Global Contact Lenses Market Size, Share, Trends and Growth Forecast Report Segmented By Material (Soft, Silicone Hydrogel, Rigid Gas Permeable (RGP), Hybrid and Polymethyl Methacrylate (PMMA)), Application (Therapeutic, Cosmetic, Corrective and Prosthetic), Design, Modality, Distribution Channel and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) – Industry Analysis From 2025 to 2033

Global Contact Lenses Market Summary

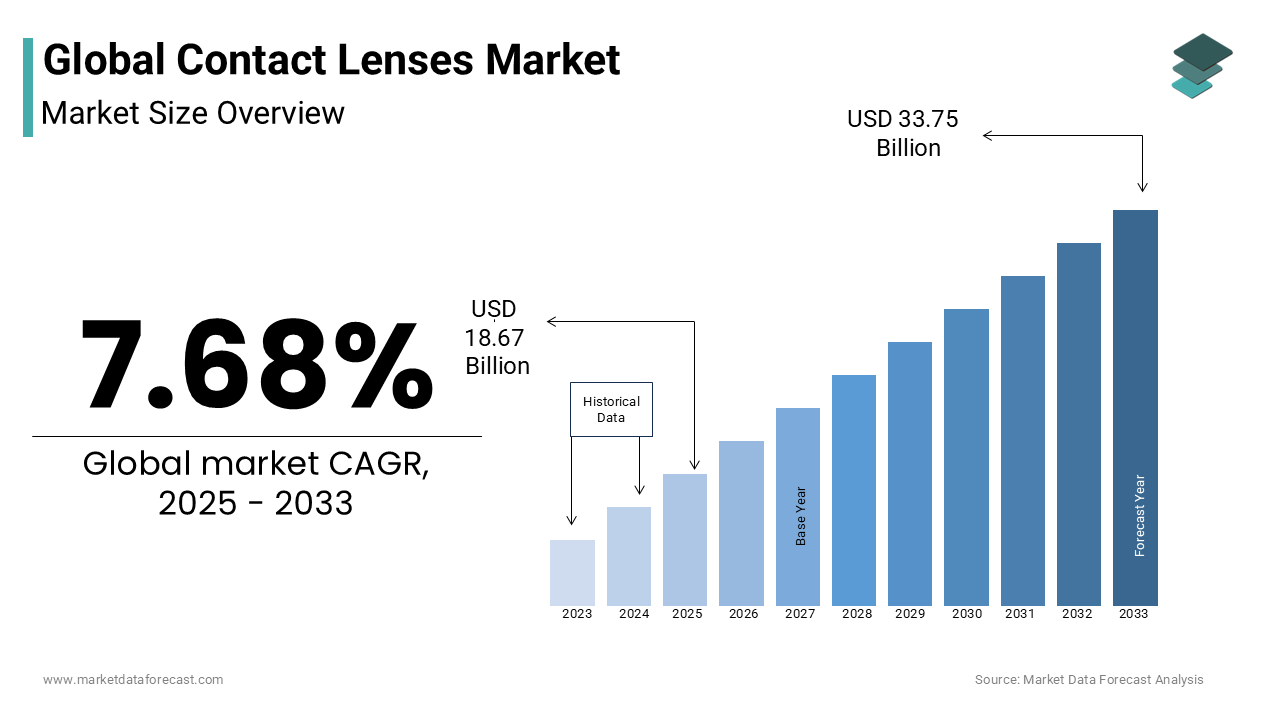

The global contact lenses market was valued at USD 17.34 billion in 2024, is projected to reach USD 18.67 billion in 2025, and is expected to expand to USD 33.75 billion by 2033, growing at a CAGR of 7.68% from 2025 to 2033. The growth of the global contact lenses market is driven by rising cases of refractive errors, increasing adoption of corrective and cosmetic lenses, and growing preference for disposable and advanced lens types for convenience and eye health. Technological advancements in lens materials and designs, along with expanding distribution channels, further support market expansion.

