Supply Chain Disruptions Due to Geopolitical Tensions and Component Shortages

The ongoing volatility in global supply chains, particularly due to geopolitical tensions and semiconductor shortages, is a significant restraint impacting the Asia Pacific speed sensor market. Speed sensors often incorporate microcontroller units (MCUs), analog-to-digital converters, and other electronic components that are sourced from a limited number of global suppliers. Since 2020, the semiconductor industry has faced persistent bottlenecks, exacerbated by trade restrictions between major powers and logistical disruptions caused by regional conflicts.

In Asia, where countries like Malaysia, South Korea, and Japan serve as key manufacturing hubs, delays in component availability have led to production slowdowns. For example, in early 2023, Japan's Renesas Electronics reported lead times extending beyond 52 weeks for certain automotive-grade chips used in sensor modules. This scarcity has forced manufacturers to either delay product launches or raise prices, thereby dampening market growth.

Besides, the U.S.-China tech rivalry has resulted in export controls affecting dual-use electronics, many of which are embedded in advanced speed sensors. Companies operating in sensitive sectors such as defense and aerospace face heightened scrutiny, limiting their ability to procure cutting-edge sensor technologies. As per the World Semiconductor Trade Statistics organization, Asia Pacific accounts for over 60% of global semiconductor consumption, making the region especially vulnerable to supply chain instability.

High Cost of Advanced Speed Sensing Technologies

The relatively high cost associated with advanced sensing technologies is another notable challenge impeding the widespread adoption of speed sensors in the Asia Pacific region. While basic Hall-effect and magnetic sensors remain affordable, high-precision optical and MEMS-based speed sensors used in aerospace, defense, and high-end industrial automation come with significantly higher price tags. This financial barrier restricts their adoption among small and medium enterprises (SMEs), which constitute a substantial portion of the manufacturing base in countries like India, Indonesia, and Vietnam.

According to the Asian Development Bank, SMEs contribute approximately 45% of GDP in developing Asia and employ over 60% of the workforce. However, these businesses often lack the capital to invest in expensive sensor technologies, preferring lower-cost alternatives that may compromise on accuracy and durability. Moreover, maintenance and calibration costs add to the overall expenditure. Precision sensors require regular recalibration to maintain performance standards, which involves specialized equipment and trained personnel.

MARKET OPPORTUNITIES

Integration of Speed Sensors in Renewable Energy Systems

The integration of these devices into renewable energy systems, particularly wind turbines and solar tracking mechanisms, is a promising opportunity emerging in the Asia Pacific speed sensor market. As governments across the region intensify efforts to transition toward clean energy sources, the deployment of wind and solar farms has accelerated dramatically. Speed sensors play a vital role in optimizing energy generation by measuring rotor speeds, blade rotations, and sun-tracking movements with high precision.

According to the International Renewable Energy Agency (IRENA), installed wind power capacity in Asia reached 380 GW in 2023, with China alone contributing over 300 GW. Each utility-scale wind turbine requires multiple speed sensors to monitor generator RPM, yaw movement, and blade pitch adjustments. For example, a typical horizontal-axis wind turbine utilizes at least three speed sensors one for each blade and one for the generator shaft to ensure optimal alignment and prevent mechanical wear.

Similarly, in solar power applications, dual-axis solar trackers use speed sensors to adjust panel orientation throughout the day for maximum sunlight exposure. As per the Solar Energy Industries Association reports that solar tracking systems can boost energy output by up to 30%, making them increasingly popular in large-scale photovoltaic farms across Australia, India, and Southeast Asia.

Growth of Smart Cities and Intelligent Transportation Systems

The development of smart cities and intelligent transportation systems (ITS) across the Asia Pacific presents a compelling opportunity for the speed sensor market. Governments in the region are investing heavily in urban digitization, traffic management, and public transport optimization, all of which rely on real-time data collection and processing. Speed sensors form a foundational element in ITS architectures, providing essential input for adaptive traffic signals, congestion monitoring, and autonomous vehicle navigation.

India’s Smart Cities Mission, launched in 2015, covers 100 urban centers and includes provisions for intelligent transport infrastructure. In addition, Japan’s Society 5.0 framework emphasizes seamless human-machine interaction in urban environments, driving demand for sensor-enabled infrastructure.

