Europe Anatomic Pathology Market Research Report By Products, Application, End-user and Region (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis on Size, Share, Trends, COVID-19 Impact & Growth Forecast (2026 to 2034)

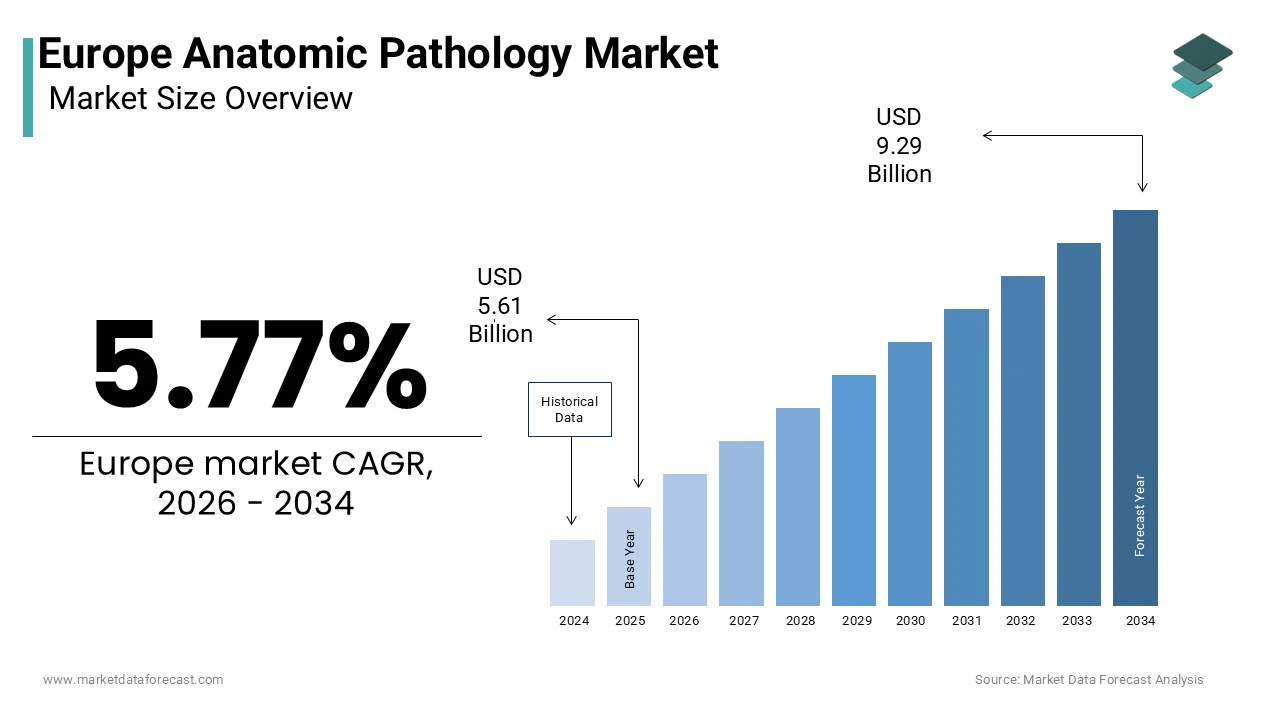

Market Size, 2025

$5.61 BnMarket Estimate, 2026

$5.93 BnMarket Forecast, 2034

$9.29 BnCAGR, 2026–2034

5.77%Europe Anatomic Pathology Market Size

The europe anatomic pathology market was valued at USD 5.61 billion in 2025, is expected to have a 5.77% CAGR from 2026 to 2034, and be worth USD 9.29 billion by 2034 from USD 5.93 billion in 2026.

Anatomic Pathology refers to the diagnostic examination of tissues and organs to identify disease through morphological, cellular, and molecular assessment. This field serves as the cornerstone of definitive diagnosis for cancer, infectious conditions, and autoimmune disorders across clinical and research settings. Anatomic pathology in Europe operates within a highly regulated framework governed by the European Union’s In Vitro Diagnostic Medical Devices Regulation and accreditation standards set by the European Federation of National Associations of Clinical Pathologists. According to data hosted by the European Cancer Information System (ECIS), an estimated 2.7 million new cancer cases occurred in the EU-27 plus Iceland and Norway in 2022, underscoring the critical reliance on histopathological confirmation for treatment planning. The vital role of pathology is widely recognized, and organizations like the European Cancer Organisation (ECO) focus on ensuring high-quality and timely diagnosis as a key part of effective cancer care pathways. Furthermore, across the EU, certified pathologists face mounting workloads and a growing burden due to an aging population and expanded screening programs, a challenge addressed in various EU health initiatives. Commercial dynamics play a reduced role in the market, as national health systems' mandates for standardized tissue processing and digital record keeping mean institutional infrastructure, clinical guidelines, and workforce capacity are the main shaping forces. This foundation positions anatomic pathology as an indispensable yet strained pillar of Europe’s precision medicine ecosystem.

