Europe Acetone Market Size, Share, Trends and Growth Forecasts Research Report, Segmented By Application, End-use and Country – Industry Analysis (2026 to 2034)

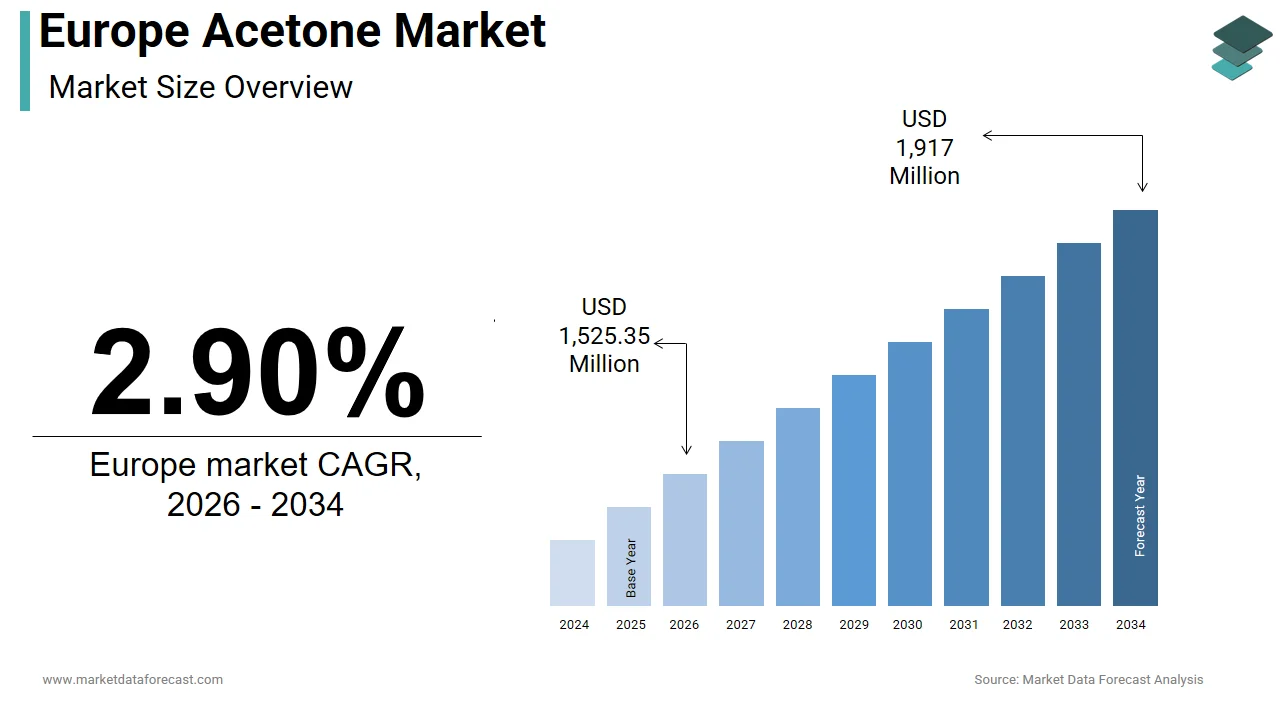

Market Size, 2025

$1,482.36 MnMarket Estimate, 2026

$1,525.35 MnMarket Forecast, 2034

$1,917 MnCAGR, 2026–2034

2.90%Europe Acetone Market Summary

The size of the Europe acetone market was worth USD 1,482.36 million in 2025. The regional market is anticipated to grow at a CAGR of 2.90% from 2026 to 2034 and be worth USD 1,917 million by 2034 from USD 1,525.35 million in 2026.

The Europe acetone market was valued at USD 1,482.36 million in 2025, is estimated to reach USD 1,525.35 million in 2026, and is projected to be worth USD 1,917 million by 2034, expanding at a CAGR of 2.90% from 2026 to 2034. Market growth is driven by strong demand from the polymethyl methacrylate (PMMA) industry, bisphenol A (BPA) production, coatings & adhesives manufacturing, and pharmaceutical synthesis, alongside the increasing role of acetone in battery materials processing and circular bio-chemistry initiatives across Europe.