MARKET CHALLENGES

Technological Obsolescence Due to Rapid Innovation Cycles

The risk of technological obsolescence driven by rapid innovation cycles is one of the foremost challenges facing the Asia Pacific speed sensor market. The sensor industry is characterized by continuous advancements in materials, design, and integration capabilities, rendering older models obsolete within short periods. Manufacturers must frequently upgrade their product portfolios to align with evolving industry standards, which can strain R&D budgets and create uncertainty for end-users.

For instance, the emergence of wireless speed sensing technologies and AI-integrated sensor nodes is reshaping traditional application landscapes. Traditional wired Hall-effect sensors are being replaced by contactless variants that offer greater reliability and ease of installation. This shift poses a challenge for legacy manufacturers who may struggle to keep pace with new entrants leveraging cutting-edge technologies.

Furthermore, the convergence of IoT and edge computing is enabling predictive maintenance systems that rely on real-time sensor data analysis. These systems demand high-frequency sampling and low-latency communication, capabilities that many existing speed sensors lack. As per Deloitte Insights, nearly 60% of industrial firms in Asia Pacific plan to replace outdated sensor infrastructure by 2026 to support digital transformation goals.

Regulatory Complexity and Compliance Requirements

Navigating the complex regulatory landscape across different Asia Pacific countries represents another significant challenge for speed sensor manufacturers. Each nation has its own set of technical standards, certification protocols, and environmental regulations governing sensor usage in industrial, automotive, and consumer applications. These varying requirements complicate product development and market entry strategies, especially for multinational firms seeking to scale operations across the region.

For example, China mandates compliance with GB/T standards for electrical and electronic products, while Japan enforces JIS standards that differ in testing methodologies and performance criteria. Non-compliance with these frameworks can result in delays, penalties, or restricted market access. According to the World Trade Organization, regulatory barriers account for nearly 20% of trade-related disputes in the electronics sector, underscoring the importance of harmonized compliance practices.

Further, environmental directives such as RoHS and REACH impose restrictions on hazardous substances used in sensor manufacturing. As per the European Environment Agency, similar regulations are being adopted across several Asia Pacific economies, requiring manufacturers to reformulate materials and redesign production processes. Compliance with these standards increases operational costs and complicates supply chain logistics.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | SICK AG, Petasense, Allegro MicroSystems, Inc., Robert Bosch GmbH, NXP Semiconductors N.V., Infineon Technologies AG, Sensoronix, Inc., TE Connectivity, Inc., SPECTEC, and Sensor Solutions Corporation. |

SEGMENTAL ANALYSIS

By Type Insights

The Hall Effect sensors segment represented the largest type in the Asia Pacific speed sensor market by accounting for 42.1% of total revenue share in 2024. Their widespread adoption across automotive, industrial automation, and consumer electronics sectors due to their cost-effectiveness, reliability, and ease of integration with digital systems is driving the dominance of Hall Effect sensors segment. Its extensive use in automotive applications, particularly in electric vehicles (EVs) and anti-lock braking systems (ABS) is also a key driver behind the growth of this segment. In addition, over 9 million EVs were sold in China during 2023, each requiring multiple Hall Effect sensors for motor control and rotational speed monitoring. Moreover, these sensors are integral to industrial motors and robotics, where they provide real-time feedback for precise motion control.

The Magneto Resistive (MR) sensors segment is projected to register the fastest growth in the Asia Pacific speed sensor market, with a CAGR of 9.8% between 2025 and 2033. Their superior sensitivity, ability to operate at high speeds, and compatibility with harsh environments make them ideal for advanced applications in aerospace, defense, and high-performance automotive systems. The increasing adoption of MR sensors in autonomous and semi-autonomous vehicles is another major factor driving this growth. These sensors offer higher accuracy in detecting minute changes in rotational speed, which is critical for adaptive cruise control and lane-keeping assist systems. According to McKinsey & Company, Level 2+ autonomous vehicle sales in Asia are expected to surpass 5 million units annually by 2027, necessitating more sophisticated sensing technologies. Furthermore, the aerospace sector in Japan and South Korea has been investing heavily in next-generation aircraft equipped with MR-based flight control systems.

By Application Insights

The automotive sector led the Asia Pacific speed sensor market by contributing 45.5% of total revenues in 2024. Rising production and adoption of both conventional and electric vehicles across the region, especially in China, India, and Japan, is one of the main reasons behind the growth ofthe automotive sector.