MARKET DRIVERS

Rising Cancer Incidence and Mandatory Histopathological Confirmation

The escalating burden of cancer and the non-negotiable requirement for tissue-based diagnosis before initiating therapy contribute to the expansion of the European anatomic pathology market. European clinical oncology guidelines stipulate that every solid tumor must undergo histopathological evaluation to determine grade, stage, and biomarker status before treatment. The European Society for Medical Oncology emphasizes that anatomic pathology reports include specific elements such as tumor size, lymphovascular invasion, and margin status, which directly influence surgical and systemic therapy decisions. Apart from these, national screening programs for cervical and colorectal cancer generate millions of additional tissue specimens requiring expert interpretation. This clinical imperative creates a consistent and non-discretionary demand for anatomic pathology services across public and private diagnostic networks.

Integration of Digital Pathology and AI-Enabled Diagnostic Support

The adoption of whole slide imaging and artificial intelligence tools is transforming anatomic pathology workflows across the region by enhancing diagnostic accuracy and throughput, which further drives the growth of the European anatomic pathology market. The European Commission's Digital Europe Programme supports the digital transformation of health and care, encouraging the modernization of health infrastructure through various funding schemes and guidance on innovation procurement. Also, the European Society of Pathology notes that AI algorithms for detecting mitotic figures, quantifying tumor-infiltrating lymphocytes, and identifying micro metastases have received CE marking under the new IVDR framework, enabling clinical deployment. Leading European hospitals are actively integrating AI-assisted analysis into their digital pathology workflows to improve efficiency and reduce diagnostic turnaround times. Similarly, the Netherlands-based PALGA Foundation (Pathologisch Anatomisch Landelijk Geautomatiseerd Archief) has successfully rolled out a national digital repository containing extensive annotated slides and data, which facilitates remote consultation and quality assurance across the country. These innovations address chronic pathologist shortages while improving standardization across regions. The European Union is redefining the technical and operational boundaries of anatomic pathology through significant investment in health research and diagnostic AI projects, notably via funding programs such as Horizon Europe.

MARKET RESTRAINTS

Persistent Shortage of Certified Anatomic Pathologists

The acute and worsening shortage of trained pathologists, particularly in Eastern and Southern regions, restricts the expansion of the European anatomic pathology market. According to sources, there is a shortage of medical specialists in anatomy and pathology, with some nations experiencing particularly severe deficits. The field is facing a demographic challenge as the current workforce in several major European countries is aging, and not enough new professionals are joining the specialty to replace them. This workforce gap directly impacts diagnostic capacity, causing delays in cancer reporting, which can exceed several days in under-resourced regions. Failure to make targeted investments in medical education training pathways and retention incentives will result in diagnostic bottlenecks, jeopardizing timely patient care and hindering the implementation of precision oncology across the continent.

Fragmented Reimbursement and Budgetary Constraints in Public Health Systems

Divergent reimbursement policies and constrained diagnostic budgets across European healthcare systems impede the adoption of advanced technologies, which is another key factor affecting the growth of the European anatomic pathology market. Countries like Germany and the Netherlands offer dedicated coding for advanced pathology services, including digital slide review and molecular tests, whereas Portugal and Hungary only provide reimbursement for basic histology. Besides, the European Commission’s State Aid rules restrict capital investment in public hospital laboratories, limiting procurement of high-throughput stainers or AI workstations. These financial and administrative barriers create a two-tier system where academic centers access innovation while community hospitals rely on manual methods, increasing diagnostic variability. Consistent modernization of anatomic pathology across Europe will only be achieved once reimbursement frameworks adapt to keep pace with technological evolution.