Key Market Trends

- The rising popularity of soft contact lenses for comfort and ease of use.

- Strong demand for corrective lenses addressing myopia, hyperopia, and astigmatism.

- The growing use of spherical lenses as the most common design type.

- Increasing adoption of disposable lenses due to hygiene and convenience benefits.

- Expansion of distribution networks through hospitals, spectacle stores, and online retail.

Segmental Insights

- Based on material, the soft contact lenses segment is expected to hold the highest share during the forecast period, supported by high comfort and affordability.

- Based on application, the corrective contact lenses segment dominated the market in 2024, reflecting widespread use for vision correction.

- Based on design, the spherical lens segment is anticipated to occupy the largest share during the forecast period, owing to its common application for basic refractive errors.

- Based on modality, the disposable segment is projected to record the highest CAGR, supported by consumer preference for hygiene and convenience.

- Based on distribution channel, the eye hospitals and spectacle stores segment accounted for the largest share in 2024, reflecting their key role in prescription and purchase.

Regional Insights

- North America dominated the global contact lenses market in 2024 and is expected to retain the largest share throughout the forecast period, driven by high adoption of premium lenses, advanced eye care infrastructure, and growing demand for cosmetic and corrective solutions.

- Europe shows steady growth, supported by increasing awareness of eye health and rising preference for advanced disposable lenses.

- Asia-Pacific is expected to grow rapidly, fueled by a large patient pool with refractive errors, rising disposable incomes, and expanding retail penetration.

- Latin America and the Middle East & Africa are emerging markets, supported by growing urbanization, rising vision correction needs, and expanding optical retail networks.

Competitive Landscape

Key players in the global contact lenses market include Johnson & Johnson, Bausch & Lomb, CooperVision, Hydrogel Vision Corp., Abbott Medical Optics Inc., Alcon Laboratories Inc., Carl Zeiss AG, CIBA Vision, Essilor International, and Contamac. These companies are focusing on product innovation, advanced lens materials, and expansion of digital and retail distribution channels to strengthen their global presence.

Global Contact Lenses Market Size

The global contact lenses market was valued at USD 17.34 billion in 2024. The global contact lenses market is expected to reach USD 33.75 billion by 2033 from USD 18.67 billion in 2025, growing at a compound annual growth rate (CAGR) of 7.68% during the forecast period.

Contact lenses are medical-grade optical aids that are manufactured from advanced hydrogel and silicone hydrogel materials that facilitate oxygen permeability, comfort, and extended wear capability. Unlike traditional eyeglasses, contact lenses offer enhanced peripheral vision, reduced optical distortion, and aesthetic appeal, making them a preferred choice for millions seeking unobtrusive vision correction. This escalating demand is further amplified by growing awareness of eye health, advancements in lens technology, and increasing access to optometric services. Innovations such as daily disposables, multifocal designs, and smart lenses embedded with sensors are redefining user experience. Regulatory frameworks administered by bodies like the U.S. Food and Drug Administration and the European Medicines Agency ensure stringent quality control

MARKET DRIVERS

Surge in Digital Device Usage Accelerates Demand for Vision Correction Solutions

The exponential increase in screen time across personal, professional, and educational domains is driving the growth of contact lenses market. As per the World Health Organization, the global population spends an average of seven hours daily on digital devices, with adolescents and working professionals in urban Asia Pacific logging over nine hours, contributing to heightened visual fatigue and refractive errors. This phenomenon, often termed digital eye strain, has led to earlier onset of vision correction needs, particularly among millennials and Generation Z. In response, ophthalmic manufacturers are prioritizing lens designs that reduce glare, enhance moisture retention, and support prolonged wear under artificial lighting. Daily disposable lenses, which minimize protein buildup and infection risk, now account for over 60% of contact lens sales in countries like Japan and Australia, as reported by the Australian Optometric Association.