China remains the epicenter of automotive manufacturing and EV adoption globally. According to the International Energy Agency, China accounted for nearly 60% of global EV sales in 2023, with over 9 million units sold domestically. Each vehicle typically integrates multiple speed sensors, wheel speed sensors for ABS, transmission sensors for gear shifting, and motor speed sensors for EVs ,making them indispensable components.

India, too, has seen a surge in automotive sensor demand due to government initiatives such as FAME II and PLI schemes. As per the Society of Indian Automobile Manufacturers, passenger vehicle production in India crossed 3.2 million units in FY 2023–24, with an increasing proportion being electrified variants. Besides, Japanese automakers like Toyota and Honda continue to expand hybrid and fuel-cell vehicle lines, further boosting sensor integration.

The industrial application segment is anticipated to grow at the highest CAGR of 9.2% in the Asia Pacific speed sensor market over the forecast period. Expanding footprint of smart manufacturing, process automation, and predictive maintenance systems across key economies is attributed to the rise of the industrial application segment.

Industrial speed sensors are crucial for monitoring motor speeds, conveyor belt operations, and robotic arm movements within manufacturing plants. As part of Industry 4.0 initiatives, companies are increasingly deploying programmable logic controllers (PLCs) and condition monitoring systems that rely heavily on real-time speed data.

South Korea stands out as a leader in industrial IoT adoption. Similarly, India's "Make in India" campaign has spurred investments in automated production facilities.

COUNTRY LEVEL ANALYSIS

China Speed Sensor Market Insights

China led the Asia Pacific speed sensor industry by contributing 35.2% of total regional revenue in 2024. As the world’s largest automotive and electronics manufacturing hub, China’s robust industrial ecosystem drives substantial demand for speed sensors across automotive, industrial automation, and renewable energy sectors.

The country leads in electric vehicle (EV) production, with over 9 million units sold in 2023 alone, according to the International Energy Agency. Each EV contains multiple speed sensors for motor control, wheel rotation, and regenerative braking. Apart from these, China's renewable energy infrastructure is expanding rapidly, with installed wind power capacity exceeding 300 GW as per the Chinese Wind Energy Association. Speed sensors play a vital role in wind turbines for rotor and generator speed monitoring.

Moreover, China’s push toward smart manufacturing under its Made in China 2025 initiative has resulted in increased adoption of industrial automation.

Japan Speed Sensor Market Insights

Japan is known for its advanced automotive engineering and high-tech manufacturing base and remains a key player in sensor technology development and deployment. Japanese automakers such as Toyota, Honda, and Mazda have been early adopters of advanced speed sensing systems, integrating them into hybrid and electric vehicles. Beyond automotive, Japan’s aerospace and robotics industries are significant contributors to speed sensor demand. The Japan Aerospace Exploration Agency (JAXA) utilizes high-precision MR and optical speed sensors in aircraft propulsion systems. Given Japan’s focus on innovation and high-value manufacturing, it continues to be a pivotal market for advanced speed sensor technologies.

India Speed Sensor Market Insights

India is emerging as a key growth engine driven by government-led industrialization and automotive electrification programs. The country’s expanding manufacturing base, coupled with rising EV adoption, is fueling demand for speed sensing technologies.

With each EV requiring four wheel-speed sensors and one motor speed sensor, this trend significantly boosts component demand. The industrial sector is also witnessing a shift towards smart factories and predictive maintenance, supported by the National Mission on Interdisciplinary Cyber-Physical Systems. With increasing urbanization and infrastructure modernization, India is well-positioned to become a dominant force in the regional speed sensor market.

South Korea Speed Sensor Market Insights

South Korea is leveraging its strong presence in automotive, semiconductor, and robotics industries. The country’s commitment to digital transformation and high-tech manufacturing has made it a key adopter of precision sensing technologies. South Korea is a major exporter of electric vehicles and hybrid models, with companies like Hyundai and Kia leading the charge. These vehicles integrate multiple speed sensors for battery management, motor control, and ABS systems. In addition, South Korea leads in industrial automation. These systems rely on real-time speed data for optimizing production line efficiency. The country is also investing heavily in autonomous mobility and aerospace R&D.