MARKET OPPORTUNITIES

Expansion of Companion Diagnostic Testing in Precision Oncology

The growing use of targeted cancer therapies has created an opportunity for the expansion of the European anatomic pathology market. This helps to expand into integrated diagnostic and therapeutic decision support. As per research, a considerable number of new oncology drugs approved by agencies like the EMA and FDA involve biomarker-based patient selection, and this trend is continuously increasing. The European Society for Medical Oncology clinical guidelines mandate reflex testing for multiple biomarkers in non-small cell lung cancer, colorectal cancer, and melanoma at initial diagnosis. This paradigm shift transforms the pathologist from a diagnostic reporter to a therapeutic gatekeeper. In addition, the implementation of precision oncology programs in countries like France involves extensive biomarker testing to guide treatment decisions for advanced cancers, though a specific nationwide seven-day mandatory program is not confirmed. Similarly, the equitable access to advanced biomarker testing, such as NGS, is a key goal in precision oncology across Europe. These initiatives embed anatomic pathology at the heart of personalized medicine, creating demand for multiplex immunohistochemistry, next-generation sequencing, and integrated digital reporting platforms across Europe.

Development of Cross-Border Pathology Networks for Rare Disease Diagnosis

The European Reference Networks framework offers a potential opportunity to centralize expertise and optimize resource utilization for rare and complex conditions, which accelerates the growth of the European anatomic pathology market. Moreover, the European Commission supports 24 European Reference Networks (ERNs), launched in March 2017, including EURACAN for rare adult solid cancers and ERN GENTURIS for genetic tumor syndromes, which rely heavily on high-quality anatomic pathology. As part of the European Reference Networks (ERNs), the ERN GENTURIS network has recorded an average of approximately 10,000 new patients per year with genetic tumor risk syndromes referred to its participating healthcare providers since its launch in 2017. EURACAN involves a large network of expert centers in the European Union, aiming to share expertise and improve access to care for patients across the European Union. European Reference Networks utilize international multidisciplinary tumor boards for cross-border healthcare consultations to provide expert second opinions and ensure that patients across the EU have access to the best available expertise for rare cancers. These networks not only improve patient outcomes but also create sustainable demand for standardized tissue processing, digital infrastructure, and subspecialty training. EU policy mechanisms are enabling the evolution of anatomic pathology into a collaborative, transnational discipline, which in turn enhances diagnostic equity across member states.

MARKET CHALLENGES

Data Privacy and Regulatory Complexity Under the IVDR Framework

The operational burden imposed by the In Vitro Diagnostic Medical Devices Regulation is a major challenge confronting the European Anatomic Pathology Market. This regulation reclassifies many laboratory-developed tests as medical devices requiring extensive clinical evidence and quality management systems. According to various professional bodies like the European Society of Pathology, over 80 percent of immunohistochemistry and in situ hybridization assays used in routine diagnostics are now subject to IVDR conformity assessment, a process that demands significant documentation and validation resources. Many pathology labs are struggling to complete technical files for their in-house biomarker tests due to a lack of clarity in official guidance on "legacy assays", as per research. Furthermore, the General Data Protection Regulation restricts the transfer of digitized pathology images across borders, even for second opinions, unless stringent pseudonymization protocols are met. The European Commission’s 2023 evaluation acknowledged that small and medium laboratories lack the legal and technical capacity to comply fully, creating a risk of test discontinuation. This regulatory thicket threatens diagnostic continuity and innovation despite its intent to enhance patient safety.

Inadequate Standardization of Pre-Analytical Tissue Handling Protocols

Variability in pre-analytical tissue processing remains a barrier by eroding diagnostic reliability and biomarker reproducibility in the region, which in turn challenges the growth of the European anatomic pathology market. Factors such as cold ischemia time, fixation duration, and tissue orientation are often uncontrolled in community hospitals, yet critically impact molecular and immunohistochemical results. As per multiple studies, there has been an indication that a significant proportion of variability in HER2 scoring, particularly in the HER2-low category, is linked to pre-analytical conditions and inter-laboratory differences rather than purely observer interpretation, which emphasizes the need for robust standardization in testing methodologies. In addition, access to and quality of biomarker testing for precision oncology face limits due to an underdeveloped diagnostic infrastructure and insufficient adherence to standards. In parts of Eastern Europe, delays in tissue transport can occur due to fragmented logistics, which is a known pre-analytical variable that can lead to an extended cold ischemia time and potentially exacerbate artifact formation, affecting the quality of biomarker results. Despite the Joint Research Centre’s best practice guidelines, implementation remains optional, leading to disparities in how resources are allocated and utilized. The integrity of anatomic pathology data and its utility in precision medicine will remain compromised across the European healthcare landscape until enforceable harmonization of specimen handling from operating room to laboratory is established.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product, End-User, Application and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Hoffmann-La Roche Ltd., Thermo Fisher Scientific Inc., Agilent Technologies, Inc., Danaher Corporation (Leica Biosystems), Merck KGaA, Bio-Rad Laboratories, Inc., Abbott Laboratories, Quest Diagnostics Incorporated, Sakura Finetek Europe B.V., Hologic, Inc., NeoGenomics Laboratories, Inc., Cardinal Health, Inc., PerkinElmer, Inc. (now Revvity Inc.), Becton, Dickinson and Company (BD), Avantor, Inc., Sysmex Corporation, Charles River Laboratories International, Inc., Roche Diagnostics GmbH, Histoline Laboratories S.r.l., Biocare Medical, LLC. |