Growing Preference for Aesthetic and Lifestyle-Oriented Vision Correction

Contact lenses are increasingly chosen not only for functional vision correction but also for their role in enhancing personal appearance and supporting active lifestyles. According to a consumer behavior survey by Euromonitor International, 68% of contact lens users in South Korea and India cited appearance enhancement as a primary reason for switching from glasses, particularly among young adults engaged in social media, entertainment, and fitness industries. Similarly, athletes and outdoor enthusiasts favor contacts for unrestricted peripheral vision and stability during movement. The rise of sports optometry programs in Australia and Germany further validates this trend. Moreover, advancements in silicone hydrogel materials have extended safe wear duration by enabling continuous use during long commutes, travel, and shift-based work.

MARKET RESTRAINTS

High Risk of Ocular Complications Due to Improper Use and Hygiene Practices

The elevated incidence of eye infections and corneal complications associated with improper lens handling and extended wear is restricting the growth of contact lenses market. As per the U.S. Centers for Disease Control and Prevention, an estimated one million eye care visits annually in the United States are linked to contact lens-related adverse events, including microbial keratitis, corneal ulcers, and contact lens-induced acute red eye (CLARE). A 2023 multicenter ophthalmic study published by the British Journal of Ophthalmology revealed that over 80% of soft contact lens wearers in urban India and Southeast Asia engage in at least one unsafe practice, such as overnight wear of non-extended-use lenses, using tap water for cleaning, or exceeding replacement schedules. In China, a survey conducted by the Chinese Ophthalmological Society found that only 34% of users adhere strictly to hygiene guidelines, contributing to a rising burden of fungal and bacterial keratitis cases in tertiary eye hospitals. Additionally, silicone hydrogel lenses, while promoting oxygen transmission, can accumulate lipid deposits if not properly maintained, reducing comfort and increasing irritation.

Stringent Regulatory Requirements and Lengthy Product Approval Processes

The development and commercialization of contact lenses are constrained by rigorous regulatory scrutiny from agencies such as the U.S. Food and Drug Administration, the European Medicines Agency, and Japan’s Pharmaceuticals and Medical Devices Agency, which mandate extensive clinical testing and biocompatibility assessments. According to the International Council of Ophthalmology, the average time required to bring a new contact lens material or design to market exceeds 36 months, significantly delaying innovation cycles and increasing R&D costs. In the European Union, compliance with the Medical Device Regulation (MDR) introduced in 2021 has intensified documentation, post-market surveillance, and conformity assessment requirements, leading to a 40% increase in approval timelines as reported by MedTech Europe. Manufacturers must demonstrate not only optical efficacy but also long-term safety, cytotoxicity, and resistance to microbial adhesion, necessitating costly in vitro and in vivo trials. In India, the Central Drugs Standard Control Organization mandates local clinical studies for imported lens brands, creating barriers for global players seeking rapid market entry.

MARKET OPPORTUNITIES

Integration of Smart Lens Technology Opens New Frontiers in Health Monitoring and Vision Enhancement

The emergence of smart contact lenses embedded with microelectronics, biosensors, and wireless connectivity is escalating the growth of contact lenses market. These advanced lenses are being developed to monitor intraocular pressure in glaucoma patients, detect glucose levels in tears for diabetes management, and enhance visual focus through adaptive optics. As per a clinical trial conducted by the University of California, San Diego in 2023, a prototype smart lens demonstrated 92% accuracy in correlating tear glucose with blood glucose levels, offering a non-invasive alternative to finger-prick testing. In South Korea, Samsung Electronics and Seoul National University Hospital have jointly tested a contact lens with an integrated pressure sensor capable of transmitting real-time data to mobile devices, potentially revolutionizing chronic eye disease management. Additionally, defense and augmented reality sectors are exploring autofocus-enabled lenses to improve situational awareness.

Expansion of E-Commerce and Tele-Optometry Services Enhances Market Accessibility

The rapid growth of digital platforms and remote eye care services is likely to elevate the growth of the contact lenses market. Companies like Vision Direct and Feel Good Contacts have optimized user experiences with virtual try-ons, prescription renewals, and AI-driven fitting suggestions, increasing convenience and reducing purchase friction. A 2022 study by the Royal Australian and New Zealand College of Ophthalmologists found that telehealth consultations increased access to vision care by 38% in remote communities.