Key Insights

- Regulatory & Industrial Ecosystem: Acetone in Europe is primarily produced as a co-product of phenol via the cumene process and is registered under REACH at volumes exceeding 1 million tonnes per annum. Production clusters remain concentrated in Germany, France, Belgium, and the Netherlands, operating under strict environmental governance frameworks such as the Industrial Emissions Directive (IED) and Best Available Techniques (BAT), which mandate VOC emission controls, vapor recovery systems, and solvent recycling infrastructure at large-scale facilities.

- Market Segmentation: In 2025, the Bisphenol A (BPA) application segment accounted for the largest market share, supported by sustained demand in polycarbonate resins, epoxy coatings, wind energy composites, and infrastructure corrosion protection systems. By end-use, the paints & coatings segment led the market due to acetone’s fast evaporation rate, solvency strength, and compatibility with hybrid & water-reducible coating technologies, while the pharmaceutical segment is expected to register the fastest growth driven by API manufacturing, crystallization processes, and advanced therapy production.

- Key Growth Drivers: Growth is supported by rising PMMA consumption in automotive lightweighting, construction glazing, and medical devices, expansion of pharmaceutical and fine chemical production capacity, increasing adoption of bio-based acetone through fermentative processes, and emerging demand from lithium-ion battery recycling, electrolyte purification, and clean-mobility material ecosystems across Europe.

Challenges:

Market expansion is limited by strict VOC emission controls and compliance costs, supply-demand imbalance arising from acetone’s dependency on phenol production economics, volatility in propylene and benzene feedstock pricing, and regional discrepancies in safety classification, storage thresholds, and handling protocols across EU member states, which complicate cross-border logistics and operational planning.

Major Market Players

Key companies operating in the Europe acetone market include: LyondellBasell Industries Holdings B.V., INEOS Group, Altivia, BASF SE, Royal Dutch Shell Co., Honeywell International Inc., Mitsui & Co., Ltd., SABIC, KUMHO P&B CHEMICALS., INC., Shell Chemicals, Cepsa, Formosa Chemicals & Fibre Corp., Borealis AG, PTT Phenol Company Limited, Prasol Chemicals Pvt. Ltd., Chang Chun Group, and Others.

Europe Acetone Market Size

The size of the Europe acetone market was worth USD 1,482.36 million in 2025. The regional market is anticipated to grow at a CAGR of 2.90% from 2026 to 2034 and be worth USD 1,917 million by 2034 from USD 1,525.35 million in 2026.

Acetone is an organic solvent and chemical intermediate widely utilized in the synthesis of methyl methacrylate, bisphenol A, and pharmaceutical actives across Europe. Its clear colorless nature, high volatility, and miscibility with water underpin its role in coatings, adhesives, and cleaning formulations. Acetone in the European Union is primarily manufactured as a co-product of phenol production via the widely used cumene process. This chemical is registered under the REACH Regulation for manufacture and/or import into the European Economic Area at quantities typically exceeding 1 million tonnes per annum. The production capacity for phenol and acetone is highly concentrated within several key EU member states, including Germany and France, which are the leading overall chemical producers in the EU. The European Commission’s Industrial Emissions Directive (IED) mandates the implementation of Best Available Techniques (BAT) to minimize emissions, including stringent vapor recovery protocols for volatile organic compounds like acetone at large-scale industrial facilities. This regulatory and infrastructural framework defines the operational landscape for acetone in a region prioritizing both chemical efficiency and environmental stewardship.

MARKET DRIVERS

Robust Demand from the Polymethyl Methacrylate and Plastics Manufacturing Sector

Polymethyl methacrylate production remains the single largest consumer of acetone in the region, a factor that drives the growth of the Europe acetone market. This is driven by demand for lightweight, transparent, and weather-resistant materials in automotive construction and medical devices. According to industry analysis, the European market for methyl methacrylate (MMA), the primary raw material for PMMA, was valued at $25.5 billion in 2023. The majority of MMA is polymerized into PMMA, often using the acetone cyanohydrin (ACH) route. The European Automobile Manufacturers Association (ACEA) reported that EU new car sales surged by almost 14% in 2023, while the automotive segment for PMMA is anticipated to experience significant growth due to its use in vehicle components such as lighting, aiming for weight reduction and design flexibility. The construction segment held the largest revenue share in the European MMA landscape in 2023, driven by the use of PMMA extruded sheets in applications like window panels and domes due to their high transparency and UV resistance. Furthermore, regulatory shifts away from polycarbonate in food contact applications have accelerated PMMA substitution. This confluence of industrial design trends, regulatory realignment, and energy policy sustains structural acetone demand beyond cyclical fluctuations.