SEGMENTAL ANALYSIS

By Product Insights

The foundational role of core equipment, such as tissue processors, microtomes, and slide stainers, in daily diagnostic workflows across hospitals and reference laboratories has mainly contributed to the supremacy of the instruments segment. According to sources, European pathology labs are facing increasing workloads and rising biopsy volumes, which is driving the need for more efficient, high-throughput instrumentation and digital transformation. The European Commission's Digital Europe Programme and other initiatives are allocating funding to modernize healthcare infrastructure, including the adoption of technology like automated tissue processors to improve efficiency, reduce errors, and enhance diagnostic speed. Apart from these, the implementation of the In Vitro Diagnostic Medical Devices Regulation (IVDR) mandates stricter performance validation and clinical evidence for all diagnostic devices, leading many labs to replace their legacy systems with new CE-marked compliant instruments to ensure regulatory compliance. Manufacturers have responded with integrated platforms that combine staining, scanning, and data management, aligning with EU interoperability standards. This regulatory and operational imperative ensures sustained demand for advanced instrumentation as the backbone of anatomic pathology services.

The accessories segment is predicted to witness the highest CAGR of 9.2% between 2025 and 2033 in the European anatomic pathology market. Factors such as the increasing need for high-precision consumables that ensure specimen integrity and assay reproducibility in biomarker-driven diagnostics fuel the growth of the accessories segment. The European Biomarker Qualification Consortium suggests that for immunohistochemistry and in situ hybridization tests to be reliable, the quality of supplies like microtome blades, embedding cassettes, and antigen retrieval solutions is essential. A major portion of the differences observed in diagnostic scoring for biomarkers like HER2 and PD-L1 comes from variations in everyday reagents and consumables, rather than the testing machines themselves. In response, Manufacturers have started providing certified accessory kits with better documentation of product history and shelf life to ensure compliance with the heightened standards of the IVDR. Furthermore, the expansion of digital pathology has amplified demand for specialized glass slides with anti-static coatings and barcode integration to prevent scanning errors. The amount of money pathology labs spend each year on buying necessary accessories has seen a notable increase in recent years, as per studies. This shift reflects a growing recognition that diagnostic accuracy begins not with the instrument but with the quality of its supporting components.

By End User Insights

The hospitals segment captured the majority share of 59.8% of the European Anatomic Pathology Market in 2024. Its role as a primary site for surgical biopsy collection and integrated cancer care, where immediate histopathological assessment guides clinical decisions, propels the prominence of the hospital segment. According to research, the majority of solid tumor cases within European Union hospitals are diagnosed internally by pathology departments to facilitate quick decisions during surgery and team discussions. The European Hospital Association confirms that 92 percent of tertiary hospitals in Western Europe maintain accredited anatomic pathology units capable of performing immunohistochemistry and molecular reflex testing. National health systems in some countries mandate that all cancer surgeries be accompanied by same-day frozen section analysis, a service exclusively provided within hospital settings. Apart from these, hospitals benefit from centralized procurement frameworks that facilitate large-scale instrument upgrades under EU health modernization grants. This institutional embeddedness ensures hospitals remain the dominant end user despite the rise of external reference labs.