MARKET CHALLENGES

Intensifying Competition from Refractive Surgery Limiting Long-Term Market Growth

The contact lenses market faces growing pressure from the rising adoption of refractive surgical procedures such as LASIK, SMILE, and PRK, which offer permanent vision correction and eliminate the need for daily lens wear. A 2023 survey by Moorfields Eye Hospital in London found that 52% of contact lens users considered surgery due to discomfort, dryness, or lifestyle limitations. Additionally, increasing insurance coverage and financing options in countries like Germany and Australia have made surgery more accessible. In India, private eye clinics report a 30% year-on-year increase in LASIK consultations, driven by urban professionals seeking long-term solutions. While contact lenses remain essential for presbyopia and irregular corneas, their position as a primary corrective tool is being challenged among individuals with stable myopia.

Shortage of Trained Eye Care Professionals in Emerging Markets Hinders Safe Adoption

The acute shortage of qualified optometrists, ophthalmologists, and dispensing professionals necessary for safe fitting, prescription, and follow-up care is restricting the growth of contact lenses market. As per the World Health Organization, Sub-Saharan Africa has fewer than 2 eye care practitioners per 100,000 people, while Southeast Asia averages only 3.7, far below the recommended 5 per 100,000 for adequate service delivery. In rural India, over 70% of vision correction needs remain unaddressed due to lack of access, according to the National Programme for Control of Blindness and Visual Impairment. This gap leads to self-prescribing, improper lens selection, and reliance on unregulated vendors selling non-FDA-approved cosmetic lenses, increasing risks of corneal damage and infection. A 2022 study published in the Indian Journal of Ophthalmology revealed that 41% of contact lens wearers in tier-2 and tier-3 cities obtained lenses without a valid prescription. Even in urban centers, optometric training programs are limited; Indonesia produces fewer than 500 certified optometrists annually despite a population exceeding 270 million, as reported by the Ministry of Health.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Material, Application, Design, Modality, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East, and Africa |

| Key Market Players | Johnson & Johnson, Bausch & Lomb, Cooper Vision, Hydrogel Vision Corp, Abbott Medical Optics, Inc., Alcon Laboratories, Inc., Carl Zeiss AG, CIBA Vision, Essilor International, and Contamac. |

SEGMENTAL ANALYSIS

By Material Insights

The soft segment held a dominant share of the global contact lenses market in 2024 with their high wearer comfort, ease of adaptation, and widespread availability across both corrective and cosmetic applications. Their popularity is further reinforced by low maintenance requirements and compatibility with modern digital lifestyles, where prolonged screen exposure demands lenses with superior moisture retention. Additionally, mass production capabilities have reduced costs, making them affordable for younger demographics. Retail expansion through e-commerce platforms like Vision Direct and Boots has enhanced accessibility, particularly in urban India and Southeast Asia.

The silicone hydrogel segment is likely to grow with an expected CAGR of 9.4% from 2025 to 2033 with the material’s superior oxygen permeability, which allows up to six times more oxygen to reach the cornea compared to traditional hydrogel lenses, significantly reducing the risk of hypoxia-related complications. These lenses are especially preferred for continuous and overnight wear, with FDA-approved variants such as Air Optix Night & Day and PureVision enabling safe usage for up to 30 nights. Additionally, their durability and resistance to protein deposition enhance user compliance and reduce replacement frequency. Clinical trials by Moorfields Eye Hospital confirmed that daily wear of silicone hydrogel lenses reduces corneal swelling by 78% compared to conventional materials.

By Application Insights

The corrective application segment was accounted in holding a significant share of global contact lenses market in 2024 with the escalating global prevalence of refractive errors such as myopia, hyperopia, astigmatism, and presbyopia, which collectively affect over 150 million people who rely on vision correction devices. The increasing onset of presbyopia among aging populations further amplifies demand, with the U.S. Census Bureau projecting that over 1.4 billion adults globally will require reading correction by 2030.