Expansion of Pharmaceutical and Fine Chemical Synthesis Activities

Acetone serves as an important reaction medium and extraction solvent in the region’s advanced pharmaceutical manufacturing ecosystem, which continues to expand despite global offshoring pressures. This expansion is likely to accelerate the growth of the Europe acetone market. Numerous pharmaceutical manufacturing facilities across the continent utilize specific solvents during the synthesis and purification stages of drug production. A significant portion of global innovative drug approvals originates from the region, indicating a consistent focus on advanced chemical processing. Certain countries maintain a high density of facilities dedicated to producing potent ingredients, employing specialized techniques like crystallization and separation that require precise chemical agents. Strategic policy shifts are emphasizing the relocation of critical intermediate production to domestic sites to decrease dependency on external supply chains. This policy has revived investment in multipurpose fine chemical plants in Switzerland and Ireland. The convergence of health security imperatives, scientific complexity, and solvent performance cements acetone’s role in Europe’s life sciences value chain.

MARKET RESTRAINTS

Stringent Volatile Organic Compound Emission Controls Under EU Air Quality Directives

The European Union’s National Emission Ceilings Directive and Industrial Emissions Directive impose rigorous limits on acetone releases, which restrict the growth of the Europe acetone market. Acetone is a classified volatile organic compound that contributes to the formation of ground-level ozone. Industrial facilities have observed a notable decrease in acetone emissions while preparing for increasingly stringent environmental standards. Adherence to updated emission limits necessitates the implementation of specialized filtration and recovery technologies, which impacts overall facility management costs. Regulatory frameworks in certain regions now emphasize continuous monitoring for sites that utilize significant quantities of the solvent. Smaller processing operations occasionally encounter challenges in modernizing their systems due to the substantial financial investment required for abatement infrastructure. These regulatory requirements, while environmentally necessary, constrain process flexibility and elevate barriers to entry for specialty chemical entrepreneurs reliant on solvent-intensive routes.

Feedstock Price Volatility Linked to Crude Oil and Propylene Markets

Acetone production in the region remains tightly coupled to phenol output through the cumene process, which further hinders the expansion of the Europe acetone market. This makes its economics highly sensitive to propylene and benzene pricing, which in turn tracks crude oil and naphtha benchmarks. Contract prices for propylene experienced significant volatility throughout the annual cycle, resulting in a substantial range between peak and trough values. Producers managing integrated facilities maintained asset utilization at reduced levels due to unfavorable economic spreads between raw materials and finished co-products. Manufacturing output for specific chemical intermediates declined late in the year as a result of diminishing downstream demand for related primary products. Inventory levels for certain derivatives increased as production rates outpaced the market's ability to absorb supply during periods of weakening consumption. Moreover, Russia’s curtailment of naphtha exports following geopolitical sanctions disrupted upstream feedstock chains. This inherent linkage to volatile hydrocarbon markets introduces pricing instability that complicates long term supply agreements and margin planning for downstream formulators.

MARKET OPPORTUNITIES

Growth in Bio-Based Acetone Production Through Fermentative Routes

The region is witnessing a strategic pivot toward renewable acetone derived from lignocellulosic biomass or waste glycerol using engineered microbial strains, offering a pathway to decarbonize solvent supply chains, which is expected to fuel the growth of the Europe acetone market. A number of pilot-scale projects were funded and initiated, with some reaching a level of technical readiness within a few years of their launch. One project successfully demonstrated a continuous fermentation process utilizing specific microbial strains, producing a high-purity product from an agricultural byproduct feedstock at a notable conversion efficiency. A separate facility was re-operationalized, initiating a consistent monthly production of the bio-based chemical, which received certification under a sustainability scheme. The use of this bio-based chemical as a precursor for a type of plastic material was shown to substantially reduce carbon emissions compared to traditional methods. The EU’s Carbon Border Adjustment Mechanism (CBAM) is increasing the urgency to reduce the carbon intensity of chemical products; this growing bio segment offers a viable pathway for aligning acetone production with circular bioeconomy goals and meeting strict customer sustainability demands.