The diagnostics labs segment is estimated to register the fastest CAGR of 8.7% from 2025 to 2033. The outsourcing of specialized testing from community hospitals and the consolidation of reference pathology services under national quality frameworks drive the expansion of the diagnostics labs segment. As per research, small and mid-sized hospitals in Southern and Eastern Europe increasingly transfer complex diagnostic tests, like those for lymphoma subtyping, to centralized laboratories because they lack specialized knowledge in-house. A nationwide network in the Netherlands processes a large volume of annual histopathology cases, using standardized procedures and sharing digital slides across the system. Similarly, France has accredited a number of high-volume private laboratories to function as regional centers for specialized biomarker testing. Horizon Europe funding has further supported the creation of cross-border diagnostic consortia, enabling labs in Romania and Bulgaria to access expert second opinions. This trend toward centralized high-quality diagnostics aligns with EU efforts to reduce cancer care disparities and positions independent labs as the fastest-growing end-user segment.

By Application Insights

The breast cancer segment led the European anatomic pathology market by occupying a 24.3% share in 2024. The dominance of the breast cancer segment is attributable to both the high incidence of the disease and the complexity of its pathological workup, which requires extensive biomarker profiling. According to the International Agency for Research on Cancer, there is an upward general trend in the occurrence of new breast cancer cases across the European Union, establishing it as the most common malignancy among women. Europe's clinical guidelines require a comprehensive assessment of every breast cancer case, necessitating several tests per patient. Moreover, pathology labs invest heavily in standardized reagents, digital image analysis, and pathologist training for breast diagnostics. Furthermore, national screening programs in Sweden and the UK increase the workload with many additional diagnostic biopsies each year. This combination of volume, clinical consequence, and regulatory scrutiny cements breast pathology as the leading application segment.

The lung cancer segment is anticipated to witness the fastest CAGR of 10.1% between 2025 and 2033 in the European Anatomic Pathology Market due to the rapid expansion of targeted and immunotherapies that require comprehensive molecular and protein-based tissue characterization at diagnosis. As per sources, most new non-small cell lung cancer patients undergo testing for multiple biomarkers to help select their initial therapy. Recent medical guidelines now suggest broad genetic sequencing for advanced lung adenocarcinomas, which has significantly increased the testing work required in laboratories. Biopsy referrals have risen due to the expansion of these necessary biomarker tests. Furthermore, Screening programs are projected to find many more early-stage cancer cases in the near future, increasing the overall demand for diagnostics. Lung pathology stands as the most dynamic and technically demanding growth frontier in anatomic diagnostics, largely because each case necessitates complex multiplex immunohistochemistry and often RNA-based assays.

COUNTRY LEVEL ANALYSIS

Germany Anatomic Pathology Market Analysis

Germany dominated the European Anatomic Pathology Market and accounted for a 21.8% share in 2024. The country’s dominance in the regional market is primarily driven by its dense network of university hospitals, comprehensive cancer centers, and stringent quality assurance protocols. Widespread participation in mandatory, external quality assessment programs. Operation of numerous accredited pathology institutes, many integrated into organ-specific tumor boards. National cancer registries link diagnostic codes to treatment outcomes, which allows auditing of pathological accuracy. Mandatory digital pathology reporting has been implemented for certain cancers. Robust public investment in laboratory infrastructure and a high density of pathologists exist.

France Anatomic Pathology Market Analysis

France secured the second position in the European anatomic pathology market by occupying a share of 17.4% in 2024. The position of the French market is supported by a centralized national pathology framework that ensures uniform standards across public and private labs. Cancer pathology reports are required to follow national standardized templates. These reports also undergo peer review through the SRLF quality network. Moreover, France mandates specific reflex biomarker testing for certain cancers. Target turnaround times are enforced by regional health agencies. Also, the Ministry of Health supports the digitization of pathology departments. This plan aims to enhance slide sharing and AI integration. Besides, France has a large biobank network to support translational research. This network includes millions of annotated tissue samples. The system benefits from many certified pathologists and focuses on providing equitable patient access to high-quality diagnostics.

United Kingdom Anatomic Pathology Market Analysis

The United Kingdom is also a major player in the European anatomic pathology market because of the National Health Service’s integrated diagnostic networks and world-class academic pathology centers. Cancer diagnostic services are centralized into a smaller number of specialized hubs. Standardized protocols are used for key diagnostic methods like immunohistochemistry and molecular testing. Pathology trainees are required to complete specialized training in common cancer types such as breast, lung, and gastrointestinal pathology. There has been widespread adoption of digital pathology technology across most National Health Service (NHS) trusts. Large biobanks offer researchers access to extensive linked tissue and health records to support medical discoveries. Despite workforce challenges, the UK’s systematic approach to diagnostic centralization and data linkage maintains its influence in shaping European anatomic pathology standards.