Cosmetic Lenses Register the Fastest Growth at 10.2% CAGR Fueled by Aesthetic and Cultural Trends

The cosmetic contact lenses segment is estimated to grow with an expected CAGR of 10.2% during the forecast period with the rising consumer emphasis on personal appearance, social media influence, and cultural acceptance of non-corrective eye enhancements. In South Korea, the epicenter of beauty innovation, over 20 million cosmetic lenses were sold in 2023 alone, as reported by the Korean Ophthalmological Society, with popular styles including enlargement (circle lenses) and gradient tints. E-commerce platforms such as YesStyle and AliExpress have amplified accessibility, offering thousands of designs with global shipping.

By Design Insights

The spherical contact lenses segment was the largest and held 62.1% of global contact lenses market share in 2024 with their primary function in correcting simple refractive errors such as myopia and hyperopia, which affect a vast proportion of the global population. As per the World Health Organization, uncorrected myopia alone impacts over 2 billion people worldwide, with prevalence rates exceeding 80% among young adults in urban East Asia. Additionally, major manufacturers such as Alcon, Johnson & Johnson Vision, and Bausch + Lomb offer extensive portfolios of spherical lenses with enhanced moisture retention and UV protection, catering to digital device users.

The orthokeratology (ortho-k) contact lenses segment is estimated to grow with a CAGR of 11.6% from 2025 to 2033 with the increasing demand for non-surgical myopia management, particularly among children and adolescents experiencing rapid progression of nearsightedness. Ortho-k lenses are rigid gas permeable devices worn overnight to temporarily reshape the cornea, providing clear vision during the day without corrective aids. Countries like Singapore, South Korea, and Japan have also integrated ortho-k into national school vision programs due to its proven efficacy.

By Modality Insights

The disposable segment was the largest and held a significant share of the global contact lenses market in 2024 with the superior hygiene, ease of use, and alignment with modern consumer preferences for low-maintenance health products. In Western Europe, over 65% of contact lens users now opt for daily disposables, as reported by the European Contact Lens Society, with high adoption in countries like Germany and the United Kingdom due to robust optometric guidance and insurance coverage. The convenience factor is further amplified by subscription-based home delivery models offered by companies such as Boots Opticians and Vision Direct, ensuring consistent supply and adherence. A 2022 patient compliance study conducted by the University of Waterloo found that daily disposable users demonstrated 92% adherence to recommended wear schedules, compared to only 58% among conventional lens users. Additionally, advancements in manufacturing have reduced production costs, making disposables increasingly affordable.

The daily disposable segment is likely to register a CAGR of 10.8% from 2025 to 2033 with the unparalleled convenience, enhanced eye health outcomes, and strong endorsement from eye care professionals. Daily disposables are designed for single-day use and immediate disposal, eliminating protein buildup, allergen accumulation, and user error in cleaning routines. As per a clinical trial published in the journal *Eye & Contact Lens*, patients wearing daily disposables reported 37% fewer dryness symptoms and 52% lower incidence of inflammatory events compared to bi-weekly or monthly lens users. Pediatric and first-time wearers are increasingly prescribed dailies due to simplified handling and reduced infection risk.

By Distribution Channel Insights

The Spectacle stores segment was the largest and held 54.3% of the contact lenses market share in 2024 with their strategic role as frontline providers of comprehensive vision care, combining optometric services, prescription validation, and immediate product availability under one roof. In countries such as the United Kingdom, Germany, and Australia, chains like Specsavers, Fielmann, and OPSM operate vertically integrated models where trained optometrists conduct eye exams on-site and directly recommend and dispense contact lenses, ensuring medical oversight and regulatory compliance. Additionally, they offer bundled services such as free eye tests, loyalty programs, and trial packs, which encourage first-time adoption.