Rising Adoption in Lithium-Ion Battery Recycling and Electrolyte Formulation

The expansion of the region’s electric vehicle ecosystem is creating novel demand channels for high-purity acetone in battery manufacturing and end of life recycling processes. Consequently, this generates fresh prospects for the Europe acetone market expansion. The expansion of battery production capacity across the region indicates a significant requirement for industrial solvents in manufacturing processes. Industry standards have been established that require extremely high purity levels for specific solvents used in preparing battery materials, primarily to prevent contamination. Effective technologies for recovering critical materials from used batteries have been demonstrated to achieve high extraction rates. New regulations are prompting increased investment in material recovery technologies by establishing mandatory minimum recycled content targets for new batteries. This dual role, as both a production enabler and circularity agent, positions acetone at the nexus of Europe’s clean mobility transformation.

MARKET CHALLENGES

Persistent Gap Between Acetone Supply and Regional Self-Sufficiency Targets

The region remains a net importer of acetone due to imbalanced phenol acetone co-production ratios and insufficient standalone plants, despite significant production capacity, which negatively impacts the growth of the Europe acetone market. The European Union was a net exporter of acetone in 2023, exporting a greater quantity than it imported. The main sources for EU imports of acetone included Singapore, Saudi Arabia, and South Africa. The European Commission’s Critical Raw Materials Act indirectly highlights this vulnerability, as acetone is essential for processing strategic materials like rare earth elements. Belgium's Antwerp port is a significant hub for European acetone imports, which originate from a diverse range of global partners. Belgium's acetone imports have shown considerable fluctuation, with import sources shifting notably from year to year. Unlike Asia, Europe lacks propane dehydrogenation linked on purpose acetone facilities, leaving producers unable to adjust output independently of phenol market signals. This structural rigidity impedes supply security and complicates the EU’s ambition to achieve greater chemical autonomy amid geopolitical supply chain realignments.

Inconsistent Classification and Handling Requirements Across Member States

National interpretations of acetone's handling guidelines vary widely, notwithstanding the comprehensive nature of the EU's REACH and CLP regulations, and thereby limit the growth of the Europe acetone market. These differences fragment operational protocols across the single market. Classifications for a common industrial substance vary significantly across different regions, with some jurisdictions using stricter hazard definitions than others. The required safety equipment and storage volume thresholds for facilities handling this substance are not uniform, leading to differing infrastructural requirements based on location. These variations in regional regulations have been associated with an increase in operational costs for entities operating across multiple locations. Emergency planning and hazard modeling requirements under a regional safety directive also lack consistency, as the thresholds triggering comprehensive response plans differ between areas. This regulatory fragmentation undermines efficiency and complicates just-in-time solvent logistics essential for lean manufacturing environments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Application, End-use, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | LyondellBasell Industries Holdings B.V., INEOS Group, Altivia, BASF SE, Royal Dutch Shell Co., Honeywell International Inc., Mitsui & Co., Ltd., SABIC, KUMHO P&B CHEMICALS., INC., Shell Chemicals, Cepsa, Formosa Chemicals & Fibre Corp., Borealis AG, PTT Phenol Company Limited, Prasol Chemicals Pvt. Ltd., Chang Chun Group, and Others. |

SEGMENTAL ANALYSIS

By Application Insights

The Bisphenol A (BPA) segment held the majority share of 42.1% of the Europe acetone market in 2024. The leading position of the BPA segment is attributed to its irreplaceable role in producing polycarbonate plastics and epoxy resins, which are foundational to construction, automotive, and electronics manufacturing. An official scientific body concluded that, with correct handling, the use of a common industrial chemical in resins presents minimal safety concerns, allowing for ongoing large-scale application within the region. One major European nation utilized a substantial quantity of this chemical, primarily in protective linings for water infrastructure and food containers. Furthermore, the expansion of wind energy infrastructure has intensified demand for BPA-based epoxy matrices in turbine blade composites. The production of components for wind energy, especially for coastal installations, consumed a notable volume of the chemical, showing a considerable increase in usage for that application compared to the previous period. This industrial embedding ensures BPA remains the primary acetone sink despite substitution efforts in consumer goods. Epoxy resins derived from BPA are important to Europe’s infrastructure durability and energy transition initiatives. A majority of coatings used for industrial maintenance purposes across Europe incorporate a compound-based epoxy system, valued for its chemical resistance and ability to adhere to surfaces. The primary materials used for installing pipelines intended to carry drinking water in two specific European countries often featured a certified epoxy lining derived from this compound. Furthermore, the aerospace sector relies on these resins for composite bonding. A major manufacturer of civil aircraft incorporates a notable quantity of composites based on this epoxy compound into the primary structures of its narrow-body aircraft models. The overall demand for this compound remains consistently high, driven by consistent production rates within the civil aviation sector. Regulatory bodies have specifically excluded these industrial epoxy uses from broader restrictions on the compound, acknowledging that the substance does not leach once the product has fully hardened. This technical indispensability and regulatory carve-out sustain acetone consumption through the BPA route.