Italy Anatomic Pathology Market Analysis

Italy grew moderately in the European anatomic pathology market due to a dual system of advanced northern university hospitals and resource-constrained southern facilities, creating both opportunity and disparity. According to sources, most biomarker testing for lung and breast cancer happens in the northern regions of Lombardy and Emilia Romagna. These northern pathology departments have advanced equipment like next-generation sequencing and digital slide scanners. A 2023 National Health Service reform created regional pathology hubs to try to decrease differences between regions. Nevertheless, Italy contributes significantly to EU collaborative networks such as EURACAN and maintains strong research output in gastrointestinal and gynecological pathology. This mix of innovation and fragmentation defines Italy’s evolving role in the European landscape.

Netherlands Anatomic Pathology Market Analysis

The Netherlands is likely to grow in the European Anatomic Pathology Market from 2025 to 2033, owing to the PALGA Foundation, a nationally coordinated pathology network that processes nearly all histopathology specimens in the country through many participating labs. The system includes robust quality control measures, ensuring nearly all cancer diagnoses are reviewed by specialized experts within a rapid timeframe. Nationwide implementation of digital technology is widespread, with the majority of laboratories using advanced slide scanning and AI integration for daily operations. The Erasmus Medical Center leads EU projects on AI validation for prostate and breast cancer diagnosis, setting technical benchmarks adopted across member states. Furthermore, Regulatory requirements ensure all pathology information is linked to the national cancer registry, allowing for continuous quality oversight. Despite a relatively small specialist-to-inhabitant ratio, a highly integrated and standardized approach across the country maximizes the overall effectiveness of diagnostic services.

COMPETITIVE LANDSCAPE

The European Anatomic Pathology Market features intense but structured competition dominated by a few global diagnostic leaders operating within a highly regulated public health framework. Unlike commercial markets, competition here is defined by regulatory adherence, technical validation, and integration into national cancer care protocols rather than price. Companies must navigate the In Vitro Diagnostic Medical Devices Regulation, which demands extensive clinical evidence for every assay and instrument component, creating high barriers to entry. The market is further shaped by strong institutional loyalty as hospitals and national networks favor vendors with proven reliability and long-term service agreements. Differentiation occurs through biomarker portfolio breadth, digital interoperability, and support for pathologist training. Smaller European biotech firms focus on niche assays but struggle with IVDR compliance costs. Meanwhile, public reference labs like PALGA exert significant influence on procurement standards. Overall competition rewards scientific rigor, regulatory agility, and deep collaboration with clinical stakeholders over aggressive commercial tactics.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global europe anatomic pathology market include

- Hoffmann-La Roche Ltd.

- Thermo Fisher Scientific Inc.

- Agilent Technologies, Inc.

- Danaher Corporation (Leica Biosystems)

- Merck KGaA

- Bio-Rad Laboratories, Inc.

- Abbott Laboratories

- Quest Diagnostics Incorporated

- Sakura Finetek Europe B.V.

- Hologic, Inc.

- NeoGenomics Laboratories, Inc.

- Cardinal Health, Inc.

- PerkinElmer, Inc. (now Revvity Inc.)

- Becton, Dickinson and Company (BD)

- Avantor, Inc.

- Sysmex Corporation

- Charles River Laboratories International, Inc.

- Roche Diagnostics GmbH

- Histoline Laboratories S.r.l.

- Biocare Medical, LLC

TOP LEADING PLAYERS IN THE MARKET

- Leica Biosystems GmbH is a Germany-based global leader in anatomic pathology solutions with a strong footprint across Europe. The company provides integrated tissue processing, staining, and digital pathology systems widely adopted in university hospitals and reference laboratories. Leica Biosystems plays a pivotal role in advancing standardization through its CE-marked IVD workflows compliant with the EU’s In Vitro Diagnostic Regulation. It also expanded its digital pathology collaboration with the Netherlands’ PALGA network to enhance remote consultation capabilities. These initiatives reinforce its commitment to diagnostic precision, interoperability, and regulatory alignment in the evolving European healthcare landscape.