The online distribution channel is projected to grow with an expected CAGR of 12.3% in the coming years with rising internet penetration, seamless e-commerce platforms, and the proliferation of subscription-based delivery services that ensure uninterrupted supply. Consumers increasingly favor online channels for their time efficiency, price transparency, and access to a broader range of products, including niche and international brands not available in local stores. The integration of tele-optometry has further strengthened legitimacy; in Canada, digital refraction services approved by provincial optometry boards now allow licensed practitioners to renew prescriptions remotely, enabling compliant online purchases. Additionally, cross-border e-commerce enables access in regions with limited physical optical infrastructure, particularly in Southeast Asia and Latin America.

REGIONAL ANALYSIS

North America Contact Lenses Market Insights

North America was accounted in holding 36.4% of the contact lenses market share in 2024 with high per capita eye care spending, advanced optometric infrastructure, and widespread insurance coverage for vision correction. Regular eye examinations are standard practice, with over 70% of adults undergoing annual vision screenings, which is facilitating early prescription and consistent product adoption. Major manufacturers such as Johnson & Johnson Vision, Alcon, and Bausch + Lomb are headquartered in the U.S., driving innovation in daily disposables, silicone hydrogel materials, and digital integration. Retail optical chains like LensCrafters and online platforms including 1-800 Contacts have streamlined access through subscription models and tele-optometry services. Additionally, lifestyle factors such as participation in sports and preference for aesthetic freedom without glasses reinforce consumer demand.

Europe Contact Lenses Market Insights

Europe contact lenses market was positioned second with well-established network of independent opticians, hospital-affiliated eye clinics, and national health systems that support routine vision care. Countries such as Germany, the United Kingdom, France, and the Netherlands exhibit high contact lens penetration, with over 30% of young adults using them regularly, as per a 2023 survey by the Royal College of Ophthalmologists. Daily disposable lenses now represent more than 60% of soft lens sales across Western Europe, driven by public health messaging on hygiene and infection prevention. The European Union’s Medical Device Regulation has strengthened post-market surveillance and biocompatibility requirements, enhancing consumer confidence in product safety. In Scandinavia, where digital screen usage exceeds seven hours daily, manufacturers have introduced blue light-filtering lenses tailored to Nordic lifestyles. Additionally, premium segments such as orthokeratology and multifocal designs are gaining traction due to aging populations and rising presbyopia rates.

Asia-Pacific Contact Lenses Market Insights

Asia Pacific contact lenses market is propelled by an unprecedented rise in myopia, particularly in urban centers, where educational intensity and prolonged near-work activities have led to some of the highest refractive error rates globally. As per the Singapore Eye Research Institute, over 80% of teenagers in Singapore, South Korea, and parts of China are myopic by the end of secondary school, creating a vast and growing user base for corrective lenses. E-commerce platforms such as Lenskart, Lazada, and Tmall have significantly enhanced distribution, offering home delivery and digital refraction tools. In China, over 40 million people currently use contact lenses, a figure projected to double by 2030 according to the Chinese Ophthalmological Society.

Latin America Contact Lenses Market Insights

Latin America contact lenses market growth is likely to grow steadily in coming years. Brazil, Mexico, and Argentina are the primary contributors, where urbanization, rising middle-class incomes, and expanding private healthcare networks are driving demand for vision correction beyond traditional eyeglasses. The preference for aesthetic enhancement is particularly strong among younger demographics, with cosmetic lenses gaining popularity in fashion and entertainment sectors. Retail optical chains such as Óticas Carol and Luxottica-operated stores are expanding in major cities, improving availability and professional oversight. Additionally, e-commerce is emerging as a disruptive force, with Mercado Libre and Dafiti offering contact lenses alongside telehealth consultations.