The methyl methacrylate (MMA) segment is predicted to witness the highest CAGR of 6.8% from 2025 to 2033 due to the substitution of traditional glazing materials with lightweight, durable polymethyl methacrylate in energy-efficient building design and electric vehicle integration. A governing body implemented stricter sustainability standards for new public constructions, prompting material selection based on enhanced insulation and light transmission qualities. Moreover, a notable increase in the installation of a specific type of polymer in commercial building projects within a particular region has been recorded. Concurrently, automotive lightweighting targets under the EU’s CO2 fleet standards have boosted PMMA use in panoramic roofs and rear light clusters. A major manufacturer has increased the average quantity of this polymer used in its new vehicle types compared to previous models. These cross-sectoral tailwinds position MMA as the most dynamic acetone derivative. Consumer and regulatory pressure to eliminate BPA from food contact and children’s products has redirected demand toward PMMA as a safe transparent alternative. Regulations regarding a chemical compound in food contact materials have been significantly restricted. This regulatory change has led major packaging manufacturers to switch to an alternative material for reusable containers and medical supply vessels. Production of this alternative material in a specific region has grown considerably, with a substantial majority of the new output manufactured using a particular base ingredient. Furthermore, the EU’s Circular Economy Action Plan incentivizes recyclable mono-material packaging, where PMMA’s homogeneity offers advantages over multilayer polycarbonate alternatives. This convergence of health, safety, sustainability, and performance cements MMA’s high growth trajectory within the acetone value chain.

By End-use Insights

The paints and coatings segment led the Europe acetone market and held a share of 35.6% in 2024. Acetone’s rapid evaporation rate and strong solvency for resins, nitrocellulose, and acrylics make it indispensable in industrial maintenance, automotive refinish, and wood coating formulations. Many European coating operations use specific solvent blends to ensure optimal finish quality and bond strength on metal surfaces. Regional paint manufacturers utilize significant volumes of these solvents to produce high-solids coatings that meet strict environmental standards regarding volatile emissions. Regulatory frameworks favour certain solvents because they do not contribute as significantly to atmospheric chemical reactions compared to other options. Large-scale infrastructure modernization efforts across the continent have increased the need for specialized protective layers on essential transportation and utility systems. There is a growing trend toward using specific chemical-based anti-corrosion treatments to maintain and extend the life of aging industrial assets in various regions. Acetone’s unique physicochemical profile ensures its continued use despite broader solvent substitution trends. Substituting acetone in specific high-performance lacquers remains challenging as alternative solvents often do not replicate its drying characteristics and final finish transparency. Acetone continues to be a preferred agent for cleaning surfaces before coating applications due to its ability to evaporate completely without leaving contaminants. A consistent reliance on acetone-based solutions persists within specialized finishing sectors to ensure optimal adhesion and surface purity. The chemical properties of acetone offer functional advantages in certain coatings that are currently difficult to match with substitute materials. Besides, the shift toward water reducible coatings has paradoxically increased acetone demand as a co-solvent to stabilize hybrid emulsions. Regulatory frameworks recognize this technical necessity. This functional indispensability anchors acetone in Europe’s coatings ecosystem.