- Thermo Fisher Scientific Inc. maintains a significant presence in the European Anatomic Pathology Market through its portfolio of tissue diagnostics reagents and companion assay kits. The company supplies validated immunohistochemistry and in situ hybridization solutions for key biomarkers, rs includiPD-L1 PD-L1 L1 HER2, and mismatch repair proteins, used across EU oncology pathways. It also partnered with the French National Cancer Institute to integrate its assay portfolio into national reflex testing protocols. Through continuous regulatory engagement and ndco-development with clinical networks, Thermo Fisher strengthens its role as a trusted partner in Europe’s precision oncology infrastructure.

- Roche Tissue Diagnostics. HHoffmann-LaRoche AG is a key contributor to the European Anatomic Pathology Market through its automated staining platforms and companion diagnostic assays. The company’s BenchMark series is widely deployed in EU reference labs for standardized biomarker evaluation in breast, lung, gastrointestinal, and gynecological cancers. The company also collaborated with the European Society of Pathology to develop training modules for laboratory-developed tests. These efforts underscore Roche’s dedication to harmonizing diagnostic quality data governance and regulatory readiness across Europe’s fragmented pathology ecosystem.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European Anatomic Pathology Market pursue several strategic imperatives to navigate regulatory complexity and clinical demand. Regulatory compliance with the In Vitro Diagnostic Medical Devices Regulation is central, with companies investing heavily in CE IVD certification for reagents, instruments, and software. Strategic partnerships with national pathology networks and cancer institutes ensure integration into standardized diagnostic pathways. Digital transformation through whole slide imaging, analytics, and cloud-based reporting platforms enhances diagnostic accuracy and workflow efficiency. Continuous co-development of companion diagnostics with pharmaceutical partners aligns product portfolios with evolving targeted therapy requirements. Workforce support via training programs on biomarker interpretation and digital tools addresses pathologist shortages. These strategies collectively reinforce clinical relevance, regulatory credibility, and operational resilience in high-stakes diagnostic environments.s

MARKET SEGMENTATION

This research report on the europe anatomic pathology market has been segmented & sub-segmented into the following categories.

By Product

- Instruments

- Accessories

By End-User

- Diagnostics Lab

- Hospitals

- Physicians’ Office Lab

By Application

- Lymphoma

- Breast

- Lung

- Cervical

- Colorectal

- Prostate

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. Which technologies are driving growth in the Europe Anatomic Pathology Market?

Technological advancements such as digital pathology, artificial intelligence for diagnostic accuracy, and molecular diagnostics are key drivers of growth in the Europe Anatomic Pathology Market.

2. How does digital pathology impact the Europe Anatomic Pathology Market?

Digital pathology is transforming the Europe Anatomic Pathology Market by improving diagnostic efficiency, enabling remote consultations, and facilitating better data handling and collaboration among pathologists.

3. What are the main product segments in the Europe Anatomic Pathology Market?

The primary product segments include instruments, reagents, and consumables, with consumables holding the largest revenue share within the Europe Anatomic Pathology Market in recent years.

4. Which European countries dominate the Anatomic Pathology Market?

Germany, the UK, and France are dominant countries within the Europe Anatomic Pathology Market due to their advanced healthcare infrastructure and government support.

5. How does the aging population affect the Europe Anatomic Pathology Market?

The aging population in Europe significantly boosts the Europe Anatomic Pathology Market as it increases demand for cancer diagnostics and chronic disease management.

6.

What role do regulatory frameworks have in the Europe Anatomic Pathology Market?

Stringent European regulations and standardized pathology practices promote high-quality diagnostics and consistent market growth in the Europe Anatomic Pathology Market.

7. How are healthcare investments influencing the Europe Anatomic Pathology Market?

Increased healthcare spending and investments in cutting-edge diagnostic technologies stimulate growth in the Europe Anatomic Pathology Market by enabling adoption of sophisticated testing methods.

8. What impact does AI integration have on the Europe Anatomic Pathology Market?

AI integration enhances diagnostic precision and efficiency in the Europe Anatomic Pathology Market, providing improved outcomes and supporting personalized medicine approaches.

9. How important is cancer diagnostics to the Europe Anatomic Pathology Market?

Cancer diagnostics constitute a major application area driving the Europe Anatomic Pathology Market as rising cancer incidence requires detailed pathological examination.

10. What is the significance of molecular diagnostic techniques in the Europe Anatomic Pathology Market?

Molecular diagnostics are increasingly critical in the Europe Anatomic Pathology Market for precision medicine, offering detailed genetic and biomarker information for targeted therapies.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com