Canada Food Service Market Research Report Segmented By Place Type (Full Service Restaurants, Quick Service Restaurants, Food Junctions Cafeterias/Buffets, Bars And Managed Food Service), End-User (Industrial Premises, Commercial And Office Premises, Hospital & Nursing Homes, Educational Premises, In-Transit Food Service, And Sports Centers/Malls), And Region – Industry Size, Growth, Share, Trends, Demand And Forecast Analysis Report 2026 To 2034

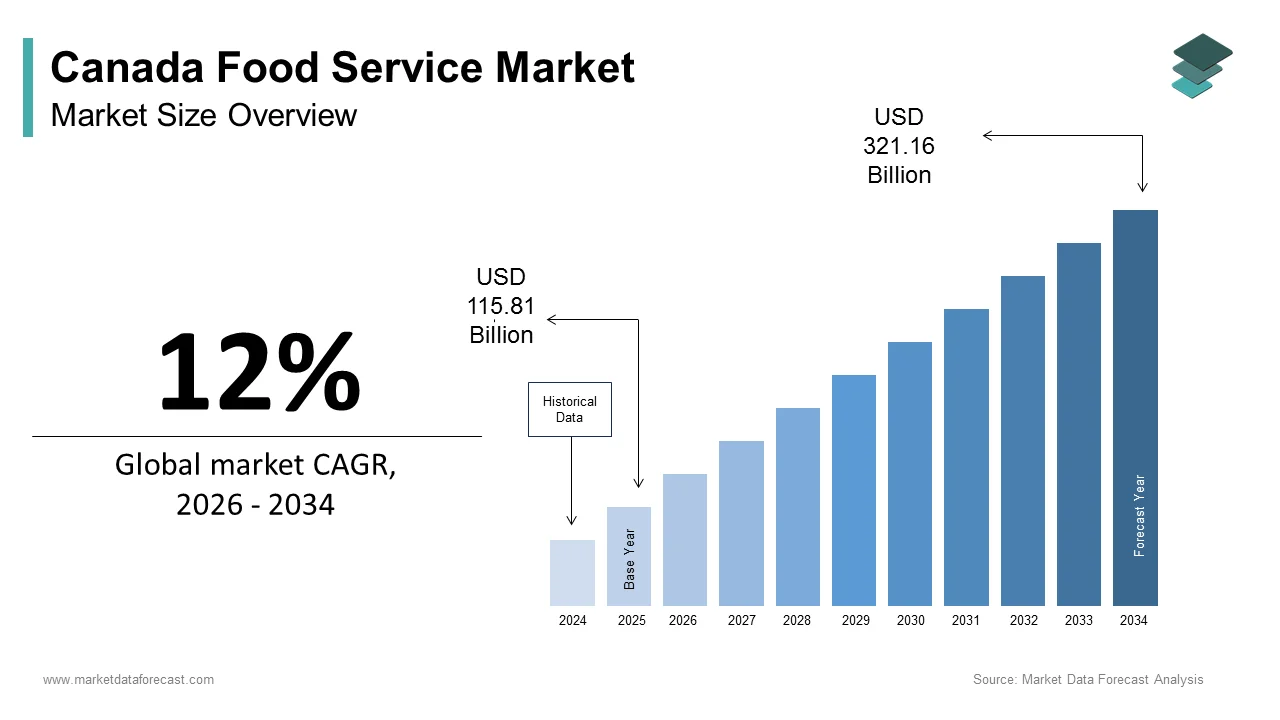

Market Size, 2025

$115.81 BnMarket Estimate, 2026

$129.71 BnMarket Forecast, 2034

$321.16 BnCAGR, 2026–2034

12%Executive Summary: Canada Food Service Market

- Market Scope: Comprehensive Canada food service market analysis covering place types, end-user sectors, regional leadership frameworks, key industry players, and emerging digital delivery and health-conscious menu trends.

- Market Valuation: Valued at USD 115.81 billion (2025), estimated at USD 129.71 billion (2026), and projected to reach USD 321.16 billion by 2034, registering a robust CAGR of 12% (2026–2034).

- Primary Growth Drivers: Rising consumer spending on dining out, expansion of quick-service restaurants, increasing demand for convenience foods, rapid adoption of online food delivery platforms, diverse cuisine preferences, and health-conscious trends promoting organic and plant-based options.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Place Type | Quick Service Restaurants (QSR) segment (leads market via affordability and urban presence) | Full-Service Restaurants (resurgence via dine-in experiences) and digital delivery platforms |

| By End-User | Commercial and Office Premises segment (holds significant share fueled by foot traffic and corporate dining) | In-Transit Food Service segment (growing notably due to travel and tourism revival) |

| By Region | Major Canadian metropolitan areas (urbanization and busy lifestyles driving ready-to-eat demand) | Suburban and digital delivery corridors across Canadian provinces |

Major Market Players & Market Structure

Market Structure: Highly competitive Canadian food service and restaurant landscape featuring major global and domestic enterprises competing on digital ordering automation, product innovation, supply chain resilience, and social responsibility initiatives.