The pharmaceutical end-use segment is estimated to register the fastest CAGR of 7.2% from 2025 to 2033, owing to Europe’s strategic push to onshore active pharmaceutical ingredient manufacturing and expand advanced therapy production capacities. Acetone serves as a critical crystallization solvent extraction medium, and cleaning agent in Good Manufacturing Practice environments where its low toxicity and high purity enable compliance with stringent pharmacopeial standards. New drug approvals consistently demonstrate a reliance on specific organic solvents during the chemical synthesis and purification processes. Central European nations maintain a high concentration of active pharmaceutical ingredient production sites that require significant volumes of high-purity solvents. Regional manufacturing trends show a sustained demand for industrial-grade chemicals to support large-scale pharmaceutical output. Regulatory strategies are shifting toward strengthening internal production capacities to minimize reliance on external supply chains for essential medicinal components. Industrial patterns indicate an ongoing integration between chemical supply availability and the advancement of domestic drug development. This policy directly stimulates solvent demand in multipurpose plants adopting continuous manufacturing, where acetone’s compatibility with in-line analytics enhances process control. The institutionalization of mRNA vaccine technology following the pandemic has created a structural demand channel for ultra-high purity acetone in lipid nanoparticle formulation. The manufacture of mRNA therapeutics utilizes large amounts of organic solvents in essential purification and stabilization stages. Key observations include the significant quantities of pharmaceutical-grade solvents needed for creating lipid-based delivery systems through processes like precipitation and buffer exchange, and the resulting continuous demand for specific chemical purification agents at large production sites. International efforts to establish enduring manufacturing networks signal the long-term integration of these production needs across numerous areas, while revised quality regulations and monographs ensure strict management of solvent residues for injectable product safety. This convergence of public health strategy platform technology and regulatory harmonization establishes pharmaceuticals as the most dynamic acetone end use.

COUNTRY-LEVEL ANALYSIS

Germany Acetone Market Analysis

Germany dominated the Europe acetone market and occupied a 28.3% share in 2024. The supremacy of the German market is credited to its integrated chemical cluster along the Rhine, where major producers such as BASF and INEOS operate world-scale phenol and acetone units. A significant volume of a specific solvent was consumed for general industrial use cases, including material synthesis and pharmaceutical manufacturing. Government relief funding was allocated to assist energy-intensive industries in implementing solvent recovery technologies. The automotive sector, a major regional manufacturing industry, utilizes the solvent in production processes such as coatings and adhesives. There was an observed increase in the use of solvent-based cleaning applications within electric motor assembly operations. This synergy of industrial-scale policy support and advanced manufacturing secures Germany’s leadership.

France Acetone Market Analysis

France was the second-largest player in the Europe acetone market and held a 16.7% share in 2024. The expansion of the French market is propelled by its balanced integration across aerospace construction and pharmaceutical sectors. Large-scale chemical facilities in the region support a steady supply of essential industrial solvents to diverse downstream sectors. The domestic aerospace industry remains a significant consumer of these materials due to the requirements of composite component manufacturing for major commercial aircraft programs. Growth in pharmaceutical production has further stabilized demand, as specific chemical solvents are integral to high-yield crystallization processes for medicine. Industrial modernization efforts and investments in manufacturing infrastructure continue to drive the consistent use of these chemical inputs. Stricter environmental regulations regarding volatile organic compounds have led to broader adoption of recycling technologies within the coating and finishing sectors. The shift toward closed-loop systems has improved overall resource efficiency and altered traditional consumption patterns in the chemical market.

Netherlands Acetone Market Analysis

The Netherlands maintains a significant position in the Europe acetone market because of the Port of Rotterdam, which handles over sixty percent of Europe’s chemical imports and exports, including acetone feedstocks. Industrial complexes focus on supplying essential chemical intermediates to meet the demands of specialized manufacturing and solvent sectors across neighboring markets. Regional initiatives are increasingly prioritizing the development of circular loops to enhance the lifecycle of industrial solvents. Public-private collaborations are exploring advanced recovery technologies, such as membrane-based systems, to improve the efficiency of chemical recycling. Technical pilots are demonstrating the feasibility of reclaiming high-purity materials from industrial waste streams to support sustainability goals. Furthermore, the Netherlands leads in sustainable coatings innovation. A significant portion of a specialized product range has transitioned to formulations that utilize specific solvents to satisfy regional environmental standards, reflecting a broader pattern of adapting product lines to align with established ecological certification frameworks. This transition focuses on meeting specific ecological criteria through the use of compliant solvent formulations. Regional logistical capabilities facilitate the rapid movement of chemical supplies to a dense network of industrial consumers, with localized infrastructure serving as a primary hub for the distribution and delivery of essential chemical components. Concentrated industrial proximity allows for highly responsive supply chain management within the sector. More information is available on the AkzoNobel website.