Australia Speed Sensor Market Insights

Australia captures a notable share of the Asia Pacific speed sensor market, driven by its expanding renewable energy infrastructure, mining automation, and intelligent transportation systems. While not a mass manufacturing economy, Australia’s focus on resource efficiency and smart mobility positions it as a growing market for high-performance speed sensors. The country is a leading producer of minerals and metals, with automation playing a key role in improving operational efficiency. In the renewable energy sector, as per the Clean Energy Council, Australia added over 3 GW of wind and solar capacity in 2023, bringing total renewable generation to 35% of electricity supply. Wind turbines and solar tracking systems require precise speed measurement mechanisms to optimize energy output. Moreover, Australia’s Intelligent Transport System (ITS) program is expanding, with state governments investing in smart highways and traffic monitoring networks. These developments are fostering steady growth in speed sensor adoption across the country.

COMPETITIVE LANDSCAPE

The Asia Pacific speed sensor market is characterized by a highly fragmented yet dynamic competitive landscape, where both global giants and regional players coexist. The market features a mix of established multinational corporations and emerging domestic manufacturers striving to capture market share through technological advancements and strategic positioning. As industries across the region increasingly adopt automation, electrification, and smart infrastructure, the demand for precision speed sensing solutions has intensified competition among vendors. Companies are differentiating themselves by offering customized sensor modules tailored for specific applications in automotive, industrial, and aerospace sectors. Innovation remains a key battleground, with firms investing heavily in R&D to develop next-generation sensors that offer superior performance, compact form factors, and compatibility with digital ecosystems. Apart from these, vertical integration and localized production have become essential strategies to mitigate supply chain risks and improve cost efficiency. While large players leverage their brand strength and global reach, smaller firms focus on niche applications and agile product development cycles to stay relevant. This blend of competition fosters continuous evolution in product offerings and market dynamics, ensuring sustained growth and technological progress in the Asia Pacific speed sensor space.

KEY MARKET PLAYERS

Some of the noteworthy companies in the Asia Pacific speed sensor market profiled in this report are

- SICK AG

- Petasense

- Allegro MicroSystems, Inc.

- Robert Bosch GmbH

- NXP Semiconductors N.V.

- Infineon Technologies AG

- Sensoronix, Inc.

- TE Connectivity, Inc.

- SPECTEC

- Sensor Solutions Corporation

TOP LEADING PLAYERS IN THE MARKET

One of the leading players in the Asia Pacific speed sensor market is TE Connectivity, a global technology company with a strong presence in sensor manufacturing. The company offers a wide range of speed sensing solutions tailored for automotive, industrial, and aerospace applications. In the Asia Pacific region, TE Connectivity has strategically expanded its local production facilities and R&D centers to cater to the growing demand for high-performance sensors. Their focus on innovation and customer-specific design has enabled them to maintain a competitive edge. Besides, their partnerships with major automotive OEMs have strengthened their foothold in the market.

Another key player is Bosch Sensortec, a subsidiary of Robert Bosch GmbH, known for its cutting-edge micro-electromechanical systems (MEMS) and precision sensor technologies. Bosch Sensortec plays a crucial role in supplying speed and motion sensing components for consumer electronics, electric vehicles, and smart mobility platforms across the Asia Pacific. With a strong emphasis on miniaturization and energy efficiency, the company has been instrumental in enabling next-generation mobility and automation solutions. Their continuous investment in R&D and regional collaborations with tech startups has further reinforced their market position.

Allegro MicroSystems is another dominant force in the Asia Pacific speed sensor market, particularly recognized for its expertise in Hall Effect and magnetic sensor technologies. The company provides reliable and durable speed sensing solutions that are widely adopted in automotive and industrial applications throughout the region. Allegro’s commitment to developing robust, application-specific integrated circuits has made it a preferred partner among system integrators and OEMs. Their localized engineering support teams ensure timely product customization and technical assistance, enhancing their competitiveness. Through strategic acquisitions and long-term supplier relationships, Allegro continues to expand its influence in the regional market.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the primary strategies employed by key players in the Asia Pacific speed sensor market is product innovation and differentiation. Companies are continuously investing in research and development to introduce advanced sensor technologies that offer higher accuracy, durability, and integration capabilities. This includes the development of MEMS-based and wireless speed sensors tailored for emerging applications such as autonomous vehicles and smart factories.

Another significant strategy is strategic partnerships and collaborations. Leading firms are forging alliances with automotive manufacturers, industrial automation providers, and technology startups to enhance their product offerings and accelerate time-to-market. These collaborations help companies align with evolving industry standards and gain access to new customer segments across diverse sectors.