Key Companies: KFC, Tim Hortons Inc., Pizza Hut, McDonald's Corp, Burger King Corporation, Starbucks Corporation, Ardent Mills, and DoorDash Canada.

Canada Food Service Market Size

The size of the Canadian foodservice market was calculated to be USD 115.81 billion in 2025 and is anticipated to be worth USD 321.16 billion by 2034, from USD 129.71 billion in 2026, growing at a CAGR of 12% during the forecast period.

The Canadian food service market is steadily growing. Previously, in 2023, the actual industry revenue (i.e. sales adjusted for inflation) has been stable compared to 2022. All areas have registered an increase, excluding Manitoba. Also, the cloud kitchen service is witnessing a significant rise, propelled by an increase in online food delivery, surging interest in world cuisine and the adoption of modern ordering systems. In the post-pandemic period, nearly 50 per cent of customers are ordering food via online platforms each week, with AI technology improving kitchen activities and enabling customised suggestions to consumers. Moreover, Canadian people aged 40 or less are progressively selecting to eat out or order food online. However, these customers are more budget-conscious than elderly people and are intended to decrease costs and alcohol consumption.

MARKET DRIVERS

The CCanadianfood service market is mainly driven by the increasing frequency of restaurant meals, busy lifestyles and the growing influence of intercultural food models, due to the strong presence of international companies.

Moreover, the rising popularity of plant-based protein substitutes also propels market growth as more customers are adopting healthy consumption habits. Sandwiches and burgers have become the favoured alternatives for instant foods or snacks.

Apart from this, sustainable development and organic ingredients are witnessing rapid adoption in the Canadian food service industry. And, more customers want meals that align with their values and diet plan. Hence, restaurants are offering organic items, domestically sourced raw materials and vegetarian substitutes.

In addition, demographic changes, as well as the rise in the number of health-conscious millennials and baby boomers, have resulted in higher demand for food services. Both quick-service and full-service restaurants feature prominently in all food services in the country. Millennial populations across the country are key contributors to the expansion of Canada food service market. Like, McDonald’s and Starbucks Corporation are among the major brands that are progressing with innovative menus and improving their portfolios to establish themselves in this lucrative market.

MARKET RESTRAINTS

The Canadian foodservice market growth is restricted by inflated costs and profit pressure.

The majority of restaurants and other industry players are bearly making any profits despite increased prices than ever coupled with overall spending on course i.e. 110 billion in 2023. This is a 10 per cent surge in comparison to 2022’s level. However, costs rose considerably which is taking several to insolvency. As per industry experts, the market growth rate decreased substantially because all the things required for functioning a restaurant have risen double digits. Also, in 2023, the first five months saw bankruptcies in the industry went up by 50 per cent against the same period the previous year and there are expectations of further rise in the future.

MARKET OPPORTUNITIES

The Canadian foodservice market exhibits potential opportunities owing to shifting customer tastes, behaviour and emerging patterns.

With an increased focus on sustainability, there's a growing need for environmentally friendly practices, domestically procured ingredients and a transparent supply network, giving openings for companies to differentiate themselves. In addition, the rising application of technology, like online ordering platforms with AI and more customized options, fast delivery apps and mobile services, presents avenues to improve consumer experience and gain a wider audience.

MARKET CHALLENGES

Labour scarcity and workforce problems in the Canadian foodservice market are major hindrances.

The market encounters obstacles in hiring and retaining skilled employees. With demographic shifts, labour shortages have become a pressing challenge, especially in kitchens and hospitality jobs. Factors like low salaries, high sales rates, and tough work environment add to this constraint. Further, COVID-19 worsened these issues, causing workforce interruptions and affecting activities and service quality throughout several establishments.

This research report on the Canadian food service market is segmented and sub-segmented into the following categories.

Canada Food Service Market By Place Type

- Full-Service Restaurants

- Quick Service Restaurants

- Food Junctions Cafeterias/buffets

- Bars

- Managed Food Services

The quick-service restaurant segment is leading under this category of the Canadian foodservice market. This can be attributed to the fast-moving lifestyle in urban cities, customer preferences for comfort and speedy eating choices and cheaper meal options. As per the April 2023 study, it was found that these have finally risen from a post-pandemic cloud. In addition, the extensive presence of QSR chains, effective business models, and the ease of drive-thru and takeaway facilities further strengthen their market share. Besides this, customers progressively prefer this segment because of its emphasis on healthier raw materials, personalised menu offerings, and generally a more calm eating atmosphere compared to those of traditional fast-food joints.