Italy Acetone Market Analysis

Italy grew steadily in the Europe acetone market. Its demand in the country is heavily oriented toward construction, automotive refinish, and cosmetics. National renovation programs for transit networks have increased the demand for specialized epoxy coatings used in the rehabilitation of bridges and tunnels. Large-scale highway retrofitting projects utilize specific solvent-based protective layers to ensure the durability of road structures. The manufacturing of high-performance vehicles has reached significant levels, requiring precise chemical treatments for advanced materials like carbon fiber. Moreover, the production and finishing of luxury automotive components rely on specialized cleaning agents to prepare surfaces for assembly. The domestic personal care market maintains a consistent reliance on solvent-based products for consumer cosmetic applications. A vast majority of topical cosmetic removers sold within the region utilize standard chemical solvents as their primary active ingredient. This triad of infrastructure aesthetics and performance manufacturing sustains Italy’s significant acetone footprint.

United Kingdom Acetone Market Analysis

The United Kingdom is likely to expand notably in the Europe acetone market during the forecast period. Despite post Brexit trade adjustments, the UK maintains robust demand from pharmaceuticals, advanced materials, and offshore energy sectors. Large-scale pharmaceutical production for specialized treatments involves the substantial use of high-purity industrial solvents across major manufacturing hubs. The UK’s offshore wind expansion further drove BPA demand. The expansion of offshore renewable energy infrastructure drives a significant demand for specialized synthetic resins used in marine foundations and cabling. Regulatory shifts regarding maritime environmental standards are influencing a transition toward specific chemical-based protective coatings in shipyards. Updates to regulatory oversight frameworks have simplified the validation process for industrial solvents, leading to faster administrative processing for relevant manufacturing methods. This regulatory agility, combined with strategic industrial strengths, preserves the UK’s relevance in the European acetone landscape.

COMPETITIVE LANDSCAPE

Competition in the Europe acetone market is defined by a concentrated yet dynamic landscape where integrated chemical giants coexist with specialized solvent distributors and emerging bio-based producers. Large players leverage scale and co-product economics from phenol manufacturing to maintain cost leadership while navigating the inflexibility of fixed acetone phenol output ratios. Smaller firms differentiate through high purity grades, logistics agility and niche applications in pharmaceuticals or electronics. Regulatory complexity, particularly around VOC emissions and workplace safety, creates both barriers and opportunities shaping competitive conduct. The absence of standalone acetone plants in Europe intensifies reliance on integrated models, making supply vulnerable to phenol market swings. Meanwhile, sustainability mandates are fostering innovation in recycling and bio routes, introducing new entrants and altering traditional supplier-customer relationships. This multifaceted environment rewards operational excellence regulatory foresight, and strategic alignment with Europe’s industrial decarbonization trajectory.

KEY MARKET PLAYERS

The leading companies operating in the Europe acetone market include:

- LyondellBasell Industries Holdings B.V.

- INEOS Group

- Altivia

- BASF SE

- Royal Dutch Shell

- Honeywell International Inc.

- Mitsui & Co., Ltd.

- SABIC

- Kumho P&B Chemicals, Inc.

- Cepsa

- Formosa Chemicals & Fibre Corp.

- Borealis AG

- PTT Phenol Company Limited

- Prasol Chemicals Pvt. Ltd.

- Chang Chun Group

TOP PLAYERS IN THE MARKET

- INEOS Group is a leading producer of acetone in Europe, operating large-scale integrated phenol acetone units in Germany, Belgium, and the United Kingdom. The company supplies high-purity acetone to global markets for use in methyl methacrylate, bisphenol A, and pharmaceutical applications. INEOS contributes significantly to global acetone supply through its asset network spanning Europe, North America, and Asia. The investment reflects INEOS’s strategy to align production with stringent European environmental standards while expanding into high-value derivative segments.