Middle East and Africa Contact Lenses Market Insights

The Middle East and Africa contact lenses market is to have significant growth opportunities during the forecast period. The United Arab Emirates, Saudi Arabia, and Qatar lead the region, where government investments in healthcare modernization and medical tourism have elevated access to advanced ophthalmic services. High disposable incomes and cultural emphasis on appearance drive preference for daily disposables and cosmetic variants among female consumers. However, pilot programs by NGOs such as Sightsavers and the International Centre for Eye Health are expanding school-based vision screening, identifying unmet needs. Egypt and South Africa show stronger market activity, with local retailers like Optical House and national chains promoting affordable lens options. Rising smartphone usage is also enabling tele-optometry pilots in Kenya and Rwanda. While overall penetration remains low, the combination of Gulf-led innovation and grassroots initiatives in public health positions the region for incremental growth, particularly as awareness of non-surgical vision correction increases across urban populations

COMPETETIVE LANDSAPE

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global contact lenses market include

-

Johnson & Johnson

-

Bausch & Lomb

-

Cooper Vision

-

Hydrogel Vision Corp

-

Abbott Medical Optics, Inc.

-

Alcon Laboratories, Inc.

-

Carl Zeiss AG

-

CIBA Vision

-

Essilor International

-

Contamac

Companies such as Johnson & Johnson, Novartis, The Cooper Companies, and Bausch & Lomb occupy most global contact lenses market shares. The key market participants focus on bettering their brand value and customer base to acquire the best possible market share and joining long-term associations with the suppliers and distributors to increase their sustainability and strengthen their regional presence.

Top Players

Johnson & Johnson Vision maintains a strong presence in the Asia Pacific contact lenses market through its pioneering ACUVUE brand which offers a comprehensive portfolio of daily disposables silicone hydrogel and multifocal lenses. The company has invested heavily in clinical research tailored to Asian eye shapes and tear film characteristics ensuring optimal fit and comfort for regional users. In 2023 it launched ACUVUE OASYS with Transitions in Japan and Australia providing adaptive lenses that darken in sunlight addressing digital eye strain and UV exposure. It also expanded partnerships with optical chains and e commerce platforms such as Lenskart and Taobao to enhance last mile delivery.

Alcon operates as a leading force in the Asia Pacific contact lenses landscape by delivering advanced ophthalmic solutions under brands like DAILIES TOTAL1 and AIR OPTIX. The company emphasizes high oxygen permeability and extended wear comfort aligning with the region’s rising demand for premium silicone hydrogel lenses. Alcon has strengthened its regional footprint through localized manufacturing in Singapore and distribution agreements with major retailers including Specsavers and OPSM. In 2022 it introduced myopia management programs in collaboration with pediatric eye clinics in South Korea and Malaysia focusing on youth vision health. Its investment in digital engagement tools such as online fitting guides and telehealth integration has improved accessibility.

CooperVision has established significant influence in the Asia Pacific market through its focus on specialty lenses including toric designs for astigmatism and Biofinity for extended wear. The company has tailored its product development to meet the unique visual needs of Asian populations including flatter corneal curvatures and higher rates of dry eye. In 2023 CooperVision launched MyDay Toric in Thailand and Taiwan enhancing options for patients with complex prescriptions. It deepened collaborations with university eye clinics in Australia and Japan to conduct real world performance studies. The company also partnered with regional e commerce leaders such as Shopee and Flipkart to expand direct to consumer reach. Through scientific workshops and training programs for eye care professionals CooperVision promotes evidence based prescribing practices.

Major Strategies

Product Innovation Focused on Comfort and Ocular Health

Leading companies in the contact lenses market are prioritizing material science advancements to enhance wearer comfort and corneal well-being. Manufacturers are investing in silicone hydrogel formulations with improved moisture retention and oxygen transmissibility to reduce dryness and hypoxia-related complications. Innovations such as embedded blue light filters, UV protection, and antimicrobial surface treatments are being integrated into daily disposables to align with digital lifestyle demands. Customized lens geometries for Asian corneal profiles have improved fit and stability. Clinical collaborations ensure evidence-based design while regulatory compliance maintains safety standards. These innovations not only extend wear time but also strengthen brand trust and patient adherence across diverse global markets.