On the other hand, the full-service restaurants generated revenue of 3.4 billion dollars in April 2023 and slightly more in the case of limited-service restaurants with 3.5 billion dollars. Consumers shifted to limited service during economic downturns or times of instability to save money. Also, the other factor was approachability, considering that limited-service food places were in an advantageous position to satisfy people during the lockdowns than full-service restaurants. Additionally, Canada’s wish for full-service eating is coming back. Segment’s revenues at these restaurants surpassed limited-service dining turnover each month last summer and majorly in December 2022.

Canada Food Service Market By End-User

- Industrial Premises

- Commercial and Office Premises

- Hospital & Nursing Homes

- Educational Premises (Colleges, Universities, Schools)

- In-transit Food Service (Airlines, Trains)

- Sports Centers/Malls

The commercial and office premises segment gained the first position and is expected to drive at a steady pace during the forecast period for the Canadian food service market. In addition, under the commercial segment, the quick-service restaurants earned the maximum revenue of 40838.3 million dollars in 2023, full-service at second place with 39715.1 million dollars, caterers at third with 6717.5 million dollars and drinking places at fourth with 2516 million dollars.

Also, the standalone restaurants in the in-transit food services segment grew notably in 2023. This progress is credited to the revival of travel and tourism operations as limitations were removed post-COVID-19. With a surging number of consumers travelling for relaxation, business, or other reasons, there's a succeeding growth in demand for dining choices in the conveyance hubs, railway stations, roads, highways and airports.

Additionally, the real sales rise in 2023 was highest in retail food service at 4 per cent against inflation-adjusted sales in the pre-pandemic period followed by institutional food services at 1 per cent. Moreover, the industry of retail food service non-commercial restaurants is propelling with an emphasis on convenience and delivering high-quality food in a non-traditional dining atmosphere.

COUNTRY ANALYSIS

The Canadian food service market is moderately moving upwards due to the dire effects of COVID-19 then escalating costs, labour shortages and high interest rates in the post-pandemic which remain the key challenges in 2025. However, the country’s market share increased because of the growing quick-service restaurants and online food platforms. Moreover, with the transition to off-premise eating, higher menu costs, distant work and persistent problems regarding going out on public transport, there continues to be a long way ahead for recovery for several food service segments. Apart from this, the prominent category in the Candia food service market includes flavour extracts, cocktail mixes, syrups, simple fruit juices, baking, pizza, and dough mixes. Another area in which the industry depends on imported products is red meat from the United States, which represents 71 per cent of imports in the category. Also, 87 per cent of Canadian imports are controlled by the United States in terms of poultry meat. Although Brazilian producers can supply frozen products at lower prices than the United States, some Canadian factories are reluctant to source poultry from Brazil, as the mix of products of American and Brazilian origin could prohibit the sale of processed products.

KEY MARKET PLAYERS

Major players in the Canadianfoodservicee market are KFC, Tim Hortons Inc., Pizza Hut, McDonald's Corp, Burger King Corporation, and Starbucks Corporation.

RECENT HAPPENINGS IN THE MARKET

- In June 2025, Ardent Mills, the first flour-milling and ingredient company, press released its latest unique product in Canada called Ardent Mills Egg Replace. It designed this affordable solution to assist in reducing supply chain problems.

- In May 2025, McDonald’s in Canada introduced its Grimace Shake at participating eateries for a limited duration.

- In May 2025, DoorDash Canada reported the introduction of Made by Women, a new platform committed to championing women restauranteurs and chefs, expanding their voices and contributions.

Frequently Asked Questions

1. What factors are driving the growth of the Canada food service market?

Key drivers include rising consumer spending on dining out, growing urbanization, expansion of food delivery platforms, and increasing demand for diverse cuisines.

2. What are the major segments in the Canada food service market?

Major segments include quick-service restaurants, full-service restaurants, cafés, street food vendors, catering services, and institutional food services.

3. Which segment dominates the market?

Quick-service restaurants and casual dining establishments hold a large share due to their affordability and convenience.

4. Which factors influence consumer dining habits in Canada?

Consumer preferences are influenced by busy lifestyles, multicultural cuisine options, digital ordering platforms, and demand for healthier menu options.

5. How is food delivery influencing the market?

Online food delivery services are growing rapidly, with many Canadians ordering meals through mobile apps and delivery platforms.

6. What role does technology play in the food service industry?

Technology such as mobile ordering, digital payment systems, and restaurant management software is improving efficiency and customer convenience.

7. What are the major distribution channels in the food service market?

Food services are delivered through dine-in restaurants, takeaway outlets, food trucks, catering services, and online delivery platforms.

8. What challenges affect the Canada food service market?

Challenges include rising labor costs, food inflation, supply chain disruptions, and increasing competition among restaurant chains.

9. How is consumer demand for healthy food affecting the market?

Restaurants are expanding menus to include plant-based meals, organic foods, and low-calorie options to attract health-conscious consumers.

10. What are the future trends in the Canada food service market?

Future trends include growth of cloud kitchens, digital ordering platforms, plant-based menus, and expansion of food delivery services.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com