- BASF SE integrates acetone production within its broader petrochemical value chain at its Ludwigshafen Verbund site in Germany. The company utilizes acetone as a key intermediate for synthesizing methyl methacrylate and specialty solvents distributed worldwide. BASF’s global footprint enables it to balance regional supply dynamics and serve diverse end-use sectors from automotive to healthcare. The initiative supports the company’s circular economy goals and strengthens its position as a sustainable solutions provider in the European acetone market.

- Shell Chemicals produces acetone as part of its integrated aromatics and olefins portfolio with primary operations in the Netherlands and Germany. The company supplies acetone to global customers in the plastics, pharmaceuticals, and electronics industries, emphasizing quality consistency and logistics reliability. Shell plays a pivotal role in linking upstream refining with downstream chemical manufacturing across continents. The innovation underscores Shell’s commitment to decarbonizing chemical operations while maintaining competitive product performance in Europe.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe acetone market focus on vertical integration by linking acetone production with downstream derivatives such as methyl methacrylate and bisphenol A to capture additional value. They invest in advanced purification and recovery technologies to meet tightening environmental regulations and serve high-purity end uses. Strategic partnerships with technology providers enable energy-efficient separation processes that lower carbon intensity. Companies also prioritize compliance with EU chemical safety frameworks to ensure uninterrupted supply chain operations. Additionally, they align production planning with regional industrial policies supporting pharmaceutical onshoring and circular economy transitions to secure long term demand stability.

EUROPE ACETONE MARKET NEWS

- In March 2024, INEOS Group completed a solvent recovery system upgrade at its Antwerp, Belgium, facility to enhance acetone purity for pharmaceutical and electronics applications. This investment is anticipated to allow INEOS to meet stringent European quality standards and strengthen the Europe acetone market presence.

- In February 2024, BASF SE implemented a closed-loop acetone recycling program across its European coatings production sites, reducing fresh solvent intake by twenty-five percent. This initiative is anticipated to lower operational emissions and strengthen the Europe acetone market presence.

- In January 2024, Shell Chemicals partnered with SolSep, a Dutch membrane technology company, to pilot an energy-efficient acetone purification process in Moerdijk, Netherlands. This collaboration is anticipated to cut separation energy use by thirty percent and strengthen the Europe acetone market presence.

- In May 2024, TotalEnergies commissioned a digital twin for its Carling France phenol acetone unit, enabling real-time yield optimization and emission control. This deployment is anticipated to improve production reliability and strengthen the Europe acetone market presence.

- In April 2024, LyondellBasell launched a new high-purity acetone grade certified for lithium-ion battery electrolyte cleaning at its Rotterdam, Netherlands complex. This product introduction is anticipated to capture demand from Europe’s expanding battery gigafactory sector and strengthen the Europe acetone market presence.

MARKET SEGMENTATION

This research report on the Europe acetone market has been segmented and sub-segmented into the following categories.

By Application

- Solvent

- Bisphenol A (BPA)

- Methyl Methacrylate (MMA)

- Others

By End-use

- Paints & Coatings

- Plastic

- Automotive

- Adhesives

- Pharmaceuticals

- Cosmetics

- Electrical & Electronics

- Others

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe acetone market?

The Europe acetone market supplies solvents and intermediates for paints, pharmaceuticals, and plastics production across manufacturing industries.

Why important is the Europe acetone market?

The Europe acetone market supports bisphenol A and MMA production essential for automotive and construction sectors regionally.

What drives the Europe acetone market?

Pharmaceutical and coatings demand propels the Europe acetone market alongside chemical industry capacity expansions.

Which countries lead the Europe acetone market?

Germany dominates the Europe acetone market followed by Belgium and the Netherlands as major production hubs.

What applications define the Europe acetone market?

Solvents lead usage in the Europe acetone market for paints, cleaners, and pharmaceutical extractions primarily.

How produced is acetone in the Europe acetone market?

Cumene process generates acetone in the Europe acetone market as phenol co-product mainly.

What challenges face the Europe acetone market?

Energy costs pressure margins in the Europe acetone market amid volatile feedstock pricing.

Which industries use the Europe acetone market?

Paints, adhesives, and pharmaceuticals consume most from the Europe acetone market volumes.

What grades exist in the Europe acetone market?

Technical and pharmaceutical grades serve the Europe acetone market for diverse purity needs.

How does sustainability impact the Europe acetone market?

Bio-acetone development emerges in the Europe acetone market meeting green chemistry demands.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com