Expansion of Digital Engagement and E-Commerce Integration

Key players are leveraging digital platforms to enhance customer reach and streamline access to contact lenses. Companies have partnered with online retailers and developed proprietary e-commerce portals offering subscription models home delivery and automated prescription renewals. Tele-optometry integrations allow licensed professionals to validate prescriptions remotely increasing compliance. Mobile applications provide fitting guidance usage tracking and personalized recommendations. Social media campaigns and influencer collaborations target younger demographics promoting lifestyle benefits. Data analytics enable targeted marketing and inventory optimization.

Strategic Partnerships with Eye Care Professionals and Institutions

Market leaders actively collaborate with optometrists ophthalmologists and academic institutions to reinforce clinical credibility and drive adoption. Sponsorship of continuing education programs scientific conferences and research trials strengthens relationships with eye care providers who influence prescription decisions. Joint initiatives on myopia management and ocular health awareness position brands as medical partners rather than mere suppliers. Training on proper fitting and aftercare ensures safe use and reduces complication rates. Partnerships with university clinics facilitate real world performance testing of new products. These alliances not only enhance product legitimacy but also create trusted channels for patient education ensuring long term engagement and adherence within professional eye care ecosystems across both developed and emerging regions.

RECENT MARKET DEVELOPMENTS

- In October 2023, Alcon launched the TOTAL30 multifocal lenses for patients with presbyopia. The lenses will be distributed in the U.S. and in some international markets.

- In March 2023, Cooper Companies Inc. launched its Cooper Vision My Day Energy lenses in the U.S. market. The lenses are for people with symptoms of pervasive digital eye strain.

- In June 2023, Bausch and Lomb combined launched multifocal silicone hydrogel lenses, Bausch and Lomb Infuse, in the U.S. market. This daily disposable lens provides a clear vision for patients with presbyopia.

- In February 2023, Alcon launched a new total toric lens for astigmatic patients. This launch expands the company's daily disposable and reusable lens portfolio with high-performing options designed especially for astigmatic patients.

- In April 2022, Alcon launched Precision, Canada's disposable contact lens for astigmatism. The daily disposable silicone hydrogel contact lenses are designed for myopic patients, continuing Alcon's mission to help people's vision.

- In June 2022, Johnson & Johnson Vision, a part of Johnson & Johnson MedTech, received FDA clearance for its latest contact lens innovation, Acuvue Oasys Maz 1-Day, and Acuvue Oasys Max 1-Day Multifocal.

- In 2022, Cooper Companies Inc. invested USD 110.30 million in research and development activities compared to USD 92.70 million in 2021. These activities mainly focus on manufacturing technology, lens development, and process enhancements.

MARKET SEGMENTATION

This research report on the global contact lenses market has been segmented & sub-segmented based on the material, application, design, modality, distribution channel, and region.

By Material

- Soft Contact Lenses

- Silicone Hydrogel Lenses

- Rigid Gas Permeable (RGP) Contact Lenses

- Hybrid Contact Lenses

- Polymethyl Methacrylate (PMMA) Contact Lenses

By Application

- Therapeutic

- Cosmetic

- Corrective

- Prosthetic

By Design

- Spherical

- Bifocal

- Orthokeratology

- Toric

By Modality

- Conventional

- Disposable

- Daily

- Monthly

- Other Disposable Modalities

By Distribution Channel

- Eye Hospitals and Spectacle stores

- Online

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

Which region accounted for the largest share in the global contact lenses market in 2024?

The North American region dominated the market in 2024 and is expected to hold the largest share of the global contact lenses market during the forecast period.

Which country led the global contact lenses market in 2024?

The U.S. accounted for the largest share of the global market in 2024 and occupied over 25%.

Which are the significant players operating in the contact lenses market?

Johnson & Johnson, Bausch & Lomb, Cooper Vision, Hydrogel Vision Corp, Abbott Medical Optics, Inc., Alcon Laboratories, Inc., Carl Zeiss AG, CIBA Vision, Essilor International, and Contamac are some of the notable companies in the contact lenses market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com