Lastly, regional expansion and localization play a crucial role in strengthening market presence. Major players are expanding their manufacturing units, distribution networks, and technical support centers within Asia Pacific to meet rising demand and reduce supply chain dependencies. Establishing localized operations enables faster response times and better alignment with regional regulatory requirements.

RECENT MARKET DEVELOPMENTS

- In February 2024, TE Connectivity launched a new line of high-precision magnetic speed sensors designed specifically for electric vehicle drivetrains. The product introduction aimed at addressing the increasing need for accurate motor speed monitoring in next-generation EVs, reinforcing the company’s leadership in the automotive sensor segment.

- In June 2024, Bosch Sensortec announced a partnership with a leading Chinese autonomous vehicle startup to integrate its advanced motion and speed sensing technologies into self-driving platforms. This collaboration was intended to enhance real-time navigation and safety features, supporting broader adoption of autonomous mobility solutions in the Asia Pacific region.

- In September 2024, Allegro MicroSystems expanded its regional presence by opening a dedicated application engineering center in South Korea. The facility was designed to provide localized technical support and customization services to automotive and industrial customers, improving responsiveness and strengthening client relationships.

- In November 2024, Murata Manufacturing acquired a Japanese sensor design firm specializing in wireless sensing solutions. This move was aimed at accelerating Murata’s development of IoT-enabled speed sensors for industrial automation and predictive maintenance applications across Asia.

- In January 2025, Infineon Technologies, though not traditionally a dominant player in the Asia Pacific speed sensor market, entered a joint venture with a Singaporean semiconductor firm to co-develop next-generation optical speed sensors for high-end robotics and aerospace applications, signaling increased competition in the premium sensor segment.

MARKET SEGMENTATION

This Asia Pacific speed sensor market research report is segmented and sub-segmented into the following categories.

By Type

- Hall effect

- Magneto resistive

- Variable reluctance

- Others

By Application

- Automotive

- Industrial

- Aerospace & defense

- Consumer electronics

- Others

By Country

- India

- China

- Japan

- South Korea

- Rest Of APAC

Frequently Asked Questions

1. What factors are driving the growth of the speed sensor market in Asia Pacific?

Growth is fueled by expanding automotive production, rising adoption of smart and IoT-enabled devices, increased consumer electronics manufacturing, and growing industrial automation across the region

2. Which countries are the leading contributors to the speed sensor market in Asia Pacific?

China, Japan, South Korea, and India are key markets, propelled by government incentives, local manufacturing boosts, and strong automotive and electronics sectors

3. What are the main end-user industries for speed sensors in Asia Pacific?

Primary end-users are automotive, consumer electronics, industrial automation, aerospace, military, biomedical, and healthcare sectors

4. Which types of speed sensors are most commonly used in Asia Pacific?

Popular types include Hall effect sensors, magneto-resistive sensors, variable reluctance sensors, engine speed sensors, wheel (vehicle) speed sensors, linear speed sensors, and photoelectric speed sensors

5. How does the vehicle speed sensor market perform in Asia Pacific?

Asia Pacific is the fastest-growing region for vehicle speed sensors, aided by automotive industry expansion and the implementation of stricter safety regulations in countries like China and India

6. How is the consumer electronics sector influencing the speed sensor market in Asia Pacific?

Rising smart gadget adoption and manufacturing competitiveness, combined with government support for local production in countries like India and Japan, are driving speed sensor demand in consumer electronics

7. What role does industrial IoT play in the Asia Pacific speed sensor market?

The adoption of IoT and industry 4.0 technologies increases the installation of smart sensors for monitoring, data analytics, and process automation throughout industrial sectors

8. How are government policies impacting the market?

Government initiatives, such as production-linked incentives, manufacturing relocation subsidies, and industrial policy support, are helping expand speed sensor manufacturing capacity and stimulate market growth in Asia Pacific

9. What are the latest trends in speed sensor technology for Asia Pacific?

Key trends include integration of smart and wireless sensors, IoT-compatibility, miniaturization, higher accuracy, and increased deployment in electric and autonomous vehicles

10. Who are the major players in the Asia Pacific speed sensor market?

The market features global sensor manufacturers and strong regional players, though individual company names are not specified in the cited reports

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com